News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

zsvq1p

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

oh wall street crooks no way greened out too huh

Kevin G. Hall | McClatchy Newspapers

WASHINGTON — When oil prices hit a record $147 a barrel in July 2008, the Bush administration leaned on Saudi Arabia to pump more crude in hopes that a flood of new crude would drive the price down. The Saudis complied, but not before warning that oil already was plentiful and that Wall Street speculation, not a shortage of oil, was driving up prices.

Saudi Oil Minister Ali al Naimi even told U.S. Ambassador Ford Fraker that the kingdom would have difficulty finding customers for the additional crude, according to an account laid out in a confidential State Department cable dated Sept. 28, 2008,

"Saudi Arabia can't just put crude out on the market," the cable quotes Naimi as saying. Instead, Naimi suggested, "speculators bore significant responsibility for the sharp increase in oil prices in the last few years," according to the cable.

What role Wall Street investors play in the high cost of oil is a hotly debated topic in Washington. Despite weak demand, the price of a barrel of crude oil surged more than 25 percent in the past year, reaching a peak of $113 May 2 before falling back to a range of $95 to $100 a barrel.

The Obama administration, the Bush administration before it and Congress have been slow to take steps to rein in speculators. On Tuesday, the Commodity Futures Trading Commission, a U.S. regulatory agency, charged a group of financial firms with manipulating the price of oil in 2008. But the commission hasn't enacted a proposal to limit the percentage of oil contracts a financial company can hold, while Congress remains focused primarily on big oil companies, threatening in hearings last week to eliminate their tax breaks because of the $38 billion in first-quarter profits the top six U.S. companies earned.

The Saudis, however, have struck a steady theme for years that something should be done to curb the influence of banks and hedge funds that are speculating on the price of oil, according to diplomatic cables made available to McClatchy by the WikiLeaks website.

The cables show that the subject of speculation has been raised in working group meetings between U.S. and Saudi officials, in one-on-one meetings with American diplomats and at least once with President George W. Bush himself.

The Saudi concerns about speculation have a particular sheen of credibility. Saudi Arabia is the world's largest exporter of oil, serving dozens of clients in addition to the United States. As such, it carefully tracks the trends that drive oil prices, which send it billions of additional dollars with every increase.

But in the cables, Saudi officials explain that they have two primary concerns about artificially high crude prices: that they'll dampen the long-term demand for oil and that the wide price swings typical of commodity speculation make it difficult for them to plan future oil field development. After that $147 a barrel peak in 2008, for example, prices plunged to $33 a barrel as the global financial crisis rocked the world. That was a stunning change in less than half a year.

One cable recounts how Dr. Majid al Moneef, Saudi Arabia's OPEC governor, explained what he thought was the full impact of speculation to U.S. Rep. Alan Grayson, D-Fla., who in July 2009 was in Saudi Arabia for the first time.

According to the cable, Moneef said Saudi Arabia suspected that "speculation represented approximately $40 of the overall oil price when it was at its height."

Asked how to curb such speculation, Moneef suggested "improving transparency" — a reference to the fact that most oil trading is conducted outside regulated markets — and better communication among the world's commodity markets so that oil speculators can't hide the full extent of their trading positions.

Moneef also suggested that the U.S. consider "position limits" — restrictions on how much of the oil market a company can control — something the CFTC is considering. But the proposal to prevent any single trader from accumulating more than 10 percent of the oil contracts being traded hasn't received final approval, and the CFTC also has yet to define what it considers excessive speculation.

Saudi concerns also came up during a May 2008 meeting in Riyadh, the Saudi capital, between U.S. officials and Prince Abdulazziz bin Salman bin Abdulaziz al Saud, the assistant petroleum minister.

Prince Abdulazziz was "extremely worried" that high prices would destroy the demand for oil, according to the May 7, 2008, account of his meeting with embassy officials.

"Aramco is trying to sell more, but frankly there are no buyers," the cable quoted him as saying, referring to the Saudi state oil company. "We are discounting crudes."

Another confidential document from the embassy in Riyadh, dated Feb. 14, 2007, indicates that Saudi officials had concluded years ago that speculation played at least as big a role in setting oil prices as traditional issues of supply and demand did.

Recounting the presentation by Yasser Mufti, a planner for Aramco, at a conference of U.S. and Saudi officials, the cable said: "The Saudi analysis indicated a link between higher oil prices and the influx of investor funds into the oil markets."

Indeed, the cable noted, "As the oil futures markets play an increasingly large role in setting world oil prices, (Mufti) remarked his team was now obtaining better insights into prospective oil prices from banks than from those working in the real oil sector, such as refiners."

Another document, from Sept. 2, 2009, offers an eerily accurate prediction of today's high prices, made by Sadad al Husseini, Aramco's former executive vice president.

