News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Julius Erving

![]()

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Taken into account the amount of oil that will be found, they better use this diamant for cutting:

https://en.wikipedia.org/wiki/Cullinan_Diamond

Not necessarily, the PR is from the 14th of April, they mention that drilling has commenced, but did not state when exactly.

They started on or before the 14th...

http://erhc.com/news/erhc-energy-inc-drilling-commences-in-kenya-block-11a/

lol.

Middy,

The Kenya block is about 600 million bbls. The JDZ was up to 10 billion bbls.

Maybe there is a fear gap. The fear is that ERHC won't find oil in this next well and won't have the resources to go forward. That is a very logical fear and is based on facts which nobody should ignore. I would like to hear what happens if ERHC doesn't find oil now? That question is never answered by those pushing this stock as a great investment.

Mininum of minimum commercial?

10 million barrels ERHC's share? Times $10,- for a barrel in the books = $100 million / 43 million shares = $2,32

$2.32 / $0.7 = factor 33.14

$33.140,- for every 'grand' invested at this moment.

Hmmm... for a minimum of minimum commercial find...

Of course they have to hit commercial oil to get this to be realistic.

The Doc.

when that oil will be sold, years from now, oil is at $60,- plus for sure.

What do you mean by divided by 5.53? Dilution?

ERHC share example of 20 million barrels at $60,- (at least!) is $1.2 billion divided by 43 million shares = $27.90

If commercial oil is found, everything is ok. And that's an understatement.

Make that a factor 6.666....

Holy Moly.

I know you can't count like that precisly, but still... what a factor!

Talking about upward potential... lol.

Versus a dilution factor of 5.73...

Smart management...

600 million barrels, at $100,- in the future (lol) is 60 BILLION $

ERHC's part close to $20 BILLION?

lol?

From 3 MILLION to somewhere near that number is a steep road... lol.

Factor 660... :P

What is ERHC worth if oil is in the $70isch, and ERHC's part of oil is, let's say, 20 million barrels?

Market cap now about $3 million. Still a bargain, imo.

43 / 7.5 = a dilution of 5.73

Did the share price also drop a factor of 5.73?

No, slightly more. lol.

Strategy,

A little bit of good news for ERHC. According to the 10Q ERHC's 419K shares in Oando that were worth $403,000 on March 31st are now worth over $600,000. Makes you wonder why a company who needs cash wouldn't just sell their OER shares.

I meant $13,20

Is that achievable? Yes. On finding oil.

We are now at 8 cents.

375 times 4 cents is where we were before CN/Glut oil, with NO oil. (from $0.15 to $0.0004 = factor 375)

375 times $0.04 = $15,-

Is this correct, Troy? :)

If so, with an oil find, $15,- should be the starting point, minus the additional dilution from 4x to 6x approximately?

Your $79,- / $15,- = factor 5.3 x the old share price, for having oil in the books? 15 cents times 5.3 in the old situation.

Achievable? How much oil do they need to have in that case?

$79,- times 40.000.000 shares = $3.16 billion, how much barrels is that? 15 bucks per barrel did you say? 210.666.000 barrels ERHC share?

It is indeed a lot. Correct? I'm quite busy doing things, can't think clear anymore. :P

Eh, little math errror. ;)

Sidenote: did you see my fellow Dutchman win the Formule 1 race in Spain just now? 18 Years old, in his first race in that car...

Worldnews.

http://edition.cnn.com/2016/05/15/motorsport/spanish-grand-prix-max-verstappen-lewis-hamilton-nico-rosberg/index.html

Troy,

I tell you I need $79 on shares I bought a decade ago to break even and you reply with "OK so you will have a long term CG"???

Do you really envision the share price exceeding $79???

I would be elated!

What did SEO pay for his convertibles again last year? Spilt adjusted...

You are valuing a discovery at Tarach-1 of 1/2 the unrisked estimated volume at less than 90 cents per barrel.

Seriously, is this guy really thinking he makes sense?

If you were referring to me, thank you. But I'd shy away from the $12 or higher price target if ERHC is lucky enough to find oil with this well. Anything over $1 - $2 is ignoring the balance sheet, dilution and dirty way this game is played imo. In the finding oil scenario, ERHC will be long gone if an offer anywhere over a dollar appeared, particularly with the positions of PN and SO.

Globaloil,

Most of the post-dilution (after 750MM O/S) shareholders are in at less than $0.20 post-split PPS, so a 10+ bagger would easily be approved by a simple majority. Just my wild theory.

Convertibles need to go. With a well under way this should be $1-$2, matbe more. Ntephe is too inept to see that.

$24.96 a share....time will tell

Ok, little bit of cheering again?

We were at almost $1,- pre JDZ.

That is diluted currently $0.25 (is it? Doesn't matter)

We are currently at $0.0006

$0.25 / $0.0006 = factor 416

Peter has 71 million shares = now 710.000 shares at .06 cents = $42.600,-

$42.600,- times 416 on finding oil = $17.721.600,- for the 'worst' CEO in history...

Is he cheering for oil onsite? Oh yeah, oh yeah baby...

The other guy has 830.000 shares...

SEO has...

They only need to find enough oil to raise the share price to $40 for someone that bought shares a decade ago,

OC,

"Selling into a discovery announcement is my biggest fear."

I thought that is a good thing, since less shares will be needed for the CN holders...

Wasn't that David Bovell and his working petroleum kitchen...?

Also rememeber his 'north of $10,-' remark, before they let him fly away.

The Doc.

This is indeed very good news, in general

According to our sources, Kosmos won’t stop there. During earlier talks on its eventual arrival in the EEZ, the American company indicated it could be interested in buying stakes in the JDZ with Nigeria. Kosmos, which is backed by equity funds and thus finds itself less exposed to swings in share prices on the stock market and in the oil price, is taking full advantage of less stringent work commitments than in the past as well as a sharp drop in the cost of seismic campaigns given the number of boats that are stuck in ports for want of contracts. A 3D seismic survey on its Sao Tome permits is already being planned for 2017.

The reward could be as much as 100x.

There is a lot of 'lying by omission' going on, Troy. Indeed.

Bad post SSC,

Uncovered again as an overly, deliberately negative poster.

I was already more conservative than Troy, just for peoples like you.

But what you 'seem' to miss is: even if you take $7,50 per barrel, it still is a factor 50.

Also you 'accidentally' leave out the fact that if oil is found, any dilution will be just a factor of what it would be last year, because the share price will be back to old levels, and higher.

We were at 15 cents, pre drilling, pre CEPSA, pre R/S, just Kenya.

So we were at $15,- / 4 times dilution, let's say a conservative $3,- pre everything. We are now at 8 cents, that is a factor 37.5 (a week ago even a factor 66) pre the oil glut/CN era, on no oil whatsoever.

If commercial oil is found we, of course, blow right past that $3,- figure by at least a factor 5, to any number the oil find will justify.

Dilution is no problem with oil in our books.

Didn't you know that? Lol. If you were looking for a valid reason why Peter & Sylvan bought so much shares last year, look for the answer to that question in this direction.

P.s. Why did I even react?

SSD,

If oil is found, the stock has a chance of retesting the bogus big jane/kaboom rumor high of .43;

http://oil-price.net/en/articles/oil-prices-recover-despite-bribery-scandal.php

Good read.

Furthermore, the promise of a great surge in supply has failed to materialize. All of which means that the supply of crude oil to the market will be greatly reduced for the remainder of 2016 than it was in 2015.

From last Tuesday:

When drilling in Kenya Block 11A commences, ERHC will announce it. It would be a violation of federal disclosure regulations to disclose this type of information selectively via email. We will announce it to everyone at the same time through approved means.

Sincerely,

Daniel Keeney, APR

DPK Public Relations

When it commences we will announce it. I could be here all day every day responding to people asking if the well has spud. Or I can just say to everyone the same thing we have been saying since the start of the year that when drilling commences we will announce it. If you don’t see an announcement you can deduce from there, right?

Sincerely,

Daniel Keeney, APR

DPK Public Relations

The only person that can explains our CEO's silence is Ntephe, and he is in hiding, for whatever reason.

This can't be!!!

According to some here his company goes not good, he can't invest in ERHC... lol.

It will always stay an mystery WHY he did not come to the CN-rescue sooner and with more $$$

A 'gesture' to PN and SO? I don't know.

If CEPSA is willing to invest 30 to 60 million dollars, why did he not want to go further that 250K...?

But one thing is for sure, SEO also cannot know whether there is oil or not in 11A.

He has invested more $ in less prospective projects I think...

Happy Eastern.

I get it.

By the way:

https://en.wikipedia.org/wiki/Going_concern

12 months at least.

And did they elaborate on the measurements in order to be able to continue the business, like salary cuts... Shouldn't they be going in depth on that?

Of course they will pay market for it.

Some who don't understand claim otherwise, but the wanderer with the diamant will of course get paid what the diamant is worth.

As long as the wanderer knows what his diamant is or could be worth... and I'm pretty sure our guys know.

if CEPSA is willing to invest/'gamble' at least 30 MILLION dollars, they know there is value in the prospect itself.

Some, the obvious ones, seem to not understand this.

If this were the case why would cespa not take the extra chunk of Kenya that Erhe has been trying to farm out, cespa probably could've picked it up cheap, probably still can! This would've maybe insured Erhe had enough money to make it to drilling and cespa claims more of the block! Strategic investor bit was to sell the RS

"Management does believe it has created and is executing on a viable plan that has the capability of eliminating the threat to continuation of our business."

Farmout of EEZ is coming... soon. IMO.

It won't be for nearly as much but these guys may be ready to avoid the risk of not striking oil. They even hinted on this approach a year ago or so.

Just Google man... :p

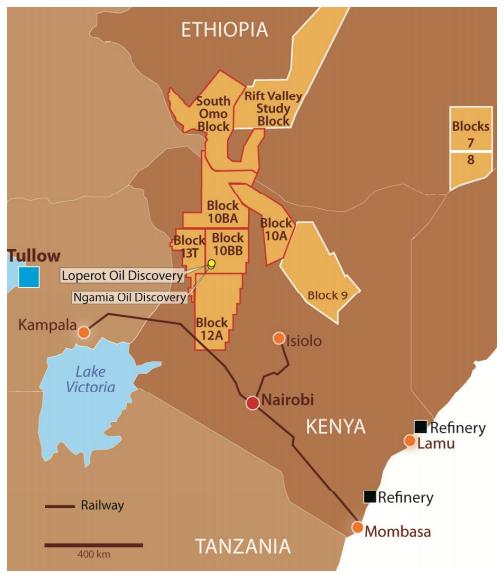

http://www.energy-pedia.com/news/kenya/new-151148

A new oil discovery in Kenya is “very encouraging indeed” for its export ambitions

http://qz.com/640595/a-new-oil-discovery-in-kenya-is-very-encouraging-indeed-for-its-export-ambitions/

“This is the most significant well result to date in Kenya outside the South Lokichar basin,”Angus McCoss, Tullow’s exploration director, said in a statement. “Encountering strong oil shows across such a large interval is very encouraging indeed.” Last year, the company drilled similar “wildcat” wells (unexplored sites with no history of oil production) in northern Kenya and came up empty handed.

Empty handed in Northern Kenya? Oh, sjit.

The only question is will they issue more convertible debt to fund drilling and pay the IRS?