News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Laize

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Samsung raises prices on Apple by 20%.

http://isource.com/2012/11/12/samsung-raises-price-of-ios-device-chips-by-20-report-claims/

"Samsung Electronics , the world's largest technology firm by revenue, raised the price of mobile processor supplied to Apple Inc. by 20% recently, Chosun Ilbo reported Monday, citing a person familiar with negotiations between the two tech giants."

Are you aware the total shares short in AAPL is less than 40% of the average daily trading volume? Even if all short positions were covered you'd be lucky to get a 1-2% gain.

This makes no sense to me. What would their strategy be? Subsidize the phones themselves?

This kind of vertical integration makes little sense to me. What are they going to do? Make iPhone exclusive to their network? They still have to subsidize their phones. That means even bigger margin cuts for them unless their wireless service is more expensive than anyone else's. Mprobably constantly paying for text messaging cross carriers, more expensive data and everything.

I don't think people will fall for it. I think they'd be overstepping their bounds if theydid this.

Is it? Analysts are always giving opinions on stocks they have no position in.

I simply do not understand why e heck apple is so high or popular, nor do I see permanent staying power.

But I'm not short apple. I have o positions in them long or short.

The tale of mr market isn't mine either. It's Benjamin Graham's. The Intelligent Investor should be required reading before anyone is allowed a brokerage account of their own.

It's Mr Market.

Warren Buffett made $40 billion buying things that Mr Market kept selling at ridiculously low prices.

I, for one, would never invest in Apple since I just do not understand the hype, nor do I see their economic moat. Personally, what I see, is a fad like UGG boots writ large.

There's nothing special about their products beyond a brand name. As such I can't justify putting my money in them, no matter how much they go up.

How outrageous is it that people get antsy and annoyed whenever Apple doesn't go up constantly?

You'd think they were some special case of a company that wasn't subject to the whims of Mr Market.

Really? Getting mad at the government for allowing large financial institutions to use program trading? For what? Because Apple was allowed to drop 11% in a week?

The biggest players in market forces are the funds that actually hold securities (Such as mutual funds and 401(k)s). Even companies like JP Morgan can't really depress or inflate prices for very long.

A company like Apple needs a lot of people either on board or jumping ship to have serious moves in price. Not just really big players getting on/off.

I, personally, don't see how Apple could continue to rise. I never have and I never will. There have been a dozen companies in the last 100 years that did the same thing as Apple and all of them have fallen from their lofty heights. I'm comfortable sitting on the sidelines.

It was never the companies' fault. It was the investors' for putting expectations that were too high on them.

Options are notably complex securities. Not only does the underlying price factor into what their premium costs, but so do other things such as implied volatility (how much the market expects the price to move), time premium left (how much time left until expiration. More time means more premium). It's entirely possible that the market considers a constant dividend an indicator of stock stability which reduced volatility and therefor option premium,

You're correct that if you sell the options themselves you won't be getting the full 40 on a 530/570 bull call spread.

If you wait until expiry and sell, you will.

I prefer working with ITM calls if I'm going to play with options. However, the position I had created was OTM at the time. Apple was hovering in the 500 range then.

While the rewards are much higher with OTM options, the problem occurs when the options fail to meet the strike as time goes on. OTM options will lose value much faster than ITM options. Since they're generally cheaper than ITM or NTM options, you feel compelled to purchase more options, thus amplifying your risk. It's like any other form of leverage.

Generally I buy options with expiries 2 years out and hold the contracts as stock analogues. Buying deep ITM you wind up with a delta of 1 (Where for every dollar the stock goes up/down, so too does the premium on the option). Thus you wind up with a position that moves up a dollar for every dollar the stock goes up for a fraction of the cost. In this case the cost of the option was less than 1/10 the cost of 100 shares of the underlying, yet I received the same payout as if I'd held the stock itself. These positions tend to hold their value much more stably (relatively speaking of course) compared to OTM options.

An additional benefit of buying ITM or NTM options (as opposed to OTM) is the use of spreads. If I purchase a 530 call for $45 and sell a 570 call for $30, my net debit is $15 with a potential payout of $40.

That means while my maximum loss is only $1500, my max payout is $4000.

Like I said, though, I only use options with play money OR to hedge a position OR to increase returns on stock I don't think will move greatly.

I generally play options with "play" money. And I do play with Apple a lot with options.

Back in February I bought a Jan 2013 Call w/ 530 strike for $45.60 and sold yesterday for $93.90.

Like I said, these are short term plays, though. Not investments.

By that logic people should only cover stocks they believe in with no one offering a contrarian opinion.

It's the "it can't happen to X" mentality that I can't get behind.

Apple has a wide moat. I won't deny that. Their brand loyalty is trumped by pretty much only cigarette customers.

However their products are NOT essential to everyday life. The idea that they could never falter is asking for trouble.

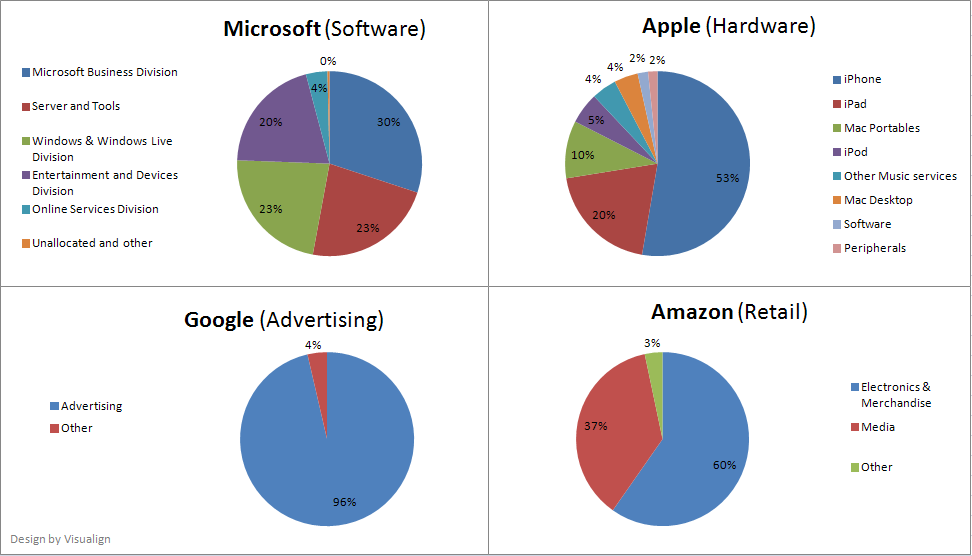

They have 2 products keeping their share price afloat. But that doesn't mean they only make 2 products.

- iPods have long since been cannibalized by the iPhone.

- Mac PCs and Macbook sales growth rates are locked in a permanent state of anemia.

- Apple TV is a product they pretty much refuse to acknowledge due to it being replaceable with an HDMI cable

There are many customers who will buy Apple products out of hand for no reason other than belonging to a bizarre cult. The majority of their customers will buy an iPhone or iPad so long as they remain better than the alternatives.

Fact is that the iPhone is already not out-of-hand better than Android options. The only advantage to having an iPhone over a high end Android phone is you get A) the Brand and B) no bloatware. iPhone is more expensive for lower performance. I'm not knocking the iPhone. I'm simply stating there's less putting the iPhone ahead of Android than there used to be.

The iPad is better positioned. I still don't see the tablet market being irrevocably and forever Apple's however.

However you only have to look at Corning's income and cash flow statements to see where their growth has been and look at forward looking statements to see where it's going.

Paying 6-7 times book value is something I cannot justify.

The fact remains that Apple is not diversified enough to withstand a hit in either the iPhone or iPad markets.

I understand that Apple's earnings multiple isn't that high compared to other techs (Though most of the ones you compared it to are services rather than manufacturer/designers).

However Apple trades at many times its equity value. I like steady but large increases in book value.

Take Corning (GLW) for example. They have a book value of $13.91. This effectively serves as a floor the stock can't realistically stay under for long (Even if the company were liquidated you'd still get at least the tangible book value). They are a 150 year old company that's a consistent leader in technology with a top line that grows by leaps and bounds. I took the opportunity to scoop up a huge number of shares because I think it's a much better deal than Apple. Hell they PROVIDE Apple with glass.

Apple's tangible book value is ~$92. That means if the next iPad or iPhone isn't a blockbuster the stock has a LONG way to fall before it reaches its floor.

They're also in a notoriously fickle business.

Last but certainly not least... there's something inherently *wrong* with a stock that doesn't stop going up even when the entire rest of the street is down by 2%. It goes against everything the history of the markets should have taught us. The "this time it's different" mentality and people's willingness to climb aboard without serious critique is unnerving.

Most fundamental based investors wouldn't dream of paying over a 15 P/E for any stock.

Myself, I won't pay more than 150% of equity/book value and 12x earnings.

I bought an iPad. I think I'll welsh on this bet and use it instead.

I will never be convinced Apple is worth this valuation until they have a more diverse product lineup that doesn't have to downplay everything but the iPad and iPhone.

Not really.

They're 2 products.

Over 70% of their revenue comes from just 2 products. Almost 100% of profits come from the iPhone.

Tell me what happens if the iPhone falls out of favor? It's ludicrously expensive for carriers to subsidize it. Realistically, Apple needs AT&T and Verizon as much as the carriers need Apple. Verizon proved that by being ridiculously profitable in the years before they got the iPhone.

My mind isn't closed. Indeed I did not say tablets or smartphones were on their way out. I simply refuse to invest in a company that has 2 products accounting for 70% of revenues and almost 100% of profits.

Indeed I have had a smartphone for the last 4 years and was first in line for the new iPad preorders this year.

Technology, however, moves so fast that it's impossible to guess what's coming down the pipe.

Apple (or more accurately, Steve Jobs) had hit the nail on the head twice in a row with how the consumer wanted the smartphone and tablet computer. He is gone now. But those 2 products have built a company with one of the most recognizable brands in the world and some of the largest profits. I'll be eager to see what Apple does with those profits besides sit on them.

If you want an insight into my investing philosophy I'm more than willing to share.

I won't invest in things that have even a tiny potential of becoming irrelevant.

I treat my stock positions as actual corporate ownership (That IS what stock is after all).

While Apple is fantastic right now, what's to say that 5, 10, 15 or 20 years down the line their products won't be eclipsed by something another company invents? What law of the Universe prevents Apple from making missteps that cost it market share or squeeze its margins?

Companies like Corning, meanwhile, have 150 year histories of innovation and products that can't be driven out of favor. How can anyone top (theoretical) unlimited bandwidth at the speed of light?

As stated, I will always take a missed opportunity before a bad investment any day.

I could have told you investing in Apple 12 years ago at $7 would have made you a lot of money. I doubt you'd care. I could tell you that investing in Citigroup $3.50 strike calls about 18 months ago would have yielded a 112% gain in 6 months, but I don't think you'd care about that.

I don't care about getting rich quickly. I care about making absolutely certain my investments are sound and safe. Not simply about gains.

I only buy companies in a way similar to Warren Buffett. I buy great companies I can find at reasonable (or even fantastic) prices. He's managed to become one of the richest men in the world long before Apple even came into the picture. I've managed to not go to the poorhouse being happy with 16% annualized gains.

The fact of the matter is that no one NEEDS Apple products. Some of my major holdings are Corning, PNC and BP. People will always need energy. Corning manufactures glass for iPads, iPhones, Android phones and tablets (In short, they'll still be winning even if Apple collapses), fiber optic cable and other products. PNC is one of the most well-capitalized banks that is expanding their footprint tremendously and they've grown 33% in the last 4 months.

I may have missed Apple, but I've done pretty damn well for myself, thanks.

I will take a missed opportunity over a bad play any day of the week. Apple simply does not fit into my investing model. If you made money on it, by all means continue to do so.

I simply cannot see myself buying a company that is as vulnerable to a change in sentiment as a company that designs pretty much TWO things.

Mind you I'm not against Apple as a company. I had my new iPad preordered the first day and I'm typing this on a Macbook Pro. What happens if Apple stumbles and loses some of their "buy it without question" branding power? What happens if someone else invents the next generation of amazing products and Apple finds themselves lagging instead of leading the tech sector?

There are too many vulnerabilities in a 2-product lineup.

Well it serves me well.

Personally I'd never invest in a company who received approximately 70% of their revenues from 1 or 2 products. No matter how "essential" those products considered, there's always vulnerability down the line.

If I think smartphones and tablets are here to stay (I do), I choose the company that wins whether or not Apple does.

I simply had to ask what the connection between Apple and Berkshire Hathaway was. I couldn't imagine 2 companies further away from each other in terms of business model.

I'm well aware of Berkshire's share price. Of course that would give Apple a market cap of $111.9 trillion.

I just browse these forums now and then to see what people are doing.

I'd never personally invest in Apple.

What does Berkshire Hathaway have to do with Apple?

Meanwhile the market pumps them over 4% today on news of their passing the Fed's stress test and potential dividend hike.

Granted this is a price level they've seen several times before. A dividend hike is pretty juicy though.

I'm keeping my price target for them at about $75.

I don't know who these companies you list are... I know a few things about this stock though.

1) Standard and Poor's rates them 4 out of 5 stars.

2) They've been shown to be consistently profitable

3) They have a long history of buying bank branches and turning them around (Huge purchase of RBC branches in the US will be profitable soon)

4) They have a healthy dividend and payout ratio

You can hate them as much as you like, but I'll be holding on my march to $70 and beyond.

There's nothing to disagree about. The government forced PNC and banks like it to take bailout money they didn't need.

As for your particular brand of hatred for PNC's receipt of TARP funds, it's clear you're uninformed about the circumstances of the funds.

They were strongarmed into accepting the funds. They neither wanted nor needed them.

In fact, they didn't need them SO much that they took the funds for what they were, a low/no interest loan they could easily pay back. With the money they made a buyout purchase of RBC's branches in the Southern United States. If you're mad about that, consider the fact that they used the money that they supposedly "needed" to SAVE another bank.

I have no idea what the hate for PNC is for.

They're the bank all other banks should be modeling.

They have the conservative practices of Wells Fargo with the customer service of... well they have some of the best customer service in the banking industry (Certainly better than WFC).

Despite the poor Q4 (Which was still profitable), they managed to increase their yearly net profit by about 3.2% and their book value by a whopping 9.2%.

With shareholder equity at $61.52 per common share and strong earnings confidence from leadership, there is no reason to avoid PNC if you're into financials at all. This isn't even counting the strong performance of Blackrock(BLK)'s fundamentals.

If you intend to make Apple your only holding, be my guest. Not my money. However, I am allowed to speak my mind on these matters. I'm not obligated to be a sycophant to the AAPL ticker symbol, and it's certainly not the only stock that's ever made anyone huge piles of money.

Personally, I would rather a company of Apple's size start repurchasing the 3-5 million shares they dilute their total outstanding shares by every quarter.

Unless they come out with a groundbreaking product in September (and not just an iPhone4GS) I wouldn't really expect the same 50% YoY revenue increases people love so much about Apple.

iOS and Android have been in a race to the top with every iteration, and the only clear victor in the battle has been the consumers who have 2 fantastic operating systems to choose from. Android copies great features from iOS while iOS copies great features from Android. It's truly a great example of why Capitalism works. The only problem is that with every new research study, the same ratio of iOS to Android users has been cropping up with only a few basis points worth of people switching now and then. So while Nokia and RIM inevitably continue losing market share, I wouldn't expect to see a clear victor of Android or iOS in that.

Tablets are a different story. There is no other tablet PC on the market than the iPad. No matter how much other manufacturers try to advertise.

Apple probably still has a ways to go before people realize their growth is finished. But if they hit $500 in 12 months I'll eat an iPad.

You dismissed the idea that equity was important in the valuation of a company? Equity serves as a floor that a stock cannot (or rather, should not) go under as long as it's being managed well.

Unless the company has a ridiculously high ROE (Like Netflix at 90%), you cannot discount it in terms of valuation.

$66.49 BV/Share

Trading too high above Book Value for my tastes. Not a good value stock. Maybe a growth stock still, but really, where else can they generate more revenue?

If I were an Apple shareholder (I'm not) I would look for Apple to start finding other ways to return value to shareholders. With about $6B in Free Cash Flow last quarter, you'd think they could start a share repurchase program... that would be only appropriate since they dilute the total shares outstanding by about 3-5M every quarter.

Or heck, maybe even a dividend. Wouldn't have to be much. Even an amount as small as 10% of their free cash flow would yield a 1.6% annual return and still leave them piles of cash for R&D, marketing and their war chest.

Not to mention the buying frenzy that would start on shares once people realized they were finally getting a piece of the cash Apple was generating.

I'd, personally, prefer a share buyback program.

Without either solution, however, it seems to me that Steve Jobs just doesn't care about his shareholders. At least he cares about his customers.

I thought Apple was at a good entry point at around the $200-$220 mark.

And leveraged Citigroup calls yielded a down payment for a car in under 6 months. It's all about how you play the game. All I said was the Macbook Air was overpriced for me. Is that so wrong?

Well, as I'm sure you know, they've recently entered the Canadian market. I'm expecting some pretty wonderful numbers from that. I can't help but feel as though my time with them is coming to an end though.

Um... I'm using the USD. And 1300 USD is (way) too much for a mid-range laptop. As in WAY WAY too much. You really can't consider a stock holding as a discount for purchasing a product. Especially since once you sell off the shares, it's gone.

All I'm saying is that their products are incredibly overpriced. And if you're ready to buy an iMac for $2400, you have gone off the deep end... especially since you can just install OSX (If that's your fancy) onto any PC nowadays.

It's possible. I certainly have no doubts about whether they have a good product or not. My concern is that they're just too pricey for the money they actually bring in. In 2009 I saw them producing their first truly great quarterlies and loaded up at $35. But as they kept going up over the year I began to have my doubts as to how much longer it could last. Their stock was outpacing their earnings by a significant margin. Just what kind of premium are people willing to pay on their growth?

I really thought Apple might've had a product on their hands that I wanted. Looking at the new Macbook Air I thought "Hey, this is exactly what I want. Something portable that can play my games, get to my sites and pretty much do everything I want.

Then I saw the price tag of $1300 for the model I wanted. They were so close to having another customer :/