News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

AngeloFoca

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

I don't think it's genuine selling going on.

I think it's perhaps a handful of manipulators selling back and forth to each other but never really letting go of the shares from amongst themselves.

Look what we knew to be a genuine buy for 10K at 2.83 did - it literally stopped the price slide for several HOURS, because to get past those 10K shares, they would have to sacrifice those 10K shares - so they did not sell to him as long as he was there... but eventually there actually were sales, from genuine sellers, that totaled 10K, and once Impact was filled... there was a flood of selling back and forth to each other again.

I think it's mostly manipulation we're seeing, and not genuine selling... but it's all guesswork on my part.

I believe Odidi has a vision and it goes beyond what they presently have showing.

All of this concentrating on Rexista has fogged the fact that Regabatin for example may well be bigger than Rexista... but additionally... they actually have multiple delivery platforms, most of which I believe are valuable but have not yet been explored because of lack of funds and manpower.

PODRAS will never be incorporated into over the counter pills - it's simply not cost effective... but a platform that would take an ibuprofen tablet and turn it into 1X a day so that it can compete against 2x a day Aleve would probably bring in say $100 million a year in royalties and another $10 to $20 million in cost plus manufacturing... and that is just one example of what IPCI still needs to explore.

I believe once IPCI gets to say $10 - $12 a share... a raise of perhaps $100 million will take place which will allow them to bring in talent that thinks out of the box to explore and maximize the potential of their complete extended release line.

As another example how about medications on those strips like listerine uses that stick to the roof of your mouth - for people who can't swallow pills.

I also think they still want to become a manufacturing force utilizing their platforms to improve other peoples indications... but most of all...

So they will need funds to hire talent to explore all the possibilities... and to build the manufacturing facilities for those possibilities.

At the end of the day, its inevitable that this company WILL in fact be bought out only after a nice run up.

I didn't expect filing to do much for the share price... but I do believe that a decent partnership with a reputable pharma will be "the" game changer.

Well Impact - looks like you've had quite an Impact on the bid... it seems they are all Impacted at $2.83!!!

They shall not pass!!!

LOL

LOL... I see your 10K at 2.83 - looks like you're getting filled a few hundred at a time - interesting to see... my guess is that someone will jump in front of you to buy some at 2.84... interesting to see... looks like you got 1,100 and now a big pause

Can you tell us what your AVERAGE cost was on those 44K shares??? - If I were to guess it would probably be around $2.94 ???

Might it not have been better if you put an order in for 44K at $2.94 ???

the bid usually goes right back to where it was once the market order spikes the price briefly.

If you are actually placing these orders... I would much rather see you sit at the bid all day long and psychologically say "you shall not pass" rather than put in a market order to affect a pop and then a sell off within minutes after that.

A bid for 44K at 2.90 would have been nice to see... and let them chip at it all day long.

ps - I would not be surprised to see a partnership announcement on Regabatin before a partnership on Rexista.

Regabatin should be ready for phase 3... and should come with about a $10 million up front payment - since it's partnering relatively early... and should be fully paid for going forward with milestone payments of perhaps $25 million on NDA filing and $50 million on FDA approval... and, with a $100 million milestone on the aggregate sale of $1 Billion.

Pregabalin goes off patent end of 2018 - starting phase 3 now should pretty much get us approval by then... or shortly thereafter.

Picked up another 5K shares at $3.01 - simply because I was bored!!!

My guess is that the MM know heavy trading is approaching, and they are shaking all the loose shares they can from weak hands.

Would not be surprised to see it close at or above $3.12.

The 2nd article seems to confuse rexista and oxtenda

PDUFA date set for May 2017, within 6 months of the filing date.

Yes that's what it's looking like to me now agreed tj...as the 74 day letter should now hit by the end of Jan 2017 making the FDA approval date on Rexista roughly around last week of July and/or 1st week of August 2017(6 months)!

Mallinckrodt - I'm really beginning to like this company... earned $5.30 last year and selling at 10.72 PE ratio.

As of 1988, Mallinckrodt was the only company in the US that is allowed to receive cocaine, which it has used to make cocaine hydrochloride, a prescription drug used in hospitals as a local anesthetic by eye and ear, nose and throat doctors.

