News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

whitenoize

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

One other random thought. Does anyone think the proceeds from the 40mil shares would/could be used to pay out the guarantees to the preferred stock holders?

(ii) waiver by holders of our Series A Convertible Preferred Stock of their right of first refusal,

OK guys and gals, help me out here. I've been sitting back watching this unfold. Several scenarios seem mildly plausible but one thing keeps nagging at me. If they are looking for a reverse merger, why fork over 6Mil cash for only 53%? They could have waited a few months and picked bones, or there are surely any number of OTC listed companies in O&G with their bankruptcy papers already drawn up that could be had for a small percentage of debt.

The optimist in me keeps wondering if maybe the Chinese are still wanting into Guinea and figure better working together with (or behind the guise of) HDYN.

- Do you think they would bid on upcoming tracts?

- Do you think they would have a snowballs chance of getting one or more?

- Do think Guinea will even go ahead with taking bids in light of the Total deal?

On the other hand why would these guys want to get into exploration at all?

Guess I can sit back and see if they let us in on the plan....

You state it much more eloquently than myself. Well put.

What is happening is a large group of promoters pumping a penny stock of a company with few prospects for the future based on a misleading technical bounce.

The underlying facts are that sometimes stocks go down in value for a reason. However, as it is a supply and demand market, promoters will try to sell something they bought on the cheap for a profit by making it sound better than it actually may be. Watch for signs of selectively picking what they choose to put up as evidence of future value vs what they dismiss and put down.

Several will probably report this post to try and have it removed as it does not follow their strategy. Even though I am simply answering your question with my opinion. If not then it will be pushed to the bottom by their continuing "sales pitches"

That said, it is very much possible to make money this way, if you are positioned correctly and know when to head for the exit (before the masses).

GLTA

OK who will be last one out this afternoon.

Just unloaded some more at .251 to reduce my losses.

Thanks guys!

Hey Rule, do you know if all of the Preferred shares got converted? Those are "refundable" if the co fails. I'm thinking since they cut the drill short, there may be a small amt of cash still available to carry rent, salaries, and such for a short time.

Thanks PHX

All is as well as can be expected here. I've repositioned sooo many times I've lost track. Will prolly carry some paper loss for a couple years.

This was supposed to be my bonus after I retired last year. Oh well LOL

Hope all is well with you.

(I had to flee over to IV cause watching this board is making me dizzy...)

Wow even Blackrock sold out and these Kidz just keep pumping.

After all these yrs and more buys and sells than I can remember I doubt if I ever made any real money on this (although I still still have a car I bought after after the US Oil fiasco).

And in spite of that I still feel relatively smart after watching this board today.

Let em play.

If they can pump this back to .50 I still have shares in my IRA I can dump on em.

Well since you showed an interest in something besides the share price, I'll share a little info with you.

The company has an Exploration license, has had for 10 yrs. Last year they were granted a 1yr extension to drill this one final well. If they had discovered hydrocarbons they would have been granted a 2yr period to appraise the discovery.

Their exploration license now expires on Sept 22nd.

No license+ no more cash+ no oil= no bounce (except what the pumpers can generate)

OK, truth be known if this were any other company I might be tempted to play the bounce myself.

But with the share price where it is and less than 2 wks until expiration of license, if Ray pulled another well out his a$$ he would be eligible for sainthood.

Buzzards trying to make a dead cat levitate...

Obviously the well site visit from the Ocean Intervention III on sept 5th was to cap the well. So once again they were raising funds and talking positive right up to the point of failure.

Sorry, but very upset and disappointed right now. Volume spiked at the same time so obviously a leaky ship still. At least some got out with less damage....

Maybe we get money for the movie rights.,.

This was in regards to the SAPETRO farm out agreement which specified, more or less, that HDYN had to raise (or ability to obtain to SAPETRO's satisfaction) min $15 million prior to drilling.

I can dig up actual wording if needed.

While well costs could run over, I believe the company is in good shape for now.

I am also presuming that share payments to PACD were included in the total.

IMHO While this much dilution to fund half of a single well is hardly ideal, this removes much uncertainty from the valuation of a discovery. (and it could have been worse)

edit:

from April 19, 2017 Press Release

In addition to the earlier signed Farmout Agreement, SCS and SAPETRO agreed that SCS's "sufficient financing for the

Obligation Well Costs" shall be $15 million in "cash and committed financing to the satisfaction of SAPETRO acting

reasonably" in addition to costs already incurred, which sets a clear objective for both Parties to work to.

The totals are in...

http://investors.hyperdynamics.com/secfiling.cfm?filingid=1104659-17-56143&CIK=937136

In the aggregate in all six closings of the Offering, the Company sold 10,471,593 Units and issued to Subscribers an aggregate of (i) 10,471,593 shares of Common Stock and (ii) Investor Warrants to purchase an aggregate of 7,853,718 shares of Common Stock, and the Company received an aggregate of $15,288,413.22 in gross cash proceeds, before deducting placement agent fees and expenses, and other fees and expenses, in connection with the sale of the Units in the Offering

Yes the hard floor at 1.46 with the increased volume suggests unwillingness to sell for a loss, so probably warrant holders. Alternately the extra volume is still being absorbed above 1.45 so this is somewhat encouraging as it indicates there is still some demand for the overhead. (unless the MM is going bonkers)

Maybe too early to get the popcorn, but we'll see if this continues...

Well if they can pay the bills with shares that's the same dilution as raising cash, so that much closer to retaining full 50%. Let's get SLB on board with this program lol!

While I've seen a lot of guesstimates based on a given number of shares outstanding, value of oil in the ground, and percentage retained. Most of them use the amount of oil to be discovered with the 1st well and come up with something in the mid $4 range.

I see a discovery as making the full NSAI estimates much more probable and I feel the market would give some allowance for that. I further believe that another prospect could be tested in the 2yr period following discovery and that prospect would be given a higher chance of success.

I also feel that oil in the ground carries a higher value in this field and at this time than the $2 number being used.

If nothing else, these things would have to be considered in a buyout. So I don't have a problem hoping for something north of $12 and even north of $22 if exuberance takes over.

Unfortunately there is still a lot of unknown on financing, retained percentage, and specific drilling plans in event of a discovery.

Just my .02

Just to clarify on E-seis stock issue. From the 8-K:

On August 23, 2017, we issued 204,373 unregistered shares of Common Stock to eSeis, Inc., a Delaware corporation (“eSeis”), in lieu of a cash payment of $291,500, as partial compensation for certain services to be provided by eSeis to the Company’s wholly-owned subsidiary, SCS Corporation Ltd.

Lately I feel like I'm watching the lottery drawing and the first 3 numbers they pulled matched mine. I know that gets me a whopping $1, but it makes me feel like it wouldn't take much more for something really good to happen.....

Welcome aboard the 'Hub ! (eom)

You mean SAPetro, not PACD, covering funding shortfall.

Several factors could be capping the share price IMHO.

-The Preferred offering "cannibalized" some long positions as they sold off their long holdings for an improved position with warrants.

-The common stock offering, which seems to be still open, will hold it close to the 1.43 pricing as larger players can buy in direct rather than on the open market.

-There is still no announced resolution on the funding, so buyers do not have specific numbers on what the companies stake in the concession will be.

- Some uncertainty remains as PACD is not obligated (though likely) to fill in any funding shortfall. The potential reverse split also adds uncertainty for some.

The silver lining? Volumes seem to be picking up, so maybe some of the overhang will get digested. Operationally, all seems to be falling into place. A discovery will resolve a lot....

Finally it's ON. I was going to post a note on Scirocco yesterday, but wasn't certain it was significant.

PACIFIC SCIROCCO

Position: 8° 37' 28" N, 14° 54' 08" W

Last seen: 2017-08-08 02:29 CDT

Location: Gulf of Guinea West, GN

Destination: OFFSORE GUINEA

ETA: 2017-08-01 19:00 CDT

2017-08-0706:51 CDT

Navigation status changed restricted manoeuvrability

Obviously, we now have only to hope for an uneventful drill and await results.

GLTA

Thanks. Note that Troms Lyra is at Scirocco now as well as Gubert Tide and a tug.

Ticking away the moments that make up a dull day...

Thought I would take a moment to check in as there is no real news.

Looks like Troms Sirius made a run to Sekondi/Takordi and is now in Abidjan. Troms Lyra has made it past the Canary Isles and shows an ETA of 7-29 for Conakry. SVS Guardsman continues to make occasional runs from port to drill ship. Haven't found any other relevant ships yet, but at least some progress is being made.

I received my voting info late last week and I see they are already sending out reminders on the reverse split vote.

I also received another solicitation from Katalysts the week before last so they are still nickel and diming the current shareholder base until they can come up with something better I suppose. I hate to see current shareholder base "cannabalised" to raise capital. It really seems to be keeping a cap on the share price. At least the market seems to be absorbing most of it and holding the line at the 1.43 price.

I am anxious to know how the "8 country deliveries" are progressing. I would like to see them start drilling. Hoping they can fund the effort and maintain the 50% (particularly if the reverse split comes to pass).

GLTA

I keep going back and forth on this and inevitably come back to the center. While some feel this R/S would be a preparatory step going forward and others question why they would even consider it, given past history on such activities, I can't help feeling this is related to current financing difficulties.

In spite of constant assurances from the company that there is a lot of interest and things are promising, there still seems to be a shortfall funding the HDYN share of drilling. If some deep pocket entity has expressed interest in funding the company but placed a caveat that the co should be listed on a major exchange, then they are back to jumping through hoops as they did trying to secure a farm out agreement. Once again there is no assurance that the funding would come through even if they meet the requirements laid out. With the timeline what it is, they may not meet listing requirements prior to completing the well, making the exercise a moot point. If they can get listed quickly , drilling SHOULD already be in progress by the time funding comes through. A player at this level will want to hedge their investment, which will put a damper on share price along with the dilution.

To me this seems like a damned if we do damned if we don't scenario. I'm not happy with it, but if it leads to keeping 50% I suppose it's worth pursuing. If it doesn't play through, and there is a discovery, we are going to be cursing mgmt.

All JMHO.....

Definitely on the move. While this sat data is delayed, you can see they are headed offshore.

Thanx for correcting me on that. Getting the CRS lately..

I have noted my funding concerns/thoughts in previous posts. SAPETRO has guaranteed the funds to complete the well in return for additional share of the concession. So the well will get drilled. While not as bad as death spiral financing, it is not ideal in that an unscrupulous partner (we haven't had any of those) might try to leverage that agreement. Is what it is at this point, just difficult to value the company before the final tally is known.

Others on here are more knowledgeable about marine activity than myself. I could speculate that a tug might be used for positioning to conserve fuel on the drillship. It could also be that anything not in the marine traffic database shows up as a tug. really don't know.

Sometimes we forget that not everyone has had the benefit of the resources posted here over the last decade.

Marine traffic site will help keep abreast of ship traffic and shows that much activity has been going on around the Pacific Scirocco's current "waiting" position.

https://www.marinetraffic.com/en/ais/home/centerx:-14.0/centery:9.0/zoom:10

This is in line with Ray's comments about having to complete mobilization AFTER the ship arrived in Guinean waters.

I haven't seen any specific info on Helicopter or other contracts yet, but helicopters aren't as hard to come by in Conakry as they used to be (there were none when the last well was spud). Unfortunately, since the ebola crisis, they are more common in the area with at least 2 currently registered locally.

http://www.rotorspot.nl/current/3x-c.php

Not saying these are contracted for oil services, but it's a remote possibility.

With the company's current funding, I see no reason to be concerned about the Schlumberger contract being met. Someone is loading all of those supplies on the rig.

Hope this helps with some of your concerns. This is an investment that requires a lot of patience more often than not...

It is nice to know you, and people like you, are invested in this company. I'm sure you have an interesting perspective on all of this.

I have been in and out since before the US Oil fiasco, I no longer have any idea where I stand in terms of gains and losses as it is now a matter of satisfaction to see the concession proven. I have always maintained that even if it is a dry hole, the movie rights and seismic data could make the company an asset to someone.

GLTA

So do you, or anyone, have any thoughts on how the funding will be handled as they get closer to spud date?

I know they want to keep offerings open as long as possible to raise as much cash as possible to preserve the company's share of the concession. At a certain point after the well is spud you get into shady area of selling shares while holding non-public information. I presume offerings will be cut off when well is spud. (this time)

To take it a step further. Since Ray has publicly stated that this well is the company's only shot at continuing operations, could any well related events now be considered material information? Shouldn't the amount of the concession retained after funding efforts end be considered material?

Just thinking aloud as we watch...

Well finally some good news. Someone now gives enough of a damn to slam the stock without explanation. I consider this a positive development.

This is an unusual development. Very Interesting....

I can't say how Katalyst Securities/Roman Livson is determining who to contact regarding offerings. Their email states "I received your contact information from Ray Leonard, Hyperdynamics CEO."

The email address they contacted at me at is registered with HYDN's website to receive investor communications. It is also the account registered with my brokerage.

If you would like to contact them, it has been reported that the private placement of common shares is ongoing for qualified investors. Here is the information:

Roman Livson, CFA

Katalyst Securities

630 Third Avenue, 5th Floor

New York, NY 10017

Mobile: +1-917-5457743

Office Direct: +1-212-4006943

Office General: +1-212-4006993

rvl@katalystsecurities.com

www.katalystsecuritiesllc.com

Well let's have a look at why the SP may not be doing what we hoped for.

While the company announced additional funding today, they still have not met their own previously announced threshold for completion of the Fatalla well. The upshot is that SAPETRO has accepted that the company has the ability to, or has secured the remainder of the $15M total, as they have closed the farmout agreement.

From a shareholder perspective this still leaves uncertainty about the exact amount of equity we will hold. Although we are getting a better idea where we stand. Additionally the farmout closure release indicates that the company is currently a 50/50 partner with SAPETRO. This is still subject to change, per the agreement, depending on final well cost and HDYN'S contribution.

On an operational front, rig preparations appear to be continuing as planned on the revised schedule (based on maritime activity). Ray indicated at the shareholder meeting that final rig preparations would have to be completed in Guinean waters to meet the PSC schedule. The revised terms with PACD obviously gave rise to concerns by many (myself included) that significant additional costs could be accrued if the farmout did not close in a timely fashion so drilling could start. I feel the farmout agreement resolves this issue, though some still have concerns.

The final key to lagging share price may be the most obvious. Those who wish to own shares have had a LOOOONG time and numerous opportunities to accumulate; those who wished to add, and have the resources, could have participated in one of multiple offerings; and Institutions who participated in the past left when the stock was delisted.

I don't have interest in running the math to see where we potentially stand with share counts at this juncture. I will continue to wait and hold my current shares until all funding is in place, or the well comes in.......unless something changes

GLTA

When the going gets weird the weird turn pro.

So things to continue to progress towards drilling except for the growing elephant in the room.

Per the 10Q, the company is paying $100K per day to have the drillship in Guinean waters. This is payable in stock at a weighted average price. This ends when the company provides a 28 day notice to commence drilling or July 17th ( I don't want to speculate which will come 1st).

While they have a received a letter of waiver from SAPETRO on the Apr 10th funding in place requirement of the agreement, they still are required to have $15M funding in place prior to closing the agreement. Otherwise the company gives up 2% of the concession for ever $1M shortfall of that amount.

I really see a need for the funding gap to be closed sooner than later. There are too many things stacking up against this need. Such as the remainder of drilling equipment and support contracts, retaining the drillship, and farmout closure. They can only continue to come up with extensions, waivers, and creative dealings for so long here. It would also be beneficial for shareholder to know what they they own (or are purchasing) as far as percentage of concession and dilution.

Still hanging in there!

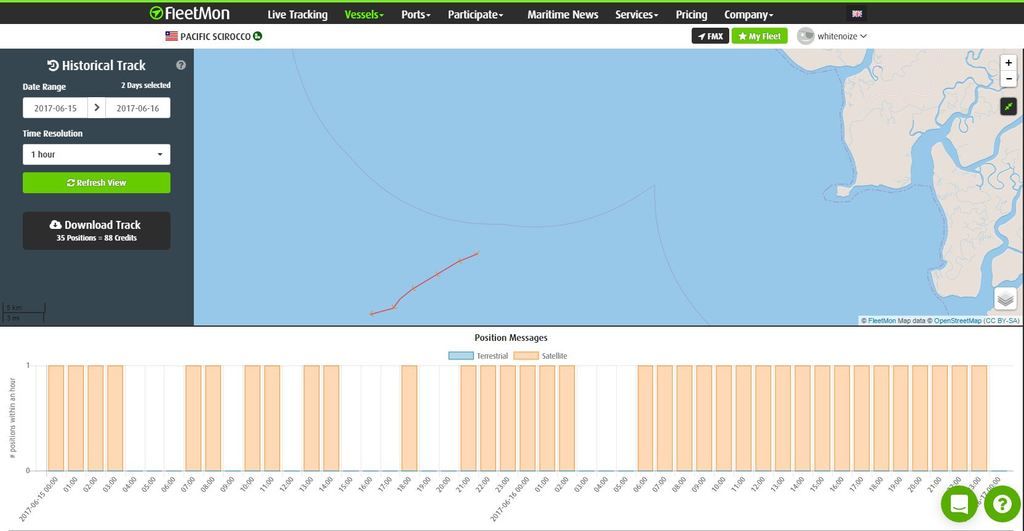

Of course, I can only get delayed SAT data. That was thru 00:00 UTC on 05-19. I just posted it to confirm the Marine Traffic data that the ship was indeed en route and on sched.

Just to confirm Scirocco position from FleetMon AIS Sat.