News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Jimmy Quick

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Yep, plan on doing a lot of that here shortly.

10 bagger where it is at now, and been over a 53 bagger, yah such a terrible investment for a long term stock. Just have to know when to buy and when to sell. LMAOROTF

I only had to look at the first one. RSI, to know that nothing makes sense and th as t those analytics are WRONG. No wonder BIG MISTAKES follow after that terrible Analysis.

Yep, means some investors just don't know what the RXMD DD is telling them. Some made the BIG MISTAKE before and are still making that same mistake today.

Some investors are confused about RXMD though. Sell 2 million shares at $.019 and then watch it rise high. It's like going fishing, but never putting any bait on the hook.

Logic, assertions and trading strategy about RXMD have not once been right in the period prior to sell, and the 3 1/2 years since. Been easy work for us experienced financial analysts.

Your right again, the BIG MISTAKE would be better labeled as the $496,000 MISTAKE or the I WILL STICK AROUND for 3 YEARS TO HEAR ABOUT MY MISTAKE! LMAOROTF

Man that is more than a 10 bagger for those that invested early even at today's undervalued share price. RXMD Management has kept this company relevant and made huge strides in Revenues, profits are next.

And still those RXMD short term investors that doubled their money sit here wasting time daily posting garbage about RXMD management. That's not RXMD Management fault.

RXMD Management took us from:

1. $ .005 on OTC PINKS not current up to $.267 on OTCQB.

2. Unaudited to 3 years audited financials.

3. $9 million annual net revenues to over $40 million annual net revenues.

4. 100k annual prescriptions filled to over 530k.

5. From 1 4500 sq ft location to 4 locations across Florida with largest facility now 11,000 sq ft.

6. 85% of companies on OTC have done none of these things and end up at $.0001 in less than a year.

7. RXMD has done quite a bit to increase my shareholder value. Even a quick to pull the trigger investor nearly doubled his investment, but that seems to be forgotten.

We understand why some investors can't make money on RXMD. when they can't hold their 2 million shares past $.019. That is no fault of RXMD Management. LMAOROTF

I'll work on something next week.

You're Right, that was a very beneficial and beautiful trade for those longs, including me, that acquired those 2 million shares @ $.019. I would like to express my thanks to that shareholder for increasing my RXMD shareholder value.

Same to you as well. Enjoy your RXMD shares.

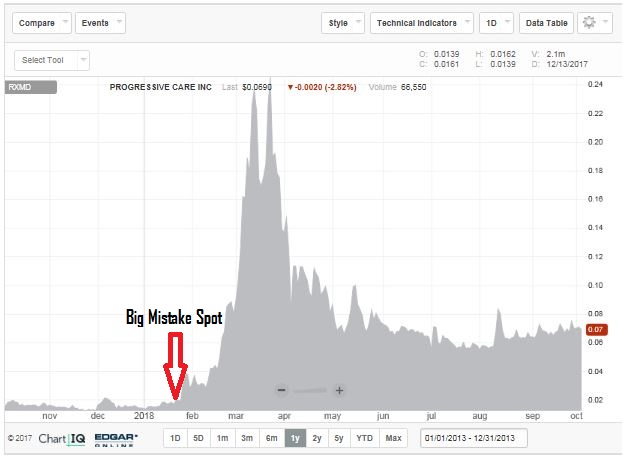

Weekend DD on RXMD historical sells.

Sell of 2 million shares @ $.019 Good indication of flaws.

Actually, when people state fiction, it allows for easy counters with non-fiction. The truth makes it's way to the top when you follow the DD, the performance, and RXMD successes over the years.

This doesn't even make sense. How would it be on Armen ever. Armen not going to open up his personal bank account for expansion. That falls on the company. And if it is through shares or cash from the company, it does make some difference, but both ways affect the balance sheet.

Twitter post:

Data is the new gold...

#ClearMetrx #ProgressiveCare #34OB #healthcaretechnology #Healthcare #healthanalytics https://t.co/f1nHY3ZZIF

We get our S1 in the next 2 months, then I am on board with that prediction.

Storyline by RXMD Management - Pretty Successful if you Ask A Real Investor and not a Here One Minute Gone the Next Trader

Here you go RXMD Shareholders

Let's not forgot RXMD purchased a new 11,000 sq ft facility. Purchased a location in Palm Beach, FL, purchased 2 new locations in Orlando and Davie, FL all within the last 3 years. Expansion comes with a price tag. Don't be that investor that doesn't listen to the DD, you will wind up selling your shares way to soon, I mean, way to soon.

I think that must have been the issue @ $.019 Focused only on the Liabilities and not the Assets and Receivables LMAOROTF

This is what we know about poor decisions. LMAOROTF

Sell of 2 million shares at $.019

Wrong about Pharmacist Renegotiation of Salary as well.

This is what we know for sure about Company Revenues.

This is for sure what we know about Debt Payoffs.

Actually, that T-trade may be the Great Unknown yet for RXMD, that we are all anxiously waiting to learn more about. Just over 10 million shares at $.1025. Yah we want to know more about it.

Not forgotten at all, I have brought it up many times. I am not throwing that in with the lot, nor was the poster I was replaying to. More importantly I haven't forgotten about the 2 million share DA-trade.

The T-trades are related to debt payoff, there is no doubt about it. The company released 10 million shares to Illiad in March 2021. They are still working through those shares.

RXMD 4 week range after sell of 2 million shares at $.019.

Low $.019

High $.267

NO BIGGIE!

LMAOROTF

Lack of RXMD DD before selling everything led to shareholder demise when 2 million shares were sold at $.019 LMAOOTF... but great quote. If only everyone could follow the advice.

Agreed So Sad! That it played out like that for some investors who gave up their RXMD shareholder value so soon in the game. All 2 million shares at $.019, we were just getting started, the gun hadn't even gone off yet, the rabbit was still eating his carrot, the light was still RED, we were still sitting at the STOP sign, the climbers were still at the base of the mountain, the space shuttle hadn't even fired up their thrusters, the plane was still in taxi. So SAD INDEED.

If only he invited everyone to breakfast and announced their big moves ahead of time, we wouldn't have this happen with 2 million shares traded away at $.019.

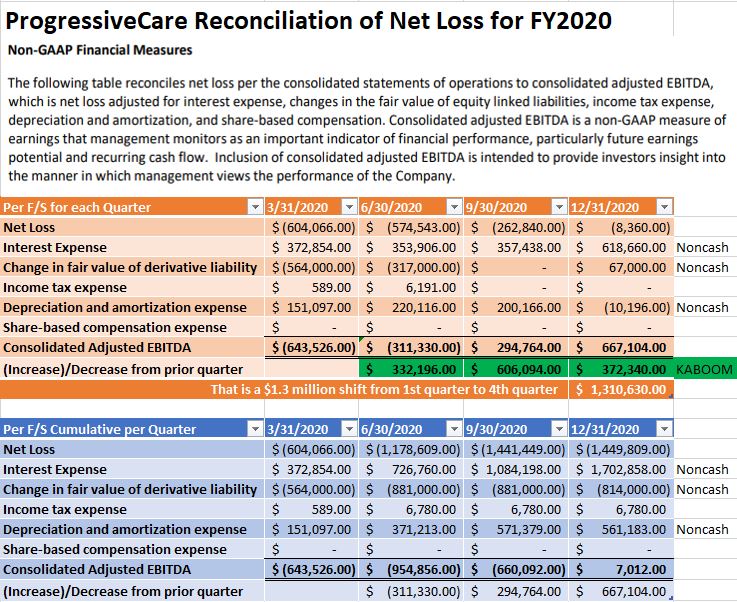

CASH ON HAND $77 MILLION

This company is sitting on $77 million in raised capital for research and trials. As noted in previous emails they have several trials ongoing, the most recent one was a success, and more to look forward to with that one in 2nd half of 2021.

Some investors have to hang their hat on the BIG mistakes instead.

2,000,000 shares sold @ $.019

Overview

We are a clinical-stage biopharmaceutical company focused on developing and commercializing novel cancer therapeutics that reactivate the mutant p53 tumor suppressor protein. p53 is the protein expressed from the TP53 gene, the most commonly mutated gene in cancer. We believe that mutant p53 is an attractive therapeutic target due to the high incidence of p53 mutations across a range of cancer types and its involvement in key cellular activities such as apoptosis. Cancer patients with mutant p53 face a significantly inferior prognosis even when treated with the current standard of care, and a large unmet need for these patients remains.

Our lead product candidate, APR-246, or eprenetapopt, is a small molecule p53 reactivator that is in clinical development for hematologic malignancies, including myelodysplastic syndromes, or MDS, and acute myeloid leukemia, or AML. Eprenetapopt has received orphan drug, fast track and breakthrough therapy designations from the FDA for MDS, orphan drug and fast track designations from the FDA for AML and orphan drug designation from the European Commission for MDS and AML, and we believe eprenetapopt will be a first-in-class therapy if approved by applicable regulators.

We are conducting, supporting and planning multiple clinical trials of eprenetapopt and APR-548:

--- Phase 3 Frontline MDS Trial -- In June 2020, we completed full enrollment of 154 patients in a pivotal Phase 3 trial of eprenetapopt with azacitidine for frontline treatment of TP53 mutant MDS. The pivotal Phase 3 trial is supported by data from two Phase 1b/2 investigator-initiated trials, one in the U.S. and one in France, testing eprenetapopt with azacitidine as frontline treatment in TP53 mutant MDS and AML patients. The data from the U.S. and French Phase 1b/2 trials were published in The Journal of Clinical Oncology in January 2021 and February 2021, respectively. In December 2020, we announced that our pivotal Phase 3 trial failed to meet its predefined primary endpoint of complete remission (CR) rate. Analysis of the primary endpoint at this data cut demonstrated a higher CR rate (53% more patients achieving a CR) in the experimental arm receiving eprenetapopt with azacitidine versus the control arm receiving azacitidine alone but did not reach statistical significance. Based on a thorough analysis of the current Phase 3 trial data and comparisons to the U.S. and French Phase 1b/2 trials, we believe that despite similar types and frequency of adverse events observed in the Phase 3 experimental arm and the Phase 1b/2 trials, patients in the Phase 3 experimental arm experienced substantially more study treatment dose modifications compared to the experience in the U.S. and French Phase 1b/2 trials. We believe that the dose modifications of eprenetapopt and azacitidine led to undertreatment in the Phase 3 experimental arm that negatively impacted efficacy, particularly the primary endpoint of CR rate. We continue to follow patients who remain on-study and anticipate discussing with FDA the Phase 3 data and future possible regulatory pathways in the second half of 2021.

--- Phase 2 MDS/AML Post-Transplant Trial -- We have completed enrollment of 33 patients in a single-arm, open-label Phase 2 trial evaluating eprenetapopt with azacitidine as post-transplant maintenance therapy in TP53 mutant MDS and AML patients who have received an allogeneic stem cell transplant. The primary endpoint of the trial is the rate of relapse-free survival (RFS) at 12 months, with a published benchmark of ~30%. An interim analysis in April 2021 showed a 62% rate of RFS at 12 months, with a median RFS of 462 days. An interim analysis of overall survival (OS) showed a 77% OS at 1 year, with a median number of events not yet reached. We anticipate initial results from the primary endpoint of RFS at 12 months in the second quarter of 2021.

---- Phase 1/2 AML Trial -- We are currently enrolling a Phase 1/2 clinical trial evaluating the safety, tolerability, and preliminary efficacy of eprenetapopt therapy in TP53 mutant AML patients. The lead-in portion of the trial evaluated the tolerability of eprenetapopt with venetoclax, with or without azacitidine, and no dose-limiting toxicities were observed in 12 patients receiving either regimen. Based on these results, we have expanded the trial to treat 33 additional frontline TP53 mutant AML patients with the combination of eprenetapopt, venetoclax and azacitidine. In the 19 frontline AML patients who are evaluable for efficacy with the triplet regimen, we have observed a 63% CR + CRi composite response rate and a 31% CR rate. We anticipate completion of enrollment in the triplet regimen expansion cohort during the second quarter of 2021 and availability of preliminary response rate data from the cohort also in the second quarter of 2021.

--- Phase 1 NHL Trial -- We are currently enrolling a Phase 1 clinical trial in relapsed/refractory TP53 mutant chronic lymphoid leukemia (CLL) assessing eprenetapopt with venetoclax and rituximab and eprenetapopt with ibrutinib in order to further assess eprenetapopt in hematological malignancies. The first patient was enrolled in the first quarter of 2021. We are also planning to evaluate the combination of eprenetapopt with venetoclax in relapsed/refractory mantle cell lymphoma.

--- Phase 1/2 Solid Tumor Trial – We are currently enrolling a Phase 1/2 clinical trial in relapsed/refractory gastric, bladder and non-small cell lung cancers assessing eprenetapopt with anti-PD-1 therapy. The dose-escalation phase of the trial enrolled 6 patients with advanced solid tumors and no dose-limiting toxicities were observed. Based on these results, we are enrolling expansion cohorts for patients with advanced gastric, bladder and non-small cell lung cancers and have currently enrolled 15 patients across these expansion arms. A poster presentation for this trial has been accepted for presentation at the 2021 ASCO Annual Meeting (abstract TPS3161).

--- APR-548 Phase 1 Trial – Our second product candidate, APR-548, is a next generation p53 reactivator that is being developed in an oral dosage form. We have planned a Phase 1 dose-escalation clinical trial evaluating safety, tolerability, and preliminary efficacy of APR-548 with azacitidine in frontline and relapsed/refractory MDS patients. We anticipate the first patient to be enrolled in the second quarter of 2021.

I know this isn't a NASDAQ message board. But some would have to feel that this could produce some good returns yet in CY 2021. Article today talked about how Aprea could have significant volatility approaching, signaling that a major move could be coming one way or the other. I think we know which way it would go with the news from 6/16/21.

The dust will fully be settled once Illiad is gone. I don't know how close we are yet to that, but that 10,000,000 share trade on April 16th still has me questioning what that went towards.

Thanks for info

So where does this go from here, have a buy order in at $.0025. In general what does company have. I mean, I own $RXMD in comparison and it has 40 million annual net revenues, S1 finished soon and then uplist and it is only at $.05 and OTCQB. I got in at .005 years back. Does this company once current have any potential revenues to continue to make an investor money?

Amen to that...NEXT