2012 – Mallinckrodt announces acquisition of CNS Therapeutics for $100 million[18]

2013 – Mallinckrodt spins off from Covidien and begins trading under ticker symbol MNK[2]

2014 – Acquires Cadence Pharmaceuticals[19] and Questcor Pharmaceuticals;[20] joins S&P 500[21]

2015 – Acquires Ikaria Inc. for $2.3 billion[22]

2015 – Acquires Therakos for $1.325 billion[23]

2015 - Sold the Contrast Media and Deliver Systems portion of the portfolio to Guerbet for $270M cash with a loan financed by BNP Paribas [24]

2016 – Acquires regeneratitive medicine company Stratatech

This part I don't like - It's one of the companies embroiled in the Medicare fiasco.

5 Most Expensive Medicare Drugs -- and Which Companies Are Getting Rich From Them

How much is Medicare spending for some drugs? You might be surprised.

Keith Speights

(TMFFishBiz)

Nov 20, 2016 at 3:03PM

Medicare spends billions of dollars each year on prescription drugs. That's not surprising. What might be surprising, though, is how much the federal healthcare program spends per patient on some of these drugs. Here are the five most expensive drugs covered by Medicare on a per-patient basis -- and which companies are making a lot of money from them.

1. H.P. Acthar

Medicare spent $162,371 per patient in 2015 on a drug that's been around since the 1950s -- H.P. Acthar. The drug, which is made from an extract from the pituitary glands of pigs, is used to treat several indications, including multiple sclerosis relapse and infantile spasms.

Acthar hasn't always been so expensive. At one point, a vial of the drug cost only $40. However, Questcor Pharmaceuticals increased the price for Acthar enormously, and the profits began to pour in. Questcor was acquired by Mallinckrodt (NYSE:MNK) in 2014.

Now it's Mallinckrodt that is raking in profits. The company made over $1 billion in net sales of Acthar in 2015, accounting for nearly 27% of total revenue.

Monthly showing the channel with $5 topside will be broken

breaking out on decent chunks of stock - or maybe shorts covering so they can sleep the week end - either way - I LIKE IT

What is your intent... with all this stock you're buying???

What... where... and when... is your EXIT strategy???

I am still hanging in with entire life savings :)

Some of my family members have now taken up sizable positions.

Thanxs for all the numbers numbers.

1. I think Rexista will have a hard time competing against Oxycontin also. 2. There is little incentive for existing Oxycontin users to switch. 3. You also have to convince doctors to prescribe your new drug over Oxycontin.

This is convenient to have readily available.

Dawson Securities Conference October 20, 2016

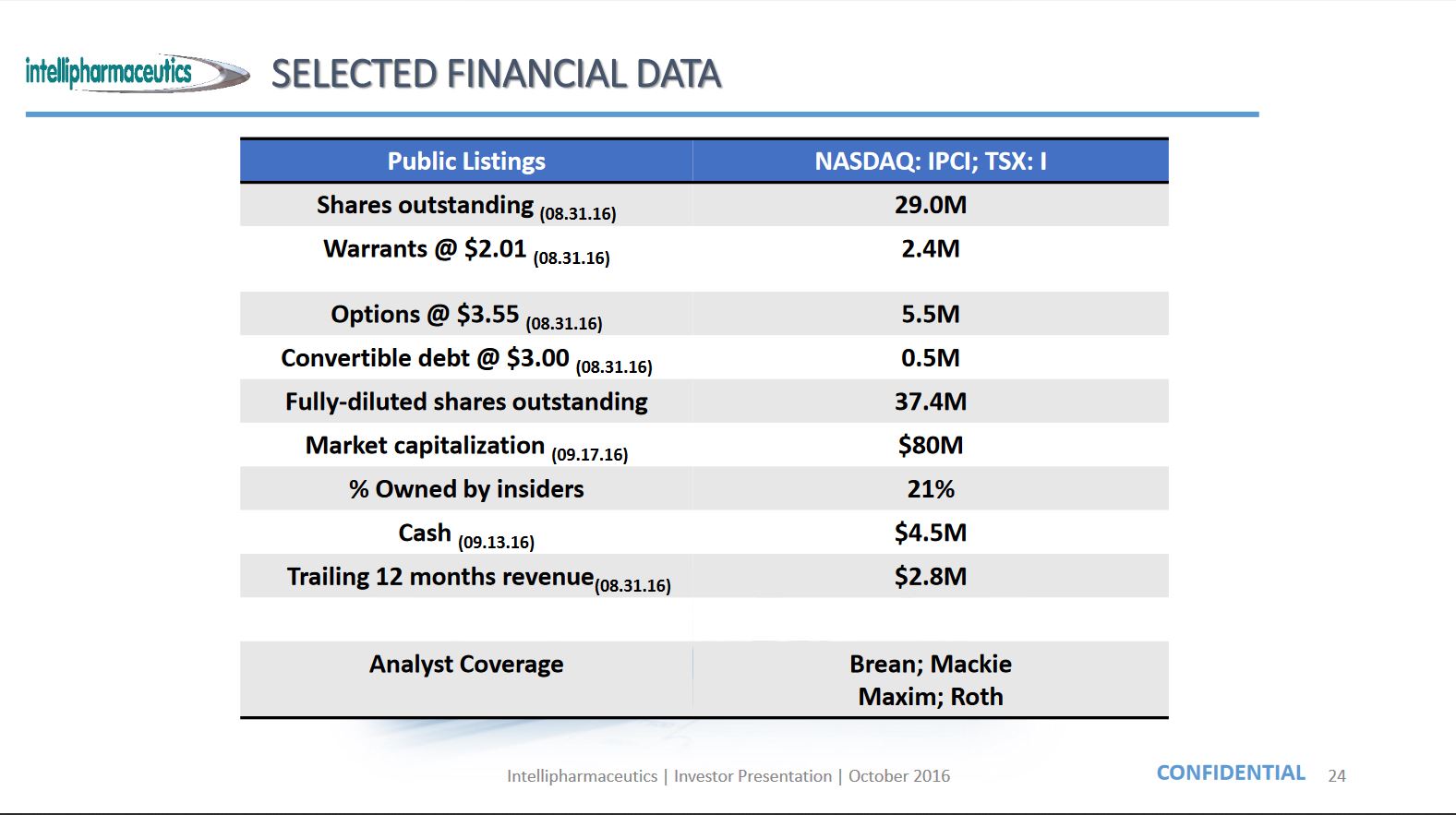

http://files.shareholder.com/downloads/ABEA-43EQSZ/1665438433x0x912718/535FA8C8-DD8D-40EC-AAE2-66CE4CC7AD08/Dawson_Securities_Conference_October_20_2016_-_Final.pdf

Slide 24 - Financial Data - as of October 2016

My friend called his pharmacy and was told that they've been selling Endo/PAR generic Seroquel XR since November 1st...

So we'll be good to go on May 1st 2017

Twice I called my pharmacy to ask if they had generic Seroquel XR 200 mg available... but twice they put me on hold with some horrendous blasting music-on-hold and I couldn't bare to listen to it another second each of the 2 times.

Anybody else wanna try??? also ask who the manufacturer is... to see if it's PAR/ENDO.

Endo Pharma, which is headquartered in Ireland, did announce Par Pharma launched generic Seroquel XR

Good post numbers and good logic... I will correct one assumption you made because you started with false numbers (excuse the pun).

>>>IPCI's pipeline chart says Focalin has $760 million U.S. sales, which includes generics... So Focalin market is generating about the same sales as 2 years ago, before generics hit the market.<<<

That is wrong... Focalin XR pre-generic was selling $1.2 Billion annually... it went down to $760 million or 63% of it's original market value... PAR/IPCI has ~ 33% of market share with 2 of the 5 doses.... so if we take 1/3 of the 40% we get 13% of total ($760 million) market or $98 million which PAR is "possibly" bringing in... more or less - of that $98 million IPCI gets a measily ~ $2.5 million or 2.5% royalties.

If you recall... several months ago I posted an old article by Odidi which said that "when they were a smaller company, they worked mostly for others... and got very little... unlike how they work now.

Focalin XR was developed by IPCI on their patented technology, BUT... it was financed by PAR and PAR brought it through FDA approval... where IPCI was awarded $3 million dollars.

If you recall further... a few months ago I posted a guideline as to what can be expected in the way of royalties... and preclinical, which is when PAR became involved with IPCI on Focalin XR, I gave an estimate of about 5% royalties... well... that's what we're getting... 2.5% to 5% royalties... common practice.

Also... IPCI/Par Focalin XR agreement is NOT mutually exclusive... IPCI can manufacture and sell elsewhere, and, so can PAR sell someone else's product... and who knows, they might be... although I don't believe so.

I hope we've gotten that out of the way... but there is something else Samsa continually misrepresents which has to be cleared up... which is that, there is no money in generics.

As an example, when Ciporoflaxin was a branded drug it was selling for $4 a pill. A year after it went generic, and every Tom, Dick, and Dr Reddy was selling it... it was 10 cent a pill... there was no money in it... because... Cipro can be manufactured by thousands of labs including those in China and India... all it is... is a powder pressed together with some epoxy in a $500 press... voila a cheap generic.

THAT... IS NOT WHAT IPCI IS ABOUT... IPCI is a measured drug release platform... with multiple patents behind it... which will not be manufactured in China or India!!! I believe there are no more than a dozen such platforms... and I also believe that IPCI's is the most sophisticated of the lot.

With Focalin XR, we have an example that can give us crystal clear guidance as to what to expect with Seroquel XR.

As you can see.... Focalin XR retained 63% of it's market value 2 years later... in my figures I low balled Seroquel XR to retain 50% of it's market value.

Seroquel XR was totally developed and brought through FDA approval on IPCI's dime... that puts it in the 50/50 category... it's a little complex but there is always a cost to bring it to market... so I allowed 10% of IPCI's royalties to be kicked back to Mallinckrodt and Mallinckrodt will re-imburse IPCI for development costs which will probably go on the books differently than royalties... If you recall... I once posted that IPCI has certain loss carry forwards it needs to apply towards earnings before they expire shortly... I believe they are handled differently... and development costs will be applied to those losses.

I've seen numbers thrown around that a pill will cost 50 cent to make and IPCI gets 75 cents thereby making 50% profit on manufacturing... another time it was 40 cents to make and it would sell for 45 cents... or 12% profit... quite a difference... I guess it depends on what side of the bed you get up on.

What I used was 20% as profit margin... no... I didn't see the contract... but I know that "captive audience" companies are allowed 20% profit which is generally considered fair all around... your PSE&G was allowed 20% profit before they were deregulated... so I assume IPCI will be granted ~ 20% as the PLUS in the Cost Plus.

Anyway... I stand by my numbers in my post, and feel confident they will be very close to what a fund manager would use if he were to evaluate IPCI's potential earnings.

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=126303761

So many misconceptions in one post I simply don't have the energy to correct them all...I'll only address this one which is so readily debunked with only a small awareness of market behavior

they (institutions) play only based on earnings.

Win some... Lose some!!!

As Charlie Brown said...

"That... would be nice"

Using a p/e of 15, 25mln of profit would call for at least 12$ per share....Just on Seroquel. But then we have to discount for the IPCI syndrome and we get 6$

a reasonable estimate would be $20M to $25M annaully.

What you're seeing has nothing whatsoever to do with shorts.

It's the MM shaking the tree and accumulating whatever they can from weak hands.

With all this coming would you be shorting now????

-PODRAS patent approval

-Rexista NDA submission

-Rexista partnership with lucrative upfront payment + milestone pymt's

-IPCI's partnership for Rexista nPODDS contract may also partner Rexista PODRAS with research totally funded by IPCI's partner

-Regabatin partnership with lucrative up front milestone payment with partner funding all forward research

-Acceptance of the Rexista NDA submission by the FDA(74-day letter)

-4 additional FocalinXR strengths approved by the FDA(licensing agreement with PAR already)

-Seroquel XR commercialization May 1st, 2017(licensing agreement with Mallinckrodt already)

-FDA approval of Pristiq(licensing agreement with Mallinckrodt)

-FDA approval of Lamictal(licensing agreement with Mallinckrodt)

-FDA approval of Protonix(licensing agreement still to be secured)

-FDA approval of Effexor(licensing agreement still to be secured)

-FDA approval of Glucophage(licensing agreement still to be secured)

-FDA granting Rexista PDUFA date Q2 2017

-Ringing of opening bell on NASDAQ on the heels of 1 of the upcoming catalysts

-Next Keppra commercialization endeavors/potential partner announced

Endo Begins Shipment of Generic SEROQUEL XR®... SEROQUEL XR® is a once-daily tablet

Slooowwwwwllllyyyy it turned...

Step by Step...

Inch by Inch...

once you believe a competitor has abandoned their 180 day exclusivity you are still sitting with a tentative approval. you must still go back to the FDA are request a final approval under one of those sections and basically say "hey, so and so failed to launch within the time frame can we have final approval" and we all know how that goes. hope that helps clarify

This is important to have readily available.

Can we have the moderator sticky it to the top?

http://files.shareholder.com/downloads/ABEA-43EQSZ/1665438433x0x912718/535FA8C8-DD8D-40EC-AAE2-66CE4CC7AD08/Dawson_Securities_Conference_October_20_2016_-_Final.pdf

upgraded by Zacks Investment Research from a “sell” rating to a “buy” rating

Looks to me like an institution coming in - $2.94 = +10% which is ringing bells on the momos alerts - let's see what that does.

Just waiting at 2,30-area.

That's exactly what I see in my minds eye as to what IPCI's chart will look like for the next year... and we will still only have approximately 40% institutional ownership... so if you get out then... you will still leave a lot of money on the table!!!

In my opinion Dawson James is the "dog" Della Penna got in bed with and who "gave us fleas"!!!!!!!!!!! and those fleas are what are manipulating the stock price... with the assurance they have by holding 1.5 million warrants - what a mistake. We will not be rid of those fleas until major funds come in and absorb the stock they short... and break their back by causing them to convert the warrants to cover.

dawson james securities complaints - 73,000 results - read'em and weep.

https://www.google.com/search?q=Dawson+James+Securities&ie=utf-8&oe=utf-8#q=dawson+james+securities+complaints

a much larger chunk of the sales revenue than they are currently seeing from the Focalin deal.

https://www.drugs.com/availability/

Focalin XR - 4 Manufacturers + Novartis - IPCI marketing 2 of 6 strenghts - you all know this one.

https://www.drugs.com/availability/generic-focalin-xr.html

Seroquel XR - There is currently no therapeutically equivalent version of Seroquel XR available in the United States. On November 1st 2016, 2 manufacturers will receive approval and IPCI will receive approval after the 180 days of exclusivity - along with 3 or 4 others.

https://www.drugs.com/availability/generic-seroquel-xr.html

Lamictal XR - 7 Manufacturers + Glaxo -

Manufacturer: ANCHEN PHARMS - Approval date: December 26, 2012 seems had Para IV

https://www.drugs.com/availability/generic-lamictal-xr.html

Pristiq XR - seems like 4 generic mfg. + Wyeth - could be more.

July 2015 the US Food and Drug Administration (FDA) announced that Alembic Pharms Ltd, Sandoz Inc., Mylan Inc., and Lupid Ltd had received approval to begin marketing the new drug product desvenlafaxine extended release (ER).Desvenlafaxine ER is the first generic version available for the medication Pristiq®.

Keppra XR - 17 Manufacturers since Sept 2011 + UCB - IPCI's approval, Feb 23, 2016 johnnie come lately on this one.

https://www.drugs.com/availability/generic-keppra-xr.html

Glucophage XR - 15 manufacturers + Bristol - generics for this have been around since 2004, but market is still $2.4 Billion and not likely to get smaller... so 5% market share would be 120 million for IPCI and partner.

https://www.drugs.com/availability/generic-glucophage-xr.html

Effexor XR - 10 Manufacturers + Wyeth

https://www.drugs.com/availability/generic-effexor-xr.html

Protonix XR - 16 Manufacturers + Wyeth

https://www.drugs.com/availability/generic-protonix.html

To add it all up and put it in a nutshell folks... with an aggregate market total of $5.5 BILLION... a measly 5% penetration equals $275 Million... given a 40% royalty which is likely since IPCI brought them all the way through approval - except Focalin - that equals $110 million in royalties - all of which goes to the bottom line... and since they will probably manufacture at cost plus there will even be a little profit on the manufacturing side... AND THAT IS ONLY THE GENERICS... the potatoes... the meat is Rexista and Regabatin!!! Sell your house... sell your car... sell your kids... buy more!!!

20K shares today makes you a millionaire in 3 to 5 years!!! ... OR SOONER

A big buyer could change that.