News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

* * $AUY Video Chart 08-24-2019 * *

Link to Video - click here to watch the technical chart video

Yes your correct and with this China traffic fiasco and today Trump had mouthing the Fed.Gold silver crypto is the logical choice and shorting your favorite stocks. You Can always buy back when the smoke clears

News: $AUY Billion Dollar Gold Belt Found In Southern Mali

August 23, 2019 FN Media Group Presents OilPrice.com Market Commentary London – August 23, 2019 – What’s it like to strike it rich? It’s probably like finding gold in the middle of nowhere. Well, that’s exactly what happened&#x...

Find out more Billion Dollar Gold Belt Found In Southern Mali

still one of the best gold bets, very cheap

News: $AUY Gold Stocks Take The Lead As Trade War Deepens: GOLD, AUY and KGC Lead

Barrick Gold Corp (NYSE: GOLD), Yamana Gold Inc. (NYSE: AUY) and Kinross Gold Corporation (NYSE: KGC) are all making their way to the top in t...

In case you are interested Gold Stocks Take The Lead As Trade War Deepens: GOLD, AUY and KGC Lead

old posting

BAA_Up Sunday, 04/28/19 04:03:51 AM

Re: Rogue Dead Guy post# 2230 0

Post #

2236

of 2259

2.08 is my next buy. But now I own really much. I am very stubborn at this, despite the down-gradings

InvestorsHub NewsWire

No, we're on schedule.

Talked to the company a long time ago. Everything I was promised was fulfilled. Because I was worried about the share price. Now what? Auy reduced his debts a lot.

Production increased. Dividend doubled. Reserves have increased.

Aqua Rica is a more than twice as good asset as Chapada.

Chapada is not a loss. Would have cost investments.

Good deal at today's copper price.

When the gold price rises, Auy will swing to old heights.

Is now again a very safe investment for the next years.

The financial fundamentals are now very good compared to the assets.

Auy also has shareholdings. Lea Gold etc.

Do a little research then you will find the company good.

Auy will now be heavily dependent on the price of gold, and will be going along with every gold move.

Don't forget that they produce 10 million ounces of silver.

Compare this with silver mines that produce much less and see their price.

Also the insider list is good. No sales. 2018 good buys.

Only Marrone earns too much. Is no longer present at conference calls. But he comes from the banking sector, and maybe that helps AUY.

He is also a director on the Lea Gold-board.

In conversation with Auy I learned that the planned buybacks of shares up to 5% are currently not planned.

Major investors have spoken out against it.

I have invested 60% of the portfolio in Auy. Good plus. but I'm not selling anything. But don't advertise here, I just say what I know or think.

Tomorrow SHOULD be a gap up to $3 but NOOOOOOOOOOO. Some lowlife boiler room weasels with short shares to cover will start an 'overstated FCF' rumor or AUY accountants will drop another asset expensing write off on shareholders during the conference call. And...back down to $2.25 we go. Really getting sick of this company being manipulated like some penny pink sheet scam...

AUY - Strong Trend More Momentum With Good News

Company Description:

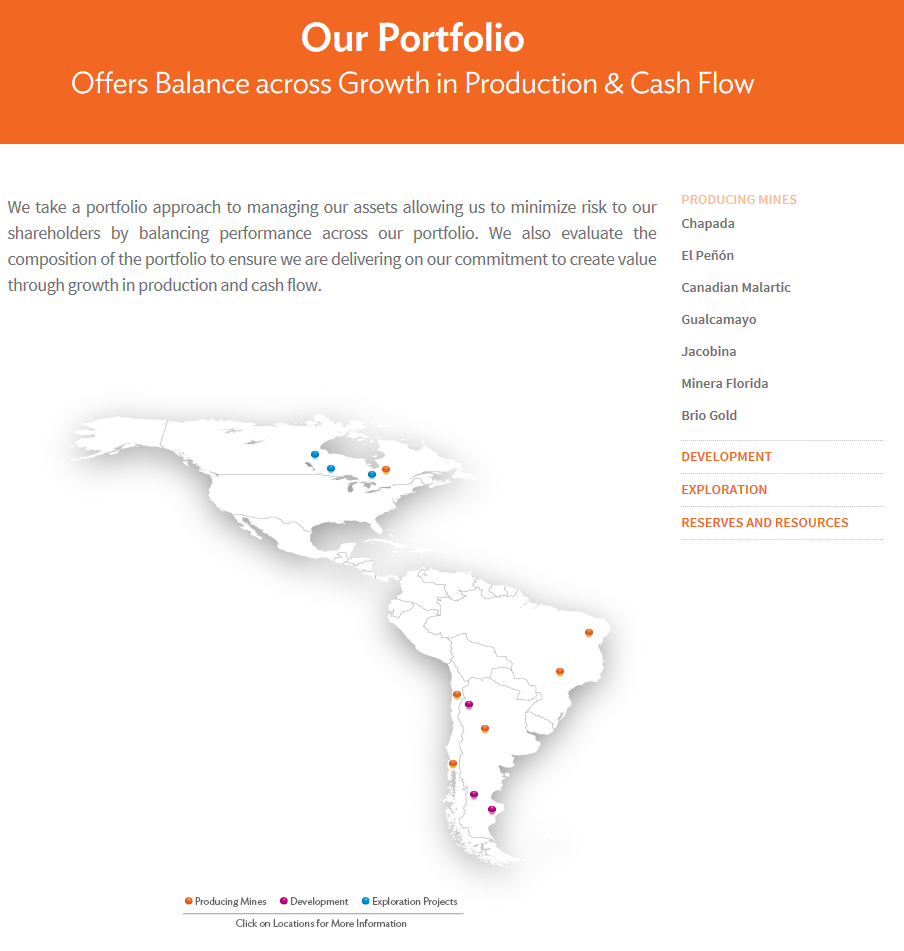

Yamana Gold Inc . is a gold producer with gold production, gold development stage properties, exploration properties, and land positions throughout the Americas, including Canada, Brazil, Chile and Argentina. The Company's segments include El Penon mine in Chile; Canadian Malartic mine in Canada; Gualcamayo mine in Argentina; Minera Florida mine in Chile; Jacobina mine in Brazil; Brio Gold Inc. (Brio Gold ), and Corporate and other. The Company's development projects include Cerro Moro, Argentina; Agua Rica, Argentina, and Gualcamayo, Argentina. Its exploration projects include El Penon, Chile; Gualcamayo, Argentina; Minera Florida, Chile; Jacobina, Brazil; Cerro Moro, Argentina; Canadian Malartic Corporation, Canada; Monument Bay, Canada; Brio Gold Exploration; Pilar, Brazil; Fazenda Brasileiro, Brazil; RDM , Brazil, and C1 Santa Luz, Brazil.

Yamana Gold Announces a Positive Pre-Feasibility Study With an Impressive and Increased NPV of $1.9 Billion and an Increased After-Tax IRR of 19.7% for the Long Life Integrated Agua Rica Copper-Gold Project (Source: https://finance.yahoo.com/news/yamana-go...)

Short Interest:

6.38M (06/28/19)

P/E Ratio (with extraordinary items)

-21.12

Analysts Prediction

$3.18

Analysts Recommendation: Overweight

Thanks Bob! I Keep an eye on $AUY and $MUX. Gold is Perking Up Again.

:)

Low $2s paying again $AUY

Lundin closes $1bn acquisition of Chapada copper-gold mine

MINING.COM Editor | July 5, 2019 | 1:55 pm Latin America Copper Gold

Lundin Mining grabs Brazilian copper-gold mine from Yamana in $1B deal

Chapada mine, in the Brazilian state of Goiás, began production in 2007. (Image courtesy of Sandstorm Gold Royalties)

Lundin Mining on Friday announced it has closed the acquisition of a

100% ownership stake in Mineração Maracá Indústria e Comércio S/A,

which owns the Chapada copper-gold mine in Brazil from Yamana Gold.

https://www.mining.com/lundin-closes-1-billion-acquisition-of-chapada-copper-gold-mine/

The Chapada mine, in the northwest state of Goiás, began production in 2007 and is expected to churn out about 54,500 tonnes of copper and 100,000 ounces of gold this year.

The deal was first announced in April.

Total cash consideration paid at closing by the Lundin was $800 million, funded by cash on hand and the Company’s $550 million revolving credit facility.

Yamana retains a 2.0% net smelter return (NSR) royalty on future gold production from the Suruca gold deposit, receives contingent consideration of up to $125 million over five years if certain gold price thresholds are met and contingent consideration of $100 million on potential construction of a pyrite roaster.

Yamana Gold Increases Gold Production Guidance and Updates Improved Strategic Life of Mine Plan and Phased Expansion for Its ...

Print

Alert

Yamana Gold Inc. Ordinary Shares (Canada) (NYSE:AUY)

Intraday Stock Chart

Today : Thursday 27 June 2019

Click Here for more Yamana Gold Inc. Ordinary Shares (Canada) Charts.

YAMANA GOLD INC. (TSX: YRI; NYSE: AUY) (“Yamana” or “the Company”) today announced an increase to the three year guidance for its wholly-owned Jacobina mine and an update on its two-phased plan to further increase production thereby improving the strategic life of mine.

The following tables present the Company's increased production expectations for Jacobina in 2019, 2020, 2021, and cost guidance for 2019, excluding further potential upside from the Phase 2 expansion described below and any benefit from higher grade ore. Increases in production are only attributable to implementation of the Phase 1 expansion, which is now in progress.

2018

Actual 2019

Guidance 2020

Guidance 2021

Guidance

Jacobina Gold Production (oz.) 144,695 152,000 160,000 170,000

Previous (oz) 145,000 - -

Total Cost of Sales

per GEO sold(2,3) Cash Costs(1,3)

per GEO sold AISC(1,2,3)

per GEO sold

2018

Actual 2019

Guidance 2018

Actual 2019

Guidance 2018

Actual 2019

Guidance

Jacobina $967 $1,005 $675 $700 $891 $890

Refers to a non-GAAP financial measure or an additional line item or subtotal in financial statements. Reconciliations for all non-GAAP financial measures are available at www.yamana.com/Q12019 and in Section 10 of the Company’s first quarter 2019 Management’s Discussion & Analysis, which has been filed on SEDAR.

Mine site AISC (all-in sustaining costs) includes cash costs, mine site general and administrative expense, sustaining capital, capitalized exploration and expensed exploration. Consolidated AISC incorporates additional non-mine site costs including corporate general and administrative expense.

Yamana reports costs on a gold equivalent ounce basis; Jacobina produces only gold. Therefore, in the case of Jacobina, gold equivalent ounces are equal to gold ounces.

The Company is one year ahead of schedule in its plans to increase sustainable production to 150,000 ounces per year and now forecasts life of mine production of over 170,000 ounces per year after 2021. Guidance for 2019 capital costs remains unchanged. Furthermore, the company expects a similar level of total capital spending during 2020.

(All amounts are expressed in United States Dollars unless otherwise indicated.)

JACOBINA PHASE 1 UPDATE

Phase 1 involves a modest plant optimization to increase throughput to a sustainable level of 6,500 tonnes per day (“tpd”) by mid-2020. This optimization is ahead of schedule with quarter to date throughput averaging 6,182 tpd thereby allowing the Company to increase its guidance. This compares to average daily throughput of 5,580 tpd in 2018.

Optimization work completed to date includes improving grinding and crushing with the installation of an Advanced Process Control system with monitoring devices for the mill and crushing circuit. Further initiatives to reduce plant maintenance downtime were completed in May. Remaining work for Phase 1 is well advanced. Commissioning of a high frequency sieve and an induction furnace is expected in the third quarter and commissioning of two gravimetric concentrators and a cyclone battery to feed the thickener is expected by the first quarter of 2020. As of the end of June, the remaining project capital costs to complete Phase 1 are approximately $3.4 million. Approximately $2 million of these costs, included in previously guided capital spending, will be spent over the balance of 2019 with the remainder in 2020.

Phase 1 is expected to increase the gold production rate to approximately 170,000 ounces per year by 2021 at the current mineral reserves grade, a 21% increase compared to original 2019 production guidance of 145,000 ounces per year.

Following completion of the mill optimization, there is potential for a further production increase driven by higher grades. In 2019, exploration work has focused on supporting the planned expansion and targeting new mineral resources at a grade of 3.0 grams per tonne (“g/t”) or better. At year-end 2018, proven and probable mineral reserves totaled 2.1 million ounces of gold contained in 27.9 million tonnes at an average grade of 2.34 g/t, measured and indicated mineral resources were 3.2 million ounces of gold contained in 40.7 million tonnes at 2.47 g/t, and inferred mineral resources totaled 1.0 million ounces contained in 12.1 million tonnes at 2.58 g/t. The mineral reserve and mineral resource estimates for Jacobina at December 31, 2018, are set out below. Updated mineral reserve and mineral resource estimates at Jacobina are expected to be provided in the third quarter of 2019. The update will incorporate infill drilling of the higher grade inferred mineral resources at João Belo, Canavieiras Sul, Morro do Cuscuz, and Morro do Vento. Assuming an increase in grade for the updated mineral reserves, sustainable production resulting from Phase 1 has the potential to exceed the 170,000 gold ounces per year production level.

While the updated guidance shows incremental production increases in the next three years, resulting from the staged throughput increases as Phase 1 is fully implemented, the Phase 1 expansion creates a sustainable production level of at least 170,000 gold ounces per year for the life of mine after the three year guidance period based on current mineral reserve grades, which would further increase with grade improvements.

JACOBINA PHASE 2 UPDATE

The Phase 2 plant expansion is expected to result in a larger increase in plant capacity with a likely scenario in the range of 7,500 tpd to 8,500 tpd, while maintaining gold recoveries of between 96%-97%. The higher throughput would gradually increase Jacobina’s gold production to at least 200,000 ounces per year and up to 225,000 ounces per year by 2023 based on current mineral reserve grades. A pre-feasibility study (“PFS”) to identify optimum mining and processing expansion scenarios, evaluate project economics, and determine a project development schedule including the timing for permit applications is expected to be completed in the first quarter of 2020. Investment for Phase 2 is expected to occur mostly in 2021 and 2022 with the objective of being at the higher throughput level at the beginning of 2023. No expansionary capital will be committed to the plant expansion until the PFS is completed. The Company’s hurdle requirement for expenditure on the Phase 2 expansion is an after-tax IRR exceeding 15%. The decision to proceed with the investment will be driven by the expansion of the plant throughput, thus bringing forward cash flows, but also an extension of mine life from continued exploration success and improvements to Jacobina’s average mineral reserve grade, which would support the investment decision. To this end, the Company has approved a $3 million increase to Jacobina’s exploration budget for the balance of 2019 and builds on the success from the 2018 program. A dedicated exploration update for Jacobina will be provided during the third quarter of 2019.

“Jacobina has improved significantly in the last several years across all measures, and it is now one of our higher quality, high value operations,” said Daniel Racine, President and Chief Executive Officer of Yamana. “We believe that it is on the cusp of becoming a world class mine, particularly once a decision is made to proceed with the Phase 2 expansion, given strong production, production growth, increasing mineral inventory at improving grades, and continuous increases in cash flow.”

The planned expansion at Jacobina is the continuation of a series of incremental improvements that have been successfully implemented over the past four years, during which gold production increased from 75,000 ounces in 2014 to 145,000 ounces in 2018.

The following table shows the incremental gold production growth trend that Yamana is targeting with the Phase 1 and Phase 2 expansions. These objectives are based on increase in throughput only and do not include further upside for an increase in grade as a result of exploration.

2018 Actual 2019 Guidance 2020 Guidance 2021 Guidance 2022 Objective 2023 Objective

Jacobina Gold Production (oz.) 144,695 152,000 160,000 170,000 200,000 200,000-225,000

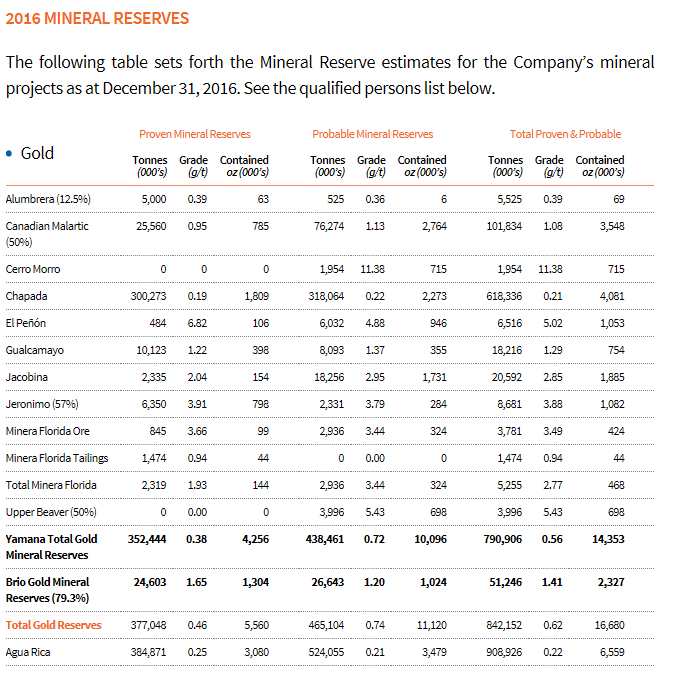

As of December 31, 2018, mineral reserves and mineral resources were as follows and supported a mine life of at least 13 years.

Mineral Reserve Statement, Jacobina

Proven Mineral Reserves Probable Mineral Reserves Total Proven & Probable

Tonnes Grade Contained Tonnes Grade Contained Tonnes Grade Contained

(000's) (g/t) oz. (000's) (000's) (g/t) oz. (000's) (000's) (g/t) oz. (000's)

Gold 18,565 2.32 1,385 9,290 2.39 714 27,855 2.34 2,099

Mineral Resource Statement, Jacobina

Measured Mineral Resources Indicated Mineral Resources Total Measured & Indicated

Tonnes Grade Contained Tonnes Grade Contained Tonnes Grade Contained

(000's) (g/t) oz. (000's) (000's) (g/t) oz. (000's) (000's) (g/t) oz. (000's)

Gold 24,999 2.48 1,994 15,711 2.45 1,238 40,710 2.47 3,232

Inferred Mineral Resources

Tonnes Grade Contained

(000's) (g/t) oz. (000's)

Gold 12,145 2.58 1,008

Mineral Reserve and Mineral Resource Reporting Notes

Metal Price, Cut-off Grade, Metallurgical Recovery:

Mineral Reserves Mineral Resources

Price assumptions: $1,250 gold

Underground cut-off grade is 1.20 g/t gold

Metallurgical recovery is 96% Price assumptions: $1,500 gold

Underground cut-off grade is 1.0 g/t gold with a

minimum mining width of 1.5 metres

Metallurgical recovery is 96%

All Mineral Reserves and Mineral Resources have been calculated in accordance with the standards of the Canadian Institute of Mining, Metallurgy and Petroleum and National Instrument 43-101 – Standards of Disclosure for Mineral Projects

All mineral resources are reported exclusive of mineral reserves.

Mineral resources which are not mineral reserves do not have demonstrated economic viability.

Mineral reserves and mineral resources are reported as of December 31, 2018.

Due to rounding, numbers may not add precisely to the totals.

A mid-year mineral reserves and resources estimate is planned for later this summer based on the extensive additional drilling information obtained since last year. An exploration update showing further geological potential and expectations will also be provided.

The Company is also evaluating a paste/backfill plan that will aim to reduce dilution and further improve production and costs. An update is planned before the end of the year.

CORPORATE OVERHEAD IMPROVEMENTS

Yamana has been critically evaluating its general and administrative (“G&A”) expenses to align its cost structure to its remaining portfolio of assets, as the Chapada sale is expected to be completed within the next few weeks. The Company now expects 2019 G&A expenses on a cash basis to be lowered to $68 million compared with previous guidance of $75 million, implying a run rate of approximately $60 million per year. The Company expects G&A expenses to remain at $60 million in 2020, resulting in savings of over $15 million annually, and the Company anticipates that further reductions will be realized through optimizations and cost reduction initiatives.

These savings will be realized from the direct impact of the Chapada sale and adjustments resulting from a smaller regional presence in Brazil. Furthermore, the Company’s overall organizational structure is being streamlined across South America in particular and over the entire organization more generally.

“The anticipated saving from the G&A initiatives that we are implementing align with the strategic rationale of the Chapada sale,” Racine said. “They will further strengthen our balance sheet and improve our financial flexibility, and they will simplify our organizational structure to match the Company’s remaining portfolio of five mines.”

UPCOMING EVENTS

The Company would like to highlight a number of notable upcoming events and milestones. These include:

The pre-feasibility study for Agua Rica.

The completion of the Chapada sale, expected in early July.

Following the closing of the Chapada sale, the repayment of the Company’s outstanding revolving credit facility and near and medium-term fixed term debt maturities from proceeds of the transaction.

Preliminary second quarter operational results, expected during the second week of July.

The release of second quarter financial and operational results on July 25.

Delivery of an exploration update press release on Jacobina during the third quarter.

An investor tour of the Jacobina mine this fall. Details to follow in the coming weeks.

Qualified Persons

Scientific and technical information contained in this news release has been reviewed and approved by Sébastien Bernier, (P.Geo and Senior Director, Geology and Mineral Resources). Sébastien Bernier is an employee of Yamana and a "Qualified Person" as defined by Canadian Securities Administrators' National Instrument 43-101 - Standards of Disclosure for Mineral Projects. Data verification related to certain scientific and technical information disclosed in this news release in connection with Yamana’s material properties can be found in the Company’s Annual Information Form dated March 28, 2019, available under the Company’s profile on SEDAR at www.sedar.com and on the Company’s website.

About Yamana

Yamana is a Canadian-based gold, silver and copper producer with a significant portfolio comprised of operating mines, development stage projects, and exploration and mineral properties throughout the Americas, mainly in Canada, Brazil, Chile and Argentina. Yamana plans to continue to build on this base through expansion and optimization initiatives at existing operating mines, development of new mines, the advancement of its exploration properties and, at times, by targeting other consolidation opportunities with a primary focus in the Americas.

FOR FURTHER INFORMATION PLEASE CONTACT:

Investor Relations

416-815-0220

1-888-809-0925

Email: investor@yamana.com

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS: CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS: This news release contains or incorporates by reference “forward-looking statements” and “forward-looking information” under applicable Canadian securities legislation within the meaning of the United States Private Securities Litigation Reform Act of 1995. Forward-looking information includes, but is not limited to information with respect to the Company’s strategy, plans or future financial or operating performance, expected G&A expenses, production and costs, the completion of the Chapada sale and expected use of proceeds, and the 2019, 2020 and 2021 production and cost guidance with respect to the Jacobina mine, the Company’s production, exploration, development and expansion plans and strategy at the Jacobina mine and the expected timing and results of such plans, the expected timing for completion of the PFS and the release of updated mineral reserve and mineral resource estimates. Forward-looking statements are characterized by words such as “plan,” “expect”, “budget”, “target”, “project”, “intend”, “believe”, “anticipate”, “estimate” and other similar words, or statements that certain events or conditions “may” or “will” occur. Forward-looking statements are based on the opinions, assumptions and estimates of management considered reasonable at the date the statements are made, and are inherently subject to a variety of risks and uncertainties and other known and unknown factors that could cause actual events or results to differ materially from those projected in the forward-looking statements. These factors include the Parties’ expectations in connection with the development, exploration and construction plans for the integrated Agua Rica and Alumbrera discussed herein being met, and the impact of general business and economic conditions, global liquidity and credit availability on the timing of cash flows and the values of assets and liabilities based on projected future conditions, fluctuating metal prices (such as gold, copper, silver, zinc and molybdenum), currency exchange rates (such as the Argentine peso versus the United States dollar), the impact of inflation, possible variations in ore grade or recovery rates, hedging programs, changes in accounting policies, changes in Mineral Resources and Mineral Reserves, risks related to other investments, risks related to metal purchase agreements, risks related to acquisitions, changes in project parameters as plans continue to be refined, changes in project development, construction, production and commissioning time frames, unanticipated costs and expenses, higher prices for fuel, steel, power, labour and other consumables contributing to higher costs and general risks of the mining industry, failure of plant, equipment or processes to operate as anticipated, unexpected changes in mine life, final pricing for concentrate sales, unanticipated results of future studies, seasonality and unanticipated weather changes, costs and timing of the development of new deposits, success of exploration activities, permitting timelines, government regulation and the risk of government expropriation or nationalization of mining operations, risks related to relying on local advisors and consultants in foreign jurisdictions, environmental risks, unanticipated reclamation expenses, risks related to fiscal stability agreements, risks relating to joint venture operations, title disputes or claims, limitations on insurance coverage and timing and possible outcome of pending and outstanding litigation and labour disputes, risks related to enforcing legal rights in foreign jurisdictions, as well as those risk factors discussed or referred to herein and in the Parties filings with applicable securities regulatory authorities and publically available. Although the Parties have attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be anticipated, estimated or intended. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. The Parties undertake no obligation to update forward-looking statements if circumstances or management’s estimates, assumptions or opinions should change, except as required by applicable law. The reader is cautioned not to place undue reliance on forward-looking statements. The forward-looking information contained herein is presented for the purpose of assisting investors in understanding the Parties’ expected plans and objectives and may not be appropriate for other purposes.

Gold 1400s is big

News: $AUY How To Buy Gold For $3 An Ounce

June 20, 2019 FN Media Group Presents Oilprice.com Market Commentary London – June 20, 2019 – What Wall Street knows as an incontrovertible truth is this: Fear is a bargain. And right now, there’s so much fear floating around the market that gold is ...

In case you are interested https://marketwirenews.com/news-releases/how-to-buy-gold-for-3-an-ounce-8388928.html

Price of gold goes up......shareprice of Yamana goes down! Ridiculous! Should not be!

I did that. And I am very satisfied. And confident for the future of AUY

* * $AUY Video Chart 05-31-2019 * *

Link to Video - click here to watch the technical chart video

1,45 USD .....joke. I call the company the next days, will tell you

Very interesting.. broke the support the other day and has just been falling.. going to have to look at the 5 year chart to find supports this low.. eyeing it for now.. $AUY

This POS is dead. Like seriously dead. What a disaster. I wish I never touched it with 7-feet pole. At lease Marone is making $5M a year. Scam company.

A couple 6 figure buys today. Hmm. $AUY

What's the point? Did you hear anything?

If not, the question is uninteresting.

And if so, does it play a role in the long run?

When gold rises all mines rise. AUY with 2 USD. What should happen in the long run? Not even a sale would be below this price.

Even without Chapada it is worth even more.

Thank AUY will see below $2.00 range soon..Noticed HMY resetting lows too.

Thanks for your reply.

Is also my opinion that Auy is a company in which one can invest.

Auy still has not convinced with the reports.

The financial deterioration in Argentina weighs on Auy, so the downgrades. My opinion

Mathematically, she should actually report well this quarter.

If there are no depreciations. But for the interest rate uncertainty, I rate the Chapada deal very positively.

I also prefer organic growth to high purchases.

Aqua Rica could be an excellent project. The insiders are also o.k. in 2018.

The dividend doubling is certainly good.

But a good signal to think about the shareholder.

Good luck

I am still waiting for someone here to calculate a takeover price.

But I hope Auy manages to become very attractive with a high gold price.

p.s. Is Leagold a play for you? 20 % owns AUY and Marrone is director.

Agreed! $2.08 is a good entry just looking at the chart. $2 is was bottom last time we got this low.. $AUY is a good company and I will be grabbing more.. especially if it hits $2.08

Has anybody a buyout price target? let me know.

2.08 is my next buy. But now I own really much. I am very stubborn at this, despite the down-gradings

Positivity can change your LIFE! : If you want my opinion, I would say... the answer my friend is blowing...

In less than a week we see the first Q. results. I hope a positive signal.

A clean report. I look forward to Aqua Rica. Would double the copper from Chapada for auy.

Agreed. "Can't go wrong at these prices for the long term."

Did the same along with a couple other miners yesterday... Can't go wrong at these prices for the long term. Gold may dip a little more in the short term but the second half of the year should be a lot better.

I don't think it's a flipping stock, although appreciation in PPS is desirable. It is a rainy day hedge for me, but I guarantee you if it runs, i will flip.! lolol

I bought yesterday as well at $2.17. Looked sketchy this morning, but held. Hoping for a nice upswing for a few days.

I’m still waiting to load.. I want to fill in the $2.00-2.10 range.. The selling will slow and it will come back. I’m watching close! $AUY

I am hoping so. I bought down here. Inflation hedge.

Have missed the case and the low today.

Will buy more tomorrow.

I see the deal with Lundin good for the future. Short and medium term debt eliminated. Rest until 2023 no topic.

The deal with GG and Glencorp could replace and double Auy's current copper production for years.

Maybe an excellent strategy.

$AUY just doesn’t want to take off.. hysterically, we are close to $3.00 by now

Cool, I hold two of the 3 companies you have mentioned. Gold Corp is my other one. It has not been doing as well as I had hoped. Some of my other holdings are Barrick and Wheaton. New Gold had been a real dog for me, hopefully they get things turned around.

I think this will come. When people are tired from others stocks volatility, fears go up, than they looking for goldstocks.

Even they dont have a clue about them.

I stay with AUY on my gold bet and I love this....

Yamana Gold, Glencore and Goldcorp Enter Into an Agreement for the Integration of Agua Rica and Alumbrera This is a copper project.

You know? The part of AUY is over 50 % .

Good luck

I own quite a bit too. Looking forward to the day when gold goes to $1900 plus per oz.

Hi, we got a small downgrade today. I am waiting too.

It is not the best company but a cheap bet on Gold for me. I own a lot.

Good luck

I'm just hanging onto my shares for when the price of gold starts moving towards the real price it should be at. Then were looking at a 5 bagger easy. Patients wins this game.

interesting setup here...

1 month no message here? The enthusiastics are gone? looks like sellers

left the board

good news from Auy look out for it I am still buying

What are projected numbers? $AUY

|

Followers

|

125

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

2315

|

|

Created

|

07/05/06

|

Type

|

Free

|

| Moderators | |||

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |