News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Nothing wrong with being a vulture.

| Followers | 21 |

| Posts | 775 |

| Boards Moderated | 0 |

| Alias Born | 01/27/2012 |

| Twitter Profile: | Temporarily Unavailable |

| Follow on Twitter: | Follow @ Temporarily Unavailable |

dpsimswm

![]()

Nothing wrong with being a vulture.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Nothing wrong with being a vulture.

Up 4.23% premarket

Today is the day the Preferred B and C get finally converted to commons, warrants, and preferred D (cash equivalent). Preferred D is callable at any moment.

A Mortgage Billionaire Bids for the Commanders NFL Franchise, GSE Shareholders and Impac's Restructuring

The NFL's Commanders Franchise may sell for $7 Billion, GSE Shareholders had a setback with a mistrial in DC, Impac's preferred is going to be swapped on November 15th.

https://ridgehaven.substack.com/p/a-mortgage-billionaire-bids-for-the?sd=pf

............

Details on Impac’s November 15th Preferred Clean-up

Judging from market prices for the Impac Preferred B (IMPHP) and Preferred C shares (IMPHO), there is still some confusion about what happens on November 15th.

Impac Mortgage Holdings, Inc. Announces Date of Redemption of Series B Preferred Stock and Series C Preferred Stock

IRVINE, Calif., October 28, 2022--(BUSINESS WIRE)--Impac Mortgage Holdings, Inc. (NYSE American: IMH) (the "Company") today announced it intends to redeem all outstanding shares of the Company’s 9.375% Series B Cumulative Redeemable Preferred Stock, par value $0.01 per share (CUSIP: 45254P300) ("Series B Preferred Stock"), and all outstanding shares of the Company’s 9.125% Series C Cumulative Redeemable Preferred Stock, par value $0.01 per share (CUSIP: 45254P409) (the "Series C Preferred Stock," and together with the Series B Preferred Stock, the "Preferred Stock"). Preferred Stock held through the Depository Trust Company will be redeemed in accordance with the applicable procedures of the Depository Trust Company.

The redemption date will be November 15, 2022 (the "Redemption Date"). Each outstanding share of Series B Preferred Stock will be redeemed for (i) thirty (30) shares of the Company’s 8.25% Series D Cumulative Redeemable Preferred Stock, par value $0.01 per share ("New Preferred Stock"), and (ii) 13.33 shares of the Company’s Common Stock, par value $0.01 per share (the "Common Stock") (collectively, the "Series B Redemption Price"). Each outstanding share of Series C Preferred Stock will be redeemed for (i) one share of New Preferred Stock, (ii) 1.25 shares of Common Stock, and (ii) a 1.5 warrants to purchase the same number of shares of Common Stock at a purchase price of $5.00 per share of Common Stock (collectively, the "Series C Redemption Price," and together with the Series B Redemption Price, the "Redemption Price").

Yesterday's move was +19% and +30% in the regular followed by the after hours session.

People must be realizing that Impac has a large DTA and are about to complete the restructuring on November 15th.

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=170367819

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=170357252

Just bought a little at 30 cents. The DTA is worth $7.50 per share. So, that seems like a good bargain.

Last night's SEC Filing 13G

https://ir.impaccompanies.com/static-files/1198f98c-5d78-4e7b-9fee-4bbd8786b2d7

Camac fund now owns 3,283,147 shares of Common or 9.9% of the total common stock.

Why does this matter?

Camac was a party to the lawsuit with Timm and chose to settle to help preserve value in the company. Amounts above 10% would begin to impair the DTA under IRS rules.

Impac's Largest Asset

The DTA comes with a valuation allowance. Full or partial reversal of this valuation allowance creates instant book value and income recorded as earnings per share. Impac will have about 34.2 million diluted shares after restructuring is complete.

Current share count: 21.5M

+ IMPHO New Shares 1,405k x 1.25 = 1.76M

+ IMPHP New Shares 665k x 13.33 = 8.9M

+ Warrants 1,405k x 1.5 = 2.1M

--------------------------------------

Total 34.2 M diluted shares

$257.3 M/ 34.2M shares =

$7.52 DTA per Share

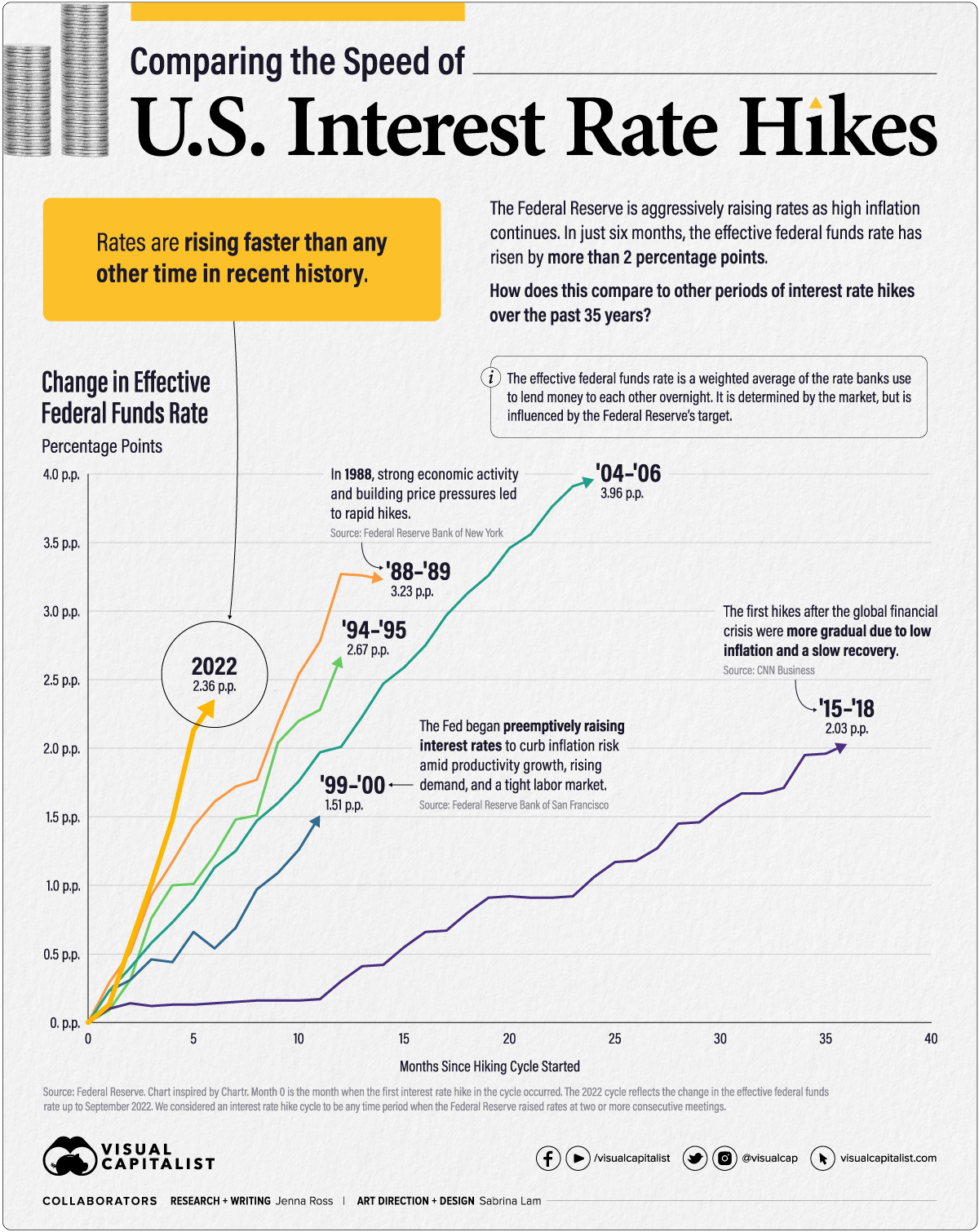

Updated to reflect the current rate hike cycle. The pace of rate hikes has made mortgage market conditions brutal.

Here's some analysis...

Impac's stock is sitting at 25 cents partly because they are going through a restructuring that took years to bring to fruition and is largely misunderstood by investors. Just prior to the restructuring, the company pulled back big time on loan production.

Here's a note on the 2nd Q results from Housing Wire.

Impac’s originations declined from $622.5 million in the second quarter of 2021 to $482 million in the first quarter of 2022 and $128 million in the second quarter of 2022. Gain-on-sale margins decreased from 175 basis points from April to June 2021 to 14 bps in the same period this year.

Meanwhile, non-QM originations fell to $80.2 million in Q2 2022, down from $314.3 million in Q1 2022 and $100.6 million in Q2 2021.

“In the second quarter of 2021, we began to increase our marketing expenditures in an effort to more directly target non-QM production in the retail channel, expand production outside of California and maintain our lead volume as competition increased,” the company said.

Impac added, “As a result of the recent dislocation within the nonQM market on account of the significant increase in interest rates, in the second quarter of 2022, we reduced our marketing spend as we pulled back on our origination volumes to mitigate the aforementioned risks associated with the current environment.”

Impac Mortgage Holdings, Inc. Announces Date of Redemption of Series B Preferred Stock and Series C Preferred Stock

IRVINE, Calif., October 28, 2022--(BUSINESS WIRE)--Impac Mortgage Holdings, Inc. (NYSE American: IMH) (the "Company") today announced it intends to redeem all outstanding shares of the Company’s 9.375% Series B Cumulative Redeemable Preferred Stock, par value $0.01 per share (CUSIP: 45254P300) ("Series B Preferred Stock"), and all outstanding shares of the Company’s 9.125% Series C Cumulative Redeemable Preferred Stock, par value $0.01 per share (CUSIP: 45254P409) (the "Series C Preferred Stock," and together with the Series B Preferred Stock, the "Preferred Stock"). Preferred Stock held through the Depository Trust Company will be redeemed in accordance with the applicable procedures of the Depository Trust Company.

The redemption date will be November 15, 2022 (the "Redemption Date"). Each outstanding share of Series B Preferred Stock will be redeemed for (i) thirty (30) shares of the Company’s 8.25% Series D Cumulative Redeemable Preferred Stock, par value $0.01 per share ("New Preferred Stock"), and (ii) 13.33 shares of the Company’s Common Stock, par value $0.01 per share (the "Common Stock") (collectively, the "Series B Redemption Price"). Each outstanding share of Series C Preferred Stock will be redeemed for (i) one share of New Preferred Stock, (ii) 1.25 shares of Common Stock, and (ii) a 1.5 warrants to purchase the same number of shares of Common Stock at a purchase price of $5.00 per share of Common Stock (collectively, the "Series C Redemption Price," and together with the Series B Redemption Price, the "Redemption Price").

No fractional shares of Common Stock will be issued pursuant to the redemption, and each holder of Preferred Stock entitled to receive a fractional share of Common Stock shall be entitled to receive one share of Common Stock in lieu of the fraction of share of Common Stock. No fractional warrants will be issued pursuant to the redemption, and the Company will round down to the nearest whole number of warrants to be issued to each holder of Series C Preferred Stock otherwise entitled to receive a fractional warrant. The applicable Redemption Price will be paid on the Redemption Date.

https://finance.yahoo.com/news/impac-mortgage-holdings-inc-announces-130000907.html

KBRA: Backlog Of Redeemable Non-QM Securities Growing

David Krechevsky

OCT 21, 2022

KEY TAKEAWAYS

A total of 27 securitizations, with a combined outstanding balance of $3 billion, are redeemable but have not yet been called.

Homeowners thinking about refinancing their mortgages are growing increasingly reluctant, since mortgage rates have more than doubled in the past year.

Why refinance when the rate on your current mortgage is better than the rate you’d get with a refinanced loan?

A similar problem now affects securitizations of non-qualified (Non-QM) mortgages.

In a report issued earlier this month, Kroll Bond Rating Agency LLC (KBRA) noted there is a growing backlog of Non-QM residential mortgage-backed securities (RMBS) that are “callable” or “redeemable,” but have not yet re-entered the market.

According to the report, 27 securitizations, with a combined outstanding balance of just under $3 billion, are redeemable but have not yet been called.

It’s a problem that has grown in the past year, and one that reflects both the volatility of the securities market and the increasingly poor market for securitizing Non-QM loans.

“Notably, only 12 of 31 transactions that became callable based on their earliest optional redemption date were redeemed between August 2021 and September 2022,” the report states, which means 19 were not redeemed. “Additionally, eight more transactions that, though they had not yet reached their earliest optional redemption date, were callable based on their collateral pool factors … were not redeemed.”

https://nationalmortgageprofessional.com/news/kbra-backlog-redeemable-non-qm-securities-growing

Non QM performance wavered in 3Q

By Bonnie Sinnock

October 14, 2022, 5:52 p.m. EDT

Non-qualified mortgages in the securitized market exhibited some mixed performance over the summer, according to a DBRS Morningstar report published Thursday.

