News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

HAHAHAHA........

Merry XMAS

janet

Thanks, more wonderful news. I guess you and me don't qualify for the TO fan club.

Thank you and Merry Christmas to you Surf, Janet and all! I vote for World Peace as well! :)

Merry Christmas to all.....including T.O.! Best of luck in 2012- make us all rich!! (and, give us world peace, of course)

Good morning Grace! What a good "team" you and Drumstick....

APH cannot have better.......lololol

Enjoy the Peace of the Festivity!.......

Happy Holiday,

janet

News Release re: stock consolidation on Stockhouse ... sounds like it's about taking on more products ... not credible given history... another scheme?

Just read this again. What a pile of BS. If a product is liked by consumers, sales do not drop from 1 mil. to zero, unless there are some serious problems with those running the company. In actuality as more people try the product that like it, the more it spreads, and sales go up. let's hope that possibly TO's good friend Harry Chew will pump some $ into this dead dog.

Thanks for the info. Looks like Terence Owen had other things on his mind than Alda. Now we find out who the real players are. Hopefully investors will start making enough noise to get him investigated. Many have speculated why he got involved with the Olympics without a solid game-plan. The Olympics plus all other positive developments, or so we were told, have been part of an ongoing P&D scam. At least that's how I see it.

Check out postings on Stockhouse ... meeting re-scheduled and more on relations among Owen and Chew X2

Thanks, I read. I imagine that TO won't be putting out a NR about this. OMG, he could be hooking up with this crook Harry Chew. Is TO finally showing his real colors? On the other hand does what ever he does matter anymore? I've been criticizing him on this board for years, and unfortunately the truth is looking even worse.

More info on folk at downtown office at Stockhouse.com

More contraction. I guess he's holding on till the bitter end, which is near.

don't know ... that location is also office that has Bio optics which Owen has some affiliation with ... I can only speculate with you ... shifting focus to other public companies ...??

So what do you think this means?

Alda moves downtown, same location as Pacific Paragon

The truth now comes out that Alda"s present terrible situation is due to Owen's greed, dis-interest, or inability to market & sell product. This is a text-book example of how not to run a business. If nothing else he is guilty of fraud, and should be charged for taking advantage of the privilege that a public company enjoys. Terry Owen, you are a lying thief.

ANOTHER POST ON DEC 6 FROM YAMASAKI ON STOCKHOUSE The stock is still not trading on the TSX-V, but it looks like all the requirements have been met. The exchange now has to approve everything. It must be such a "black spot" for the Venture Exchange, as Alda was endorsed as one of their 2010 Venture 50 co. With the company teetering on receivership we can only hope that management improve things. Although their inaction doesn't exactly give me any confidence.

Having read the MD&A and financials, and it paints a pretty ugly picture. Out of money, racking up loans to directors and management, defaulting on the Olympic sponsorship loan obligations, and not enough cash on hand to produce or sell new products. Management sites that additional funding is required, but not in this market with the epic asinine mis-management Terry and Peter have made even before the whole Olympics debacle.

One other beef I have is that the involvement of Scott Young in Investor Relations. Many have tried contacting him but there is no reply, yet they were paying him compensation. Terry needs to re-organize the company, and stop the bleeding.

These guys are crooks, and deserve to be prosecuted. TO has repeatedly lied to shareholders to only raise sp for his personnel gain.

Also, bear in mind that this piece of work, TO, owned the building where Alda offices were situated. For that he charged an over the market rate for rent. Kind of tells you a lot about where this guy was coming from I think. I mean, if he was really behind his company he would have given the rent free, or at least at a reduced price. Think about it.

As I said in my last post. The only logical explanation for the Olympic deal I can see was to take advantage of the rise in sp to .74 that we saw 2 years ago. After that one can only assume wishful thinking, but that's no way to run a business.

mtg in Dec? from another board, posted by Yamasaki

I believe Terry and Peter are meeting with the investment regulators in early December to establish that conditions have been met, and to provide an explanation of why they were remiss in filing in the first place. It will be then up to the regulators decision on whether to reinstate the company to active trading status. At this stage who knows what is going to happen next for Alda, but the situation is pretty dire for them. They really need to get back on track as far as generating some revenue, partnerships, or anything that can get them out of the hole that they've dug themselves. It still boggles my mind from a cost-benefit perspective, how TO and PC expected the Olympic sponsorship to drive the revenues to the point that it would make sense. Spending that kind of money is the domain of larger companies with multi-million dollar marketing budgets. Alda had no business participating in this to begin with unless they had a clear plan on how to grow revenues and penetrate the hand sanitizer or disinfectant markets to justify the expense.

Surf I agree with you about competition, and a tough investment climate. But why in the name of God did they enter into the Olympic deal, if they didn't have a solid marketing strategy to take advantage of the situation? Without a strong marketing plan they were destined to fail, as they did. Was the real reason only to get a very brief rise in sp as was the case, so insiders could have a nice big pay-day. This Olympic thing is really stuck in my crock because of the huge liability they took on. Sadly this one time opportunity that looked like it would be the launch pad for bigger and better things to come turned into a death blow. To that there's no excuse that Owen can give that holds any water. I find it hard to believe he could have expected any other out-come, unless he's a complete moron. Which leaves me only 1 explanation for Alda's Olympic disaster, and that would be to take advantage of the rise in sp we saw 2 years ago.

my take........... The plan, I think, was to market and sell T36 hand gel, and surface disinfectant, to generate enough income to further develop the therapeutic agents(which would then generate the "serious" profits-That was the main goal)...... They used their contacts to get some financing from investment, landed the Olympics- the problem was, there was(is) just too much competition in that arena(Purell, etc)- so, they have not been able to get to the next level- that, in conjunction with the horrible climate for investment- It looks like they may not be able to hang on, but if they can, may still get those therapeutic agents yet.....

I cannot tell you any of the sordid details that have led to this sad state of affairs. Obviously massive mistakes were made or things wouldn't be where they are now. We must blame Owen since he's the boss, which is exactly what I've been doing on this board for a long time. I wish I had been wrong, but the lack of any real attempts by Alda to market, and sell product was 1 of my main criticisms. Owen has always used his favorite excuse, "market conditions." I guess he's referring to the stock market, as opposed to the growing market for effective protection against many of the nasty infections out there in the world today. T-36 has been proven to be a powerful strategy in this respect. Thing is that Owen's pre-occupation with the stock market kind of shows you where his head is truly at, and in that respect it wouldn't surprise me in the least to know that this is what has destroyed this company.

agreed: arrogance and incompetence. how clear is it that fiduciary responsibilities not met? is there evidence of insider trading? of misusing corp funds to advantage of directors?

We can blame TO 100% for the failure of Alda. Through his arrogance, and incompetence, he destroyed what could have been a great Canadian success story.

Thanks, so sounds like more process .... can they meet requirements? how it will shake out? may or may not be rhetorical Qs

Grace4......according to the TSX rules:

Reinstatements

3.4 Generally, reinstatement of trading will not be automatic upon the Issuer having remedied the deficiency which gave rise to the halt or suspension, as the Issuer will be required to make a request to the Exchange for any such reinstatement.

3.5 An Issuer whose Listed Shares have been halted or suspended for up to 10 business days can be reinstated for trading if it submits a plan (a “reinstatement submission”) to meet the Continued Listing Requirements in a reasonable period of time and the Exchange is satisfied with the public disclosure of its affairs.

3.6 An Issuer whose Listed Shares have been halted or suspended for between 10 business days and 90 calendar days must make application for reinstatement and demonstrate to the Exchange that it meets the Continued Listing Requirements and is otherwise in good standing before the Exchange will reinstate trading.

3.7 An Issuer whose Listed Shares remain halted or suspended for a period of more than 90 days must meet the following requirements in order to be reinstated for trading:

Any idea why trading remains halted if financials posted?

from Agoracom:

On SEDAR it looks like they have filed their financials, MD&A and quartely reporting requirements and are waiting for regulstor approval and reinstatement to trading status. That is the good new. The not so good news is the financials themselves. The company is not only out of money, but the directors and management, through associated companies loans are putting the co. on life support and racking up Alda's debt. This can only last for so long, and even though it is good to see them personally become invested with the co. we need something epic to pull us out of this nosedive. I am amazed in reading on another forum that Terry was shocked to see that even though they got good feedback on their product that they saw sales fall. I suppose he missed classes in Marketing 101, because really it is not always about who has the best product. Just read about the VHS vs BETA story.

Unfortunately, unless shareholders have something good to hear in terms of future revenue, we will see a mass exodus once trading resumes.

This is a typical kind of excuse from this guy. His incompetence or was it intention to build Alda has been the real factor all along culminating with the Olympic disaster. I've been saying this for years, and you as well as others criticized me many times. Now do you see why I was so pissed off? When he had the ability to make any serious progress, he did nothing. In early 2008 when sp was going up daily he put out the NRs fast and furious. That was all P&D BS, and when the dump came I'm convinced it was TO and the others at the front of the selling line. I believe he blamed it on the shorting at the time. His "market conditions" statement has been his ongoing fallback ever since. Not surprising he said it again in his response to your email.

Anyway I knew it would eventually come to this, although I always felt that something would break, considering the quality of the product, and the intellectual property. I thought, and prayed for a buy-out from maybe J&J for example. Maybe it's still not too late for that, but as long as TO is making the decisions I won't hold my breath.

R.I.P. Alda...

Still halted, guess that's about it. Sad indeed, and I don't except any of TO's lame excuses. They got they're big break 2 years ago with the Olympics, and they totally blew it.

Investment Industry Regulatory Organization of Canada - Trading Halt - ALDA PHARMACEUTICALS CORP - APH

3 hours ago - ACQUIREMEDIA

VANCOUVER, Nov. 7, 2011 /CNW/ - The following issues have been halted by Investment Industry Regulatory Organization of Canada (IIROC):

Issuer Name: ALDA Pharmaceuticals Corp

TSX-V Ticker Symbol: APH

Time of Halt: 8:33 E.S.T.

Reason for Halt: Cease Trade Order

Ok who sells 5000 shares at say 0.015 profit? If my math is right, that would be $75.00 before fees. If someone is trying to recoup their losses, it will take a hell of a long time at that rate! :)

Well I certainly plan on keeping in touch with him; and I am intrigued by his comment about "We are working on arrangements for ALDA that will bring the most benefit to shareholders in these terrible economic times." Not sure what that means; but I will be staying tuned and hoping for the best for all of us. I may even buy some more if I start to see a steady improvement in the volume. Have a good evening and I hope the turmoil down under is not causing you much pain. Go "Occupy Wall Street" Go! :)

woodstock...... 259,000 ALDA bought today- now .035- Maybe you should have emailed him earlier... :)

This is in answer to another email that I sent today concerning a question that I forgot to ask in my earlier email. This was from his gmail account.

Hello #####.

Due to the disclosure rules for public companies, we cannot provide specific information that is not already disclosed. It was particularly difficult for us to see our sales of the hand sanitizer drop from nearly a $1 million in one quarter to virtually zero particularly when everyone who uses the product likes it so much better than competing products. This experience is like a death in the family and it has been very hard on me personally and financially. We are working on arrangements for ALDA that will bring the most benefit to shareholders in these terrible economic times. As I commented in my earlier e-mail, I have been through tough times before but I have never seen such a simultaneous collapse of sales of a product line and the stock market.

As for Seavan, we still have an agreement in place but due to the market, it is obviously on hold.

Regards,

Terry Owen

woodstock...... Thanks for posting that..... I believe Dr Owen, in that these are the most difficult times(especialy) for small cap stocks- Nobody has any money to throw at these companies- If thses is any cash, it is on the sidelines- I haven't posted much on my board for awhile, because there is not much to post- Every chart I look at is a disaster- Indivuduals, businesses, investors, banks, are holding(tightly) onto their cash- everyone sees more bad times ahead, before it all turns around- (hopefully, starting Nov, 2012, here in the US)- One effect of these harsh economic times, is the increase in scams, rip-offs, pump and dumps to the max-

I actually think that ALDA can still have success with their products- but not for another couple years at least, if they can hang on-

I will not post my email to Dr Owen suffice to say that it was rather harsh; but below was his answer, and I can only say that it was good of him to reply.

Your e-mail below was passed on to me. I have responded to both e-mail addresses provided.

We can only report news as it happens, such as the recent announcement about the new NPN for hydrocortisone ointment.

As disclosed in recent quarterly reports, the market for hand sanitizers, which had been our main source of revenue during the 2010 fiscal year, dropped unexpectedly and precipitously during 2011. Other producers have faced the same problem.

The global financial turmoil has affected small cap companies particularly severely, even those in the gold sector. This has led to lower share prices and a shortage of capital.

The company has developed a significant portfolio of intellectual property and we are working very hard on pulling the company through these difficult times and are seeking to regain value for shareholders from this asset.

Having been in public companies since 1987, I can comment that the these are the most difficult times that I have seen despite having survived many previous downturns.

Regards,

Terry Owen

--

Full contact info:

Terrance G. Owen, Ph.D., M.B.A.

President & CEO

ALDA Pharmaceuticals Corp.

(APH:TSX-V, OTCBB:APCSF)

170 - 4320 Viking Way

Richmond, BC V6V 2L4

604-521-8300 Ext. 207 Phone

604-521-8322 Fax

1-866-521-ALDA (2532)

owen.terrance@gmail.com

www.aldacorp.com

Thanks for that. Let's hope that maybe something good will happen sooner than later, because I think hope is all that's left.

The shareholders, I believe own part of the intellectual property..... their press releases always stated that ALDA received the patents..... Unfortunately, all things considered, the market is valuing the shares at .02 right now....

Surf, it wouldn't surprise me in the least if they sell off all the intellectual property leaving shareholders in the cold. Any thoughts...

All I can say is I wish I never heard of this POS. Not having the luxury of knowing the real story we can only spectulate, but if it ever comes out I'd say it's been a liteny of mistakes, combined with incopetence, arrogance, and dishonesty by this bush league management. I've been saying this all along, as you well know, but somehow I held on to a flicker of hope that somehow things would eventually turn around.

I can only therefore feel at this point that as Alda Pharma slowly sinks into the abyss, these %^&* will for once think of the shareholders, who have bourne the brunt of Alda management's inability, or maybe even intent to do the right thing, and pursue a vigoris effort to find a party with the where-with-all to get the company on it's feet someday.

If in fact all the intellectual property does exist that we've been led to believe, then with a good shot of $ and a talented marketing team, this should not be an impossible task.

At this point, you would need to get a psychic's opinion, to read TO's mind on this..... without financing, seems like a "done" deal..... That being said, the products and patents have some value, if anyone is interested.....

Surf, any thoughts? I guess it's all over. What a shame.

Surf, for Alda I agree it's the end, but it ain't well. Aed sorry to say, but it should be no surprise that I do have hard feelings towards the CEO.

Thanks, I wrote to DB.

Well, I can accept that "modification"........ I also have always liked "all's well that ends well"..... I have no ill will towards the ceo.....

No, I'm afraid nothing positive to offer about the corp or its executive. And I've modified the old adage "if you can't say anything nice, don't say anything at all" to "say as little as possible, without misleading."

|

Followers

|

26

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

4094

|

|

Created

|

08/07/04

|

Type

|

Free

|

| Moderators | |||

INVESTMENT SUMMARY

- Received a Drug Establishment License ("DEL") and approvals from Health Canada for 30 of its 49 prescription generics products; already has manufacturing approved, labeling and packing secured, and is establishing a sales force 1Q15 salesforc

- Simple business model: Vanc sources drugs that have already obtained FDA equivalent approvals through affiliated companies in China and India, in exchange for manufacturing rights when the drugs are approved by Health Canada

- Potential to scale quickly, comparable to another Canadian company, Paladin Labs, that got bought out for $1.6 billion in 2013 by Endo Health (NASDAQ:ENDP)

- CEO, Arun Nayyar has an extensive track record in the industry - specifically generics - having held executive positions with pharma companies in Latin America, Asia, and Canada and played an instrumental role opening up new markets abroad

- Pre-revenue, albeit with all of the components in place to immediately impact the generics market in Western Canada, and unlock shareholder value through a number of visible, value-unlocking events throughout 2015

Between 2010 and August 2013, brand-name drugs with sales totaling $6 billion a year in Canada lost their patent protection - opening the door to far cheaper generic copies, according to the IMS Brogan market-research company.

Compounding the so-called "patent cliff," a growing list of insurance companies that manage private, workplace drug plans have recently made substituting generics for brands a mandatory policy - a step that most government plans took years ago. The result: more then two thirds of prescriptions in Canada are now filled with generics, while some brand manufacturers lack new drugs in the pipeline to take up the slack.

COMPANY OVERVIEW

Vanc Pharmaceuticals Inc. ("Vancpharma") (OTCQB: NUVPF) is a Canadian company (TSX-V: NPH) focused on providing Canadian health care professionals and consumers with high quality, affordable generics and over-the-counter ("OTC") healthcare products. They are the first Canadian generics company in Western Canada.

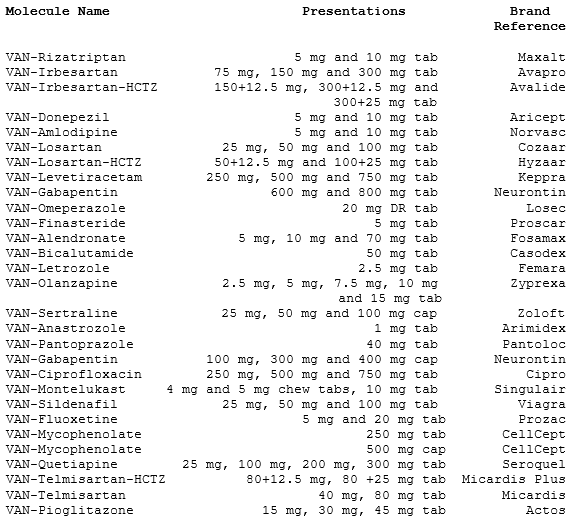

GENERICS PORTFOLIO

The company's currently approved in-licensed generics portfolio consists of 30 molecules, comprising of 67 dosage forms across various therapeutic categories: including both chronic (long-term) therapy and acute (short-term) therapy. Management estimates that the aggregate annual Canadian sales of its 30 approved products represents "a $1-billion market opportunity". Furthermore, the company plans to launch "with additional products and we will provide further updates in the coming months," said Arun.

The generics division of the company was only launched last Spring, since then the new management team has reached a number of significant milestones including:

On April 15th, 2014 Vancpharma announced that it had signed Cross Referencing Agreements ("CRA") "for prescription generic products for Canadian markets. These agreements are with three large pharmaceutical companies and cover 48 prescription generic products. The suppliers will handle manufacturing, and Vancpharma will market and sell these new product lines under its own label.

On November 18th, 2014 the company received approval via a Notice of Compliance ("NOC") from Health Canada for 22 generic molecules, comprising 51 dosage forms.

On December 10th, 2014 the company announced that it had been issued a drug establishment licence ("DEL") (licence No. 102220-A) by Health Canada. "The issuance of a drug establishment licence, along with the approval of our partner's GMP manufacturing site, is a key step towards the commercialization of our generic drug portfolio," said Arun Nayyar, CEO. The licence allows Vancpharma to import pharmaceutical products and distribute them within Canada.

This news was particularly important for the company and shareholders because: it positioned Vancpharma to become one of the only 40 companies in Canada that are licensed to manufacture current and future drugs at its GMP facility; allows Vancpharma to import from other manufacturers across the world and faces less barriers to entry; allows for importing both generic and non-generic drugs thus allowing the company to compete with other companies in branded drugs as well as their core generics business; and adds major clout when negotiating for exclusivity rights across Canada. Previously, manufacturers wouldn't commit their exclusively to Vancpharma as they were unsure if it could make good on importing and selling their products.

On December 15th, 2014 the company received an NOC from Health Canada for 7 additional generic molecules, comprising 15 dosage forms.

Lastly, on January 14th, 2015 Vancpharma placed inventory purchase orders for 30 generic molecules and expects to deliver these products 2Q 2015. "We are excited to take this important step towards commercialization and look forward to launching sales in Q2 2015. These 30 molecules represent best-selling generics in the Canadian market and our aim to provide Canadians with quality and cost-effective products is well served by them," said Arun. "Our initial marketing and outreach activities with select pharmacy customers in Western Canada have been positive and we look forward to working with our partners."

Figure 1: Generics Portfolio

Source: Press Release/Company Website

*Note: I'm aware that's only 29, however the 30th hasn't been updated on the website although it's been mentioned as approved (new approvals could come at any time)

Here are the next steps with the generics portfolio:

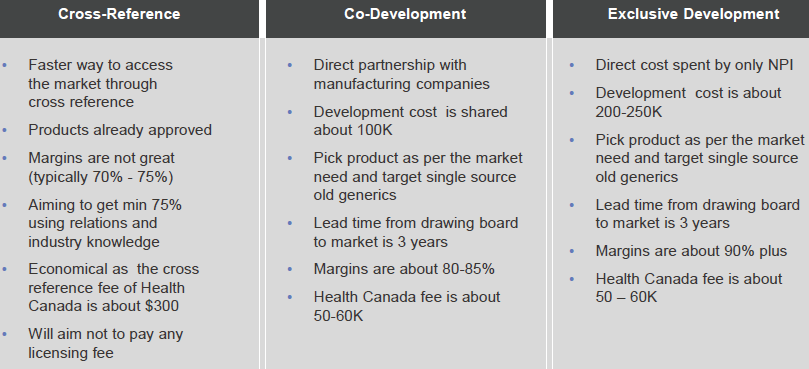

Figure 2: Generics Through Global Partnership

For those wondering what Vancpharma's margins are, the company has not made that public yet. As you can imagine, they don't want to expose their margins for specific drugs too early. Investors will be able to see them in the financial statements at a later date. However, generics are quite lucrative. Vancpharma will be taking on the risk of inventory, licensing, approvals, sales and marketing, whereas the manufacturer takes and fills an order from Vancpharma as necessary and collects payment. Accordingly, the reward follows the risk and in this case, Vancpharma would pay a fixed price to the manufacturer depending on the size of the manufacturing run. If you look at the financials of another generics company, Biosyent (TSX-V: RX) you will see margins typically ~70%-75%.

The margins generated from strategic cross-reference partnerships, while very enticing, pale in comparison to the financial opportunities presented by exclusive or co-development partnerships which management has indicated they want to pursue in the future.

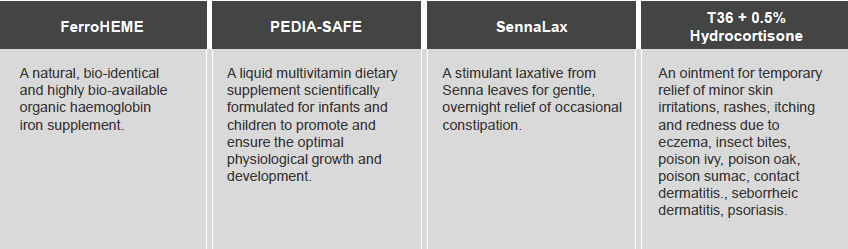

OTC PRODUCTS

The OTC Products Division is focused on the marketing and sales of novel and proprietary healthcare products and consists of four (4) such products, all of which now have a Natural Product Number.

Figure 3: Vancpharma Pharmaceuticals OTC Products

It can't and won't be the cash cow for Vancpharma like its generics portfolio - the Canadian market for these OTC products is only ~$60-70 million - but it should actually start generating revenue sooner. Manufacturing should commence in January, with the first sales hopefully starting to come sometime during March.

Looking ahead at the future pipeline of OTC products, they include nutraceuticals, vitamin supplements, and skin care products.

MANAGEMENT

The team has extensive experience and expertise that spans across various functions such as research, development, manufacturing, and marketing of generics and OTC health care products in the global pharmaceuticals industry. This understanding of industry best practices and strong insight allows the company to identify emerging trends in medicine and the marketplace.

The secret to being able to license so many drugs within such a short period of time, less than a year after being restructured is CEO, Arun Nayyar.

Arun only joined the company November 25th, 2013, but came with an extensive track record in the industry - specifically generics - having held executive positions with pharmaceutical companies in Latin America, Asia, and Canada. He has been instrumental in opening up new markets abroad, and domestically his accomplishments include Director, Business Development and International Sales for Shoppers Drug Mart ("SDM"), and consulting for Sanis Healthcare, George Weston Ltd. (Loblaws group), and SDM. To have a more extensive look at Arun's resume and job history, you can view his LinkedIn here.

Some information that you won't find on LinkedIn is that he's an owner of a few Shoppers Drug stores in the Vancpharmaouver area, and also has deep-ties, and solid connections in India. This helps to secure licensing of the generics in exchange for manufacturing rights when Health Canada approves the products.

The newest hire, replacing Jamie Lewin as director and CFO and announced December 3rd, 2014 was Aman Parmar. "I look forward to working with the team at Vancpharma Pharmaceuticals and am impressed by how far they have progressed with limited capital," said Mr. Parmar. "Capital efficiency and creating shareholder value will be my primary focus at Vancpharma." Since joining Vancpharma, Aman has purchased 135,000 shares on the open market ranging from 19 to 24 cents - clearly indicative that he believes the company is undervalued at these levels.

Given the fact that the company is ramping up its business, they've already started putting together a sales and marketing team, it wouldn't surprise me if another executive was brought in to help.

You can read more about the entire Vancpharma team by clicking this link (note, this page needs to be updated with Jamie/Aman).

FINANCIALS

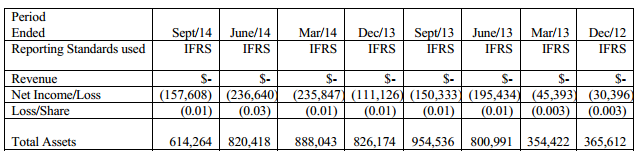

Although Vancpharma is a pre-revenue company, I see a multiple number of visible, value-unlocking events through 2015 that can meaningfully impact stock performance.

Figure 4: Summary of Quarterly Results

Source: MD&A

The company closed an oversubscribed, non-brokered private placement for gross proceeds of $1,141,000 by issuing 7,607,332 units at $0.15/unit on December 11th, 2014. "This round of funding enables us to move our portfolio of generic drugs and OTC products into commercialization," said Arun Nayyar. "Specifically we will be acquiring generic drug inventory and building our sales team to target pharmacy customers."

The company is financed for the time being, but may have to do another round in March depending on how the roll-outs are going, and for general working capital purposes. If so, I'm sure that it would be strategic - I would think at least >$0.20, comprised primarily by sophisticated retailers and brokers, and it would not be a raise of much more than $1 million. Management only wants to raise whatever money they believe is necessary right now because they know as soon as the company starts generating revenue that its valuation has easily be many multiples of where it sits today.

SHARE STRUCTURE

Shares outstanding: 44,374,407

Stock Options: 3,975,000

Warrants: 16,212,252

Fully Diluted: 64,561,659

Major shareholders of the company, and percentage owned include:

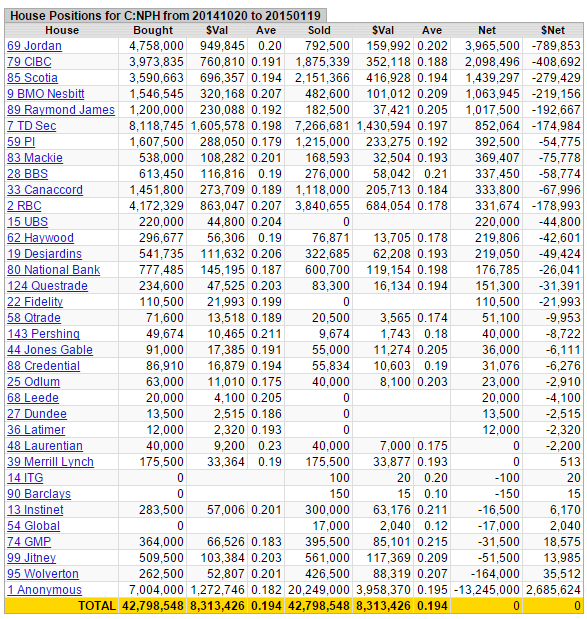

It's a tight share structure, the 'effective' float is ~9 million shares - much less than what's been traded the past few months - 42,798,548 shares at an average price of $0.194:

Figure 5: House Positions

Source: Stockwatch

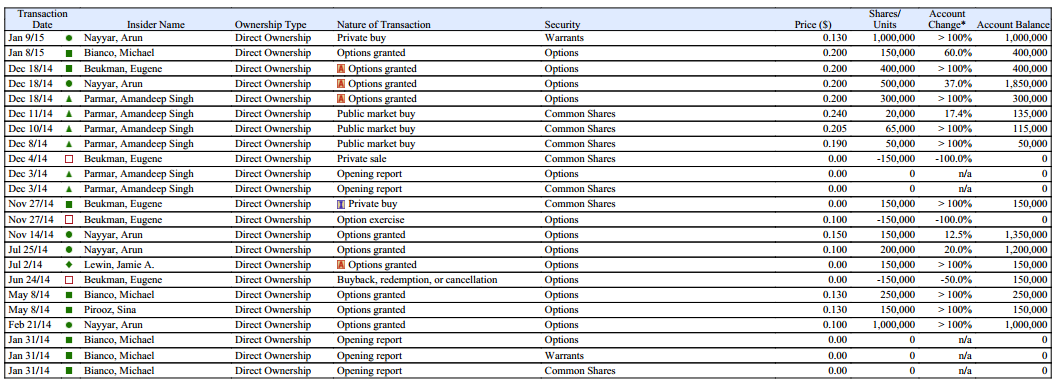

Figure 6: Management Insider Filings

Source: TD

REVENUE RAMP/VALUATION

It's a little early for me to try and assign a valuation, or forecast revenue and earnings for the company, however I anticipate doing so before year-end. The company hasn't informed investors of the specific margins and obviously we don't know the adoption rate because we don't know how good the sales team will be. Take a look at this article though, "The Top 11 Fastest-Growing Generis Companies", when compared some of the other generics companies, Vancpharma looks very undervalued based solely off of its standing drug portfolio.

The two best examples that come to my mind are: Paladin Labs and BioSyent (OTCPK:BIOYF).

Former pharma sales rep., and Cantech Letter contributor Hogan Mullally wrote that Paladin "became the poster child for Canadian specialty pharma. They built a remarkably successful business by acquiring the Canadian rights to a wide variety of drugs. These drugs were either too small for medium/big pharma, or were developed by a company without a Canadian commercial footprint, whatever the reason, Paladin was able to amass an eclectic and diverse portfolio of prescription and OTC drugs for the Canadian market. Through their "sum of the parts" strategy, Paladin grew to over $200 million in annual sales and in 2013 was acquired by Endo Pharmaceuticals for approximately $1.6 billion.

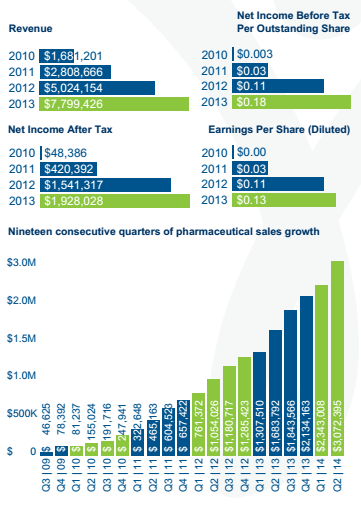

BioSyent is in between Vancpharma and Paladin, as it has already amassed an impressive portfolio by searching the globe to in-license or acquire innovative pharmaceutical products for the Canadian market. It too focuses on products that are too small for medium/big pharma, and have a competitive angle that can be exploited by a modest sales force. BioSyent's business model is structured to minimize risk, and to produce high growth. For the four years ended December 31, 2013 the company experienced a CAGR of 67% while consistently growing profits:

Figure 7: BioSyent Financials at a Glance

Source: Fact Sheet

There is an exit strategy for the company and shareholders - take-out target for an M&A transaction. It might take getting into a few hundred pharmacies, but the precedent has already been set. The initial adoption rate risk is reduced from the outset because between members of the management team, they own a little more than a dozen pharmacies. Not to mention now that Health Canada has granted the company a Drug Establish License it can pursue additional revenue opportunities and further de-risked the investment.

RISKS

Vancpharma is still considered an early stage company, as such there are a number of risks associated with making an investment at this point in time, including but not limited to:

(1) The company just hired a new CFO, and has a management team has dozens of years of business experience, most dealing with generic pharmaceuticals.

(2) The company plans to manufacture its products at four certified GMP pharmaceuticals factories in Canada, India and China. These U.S. FDA approved plants are capable of manufacturing a wide range of Generic Pharmaceuticals and OTC Health care products at these facilities, under the VANCPHARM label.

(3) Like I mentioned before, management controls a number of pharmacies which will de-risk the rollout process and immediately start generating revenue form the company's generics portfolio.

(4) Arun has built deep, extensive relationships in India and China, and has a lot of ideas to add more products to the portfolio (not to mention the future potential to co-development or development exclusively).

(5) The company sources its products from big products that are already approved by either the U.S. FDA or UPHRA, and also approved by Health Canada. As long as the company is in compliance with Health Canada guidelines then the ANDS application gets expedited, updated and faster tracked. The company hasn't had so much of a hiccup yet, because of the experienced team in place filing all of the paperwork.

(6) The company hasn't had an issue raising money despite the poor market for companies trading on the TSX Venture. The last PP was oversubscribed, and the shares were spread around to strong, strategic hands. Presuming management continues to achieve its milestones, I anticipate lots of eagerness for the next round.

CONCLUSION

Vancpharma set forth some ambitious goals, but has already accomplished so much in such a short amount of time that I really have large aspirations for it (and shareholders).

The company has a tried and tested business model which is simple to understand. Vancpharma enters into Cross-Referencing agreements with affiliated companies whom source products from China and India which are already approved, in exchange for manufacturing rights when the drugs are approved by Health Canada. This is very economical as there is a minimal cross-referencing fee paid to Health Canada, and a very large market opportunity (>$1 billion for current generics portfolio), with margins typically ~70%-75%.

Source: StockCharts.com

Taking a look at recent trading, there has been some healthy consolidation after the initial big run-up, ~33% off its 52-week high. MACD and RSI indicators are now in 'oversold' territory, and the stock is approaching its 200-day moving average. Up until a few months ago this stock traded 'by appointment only'. Since the middle of October, 42,798,548 shares at an average price of $0.194 have traded.

Now that the company has received 30 of its 49 Health Canada approvals (with the rest to be submitted shortly), there is a bit of work that needs to be done in order advance it from being a purely speculative growth biotech with Health Canada approvals, to one that's one being noticed by institutions and an American audience.

In the meantime, investors have two options: (1) buy now, taking the risk knowing that the company may need to finance further, but is extremely close to generating revenue; or (2) sit on the sidelines and wait until the second quarter financials are released, and make a decision then.

The latter is much less risky, however if management successfully executes on its business plan and stays on track with milestones, then I'm sure its share price will reflect it this, and it will be at a significant premium.

Bottom line, I think that there is a very compelling opportunity to invest right now given: (1) the recent pullback in share price; (2) the significance of forthcoming news releases to act as catalysts to unlock shareholder value; (3) management's achievements to date and their track record to deliver results; (4) market opportunity (>$1 billion on current portfolio) and attractive valuations of sector peers; and (5) lack of competition in the Western Canadian generics market and the opportunity to generate imminent revenue.

(For additional liquidity, NUVPF. trades in Canada on the TSX Venture as "NPH". 3-month average volume 637,531 shares/day.)

Please feel free to comment below or send me an inbox message if you have any questions or comments about this article.

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |