News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

al44

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

How QE Helped Main Street

Tyler Durden's picture

Submitted by Tyler Durden on 02/08/2015 10:25 -0500

Submitted by Michael Gipp of The World Complec

How QE helped Main Street, Example 2: Maserati dealerships

I haven't written on this topic in a long time, but it is time once again to look at the magnificent benefits that have accrued to main street businesses as a result of bailing out bad bets of banks. Today I have selected another typical main street business--the car dealership. I have randomly selected the Maserati brand as the subject of today's investigation.

Sales data for Maserati sold in North America are available here.

Annual sales of the Maserati brand (in number of cars sold) ranged from less than a thousand per year in 2002 to nearly 13,000 in 2014, thanks to the benevolent leadership of the Fed.

This is a chart that truly screams "Recovery!" In fact, it is quite clear that things are far better now than they have ever been before. If your life seems to be at odds with the obvious economic reality, you are clearly not working hard enough (or perhaps not at all).

All the propaganda to the effect that the goal of quantitative easing was to make the richer even richer still is thoroughly debunked. We can see that small, struggling family businesses like high-end diamond retailers and Maserati dealerships have indeed benefited from quantitative easing.

http://www.zerohedge.com/news/2015-02-08/how-qe-helped-main-street

I've got groundhog families living under 2 of my outbuildings and haven't seen any of them since last fall. Have seen a few skunks but not regularly. Deer always around. The bear living on top of the hill hasn't been out yet. It's 40 here right now and the first above 32 in weeks. Where's Al Gore???????? Send some of that global warming here.

......al

basserdan- great article. Every head of state needs to read it. I've always maintained that only Iceland did it right after the crisis of 08. It looks like history is becoming stronger in it's agreement. Boot the politicians and jail the bankers. Seems it worked pretty well. Read it America!!!

.........al

Hey Chris- you're right you can definitely include both Bushes, Reagan, Clinton, Carter Ford, Nixon, and Johnson. Obama didn't start nor create this mess, but he is sure doing a great job perpetuating it along with a spineless congress.

.......al

balihi- true story because it's quite close to home.

Young couple, married 1 child 8 years old. Mom has a job that pays $11 and change an hour but has rolls royce health benefits. Great job for her. Husband unemployed. They receive almost $400 in food stamps and get heating assistance(HEAP) from NY state. So husband finds a job at minimum wage as all the jobs in the area are minimum wage he starts work. After getting his first paycheck he quits his job, Why? After taxes and social security are taken out, cost of travel back and forth to job, extra costs for child care as needed due to no one home, looming loss of food stamps and decrease in HEAP he found he was working for about $1 an hour possibly less.

There are still quite a few jobs available in this area but all paying minimum wage. Why work for a buck an hour when all this assistance is available?

gm balihi- you make some good points, I don't trust gov't either. To me able bodied unencumbered means a single person w/o children that has no disability to prevent him/her from working. I don't know if you saw it but last year a news channel did an interview with a young man in California. He is a surfer and admitted to just surfing and smoking weed and drinking beer and living the good life and didn't need to go to work as he got food stamps from the state. I'm sure this is not an isolated case. And yes I agree this is peanuts compared to the bigger rip offs of we the taxpayers by our gov't officials colluding with corporate America. Scroll down and take the pledge, it's just a start but maybe we can go from there if enough people wake up and realize what is really going on.

......al

How The Middle Class Has Fared Under Obama

Thanks to ONEBGG for original post

27 Facts That Show How The Middle Class Has Fared Under 6 Years Of Barack Obama

Michael Snyder

January 19, 2015

During his State of the Union speech on Tuesday evening, Barack Obama is going to promise to make life better for middle class families. Of course he has also promised to do this during all of his other State of the Union addresses, but apparently he still believes that there are people out there that are buying what he is selling. Each January, he gets up there and tells us how the economy is “turning around” and to believe that much brighter days are right around the corner. And yet things just continue to get even worse for the middle class. The numbers that you are about to see will not be included in Obama’s State of the Union speech. They don’t fit the “narrative” that Obama is trying to sell to the American people. But all of these statistics are accurate. They paint a picture of a middle class that is dying. Yes, the decline of the U.S. middle class is a phenomenon that has been playing out for decades. But without a doubt, our troubles have accelerated during the Obama years. When it comes to economics, he is completely and utterly clueless, and the policies that he has implemented are eating away at the foundations of our economy like a cancer. The following are 27 facts that show how the middle class has fared under 6 years of Barack Obama…

#1 American families in the middle 20 percent of the income scale now earn less money than they did on the day when Barack Obama first entered the White House.

#2 American families in the middle 20 percent of the income scale have a lower net worth than they did on the day when Barack Obama first entered the White House.

#3 According to a Washington Post article published just a few days ago, more than 50 percent of the children in U.S. public schools now come from low income homes. This is the first time that this has happened in at least 50 years.

#4 According to a Census Bureau report that was recently released, 65 percent of all children in the United States are living in a home that receives some form of aid from the federal government.

#5 In 2008, the total number of business closures exceeded the total number of businesses being created for the first time ever, and that has continued to happen every single year since then.

#6 In 2008, 53 percent of all Americans considered themselves to be “middle class”. But by 2014, only 44 percent of all Americans still considered themselves to be “middle class”.

#7 In 2008, 25 percent of all Americans in the 18 to 29-year-old age bracket considered themselves to be “lower class”. But in 2014, an astounding 49 percent of all Americans in that age range considered themselves to be “lower class”.

#8 Traditionally, owning a home has been one of the key indicators that you belong to the middle class. So what does the fact that the rate of homeownership in America has been falling for seven years in a row say about the Obama years?

#9 According to a survey that was conducted last year, 52 percent of all Americans cannot even afford the house that they are living in right now.

#10 After accounting for inflation, median household income in the United States is 8 percent lower than it was when the last recession started in 2007.

#11 According to one recent survey, 62 percent of all Americans are currently living paycheck to paycheck.

#12 At this point, one out of every three adults in the United States has an unpaid debt that is “in collections“.

#13 When Barack Obama first set foot in the Oval Office, 60.6 percent of all working age Americans had a job. Today, that number is sitting at only 59.2 percent…

#14 While Barack Obama has been in the White House, the average duration of unemployment in the United States has risen from 19.8 weeks to 32.8 weeks.

#15 It is hard to believe, but an astounding 53 percent of all American workers make less than $30,000 a year.

#16 At the end of Barack Obama’s first year in office, our yearly trade deficit with China was 226 billion dollars. Last year, it was more than 314 billion dollars.

#17 When Barack Obama was first elected, the U.S. debt to GDP ratio was under 70 percent. Today, it is over 101 percent.

#18 The U.S. national debt is on pace to approximately double during the eight years of the Obama administration. In other words, under Barack Obama the U.S. government will accumulate about as much debt as it did under all of the other presidents in U.S. history combined.

#19 According to the New York Times, the “typical American household” is now worth 36 percent less than it was worth a decade ago.

#20 The poverty rate in the United States has been at 15 percent or above for 3 consecutive years. This is the first time that has happened since 1965.

#21 From 2009 through 2013, the U.S. government spent a whopping 3.7 trillion dollars on welfare programs.

#22 While Barack Obama has been in the White House, the number of Americans on food stamps has gone from 32 million to 46 million.

#23 Ten years ago, the number of women in the U.S. that had full-time jobs outnumbered the number of women in the U.S. on food stamps by more than a 2 to 1 margin. But now the number of women in the U.S. on food stamps actually exceeds the number of women that have full-time jobs.

#24 One recent survey discovered that about 22 percent of all Americans have had to turn to a church food panty for assistance.

#25 An astounding 45 percent of all African-American children in the United States live in areas of “concentrated poverty”.

#26 40.9 percent of all children in the United States that are living with only one parent are living in poverty.

#27 According to a report that was released late last year by the National Center on Family Homelessness, the number of homeless children in the United States has reached a new all-time record high of 2.5 million.

Unfortunately, this is just the beginning.

The incredibly foolish decisions that have been made by Obama, Congress and the Federal Reserve have brought us right to the precipice of another major financial crisis and another crippling economic downturn.

So as bad as the numbers that I just shared with you above are, the truth is that they are nothing compared to what is coming.

We are heading into the greatest economic crisis that any of us have ever seen, and it is going to shock the world.

I hope that you are getting ready.

Source

Take a look at the future of America: The Beginning of the End.

http://freedomoutpost.com/2015/01/27-facts-show-middle-class-fared-6-years-barack-obama/#JhSEKPwkacqLcI2j.99

Note: There are active links for everyone of the 27-Facts contained within the original article at the website posted above.

absolutely.., been a fan of shadowstats for a long time. The Bureau of Lies and Scams (BLS) is more influenced by politics than reality.

........al

dickmilde- thanks for the add on the BDI. Yes BDI is not the whole picture. It all comes in to play eventually. What that plus other numbers not from our lying gov't tell me is we are in deep doodoo and things are not getting better.

..........al

traderguy- got a blurb from somewhere last week on that possibility. Looks like it happened

......al.

Good one, LOL. I do believe she was referring to criticisms at the time that the members did not have time to read the bill before voting on it.

PS I enjoyed history far more than civics

Dinner time here in the east. Once again enjoyable dialogue with you

.........al

And of course you won't be able to explain why.

I thought I did. And let me add Mrs Pelosi's infamous remark-

"you have to pass this bill to find out what's in it."

Hi Arizona- yup, I read that and whether the repub plan is good or not or viable or not it still doesn't deny everyone maternity coverage. It would just not mandate it for coverage. I would think if an insurance company would not voluntarily offer coverage it would take a big chunk out of their demographics of possible customers. Gee and none of this was a problem before Obamacare. No one will ever convince me Obamacare is good for the country. Did you miss Dr Gruber's videos? We're too stupid to know the difference. Obama and his minions of miscreants also knowingly lied to us. If you like your doctor you can keep your doctor PERIOD. If you like your current plan you can keep your plan PERIOD. Even after all this it amazes me that people still trust and respect him.

balihi- did you read the whole article? From your response it seems like you just took a phrase and pounded on it. The state of Maine will be requiring able bodied non encumbered individuals to do some work for their welfare and/or food stamps. Do you have a problem with that?

Here's another look-

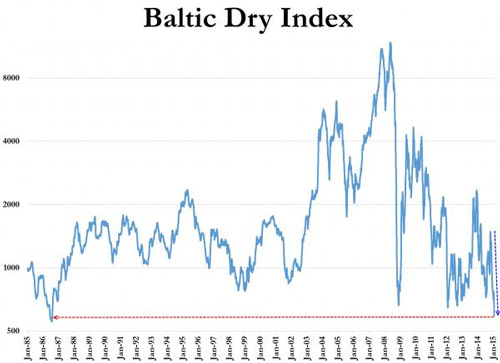

Shocking Chart: The Global Economy Is About To Implode: ‘Inching closer to… the lowest level ever’

Mac Slavo

www.SHTFplan.com

February 5th, 2015

The Baltic Dry Index (BDI) is used by economists and stock traders alike as a leading economic indicator because it predicts future economic activity. The index tracks in US dollars and measures global supply and demand for commodity shipments among bulk carriers including raw materials like lumber, coal, metallic ores, and grains. What makes this particular measurement so distinct from others, according to economic Howard Simmons, is that the BDI “is totally devoid of speculative content” because “people don’t book freighters unless they have cargo to move.”

When cargo is moving the price to move that cargo rises. During the boom-times of the mid 2000’s the Baltic Dry Index hit historical record highs of over $8000 for charter higher rates. It promptly collapsed under $1000 into mid-2008, just ahead of the stock market crash.

What you’re about to see may shock you if you’re of the opinion that an economic recovery has taken hold.

Not only has the index lost 90% of its value in the last several months, but according to Zero Hedge it is just a day or two away from its all-time record lows.

Where is the global economy headed in the next few months?

If The Baltic Dry Index is any guide, it’s about to implode.

And the collapse just keeps going… since Thanksgiving, The Baltic Dry has fallen on 43 or the 47 days, down over 60% from the “China growth is back and all-is-well” hope-filled days of late October (when Jim Cramer “stressed the importance of watching the Baltic Dry Freight Index,” as his bullish thesis confirmation). At 569, The Baltic Dry is inching ever closer to what will be the lowest level ever (554 on 7/31/1986) for the global shipping cost indicator…

One or two more days like this and it will be the all-time low…

It should be obvious, despite the machinations from governments and central banks the world over, that the economy is coming to a standstill. The collapse in the oil price has certainly pushed it along, but the problems go much deeper.

According to many contrarian analysts we’re so far gone that at this point nothing will stop it:

“We are setting up for a collapse that is going to be worse than 1929, and it’s going to come sometime within the next two years. It could come as soon as the next couple of months, but it is going to happen, and there’s nothing that is going to stop it.”

Going forward we will see continued volatility with wild price swings for all asset classes, including gold and oil. It is a sign of a system on its last legs and for those who have failed to prepare a backup plan things are going to be horrific.

It’s imminent. Get ready.

- See more at: http://www.thedailysheeple.com/shocking-chart-the-global-economy-is-about-to-implode-inching-closer-to-the-lowest-level-ever_022015#sthash.Pi1Q2k0L.dpuf

Good afternoon Ayock

IMHO trickle down economics does not work as the human elements of greed and corruption are not and cannot be factored into the equation. Reaganomics was also a failure. He was the first president to start us on the road to extreme deficits as his philosophy was deficits don't matter. Keynesian economics looks good on paper but has never worked in the real world. Reagan started it by endorsing Keynes and his philosophy. Maybe it might have worked if the next presidents followed through by putting aside the excess for harder times. Bush2's tax cuts were a slap in the face to the Keynesian economics model.

My take? No matter how the gov't and media tries to put it, we have never even started to climb out of the recession. America is on a downhill slope and may not ever recover as many of the engines of growth and prosperity have left seeking cheap labor. I wish I had the answers but my ignorance is in good company with the people trying to govern America.

..........al

Labor Force Participation Increases as Unemployment Rate Ticks Up

February 6, 2015 - 11:05 AM

By Ali Meyer

(CNSNews.com) – The labor force participation rate increased from 62.7 percent to 62.9 percent in January as the number of people not in the labor force declined from 92,898,000 in December to 92,544,000 in January, and the unemployment rate ticked up from 5.6 percent to 5.7 percent.

The labor force participation rate is the percentage of those in the civilian noninstitutional population who participated in the labor force by either having a job or actively seeking one in the past four weeks.

BLS employment statistics are based on the civilian noninstitutional population, which consists of all people 16 or older who were not in the military or an institution such as a prison, mental hospital or nursing home.

In December, according to BLS, the nation’s civilian noninstitutional population was 249,027,000. In January, it climbed to 249,723,000, an increase of 696,000. Among that civilian noninstutional population of 249,723,000, 157,180,000 participated in the labor force by either holding a job or actively seeking one. That was an increase of 1,051,000 from the 156,129,000 who participated in the labor force in December.

The 157,180,000 participating in the labor force in January equaled 62.9 percent of the 249,723,000 civilian noninstitutional population—thus, the labor force participation rate was 62.9 percent.

The BLS has tracked the labor force participation rate since 1948. Since then, it hit its historical peak in January through April 2000, when it was 67.3 percent. The 62.9 percent participation rate in January was 4.4 percentage points below that peak.

Another 92,544,000 did not participate in the labor force. These Americans did not have a job and had not actively sought one for four weeks. This group was down 354,000 from the 92,898,000 who were not in the labor force in December.

Of the 157,180,000 who did participate in the labor force in January, 148,201,000 had a job and 8,979,000 did not have a job but were actively seeking one--making them the nation’s unemployed.

The 8,979,000 job seekers were 5.7 percent of the 157,180,000 actively participating in the labor force during the month. Thus, the unemployment rate was 5.7 percent.

The number of unemployed and employed both increased in January. The number of unemployed individuals climbed from 8,688,000 in December to 8,979,000 in January, an increase of 291,000. The number of employed people climbed from 147,442,000 in December to 148,201,000 in January, an increase of 759,000.

http://cnsnews.com/news/article/ali-meyer/labor-force-participation-increases-unemployment-rate-ticks-0

Report: The Gravy Train Is Over For Welfare Recipients: ‘Earn Your Keep or Go Hungry’

Mac Slavo

February 3rd, 2015

SHTFplan.com

For those who are tired of seeing their hard earned money forcibly seized by the government and redistributed to those who refuse to contribute anything of value to society. Even the staunchest of conservatives and libertarians understands that a civilized society needs to provide some level of support for those who are sick, disabled, or simply going through a rough period like losing a job. Americans are a generous people and for the most part we’re all willing to chip in to make our country a better place.

But we can all probably agree that within the social programs designed to provide for the truly needy there also exist hundreds of thousands of people who have made a career out of taking advantage of our good nature and living off government subsistence. These people are able-bodied and fully capable of performing labor of some kind, but like one woman who recently called in to an Austin radio show, they prefer to sit at home because they know they are “still gonna get paid.”

I get to sit home… I get to go visit my friends all day… I even get to smoke weed…

Me and people that I know that are illegal immigrants that don’t contribute to society, we still gonna get paid.

Our check’s gonna come in the mail every month… and it’s gonna be on time… and we get subsidized housing… we even get presents delivered for our kids on Christmas… Why should I work?

Full interview

But life for people like this woman may soon undergo drastic changes. In the State of Maine, it’s time for those who have been collecting welfare and providing the taxpayers nothing in return to get to work. A law passed in 2008 was put on hold because of the recession and high unemployment, but the governor has reinstated it and is now moving to force at least 6,000 of the state’s welfare recipients to either get a job or go hungry. Mad World News reports:

It’s the end of the road for over 6,000 childless, able-bodied residents who have enjoyed regular free food on the taxpayer dollar. The Maine Department of Health and Human Services just told them it’s time to get up and do something to earn their keep or go hungry.

…

The state will now impose a work requirement on welfare recipients without dependents, which must be fulfilled in order to receive food stamps. All adults without a disability must have to actually work for food, volunteer twenty hours per week, or enroll in an employment training program if they want to ensure their EBT card (Electronic Benefits Transfer) is loaded each month. People under the age of 18 and over 50 are excluded from that law.

…

“We must continue to do all that we can to eliminate generational poverty and get people back to work,” Governor Paul LePaige said in a statement on the decision. “We must protect our limited resources for those who are truly in need and who are doing all they can to be self-sufficient.”

Welfare leeches have experienced a double whammy so far this year. First, an investigation found that free Obamaphone programs are plagued with rampant fraud and are soon to be reformed. And now, if you have two working arms and legs you actually have to get a job to earn money for food.

Families and the elderly who receive the benefits will not be affected. The law only applies to individuals without dependents who have no disabilities, like for example, the woman from Austin who enjoys time on the couch smoking weed with her friends all day – weed that’s probably been purchased with your tax dollars.

But Maine’s new policy isn’t popular for some people who have gotten used to free money:

The entitlement mentality riddled with pathetic excuses for lazy behavior is particularly evident from Maine resident Melania, who whined about how she was particularly disturbed by the news that she would have to do something in order to receive her special “expensive” food.

“I was just so upset after I got the phone call. It was a cushion especially for me because I have dietary restrictions; I have a lot of them, and the food is very expensive,” she explained.

One commentor pointed out that working Americans who are seeing their paychecks dwindle because of high taxes forced upon them in the name of people like Melania also have restrictions to which they must adhere:

“I have dietary restrictions also, I am restricted to the food I can afford.”

Maine’s new policy, though unpopular with some, is a common sense requirement for those receiving temporary assistance from the government.

If you don’t work, you don’t eat. It’s a natural law of survival.

http://www.shtfplan.com/headline-news/report-the-gravy-train-is-over-for-welfare-recipients-earn-your-keep-or-go-hungry_02032015

None to my knowledge. Military service should be a requirement for the office as look what happens when a novice is left in charge.

........al

Move over FOX news you have a friend at NBC

Rumor: He’s Hard Core: Jordan’s King Abdullah To Personally Lead Airstrikes Against Islamic State

Gee, thought he would have been on the golf course laughing and joking with friends......my add

Earlier today the Jordanian government launched widespread airstrikes against Islamic State targets in response to the horrific execution of one of their pilots.

In a statement to the father of pilot Moarth al-Kasbeh, King Abdullah II of Jordan said that they will fight ISIS until they are completely eliminated.

And if various reports are to be believed, King Abdullah, a trained fighter pilot, will lead the charge:

What remains unclear is whether Abdullah is personally suiting up and flying a plane, or instead commanding units involved in the mission.

“The Jordanian King Abdullah II will participate personally on Thursday in conducting air strikes against the shelters of the terrorist ISIL organization to revenge the execution of the Jordanian pilot [Kasasbeh] by the ISIL,” said the IraqiNews report.

Others on social media have reported similar statements.

Jordanian Author Waleed Abu Nada Tweeted on Wednesday afternoon, “Local reports here in Jordan say that King Abdullah will personally fly and lead the airstrikes against ISIS tomorrow.”

Middle East commentator Joseph Braude wrote on Twitter: “Reports that Jordanian King Abdullah, himself a pilot, will fly sorties on ISIS targets.”

Before assuming the throne, Abullah II was a Major General in charge of Jordanian Special Forces. Abdullah is also certified as a Cobra Attack Helicopter Pilot. In 1980, he joined the UK’s Royal Military Academy Sandhurst and was commissioned as a 2nd Lt. in the British Army.

- See more at: http://www.thedailysheeple.com/rumor-jordans-king-abdullah-to-personally-lead-airstrikes-against-islamic-state_022015#sthash.O9WMnyVl.dpuf

Rumor: He’s Hard Core: Jordan’s King Abdullah To Personally Lead Airstrikes Against Islamic State

Gee, thought he would have been on the golf course laughing and joking with friends......my add

Earlier today the Jordanian government launched widespread airstrikes against Islamic State targets in response to the horrific execution of one of their pilots.

In a statement to the father of pilot Moarth al-Kasbeh, King Abdullah II of Jordan said that they will fight ISIS until they are completely eliminated.

And if various reports are to be believed, King Abdullah, a trained fighter pilot, will lead the charge:

What remains unclear is whether Abdullah is personally suiting up and flying a plane, or instead commanding units involved in the mission.

“The Jordanian King Abdullah II will participate personally on Thursday in conducting air strikes against the shelters of the terrorist ISIL organization to revenge the execution of the Jordanian pilot [Kasasbeh] by the ISIL,” said the IraqiNews report.

Others on social media have reported similar statements.

Jordanian Author Waleed Abu Nada Tweeted on Wednesday afternoon, “Local reports here in Jordan say that King Abdullah will personally fly and lead the airstrikes against ISIS tomorrow.”

Middle East commentator Joseph Braude wrote on Twitter: “Reports that Jordanian King Abdullah, himself a pilot, will fly sorties on ISIS targets.”

Before assuming the throne, Abullah II was a Major General in charge of Jordanian Special Forces. Abdullah is also certified as a Cobra Attack Helicopter Pilot. In 1980, he joined the UK’s Royal Military Academy Sandhurst and was commissioned as a 2nd Lt. in the British Army.

- See more at: http://www.thedailysheeple.com/rumor-jordans-king-abdullah-to-personally-lead-airstrikes-against-islamic-state_022015#sthash.O9WMnyVl.dpuf

I Read the article. You made it sound like they want to deny maternity coverage for everyone and clearly that is not the case.

GM Arizona- not paranoid, was just a simple question. He has violated his oath of office and ignored the constitution by unilaterally changing laws passed by congress and signed into law by a president. What's to stop him from ignoring the courts?

Arizona- gotta run, nice conversations with you today.

..........al

Well, Boehner IS suing Obama twice so let's see what the lawsuits bring.

I think we both know that was an exercise in futility. What is to stop Obama from ignoring the courts?

They would have to go through the SC. It's already been decided.

The SC is just one branch. If a president can ignore congress why not the SC. Who would the SC get to enforce their decisions?

You brought up previous presidents so feel free to enlighten me.

They despise the ACA but have no solutions to replace it with.

I just read today that they have one to propose. Don't know any details.

Why would an Iranian calling the US weak in negotiations be propaganda? How would that further the Iranian negotiating position by having one of it's generals calling the US weak? One might think it would encourage Obama and company to take a harder line to save face in the international community.

Well then it comes down to the point I'm trying to make to let you see what Obama's lawlessness could possibly bring.

What if the next president or the next or the next uses his pen and phone to outlaw abortion, or exempt all income over $1 million from taxation, or ban protests, or nullify minimum wage laws, or nullify any law near and dear to a liberal's heart? If it's not stopped here then where?

Ah, yes, but how many presidents have used executive orders to literally changes laws on the books?

Is that right? If it was working so well why do virtually every republican and Netanyahu want to bomb, bomb, bomb Iran?

I don't know if that's true or not but if I had an answer for you I would post it.

Americans Now Joining Up To Fight ISIS On The Ground

28-year-old American soldier gives his reasons why he's fighting.

Americans and other westerners are now joining up with the Kurds to help with the fight against ISIS on the ground.

So far, dozens of Westerners have joined the ground fight against ISIS.

28 year old Jordan Matson, a former US Army soldier who joined up to fight ISIS, told the Associated Press: “I’m not going back until the fight is finished and ISIS is crippled.”

He went on to say:

“I decided that if my government wasn’t going to do anything to help this country, especially Kurdish people who stood by us for 10 years and helped us out while we were in this country, then I was going to do something.”

The Kurds use the Internet to find soldiers. They have created a Facebook page called “The Lions of Rojava,” with the stated aim being to send “terrorists to hell and save humanity.” It is replete with images of beautiful, heavily armed female Kurdish commanders and fighters.

In addition to Matson, three other Americans and an Australian national spoke to the Associated Press and said that they agreed to join the fight against ISIS through the Kurdish Facebook page.

He and the others crossed from Syria into Turkey and then joined a Kurdish offensive that came into Iraq last month.

Matson also discussed the reason he joined up to fight ISIS:

“How many people were sold into slavery or killed just for being part of a different ethnic group or religion?” Matson said. “That’s something I am willing to die to defend.”

http://www.westernjournalism.com/americans-now-joining-fight-isis-ground/#M5eGxi2sgtXVA12v.99

Iranian General: U.S. ‘Begging Us For A Deal’

Says the U.S. is operating from a position of weakness.

I guess I'm no the only one that sees it.....al

F. Peter Brown — February 5, 2015

An Iranian general, Mohammad Reza Naghdi, recently claimed that the “Americans are begging us for a deal on the negotiation table.”

In fact, he stated that American officials often “plea” with Iran in negotiation and that the U.S. is operating from a position of weakness.

According to the Associated Press, Iran will be allowed to keep much of its uranium-enriching technology, which can be used for “anything from chemotherapy to the core of an atom bomb.”

Saeed Ghasseminejad, an Iranian dissident and associate fellow at the Foundation for Defense of Democracies, had this to say:

America’s “hostility toward its traditional allies in the region, Israel and Saudi Arabia, is at its historical peak and the Obama administration either supports Iran to expand its influence in the region or at least does not oppose it at all,” Ghasseminejad explained. “Iran feels as long as the negotiation is going on, it has a green light to do whatever it wants in the region, so why should they bother to sign a deal?”

Hossein Salami, another high level Iranian military official, said: “Iran prepares itself for war with global powers, and the Israeli’s are much smaller than them.”

In a recent television interview, speaking of the aid Iran plans to provide to Palestianian terror groups, he stated: “Opening up a new front across the West Bank, which is a major section of our dear Palestine, will be certainly on the agenda, and this is part of a new reality that will gradually emerge.”

http://www.westernjournalism.com/iranian-general-u-s-begging-us-for-a-deal/#ffoLt0gpfpsjb1Po.99

How about do you agree with his pen and phone changing laws by executive order that have been passed by congress and signed into law by a sitting president.

We, meaning the US and our close allies, have almost total control of the world economy through the banking system. It was being used in sanctions on Iran previously and was working well towards causing economic chaos in the Iranian economy. It was no secret. Do I have sympathy for the poor peoples that suffer for the actions of their gov't? Yes absolutely. But as long as they are willing to support their gov't's policies due to beliefs or religion then so be it.

...al

Glad you liked it