News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

B RY

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Solving Muln puzzles isn't for everyone, lol!https://investorshub.advfn.com/boards/read_msg.aspx?message_id=174359017

Hi janice! My latest Muln humor contribution was last june. The portion in paréntesis was from Fintel website. The emotional support dog pic was a humoring on the mark statement for anyone considering Muln a good investment. Injecting humor to make a point is my style. It makes ihubub more entertaining. https://investorshub.advfn.com/boards/read_msg.aspx?message_id=174567588

CORRECTION!!!! Oh brother! I was reviewing Lucy Q2 among several other quarterly reports this morning and got my numbers mixed up...obviously! Their Q2 revenues were $308k, not $3 million. Glad I double checked! I wish I double checked it while I was still able to erase it. It still has the promising ability to achieve the $3 million estimate by the end of 2024. But it has a long way to go from $308,000 - $3 million!!! The rimless glasses will be a big help to sales. I simply apologize to all for not double checking the earlier post sooner.

As much as I despise the rs, the $3 million Q2 revenues blew away the $900k projected. The increased institutional interest lately along with growing revenues is the reason why I still keep an eye on Lucy. If they only produce half the $14 million revenue estimate in 2025, I think it will be a good investment for a couple of years timeframe. Full disclosure...I sold before the rs occurred. I'm not as dumb as I look, lol! I didn't think the rs was necessary, but apparently Harrison Gross did. The price was back sliding anyway. The rs didn't do much more damage than already was occurring. Institutional interest growing is a good move for their long term interest. I think I'll wait until closer to Q3 report to jump back in. I think the price will grow slowly, but slow growth is dead money to me. Others may feel different. I don't mind selling for a small percentage loss before the rs. I easily made that back trading stocks shortly after selling. Lucy simply reaffirmed why I prefer to trade instead of holding. Every once in a while a stock like Lucy gives me logic to hold until the red flags appeared. Apple had amazingly strong growth after the first iphone. I am hoping in 2025 Lucy performs even a fraction of what Apple did. Time will tell. Glta as I hope many others sold before the rs and recovered their loss in other plays since then. Those still holding may still make good with Lucy holding long term. I hope they do. I was bullish before the rs was announced. I did a 180°, stayed silent because I had nothing good to say. Now I think once again Lucy will be ok, but only time will tell. Lucy already accomplished it's $3 million revenue estimate for 2024 by Q2. I'm simply watching this closely on the sidelines. Glta!

Personally I'm enjoying and accumulating this price backslide of a company with analyst projected revenues 3x more than the 1st quarter. We all know it's a legitimate company with heavy sales from an expanding product line. The 2nd quarter 10q will quickly make any social media discussion of a reverse split unnecessary in my opinion. It is my understanding that most institutional investors have criteria to uphold in their buying decisions. Letting the numbers speak for themselves is one of them. I believe seeing the actual numbers in the 2nd quarter report in august will allow institutional investors to add Lucy more freely than the current 0.76% owned. Time will tell and glta. Every picture tells a story...

"LUCY Upcoming Qr. Earnings

Announce Date

8/13/2024 (Estimated)

EPS Normalized Estimate

-$0.15

EPS GAAP Estimate

-

Revenue Estimate

$900.00K"

"estimated earnings date is Tuesday, August 13th"

Here is a Lucy ceo interview posted on his twitter account 2 days ago for anyone interested in more indepth company goals. Of the 44 minutes the first half put me to sleep. When I woke up from my old man nap I skipped to halfway to get past the Skyline investor relation and interview introduction speech. I suggest everyone else do the same. We want interesting info, not rhetoric. The upcoming safety glasses line look sharp, but if they do not have an ANSI stamp then they are not OSHA approved for workplace requirements. I went on Lucyd's website and asked about it, but they did not have an answer. It's not a big deal as their non safety wear will be their bigger sellers anyway. There is no doubt in my mind for those who wear stylish prescription glasses it's only logical to wear rimless smart glasses with amazing capabilities. In the 2nd half of the harrison gross interview he discusses some of the drawbacks of the camera feature in competitors glasses. I believe Lucyd was wise in not adopting a camera feature. The extra weight and invasion of privacy in sensitive places are 2 good reasons imo. Time will tell if they use revenues to cover operating costs later this year and grow their stock like Apple did or use dilution methods in years ahead to cover costs and destroy their shareholder base like 99.99% of penny stocks do. I don't mind holding it until one of those 2 paths become more evident. Glta and here is the ceo interview that I find the 2nd half interesting.

Just my opinion, but Lucy has an opportunity to become a large high tech innovator if they follow a proven path. The ball is in their hands and time will tell. Let's see if Lucy hits 39 cents and rebounds like another company with potential did so many years ago. I feel comfortable with the correlation comparison considering they both started with a hot selling high tech product made in china.

"Apple was co-founded by Steve Jobs and Steve Wozniak in 1976 and one year later launched the Apple II computer. The company, officially known at the time as Apple Computers Inc, went public on the Nasdaq stock exchange on 12 December 1980, at a split-adjusted cost of 39 cents per share. Four years later Apple launched the first Macintosh computer.

Apple’s board of directors ousted Jobs from the company in 1985 only for him to return as CEO in 1997. At that time, Apple was on the verge of bankruptcy but Jobs had a turnaround plan, including securing a $150 million investment from Microsoft to support Office products for the Mac.

By October 1997, Apple stock growth history hadn't started yet as shares were trading at 78 cents (split-adjusted) a piece. Savvy investors who recognised Jobs’ vision were in for a treat over the coming decades. Apple’s 1998 launch of the iMac was an important moment for Apple but not as important for Apple stock history."

Manufacturing costs money until sales can sustain operating costs. If institutions come aboard(currently only 0.76%), that would be nice for retail investors. I think most Lucy investors understand this is not currently a good short term stock with their sales going through the roof along with their manufacturing costs to supply customers. I'm banking on their audited financials next march to be impressive. Good luck to all...especially short term investors who are going to need luck to profit imo. I prefer to daytrade for my main income. Lucy's volitility for a few good daytrading days is where it caught my attention. It's business model has my long term attention. Time will tell. I hope this helps and you do well with your investments gititrit.

Found you to buy warrants, didn't he?!

I found 14 total patents granted in 2024. Two in march and 12 in april. They were filed in feb 2023. That tells me their asset value will be reflected in their financials going forward. They are only assets when granted, not filed. Plus any possible infringement lawsuits could not be filed until after the march 2024 patents were granted. I simply am intrigued to what asset value they give the 14 patents in their financials. I'm not trying to push Lucy and am not recommending anyone buy or sell it. I'm newer to Lucy, bought it and am just posting my findings so far. I see some older postings feel like it is a dilution machine. I see their financials clearly show them to be in the red. From what I see 2024 has a good chance to be the breakout year they have been struggling for since inception. I could honestly care less if the price continues down for a short time. It's next year that I'm banking on. The patents values will have an honest reflection in next years audited financials along with the increase in sales. Time will tell and glta.

https://patents.justia.com/assignee/innovative-eyewear-inc

"Mullen Automotive, Inc. (NasdaqCM:MULN) institutional ownership structure shows current positions in the company by institutions and funds, as well as latest changes in position size. Major shareholders can include individual investors, mutual funds, hedge funds, or institutions. The Schedule 13D indicates that the investor holds (or held) more than 5% of the company and intends (or intended) to actively pursue a change in business strategy. Schedule 13G indicates a passive investment of over 5%.

The share price as of June 7, 2024 is 2.86 / share. Previously, on June 8, 2023, the share price was 421.20 / share. This represents a decline of 99.32% over that period."

$421 last year obviously accounted for most recent reverse splits, lol. Wake me up when MULN's decline reaches 99.99999%. This soap opera got too old and became a snoring festival.

Btw...can you imagine being an active student and playing golf, tennis or just working out while researching through chatGPT? I personally like and think the Lucyd rimless glasses will be a big seller to students who care more about grades than drinking, lol. I can care less about next weeks pps. It's next year financials that holds my interest. GLTA!

Interesting article on the direction of AI as the big players invest heavily in it's future. For those that research on the go smart glasses are the preferable tech. Something VERY IMPORTANT to understand and consider. I've read many opinions criticizing Lucyd glasses due to the fact they chose not to incorporate a camera. There are MANY businesses that DO NOT allow employees to take pictures inside the workplace to protect their proprietary technologies. I worked at a business over 20 years ago when flip phones with a camera were coming of age. Even back then the company had it in their company rules posted that taking pictures was absolutely prohibited. So any complaints of smart glasses not having a camera are dismissed by me as naive opinions. Today's phone cameras have amazing capabilities anyway making the point of having glasses with a camera a mute argument. I think this factor bodes well for Lucy's future bottom line imo. Perhaps it helps explain the multiple analysts projecting $14 million revenues in 2025. GLTA and here is the article I find very interesting about the future of AI.

https://www.cnbc.com/2024/06/07/after-chatgpt-and-the-rise-of-chatbots-investors-pour-into-ai-agents.html?__source=iosappshare%7Ccom.apple.UIKit.activity.CopyToPasteboard

Trilla in moneyilla for us old people, lol.

Btw, I got $14 mill from Fintel. Here>>

Great...david's hiring munster's now, lol.

$14 million, not 25. Works as well.

I think this youtube review is interesting. Lucy's glasses(Lucyd) may not beat Bose glasses for music sound quality, but surprisingly beat Bose and the other competition for phone call sound quality as this review test indicates. Personally I enjoy my Bose earbuds when I'm listening to music, but I don't wear them otherwise because I prefer to text and rarely even answer my phone. I wear glasses almost everywhere anyway. I'm willing to bet once I buy a pair of Lucyd prescription glasses I'll be listening to music more through my glasses to allow me to hear someone talking to me and other matters of importance like an airport boarding call. Another factor to consider when shopping for smart glasses is pic below of their latest model. Most of my glasses are rimless and I think they will be a big ticket item for the suppliers involved with Lucy. It will be interesting to see if other big brands decide to partner up with Lucy for their wide variety of styles(80) as well as rimless designs. Let's get serious...it's a very small percentage of people who do not prefer rimless glasses. I can clearly see why the Seeking Alpha Lucy's earnings estimate for 2025 I posted shows $25 million. That should finance manufacturing costs going forward in 2026. But we all know executives can get greedy and buy a corporate jet instead of financing manufacturing costs. Time will tell how Lucy handles their finances. Currently I believe they are financing operations in the best way they can with offerings. I'm ok with that for now as they have an excellent product line of proven products and heavy demand to fill. Personally I think the introduction of rimless glasses is going to send pre-orders through the roof.

Lucy's 2025 revenue forcast on Seeking Alpha is the direction I'm looking for in a small company gaining momentum. I might even hold Lucy past next year. I'll read their annual next year and see. GLTA!

"By connecting to ChatGPT with your voice on Lucyd smart eyewear, you can access a wealth of detailed research on just about any subject, making it one of the most powerful mobile learning systems available,’ said Harrison Gross, Innovative Eyewear’s CEO.

The Lucyd Lyte 2.0 line comprises 15 styles. The app can be downloaded in beta here, with a free trial. Customers can upgrade their eyewear at lucyd.co and receive the app for free."(2023 info, but still revealing)

I'm interested in holding this until next years 10k comes out. There are large companies like apple competing in this market space. Lucy's attachment to brand names will allow their sales to do just fine. Their easy access research capabilities with chatGPT will be used widely by college students, fast paced business workers and many productive on the go professionals. The direct offerings are a good way to access necessary operating capital as manufacturing expenses have been slowing their sales growth from the start. You can't sell a product you can't afford to produce. I think Lucy will do just fine over the next few years. After that we'll see if the competition either overtakes the marketplace, Lucy stays relevant, or someone buys Lucy for their proprietary technologies. Time will tell. Here is a 2023 StartEngine interview I think answers a few questions. Especially about addressing increasing manufacturing costs.

https://www.startengine.com/blog/interview-with-harrison-gross-ceo-co-founder-innovative-eyewear/

I think it would be a fun MULN exercise/game for those that reading filings and wants to participate to post your favorite paragraph in the Schedule 14A posted by MULN today just for educational entertainment value. We're all onto david's antics. I personally find david quite entertaining as he does his job well. As a ceo his main job/priority is to raise capital. He does that quite well and my hat is off to him. I think david and joe would make good golfing buddies if they had reason to have a conversation. I don't believe that is in the cards though. They both do/did well with the companies they involved themselves with. Our jobs as stock traders is learn to spot red flags early and often to minimize losses and increase our gains. Hopefully david finds my antics as entertaining as I find his antics. Now on to my favorite paragraph:

"If, during restricted period, the Company effects a subsequent financing, including the issuance of options and convertible securities, any Common Stock, issued or sold or deemed to have been issued or sold for a consideration per share less than a price equal to the current conversion price of the Notes or exercise price of the Warrants (a “Dilutive Issuance”), then immediately after such issuance, the conversion price or exercise price, as applicable, will be reduced (and in no event increased) to the price per share as determined in accordance with the following formula:"

Hi I-Glow! Another Esousa Holdings share purchase agreement I see. As much as david and Esousa have made off of their business relationship together, I can't help but wonder if the two ceo's alternate going over each others house for thanksgiving every year. Sometimes business and pleasure do mix well. David could put out a really nice thanksgiving dinner with the $6 million from the purchase agreement. 👌

Stop it...you're scaring me. LOL!

Oh no, the price/sky is falling, lol.

Not adding as well. Long term hold imo.

It's important to distinguish charts vs charting. Charts are past performance and do not account for positive material event filings. Therefore not able to accurately predict future performance. If you feel the pr's/events are misleading, then you don't need a charting technical analysis to predict a downtrend coming. Imo charts are only good for posting on social media platforms like ihubub to show newbies in case they don't know where find the chart history. In AGBA's case we are all waiting for both insitutional investor additions and merger finalization. I've seen inst ownership go from .03% to 1.2% this week on finviz website. On fintel inst ownership went from 3 longs last week to 6 long term this week. Slow and steady is fine by me. I've stated before my interest is in their audited year end filings next march. I see no reason to care about the day to day price. If you look at my ihubub post history you'll see AGBA is simply my new soap opera. Binge watching Heartland season 16 is my other favorite soapbox.

Kudo's to those that bought around the $2.10 range. For those that profit monthly/annually, trading stocks is a chess game. It involves learning strategies to win more games than you lose. Luckily my dad taught me to play chess around 7 yrs old. Strategies are a vital part of success in the lives of self made people. I find as many others have that flipping stocks for a consistent income takes the pressure off AGBA being down. I initially jumped in agba @ 4.02 before averaging down. I could sell it for a 50% loss and it wouldn't bother me one bit. It's unnecessary because I enjoy stock trading and have no worries. But I find flipping other stocks instead of spending too much capital averaging down is the wiser strategy. To each his/her own. GLTA!

He's right. It's hilarious...that less than the average volume of 2 mill has some yelling the sky is falling. Rediculous indeed. We're good.

Same bottom as 2 weeks ago. No worries.https://investorshub.advfn.com/boards/read_msg.aspx?message_id=174345096

Citadel jumped in yesterday. 2024-05-15 13F Citadel Advisors Llc. 43,110 shares.

UBS on monday. 2024-05-13 13F UBS Group AG 25,275 shares.

https://fintel.io/so/us/agba

My honest opinion of your news reaction.>>

One pr should correct downturn. No worries.

Pr's increasing price put out by same peeps.

If I don't get my 10% bounce today then I'll hug my pillow and cry, lol. Imo the worse case scenario is I averaged down my holdings. No worries.

I'm holding what I bought 2 weeks ago long term, but I like bounce plays to build my cash further. This is an easy around 10% bounce profit day just like yesterday imo. Time will tell...but I like making money and I'm not too bad at it.

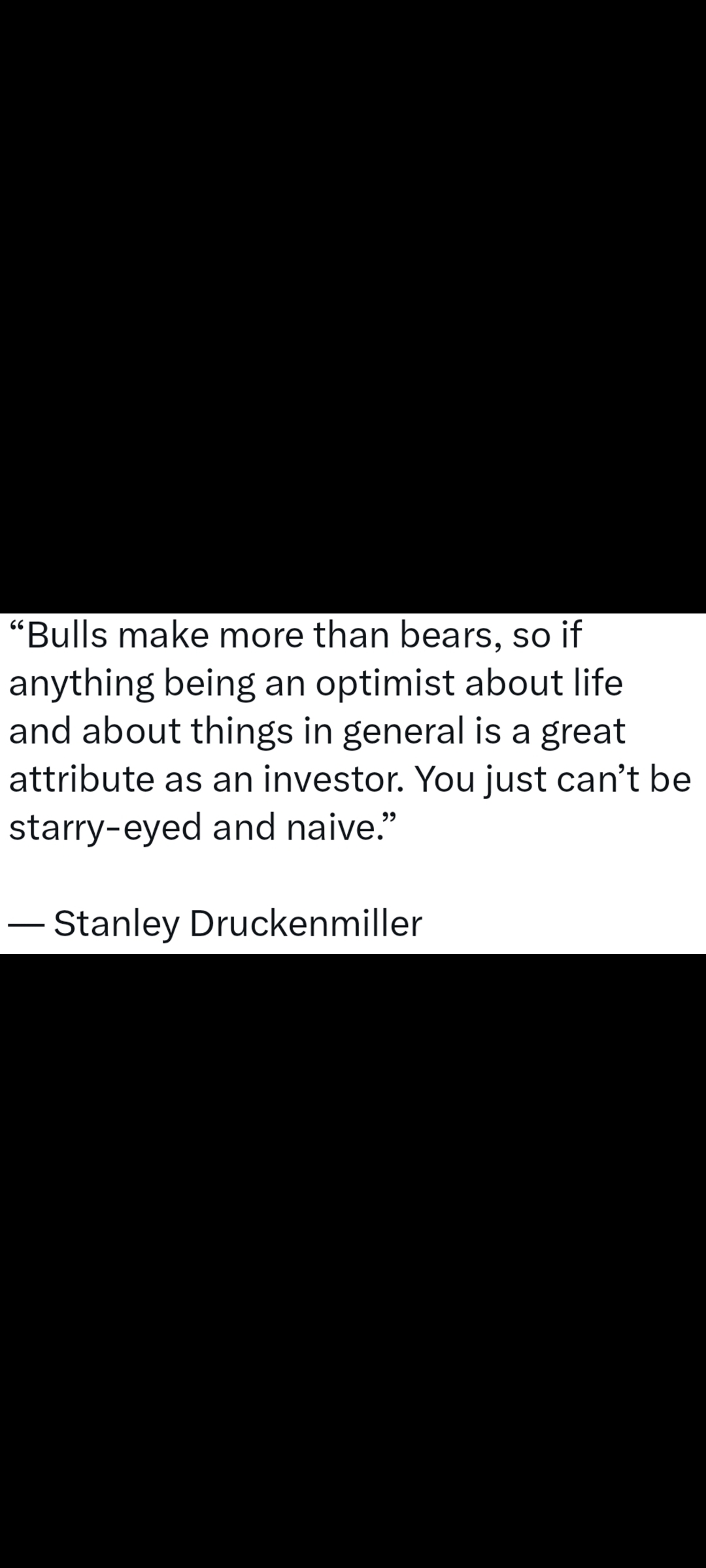

Low vol short sellers aren't very experienced. When they run out of shares the price moves back north. They are trying to take advantage of a slow buying day. They won't accept stanley druckenmiller's great advice.