The delinquency rate in the third quarter overall was slightly higher than in the second at 3.8% compared to 3.5% in the second.

But whether distress continues to grow in this part of the market remains to be seen.

The latest monthly number for the net impairment rate reported by dv01 this week suggests distress declined in August, falling to 3.9% from 4.1% in July. (Fitch Ratings' parent company has agreed to buy a majority stake in dv01.)

The relative stability in non-QM loan performance over the summer suggests that interest rates continue to be a bigger concern than credit for the time being.

"When you have a rate move that's violent, like the one that we've had this year, you're going to see a situation where the securitizations that are coming to market are still reflecting a lot of loans that have been originated in a very different rate environment," said Vadim Verkhoglyad, vice president and head of research publication at dv01.

A backlog of seasoned non-QM loans has grown as a result of this, Kroll Bond Rating Agency noted in a report published Thursday.

"The current rising rate environment dis-incentivizes issuer redemption by reducing the value of existing loans and increasing the required coupon on newly securitized classes," KBRA said in the report, noting that that's created a "glut" which will eventually re-enter the market.

https://asreport.americanbanker.com/news/non-qm-performance-wavered-in-3q

Some NonQM news....

Jumbo and Non-Agency Loan Changes

HELOCs are a big topic these days, despite the run up in the index rates. HELOCs even have their own home equity lending news: HEL.news. But jumbo, non-conforming, non-Agency, non-QM… although this general product is still the minority of production, loan originators need these products in order to help clients either refinance their existing homes, especially for self-employed borrowers, or purchase a new home.

The question occasionally comes up about why jumbo rates are less than conforming rates. The basic answer is that jumbo loans do not have a 52-basis point (about half a percent) guarantee/guarantor fee attached to each loan. The gfee is firmly in the domain of the FHFA’s Fannie Mae and Freddie Mac.

Life is not easy for non-QM lenders and investors. For example, this month Angel Oak Mortgage Inc., the publicly traded non-QM mortgage REIT, disclosed it had received a two-week extension on a financing facility it has with Barclays Bank. The new termination date is Oct. 14.

The facility was negotiated a few days ago through AOMI subsidiary Peachtree Mortgage. Angel Oak Mortgage parted ways with CEO and President Robert Williams, who helped take the company public in 2021.

Angel Oak Mortgage Solutions’ Non-QM products include delayed financing options. “It is a great way to pay to win a bid and then get the majority of it back within six months of purchase without waiting.”

https://www.mortgagenewsdaily.com/opinion/pipelinepress-10172022

Companies like Impac specialize in NonQM loans and providing alternative methods to finance mortgages. Mortgage credit availability has a long way to go to be back to normal.

With rates surging, this is a business that could be incredibly profitable, given stable rates and better spreads.

Overall, the rumor that the housing market is going to be destroyed by higher rates is definitely hyperbole.

Here's some facts:

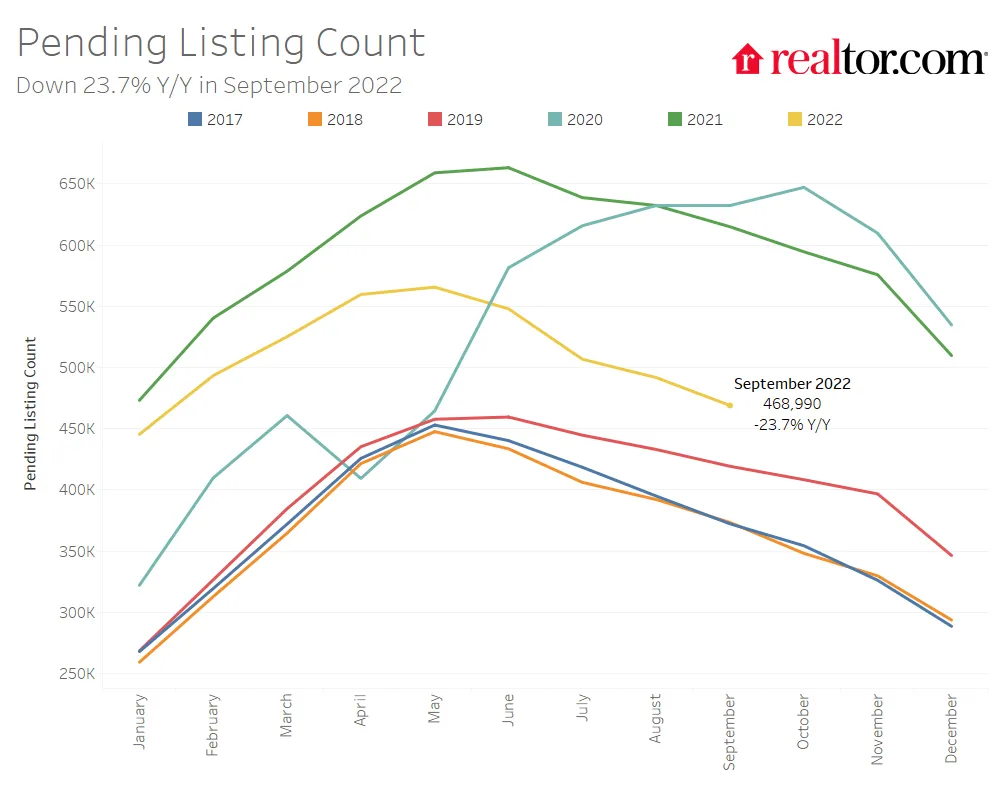

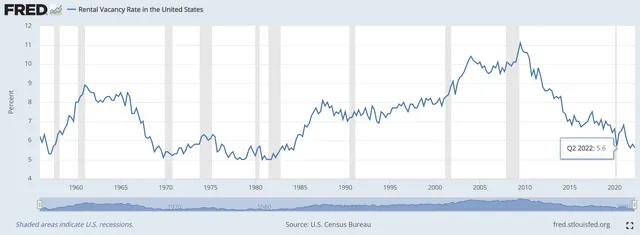

Active home listings are up 26% year over year, but still 42.6% lower than prepandemic.

[img]http://substackcdn.com/image/fetch/w_1456,c_limit,f_webp,q_auto:good,fl_progressive:steep/https%3A%2F%2Fbucketeer-e05bbc84-baa3-437e-9518-adb32be77984.s3.amazonaws.com%2Fpublic%2Fimages%2Faae832d2-59e0-43b6-a68b-3f9b460f810c_1000x800.png

[/img]

Pending home listings are not rebounding.

Add in the unavailable rental housing and you have a complete lack of supply.

Rental vacancies continue to decline.

Bottom line: Mortgages will remain secured by high quality property that doesn't lose value.

Here are a couple of recent pieces on Impac Common stock and the company after restructuring the preferred shares.

Impac Mortgage Positioned For Optimal Growth After Restructuring

https://ridgehaven.substack.com/p/impac-mortgage-positioned-for-optimal

Real Opportunity Brewing in Mortgage Market Stocks

https://ridgehaven.substack.com/p/real-opportunity-brewing-in-mortgage?sd=pf

How a Company Like Impac Mortgage Will Save Housing

https://medium.com/@david.sims321/how-a-company-like-impac-mortgage-will-save-housing-67dda7f76f9c

Good afternoon! I just saw this post. Take a look at last Friday's SEC Filing. The remaining preferred will be converted under the existing terms on 11/15. Then, the balance sheet is nearly fixed.

By the way, you might not have noticed that the Impac common and preferred actually have positive book value. Restructuring the shares won't take an act of Congress or a Supreme Court ruling. We aren't relying on a senile old man who can't remember where his father was born to save us from permanent limbo status.

And the preferred have won a court room ruling for the B shares. The C shares have a strong chance on appeal, due to the realization that C shareholders were not given an opportunity to provide "written consents" or vote at a special meeting. Trial date is set for October on the appeals.

Meanwhile, none of the old management is still in place. And new management has accumulated excess proceeds from sales of MSRs to fund securitization of over $700 million in Non-QM. So, the picture of this stock is set to change.

Can I ask you exactly what it is that I did to harm you?

If I recall, the only person that dumped anything is you. Now, you hang out on message boards trolling people. I notice when your GSE shares are down, you ignore us completely. Now you are doing a victory lap. I guess when the tables reversed, I should come find the hole you are lurking in and troll you.

