News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

MTE what a beaut stuff's call

CEGE rnd 2?

ACTU chart.

PANC chart.

NSTR chart.

JOEZ chart.

ABK chart.

VYYO chart.

Looks like stocks are headed lower today.

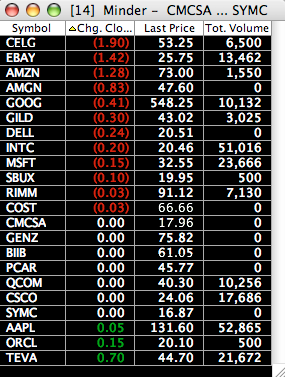

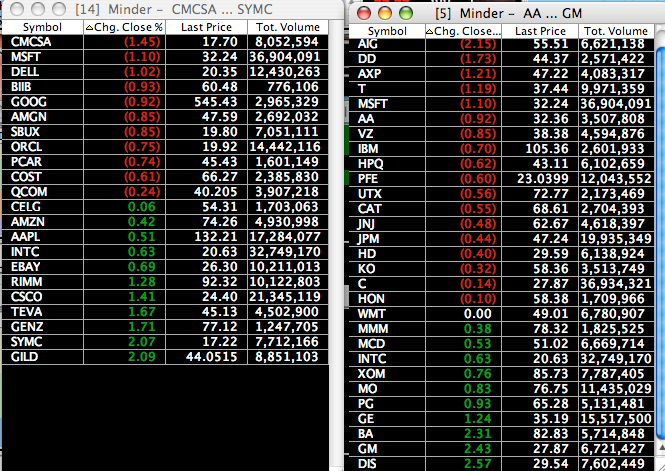

QQQQ components PM screen

HOV my call last week options HOVBB at .85 Now 2.60 over 200%

XLF and RKH IAT thinking about puts for bank write down news when i find its high.

TY bud im curious to see what kinda picks they bring to the table!

lol..you got urself some real playerzzz bud..congrats :D

tell me about it man i had to pay big $ to get them up there LMAO

dude that's some of the best ASSISTANT MOD you got from ihub there LMAO

SPY options on watch for today

Feb 130 puts ticker: SFBNZ

Feb 139 calls TIcker: SFBBI

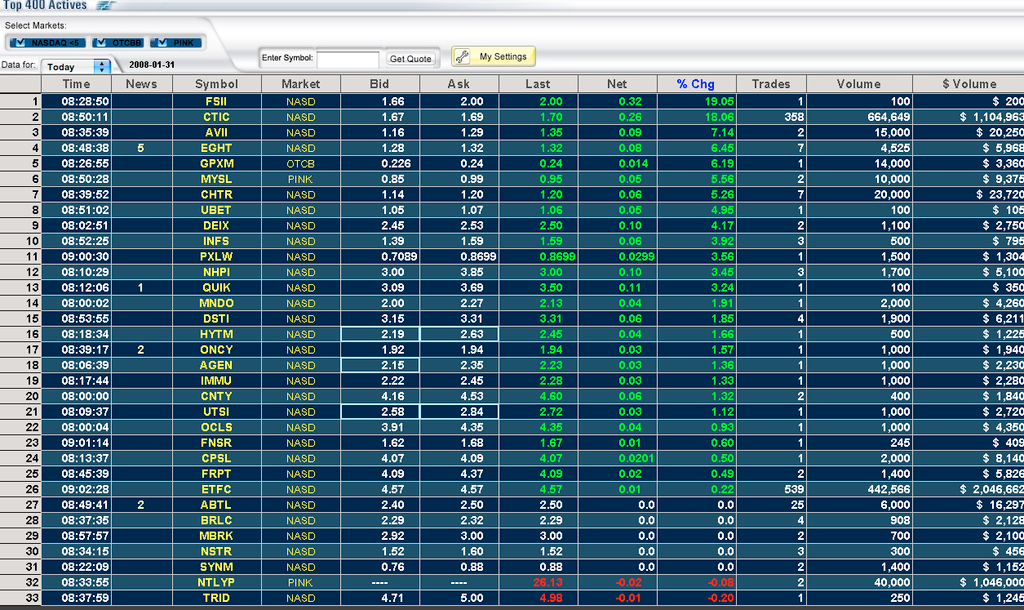

Microcaptrade's premarket movers screenshot.

MBIA Loses $2.3 Billion on Write-Downs

Thursday January 31, 8:12 am ET

By Stephen Bernard, AP Business Writer

MBIA Posts 4Q Loss of $2.3 Billion on Derivatives Write-Down, Growing Loss Reserves

NEW YORK (AP) -- MBIA Inc. reported write-downs of $3.5 billion on souring credit derivatives in the fourth quarter Thursday, raising the possibility that the world's largest bond insurer could lose its top credit rating.

ADVERTISEMENT

Continued weakness in the bond insurance market may put struggling banks in a precarious position. Banks, which have reduced portfolio values by more $140 billion during the second half of 2007 in a deteriorating mortgage market, might be forced to take further write-downs tied to bonds insured by companies like MBIA.

MBIA said it is considering new options to raise capital.

The insurer lost $2.3 billion in the fourth quarter, or $18.61 per share, compared with earnings of $181 million, or $1.32 per share, during the same period the previous year.

Analysts polled by Thomson Financial, on average, forecast a loss of $2.97 per share for the quarter.

Shares fell more than 4 percent, or 60 cents, to $13.36 in pre-market trading.

During the quarter, MBIA reduced the value of its credit portfolios by $3.5 billion, reducing earnings by $18.04 per share. The losses were primarily tied to the reduced value of collateralized debt obligations in its insured portfolio.

So-called CDOs are complex financial instruments that combine various forms of debt.

MBIA also took a $713.5 million pretax loss on its exposure to rising delinquencies and defaults among home equity products. Of the $713.5 million, $100 million was placed in reserve to cover potential future losses.

The beleaguered bond insurer also reduced the value of its 17.4 percent stake in reinsurer Channel Re to $0 from $85.7 million.

"The effect of these reserving and impairment activities on our capital position will be more than offset by the successful completion of our capital plan, which will increase our capital position by well over $2 billion," Gary Dunton, MBIA's chairman and chief executive, said in a statement.

MBIA raised more than $1.5 billion in recent months to try and maintain its critical "AAA" rating. The company raised $1 billion through the offering of surplus notes and another $500 million through a direct investment by private equity firm Warburg Pincus, which closed Wednesday. Warburg Pincus has also pledged to backstop an additional $500 million rights offering.

Oppenheimer & Co. analyst Meredith Whitney said banks' could take up to $70 billion in additional write-downs because of the faltering bond insurers.

Struggles at bond insurers would also make it more expensive for municipalities -- ranging from local governments to school districts -- to raise money to fund new projects.

The bond insurance market is in the midst of a major upheaval after ratings agencies began reviewing their operations during the fourth quarter. Due to rising delinquencies and defaults on mortgages, ratings agencies believe bonds and securities backed by those troubled loans will increasingly default as well, forcing bond insurers to pay out claims.

Bond insurers make principal and interest payments when issuers default. Under extreme loss scenarios, ratings agencies believe many bond insurers do not have enough cash available to pay out claims, which has forced the companies to either raise new capital or face a downgrade from the "AAA" financial strength rating.

Bond insurers essentially need "AAA" ratings to book new business.

Fitch Ratings already downgraded Ambac Financial Group Inc., Security Capital Assurance Ltd. and most recently Financial Guaranty Insurance Co. Both Moody's Investors Service and Standard & Poor's said they are currently reviewing ratings on bond insurers, including MBIA.

For the full year, MBIA lost $1.9 billion, or $15.22 per share, compared with earnings of $819.3 million, or $5.99 per share, in 2006.

Stocks selling off into the open.

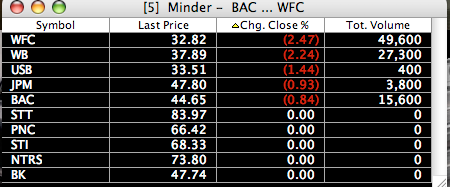

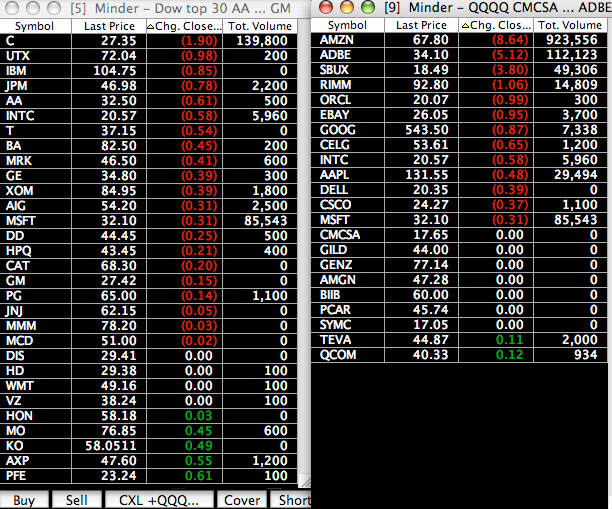

QQQQ DOW components update

Starbucks-SBUX downgraded to Accumulate from Buy@THNK

Jan 31, 2008 7:49:00 AM

View Additional Profiles

Downgrade based on slowing growth profile. Target to $20 from $30.

QQQQ options on watch

Febuary 44.00 calls ticker: QQQBR

Febuary 44.00 Puts ticker: QQQNR

Way early QQQQ and Dow top components actives.

S&P Mulls $500B in Mortgage Downgrades

Wednesday January 30, 5:48 pm ET

S&P Considers Downgrading More Than $500 Billion in Downgrades of Mortgage Debt

NEW YORK (AP) -- Standard & Poor's Ratings Services is considering slashing its rating on more than $500 billion of investments tied to bad mortgage loans, the ratings agency said Wednesday.

The massive downgrade would threaten a broad swath of the world's finance industry, S&P said, ranging from Wall Street's trading desks to regional banks to local credit unions.

ADVERTISEMENT

Ratings from agencies like S&P play a vital role in how much investments are worth. Many funds can only buy investments carrying strong ratings, and some people blame the agencies for granting top-notch credit scores to risky investments during the housing boom.

S&P has downgraded or is considering downgrading $270.1 billion in "mortgage-backed securities," or bonds deriving their payments from home loans. Assuming more people, strapped by the struggling housing market, will not be able to repay their debts, S&P is reviewing 6,389 classes of bonds backed by home loans issued in 2006 and the first half of 2007.

The 238-page list of bonds considered for downgrade includes transactions involving virtually all the major investment banks, including Citigroup Inc., Lehman Brothers Holdings Inc., Bear Stearns Cos., and Merrill Lynch & Co.

The bonds considered for downgrade represent nearly half the bonds of that kind sold between January 2006 and June 2007, S&P said.

The ratings agency has also downgraded or is considering a downgrade of $263.9 billion of collateralized-debt obligations, which are complicated securities splicing payments from a number of different sources, including mortgage-backed bonds.

S&P acknowledged the potential for these downgrades to ripple throughout the world of banking and finance. Banks have already posted $90 billion in losses on these types of mortgage investments, and S&P expects losses to reach $265 billion.

Investors Get a Glimpse of the Future

Yesterday's trading provided a rare opportunity -- a look into the future. The Fed action, as we expected, showed determination to fight recession prospects in an aggressive fashion. The FOMC is attentive both to the current economy and to financial disruptions that could spiral into negative economic effects.

While many traders were poised to bet against a rally from a 50 bp cut, they were quite wrong -- for a while. The market was rallying strongly based not only on the move, but the statement. It is clear that the Fed is attentive and ready for more action if needed. The market rallied strongly and our opinion is that it was poised to go much higher, breaking through technical resistance levels.

That is the important view into the future.

What Happened?

The first thing to understand is that much of the punditry has been wrong about the Fed. The media has been focused upon the question of whether the Fed was "duped" or "fooled" by the unwinding of bad trades at SocGen (SCGLY.PK). We analyzed this and there is plenty of evidence that our view was correct. The Fed is acting in accordance with principles developed by Chairman Bernanke and explained by a colleague in this article. In a conference call to Bear Stearns investors, David Malpass cited the same Mishkin speech we did in our article. The Fed move and statement confirm the reasoning.

The Fed is concerned about disruptions in financial markets and a possible downward spiral that translates markets into economic effects. Briefly put, they are on the case.

The market decline was sparked by a downgrade of FGIC. We highlighted the importance of this concern, noting the stock market rally when a successful plan seemed to be imminent. Lower ratings for bond insurers threaten the asset value of securities held by many firms. Announcements about further downgrades have moved overnight futures even lower, suggesting a weak market opening tomorrow.

What Will Happen?

We expect a solution to this problem simply because there is so much at stake for the counter parties of the bond insurers. The solution is difficult because the financial institutions involved need to agree both upon the design of the plan (investments or a reinsurance pool) and how much each might invest. Yesterday's Wall Street Journal featured an excellent article on the issues.

Federal officials are not yet involved in a bailout plan, so attention is focused on New York Insurance Commissioner Eric Dinallo, now advised by Perella Weinberg Partners. Seeking outside advice makes sense, because a talented insurance commissioner may not have the right skill set for putting together a bailout plan.

Some have confidence in Dinallo and he is well aware of the urgency.

To emphasize, we expect a successful bailout plan because the amount at stake for financial institutions is much greater than the cost of investing in the plan. They will get it done, but the market will be nervous as the story unwinds.

Conclusion

The issues involved in counter-party risk are so great that the market reacts to any whiff of negative news. Bids are pulled, and stocks sell off rapidly.

When there is a resolution to the issues related to bond insurers, investors and traders alike will move back to a focus on economic prospects, future earnings, and Fed policy.

Yesterday's trading gave us a look into the future about the market reaction to these fundamental factors. Those who believe, as we do, that there will be a resolution to the bond insurance problem will see current market levels as an opportunity to buy.

It is so easy to see the problems, and so difficult to see the solutions

holy sh*t....

http://www.ebaumsworld.com/video/watch/82107

BUY THE PUTZZZZ 800lb option gorrillas im tellin yaaaaa

Into the fed meeting going undecided?

QQQQ puts from HOD

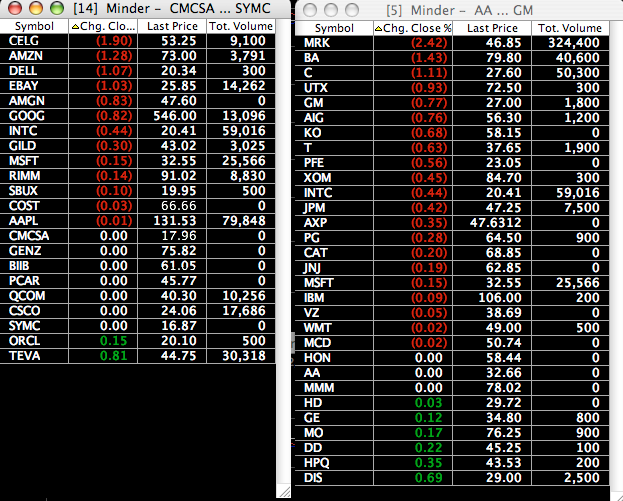

QQQQ and dow components update

SPY options on watch.

CALL - February 137 call SFBBG

PUT - February 135 put SFBNE

Thanks bud hope you're welcome to stop by whenever!

|

Followers

|

3

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

63

|

|

Created

|

01/29/08

|

Type

|

Free

|

| Moderators Jesus Mickey Mouse bugs bunny Big Bird | |||

|

Posts Today

|

0

|

|

Posts (Total)

|

63

|

|

Posters

|

|

|

Moderators

|

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |