News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

jyyoo

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

The lawsuit will take many years (read or talk to others about how long such a case like this can take and likelihood of success) but I believe it is being used more as a tool to pressure Solomon to be shareholder friendly. They don't want more common shares in the company. They want Solomon out of the drivers' seat, professionals in the CEO/CFO position and on the board, cash dividends, buybacks, and TRW shares. Nothing wrong with that.

And if the settlement is dilution after being sued for reckless dilution that would be pretty comical.. Not going to happen. Not a fan of the decisions up until this point but I strongly believe Garrett more of less took over influence since last year which has never happened before and the goal is to simply focus on selling fish AKA TRW and stop spending money elsewhere. SIAF has finally managed to stop the bleeding due to stupid decisions and return to growth as a smaller company as proven by this quarter. The market is valuing this as a bankrupt company, which I strongly disagree with. After the last few quarters I'm now convinced it looks like a profitable company with very high upside growth potential if they can close loans. That's my thesis.

Looks like TRW, including the TRW Trade Division is ramping up as planned. SIAF revenue/income is finally increasing significantly. If they continue to do this a few more quarters and get a few loans/contracts SIAF should finally make it's way to a more fair valuation. SIAF's stock price imploded because revenue/earnings imploded, and they diluted at the same time; now we have revenues/earnings increasing and no dilution so price should follow upwards. Quarters like this of increasing revenue/income make it much easier to wait for loan/CA contract catalysts that I still think will eventually come and surprise the market.

"-Revenue in the fourth quarter of 2019 was USD 38.6 M, an increase of 14% from Q2 of 2018, and an increase of 32% compared to Q1 of 2019.

-Gross profit in the second quarter of 2019 was USD 6.9 M, an increase of 28% from Q2 of 2018, and an increase of 38% compared to Q1 of 2019. All business segments booked positive gross profits in Q2 2019, highlighted by a 300% increase to USD 2.4 M at the Cattle Farm business (MEIJI).

-Income from SIAF’s equity investee, Tri-Way Industries totaled USD 3.6 M, a 42% increase over the previous quarter, Q1 2019, and contributed .07 to SIAF’s earnings per share.

-As of August 14, 2019 there were 49,99 M common shares issued and outstanding, unchanged from the previous quarter’s end."

RealUSA, how are you arriving at your dividend yield calculation?

If each preferred share pays out $2.8 every year on August 15th, and it costs 112 common shares to convert to a preferred share, then it would cost (112* $.24 = $26.88) for each preferred share. So each preferred share costs $26.88 and you get paid $2.8 every year on that preferred share so $2.8/$26.88 = 10.4% annual yield.

Are my calculations wrong? Because if not, that makes a significant difference in your argument for the attractiveness of converting, 10.4% vs. 2.5%

Regardless, I do agree they must believe the stock will not be below $1 soon, which likely has to do with financing or the CA contract they've mentioned. Hopefully there's news soon because there won't be much interest in these shares without it. I would also keep in mind even RD has become very bearish on the stock lately which if anything should be a buy signal..When you look at the technicals, we've broken the 200-day moving average so clearly the trend has turned not to mention we will finally have growing earnings and share count reduction this year.

If the dividend is 2.80/112 shares = 2.5% yield.

In the 10-K it says multiple times that by end of September 2019 all collateralized shares will be due for redemption and returned to the company. I believe the specific date is September 23rd. In the latest Q&A Solomon stated, "One might reasonably regard our outstanding share count as reducible by the number of collateralized shares, not if, but when the loans are repaid or refinanced."

What they did a year and a half ago was reduce the line from $20M to $15M so no more collateral shares had to be issued. It has recently been further reduced to $13M. They specifically stated these collateral shares cannot and have not been sold into the market. (Plenty of other shares were being issued through normal dilution for other payables, that's why the stock was tanking, though it has stopped since the beginning of the year).

I'll just copy and paste some basic info from the latest 10-K that has the info:

This includes the Trade Facility consisting of 5,708,312 collateral shares, and Third-Party Loans consisting of 2,662,735 collateral shares, collectively that do not hold voting or dividend rights to be returned to the Company upon repayment. The maturity date on the Third-Party Loans and Trade Facility run through September 2019, but the Company anticipates repayment of a portion or all the loan balances as well as a reduction in the maximum Trade Facility line to occur before that time, as exemplified in the reduction of the Trade Facility line from $20,000,000 to $13,000,000 and the third parties’ loan debt has been reduced from $10,428,034 to $2,103,000 as at December 31st 2018.

Subsequently as of March 31, 2019 there is $3,303,000 in CB Notes remaining outstanding collectively and out of which $2,130,000 is secured by 2,666,735 shares due for redemption and the return of collateralized shares on September 23, 2019.

TPA repaid $5,000,000 in Cash payment on December 19th 2017 to the Trade Facility Provider and agreed to have its facility face-value reduced to $20,000,000 and the net amount employed to $15,000,000. This amended arrangement was agreed to avoid further issuance of shares due to the current share price. As at December 31, 2018 TPA has further reduced the net amount employed to $13 million.

As it was mentioned in the 10-K for the fiscal year ended 2017, the ITP loans (provided through the same third parties) were provided to Tri-way (“Borrower”) with the final agreement entered into on August 5, 2016; the loan proceeds having been incrementally received between July 15, 2016 through September 28, 2016 for a total net principal amount of $10,428,034 at interest free term collateralized by 2.66 million shares (inclusive all top-up shares) matures by 23, September 2019. When the loan principal amount will be fully repaid the collateralized shares will be returned to the Company. As of the date of this report, there is $2,103,000 outstanding in this ITP.

On September 22, 2015, the Company entered into a trade facility agreement with two independent third parties. Pursuant to the agreement, the Company provides collateral in the form of Company's common shares to a PRC based lender (the "Lender") and the Lender agrees to provide a revolving trade facility loan up to $20,000,000 to a PRC based borrower. The arrangement was commenced on February 15, 2016 and will be expired on September 15, 2019.

If you had to guess, what kind of catalysts would you think are up next and how soon would you guess? How confident do you feel Solomon will deliver?

I am very bullish from a technical perspective since a couple weeks ago. It is clear the downtrend is over and we are now in an uptrend. We took out the 100-day MA and 200-day MA recently, feats not seen for years in this stock due to dilution and deterioration in earnings. Now dilution has stopped (exactly like Solomon said) and earnings are improving (with the possibility of serious growth acceleration w/ CA contracts and financing). In a couple months we'll get about 8 million shares of collateral shares back to start reducing the share count ("When not if", according to Solomon).

This stock used to jump 75% in a few days on good news with millions of shares on the ask due to dilution so I am curious how it will trade with long awaited good news and no more dilution/fear selling on the ask.

Dilution + decreasing earnings = lower stock price

Sharecount reduction + increasing earnings = higher stock price

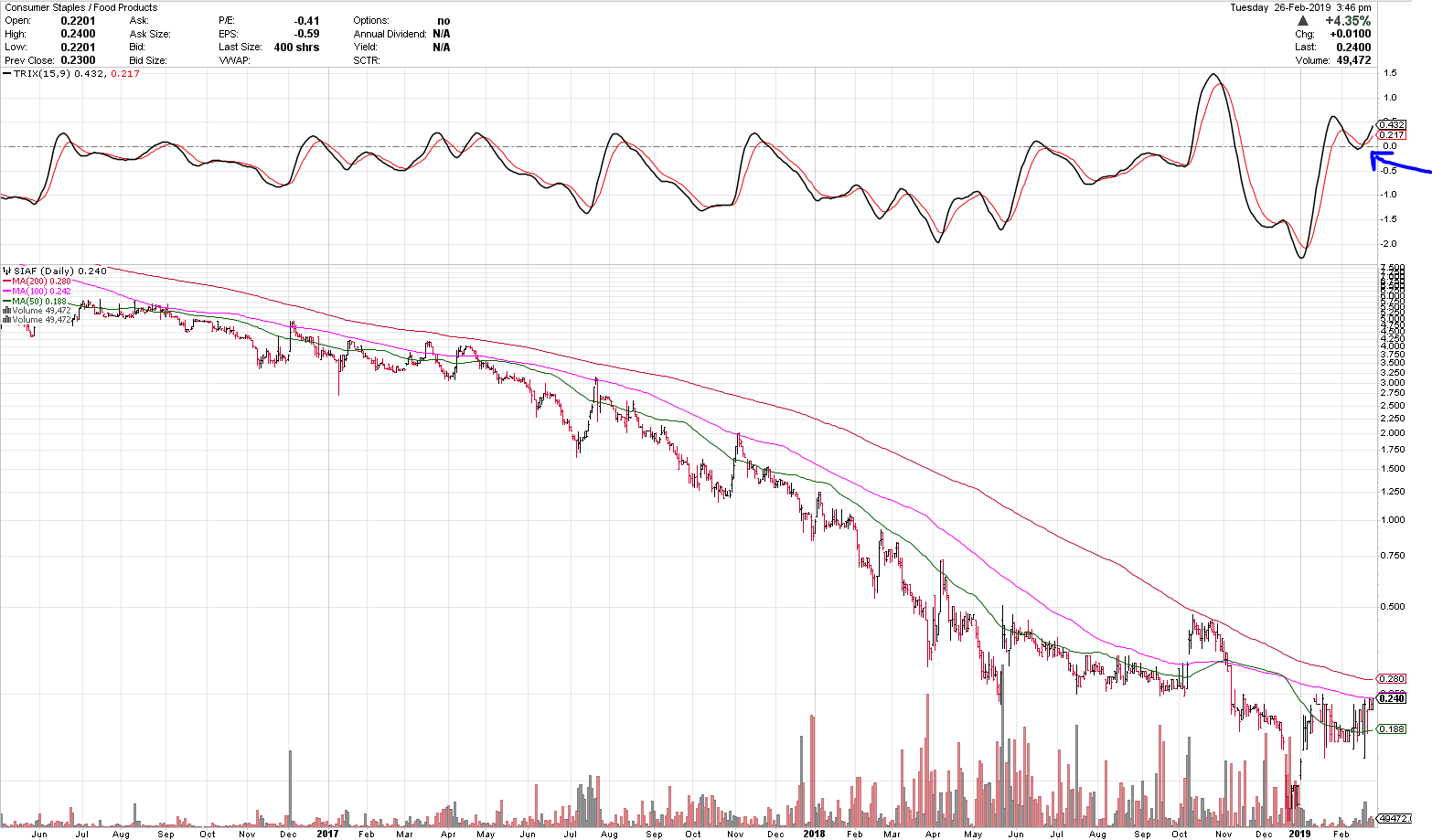

Agree. But pretty bullish action we're continuing to see. SIAF hasn't seen a positive TRIX cross in years (I pointed this out on the chart below). The price should have kept going down after doubling from the beginning of the year, but on Feb 20th you saw strong support come in and shares getting picked up with very decent volume. A week later and we've seen continued early indications that the trend is finally up, rather than down. A price above $.24 and $.28 and it'll be a strongly confirmed trend reversal. All this without even any positive surprises from the company.

I still can't wait to see how SIAF trades after a positive PR from the company since dilution and millions of shares were always previously there selling into rallies.

Personally the reason I even considered looking at SIAF was because of American management. There was the CFO Dan Ritchey before he recently passed away, Tony Ostrowski the Chief Technology Officer (You can talk to others in the industry and ask what their opinion of him is. They talk very highly). Fredrik (not American but reputable), from ECAB who did due diligence on the company for many years before giving the company money. And lastly Garrett D'Alessandro, the CEO of City National Rochdale who has the largest position in the company.

And the Investor Relations, Peter is American as well.

Does SIAF have honest management? I don’t want to own shares in a Chinese OTC if it has shady managers

On Jan 3rd we gapped up and opened at $.16 and closed at $.19. So far we've tested that $.16 range nicely and found good support there. We have a pretty nice bull flag that's starting to move up the past two days. Last time we flagged we couldn't hold that gap up point like we have this time.

It's been a while since we've been able to talk about breaking major moving averages like the 100-day at $.24 but it looks like it's setting up to potentially take it out soon, especially if we get any good news. I know you hate it fundamentally but what do you think technically?

Tony is largely responsible for the deal with Nortus, so yes he is good at producing. Nortus came to Tony because of his reputation within the industry. Because of the special relationship with the Chinese government for funding, Nortus wanted to partner with a Chinese company like SIAF. Tony speaking English was also an advantage.

With dilution finally gone (like the company told us) the sellers are gone as well. This is clearly reflected in the positive share price increase this year, compared to the previous share price implosion we had seen the past few years. People just need an announcement to buy the stock now so any little good news will move the stock price dramatically because it is so illiquid and we have finally gotten rid of the millions of shares that were waiting to be sold into rallies like before. In terms of technical analysis we are only a few cents away from breaking through major moving averages like the 100-day at $.25 and the 200-day at $.29, both of which have been flattening out recently. With the lack of supply, it would only take a few buyers to cut through these levels.

Even if we don't get major financing news announcements like the small loans talked about previously, or the $100M loan or Angola financing, I believe seeing a return back to revenue/earnings growth (which was forecasted this year) will bring in buyers, particularly since we haven't seen such growth in years.

With dilution finally gone SIAF shares are basically call options with no expiration date. Previously, Solomon was unfortunately sucking the premium out of the these "call options" with his dilution.

https://www.undercurrentnews.com/2018/11/23/sino-agro-signs-mou-for-60000t-aquaculture-farm-in-angola/

Looks like the Pacific White Shrimp (Penaeus Vannamei) is having success in their trials since Tony's giving a presentation on it next month. SIAF published on their website the results of one successful trial to 3 kg/m3. Current trial is targeting 6-9 kg/m3 in 50 m3 tanks, which he'll likely talk about at this conference.

SIAF's goal is to prove APRAS in 50 and 150 m3 tanks for the Pacific White Shrimp, scale to commercial production level and then also expand to fish. RD I assume they can do this even without the $100M loan?

Sunday, March 10, 2019

Biological and Economic Performance of (Penaeus vannamei) in Commercial RAS in China (Anthony Ostrowski)

The Shrimp Sessions at Aquaculture 2019

World Aquaculture Society Triennial Meeting

March 7 to 11, 2019

New Orleans, Louisiana, USA

http://www.shrimpnews.com/FreeReportsFolder/SpecialReports/ShrimpSessionsAtAqua2019WAS.html

It seems very clear that Garrett has finally gotten through to Solomon in getting him to understand how to properly manage SIAF going forward with a more "Western" mentality of valuing cashflow more importantly than just simply building assets. Below is the quote from the last Q&A:

"We will also raise the relative priority of generating cash flow, having emphasized — perhaps overemphasized — net asset accumulation in the past."

This is a complete reversal in thinking that we've seen from Solomon and no doubt comes from Garrett and other advisors around him that have finally changed his mind (I'm sure the imploded share price has helped change his mind as well).

I've followed the company for many years now and have never seen the word cash flow used or stressed so much before until now. I'm sure old-timers would agree as well. Below I made a little highlight of the quotes talking about "cash flow", which Solomon would care less about in the previous years. It was always, who cares about cash flow when we can just build equity? Finally things have changed it seems, and I believe the market will appreciate this change. It looks like it's already starting to.

"This reinforces our commitment to prioritize positive cash flow in 2019 to meet business needs."

"Because of efforts to date and by concentrating on positive cash flow, the Company does not foresee a need to raise its authorized share capital."

" During the third quarter we continued restructured and restructuring operations by reducing capital expenditures, adding some non-operational income, and embarking on new cash flow positive initiatives."

" Restructured businesses have already reduced new capital development; businesses are beginning to perform more efficiently; the Company has embarked on several initiatives that have begun to generate incremental positive cash flow."

" With all SIAF owned business segments stabilized or on a modest revenue growth trend, the Company is dedicated to managing toward positive cash flow"

"Tri-way began its own trading business during Q4, and will generate incremental cash flow during 2019."

"Tri-way’s new trading platform will create incremental positive cash flow in 2019, compared to zero through November of 2018."

"I fully expect a return to year over year positive revenue comparisons in 2019."

"The Company believes that for most segments, revenue and profit margins will improve organically, assuming underlying market conditions remain stable."

"And as noted earlier, several new projects or complementary businesses have commenced in Q4, with others intended for 2019. As these reach anticipated levels, we expect the total accretive impact to be at least low double-digit percentages."

"With all SIAF owned business segments stabilized or on a modest revenue growth trend, the Company is dedicated to managing toward positive cash flow, concentrating its efforts on improving aquafarm efficiency, increasing aquafarm production, and then raising aquafarm capacities. Tri-way began its own trading business during Q4, and will generate incremental cash flow during 2019."

The quotes above are what the company last stated in their Q&A. I'm not expecting much from SJAP but it would be nice if you're correct in that the beef market prices have bounced back. Regardless, it seems pretty clear revenue/income/cashflow should be improving in 2019; something we haven't seen in years. The company never gave any form of guidance like they did in this past Q&A, mostly because they didn't want to talk about decreasing revenues etc. They always talked about hopeful stabilization, but now that things have actually stabilized and we're returning to revenue growth they're fine giving some guidance. Base case, SIAF will make more money than it did last year, regardless of financing which will of course be enormous drivers if/when accomplished.

Sounds like there has been some recovery in the beef market for SJAP?

RD what kind of margins would you expect to see for Tri-way's new trading business? They said they target low 9 figures for 2019 (let's assume the lowest at $100M). How would that ultimately translate into income for Tri-way?

Yes, the trading business has begun. Remember that this business is Tri-way’s, separate and apart from SIAF’s trading division. So they will run it. Sales started in November and December totaling in the low millions. Financing has been arranged. Tri-way intends to ramp the business starting in the first quarter of 2019. It’s difficult to project 2019 revenue, but Tri-way’s ambitions are low nine figures in the first full fiscal year. As already stated, this will provide incremental income to Tri-way, comparing to zero in the first ten months of 2018, and will flow through to SIAF on SIAF’s income statement proportionate to its equity interest.

Why don't you just read through the latest Q&A we received from the company? They specifically addressed the Memorandum of Understanding they signed with Nortus:

"At present our MOU covers consulting, project specification, and costing resulting in a report to be used in essence as an application for project funding. SIAF will announce progress after material events or major milestones are reached."

They stated their new policy, which I 100% agree with about not giving updates to impatient shareholders because it ultimately leads to disappointment. Instead they will only announce when things are done/signed etc.

"Again, going forward we will report material events or accomplishing milestones after the fact rather than good faith prospective plans, regardless of confidence."

I don't know how much consulting revenue is being generated from the MOU alone but obviously once Nortus gets financing, that would be an enormous revenue boost to CA and ultimately SIAF. And I have much more confidence in a company like Nortus getting financing since they're familiar with this process already.

I was talking more in generalities, the silence is deafening!

Redbull, we've been over this countless times. TRW (independent, private Hong Kong company) is applying for the loans not SIAF and has a much better and simpler balance sheet/business than SIAF, and therefore much greater chance of getting large financing. We are also hearing about more involvement from C. S. Ravindran as he shows up as managing director on Tri-way's website. It says he has 36 year in financing/fund raising and it is likely no coincidence that the syndicate banks for the $100M loan are from Indian banks, and this guy has years of fund raising expertise in India. He is no doubt very involved in the talks.

Also dilution has stopped finally as they forecasted. Every day this year has been very clear how big a part dilution played in the destruction of share price in the past. If SIAF can manage to PR something positive for once it will be very interesting to see how high the price goes now that there aren't millions of shares on the ask.

As for the ECAB loan, it seems their notice was a warning to not do the cash dividend since it was issued to the company right before the cash dividend announcement was expected to be (Q&A). In the Q&A and reasoning for not doing the cash dividend SIAF even mentioned it was "in consideration of creditor priorities". "The Board will reevaluate the dividend after positive cash flow and cash balances demonstrate a greater than current cushion, and more progress is made paying down or refinancing existing credit lines or debt."

If you're ECAB you likely would have been just as pissed with a company paying out a cash dividend instead of paying you back first. It makes sense. Also if you're ECAB and you know SIAF's cash flow is already improving/will be improving throughout the year, it seems like your best chance is to renegotiate to get paid. I believe this is why they decided not to accelerate payments.

I believe they’re past getting normal loans at least until the have paid back the existing loans. I would reach out to every VC’s out there in order to handle ECABs loan and stop the dilution.

Yep, kinda like the couple dozen other non events that brought the stock from 17 bucks to 10 cents. A bunch of non events. smile

Wow, crazy speculation on this board as usual...SIAF IHUB never fails to disappoint. For those based in facts, the 8k literally stated:

While ECAB stated in the Notice that it has not elected to accelerate the right to repayment of the entire principal amount, including accrued but unpaid interest on the ECAB Note, it reserves the right to do so.

Prior to receipt of the Notice from ECAB, the Company was attempting to reach a negotiated settlement with ECAB. Notwithstanding receipt of the Notice, the Company hopes to continue to work with ECAB to settle its obligations under the ECAB Note.

I bet ECAB has found a buyer for some of the facilities already and think it’s time to put this clown down before he destroys even more value. And I totally agree.

I wonder where all the money went from all the issued shares over the past year.

Andrewflying, thanks for sharing info like this.

Ironically, had Garrett not revised his conversions, this would not have happend.

Either way, if you have shares, dont sell. It is their intention to take control, but probably it probably wont go that smooth.

When I talked to Solomon in May, he badically said FD is behind all the trouble. He did not mention the name, but I think he cleatly referred to ECAB. THEN I asked about what if convertible loan owners want to damage and take control of the company, he said Garrett wont. Then be said, I will not let them succeed. He was really mad when he talked about that person.

We already knew SIAF wasn't making payments to ECAB and were in renegotiation talks because they told us in the SEC filings, so this wasn't really news. With the notice of default, it looks like this will either go to court because ECAB or Fredrik got fed up or they're using this as a negotiation tactic since we know they were in the middle of renegotiations. I suspect the later since the 8k stated "While ECAB has not elected to accelerate the right to repayment of the entire principal amount, including accrued but unpaid interest on the ECAB Note, it reserves the right to do so."

If SIAF does end up being forced to pay up, maybe Tri-way will finally repay back all that debt RD keeps talking about. Best case is they are able to continue negotiating.

It could be an orchestrated move by ECAB and Solomon altogether to wipe out ordinary shareholders.

Why? Sounds like you have too high expectations here.

Snow I agree with RD's answer that it looks different compared to the previous debt settlement, and this is likely contractual. However, I do think they'll delay the cash dividend (they did the same thing with the F-shares because they had never done something like that before, similar to how they screwed up the TRW distribution, but it's important to remember they eventually did pay it). In this case, they know the procedures very well on how to get FINRA approval for a cash dividend because they'd done it 3 times before. The fact that the record and pay date haven't been announced already, while other companies who have pay dates on Dec. 31st have already announced it, likely means the pay date will be some time in Q1, probably Jan or Feb? Most people won't really care when the pay date actually is because once the record date is announced the share price will go up.

Aside from those 210,000 shares, we have seen diluton/dumpage stop which is very positive for both the cash dividend (even though I think it'll come in Q1) and the company in general. This is also what they forecasted; dilution stopping due to increased income/cashflow. Improved cash flow is something we haven't seen in quite a long time, so it finally looks like we've started to turn around, even if it's slower than shareholders want/were told.

I don't know how you plan to try to trade this short term because the second they come out with dates it'll skyrocket (I assume you agree?), even if the payout date is much later than the record date say Feb. 31st for payout and record date Jan 15. Which is what I think they should do if they can't deliver this year which is looking unlikely at this point.

Medifast (MED) for example just announced a cash dividend with record date of Dec. 21st and pay date not until Feb 7th. Scholastic just announced one w/ payout date on Mar 15th and record date Jan 31st. As someone without a full position do you just pray it goes to $.10 and load up or what? Because I really don't think things will set up technically before an announcement. I think it'll just gap up one day when they PR the dates.

I believe people will invest in SIAF not for the dividend yield but because it will signify 1) they finally care about shareholders 2) their cash flow is improving 3) their cash flow is real.

After they're convinced the earnings are actually real due to the cash dividend they'll invest for the earnings growth, whether it's due to beef prices bouncing back, MegaFarm expansion after closing financing, success with the new TRW trade division, Nortus getting financing for Angola project, etc. The cash dividend will simply create credibility to start valuing the stock like a normal, even OTC stock. A 5 P/E will do and get us way past $1. And as I mentioned before, the dilution is what was responsible for the real waterfall in the share price.

The important part is knowing that dilution is permanently gone. Having a semi-annual cash dividend in place will be a nice reminder to shareholders that the company has more than enough money to not dilute. I think Solomon is more than incentivized to announce the cash dividend dates ASAP, and the fact that he hasn't probably means we won't get it by year end (the market seems to be pricing this in as well). I've seen some companies with payouts for Dec. 31st and record dates as late as Dec. 22nd, but they already made the announcement of these dates last week whereas SIAF hasn't.

Different time horizon's but I mostly agree with what you've said Redbull. I think if the company were going to pay a cash dividend by year end (meaning have the pay date at least by December 31st) they would have already announced the record date by now. I guess it's a possibility they announce it with the Q&A's on Friday but I don't think they'd hold on to good news like that. I do think we'll eventually get the cash dividend (meaning 50% yield at these prices), possibly in January if they have to delay it. I'm hoping if there's a delay, they can at least announce the record date for let's say Dec. 31st and pay it January 31st. The beautiful thing with the cash dividend, which is why I've always advocated for it, is that no matter how low the price goes, a cash dividend will immediately put a floor so things could move quickly to $1.00 once announced/paid.

Stopped dilution which we've been seeing for a few months now will also help any price spikes as well that was previously met by a wall of shares in the past. What you were seeing technically in the $.40's after the TRW announcement was the dilutive shares hitting the market, keeping us from moving much higher. We shouldn't have that during future rallies.

250K shares were recently issued, which they should clarify the reason for through Merkur since they got in trouble for not reporting it immediately in the past. Aside from that, dilution has stopped the past few months which is positive and in my opinion one of the sole reasons for the complete destruction in share price we've seen.

Another positive is Garrett's influence in the selection of the new CFO. Business wise, cash flow (not just income) should be increasing as well which we haven't seen in years.

Personally I'm not really looking forward to the Q&A because it almost always leads to confusion and more questions from lack of clarity. The question short term is whether any likely bad news from cash dividends/TRW delays is already priced in at this point. If one considers this a venture capital investment, however, the risk/reward is still enormous.

For those that haven't watched I would suggest watching the Elon Musk interview with 60 minutes he just did for insight on how entrepreneurs like Solomon think and run businesses. Many of SIAF's problems due to Solomon are because of his entrepreneurial attitude towards this business. If you read last Q-report it's clear he's finally focused on running a more lean, smaller, and cash flow focused business going forward.

https://www.cbsnews.com/video/tesla-ceo-elon-musk-the-2018-60-minutes-interview/

The part below talking about people calling him a "liar" for being late and screwing things up sounds very familiar...

Lesley: It’s not a car for the “every-man” which is what you set out to build.

Elon: It’s getting there. We’re not that far from being able to produce that $35,000 car; It’ll be ready in probably 5 or 6 months.

Lesley: Alright here you go, you’ve already set a new deadline, right 5 or 6 months?

Elon: That’s just my guess. It’s not like some promise or so help me God and strike me dead.

Lesley: You are notorious for setting these deadlines for yourself that no one thinks you can meet and you often don’t meet. And I’m just wondering why you do that?

Elon: Well punctuality is not my strong suit. Well why do people who think that if I’ve been late on all the other models that I won’t with this one?

Lesley: Your naysayer say that you lie, that’s the way they interpret it.

Elon: People should not ascribe to malice that which can easily be explained by stupidity. So it’s like, just because I’m dumb at predicting dates does not mean I am untruthful. I never made a mass produced car. How am I supposed to know with precision when it’s going to get done?

True. Well if Dec. 31st is the latest to pay it out, which makes sense after re-reading their wording of "issuing a dividend before year-end", then I would expect the record date to be Dec. 15th and an announcement within the next two weeks, more likely next week. We'll see.

Hey RD, if they pay it out before Christmas you have to swear to start referring to Solomon as Santa Solly from now on. Or Jolly Solly. Take your pick.

No particular reason, just low expectations I guess. I'll be happily surprised if they make an announcement within the next week or two for a December 15th record date and pay it out December 31st. Very much a possibility as well.

The price action has been very interesting recently. Seems like the shorts' games aren't working because they can't front run the dilution/dumping anymore. AKA Solomon isn't helping them anymore.

Why would you expect that when they always said they would pay/issue the dividend in Q4.

The last time SIAF paid a normal cash dividend back in 2012 they declared/announced it on Dec. 6, the record date was set for December 26 and it was paid out to shareholders January 15th.

As I mentioned before, in 2011 they didn't declare the dividend until 2 trading days before the record date. They declared/announced it Oct. 26th and record date was Oct. 31st. It was then paid out to shareholders November 15th.

I would expect the pay date to likely be January 15th, with a record date of Dec. 31st. Who knows when they'll declare/announce it though; hopefully soon. I would have thought they'd have done it by now...Hopefully they don't wait until 2 days before the record date to announce like they did in 2011.

Again, every day there is no longer any dilution the stronger the probability of a cash dividend being paid out (my opinion differs from everyone else's who thinks the longer we go with no news the higher the probability they won't pay it), which the market has put the odds of at basically 0% given the 75% implied yield since holding it for a little over a year would get you 3 cash dividend payments of $.05

Red, ask some of the Jordanfund guys because I heard Nisse was offered another position on a board for another company, but was not allowed to be on the board of a U.S. company simultaneously. Regardless of that excuse, I obviously believe he was also sick of angry shareholder emails and ultimately Solomon, which probably made it an easy decision.

I still believe it comes down to the cash dividend, which is being made possible due to the bottoming and slight turn around in earnings. They've finally gotten cap-ex under control and starting leasing assets etc. CA was actually making better money again last quarter as well. The Tri-way trade division has apparently started as well; Hopefully we can get an update on the CC. Obviously, any loans will increase growth prospects as well.

And like I said before, every day they continue to remain halted on dilution like we've been seeing for over a month now, the greater the chances become on following through on the cash dividend, since the dilution ending coincides with the timing of their guidance they provided. Once the cash dividends are being paid, focus will finally be brought to earnings growth and valuation etc. as opposed to "is this a fraud or not". Once we get to that point, even low valuations for a slow growth company will be many multiples higher than current prices. Simple as that.

I'll post again since people may have missed it and kind of answers your question:

Below are dates for the cash dividends SIAF has announced and paid in the past years.

For 2010:

Jul 15: Announced

Aug 31: Record Date

Oct 15: Paid cash dividend

For 2011:

Oct 26: Announced

Oct 31: Record Date

Nov 15: Paid cash dividend

For 2012:

Dec 6: Announced

Dec 26: Record Date

Jan 15: Paid cash dividend

For 2011, the cash dividend was announced and paid in less than a month (we have 1.5 months until end of year). And the record date (Oct 31) was announced Oct 26, which was only 1 day before the ex-date (Oct 27) since things were T+3 back then. So you only had the day after the announcement to buy the stock and qualify for the cash dividend. I expect them to give shareholders and outside investors more time to buy shares to qualify but I'm just pointing out they have done this in the past. I'm sure you could imagine what would happen price wise due to illiquidity if they only gave us 1 day to qualify for the record date. I wouldn't be surprised if they announce something very shortly, with the record date being Dec 1st and payout being Dec 31st for example.

Completely agree. And 1) dilution has stopped 2) dilution stopping is directly tied into the probability of following through on the cash dividend and every day we continue to see dilution stopped, the odds of the cash dividend go up.

Personally I don't think we'll see the cash dividend announcement within the quarterly report (hopefully I'm surprised) but I think we'll see it in a separate PR shortly after.

The company deserves plenty of criticism and receives it on a daily basis, but no one is talking about the fact that dilution has stopped like they said it would. Because of this I am probably one of the few who actually believes they will set dates and pay the cash dividend like they said they would (very shortly). Obviously, people disagree with me because of the current implied yield of 50% but if they announce dates and pay the cash dividend I think we can all agree we won't be trading at $.20 cents...

All that matters at the moment:

- Dilution has to stop

- Cash dividends

Like I said, credibility for any TRW distribution solution they give us will have to be rebuilt as they follow through on things like the cash dividend being announced and paid, and dilution continuing to remain halted.

If they announce and pay the cash dividend, people will believe whatever TRW distribution solution they propose much more. At this point, it's understandable that no one believes them. That doesn't mean things won't change or sentiment won't be different in the future.

Well, like I said before, I would expect the Q-report to clarify the TRW distribution delay. It sounds like you and others who sold think it won't be distributed at all and got "tricked" but I view it as a delay (due to complexity and incompetence) and if the Q-report explains the details of the delay with a quick doable fix that should be positive. Again, whether anyone believes they are competent enough to follow through on a quick fix or that it would even be quick is an entirely different story. But the cash dividend, if announced and paid will definitely help restore credibility for their Tri-way F-up no doubt. And every day we go without any dilution is positive as well, not just for the share price but since it adds to credibility, since that was part of their plan before the cash dividend and they seem to be following through on it.

Yeah, we will see. I think the frustration is enough for people to sell shares when they got tricked to buy 10+ million shares and didn't even get the TRW dividend.

For anyone interested, here's the dates/info for SIAF's past cash dividends.

RD, perhaps you can find the exact FINRA rules but I believe there is a limit on how far out a company can announce the record date. For example, if the planned record date is on the last possible day for the year Dec. 31st, then the company can't announce the record date more than 45 days prior (this is what I'm unsure about), making the earliest announcement by the company for the record dates to be on Nov. 15th. Obviously, they could set the record date earlier, or wait longer for the announcement (although I would assume they'd PR the announcement as soon as they can given the angry shareholders).

In 2010, SIAF announced the cash dividend record date 45 days prior to record date.

July 15th-Record date announcement

August 31st-Record date

October 15th-Cash dividend paid to shareholders

In 2011, SIAF announced the cash dividend record date only 5 days before the record date.

October 26th-Record date announcement

October 31st-Record date

November 15th-Cash dividend paid to shareholders

In 2012, SIAF announced the cash dividend record date only 20 days before the record date.

December 6th-Record date announcement

December 26th-Record date

January 15th-Cash dividend paid to shareholders.

Maybe. Q-report in a few days. There was definitely some frustration selling after the Tri-way delay/F-up but I think the Q-report should explain what went wrong/provide the solution. Whether anyone believes how quickly they'll correct the solution is another story.

It's also been roughly 23 days without any dilution/dumping which, correct me if I'm wrong, should be close to a record for the year? This falls in line with what they previously told us about stopping dilution mid-Q4 before the cash dividend announcement. So if ending the dilution is going according to plan, that should be a positive especially in terms of the cash dividend announcement (which at a 50% yield is not being priced in whatsoever).

I spoke with IR today. Sounds like Dan confirmed ex date was when they said (Oct 30) as well. Fact is only shareholders of record on oct 31 receive trw shares stated multiple times by the company. In the U.S. there is no other way to be shareholders of record on Oct 31st without buying shares by at least Oct 29. Believe whatever but I listen to facts. You guys seem like the other guys on the board except you seem to be desperately trying to get people to not sell their shares, I assume because You fear the stock price going down.. To be clear I am still very bullish.

Neither IR nor the company has said squat about the ex date, even though several people have asked them about it

Someone just posted they were selling on Merkur and buying 20% higher on OTC because they were trying to get double the Tri-way dividend based on RD's posts..I'm sure others may be thinking the same thing since he's been relentlessly trying to post about it. All facts say otherwise. That's why I posted.

As I said before, it's entirely possible for these "guys with big pockets" you just mentioned, to be U.S. investors who just can't buy at Merkur.

The company stated ex-date was Oct. 30, 2018. Peter and Dan said the ex-date is Oct. 30, 2018. If you actually read the press release from Tri-way it says:

"Thus, a common shareholder possessing 100 shares of SIAF on October 31, 2018 would be eligible to receive 39 common shares of TRW."

"The 18,300,000 (that is, 18.3% ownership in TRW) shares of TRW will be distributed to those shareholders of record as of October 31, 2018 eligible to receive dividend shares"

Could not be more clear..The cognitive bias on this board is incredible. So please tell me how you can be a shareholder of record on October 31, 2018 here in the U.S. without buying shares at the latest by Oct. 29? (thus making Oct. 30 the ex-date, just like they announced)

Everyone is stupid except you, right!?

Sounds like Peter and Dan think the ex-date was Oct. 30 as well for all shares including OTC. From the Tri-way press release:

"Rather, all TRW shares will be registered / recorded in book-entry form (only) by TRW’s company registrar on November 14, 2018"

FINRA's not even involved. The November 14th date was just saying that's when it'll be recorded book-entry form by Tri-way's company registrar based in Hong Kong.

"The 18,300,000 (that is, 18.3% ownership in TRW) shares of TRW will be distributed to those shareholders of record as of October 31, 2018 eligible to receive dividend shares in two (2) tranches"

How are you considered a shareholder of record as of Oct. 31, 2018? By buying at least two days before on Oct 29 being the latest...If you buy any date later, you will not be considered a shareholder of record on Oct. 31, thus no TRW shares. I don't think they could be more clear.

Based on the link you sent, you are arguing that the ex-date is the first business day following the payable date (which you are saying is Nov 14th). If that were true then you would have 2 ex-dates which is not possible since we have two tranches with two pay-dates. Again, below it says the second tranche goes to those same shareholders of SIAF record as of October 31, 2018, which again is not possible in the U.S. because of T+2 unless you buy the shares at the latest by Oct. 29, thus making the ex-date Oct. 30th which is exactly what they told us..

"Once the 3.29m TRW shares have been returned to SIAF the distribution / pay-date of the second tranche of TRW shares will be announced and processed in book-entry form with the Company registrar for those same shareholders of SIAF record as of October 31, 2018."

Again, not trying to change your mind so please don't comment back.

Wait...did you just say you sold on Merkur and paid 20% more for OTC shares because you think you may get extra Tri-way shares distributed to you? I assume because of what RD has been posting? Even though IR said the ex-date was Tuesday (Oct 30) and the company announced on Tuesday that the ex-date was Tuesday?

Again let me quote directly from the company: "The shares in the Company will trade exclusive of the right to receive Distribution Shares today, 30 October 2018."

Anyone who knows rules in the U.S. understands that to be considered a shareholder of record (record date specifically stated as Oct. 31) you need to own shares two days prior because of T+2, which makes Oct 30 the record date. Then on Oct. 30 they announced that that was the ex-date...Mind blown right now with this board.

The strength on OTC could be coming from U.S. hedge funds (or other U.S. investors) accumulating a position.

RD, in cases where there are different ex-dates on different exchanges it is usually with ADS or ADR stocks like the example you provided with Statoil. If there were two different ex-dates they would need to tell us like Statoil did. On top of that the company specifically told us the Record Date is Oct. 31st which means because of T+2, you would need to own your shares on Monday to be considered a shareholder on record on Oct. 31st and thus qualify for the distribution, making Tuesday the ex-date. Then on Tuesday they told us the ex-date is Tuesday..You are trying very hard to not admit that you might actually be incorrect. Here is a quote from the announcement on Tuesday. Nowhere does it say only shares traded on Oslo ex-right to receive shares in Tri-way, it says "Shares".

Shares trade ex right to receive shares in Tri-Way Industries today.

Reference is made to the announcement made by Sino Agro Food Inc. (“SIAF” or the “Company”) on 8 October 2018 regarding the distribution of shares in Tri-Way Industries (the “Distribution Shares”) to shareholders of record 31 October 2018 (the “Record Date”). The shares in the Company will trade exclusive of the right to receive Distribution Shares today, 30 October 2018.