Are you trying to get intel on this stock?

Rethinking your decision to bail on the group like the turd you are?

How many years has it been and you can't let it go?

Hey Joe,

I don't pay for the subscription, so I can't message you privately.

Do you mind sending me an email at david . sims321 at gmail?

Regarding the lawsuit, I don't know many of the answers. The court filings are available through the clerk of the court.

Regarding IMPHO, the book value per share is $25. That's what it is worth. Have a great week!

JW, the value creation story is now getting derailed by the preferred. That's the reality and I hope the company realizes it. We've done our best to be team players, but there are other forces at work here.

There's a hit piece on it's way through Seeking Alpha. Just got off the phone with a guy trying to build a case against these shares. I recommend you wait a few days if you are looking to buy these. Someone will probably sell some shares to you.

There are there main groups. Camac Fund, Curtis Timm (and his followers), and Impac Mortgage.

Impac and Timm will appeal.

If only one party wins, the fight continues. The other two parties plan appeals....

I do think that IMHPO should at least be on par with IMH common at minimum

Could be that these loans just didn't conform to whatever security they planned to issue too....

Deephaven Readies New Nonprime MBS with Mortgages from Angel Oak, Impac, 61 Others?

By Brandon Ivey

bivey@imfpubs.com

Deephaven Mortgage is set to issue a $308.2 million nonprime mortgage-backed security, according to a new presale report. Deephaven Residential Mortgage Trust 2018-1 will include non-agency loans funded by Angel Oak Mortgage Solutions and Impac Mortgage Holdings, among others.

The deal is largely backed by adjustable-rate mortgages, including some with interest-only terms. Purchase mortgages account for 67.6 percent of the issuance. Roughly 20.4 percent are loans on investment properties.

The mortgages have an average credit score of 693, an average combined loan-to-value ratio of 74.8 percent and an average debt-to-income ratio of 36.2 percent. Morningstar Credit Ratings and S&P Global Ratings assigned preliminary AAA ratings with credit support from subordination of 35.9 percent on the senior tranche.

Mortgages from 63 lenders were included in the deal led by Angel Oak with a 19.9 percent share and Impac (12.3 percent). While Impac has been originating non-QMs the past few years, its production generally has not found its way into non-agency MBS.

-----------------------

This may mean that Impac's previously announced Non-QM MBS is not happening. Impac was saying that they would issue $300 or $400 million themselves.

Judge P ruled on 12/29 that the B Series had a right to receive cumulative dividends and elect two board members. Impac will appeal. So will Curtis Timm as a holder of IMPHO.

With $21 in cumulative dividends, a full valuation on IMPHP would be about $46. IMPHO is worth $25, in my opinion. The greater risk reward is with IMPHO right now. That's my belief.

Also, I believe the common shares have nearly the same risk/reward as IMPHO at the current price. IMPHO may be slightly undervalued in comparison.

Administrative overhead is down, with the resignation of Ashmore. That savings is several million per year. Perhaps now they can afford to pay the preferred holders. A year ago, only three profitable companies failed to pay dividends to preferred stockholders.

https://seekingalpha.com/article/4029584-open-letter-board-directors-impac-mortgage

$IMPHP $IMH $IMPHO

Welcome.

More to come.

Four Years In, Non-QM Market Struggles to Amass Volume

By Thomas Ressler

tressler@imfpubs.com

The game-changing ability-to-repay mortgage lending rule from the Consumer Financial Protection Bureau took effect four years ago this month. At that time, regulators said there would be plenty of mortgage lending outside the parameters of the qualified-mortgage box. So far, however, that expectation has yet to be realized.

Authoritative numbers on the size of the non-QM space are difficult to come by. One clear indicator is the volume of interest-only mortgage originations, $20.2 billion during the first nine months of 2017 by 15 major lenders, according to Inside Nonconforming Markets.

And a handful of nonbanks have established a growing securitization market for a variety of non-QM loans and other expanded-credit mortgages, including a new breed of nonprime loans and products for borrowers who don?t easily fit into the agency box such as the self-employed and foreign nationals.

Suzanne Mistretta, a senior director in Fitch Ratings? residential mortgage-backed securities ratings group, told Inside Mortgage Finance this week the sector has been growing. However, ?it is still a very small percentage of total issuance,? she said. For the full analysis, see the new edition of Inside Mortgage Finance.

Other areas of interest: Originations, Regulatory, Nonconforming

Preferred volume today 7K

Common volume today 5K

Something is wrong with that....

On that note....

New Residential to Raise $440 Million Via Stock Sale. More Acquisitions Ahead?

By Paul Muolo

pmuolo@imfpubs.com

Fast-growing mortgage REIT New Residential Investment Corp. has filed to sell 25 million shares of common stock, an offering that could raise upwards of $440 million based on the current share price.

In a statement, New Rez said it intends to use the proceeds for ?general corporate purposes? but in all likelihood the money will be used to finance further acquisitions in the mortgage space.

A few months back, the REIT inked a deal to acquire Shellpoint Partners for roughly $190 million in cash through a three-year earn-out deal. New Rez also has been an active buyer of mortgage servicing portfolios in the open market and now ranks fifth overall, according to figures compiled by Inside Mortgage Finance.

The REIT has a current market cap (share price multiplied by number of units outstanding) of $5.27 billion.

Late Tuesday, New Rez ? in tandem with the stock sale announcement ? disclosed estimated fourth quarter earnings ranging from $117.8 million to $202.8 million.

"The consideration being offered in the Note Offer and the Series D conversion is fair in relation to the market price for each series of Preferred Stock prior to the announcement of the transactions, in relation to the historical market prices of each series of Preferred Stock and by comparison to the consideration paid by Dynex Capital in the tender offer completed by Dynex in February 2003. The consideration being offered in the Note Offer and that would be provided by the Series D conversion each represents a premium to the closing bid price for each series of Preferred Stock as of January 7, 2004, which was the last trading day prior to the announcement of the recapitalization transactions. The closing per share bid price of the Series A Preferred Stock on January 7, 2004 was $26.50, and the market price of the Series A Preferred Stock from January 1, 2001 to December 31, 2003 ranged from a low of $6.63 per share to a high of $28.25 per share. The closing per share bid price of the Series B Preferred Stock on January 7, 2004 was $26.90, and the market price of the Series B Preferred Stock from January 1, 2001 to December 31, 2003 ranged from a low of $7.00 per share to a high of $27.89 per share. The closing per share bid price of the Series C Preferred Stock on January 7, 2004 was $34.30, and the market price of the Series C Preferred Stock from January 1, 2001 to December 31, 2003 ranged from a low of $7.81 per share to high of $34.30 per share. In the February 2003 tender offer, holders of Series A Preferred Stock who tendered their shares received either $24 in cash per share or $25.20 in 2005 Senior Notes holders of Series B Preferred Stock who tendered their shares received either $24.50 in cash per share or $25.725 in 2005 Senior Notes, and holders of Series C Preferred Stock who tendered their shares received either $30 in cash per share or $31.50 in 2005 Senior Notes."

Historic Restructuring at Dynex - SEC Filing 14A

<--- Just added this to the ibox. It's everything you need to know.

"Third, the company has included the preferred stockholders in calculations of book value. This indicates that they do intend to make good on their borrowings."

"Second, the company continues to operate with a retained deficit in earnings. In our view, the issue of the retained equity deficit of $114.7 million needs to be addressed. Preferred stockholders committed capital to the company and have not received this capital back through previous dividend payments or redemption. No business can borrow money and simply refuse to pay the lender their invested capital."

"First, in the company's balance sheet, the company states the liquidation value as $16.6 million and $35 million. This has been stated at least four times a year since any tender offer may have altered any rights of the preferred in 2009. To any ordinary investor, the understanding would be that the company intends to pay this out to the shareholders in the event of a liquidating event. In the broadest possible terms, most investors understand that a liquidating event is a sale, merger, divestiture or bankruptcy."

Impac Preferred Own At Least $51.8 Million Of Book Value

Jan. 10, 2018 7:58 AM ET|17 comments| About: Impac Mortgage Holdings, Inc. (IMH)

David Sims

Summary

Impac's SEC filing language is plain and simple.

Book value per common share is $12.30.

As Impac returns to a strong financial position, the Preferred are due their contributed capital.

https://seekingalpha.com/article/4136526-impac-preferred-least-51_8-million-book-value