"In his view, the bearish energy analysts arguing that the oil price shocks of last summer are not likely to be repeated anytime soon are making inaccurate assumptions," the cable said, warning that the former Aramco executive saw political uncertainty and a perception of tight supplies as fuel for speculators.

The cable said that "al Husseini predicted that another oil price shock would likely hit sometime in the next year or two."

A McClatchy investigation earlier this month showed the extent to which financial institutions now influence the price of oil. Until recently, end users of oil — such as airlines, refineries and other consumer of fuel — accounted for about 70 percent of oil trading as they tried to hedge against price fluctuations.

Today, however, speculators who'll never take possession of a barrel of oil account for that 70 percent of oil futures trading, and the volume of speculative trading has grown fivefold.

That's why the Air Transport Association, in a filing March 28 to the CFTC, called for aggressive curbs on speculators. The association complained of rapidly climbing jet fuel prices, which have outpaced the rapid climb in crude prices and have reached their highest point since September 2008, right before the near-collapse of the U.S. economy.

"At the same time, according to data recently released by the commission, speculators have increased their positions in energy markets by 64 percent compared to June 2008, bringing speculation to the highest level on record," wrote David Berg, the airline group's chief lawyer.

The WikiLeaks documents also shed light on other aspects of Saudi Arabia's oil industry.

One document said that Saudi Arabia has boosted its excess capacity — the difference between the amount of oil it could produce and the amount it pumps for its clients — from 2 million barrels per day to 4 million, a margin that offers assurance that there'll be little disruption to oil supplies from political unrest in places such as Libya, where oil production has ground to a halt.

Another quotes the chief economist of Saudi investment bank Jadwa Investment as estimating in June 2008, shortly before oil prices peaked, that the kingdom earned more than $1 billion a day from oil. Another quotes Aramco's treasurer as saying the state oil company had its own Europe-based global investment fund that in April 2008 had assets worth $60 billion.

A fourth document quotes the Saudi assistant petroleum minister as expressing concern to Ambassador James Smith that Saudis could be "greened" out of the U.S. market. The minister noted in 2009 that the United States for the first time had consumed more ethanol than it did Saudi oil.

Read more here: http://www.mcclatchydc.com/2011/05/25/114759/wikileaks-saudis-often-warned.html#storylink=cpy#storylink=cpy#storylink=cpy

gap should now fill...

at $44.24?

I think all the charts say hold on...

I buy UCO... not USO. I sold several 100 shares of UCO, but the majority I did not get stopped yet because it triggers at $44.50

Then I put a 1% trailing stop. Today if the market was open, we would have opened at over $45.50 in UCO. My trigger would have happened and my stop would be around 45.. a good profit for this trade.

I can see oil maybe topping $110 but it is s crap shoot.

http://investorshub.advfn.com/boards/board.aspx?board_id=14846

It looks like we open above 45.50

makes pssoble clear sailing to about $50...

Oil is funny though

Looks like we are going to bump $45

It really is a guess. But I think we for now long may be the ticket... But I have my stops in place...

We own this one... $18K A little paint is all she needs. What can you rent that for?

Hey xero90...

I'm in UCO, the 2x... I took a profit in part yesterday. I have a trade trigger in at $44.35 with trailing stop of 1%. We'll see what happens.

If economy is good, I suppose this will be good too.

It just seems to me for a company to get Grants... CEO leaves with $250K exit pay... a technology that was never really valid until gasoline price hits a $$. Why the heck should a taxpayer grant crap like this?

The free market crowd is money motivated. The get it where they can. Even more reason the government needs to stay out. I can understand a tax break.. but grants?? For People to abuse grants like the CEO of this company.

You and I get fired... NO exit pay. Nothing but maybe vacation pay left over. Like I said, a scam. The board played favorites and rewarded this guy when they should have told him to take a hike. Favors to these companies from our politicians so they can "fake" everyone out like us small traders.. lol... And believe me, this was only a small part of the money flowing to those that should not have gotten it nor would have in a free market company startup company.

Thinking this one could be good soon.

Big.. If the Feds wanted, they could pass a law that say only Nuke energy. Then some company would step up.

If the Feds really wanted to create demand and eliminate oil and gasoline, they pass a law that says “no more gasoline cars by 20??”. Then allow the car makers to switch to natural gas, electric or whatever. These laws aren't going to happen because it makes no sense. We have other ways of making electricity so much cheaper. Natural gas turbine and gasoline is just not short in supply yet. Until gasoline price gets high enough to change demand, we stay gasoline until to maybe a car like the Volt.

This company was kinda of a scam anyway. That past CEO and others took huge exit payoffs when they left when the business was losing money and a fat pig. What did he get to leave $250K? Let's see, you drive the company into BK and get $250K... All with grant money and the support of both republican and democrats. The politicians are just not smart enough to pick a winner. Let free enterprise do it.

Feds spent money that is a dead again. Lucky, I saw this playing out last year and only lost a $1000 or so.

Hey... what about Lugar?

Obama pushes energy plan in campaign-style tour

By Caren Bohan

LAS VEGAS | Thu Jan 26, 2012 3:37pm EST

LAS VEGAS (Reuters) - President Barack Obama pitched a plan on Thursday to boost U.S. use of natural gas and open more land for offshore drilling during a campaign-style tour aimed at bolstering confidence in his economic stewardship.

At a stop in Las Vegas, Nevada, the Democratic president sought to counter Republican criticisms of his energy policies as he proposed tax incentives for companies to buy natural gas trucks, which would help build demand for abundant domestic supplies of the fuel.

Republicans have hammered Obama on his handling of the energy issue, and were angered by his decision to block the Keystone XL Canada-to-Texas oil pipeline, which they say would have created jobs and reduced U.S. dependence on oil from the Middle East.

Obama said the United States needs an "all-out, all-in, all-of-the-above strategy" to develop energy resources at home and that doing so would create American jobs. Critics complain that Obama, gearing up for the November 6 election in which he is seeking a second term, favors a green agenda over traditional oil and gas energy development.

"A great place to start is with natural gas," Obama said during a visit to a UPS facility in Las Vegas, which received stimulus funding to invest in liquefied natural gas vehicles and build a public LNG refueling station.

"We've got a supply of natural gas under our feet that can last America nearly a hundred years," he said. "Developing it could power our cars, our homes, and our factories in a cleaner and cheaper way. The experts believe it could support more than 600,000 jobs by the end of the decade."

Obama, seeing some improvement in his poll numbers, is touring five states - Iowa, Arizona, Nevada, Colorado and Michigan. The trip follows his State of the Union address on Tuesday in which he took a combative tone toward congressional Republicans and spoke of the need to reduce income inequality.

Obama's overall approval ratings had sagged amid voter concern over the lackluster economy, but his popularity has inched higher and in some recent surveys has climbed above the important 50 percent threshold.

In Tuesday's address to a joint session of Congress, Obama spoke of the nation's booming natural gas sector, which has grown dramatically in recent years as advances in technology have unlocked vast new reserves.

Later on Thursday, Obama will visit Buckley Air Force Base in Aurora, Colorado, where the Air Force is installing a one-megawatt solar panel system, and where last year it test-piloted jets that run on advanced biofuels.

A CLEAN ALTERNATIVE?

Increasing domestic natural gas consumption would benefit drillers, as U.S. natural gas prices have fallen sharply because of the growing glut and the relatively warm winter.

Using domestic natural gas as a cleaner alternative to importing foreign oil has been heavily promoted by Texas oil billionaire T. Boone Pickens and has attracted support from both sides of the aisle in Congress.

Still, Obama's natural gas truck proposal, which would need congressional approval, could face an uphill battle to make it into law. Republicans, campaigning on promises to cut government spending, would likely resist costly energy subsidies.

Similar measures aimed at expanding tax breaks for natural gas vehicles have failed to break through partisan gridlock, and conservative groups have opposed such legislation on the grounds that government should not be in the business of picking winners and losers in the energy sector.

Obama also announced that the Interior Department will hold the last scheduled offshore lease sale of the government's current five-year drilling plan in June, offering 38 million acres (15 million hectares) for development in the central Gulf of Mexico.

In December, the department held its first offshore lease sale since the massive BP oil spill in April 2010. Companies successfully bid more than $337 million for rights to drill in the Gulf.

Analysts said those results were a sign that drilling is rebounding in the Gulf after the administration temporarily shut down deepwater exploration after the BP disaster.

Still, oil and gas industry backers have complained that the administration has hindered drilling through slow permitting and a raft of new rules implemented since the 2010 oil spill.

Obama: U.S. 'Saudi Arabia of Natural Gas'

Obama calls America the "Saudi Arabia of natural gas," pushes for more refueling stations

By Jason Koebler

January 26, 2012 RSS Feed Print

President Obama called America the "Saudi Arabia of natural gas" Thursday and said the country should start using natural gas to power more cars and trucks.

Obama made the remarks in light of his decision to open nearly 38 million acres of the Gulf of Mexico for oil and natural gas extraction, saying that natural gas could support more than 600,000 jobs by the end of the decade.

"Because of new technologies, because we can now access natural gas that we couldn't access before in an economic way, we've got a supply of natural gas under our feet that can last America nearly a hundred years," he said.

Much of that gas—up to 4 trillion cubic feet, according to the Department of the Interior—lies beneath the Gulf of Mexico area that the administration will lease out starting in June.

According to the Department of Energy, the United States produced 21 percent of the world's natural gas in 2009. That share figures to increase over the next several years as Obama employs an "all-in, all-of-the-above" energy strategy.

Obama said the government is working with the private sector to build "natural gas corridors" along U.S. highways with natural gas fueling stations.

So far, American consumers haven't taken to natural gas-operated cars. According to the Department of Energy, the number of natural gas operated vehicles remained fairly stagnant between 2001 and 2009, hovering just above 110,000 nationwide, and only half of the 900 or so natural gas stations in the country are open to the public. By comparison, there were more than 160,000 conventional gas stations in 2009, according to the Department of Energy.

Natural gas as car fuel isn't a new idea—it's been used sporadically since the 1930s. Natural gas burns cleaner and has traditionally been cheaper than standard gasoline. It also gets similar gas mileage and driving performance as standard gasoline. But natural gas tanks take up more space in a car, leading to a lower overall range per tank, which is a huge problem considering the lack of refueling stations nationwide.

That's slowly changing. In 1998, Honda introduced the Civic GX, which runs on natural gas, in California, whose 215 natural gas refueling stations represent about a fifth of the nation's total. In September 2011, the company announced that it'd make the car available to 200 dealers in 35 states to "support growing consumer interest in alternative-fuel vehicles."

See.. everything is going to be very good for gas fund

Robert New WTIC

Saudi Arabia is not ‘targeting’ $100 oil

Reuters Jan 17, 2012 – 3:20 PM ET | Last Updated: Jan 17, 2012 1:58 PM ET

By John Kemp

Commentators identifying a new Saudi “price target” at $100 per barrel are wide of the mark.

Saudi Arabia’s views on what constitutes a reasonable price for oil have less influence than analysts would like to believe.

Past experience suggests the kingdom is unwilling or unable to influence prices by adjusting production policy, except in extreme circumstances, and normally allows the market to set the price of crude with little intervention.

Interviewed by CNN on Monday, veteran oil minister Ali al-Naimi promised the kingdom would respond to customer demand in the event that sanctions restrict the supply of crude from Iran.

“We can easily get up to 11.4, 11.8 (million barrels a day, b/d) almost immediately in a few days,” Naimi told CNN, up from just under 10 million b/d now. “all we need is to turn valves.” The Saudi oil chief said the country could add another 700,000 b/d to reach full capacity of 12.5 million b/d within 90 days.

Naimi also appeared to state a new price target. “If we were able as producers and consumers to average $100, I think the world economy would be in better shape.”

“Our wish and hope is we can stabilise this oil price and keep it at a level around $100,” Naimi said.

It is the first time a senior Saudi official has identified a price since King Abdullah stated $70-80 per barrel would be a “fair” price for consumers and producers back in November 2008.

Oil analysts have seized on the revision as confirming their view leading OPEC members need higher prices to cover the cost of increased social spending following the Arab Spring, putting an effective “floor” under the market at around $100, and ensuring crude prices remain on a medium-term upward trend.

But that is not what Naimi said and does not accord with previous Saudi decision-making. Traders and investors would be unwise to place too much emphasis on the $100 figure. It certainly will not guide the kingdom’s output policy.

The last time the kingdom stated a preference for prices analysts and traders treated it as an informal target. Statements from Saudi officials and other members of OPEC gave some support to that interpretation. But as prices pushed above $80 the kingdom refused to add extra barrels, insisting the physical market was well supplied and there was no need for more oil.

There is no evidence the Saudis themselves treated the $70-80 figure as an operational target rather than simply an aspiration. For a figure to function as a target, there would need to be some sort of feedback from observed market prices to production policy, and in this case there was not.

While Saudi Arabia has periodically expressed views about what constitutes a “reasonable” price, policy has usually focused on targets other than price, for example stock levels or customer demand. There is no more reason to believe Saudi Arabia will adjust production to keep prices at $100 than there was to assume it would alter output to keep them at $70-80.

If Naimi was expressing any firm view at all, it was that the kingdom did not want to see a further escalation in prices, not that it wanted to establish a floor.

When King Abdullah suggested $70-80 would be a fair price for both consumers and producers, actual spot prices were around $55. Abdullah was really asking for a price increase, and suggesting consuming countries should not complain too much if prices rose.

What he was not doing was promising to add extra barrels to the market if prices went above $80. Abdullah was expressing a view on the desirable direction of prices, not committing the kingdom to a price-targeting policy.

Fast-forward to January 2012, and Naimi also seems to have been indicating a view about the desirable direction of prices rather than creating a new target.

Naimi spoke when spot Brent prices were around $111.

By implication Naimi was indicating prices were already high and the kingdom would be happy to see them drop slightly. Certainly the kingdom would not welcome a spike in prices to $120 or $150 or more as some analysts have suggested may happen.

The oil minister’s concerns about rising prices are consistent with the kingdom’s current views about the global economy and Iran. On growth, the kingdom seems anxious to avoid another sharp rise in prices that would throw the global economy into another tailspin.

On Iran, the kingdom has quietly supported efforts by the United States and its allies to pressure Tehran into ending its uranium enrichment program. But like the Obama administration, EU policymakers and sanction promoters like Mark Dubowitz, head of the Washington-based Foundation for Defense of Democracies, the Saudi government wants to ensure that sanctions do not lead to a damaging price spike.

In his interview, Naimi was actually promising to provide more oil in the event that sanctions or a military confrontation disrupt supplies from Iran (because the kingdom fears an uncontrolled price increase) not withdraw them to support prices at $100.

Saudi officials are well aware that Iran benefits from higher oil prices (both directly as an oil exporter and indirectly because the economic fallout for consuming countries increases their reluctance to risk further disruptions).

From a diplomatic perspective, Saudi Arabia has an interest in seeing stable or lower prices, not encouraging higher ones.

But Saudi officials are realistic about the limits of their influence. In the short term (3-12 months), Saudi Arabia will not be able to keep prices above $100 if the world economy slides back into a second recession.

In the long term (5-10 years), the kingdom and other OPEC members face a challenge from increasing oil supplies outside the cartel, especially from unconventional methods such as fracking, that could cut their market share.

The most Saudi Arabia can realistically hope for is to stabilise market expectations and help dampen the wild (and irrational) price swings as investors and other market participants swing from extreme concerns about supply (“peak oil”) to fears about demand (“double dip”).

In referring to $100, Naimi probably hoped to provide an informal “anchor” for expectations against a further rise, not a fall.

By its own account Saudi Arabia has around 2.5 million barrels per day of spare production capacity, most of it available on short notice and the remainder within 90 days. Saudi Arabia can pledge that spare capacity to make up any shortfall in physical supplies from Iran, or stabilise prices, but it cannot pledge the same spare capacity twice over.

It is a subtle point but an important one. If Saudi Arabia boosted exports now by 500,000 b/d to push prices to $100, it would no longer have enough capacity still in reserve to meet a cessation of Iran’s exports in future.

If Saudi Arabia is, at some point, forced to make up for the loss of 1.5 million b/d of Iranian exports, it will have little or no spare capacity to deal with any further disruptions beyond that, and little or no capacity to stem a further rise in prices.

If Saudi Arabia’s spare capacity is (informally) hypothecated to make up for Iranian exports if and when they are disrupted, the same spare capacity cannot be ear-marked to defend against price increases for other reasons (stronger than expected growth in China, recovery in the West, disruptions in Nigeria).

In his interview, Naimi may have indicated the kingdom would prefer slightly lower prices, but he was careful not to pledge to turn on the taps to achieve them.

The $100 figure is an aspiration and indication the kingdom would prefer not to see another price spike. It is not a target or a floor, let alone a commitment to cut production if prices drop below that level.

John Kemp is a Reuters market analyst. The views expressed are his own.

Keystone XL Pipeline Seen Moving Ahead on Alternative Route.

Jan. 18 (Bloomberg) -- The Obama administration will announce rejection of TransCanada Corp.’s Keystone XL pipeline as soon as today, according to two people familiar with the matter. Peter Cook reports on Bloomberg Television's "InBusiness With Margaret Brennan." (Source: Bloomberg)

Workers wearing anti-OPEC shirts attend the State Department's open hearing for the proposed Keystone XL Pipeline at the Port Arthur Civic Center in Texas on Sept. 26, 2011.

A TransCanada Corp. (TRP)’s $7 billion Keystone XL oil pipeline still will move ahead with an alternate route after President Barack Obama’s decision to deny a permit, investors, public officials and analysts say.

Obama blamed congressional Republicans yesterday for imposing a deadline on his decision, which he said left no time to approve the project. His administration invited TransCanada to reapply, an overture the Calgary-based company promptly said it would accept.

Denying the permit pushes a final decision on the pipeline into 2013, safely past this year’s presidential election. John Stephenson, who helps manage $2.7 billion for First Asset Management Inc. in Toronto, said he bought 350,000 shares yesterday as TransCanada fell the most in 18 months.

“This is clearly the biggest infrastructure project on the continent, and once the election is settled, we believe it will be approved,” Stephenson said in an interview. “All the waffling just gives people an opportunity to trade around it.”

TransCanada closed yesterday at $41.41, down 0.8 percent in New York trading, after falling as low as $39.74 on news of the president’s decision. That was a decline of 4.8 percent, the most since June 2009.

Yesterday’s decision by the State Department was praised by environmentalists and was decried by the U.S. oil and gas industry and Republican presidential candidates and lawmakers, who had pushed Obama to approve the project as a way create jobs.

Congressional Deadline

Obama acted before a Feb. 21 deadline Congress set after he postponed a decision to allow for a review of of a revised route through Nebraska. TransCanada said the 1,661-mile (2,673- kilometer) project would carry 700,000 barrels of crude a day from Alberta’s oil sands to refineries on the U.S. Gulf of Mexico coast, crossing six states and creating an estimated 20,000 jobs.

Obama called Canadian Prime Minister Stephen Harper, who told the president Canada will seek to diversify its energy exports after Keystone was rejected. Harper “expressed his profound disappointment” with the Keystone decision, according to a statement from his office.

Currently, 99 percent of Canada’s crude exports go to the U.S., a figure that Harper wants to reduce in his bid to make Canada a “superpower” in global oil markets. Canada this month began hearings on a proposed pipeline from the oil sands to the British Columbia coast, where it could be shipped to Asian markets.

‘Proper Routing’

The State Department said in a report to Congress yesterday that the pipeline would create 5,000 to 6,000 construction jobs during the two years needed to build the project, based on labor expenses TransCanada included in its application.

“Once we get the proper routing done, I think it’s very appropriate that the country accept that as an oil source,” Anadarko Petroleum Corp. (APC) CEO Jim Hackett said Wednesday at a conference in Houston on North American energy prospects. “We have one of the most friendly nations to our country who has never stopped trade in my lifetime that is willing to send their supplies down to us as if it were domestic oil.”

Congress’s deadline would have forced Obama to choose in an election year between environmental supporters, who said the pipeline will worsen climate change and endanger drinking water supplies in Nebraska, and organized labor.

‘Politically Motivated’

The decision to deny the permit was “politically motivated” and will make the U.S. more dependent on foreign nations “that don’t share our interests,” U.S. Chamber of Commerce President Thomas Donohue said.

Environmental groups praised the decision, mindful that the pipeline still is a possibility.

“We’re going to declare victory today and tomorrow we’ll deal with the new application,” Susan Casey-Lefkowitz, director of the international program at the Natural Resources Defense Council, said in an interview. “I don’t think that they are predisposed to approving the pipeline.”

U.S. House Speaker John Boehner, an Ohio Republican, accused Obama of “selling out American jobs for politics,” and said Congress would consider adding pipeline language to a longer-term extension of the payroll tax cut sought by Obama, and the reauthorization of Federal Aviation Administration and surface transportation programs.

House Energy and Commerce Chairman Fred Upton, Republican from Michigan, said his committee has asked Secretary of State Hillary Clinton to testify next week on the decision.

American-Made Energy

“I’m disappointed that Republicans in Congress forced this decision, but it does not change my administration’s commitment to American-made energy,” Obama said in a statement. “We will continue to look for new ways to partner with the oil and gas industry to increase our energy security.”

TransCanada applied for a U.S. permit in 2008. Canada is the largest U.S. oil supplier at about 2.67 million barrels a day, compared with about 970,000 barrels a day from Venezuela, which ranked fourth in exports to the U.S. in the first 10 months of 2011, according to the Energy Department. Mexico and Saudi Arabia ranked second and third in shipments to the U.S.

“Until this pipeline is constructed, the U.S. will continue to import millions of barrels of conflict oil from the Middle East and Venezuela,” TransCanada Chief Executive Officer Russ Girling said in a statement. The company said the pipeline might still be ready to open in 2014 if the U.S. expedites review of its new application.

New Plans ‘Underway’

“While we are disappointed, TransCanada remains fully committed to the construction of Keystone XL,” Girling said. “Plans are already underway on a number of fronts to largely maintain the construction schedule of the project.”

Nebraska Governor Dave Heineman also said he was disappointed.

“Approval of the pipeline would have allowed TransCanada to move forward with the project while Nebraska finished the review process of a new segment of the route,” Heineman said in an e-mailed statement.

Heineman, in an interview this week with the Governor’s Journal website, said he expected TransCanada to propose at least one more route for the pipeline in the next 10 days. State environmental reviews would take up to nine months, he told the website.

Alternate Pipelines

The ultimate fate of the project may rest on oil prices and whether alternate pipelines emerge, according Kevin Book, managing director at ClearView Energy Partners LLC, a Washington-based policy-analysis firm.

“We regard realization of the XL project as more likely under a Republican Administration in 2013, but we don’t believe the project is necessarily dead even if President Obama returns in 2013 for another term,” Book said in a client note yesterday.

If the U.S. rejects Keystone, two possible pipelines could send the crude west for export to Asian markets, according to Neil Beveridge, a Hong Kong-based analyst at Sanford C. Bernstein & Co. Canadian Prime Minister Stephen Harper touched on alternate export routes when he told Obama in a telephone call yesterday that Canada will seek to diversify its energy exports.

“If it’s not taken to the lower 48 states, I know that it will be developed and probably go to the Asian markets,” ConocoPhillips (COP) CEO Jim Mulva said yesterday at a conference in Houston. It would be a “significant lost opportunity for the United States.”

Saudi Arabia’s November Oil Output Rise to 30-Year High

January 19, 2012, 3:21 AM EST

By Wael Mahdi

Jan. 18 (Bloomberg) -- Saudi Arabia, OPEC’s largest crude producer, increased output in November to the highest level in more than 30 years while boosting exports by more than 10 percent, according to the Joint Organization Data Initiative.

The country pumped 10.047 million barrels a day of crude, up from 9.36 million in October, statistics posted today on JODI’s website show. Exports rose by 721,000 barrels a day to 7.8 million barrels a day, according to the figures, which include condensates and exclude natural-gas liquids.

Saudi Arabia’s crude-oil consumption fell by 9.2 percent in November from the previous month, when it reached the highest level since at least 2002, according to JODI. The world’s largest exporter of crude used an average of 1.84 million barrels a day of oil in November, compared with 2.02 million barrels in October. The kingdom’s oil consumption has grown at an average of 4.8 percent a year in the past five years, Riyadh- based Jadwa Investment Co., said last month.

Oil Minister Ali Al-Naimi said at last month’s meeting of the Organization of Petroleum Exporting Countries in Vienna that Saudi output increased because there was no excess supply in world crude markets and that his nation had been adjusting output to match fluctuating demand of recent months.

JODI’s production figure corroborates comments made by al- Naimi on Dec. 6, when he said in an interview in Durban, South Africa, that November output exceeded 10 million barrels a day, more than most independent estimates at the time.

The initiative is supervised by the Riyadh-based International Energy Forum and compiles data provided by member governments. The IEF is a group of nations accounting for more than 90 percent of global oil and gas supply and demand, established as a forum for producing and consuming countries to discuss international energy security.

--Editors: John Buckley, Raj Rajendran

He says oil going down in next couple days.. We'll see.

Still very mixed

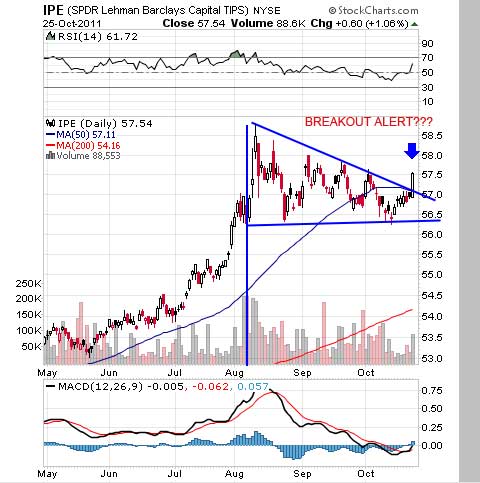

A new TIPS type fund

ProShares, the country’s fourth most successful exchange traded fund (ETF) company,1 today announced the launch of ProShares 30 Year TIPS/TSY Spread (NYSE: RINF) and ProShares Short 30 Year TIPS/TSY Spread (NYSE: FINF), the first ETFs designed to provide exposure to breakeven inflation,2 a widely followed measure of inflation expectations. The ETFs list on NYSE Arca today.

The two new ProShares ETFs are:

• RINF — seeks to match the performance of the Dow Jones Credit Suisse 30-Year Inflation Breakeven Index, before fees and expenses.

• FINF — seeks to provide the inverse of the daily performance of the Dow Jones Credit Suisse 30-Year Inflation Breakeven Index, before fees and expenses.

“Many investors are focused on inflation and closely follow breakeven inflation, a common yardstick for inflation expectations,” said Michael L. Sapir, Chairman and CEO of ProShare Advisors LLC, ProShares’ investment advisor. “We are pleased to offer investors the first ETFs linked to this important economic indicator.”

Breakeven inflation aims to isolate the market’s expectation of inflation implied by the difference in yields between Treasury Inflation Protected Security (TIPS) and Treasury bonds. The Dow Jones Credit Suisse 30-Year Inflation Breakeven Index tracks the returns of a long position in 30-year TIPS and a short position in Treasury bonds.3, 4

WTIC back down to 80... So I wait for good time to enter here.

Hummm...??

Fighting resistance... What's next?

DeadC... I think the PR yesterday means the company is about to be heavily diluted. That was a bridge loan until the figure out how to make some cash (Which I cannot see this happening soon) or Grant or big loan.

Trade it like a penny stock... small investestment, in and out... make the bid and ask come to you... imo

This is a penny stock and I would expect that to be the norm.

I did a candlevolume chart.. SYTE had some pretty big volume days this years. I suppose it's Jonathan Dash trying to exit. He is the one who drove it up above 10 Cents too. But this is a new business plan now.

I'm thinking this is a buy right now.

nice cash flow machine....

Wow.. last Q FRE sold $789,411 worth of property!

Seems to me this one will go like most penny stocks...

Russian will put some cash into company, do it by RS, screwing all current shareholders, yet giving himself enough shares to keep total control over the company.

I say no way another USA grant is coming give the Solyndra scam.

Electric cars are ahead of the times right now. It is going to take gasoline to reach at least $10+ a gallon for this stuff to take off. And meanwhile the auto companies are coming up with higher MPG cars.. it is going to be a long time before a car like the Think will be high demand.

Russians are mobsters anyway and you place enough money in this stock, they are gonna take it.

IMO.

$.169 divy 11/9/11

OPEC expects oil prices at $85-95 over next decade

.

Reuters Nov 8, 2011 – 3:40 PM ET

By Alex Lawler and Sylvia Westall

LONDON/VIENNA – Oil producer group OPEC is investing in new supplies to meet rising consumption, even as it sees the risk to the demand outlook as being on the downside because of Europe’s sovereign debt crisis and a slowing global economy.

The Organization of the Petroleum Exporting Countries in its 2011 World Oil Outlook increased its estimate of supplies, saying the amount of unused oil production that the 12-member group holds in reserve in case of supply shocks would double by 2015.

World oil demand is expected to rise to 92.9 million barrels per day (bpd) by 2015 in OPEC’s reference case presented in the report, up 1.9 million bpd from last year’s forecast. Actual oil demand averaged 86.8 million bpd in 2010.

But the report cited an array of challenges for the global economy such as waning monetary stimulus, the euro zone debt crisis and signs that emerging countries — expected to drive oil demand — are not immune to worsening economic conditions.

“All this has led to heightened downside risks for the world economy,” OPEC Secretary General Abdullah al-Badri wrote in an introduction to the 287-page annual report published on Tuesday.

OPEC, which pumps more than a third of the world’s oil, is typically more conservative on oil demand than other forecasters such as the International Energy Agency. The IEA is due to issue its own long-term energy outlook on Wednesday.

“It is worth stressing that risks appear skewed towards the downside, especially since the sovereign debt crisis in some EU countries seems to be spreading and the world economy slowing down further, with potential consequences for the global financial system,” OPEC said.

Increased political uncertainty in Italy, where Prime Minister Silvio Berlusconi is under pressure to resign, has added to turmoil in Europe from the Greek crisis, which has hit markets in recent weeks.

OPEC’s report looks out to 2035, when it expects world oil demand to reach almost 110 million bpd in the reference case. Last year’s report stopped at 2030, when it foresaw demand of 106 million bpd.

HIGHER PRICES

The report assumes an oil price of $85-$95 a barrel this decade, up from a $75-$85 assumption last year and below Tuesday’s session high of more than $116 for Brent crude.

Oil reached a high so far in 2011 of $127 a barrel in April as the conflict in OPEC member Libya shut down its supplies. Badri told a news conference in Vienna he did not expect oil to fall below $100 soon.

“We leave it to the market to decide but to be more specific I don’t think the price will come down below $100 by the end of this year,” he said.

Saudi Arabia and its Gulf OPEC allies raised production unilaterally after failing at the group’s last meeting in June to convince other members to agree a coordinated increase to meet the Libyan shortfall.

As a result, OPEC’s unused production capacity declined to about 4 million bpd for part of this year, the report said.

OPEC estimated its spare capacity would double from that level and reach 8 million bpd in the medium term to 2015 as Libyan supply recovers and as a result of investments by other OPEC countries to expand output.

The report said member countries had provided details of 132 projects they were planning from 2011-2015, which would result in investment close to $300 billion in that period if all the ventures are developed.

“Regardless of all the challenges and uncertainties, OPEC member countries continue to invest in additional capacities,” the report said.

The report reiterated OPEC’s view that Libyan output would return to pre-war levels relatively quickly — in 15 months or less. Libya produced 1.6 million bpd in January before the civil war.

Supply is also expected to rise from countries outside OPEC, and the report saw demand for OPEC crude climbing slowly to 31.3 million bpd in 2015, up 500,000 bpd from last year’s forecast.

OPEC has often made clear that carrying spare capacity can be a huge financial risk. The report stressed that producers were concerned about the impact on demand of consumer countries’ energy and climate policies.

In another scenario in which a more rapid shift to hybrids and electric cars takes place, OPEC said world demand by 2035 would reach about 102 million bpd, curbing the need for extra OPEC oil.

“By 2035, the amount of OPEC crude needed will be less than current levels,” under that scenario, the report said. “This means that OPEC upstream investment requirements are subject to huge uncertainties.”

bumping resistance in wti

I don't know about that but it's getting beat up soundly. How low can she go?

Breakout yesterday maybe...

Humm IS $93 too high price for oil right now???

How many ETF's can do this is under 30 days?

Close to a one bagger!

And with the threat of Greece credit defaults bringing down the banks too!