News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Q&A about the Fed's 'Operation Twist'

NEW YORK (WTW) — Q. What did the Federal Reserve say it would do?

A. The Fed on Wednesday announced a new effort to drive down long-term interest rates. The plan is to sell $400 billion in Treasurys coming due in the next few years and use the cash to buy Treasurys due between six to 30 years from now. The move is designed to nudge down long-term interest rates, already at record lows, and make it even cheaper for corporations and consumers to borrow.

Fed-watchers had expected the move and had a name ready: "Operation Twist." It's a nod to economic history and Chubby Checker. In 1961, the Kennedy administration cut long-term rates while leaving short-term rates alone. They dubbed the move Operation Twist, after the dance craze.

Q. How did markets react?

A. Stock indexes took a dive. The Standard & Poor's 500 index dropped 2.9 percent, its biggest loss since Aug. 18. The Dow Jones industrial average fell 2.5 percent. Commodities from crude oil to gold and copper dropped, usually a sign traders are betting on a weaker economy.

But the Fed couldn't have asked for a better response from the bond market. Long-term interest rates hit modern-era lows. The yield on the 10-year Treasury note, a benchmark for mortgages and corporate loans, sank to 1.85 percent. The 30-year Treasury dropped to 2.99 percent.

Q. Do investors think the Fed's move will help the economy?

A. Investors and market economists seem split between those who think Operation Twist will give economic growth a slight lift and those who think it will do next to nothing.

"I don't think it's going to help," said Michael Sansoterra, portfolio manager at Silvant Capital Management. "The issue is we need to spur jobs," he said. And encouraging corporations to hire workers is out of the Fed's hands.

What the country needs, many economists say, is government spending. The Fed has already tried two rounds of bond-buying. Each effort raised hopes that Fed would stimulate economic growth. Stock markets jumped in anticipation. Starting last year, the Fed bought $600 billion in Treasurys and helped launch a rally that sent stocks up 28 percent in eight months. But the economy grew a mere 0.7 percent the first half of the year.

The Fed is "running out of bullets," said Lawrence Creatura, a portfolio manager with Federated Investors. "And it's not because they haven't done a good job. But monetary policy only takes you so far. The true solutions no longer lie with the Fed. They lie with Washington."

Q. What's likely to happen now?

A. Investors don't expect much to change, because everybody saw the Fed's move coming. Economists estimated "Operation Twist" would knock roughly 0.2 percentage points off long-term interest rates. But much of that has already been priced into stocks, says Guy LeBas, fixed income strategist at Janney Montgomery Scott.

The Fed's actions may have even less of an impact on other markets, says David Kelly, chief market strategist at J.P. Morgan Funds.

Q. So investors don't think Operation Twist will do much good. Do they have any better ideas?

A. Kelly said the Fed should threaten to raise rates instead of promising to keep short-term rates near zero until the middle of 2013. Why? It would be an incentive to borrow and spend, he says. People looking to buy a house may rush to lock in current record low mortgage rates before they start rising. "Right now they have zero incentive," Kelly said.

Higher interest rates also drive down bond prices. So the threat of an interest rate hike would likely "kick people out of Treasurys," he said, and coerce them into the stocks or other investments.

"It's like a patient that's been in the sick bay too long," Kelly said. "The Fed really needs to tell the economy to get out of bed and walk around. Unfortunately, they keep giving it more and more doses of morphine."

5/11/2010 IPE SPDR SERIES TRUST BARCL CAP DIVIDEND OF IPE @ .07607

4/12/2010 IPE SPDR SERIES TRUST BARCL CAP DIVIDEND OF IPE @ .19376

2/9/2010 IPE SPDR SERIES TRUST BARCL CAP DIVIDEND OF IPE @ .09599

1/7/2010 IPE SPDR SERIES TRUST BARCL CAP DIVIDEND OF IPE @ .10948

12/9/2009 IPE SPDR SERIES TRUST BARCL CAP DIVIDEND IPE @ .09535

11/10/2009 IPE SPDR SERIES TRUST BARCL CAP DIVIDEND OF IPE @ .16637

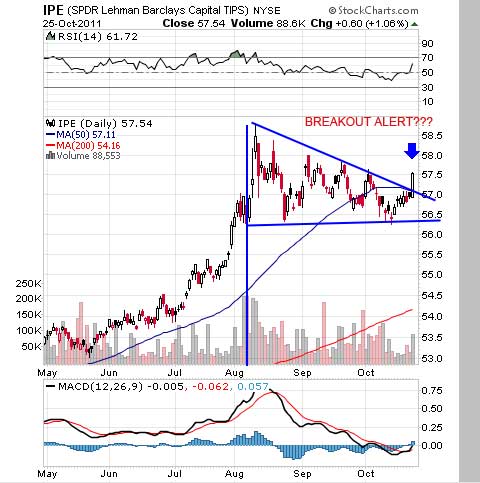

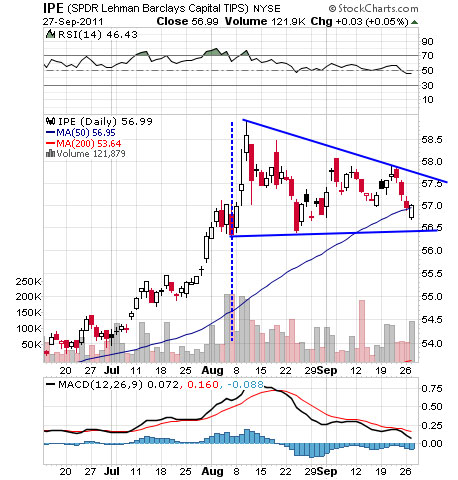

maybe i'm wrong

|

Followers

|

1

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

22

|

|

Created

|

12/28/09

|

Type

|

Free

|

| Moderators | |||

The SPDR® Barclays Capital TIPS ETF seeks to provide investment results that, before fees and expenses, correspond generally to the price and yield performance the Barclays U.S. Government Inflation-linked Bond Index (ticker: BCIT1T). Our approach is designed to provide portfolios with low portfolio turnover, accurate tracking, and lower costs.

Looking to safeguard your portfolio from the potential erosion of purchasing power? TIPS, or Treasury Inflation Protected Securities, were designed to do just that. During inflationary periods, TIPS help protect a portfolio from the declining purchasing power of the US dollar. Introduced by the US federal government in 1997, TIPS are an important addition to the vast array of government debt instruments available today. Backed by the US government, TIPS provide investors with a means to hedge against inflation.

Consumer Price Index chart

Treasury Inflation-Protected Securities, or TIPS, provide protection against inflation. The principal of a TIPS increases with inflation and decreases with deflation, as measured by the Consumer Price Index. When a TIPS matures, you are paid the adjusted principal or original principal, whichever is greater.

TIPS pay interest twice a year, at a fixed rate. The rate is applied to the adjusted principal; so, like the principal, interest payments rise with inflation and fall with deflation.

You can buy TIPS from us in TreasuryDirect and Legacy Treasury Direct through non-competitive bidding.

Treasury Inflation-Protected Securities (TIPS)

The U.S. Treasury has been issuing Treasury Inflation-Protected Securities (TIPS) since 1997. TIPS provide investors with an investment option that protects against the effects of inflation. Like all marketable US Treasury securities, TIPS are backed by the full faith and credit of the US Government. TIPS are available to individual and institutional investors alike.

Interest payments on TIPS are made semi-annually and are linked to the Consumer Price Index for Urban Consumers (CPI-U). The underlying value of the principal grows at the same rate that prices (as measured by CPI-U) rise. When the principal grows, interest payments grow also since interest payments are a fixed percentage of principal. At maturity, if inflation has occurred and increased the value of the underlying security, Treasury pays the owner the higher inflation-adjusted principal. If, however, deflation has occurred and decreased the value of the underlying security, the investor receives the original face value of the security.

Earnings from TIPS are exempt from state and local income taxes just as other US Treasury notes and bonds. TIPS owners pay federal income tax on interest payments in the year they are received and on growth in principal in the year that it occurs.

Treasury offers TIPS in terms of 5, 10, and 30 years. US Treasury securities are available directly from us as well as from banks and brokers.

TIPS In Depth How TIPS Are Tied to Inflation

Treasury Inflation-Protected Securities (TIPS) are marketable securities whose principal is adjusted by changes in the Consumer Price Index. With inflation (a rise in the index), the principal increases. With a deflation (a drop in the index), the principal decreases.

The relationship between TIPS and the Consumer Price Index affects both the sum you are paid when your TIPS matures and the amount of interest that a TIPS pays you every six months. TIPS pay interest at a fixed rate. Because the rate is applied to the adjusted principal, however, interest payments can vary in amount from one period to the next. If inflation occurs, the interest payment increases. In the event of deflation, the interest payment decreases.

At the maturity of a TIPS, you receive the adjusted principal or the original principal, whichever is greater. This provision protects you against deflation.

Treasury provides TIPS Inflation Index Ratios to allow you to easily calculate the change to principal resulting from changes in the Consumer Price Index. To learn more about determining how inflation adjustments affect your security, please see TIPS: Rates and Terms.

Methods of Buying TIPS

TIPS are sold in TreasuryDirect and Legacy Treasury Direct, and through banks, brokers, and dealers. NOTE: One maturity of TIPS, the 30-year TIPS, isn't offered in Legacy Treasury Direct.Effective April 2009, TreasuryDirect permits accounts for both individuals and various types of entities including trusts, estates, corporations, partnerships, etc. See Learn More about Entity Accounts for full information on the new registration types. The price of a TIPS can be less than, equal to, or greater than the face value. For a full discussion of the price of a TIPS, see TIPS: Rates and Terms.

You can bid for TIPS in either of two ways:

1) With a noncompetitive bid, you agree to accept the yield determined at auction. With this bid, you are guaranteed to receive the TIPS you want, and in the full amount you want.

2) With a competitive bid, you specify the yield you are willing to accept. Your bid may be: 1) accepted in the full amount you want if your bid is less than the yield determined at auction, 2) accepted in less than the full amount you want if your bid is equal to the high yield, or 3) rejected if the yield you specify is higher than the yield set at auction.

To place a noncompetitive bid, you may use TreasuryDirect, Legacy Treasury Direct, or a bank, broker, or dealer. To place a competitive bid, you must use a bank, broker, or dealer.

Key Facts:

TIPS are issued in terms of 5, 10, and 30 years. The 30-year TIPS isn't offered in Legacy Treasury Direct, but is available in TreasuryDirect.

The interest rate on a TIPS is determined at auction.

TIPS are sold in increments of $100. The minimum purchase is $100.

TIPS are issued in electronic form.

You can hold a TIPS until it matures or sell it in the secondary market before it matures.

In a single auction, an investor can buy up to $5 million in TIPS by non-competitive bidding or up to 35% of the initial offering amount by competitive bidding.

PERF Chart comparing other TIP ETF's

Western Asset/Claymore Infla (WIA)

Western Asset/Claymore US Treasury Inflation Protected Securities Fund 2 (WIW)

iShares Barclays Treasury Inflation Protected Securities Bond Fund (TIP)

American AAdvantage Treasury Inflation Protected Securities Fund (ATPIX)

DWS Global Inflation Plus S (TIPSX)

LINKS

en.wikipedia.org/wiki/United_States_Treasury_security

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |