News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

>>> Southwest Airlines reinstates dividend, sees strong travel demand

Reuters

December 7, 2022

https://news.yahoo.com/southwest-airlines-reinstates-quarterly-dividend-115829890.html

(Reuters) -Southwest Airlines Co on Wednesday became the first major U.S. airline to reinstate its quarterly dividend, more than two years after suspending it in the wake of the coronavirus pandemic.

U.S. airlines have benefited from pent-up demand for leisure trips and a gradual return of lucrative business travel, helping them post strong quarterly earnings despite worries of an economic slowdown.

"Our fourth-quarter 2022 outlook remains strong, and we have a solid plan for 2023," Chief Executive Officer Bob Jordan said in a statement.

In a regulatory filing ahead of its investor day on Wednesday, Southwest said it was expecting "strong leisure revenue trends" to continue into the first quarter of next year, while business travel was expected to improve.

The carrier also trimmed its fourth-quarter fuel cost forecast by about 5 cents per gallon, compared with its previous estimate.

Southwest declared a third-quarter dividend of 18 cents per share, the same level at which it was prior to the pandemic. The dividend will be paid on Jan. 31.

The airline did not detail any stock buyback plans, which have been fiercely opposed by unions, who have asked U.S. airlines to focus on investing in their workers and fixing operational issues.

As part of the federal COVID-19 relief package, airlines had been prohibited from buying back their shares. The ban, however, expired on Sept. 30.

<<<

---

>>> U.S. Congress averts railroad 'Christmas catastrophe,' Biden says

Reuters

December 1, 2022

By David Shepardson and Moira Warburton

https://finance.yahoo.com/news/1-biden-administration-makes-case-184803591.html

WASHINGTON, Dec 1 (Reuters) - Congress gave final approval to a bill blocking a national U.S. railroad strike that could have devastated the American economy but rejected a measure that would have provided paid sick days to railroad workers.

The U.S. Senate voted 80 to 15 on Thursday to impose a tentative contract deal reached in September on a dozen unions representing 115,000 workers, who could have gone on strike on Dec. 9.

The bill now goes to President Joe Biden, who will sign it into law. Once the bill becomes law, any strike would be considered illegal and the strikers could be fired.

Eight of 12 unions have ratified the deal. But some labor leaders have criticized Biden, a self-described friend of labor, for asking Congress to impose a contract that workers in four unions have rejected over its lack of paid sick leave.

"We have spared this country a Christmas catastrophe in our grocery stores, in our workplaces, and in our communities," Biden said in a statement that praised Congress for acting to avoid devastating economic consequence for workers' families.

A rail strike could have frozen almost 30% of U.S. cargo shipments by weight, stoke already surging inflation, cost the American economy as much as $2 billion a day and stranded millions of rail passengers.

The U.S. House of Representatives approved the bill to block a strike on Wednesday and separately voted to require seven days of paid sick leave for rail workers.

Paid sick leave was one of the outstanding issues in the negotiations. There are no paid short-term sick days under the tentative deal after unions asked for 15 and railroads settled on one personal day.

Teamsters President Sean O'Brien harshly criticized the Senate vote on sick leave. "Rail carriers make record profits. Rail workers get zero paid sick days. Is this OK? Paid sick leave is a basic human right. This system is failing," O'Brien wrote on Twitter.

The measure to provide seven paid sick days did not win the required 60-vote supermajority in the Senate and was not endorsed by the White House.

A total of 52 senators, including 44 Democrats, two independents and six Republicans voted to mandate sick leave for rail workers, while 42 Republicans and Democratic Senator Joe Manchin voted against it saying he was sympathetic to workers' concerns but said Congress should not "renegotiate a collective bargaining agreement that has already been negotiated."

CONGRESSIONAL POWERS

Congress invoked its sweeping powers to block strikes involving transportation - authority it does not have in other labor disputes - because of the significant impact a rail stoppage could have on the U.S. economy, especially at the height of the holiday shopping season.

The Senate earlier on Thursday rejected a proposal by Senator Dan Sullivan to extend the cooling-off period by 60 days to allow for further negotiations.

Biden has praised the proposed contract, which includes a 24% compounded pay increase over five years and five annual $1,000 lump-sum payments, and he had asked Congress to impose the contract without any modifications.

American Association of Railroads CEO Ian Jefferies praised the vote.

"None of the parties achieved everything they advocated for" Jefferies said in a statement and added "without a doubt, there is more to be done to further address our employees’ work-life balance concerns."

Without the legislation, rail workers could have gone out next week, but the impacts would be felt as soon as this weekend as railroads stopped accepting hazardous materials shipments and commuter railroads began canceling passenger service.

U.S. Chamber of Commerce CEO Suzanne Clark praised "Congress for averting a catastrophic rail strike" and called it "a win for our country."

Senator Bernie Sanders and others denounced railroad companies for refusing to offer paid sick leave.

"They are maybe the worst case of corporate greed that I have seen," Sanders said. "That is really barbaric in the year 2022 in America."

The contracts cover workers at carriers including Union Pacific, Berkshire Hathaway Inc's BNSF, CSX , Norfolk Southern Corp and Kansas City Southern.

<<<

---

>>> Skyworks and MediaTek Collaborate to Offer End-to-End 5G Automotive Solutions

BusinessWire

November 13, 2022

https://finance.yahoo.com/news/skyworks-mediatek-collaborate-offer-end-040200548.html

MediaTek and Skyworks Develop 5G New Radio Design Enabling Seamless Integration With Automotive Communications Systems

MUNICH, November 14, 2022--(BUSINESS WIRE)--Skyworks Solutions, Inc. (Nasdaq: SWKS) today announced that the company has engaged with MediaTek to offer a complete modem-to-antenna automotive-grade 5G solution. This 5G New Radio Sky5A RF front-end solution will accelerate the deployment of this cutting-edge protocol across an array of automotive OEM and consumer service offerings.

"The rollout of 5G is reshaping the automotive market with a variety of safety and entertainment telematics applications to improve the driving experience," said Martin Lin, deputy general manager of the Wireless Communications Business Unit at MediaTek. "Through this collaboration with Skyworks, MediaTek is providing OEMs and automotive customers a complete solution that offers high performance, reliability and flexibility to meet the growing demands for bandwidth and advanced connectivity in next-generation vehicles."

As automotive OEMs create entirely new vehicle platforms with cutting-edge processing and sensing capabilities to support advancements in electric vehicle (EV) technology, driver-assistance systems (ADAS), and artificial intelligence, they are looking for solutions that can support the expanded data and connectivity demands of these next-generation innovations.

"This strategic initiative allows Skyworks and MediaTek to address the stringent requirements of the global automotive industry," said John O’Neill, vice president of marketing at Skyworks. "Our combined engineering expertise enables our customers to innovate new vehicle communication architectures, with the confidence that their designs will continue to meet future bandwidth needs and the rapid evolution of global wireless networks."

The 5G NR Sky5A RF front-end complete solution was designed for automotive applications, supporting 3GPP R15 and R16 standards, bandwidth exceeding 100MHz, flexible antenna architectures, regional optimization, aux ports to support the addition of future bands, and full automotive grade reliability qualification.

Skyworks will be exhibiting at Electronica Stand B5-138, taking place in Munich from Nov. 15-18, 2022, where the company will be highlighting its latest infrastructure, IoT, automotive, timing and power solutions.

About Skyworks

Skyworks Solutions, Inc. is empowering the wireless networking revolution. Our highly innovative analog and mixed signal semiconductors are connecting people, places and things spanning a number of new and previously unimagined applications within the aerospace, automotive, broadband, cellular infrastructure, connected home, defense, entertainment and gaming, industrial, medical, smartphone, tablet and wearable markets.

Skyworks is a global company with engineering, marketing, operations, sales and support facilities located throughout Asia, Europe and North America and is a member of the S&P 500® and Nasdaq-100® market indices (Nasdaq: SWKS). For more information, please visit Skyworks’ website at: www.skyworksinc.com.

<<<

---

>>> O'Reilly Automotive, Inc. (ORLY), together with its subsidiaries, operates as a retailer and supplier of automotive aftermarket parts, tools, supplies, equipment, and accessories in the United States. The company provides new and remanufactured automotive hard parts and maintenance items, such as alternators, batteries, brake system components, belts, chassis parts, driveline parts, engine parts, fuel pumps, hoses, starters, temperature control, water pumps, antifreeze, appearance products, engine additives, filters, fluids, lighting products, and oil and wiper blades; and accessories, including floor mats, seat covers, and truck accessories. Its stores offer auto body paint and related materials, automotive tools, and professional service provider service equipment. The company's stores also provide enhanced services and programs comprising used oil, oil filter, and battery recycling; battery, wiper, and bulb replacement; battery diagnostic testing; electrical and module testing; check engine light code extraction; loaner tool program; drum and rotor resurfacing; custom hydraulic hoses; and professional paint shop mixing and related materials. Its stores offer do-it-yourself and professional service provider customers a selection of products for domestic and imported automobiles, vans, and trucks. As of December 31, 2021, the company owned and operated 5,759 stores in the United States, and 25 stores in Mexico. O'Reilly Automotive, Inc. was founded in 1957 and is headquartered in Springfield, Missouri.

<<<

---

O'Reilly Automotive - 3 Top E-Commerce Stocks to Buy Right Now

Motley Fool

By Bradley Guichard

Mar 27, 2022

https://www.fool.com/investing/2022/03/27/3-top-e-commerce-stocks-to-buy-right-now/?source=eptyholnk0000202&utm_source=yahoo-host&utm_medium=feed&utm_campaign=article

Let's start with an unconventional e-commerce company. O'Reilly Automotive ( ORLY 1.54% ) probably isn't the first name that pops into your head when it comes to online shopping. However, its growth strategy has an omnichannel focus. Professional service providers can now place orders and receive local delivery with O'Reilly's proprietary platform made just for them. At the same time, DIY customers can do the same through the company's website.

O'Reilly could also capitalize on the enormous inflation we see in the new and used car markets. Gone are the days of haggling with the dealer for a deal well below the manufacturer's suggested retail price (MSRP). Instead, new car buyers are getting sticker shock. Thanks to dwindling inventories and the rising cost of new cars, used car prices have been up more than 40% over the past year. As a result, it's a good bet many drivers will be holding on to their vehicles longer, and the demand for parts from both professional service providers and DIY car owners will remain strong.

The company is already posting impressive results with revenue increasing to $13.3 billion in 2021, up 15%. The company's diluted earnings per share (EPS) also increased 32% to reach $31.10 last year. That was due in part to the company's lucrative share buyback program, which totaled nearly $2.5 billion in 2021 alone. O'Reilly stock has gained over 40% in the past year, and the company is set up to continue its impressive run long term.

<<<

>>> Top Railroad Stocks for Q1 2022

CP, CNI, and GBX are top for value, growth, and momentum, respectively

Investopedia

By MATTHEW JOHNSTON

February 01, 2022

https://www.investopedia.com/investing/railroad-stocks/

The railroad industry is one of the major components of the transportation sector and is closely tied to the economy's growth. Railroad companies operate vast networks that transport agricultural products, packaged foods, commodities, electronics, and other goods to companies and consumers. Major companies in the industry include Union Pacific Corp. (UNP), Norfolk Southern Corp. (NSC), and CSX Corp. (CSX).

The railroad industry does not have its own benchmark, but as a part of the broader transportation sector, its performance can be reasonably approximated by the iShares Transportation Average ETF (IYT). IYT has underperformed the broader market with a total return of 20.6% over the past 12 months, below the Russell 1000's total return of 23.0%.1 These performance figures and all others below are as of Jan. 11, 2022.

Here are the top 3 railroad stocks with the best value, the fastest growth, and the most momentum.

Best Value Railroad Stocks

These are the railroad stocks with the lowest 12-month trailing price-to-earnings (P/E) ratio. Because profits can be returned to shareholders in the form of dividends and buybacks, a low P/E ratio shows you’re paying less for each dollar of profit generated.

Best Value Railroad Stocks

Price ($) Market Cap ($B) 12-Month Trailing P/E Ratio

Canadian Pacific Railway Ltd. (CP) 74.75 49.9 20.2

CSX Corp. (CSX) 36.30 80.5 22.8

Canadian National Railway CO. (CNI) 122.28 86.4 23.3

Canadian Pacific Railway Ltd.: Canadian Pacific Railway is a Canada-based company that offers rail transportation services, including intermodal shipping, rail siding construction, and logistics services. The company announced in mid-December that it has completed its acquisition of Kansas City Southern (KSU), a cross-border railroad between the U.S. and Mexico, for approximately $31 billion. The shares of Kansas City Southern were placed in a voting trust upon the close of the acquisition, ensuring that the railroad operates independently of Canadian Pacific until the U.S. Surface Transportation Board makes a decision on the companies' joint railroad control application. The board's review of Canadian Pacific's proposed control of Kansas City Southern is expected to be finalized during the fourth quarter of 2022.2

CSX Corp.: CSX is a transportation company that provides rail, intermodal, and rail-to-truck transload services and solutions. It serves customers in a variety of markets, including energy, industrial, construction, agricultural, and consumer products.

Canadian National Railway Co.: Canadian National Railway is a Canada-based transportation company that offers fully-integrated rail and other transportation services, including intermodal, trucking, freight forwarding, warehousing, and distribution.

Fastest Growing Railroad Stocks

These are the top railroad stocks as ranked by a growth model that scores companies based on a 50/50 weighting of their most recent quarterly YOY percentage revenue growth and their most recent quarterly YOY earnings-per-share (EPS) growth. Both sales and earnings are critical factors in the success of a company.

On Nov. 15, 2021, President Biden signed into law the Infrastructure Investment and Jobs Act, which will invest approximately $550 billion in America's roads and bridges, water infrastructure, resilience, internet, and more. Of this $550 billion, $66 billion will be allocated to improving America's passenger and freight rail system.3

Therefore ranking companies by only one growth metric makes a ranking susceptible to the accounting anomalies of that quarter (such as changes in tax law or restructuring costs) that may make one or the other figure unrepresentative of the business in general. Companies with quarterly EPS or revenue growth of over 2,500% were excluded as outliers.

Fastest Growing Railroad Stocks

Price ($) Market Cap ($B) EPS Growth (%) Revenue Growth (%)

Canadian National Railway Co. (CNI) 122.28 86.4 81.7 11.5

CSX Corp. (CSX) 36.30 80.5 34.4 24.3

Trinity Industries Inc. (TRN) 30.87 3.0 57.1 9.6

Canadian National Railway Co.: See company description above.

CSX Corp.: See company description above.

Trinity Industries Inc.: Trinity Industries provides rail transportation products and services in North America. It offers railcar leasing and management services, as well as railcar manufacturing and modifications. The company announced in October financial results for Q3 of its 2021 fiscal year (FY), the three-month period ended Sept. 30, 2021. Net income attributable to shareholders rose 27.5% compared to the year-ago quarter. Revenue rose 9.6% YOY. Trinity Industries said that results were adversely impacted by labor shortages, turnover, and disruptions in supply chains, partly due to the economic impact of the COVID-19 pandemic. However, it expects profitability and demand for railcars to continue improving.4

Railroad Stocks With the Most Momentum

These are the railroad stocks that had the highest total return over the last 12 months.

Railroad Stocks with the Most Momentum

Price ($) Market Cap ($B) 12-Month Trailing Total Return (%)

Greenbrier Companies Inc. (GBX) 40.82 1.3 17.2

Union Pacific Corp. (UNP) 246.42 158.4 15.6

CSX Corp. (CSX) 36.30 80.5 14.7

Russell 1000 N/A N/A 23.0

iShares Transportation Average ETF (IYT) N/A N/A 20.6

Greenbrier Companies Inc.: Greenbrier Companies is a supplier of equipment and services to global freight transportation markets. The company designs and manufactures freight railcars and marine barges in North America, Europe, and Brazil. It also provides freight railcar wheel services, parts, maintenance, and retrofitting services in North America. Greenbrier announced in late October the appointment of President and Chief Operating Officer (COO) Lorie Tekorius, to the role of chief executive officer (CEO), effective March 1, 2022. Co-founder, Chairman, and CEO William A. Furman will assume the newly created role of Executive Chair on that same date.5

Union Pacific Corp.: Union Pacific connects 23 states in the western two-thirds of the U.S. by rail. It operates rail transportation services from all major West Coast and Gulf Coast ports to eastern gateways, connects with Canada's rail systems, and serves all six major Mexico gateways. The company announced in December that its board of directors approved a 10% increase in the quarterly dividend on the company's common shares, bringing it to $1.18 per share. The dividend was payable on Dec. 30, 2021 to shareholders of record as of Dec. 20, 2021.6

CSX Corp.: See above for company description.

<<<

>>> O'Reilly Automotive, Inc. (ORLY), together with its subsidiaries, operates as a retailer of automotive aftermarket parts, tools, supplies, equipment, and accessories in the United States. The company provides new and remanufactured automotive hard parts and maintenance items, such as alternators, batteries, brake system components, belts, chassis parts, driveline parts, engine parts, fuel pumps, hoses, starters, temperature control, water pumps, antifreeze, appearance products, engine additives, filters, fluids, lighting products, and oil and wiper blades; and accessories, including floor mats, seat covers, and truck accessories. Its stores offer auto body paint and related materials, automotive tools, and professional service provider service equipment. The company's stores also offer enhanced services and programs comprising used oil, oil filter, and battery recycling; battery, wiper, and bulb replacement; battery diagnostic testing; electrical and module testing; check engine light code extraction; loaner tool program; drum and rotor resurfacing; custom hydraulic hoses; and professional paint shop mixing and related materials. Its stores provide do-it-yourself and professional service provider customers a selection of products for domestic and imported automobiles, vans, and trucks. As of December 31, 2020, the company operated 5,616 stores. O'Reilly Automotive, Inc. was founded in 1957 and is headquartered in Springfield, Missouri.

<<<

>>> CSX Corporation (CSX), together with its subsidiaries, provides rail-based freight transportation services. The company offers rail services; and transportation of intermodal containers and trailers, as well as other transportation services, such as rail-to-truck transfers and bulk commodity operations. It transports chemicals, agricultural and food products, automotive, minerals, forest products, fertilizers, and metals and equipment; and coal, coke, and iron ore to electricity-generating power plants, steel manufacturers, and industrial plants, as well as exports coal to deep-water port facilities. The company also offers intermodal transportation services through a network of approximately 30 terminals transporting manufactured consumer goods in containers; and drayage services, including the pickup and delivery of intermodal shipments. It serves the automotive industry with distribution centers and storage locations, as well as connects non-rail served customers through transferring products from rail to trucks, which includes plastics and ethanol. The company operates approximately 19,500 route mile rail network, which serves various population centers in 23 states east of the Mississippi River, the District of Columbia, and the Canadian provinces of Ontario and Quebec, as well as owns and leases approximately 3,539 locomotives. It also serves production and distribution facilities through track connections. CSX Corporation was incorporated in 1978 and is headquartered in Jacksonville, Florida.

<<<

>>> Old Dominion Freight Line, Inc. (ODFL) operates as a less-than-truckload (LTL) motor carrier in the United States and North America. It provides regional, inter-regional, and national LTL services, including expedited transportation. The company also offers various value-added services, such as container drayage, truckload brokerage, and supply chain consulting. It owns 9,288 tractors and 42 maintenance centers. As of August 3, 2021, it owned 248 service centers. Old Dominion Freight Line, Inc. was founded in 1934 and is based in Thomasville, North Carolina.

<<<

>>> United Parcel Service, Inc. (UPS) provides letter and package delivery, transportation, logistics, and financial services. It operates through three segments: U.S. Domestic Package, International Package, and Supply Chain & Freight. The U.S. Domestic Package segment offers time-definite delivery of letters, documents, small packages, and palletized freight through air and ground services in the United States. The International Package segment provides guaranteed day and time-definite international shipping services in Europe, the Asia Pacific, Canada and Latin America, the Indian sub-continent, the Middle East, and Africa. This segment offers guaranteed time-definite express options. The Supply Chain & Freight segment provides international air and ocean freight forwarding, customs brokerage, distribution and post-sales, and mail and consulting services in approximately 200 countries and territories; and less-than-truckload and truckload services to customers in North America. This segment also offers truckload brokerage services; supply chain solutions to the healthcare and life sciences industry; shipping, visibility, and billing technologies; and financial and insurance services. The company operates a fleet of approximately 127,000 package cars, vans, tractors, and motorcycles; and owns 58,000 containers that are used to transport cargo in its aircraft. United Parcel Service, Inc. was founded in 1907 and is headquartered in Atlanta, Georgia.

<<<

$EXN Excellon Resources Inc., a silver mining and exploration company, acquires, explores for, evaluates, develops, and finances mineral properties in Mexico and Canada. The company primarily explores for silver, lead, zinc, and gold deposits. It holds 100% interests in the Platosa property covering an area of 11,000 hectares located in Durango State, Mexico; the Evolución property that covers an area of 45,000 hectares situated in the states of Durango and Zacatecas, Mexico; and the Silver City Project totaling an area of 164 square kilometers in Saxony, Germany. The company also holds 100% interests in the Kilgore Project that covers an area of 6,788 located in Clark County, Southeastern Idaho; and the Oakley Project covering an area of 2,833 hectares in Oakley, Idaho. Excellon Resources Inc. was incorporated in 1987 and is based in Toronto, Canada.

$IDEX 2021 Earth Day MEG China

$NAK The global rare earth market will grow in value from $8.1 billion in 2018 to more than $14.4 billion by 2025 as demand for electric vehicles, cellphones and other products rise.

$IDEX Ideanomics Mobility is a turnkey solution that provides economic and operational confidence. With a synergistic ecosystem of products and services, we are helping commercial fleets navigate the barriers of electrification across vehicles, charging and energy. From vehicle procurement, to charging infrastructure, to energy management, we are demystifying fleet electrification, and delivering the simplicity and scalability our customers are looking for.? https://ideanomics.com/our-company/

>>> Top Railroad Stocks for Q2 2021

CP.TO, CSX, and GBX are top for value, growth, and momentum, respectively

Investopedia

By NATHAN REIFF

Mar 17, 2021

https://www.investopedia.com/investing/railroad-stocks/?utm_campaign=quote-yahoo&utm_source=yahoo&utm_medium=referral

The railroad industry is one of the major components of the transportation sector and is closely tied to the economy's growth. Railroad companies operate vast networks that transport agricultural products, packaged foods, commodities, electronics, and other goods to companies and consumers. Major companies in the industry include Union Pacific Corp. (UNP), Norfolk Southern Corp. (NSC), and CSX Corp. (CSX).

The railroad industry does not have its own benchmark, but as a part of the broader transportation sector its performance can be reasonably approximated by the iShares Transportation Average ETF (IYT). IYT has outperformed the broader market with a total return of 78.4% over the past 12 months, above the Russell 1000's total return of 53.5%.1 The benchmark figures above and all statistics in the tables below are as of March 15.

Here are the top 3 railroad stocks with the best value, the fastest growth, and the most momentum.

Best Value Railroad Stocks

These are the railroad stocks with the lowest 12-month trailing price-to-earnings (P/E) ratio. Because profits can be returned to shareholders in the form of dividends and buybacks, a low P/E ratio shows you’re paying less for each dollar of profit generated.

Best Value Railroad Stocks

Price ($) Market Cap ($B) 12-Month Trailing P/E Ratio

Canadian Pacific Railway Ltd. ( CP.TO) CA$464.64 CA$61.9 25.8

CSX Corp. (CSX) 93.48 71.3 26.0

Union Pacific Corp. (UNP) 212.67 142.5 27.0

Canadian Pacific Railway Ltd.: Canadian Pacific Railway is a Canada-based company that offers rail transportation services, including intermodal shipping, rail siding construction, and logistics services. In early march, Canadian Pacific announced updates to its Hydrogen Locomotive Program, whose goal is to create a locomotive that produces zero emissions. In the latest development, Canadian Pacific plans to retrofit a diesel-powered locomotive with Ballard hydrogen fuel cells. It would be the first hydrogen-powered line-haul freight locomotive in North America.2

CSX Corp.: CSX provides domestic and international freight transportation services. The company offers rail, domestic container shipping, barging, intermodal, and contract logistics services between global hubs. The company's rail transportation services are focused in the eastern U.S. In February, CSX announced that its board of directors authorized an 8% increase in its quarterly dividend, from $0.26 to $0.28 per share. The new dividend was paid on March 15, 2021.3

Union Pacific Corp.: Union Pacific transports agricultural, automotive, chemical, and other products. The company provides routes from West Coast and Gulf Coast ports to eastern gateways, Canada, and Mexico.

Fastest Growing Railroad Stocks

These are the railroad stocks with the highest year-over-year (YOY) operating income, also called operating earnings, growth for the most recent quarter. Rising earnings show that a company’s business is growing and is generating more money that it can reinvest or return to shareholders. Operating income excludes non-operating income and expenses (such as investment gains or losses), one-time items, as well as interest and taxes. This helps investors get a clearer picture at the strength of the underlying business without the effect of unusual one-off events, such as large tax credits, asset sales, or lawsuit settlements. If you decided to invest in a company, it's still important to look at these one-off non-operating expenses and incomes, as they can still influence a company's overall financial health.

Fastest Growing Railroad Stocks

Price ($) Market Cap ($B) Operating Income Growth (%)

CSX Corp. (CSX) 93.48 71.3 5.3

Canadian Pacific Railway Ltd. ( CP) 372.40 49.6 2.6

Norfolk Southern Corp. (NSC) 260.27 65.6 1.4

Source: YCharts

CSX Corp.: See company description above.

Canadian Pacific Railway Ltd.: See company description above. Note that common shares of Canadian Pacific Railway Ltd. trade on both the Toronto Stock Exchange and the New York Stock Exchange.4

Norfolk Southern Corp.: Norfolk Southern is a rail transportation company operating primarily in the Southeast, East, and Midwest. The company transports raw materials, intermediate products, and finished goods. Through agreements with other carriers, it also provides service throughout the U.S., as well as transport of overseas freight.

Railroad Stocks with the Most Momentum

These are the railroad stocks that had the highest total return over the last 12 months.

Railroad Stocks with the Most Momentum

Price ($) Market Cap ($B) 12-Month Trailing Total Return (%)

Greenbrier Companies Inc. ( GBX) 48.83 1.6 172.2

Norfolk Southern Corp. (NSC) 260.27 65.6 80.5

Kansas City Southern ( KSU) 219.81 20.0 73.9

Russell 1000 N/A N/A 53.5

iShares Transportation Average ETF (IYT) N/A N/A 78.4

Source: YCharts

Greenbrier Companies Inc.: Greenbrier Companies is primarily engaged in the design, manufacture, and marketing of railroad freight car equipment. The company manufactures both railcars and marine vessels, provides repair and refurbishment for intermodal and conventional railcars, and provides complementary leasing and services. In February, Greenbrier announced plans to form GBX Leasing, a joint venture with The Longwood Group, a transportation equipment advisory and asset management firm. GBX Leasing will develop a portfolio of leased railcars primarily built by Greenbrier. The initial equity investment in the JV will benefit from specific tax advantages related to financial losses under the U.S. CARES Act passed in early 2020 to address the impact of the COVID-19 pandemic.5

Norfolk Southern Corp.: See company description above.

Kansas City Southern: Kansas City Southern is a holding company that, through its subsidiaries, operates a railroad system providing shippers with freight services in commercial and industrial markets in the U.S. and Mexico.

<<<

>>> Canadian Pacific to buy Kansas City Southern in $25 billion railway bet on trade

Yahoo Finance

Nandakumar D, Ann Maria Shibu and Rebecca Spalding

March 20, 2021

https://finance.yahoo.com/news/canadian-pacific-buy-kansas-city-034255096.html

Canadian Pacific to buy Kansas City Southern in $25 billion railway bet on trade

(Reuters) - Canadian Pacific Railway Ltd agreed on Sunday to acquire Kansas City Southern in a $25 billion cash-and-stock deal to create the first railway spanning the United States, Mexico and Canada, standing to benefit from a pick-up in trade.

It would be the largest ever combination of North American railways by transaction value. It comes amid a recovery in supply chains that were disrupted by the COVID-19 pandemic, and follows the ratification of the US-Mexico-Canada Agreement (USMCA) last year that removed the threat of trade tensions that had escalated under former U.S. President Donald Trump.

"Think about what we've gone through, think about the importance in North America of near-shoring that is occurring. This network uniquely provides a supply chain that allows our customers and our partners to actually benefit from that and leverage that opportunity," Canadian Pacific Chief Executive Keith Creel told Reuters in an interview.

The combination needs the approval of the U.S. Surface Transportation Board (STB). The companies expressed confidence this would happen by the middle of 2022, given that the deal would unite the smallest of the seven so-called Class I railways in the United States, which meet in Kansas City and have no overlap in their routes. The combined railway would still be smaller than the remaining five Class I railways.

The STB updated its merger regulations in 2001 to introduce a requirement that Class I railways have to show a deal is in the public interest. Yet it provided an exemption to Kansas City Southern given its small size, potentially limiting the scrutiny that its acquisition will be subjected to.

"I don't see it as the kind of consolidation that should raise concerns because it's what you call an end-to-end or vertical merger. Their networks fit nicely with each other and help fill out North America with real service," said economist Clifford Winston, a senior fellow at the Brookings Institution who specializes in the transportation sector.

An STB spokesman said the regulator had not yet received a filing from the companies, which would start its formal review process. He declined to comment further.

Still, Canadian Pacific agreed in its negotiations with Kansas City Southern to bear most of the risk of the deal not going through. It will buy Kansas City Southern shares and place them in an independent voting trust, insulating the acquisition target from its control until the STB clears the deal.

Were the STB to reject the combination, Canadian Pacific would have to sell the shares of Kansas City Southern, and one source close to the agreement suggested they could be divested to private equity firms or be relisted in the stock market. Kansas City Southern shareholders would keep their proceeds.

There is a $1 billion reverse breakup fee that Canadian Pacific would have to pay Kansas City Southern if it cannot complete the formation of the trust, the source added.

Shareholders of Kansas City Southern will receive 0.489 of a Canadian Pacific share and $90 in cash for each Kansas City Southern common share held, valuing Kansas City Southern at $275 per share, a 23% premium to Friday's closing price, the companies said in a joint statement. Including debt, the deal is valued at $29 billion.

Kansas City Southern shareholders are expected to own 25% of Canadian Pacific's outstanding common shares, the companies said. Canadian Pacific said it will issue 44.5 million shares and raise about $8.6 billion in debt to fund the transaction.

It is the top M&A deal announced thus far in 2021. While it is the biggest ever involving two rail companies, it ranks behind Berkshire Hathaway's purchase of BNSF in 2010 for $26.4 billion. For a Factbox on the deal highlights see:

Creel will continue to serve as CEO of the combined company, which will be headquartered in Calgary, the companies said in a statement.

The companies also highlighted the environmental benefits of the deal, saying the new single-line routes that would be created by the combination will help shift trucks off crowded U.S. highways and cut emissions.

Rail is four times more fuel efficient than trucking, and one train can keep more than 300 trucks off public roads and produce 75% less greenhouse gas emissions, the companies said in the statement.

FAILED BIDS

Calgary-based Canadian Pacific is Canada's No. 2 railroad operator, behind Canadian National Railway Co Ltd, with a market value of $50.6 billion.

It owns and operates a transcontinental freight railway in Canada and the United States. Grain haulage is the company's biggest revenue driver, accounting for about 58% of bulk revenue and about 24% of total freight revenue in 2020.

Kansas City Southern has domestic and international rail operations in North America, focused on the north-south freight corridor connecting commercial and industrial markets in the central United States with industrial cities in Mexico.

Canadian Pacific's latest attempt to expand its U.S. business comes after it abandoned a hostile $28.4 billion bid for Norfolk Southern Corp in April 2016. Canadian Pacific's merger negotiations with CSX Corp, which owns a large network across the eastern United States, failed in 2014.

A bid by Canadian National Railway Co, the country's biggest railroad, to buy Warren Buffett-owned Burlington Northern Santa Fe was blocked by U.S. antitrust authorities more than two decades ago.

A private equity consortium led by Blackstone Group Inc and Global Infrastructure Partners (GIP) made an unsuccessful offer to acquire Kansas City Southern last year. The sources said that bid helped revive Canadian Pacific's interest in Kansas City.

BMO Capital Markets and Goldman Sachs & Co. LLC are serving as financial advisors to Canadian Pacific, while BofA Securities and Morgan Stanley & Co. LLC are serving as financial advisors to Kansas City Southern.

<<<

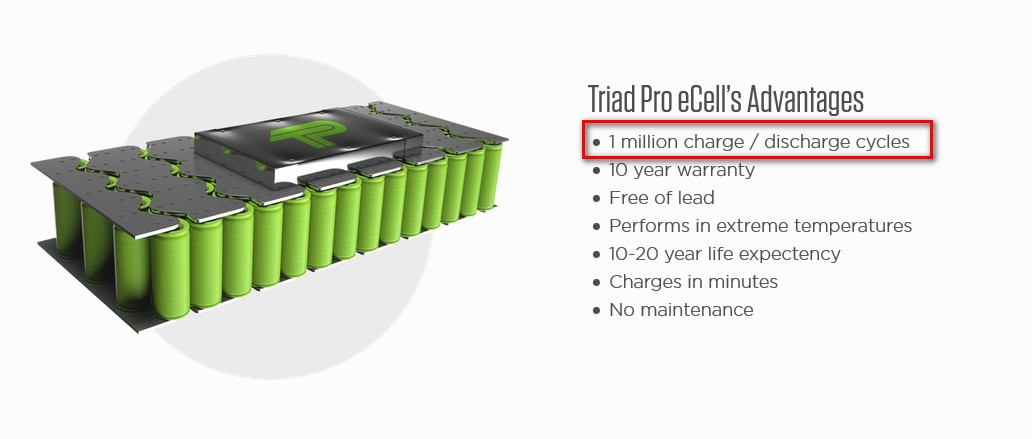

$TPII still the most promising breakthrough EV and fixed-site energy storage technology around. $TPII's super-capacitor energy storage technology replaces OR supplements lithium batteries in EVs, trucks, golf carts as well as fixed-site storage facilities.

Check out their site: http://www.TriadProInc.com

$TPII Breakthrough EV-Storage-Tech in production: Replacing Lithium!

http://www.TriadProInc.com

Watch the Video: http://www.TriadProInc.com/

>>> Railroads Make Up 36.7% Of This Transportation ETF

Seeking Alpha

Oct. 09, 2020

by Sven Carlin

https://seekingalpha.com/article/4378292-railroads-make-up-36_7-of-this-transportation-etf

Summary

Railroads are good businesses with a strong moat, high profitability, good growing dividends and buybacks that push stock prices higher. It is likely railroad stocks will keep being the stable ones within the transportation ETF.

The buyback game is a risky game to play and can't be played forever. The key is to sell at some point in time before the debt becomes a burden.

At the bottom of the article you have a video discussing the topic if you prefer watching.

We all know Warren Buffett owns a railroad, Burlington Northern Santa Fe. Therefore, it is always good to look into railroad stocks to see whether a railroad stock might fit your portfolio too. A way to get exposure to railroad stocks is the iShares Transportation Average ETF (IYT) as 36.7% of its weight consists of 4 railroad stocks:

Norfolk Southern (NSC)

Union Pacific (UNP)

Kansas City Southern (KSU)

CSX Corp. (CSX)

This article will describe the investment thesis for railroad stocks, give an overview of all railroad stocks traded in the US, discuss the main trends within the sector, the valuation and the risks of investing in them.

Railroad stocks investment thesis – Moats, Growth & Profitability

The 4 key ingredients that make something a great business to own are moat, growth, increasing profitability and fair price. We analyze the moat strength of railroads, the growth opportunities, profitability and valuation.

Railroad stocks offer a moat

A railroad is a typical Buffett business. Over the last few decades the sector has consolidated and the number of railroads fell from 40 to 7. Each railroad has its own geography and nobody wants to build new railroads because that would impact the profitability of the other and your own railroad. Once you build it, you own it and you can enjoy the economic benefits of it without worrying that somebody will build a new one next to you.

It is unlikely anybody could get permission to build a big, new railroad (not in my backyard) and it is also unlikely a new railroad would ever be profitable because of the competition. Therefore, we can say railroads have a wide moat.

Railroad stocks offer growth and sustainability

When you have a moat, and a stable infrastructure, the more business you do using your infrastructure, the more money you make because your costs increase less than your revenue, thanks to the fixed cost part.

The Association of American Railroads predicts a 30% increase in U.S. freight movements by 2040. That is not much per year, but when you have a moat, when you don’t need to worry about competition too much, when you can focus on reducing costs, improving operations and increasing profitability as much as possible, it adds up to significant profitability increases.

Rail is already the most efficient way to move freight as a gallon of fuel can move a ton of freight for 470 miles on average.

The fuel efficiency makes it also environmentally positive to move things with trains.

We have discussed how railroads offer a moat and growth. But that is not enough to make them a good investment. What you need are profitability and a good price.

Precision Scheduled Railroading Increases Railroad Profitability + Scale

Since the Staggers Rail Act of 1980 that deregulated railroads, railroads spent more than $710 billion on their infrastructure. They did that because it was profitable to do so. The average railroad had returns on capital employed between 7% and 13% over the last 15 years where the returns even increased over the last decade as more and more railroads implemented Precision Scheduled Railroading.

High profitability, a moat, stable businesses, a good return on capital and a focus on rewarding shareholders have pushed railroad stocks to extremely high levels.

Railroad stocks performance and valuation

Actually, over the last 5 years, all railroad stocks have beaten the S&P 500.

Railroad stocks performance over the last 5 years

What happened happened, and there is nothing we can do about it. What we have to do is see how railroad stocks fit our portfolio now. The best way to value a business like a railroad is to look at cash flows and future growth opportunities.

I have compiled a table that compares all railroad stocks and the free cash flow yield is between 3% and 3.7% except for CSX, but that might be due to the coal exposure CSX has, thus it can be considered riskier. If you are interested in individual analyses you can find all the links below.

Railroad stocks dividends and buybacks

All railroad stocks pay a dividend but their key focus is buybacks. All listed ones take on as much debt as possible in order to do as much buybacks as possible. This is probably the reason why railroad stocks have outperformed the S&P 500.

However, as they are taking on more and more debt to do buybacks at any price, as investors we have to be careful to get out in time because when the buybacks stop and liquidity dries up, railroad stock prices will likely crash. So, enjoy the ride while it lasts and see how holding a business with a yield slightly above 3% but relatively safe fits your portfolio.

3% free cash flow yield as valuation metric

A good valuation metric for railroad stocks is also what would a railroad be worth to an owner. Recently KSU rejected a takeover bid for a free cash flow yield of 3%. Thus, we could see that as a margin of safety in this environment. Investment funds that can borrow at below 2% see railroad stocks as attractive when those offer long-term growth and a 3% cash flow yield. However, I don’t think many can come up with more than $20 billion to buy the bigger railroads, so the investment thesis with the bigger railroads is based on the cash flow yield and buyback activity.

Railroad stocks investment thesis

The investment thesis depends on what perspective you take; a relative or absolute perspective.

From an absolute investing perspective, railroads offer a 3% cash flow yield in the form of dividends and buybacks, slow growth alongside a strong moat. Nothing wrong with their businesses and it is likely in 20 years everything will look the same with improved profitability and likely even more traffic. The debt piled up might be an issue if interest rates go up, but interest rates going up is also unlikely for the short to medium term. So, we have safety and quality alongside a yield between 3% and 3.7% on average.

From a relative perspective, with your bank giving you miserable returns on savings, with investment banks and hedge funds being able to borrow at ridiculously low rates, if the market starts liking railroad stocks with a 2% free cash flow yield, that will represent a 50% upside from current levels. Plus, all the buybacks might make it much easier for railroad stocks to go up and do well. Actually, I think that until the buyback game lasts, railroad stocks will likely outperform the market.

Further, with the Fed saying it will allow inflation and railroads focusing on cost savings, their actual margins might improve especially as interest rates on debt stay low. So, railroads could be a safe bet to add portfolio protection against the loose monetary environment we will likely have the coming decade.

Railroads go for automation that lowers costs and improves safety

I hope to have given you a good perspective on railroad stocks so that you can compare them to other investment opportunities you have and see what is the best investment that will lead you to your financial goals – that is the key, nothing else matters.

Railroad stocks as part of IYT

For now, railroad stocks give the necessary stability to IYT as the dividends haven't been cut in this environment and the buybacks stay strong. However, the buyback game can only last up till a point.

One day, there will be no liquidity to take on more debt, or perhaps in a bad economy cash flows will dry up. At that moment in time, there will be no fundamentals and no buybacks to protect the stock price. That is a time to avoid being a shareholder and unfortunately an ETF cannot protect you from that. Despite having 36.7% of its weight in railroad stocks that have all outperformed the S&P 500 (SPY) over the last 5 years and decade, IYT has underperformed SPY.

The point of this article was to give you a good perspective on what you own when you own the IYT ETF, explain the risk and rewards so that you can see whether you have better options for your portfolio. Railroads contribute a 3 to 3.7% free cash flow yield and strong buybacks alongside business stability. On the risk side, all take on debt that pushes the stock higher and forces the ETF to buy more due to weight requirements. Be careful not to be on the other side of that financial engineering game.

<<<

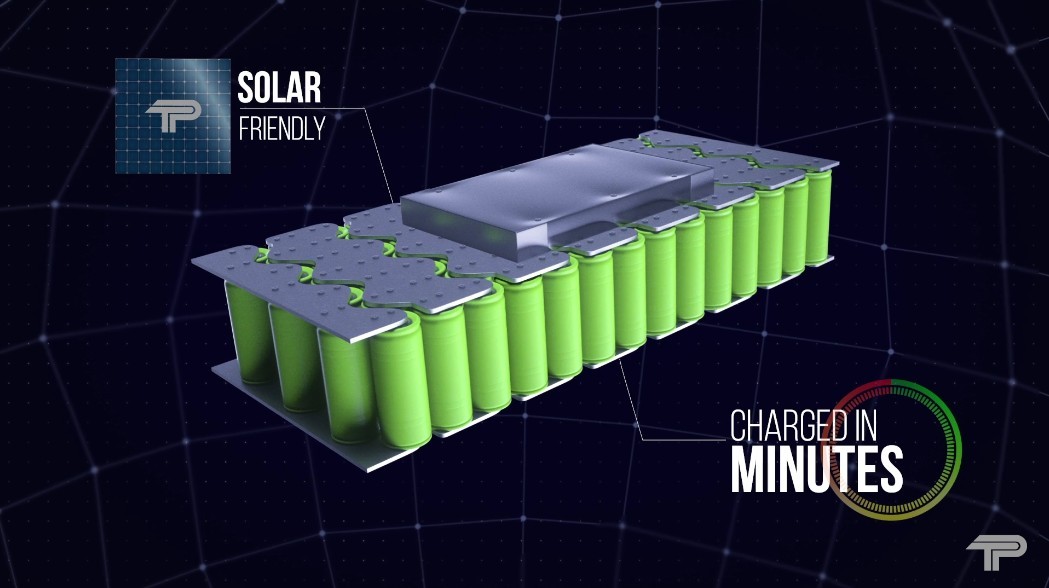

$TPII has breakthrough energy storage technology. EV, trucks, on-site, etc.

$TPII EV Tech: Charge in Minutes / Solar Friendly:

They are in production!

Watch the Video: http://www.TriadProInc.com/

>>> Batteries Serve as 'Secret Sauce' for EVs: 4 Stocks in Focus

Yahoo Finance

by Rimmi Singhi

December 22, 2020

https://finance.yahoo.com/news/batteries-serve-secret-sauce-evs-140902027.html

Electric vehicles (EVs) are the future of transportation. For years, it seemed that Tesla TSLA was the only automaker that was playing at the forefront of the EV phenomenon and taking the concept of green vehicles seriously from a real-world functionality standpoint. However, things are changing as most of the automakers are now fast changing gears to electric. Climate concerns, stringent fuel-economy targets, and advancement in technology as well as charging infrastructure are boosting the environment-friendly EV market.

EV sales across the globe are projected to grow 50% or more in 2021 compared with ICE expected sales growth of a meager 2-5%, as predicted by analysts at Morgan Stanley, quoted in a MarketWatch article. Global EV penetration is projected to jump from 3% to 31% by 2030.

Widespread adoption of e-mobility will have a trickle-down effect in the supply chain, making battery stocks more attractive than ever. Batteries are the most common element of green cars and will play the most important role in accelerating the EV revolution. Battery specs are the cornerstone of an electric vehicle’s performance. Without the right battery technology, the EV industry wouldn’t be able to live up to its hype.

Global EV Battery Market Charged Up

The EV battery space is mostly dominated by Asia, with Contemporary Amperex Technology Co Ltd, LG Chem, BYD Co. Ltd BYDDY, Panasonic Corp. PCRFY and Samsung SDI spearheading the game. Riding on the enormous optimism in the battery space and EV frenzy, California-based EV battery maker QuantumScape QS recently made its NYSE debut. The Bill Gates-backed EV battery supplier is developing the next generation of batteries utilizing lithium metal, which has a significantly higher energy density than lithium ion. Set to disrupt the world of batteries, QuantumScape claims that its batteries are designed to offer up to 80% longer range than the existing lithium-ion batteries. Per the company, its batteries would charge up a vehicle to 80% of its full capacity in around 15 minutes.

Per ReportLinker data, the global market for EV battery is estimated at $30.7 billion in 2020 and expected to witness a CAGR of 16% over the next seven years to reach $87.2 billion. Currently, the most popular source of power in green vehicles is lithium-ion batteries. Notably, the lithium ion battery segment is likely to record a CAGR of 17.7% over the next seven years, with China, the United States of America, Europe, Japan and Canada driving global demand. Amid the upbeat scenario, investors should put battery-related stocks onto their radar.

4 ‘Pick & Shovel’ Stocks to Play the EV Boom

Panasonic Corp.: Panasonic is one of the key players in the development of next-generation lithium-ion batteries for green vehicles. Continuous research and cutting edge technology have kept the company at the forefront of battery development. Its advanced lithium-ion battery tech offers improved energy density, lower costs and improved driving range. Partnerships with auto biggies like Tesla and Toyota TM are likely to boost the firm’s prospects. Notably, the company is targeting zero cobalt in its battery cells and plans to commercialize cobalt-free batteries in a few years. Panasonic currently carries a Zacks Rank #2 (Buy). The Zacks Consensus Estimate for its fiscal 2022 earnings indicates a year-over-year increase of 82.1%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

EnerSys ENS: Headquartered in Pennsylvania, EnerSys engages in manufacturing, marketing and distribution of various industrial batteries. Battery brands of the firm include EnergyCell, NexSys and PowerSafe. Solid product portfolio, new product offerings, acquired assets and shareholder-friendly policies are key strengths of EnerSys. Amid the changing dynamics of the industrial battery landscape, the company remains focused on the development of Thin Plate Pure Lead and advanced Lithium-ion technologies. It currently carries a Zacks Rank #3 (Hold) and has an expected EPS growth rate of 10% for the next three-five years.

Albemarle Corp. ALB: Considered as the world’s biggest lithium producer, this Charlotte-based company is expected to gain immensely from rising production of electric cars. Albemarle has battery-grade lithium-producing plants in Europe, Australia, China, Chile and the United States. This Zacks Rank #3 firm remains focused on strengthening the lithium business. Even amid the coronavirus crisis, Albemarle managed to surpass earnings and sales estimates in the last reported quarter. The company expects net sales for 2020 between $3.05 billion and $3.15 billion. Solid cost-cut initiatives and investor-friendly moves of the firm are encouraging. The company has an expected EPS growth rate of 11.9% for the next three-five years.

Vale S.A.VALE: Wondering why this Brazil-based giant miner is also on the list? Well, lithium-ion batteries mostly rely on nickel and Vale is the largest producer of the metal in the world. Most of the EV makers are aiming to eliminate the usage of cobalt in battery cells as the commodity is expensive and instead increase the nickel content. At the Battery Day event, Tesla revealed its intent to increase the nickel content in its battery composition, which would improve the range of vehicles and cut costs. So, the rising popularity of EVs is not just likely to buoy lithium demand but will also jack up nickel demand. Hence, Vale could very well be on your watchlist if you want to tap the EV boom. This Zacks Rank #3 company carries a VGM Score of A and has a long-term expected EPS growth of more than 25%.

<<<

Canadian National Railway - >>> A reliable stock for all times

https://www.fool.com/investing/2020/10/24/5-great-stocks-you-can-buy-and-hold-forever/

Canadian National Railway (NYSE:CNI) has quietly made massive profits for investors who've held the stock and reinvested dividends through the past couple of decades. The company has increased its dividend every year since 1995 at a compound annual growth rate (CAGR) of 16% through 2019.

Railroads haul one-third of U.S. exports and support nearly $220 billion in economic output each year. It's an essential industry and Canadian National's a leading player in it, operating the longest rail network in North America covering nearly 20,000 route miles, and the only one connecting the Atlantic, Pacific, and Gulf coasts.

Canadian National is also an efficient and diverse railroad, moving goods from many vital commodity markets including petroleum, grains, metals, and forest products. The company pumped a record $3.9 billion Canadian dollars into capital investments last year and is upping its automation game. For example, its Autonomous Track Inspection Program, which uses artificial intelligence to monitor and test track parameters in real time, could reduce the need for manual inspections by 50%.

Canadian National's a well-established, well-run company in a critical industry, is investing in growth, and pays one heck of a dividend. That's a great package to own for a lifetime.

<<<

Werner Enterprises - >>> 19 of the Best Stocks You've Never Heard Of

Kiplinger

by Jeff Reeves

6-23-20

https://www.kiplinger.com/slideshow/investing/t052-s001-19-of-the-best-stocks-youve-never-heard-of/index.html

Werner Enterprises

Sector: Industrials

Market value: $3.0 billion

Dividend yield: 0.8%

Werner Enterprises (WERN, $43.46) is one of the five largest freight carriers in the United States, with terminals and routes that weave across every part of the country. Even if many motorists never notice the name on the big rig beside them, Werner has likely been driving on a road near you recently as it actively operates in the 48 contiguous states and portions of Canada and Mexico.

While brick-and-mortar shopping trends have been disrupted in 2020 by coronavirus, the pandemic has also proven the power of logistics companies that power the e-commerce enterprises of the world. After all, if Werner wasn't picking up and dropping off its shipments at warehouses then that Amazon or UPS employee wouldn't have anything to package up and deliver to your front porch.

Strong fundamentals recently have also coincided with a big chance for an evolution at WERN as founder and executive chairman Clarence Werner stepped down at the end of May. The 83-year-old executive, who started the company with one truck back in 1956, surely saw success in his career. But he might not exactly be the leader shareholders were looking for in a modern era with complicated supply chains and talk of self -driving fleets.

Analysts see a lot of hope for continued growth and evolution at WERN, with increased price targets since April from a host of investment banks including Citigroup, Credit Suisse, Morgan Stanley and others.

<<<

Amazon Prime Air Seen Surging Fivefold to 200 Jets, Rivaling UPS

Bloomberg

By Spencer Soper

May 22, 2020

Kentucky air hub could emerge as key to more national service

Amazon now offers service to small a number of destinations

https://www.bloomberg.com/news/articles/2020-05-22/amazon-prime-air-will-grow-to-200-planes-rival-ups-study-says?srnd=premium

Amazon.com Inc.’s Prime Air fleet will grow to about 200 planes -- up from 42 now -- in the next seven or eight years, creating an air cargo service that could rival United Parcel Service Inc., according to a study.

“At a time when many other airlines are downsizing due to the pandemic, Amazon’s push for faster and cheaper at-home delivery is moving ahead on an ambitious timetable,” said the report issued Friday by DePaul University’s Chaddick Institute of Metropolitan Development. “Amazon Air’s robust expansion makes it one of the biggest stories in the air cargo industry in years.”

Amazon unveiled the air cargo service in 2016, prompting speculation that it would ultimately create an overnight delivery network to rival delivery partners UPS and FedEx Corp.

Prime Air operates out of smaller regional airports close to its warehouses around the country, helping Amazon quickly move inventory to accommodate one- and two-day delivery. For that reason, some analysts have dismissed Amazon as a potential competitor to UPS and FedEx since it can only offer limited service to a small number of destinations and seems designed to handle Amazon packages.

Key to its ability to take on the entrenched players, the report says, is Amazon’s new $1.5 billion facility near Cincinnati that will accommodate up to 100 planes and as many as 200 flights each day. Amazon’s lack of a central hub has kept it from competing in the overnight delivery services offered by UPS and FedEx, which have more planes flying to more destinations.

“The massive investment being made in a large hub at Cincinnati/Northern Kentucky International Airport, however, could change everything,” the report says. “This hub appears to be the linchpin to Amazon’s efforts to develop a comprehensive array of domestic delivery services.”

A separate report released Monday noted Amazon’s lack of a central hub in concluding it was not a competitive threat to FedEx, which has a hub in Memphis, or UPS, which has one in Louisville. FedEx’s network can offer 9,000 daily flight connections, UPS’ 5,500 and Amazon Air just 363, according to the report from Bernstein.

“The viability of a commercial overnight offering from Amazon remains very limited,” Bernstein analyst David Vernon wrote. “Offering a low cost on shipping to a small number of markets every so often will never be a serious competitive threat.”

<<<

Ferrari - >>> One Car Maker That Will Emerge Stronger From the Pandemic. It’s Not Who You Might Think.

Barron's

By Al Root

May 7, 2020

https://www.barrons.com/articles/the-auto-industry-is-suffering-ferrari-will-emerge-stronger-from-the-pandemic-51588850101?siteid=yhoof2&yptr=yahoo

There is one automotive company that will emerge unscathed from the coronavirus crisis—and actually come out stronger than before the outbreak. It sounds impossible, but that’s what Morgan Stanley analyst Adam Jonas believes about one of the companies he covers.

There have been some bright spots among car makers lately. General Motors stock (ticker: GM) jumped after the company reported better-than-expected first-quarter earnings Wednesday. Tesla (TSLA) has strung together a few impressive quarters, sending shares up more than 200% over the past year. But it’s neither of those.

The company in question is Ferrari (RACE). And Jonas has five reasons backing up his argument.

The Balance Sheet

Ferrari will generate positive free cash flow in 2020. Jonas models about $150 million in free cash flow, while Wall Street consensus calls for about $200 million. Mainstream auto maker Ford Motor (F), on the other hand, will burn through about $2 to $3 billion this year, according to analysts.

New Models

Ferrari is launching four models in 2020, including the SF90 Stradale, the 812 GTS, F8 Spider and the Roma grand touring model. The Roma has a V-8 engine, generating more than 600 horsepower, and the car starts at $220,000. Two more models are coming in 2021, according to Jonas. New products should help simulate new demand, regardless of the economic environment.

Formula One Racing

This benefit isn’t obvious. But some new rules for the highest level of auto racing have been pushed out until 2022, keeping costs down. That’s saving Ferrari money over the near term. The company doesn’t break out its Formula One spending in its annual report.

The Brand

“The pedigree of the Ferrari brand is more relevant than ever now,” wrote Jonas in a Wednesday research report. He sees more licensing opportunities in the future. What’s more, the company can bring a new generation of Ferrari enthusiasts into the fold by focusing on esports.

Achievable Financial Guidance

Ferrari reported quarterly numbers on May 4. It did something unique regarding guidance: It actually gave some. Most companies have withdrawn full-year 2020 guidance because Covid-19 has made the outlook too murky.

Looking ahead, the company expects to generate about $1.1 billion in Ebitda, short for earnings before interest, taxes, depreciation, and amortization. Management’s initial guidance was about $1.4 billion.

Ferrari actually missed earnings estimates when it reported on May 4, but the stock jumped 7% anyway. Weak earnings in the first and second quarter of the year aren’t a surprise. Italy, after all, is one of the countries hit hardest by the Covid-19 outbreak.

Cases in Italy topped 210,000 and deaths surpassed 29,000. The government locked down much of Northern Italy in early March, including Modena. Ferrari’s primary manufacturing location is in Maranello, Italy, just south of Modena.

Ferrari production was halted for seven weeks, and company management addressed a May restart on their quarterly conference call, stressing caution. “We now have the capacity to perform 800 voluntary blood tests a day to cover both our employees and their families,” said CEO Louis Camilleri.

In addition to all the points Jonas makes, it probably helps that Ferrari only sells about 10,000, incredibly valuable sports cars each year. Ferrari is a luxury goods company as much as it is a car maker.

So it makes sense that Ferrari trades like a luxury stock. Shares fetch about 35 times estimated 2021 earnings. GM stock, for instance, trades for 5 times estimated next year’s earnings. LVMH Moët Hennessy Louis Vuitton (MC.France), a luxury stock, trades for 23 times estimated 2021 earnings. That’s lower than Ferrari, but LVMH is buying jewelry giant Tiffany (TIF) for about 30 times 2021 earnings.

Investors, it seems, remains confident the richest consumers will keep spending.

Jonas, for his part, rates Ferrari shares the equivalent of Buy. His price target for the stock is $180, about 15% higher than recent levels.

Ferrari shares are down about 5% year to date, performing a little better than comparable drops of the Dow Jones Industrial Average and the S&P 500.

<<<

>>> French Giant Looks at Tesla With Burning Envy

Legacy carmakers won't get much help financing their climate conversion and it's going to be painful.

Bloomberg

By Chris Bryant

February 14, 2020

https://www.bloomberg.com/opinion/articles/2020-02-14/renault-can-t-expect-tesla-style-helping-hand-for-electric-push?srnd=premium

It’s going to be expensive to create an electric car market.

On one side of the Atlantic, Tesla Inc. is capitalizing on its soaring share price by selling $2 billion in stock so it can build more electric vehicles. On the other, French manufacturer Renault SA has been forced to cut its dividend by 70% and announce a big reduction in fixed costs so it can afford to do the same.

Dwindling profits and Renault’s drastic remedies were mirrored this week by its Japanese alliance partner Nissan Motor Co., as well at Daimler AG. (Renault has an engineering partnership with Daimler and owns a small stake in the German car and truck maker.) Their problems aren’t identical but all three had expanded their workforces in anticipation of demand that hasn’t materialized and now they have to tighten their belts to pay for expensive electric vehicles, for which demand remains uncertain.

Renault’s shares are near their lowest level in eight years, which means the company is capitalized at barely 10 billion euros ($11 billion), a sum that includes the 43% stake Renault owns in Nissan. Needless to say, that’s a sliver of what Tesla is worth, even though the U.S. company’s annual output is still almost a rounding error for the Renault-Nissan alliance.

This juxtaposition sends a crystal clear message: Carmakers that grew fat and happy producing combustion engine vehicles won’t get any help from the stock market now that they’ve decided to embrace an electric future. Instead the gasoline gang are going to fund these changes themselves and it’s going to be painful, for both employees and shareholders.

Long-established automakers have decided that their salvation is to be found in alliances and partnerships, which spread the cost of developing expensive technology over a greater number of car sales. It’s why Renault tried to merge with Fiat Chrysler Automobiles NV, before Peugeot-owner PSA Group beat them to it.

But in Renault’s case its links to other manufactures are amplifying its problems right now, not solving them. Relations with Nissan fell apart when former alliance boss Carlos Ghosn was arrested and remain fragile now that he’s free to settle scores. Both sides have since hired new CEOs but their shareholders aren’t yet ready to buy the story that harmony has been restored.

With its own profits slumping, Nissan can’t afford to pay big dividends to Renault and the French are also earning less from the Daimler partnership. The upshot is that Renault is a bit squeezed for cash — net cash at the automotive unit dwindled to just 1.7 billion euros at the end of December (though gross liquidity, including available credit lines, was a more respectable 16 billion euros).

One way Renault could free up some money would be to sell part of its Nissan stake, which might have the added benefit of helping to re-balance the alliance in Nissan’s favor, something the Japanese have long sought. The trouble is Nissan’s shares have halved in value over the last two years so selling now wouldn’t provide Renault with nearly as much as it once would. Interim CEO Clotilde Delbos all but ruled out such a move on Friday.

So it’s no wonder that Renault has opted to drastically scale back its own dividend and will try to cut costs by 2 billion euros in the next three years. Delbos, who’s also the chief financial officer, didn’t go into much detail about how those savings will be delivered but the company plans to review its “industrial footprint,” which suggests plant closures are a possibility. (Alliance partner Nissan has already announced 12,500 job cuts, while Daimler is targeting at least 10,000.)

Lowering costs won’t be straight forward. New Renault CEO Luca de Meo, a former Volkswagen AG executive, doesn’t start until July and French unions aren’t known for championing efforts to slash jobs. In the near term, restructuring costs will also put further pressure on Renault’s cash flow and the coronavirus could yet create unexpected problems.

But unlike at Tesla, Renault doesn’t have a queue of wealthy supporters clamoring to help fund this epochal clean-vehicle transition. One way or other, employees and existing shareholders will end up paying.

<<<

>>> Tesla Surges Past $100 Billion Market Value, Eclipsing VW

Bloomberg

By Dana Hull, Christoph Rauwald, and Gregory Calderone

January 21, 2020

https://www.bloomberg.com/news/articles/2020-01-22/tesla-hits-100-billion-mark-musk-must-sustain-for-big-payout

VW sold almost 30 times as many cars last year as Musk

CEO may be in store for $346 million award if rally sustained

Tesla Market Cap Surges Past Volkswagen's to More Than $100 Billion

Tesla Inc.’s market value has climbed above Volkswagen AG’s for the first time to more than $100 billion, a threshold that will trigger a huge payout for Elon Musk if he can sustain the feat for months.

The electric-car maker’s shares soared as much as 8.6% on Wednesday to a new intraday high of $594.50. At that price, Tesla’s market capitalization was roughly $107.2 billion, exceeding Volkswagen’s $99.4 billion and trailing only Toyota Motor Corp.

While Musk’s skeptics are dubious that Tesla should be worth more than a carmaker that sold almost 30 times as many vehicles last year, Volkswagen’s own Herbert Diess isn’t so dismissive. He’s been arguably the most vocal CEO among traditional carmakers to praise Tesla and point to its role in a radical shakeup of the more than century-old auto industry.

After saying three months ago that Tesla was no niche manufacturer anymore, Diess told top Volkswagen executives at an internal meeting in Germany last week that connected vehicles will almost double the time consumers spend online, and that cars will “become the most important mobile device.”

“If we see that, then we also understand why Tesla is so valuable from the view of analysts,” he said.

Diess, 61, is rolling out the industry’s largest electric-car fleet and aims to boost the company’s value to a level rivaling Toyota, whose $232 billion market cap is still more than Tesla and VW’s combined.

“Tesla has high innovative strength regarding battery-electric vehicles as well as connectivity, which can partly explain the high market capitalization,” Stefan Bratzel, a researcher at the Center of Automotive Management near Cologne, Germany, said in a report Wednesday. The relatively low valuation of traditional automakers is linked to uncertainty over whether they can navigate the looming industry shift, he said.

The jump above $100 billion is about more than just bragging rights for Musk, Tesla’s billionaire chief executive officer. He’s eligible to receive the first tranche of an all-or-nothing pay award if the company’s market value stays above that threshold for a sustained period. On paper, the first chunk of the award would net him about $346 million.

Tesla shares have more than doubled since the company reported a surprise third-quarter profit and told investors it was ahead of schedule bringing out its next product, the Model Y crossover, and opening its factory near Shanghai.

The stock has room to run as Tesla grows in China, Wedbush analyst Dan Ives wrote in a report Wednesday. He boosted his target price to $550 from $370 while maintaining the equivalent of a hold rating.

What Bloomberg Intelligence Says:

“Tesla’s tepid 0.3% gain in 2019 domestic unit sales suggests a tapped-out U.S. Sales in China skew the U.S. demand picture, which should become clearer by year-end with the ramp-up in Shanghai output.”

- Kevin Tynan, senior autos analyst

Gary Black, who was chief executive of Aegon Asset Management from mid 2016 through September and now holds Tesla as a private investor, said he expects Tesla to earn more than VW by 2025 and believes consensus estimates for vehicle deliveries this year are too low. He expects Musk to forecast at least 550,000 units for 2020 during next week’s earnings webcast and to tout the launch of the Model Y.

While at least eight analysts have boosted their price targets by more than $100 since the year began, consensus is still well below where Tesla’s shares are trading. The average target is $363.92 with just 10 analysts rating the stock a buy, compared with 10 holds and 16 sells.

<<<

>>> SmartETFs Launch Smart Transportation & Technology ETF ‘MOTO’

ETF Trends

by AARON NEUWIRTH

NOVEMBER 15, 2019

https://www.etftrends.com/innovative-etfs-channel/smartetfs-launch-smart-transportation-technology-etf-moto/

SmartETFs Funds launched a new, actively managed transportation and technology ETF on Friday that invests in companies believed to benefit from the current revolution in transportation.

The SmartETFs Smart Transportation & Technology ETF (MOTO) seeks long term capital appreciation from investments involved in the manufacture, development, distribution, and servicing of autonomous or electric vehicles and companies involved in related developments or technologies to support autonomous or electric vehicles including infrastructure, roadways, or other pathways.

As noted, the ETF is actively managed, as well as fully transparent, investing in approximately 35 equally weighted positions on a global basis. This includes companies that manufacture, distribute, service, offer, support, or enable the following: electric vehicles, autonomous vehicles, transportation as a service, flying autonomous vehicles, autonomous or electric public transportation, and hyperloop-based transportation, for passengers or goods.

Adapting To Tech Change

Jim Atkinson, CEO for Guinness Atkinson Asset Management, which manages SmartETFs, spoke to ETF Trends about MOTO and how it will adapt to changes in the technology sector.

The technology demands for autonomous and electric vehicles are high and the competition to win, particularly in the autonomous challenge, is fierce, Atkinson stated.

“It is very difficult to pick the winners in this competitive challenge,” he said. “We know some firms have an obvious lead, most notably Waymo and Tesla in autonomous technology and Tesla in the EV space. But how this plays out over the next decade is hard to predict.”

Atkinson added how this is one reason SmartETFs believes an actively managed strategy is preferable. Their style is low turnover, but the managers are acutely aware of these challenges and will seek to position the portfolio to take advantage of developments over time.

MOTO: A Progressive ETF

In discussing how MOTO is a progressive ETF looking at future revolution, Atkinson also noted how he believes a transportation revolution is underway.

“We’re at the beginning so it doesn’t look like much at the moment but as EVs gain market share and self-driving vehicles begin to be deployed in larger numbers our entire system of transportation may change,” he said. “The combination of electric autonomous vehicles and application-based ride-hailing may mean an end to the own and drive transportation model. The average automobile in the US is idle 95% of the time.

“A more efficient utilization means a cheaper, safer and more convenient alternative. It isn’t entirely clear where this revolution is headed but the direction of travel is for safer, cleaner, cheaper and better transportation.”

As far as where this ETF fits in a portfolio and who it’s for, Atkinson explained that MOTO is for investors who recognize the changes coming in transportation. That said, this is not a core holding and most investors that want to invest in the smart transportation revolution will likely want this as a small portion of their overall portfolio.

The SmartETFs Smart Transportation & Technology ETF (MOTO) is now available to trade on NYSE. Learn more about MOTO by visiting SmartETFs webpage.

<<<

>>> Electric Vehicles to Rev Up in 2020: Play These ETFs

Zacks

Sanghamitra Saha

January 9, 2020

https://finance.yahoo.com/news/electric-vehicles-rev-2020-play-130001956.html

With automation and technological breakthrough emerging rapidly, the fast pickup in autonomous vehicles is in the cards. Elon Musk’s Tesla TSLA’s solid growth momentum and amazing one-year stock performance supports the fact.

Electric vehicle maker Tesla's shares have surged 39.9% in the past year, breezing past the S&P 500’s 25.7% (as of Jan 7, 2019). It clearly performed better than other car makers as Ford F was up 10.5%, Honda Motors HMC and General Motors GM were almost flat and Toyota Motor TM gained 15.7%.

Tesla’s previous issues like production delays and heavy financial losses are really a matter of the past. The company delivered approximately 367,500 vehicles last year, marking a notable jump of 50% jump from 2018. The deliveries were within the range of the company’s guidance but higher than Wall Street estimates. The stock has a Zacks Rank #2 (Buy) and a Growth Score of A.