News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

MEDH No dilution here!

MedX Holdings, Inc. $MEDH Attention Shareholders: The float is the same it has been the entire year of 2018. There has not been 1 single share diluted (sold) into the market. The day to day trading you see is all retail and has nothing to do with the company. Thanks, Mark

2:07 PM - 26 Nov 2018

MedX Holdings, Inc. $MEDH Attention Shareholders: The float is the same it has been the entire year of 2018. There has not been 1 single share diluted (sold) into the market. The day to day trading you see is all retail and has nothing to do with the company. Thanks, Mark

— MedX Holdings (@MedX_Holdings) November 26, 2018

Right now using the PE avg. in this sector of 22 and the current SP of 0.0165 is= only $150k net profits per qtr. Annual: $600k*22/800m= 0.0165 No diluting since Aug. 2015

Forecast of several million$ with high profit margins.

No insider dumping nor diluting with these forecasts

MCGI No Dilution OS=840 million

Filings are happening.

From the 10Q filed on 5/3/18:

"Additionally, we are working towards to becoming current with all required filings including the January 31, 2018 Form 10-K. With the completion of this process coming to a close, we are presently looking at various strategic options to enhance shareholder value....."

The CEO was the CEO of Jobs.com who raised $100 million from VC's

Warrants were issued at $0.12 and $0.10

Thank you MSN Money for listing Hannover House as one of the top three Most Notable companies in Arkansas!

Always nice to have the mainstream media recognize the value of the Hannover House brand name!

I guess when you've been operating continuously for TWENTY-FIVE years, and with over EIGHT-MILLION (8,000,000) total published / distributed units sold into the marketplace (books and videos combined), you start to become a known commodity to consumers!

https://www.msn.com/en-us/money/companies/the-most-famous-companies-in-every-state-and-dc/ss-BBICksA#image=5 ;

What a great honor to be one of only three companies listed, the others being Walmart Stores, Inc. (arguably the world's largest company based on the dual factors of gross revenues and total employees) and Stephens, Inc., recognized as the largest institutional investor group outside of Wall Street. Two other Fortune 500 companies were skipped over: Tyson Foods and J.B. Hunt... making our designation quite impressive! Go HHSE!

ARKANSASOver in Arkansas, one major company rules the roost: Walmart. The planet's biggest retailer is headquartered in the town of Bentonville. Other leading Arkansas-based businesses include private investment bank Stephens and media distributor Hannover House.

www.MSN.com

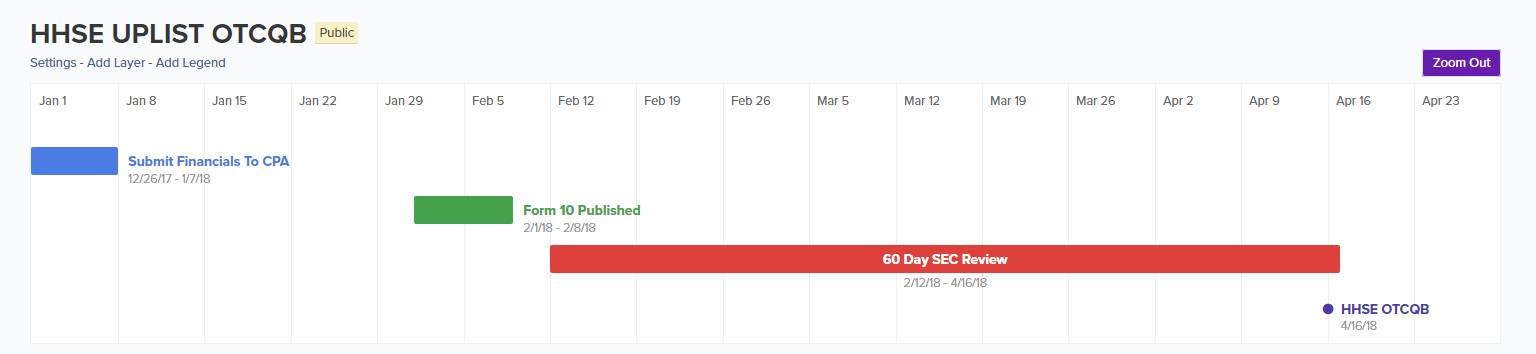

Completion of formatting and overview by outside CPA - covering 2015 Tax Returns, and the full years of 2016 and 2017. This step is expected to be completed this week, with the results handed over (along with the remainder of the audit materials) to our PCAOB firm.

HHSE UPLIST REGISTRATION - The dissolution with Crimson Forest will be completed this week, with a formal termination document that has been mutually approved, and a series of short-form terminations for the individual title agreements (as some had different licensors than Crimson Forest Entertainment Group, Inc.). This will also trigger the long-requested removal of HHSE management names off the Nevada Secretary of State listing as corporate officers. Part of the overall settlement with CRIM involves the reversion of rights in "Where's the Dragon" back to the original licensors... which is why this item has not appeared on any of the HHSE release schedules for the past four months. With the Crimson merger obstacle removed, the next steps for our uplist are as follows:

a). PRE-AUDIT - Completion of formatting and overview by outside CPA - covering 2015 Tax Returns, and the full years of 2016 and 2017. This step is expected to be completed this week, with the results handed over (along with the remainder of the audit materials) to our PCAOB firm.

b). UPDATED LIBRARY REPORT - This step is expected to be completed by Feb. 26, and provided to the auditors as the last item for full delivery.

c). REDRAFTED FORM 10 REGISTRATION - This is already completed, awaiting review by outside S.E.C. counsel, and the auditor's letters.

d). TIMING - Once filed with the S.E.C., the registration becomes effective on the earlier of 60 days, or S.E.C. approval. This will trigger our uplist to OTC: QB and the activation of stock share transfers electronically through the DTC. Management believes that being fully registered, and uplisted away from the Pinksheets, will spark a wave of new investors and funds.

First of all, we'd like to point out that Hannover House is unlike most any other "OTC Pinksheet" listed company. We have been operating continuously since 1993 (24-years) and have been reporting to the OTC Markets since Dec. 2009 (8-years). Statistically, most OTC listed equities are flashes-in-the-pan time wise... lots of Stock Hype / I.R. Promotions, insider share dumps, and quick closures. That's definitely not HHSE.

Thanks, very interesting....

That link doesn't work for me....

Amazon News: VODwiz Niche, Value Just Got Bigger

Exclusive: Amazon Studios to cut back on indie films in programming shift:

https://www.reuters.com/article/us-amazon-com-films-exclusive/exclusive-amazon-studios-to-cut-back-on-indie-films-in-programming-shift-sources-idUSKBN1F70IG ;

This is good news for VODwiz. The value and niche of VODwiz is Independent Films. A niche that just got bigger.

HHSE initial (first year) target is to have 100,000 subscription customers, averaged at $8.50 per month - for annualized gross revenues of $10.2-million.

Go $HHSE

you're welcome...

I did too Harley, looks like a Netflix deal to me....

OS has been the same for over 2 years, reminds me of another stock..lol..

Number of shares of Cord Blood America, Inc. common stock, $0.0001 par value, outstanding as of November 3, 2017, 1,272,066,146 exclusive of treasury shares.

SEC reporter since inception, sitting on $959,534 in cash.

No Toxic notes at all.

https://www.sec.gov/Archives/edgar/data/1289496/000165495417010387/cbai_10q.htm

All SEC filings..

https://www.sec.gov/cgi-bin/browse-edgar?company=cord+blood+america&owner=exclude&action=getcompany

Do you have any info on the share structure and the no dilution that you can share?

Myth,

Thanks for sharing this one, going to check it out now....

HHSE New Ventures - With Sony and Cinedigm handling selected HHSE releases, our management time can be redirected towards theatrical releases, higher-end acquisitions (including productions) and our VODWIZ streaming venture. As will be seen in our 2017 filings, theatrical release activities are the engine that is now driving HHSE revenues in all other arenas. Theatrical titles get more shelf space and priority placement when released to home video; theatrical titles get larger license fees from Netflix and Television licensors; and theatrical titles provide two direct revenue streams for HHSE in the form of both servicing fees and revenue participations. The current mass merchant and key video retail support for "BATTLECREEK" evidences the sales boost that a targeted, limited theatrical release can deliver for the subsequent home video release.

Hannover House Joins Forces with the Producers of the Award-winning Drama, GETTING GRACE, for National Theatrical Launch, March 23

Jan 14, 2018

OTC Disclosure & News Service

-

Acclaimed Comedy from Writer-director Daniel Roebuck Follows a Teenaged Girl with Cancer, Who Forges an Unconventional Approach for Dealing with Her Impending Death.

LOS ANGELES, CA / ACCESSWIRE / January 14, 2018 / Hannover House, Inc. (OTC PINK: HHSE) and theatrical affiliate Medallion Releasing, Inc. have entered into an agreement with Getting Grace, LLC, the production company behind the comedy-drama, ''GETTING GRACE'', for a nationwide theatrical release this spring. The award-winning feature was written, produced and directed by Daniel Roebuck. Roebuck is one of Hollywood's most familiar faces. His acting resume spans 35 years and includes popular television hits (MATLOCK, LOST), blockbuster films (THE FUGITIVE), faith-based films (LET THERE BE LIGHT), horror films (HALLOWEEN 2) and one of the Internet's most watched original series (THE MAN IN THE HIGH CASTLE).

In Getting Grace, Roebuck portrays a small-town mortician whose world is rocked by a rambunctious teenaged girl dying of cancer, as she plans for her departure and a better impact lives for those who will survive her. Newcomer Madelyn Dundon plays the title character of Grace; Marsha Dietlen (LITTLE CHILDREN, NEWLYWEDS) plays Grace's mother, Venus; Duane Whitaker (PULP FICTION, HALLOWEEN II) plays Reverend Osbourne, and Dana Ashbrook (TWIN PEAKS) plays the successful and handsome author who challenges Roebuck's character (Bill) in a duel for the romantic attentions of the lovely Venus.

Roebuck produced the film with a team that included his wife, Tammy Roebuck, as well as Mark Rupp and Davie Cabral. The film was executive produced by Samantha Edwards, Mike Molewski, Mick Trombley, Zach Tran, Melanie Molewski and Robert ''R.J.'' Morris. GETTING GRACE was directed by Daniel Roebuck from a screenplay by himself and award-winning writer, Jeff Lewis.

Getting Grace premiered in September at the Northeast Film Festival in Teaneck, New Jersey, where it won Best Feature, Best Director, Best Actress (Madelyn Dundon) and the Audience Choice awards. The film was also exhibited in competition in October at the Adirondack Film Festival, where it won the coveted ''Best of the Best'' Audience Award, over notable contenders (including LOVING VINCENT).

Hannover House and Medallion Releasing will launch the film to theatres in top USA markets commencing March 23, with a campaign that will include non-traditional promotional events and cross-promotions designed to build audience interest. All of the top 20 largest markets are targeted, along with 20 additional key markets that collectively represent theatrical markets with about 80% of the total U.S. population.

''As a filmmaker, who has spent the last nine years bringing our 'Grace' to an audience, I am thrilled to be teaming with Hannover House and my long-time friend, Eric Parkinson,'' Roebuck recently commented from his Los Angeles home. ''Together we are hoping to make history with our extraordinary and unique approach to building audience interest for this film that has, so far, touched people of all ages and all faiths. We can't wait to share Grace with the rest of world!''

HHSE-DD/Summary: Audits/Form-10, SEC-Compliant, No-Dilution, Sony/Cinedigm, VODWIZ, Uplist OTCQB

Audited Financials = Third (3rd) Party Verification = SEC Reporting Standards

Three (3) Rock Solid Foundations Of HHSE

1.) Successful, Experienced, Respected, Shareholder Friendly Management Dedicated to Building HHSE Based on Business Fundamentals Rather than Stock Promotion.

2.) Since Going Public in 2010, 32 Consecutive Quarters of Revenues & Profitability out of 32.

3.) No Dilution in 2 1/2 Years. No Plans To Ever Again.

HHSE MATURATION TO "THE NEXT LEVEL" ALREADY WELL UNDERWAY

1.) New Business Model

Handling HIGHER PROFILE titles and ORIGINAL PRODUCTIONS. To create better quality titles with the greatest commercial value. End of the micro-budget, direct-to-video market.

2.) NEW DISTRIBUTION PARTNERSHIPS

- Sony Pictures Home Entertainment

- Cinedigm Entertainment

- Random Media (the indie studio headed by former Paramount President Eric Doctorow and indie-film producer Tom Skouras).

3.) HHSE Executve Producers / Worldwide Distributors

- Two different CURRENT Productions.

4.) Two Major Titles In Theatrical Releases.

- a.) "BATTLECREEK"

- b.) "DAISY WINTERS"

5.) Five Genre Titles In Limited Theatrical Releases Soon.

- a.) "BLOODFEAST"

- b.) "CHOSEN"

- c.) "DEATH HOUSE"

- d.) "WHERE'S THE DRAGON?"

- e.) "THE RIOT ACT"

6.) DVD & BluRay New Releases Pipeline (12 Titles, $4,000,000+ Gross Shipments).

"THE LENNON PROJECT", "SACRED HEART", "GETTING GRACE", "BONOBOS" and "ALGERIAN" (now renamed as "SLEEPER CELL"), as well as the romantic comedy "SPICES OF LIBERTY", the Red Bull motorsports actioner "RIDE UNITED", and the also long-awaited "DINOSAURS OF THE JURASSIC". Other home video titles include the thrillers "IDENTITY CRISIS", "MUSE" and "INSOMNIUM".

7.) VODwiz - Online Independent Films Streaming Portal

* Doubled Film Titles In Library (Second only to Amazon at this point).

* VODWIZ has now partnered with Amazon Digital Services for hosting, operations, payment processing and customer service of all activities.

* VODWIZ site now being assembled, prepared and uploaded will feature THREE main categories of programming on the home-page menu:

A.) WATCH - Thousands of feature films and television episodes

B.) LEARN - Educational Programming, Many subjects and achievement levels.

C.) PLAY - Single-player, interactive and group-play VideoGames

* Two User Options:

a.) Pay-Per-Transaction

b.) Monthly Subscription Models

* HHSE initial (first year) target is to have 100,000 subscription customers, averaged at $8.50 per month - for annualized gross revenues of $10.2-million.

https://www.whois.com/whois/vodwiz.tv

8.) New HHSE Staff Hires:

- Tom Sims to Become President of VODWIZ, INC.,

- Engagement of EARL HALE as Technical Services Director for VODWIZ and Hannover House. Earl has an impressive resume in video production, mastering and technical services, including multi-year directorships at Walmart TV and the Media Center of the University of Arkansas Global Campus.

- Desiree Garnier as our Director of Marketing.

9.) Two Major Financing Agreements of Epic Productions (Transform HHSE Profile & Revenues).

- a.) "MOTHER GOOSE"

- b.) "MELTDOWN"

10.) HHSE engaged two professional service advisors to assist Form 10 & Uplist OTCQB.

- CPA Lisa Lashley Higgins has been engaged to review the company's books, records and financial filings covering the years 2015, 2016 and 2017, and to verify compliance with the needs set forth by the company's auditors.

- Attorney Steven H. Kay has been engaged to provide general transactional legal counsel, as well as filings relating to the elimination of contestable debts and prior litigation matters.

11.) HHSE Corporate Governances

* Updated TV & Films Library Valuation

* Audited 2016, 2017 Financials

* SEC Form 10 Registration

* SEC Review (60 Days Maximum)

* HHSE Uplist to OTCQB

Below is a visual timeline organized per my DD. Should roughly be representative of the time frame.

1/14/18 HHSE Press Release:

Award-Winning Drama "GETTING GRACE" Theatrical March 23

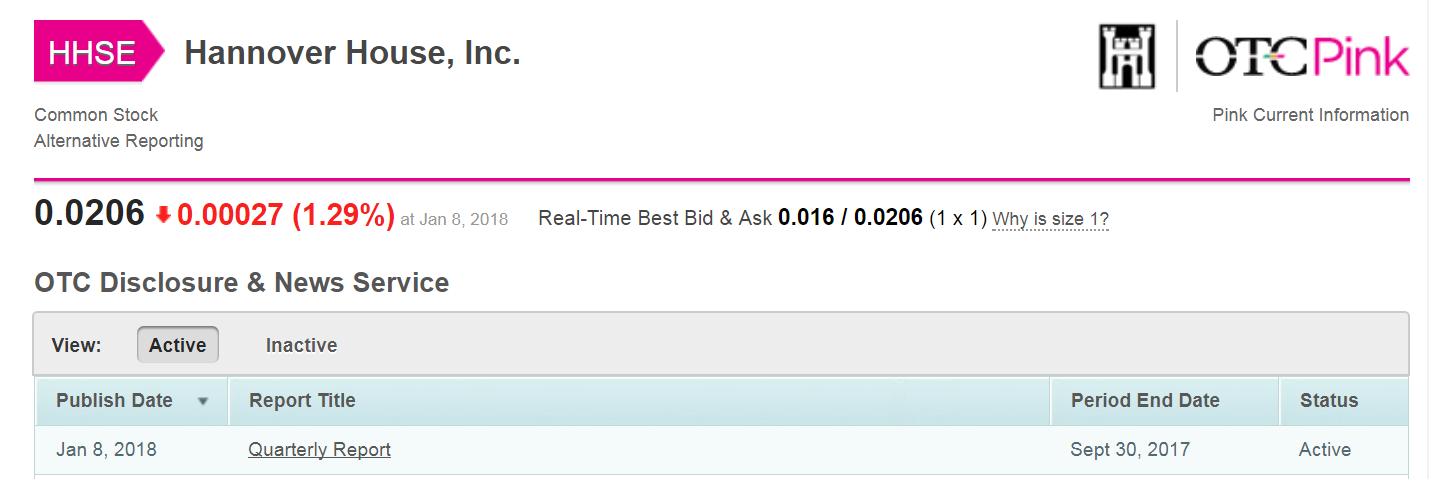

1/8/18 HHSE Filing - 3rd Quarter Report

Q3 Revenues $351,252 Net Income $100,594

1/5/18 HHSE Press Release:

"HHSE Engages Two Advisors To Perform Form 10, Uplist OTCQB Duties"

1/4/18 Two HHSE IR BLOGS:

HHSE Engages Counsel To Dispute Frivolous Lawsuits & Erroneous Debts; Q3 Soon

1/2/18 HHSE IR BLOG:

Preparing 2016/2017 Financials For CPA/Audits, Form_10, Uplist-OTCQB

12/29/17 HHSE Press Release:

Hannover House Epic Horror Feature "DEATH HOUSE" Theatrical Release February 23

12/23/17 HHSE IR BLOG:

HHSE Past, Present, Future

11/22/17HHSE IR BLOG

HHSE NEEDS To UPLIST, but No Dilution By Way Of Merger Required

10/23/17 HHSE IR BLOG

HHSE Board of Directors Approves UPLISTING, Form 10 Costs & Implementation

10/22/17 HHSE IR BLOG

HHSE Maturation "To The Next Level" Already Well Underway

HHSE CEO Eric Parkinson Professional BIOgraphy With Photos

* 51 Producer Credits

* 17 Writer Credits

* 11 Actor Credits

* 8 Director Credits

* More Than 100 Credits (103) Total in All Aspects of Film Entertainment Industry (Must See)

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=137331997

Hannover House (No Dilution 2.5 Years, None Planned)

Market Cap

------------------

Shares In Issue

HHSE Transfer Agent:

HHSE Self Updating Short & Long Term Charts

Daily (Short Term)

Weekly (Long Term)

HHSE

HHSE has not issued any shares in over 2.5 Years

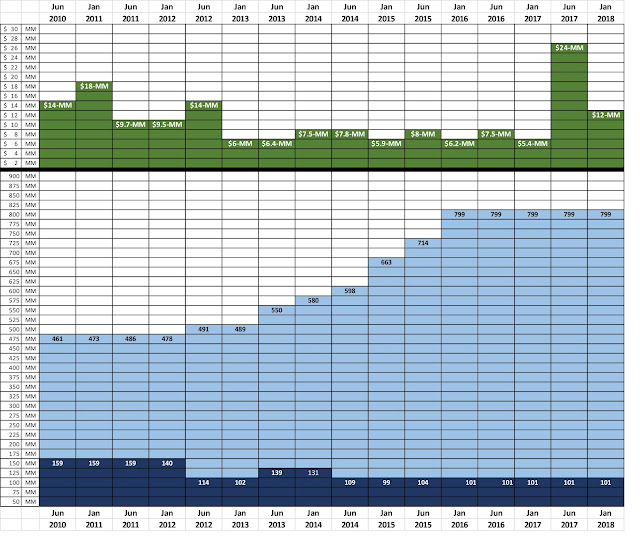

1). Hannover House has Not Issued any Shares in 2.5-years. See the chart below. For the company's first two years as a public equity, the stock structure was quite stable. For the past 2-1/2 years, the stock structure has also been stable. But in 2013 and 2014, the company got involved in some ugly predatory lender situations, most notably TCA Global and JSJ, which precipitated a rapid growth in share issuances. The business model for both TCA and JSJ - as exercised against HHSE and many other borrowers - is to make repayment with cash as difficult as possible, in order to force a "conversion of the debt" into freely trading shares of the issueer at a dramatic discount-to-market. Such returns grossly exceed the legal usury law limitations in all states, and this general business practice is operating in a legally dubious space. JSJ, for instance, refused to accept repayment from HHSE via a bank wire transfer (including all applicable, legal interest per the note), preferring instead to file a lawsuit (in Texas?!), in order to try to force repayment via shares at 200% or more interest. These predatory lenders generally prey on companies that are unable to defend themselves, and therefore are forced to allow the lenders to squeeze out profits far in excess of lending laws through toxic-conversions; most of the time, these small borrowers are ultimately forced out of business. However, this was not the case with Hannover House - as the company has a operating business that is unaffected by fluctuations of our stock price and not dependent on the issuance of shares for capital. These toxic dilutions from 2013 and 2014 definitely hurt our shareholders, and hurt our "market cap," as demonstrated in the charts. So, the Board voted to cease such forms of borrowing, and as a result, HHSE has not issued any new shares in 2.5-years. Anyone predicting on a chat board or anywhere else that a "big dilution is coming" is mistaken.

$HHSE$ --

Yowsa! Mega-Success of "IT" video release spurs THOUSANDS of new orders for HHSE's BATTLECREEK!

Dear HHSE Friends & Followers - This Tuesday was the Video release date for the blockbuster theatrical hit "IT" - starring Bill Skarsgård as the super-scary clown. Consumer response for "IT" has been so substantial that Hannover House has already received new orders for multiple thousands-of-units of "BATTLECREEK" (street date Feb. 6), also starring Bill Skarsgård! The momentum might get even stronger with the February launch of Bill's new TV series, "CASTLE ROCK" from J.J. Abrams, Stephen King and HULU. With "BATTLECREEK" right in the middle of a media-feeding-frenzy for Bill Skarsgård - this title looks to be positioned as a very successful video release for Hannover House!

HC, gonna be huge when the uplist happens!!!!

Go HHSE!!!!

I really like the looks of this trailer....could be the best movie yet for HHSE!!!! Lots in the pipeline!

CBAI.....

check it out...

Great stock on the verge of a breakout...bigtime

Go HHSE!

Nice! How many other OTC stocks can say they don't need to dilute shareholders!

HHSE The Board believes that Fully Registered Shares will be more attractive to HHSE program suppliers and investors - as well as to institutional investors and hedge funds - and that pursuing these activities now is a good use of ongoing cash flows

HHSE-UPLIST-OTCQB:

Audited Financials = Third (3rd) Party Verification = SEC Reporting Standards

HHSE Successful, Experienced, Respected, Shareholder Friendly Management Dedicated to Building HHSE Based on Business Fundamentals Rather than Stock Promotion.

HHSE Since Going Public in 2010, 32 Consecutive Quarters of Revenues & Profitability out of 32.

BLOG: Audits/Form-10, UPLIST, No-Dilution, Robust-Pipeline, VODwiz, Distribution Partnerships

*** NOTE: NOT Verbatim, several lines omitted ***

Saturday, December 23, 2017

Where we have been... Where we are now... and Where we are going at HHSE...

Greetings HHSE Friends & Followers:

As we reflect back on 2017, HHSE Management is taking a few days to look at our past, present and future activities to help guide sage decisions. 2017 has been a momentous year for the company - due in large part to the attempted (but terminated) merger with Crimson Forest, and the subsequent re-focus of the company's primary activities and revenue streams.

Looking much further back - five, six, seven years and more - and looking forward in time for an equal time-frame, we can see trends and opportunities for HHSE and our shareholders.

First of all, we'd like to point out that Hannover House is unlike most any other "OTC Pinksheet" listed company. We have been operating continuously since 1993 (24-years) and have been reporting to the OTC Markets since Dec. 2009 (8-years). Statistically, most OTC listed equities are flashes-in-the-pan time wise... lots of Stock Hype / I.R. Promotions, insider share dumps, and quick closures. That's definitely not HHSE.

So, let's take a few minutes to take a high-altitude look at the Company and where we are going.

WHAT IS OUR PLAN FOR GROWTH IN 2018 AND BEYOND?

* We believe that HHSE is "one film away" from being a major independent studio. All it takes is any one of the many titles in our current release queue to become a surprise box officer performer such as "Lady Bird" or "Get Out" and we are suddenly a $100-MM company.

* We have an impressive slate of titles for 2018 and 2019 - and two terrific distribution partners for North America (Cinedigm Entertainment and Sony Pictures Home Entertainment) - as well as our direct relationships with all of the major theatre exhibition chains. Our "lower-end" titles are much higher profile than in past years... and our higher-end titles are now genuine theatrical caliber contenders. We are positioned for the proverbial lucky break that happens when the right film is released at the right time...

* Our recently re-focused Theatrical Release model is delivering huge benefits to our ancillary revenues... and our new partnerships with indie labels is providing access for the VODWIZ streaming venture, which truly could become "the tail that wagged the dog" for HHSE shareholders.

What else is worth noting for this long, holiday weekend? Here are a few observations:

1). Hannover House has Not Issued any Shares in 2.5-years. See the chart below. For the company's first two years as a public equity, the stock structure was quite stable. For the past 2-1/2 years, the stock structure has also been stable. But in 2013 and 2014, the company got involved in some ugly predatory lender situations, most notably TCA Global and JSJ, which precipitated a rapid growth in share issuances. The business model for both TCA and JSJ - as exercised against HHSE and many other borrowers - is to make repayment with cash as difficult as possible, in order to force a "conversion of the debt" into freely trading shares of the issueer at a dramatic discount-to-market. Such returns grossly exceed the legal usury law limitations in all states, and this general business practice is operating in a legally dubious space. JSJ, for instance, refused to accept repayment from HHSE via a bank wire transfer (including all applicable, legal interest per the note), preferring instead to file a lawsuit (in Texas?!), in order to try to force repayment via shares at 200% or more interest. These predatory lenders generally prey on companies that are unable to defend themselves, and therefore are forced to allow the lenders to squeeze out profits far in excess of lending laws through toxic-conversions; most of the time, these small borrowers are ultimately forced out of business. However, this was not the case with Hannover House - as the company has a operating business that is unaffected by fluctuations of our stock price and not dependent on the issuance of shares for capital. These toxic dilutions from 2013 and 2014 definitely hurt our shareholders, and hurt our "market cap," as demonstrated in the charts. So, the Board voted to cease such forms of borrowing, and as a result, HHSE has not issued any new shares in 2.5-years. Anyone predicting on a chat board or anywhere else that a "big dilution is coming" is mistaken.

2). It Doesn't Take Much to Double or Triple the HHSE Share Price - Look at the market-cap spike for HHSE stock earlier this year (seen as June, 2017). This increase in PPS was due to shareholder excitement about the prospect that a merger with Crimson Forest would provide HHSE with high-profile films to distribute. The growth in PPS was not based on any increase in revenues (in fact, the time-distraction of the Crimson merger caused many 2017 releases to be delayed). The PPS spike was driven solely by enthusiasm.

3). Does HHSE Need a Merger Partner? - If the right opportunity came along that would provide HHSE with a reliable source of high-end theatrical titles, we would be responsive to consider such opportunities. However, the programing philosphy ultimately revealed by Crimson Forest did not conform to North American market conditions, in HHSE's opinion. When the promised operating funding didn't materialize, the promised high-end productions turned into low-end films, and the promised "big" releases all turned out to be Mandarin-language releases, we knew that the partnership would not deliver what HHSE wanted for our step-up to major independent status.

4). What's in Store for the first half of 2018?

a). Release Activities: January will see the theatrical release of "BLOODFEAST" - delayed since July due to MPAA re-cut needs. February will see a massive placement of DVDs and BluRays for "BATTLECREEK" (street date Feb. 6). That same week, on Friday (Feb. 9), HHSE will commence the initla theatrical launch of "DEATH HOUSE" to theatres. In April, three titles will be released via Sony Pictures Home Entertainment (including "DAISY WINTERS"); in May, HHSE will release "THE RIOT ACT" to theatres and Cinedigm will release DVD's and BluRays of "THE LENNON PROJECT" for the Company. Other titles in queue for theatrical and / or home video during the first half of 2018 include "MUSE", "INSOMNIUM", "IDENTITY CRISIS", "SLEEPER CELL", "DINOSAURS OF THE JURASSIC" and "SACRED HEARTS" (all but the last title were planned for 2017, but delayed during the Crimson merger pursuit).

b). Corporate Governance: HHSE will be re-filing a Form 10 Registration with two full years of audits (2016 and 2017) early this coming year, during the first few weeks; the CPA review is already underway and much of the documentation and procedural steps for the audit were already assembled during 2017 while planning for the Crimson merger. We feel that a registration of the shares and the subsequent uplist to OTC:QB will attract more investors and some institutional funds... resulting in a higher anticipated daily trading volume, and a predicted much higher HHSE stock price (based on business results, industry fundamentals and the proven power of Shareholder Enthusiasm).

c). New Ventures - With Sony and Cinedigm handling selected HHSE releases, our management time can be redirected towards theatrical releases, higher-end acquisitions (including productions) and our VODWIZ streaming venture. As will be seen in our 2017 filings, theatrical release activities are the engine that is now driving HHSE revenues in all other arenas. Theatrical titles get more shelf space and priority placement when released to home video; theatrical titles get larger license fees from Netflix and Television licensors; and theatrical titles provide two direct revenue streams for HHSE in the form of both servicing fees and revenue participations. The current mass merchant and key video retail support for "BATTLECREEK" evidences the sales boost that a targeted, limited theatrical release can deliver for the subsequent home video release.

5). Thoughts on the HHSE Stock Chart - The chart below is divided into two sections. The top section shows the "approximate market cap" at six-month intervals beginning in June 2010 and continuing through to this week. The Market Cap was calculated by the total of all shares in issue, multiplied by the closing price of the stock during a one-week period during the stated month. The bottom section of the chart shows the total SHARES IN ISSUE for the company during this same time frame. The dark-blue shares represent those that are "restricted" from sale, and the light-blue shares represent the total share count of restricted plus unrestricted shares for that time period.

Perhaps the most visible trends to see on this chart are that the company did very little in share issuances for the first two years... and none for the past 2.5-years - as seen by the flat-line of total shares in issue.

The next interesting item of note is the tremendous PPS Spike that occurred earlier this year, at which time the Market Cap jumped from $5.4-MM to $24-MM in just a few month's time. What's interesting about this result is that the company was functionally frozen from new releases during that time, so the sudden shareholder enthusiasm cannot be attributed to improved revenues... it can only be viewed as a reaction to the prospective merger with Crimson. The current Market Cap of $12.4-MM has been stable for quite a few months now.

A third observation can be seen during the "heavy dilution" time-frames of 2013 to the end of 2015, when TCA (via MAGNA) and JSJ were flooding the market with toxic-conversion shares. What is interesting about this? Well, the market cap stayed surprisingly stable during this dilution... meaning that the average PPS went DOWN while the total float went UP, but the overall Market Cap remained steady. HHSE Management believes that the Market Cap remained relatively steady during these dilution times due to Investor Relations / Stock Promotions. As the toxic-lenders dumped their HHSE shares onto the market, some effort was being expended (by them or third parties) to create an investor market for their share dumps... which is another reason why HHSE management hates the concept of these toxic-conversion notes. It also answers the question that some shareholders have posted to HHSE management over the past few years about "why aren't you doing IR / Stock PR now?" The answer is that we are are focused on building the fundamentals of the business rather than on creating a momentary spike in PPS interest while some third party lender dumps out shares. We are not philosophically opposed to I.R. and new investor outreach. We just feel that the cost of such promotions would be best utilized after our Registration and other major events in the works.

There are more thoughts and developments to share... watch this blog over the holidays, and watch for news releases occuring between Christmas and New Years, as well as during the first week of January. Happy Holidays / Merry Christmas / Happy New Year and Best Wishes to all our HHSE shareholders!

http://hannoverhousemovies.blogspot.com/2017/12/where-we-have-been-where-we-are-now-and.html

HHSE

HHSE: “GETTING GRACE” Moneymaker

BLOG-9/11/17: "GETTING GRACE" Wins-All-Top-Four Categories NYC-Metro Film Festival

Monday, September 11, 2017

GETTING GRACE wins all top four categories at NYC-Metro Film Festival

HHSE Congratulates our good friend, actor-director DANIEL ROEBUCK on your victorious SWEEP of all four top awards this past weekend at the NORTHEAST FILM FESTIVAL (NYC- NJ Metro). WOW! What a great way to launch your inspiring movie! GETTING GRACE... well, I guess they GOT it!!!

AUDIENCE FAVORITE

BEST ACTRESS

BEST DIRECTOR

BEST FEATURE

http://www.nefilmfestival.com/

http://hannoverhousemovies.blogspot.com/2017/09/getting-grace-wins-all-top-four.html

HHSE

HHSE-Where we have been... Where we are now... and Where we are going at HHSE...

WHAT IS OUR PLAN FOR GROWTH IN 2018 AND BEYOND?

* We believe that HHSE is "one film away" from being a major independent studio. All it takes is any one of the many titles in our current release queue to become a surprise box officer performer such as "Lady Bird" or "Get Out" and we are suddenly a $100-MM company.

* We have an impressive slate of titles for 2018 and 2019 - and two terrific distribution partners for North America (Cinedigm Entertainment and Sony Pictures Home Entertainment) - as well as our direct relationships with all of the major theatre exhibition chains. Our "lower-end" titles are much higher profile than in past years... and our higher-end titles are now genuine theatrical caliber contenders. We are positioned for the proverbial lucky break that happens when the right film is released at the right time...

* Our recently re-focused Theatrical Release model is delivering huge benefits to our ancillary revenues... and our new partnerships with indie labels is providing access for the VODWIZ streaming venture, which truly could become "the tail that wagged the dog" for HHSE shareholders.

What else is worth noting for this long, holiday weekend? Here are a few observations:

1). Hannover House has Not Issued any Shares in 2.5-years.For the company's first two years as a public equity, the stock structure was quite stable. For the past 2-1/2 years, the stock structure has also been stable. But in 2013 and 2014, the company got involved in some ugly predatory lender situations, most notably TCA Global and JSJ, which precipitated a rapid growth in share issuances. The business model for both TCA and JSJ - as exercised against HHSE and many other borrowers - is to make repayment with cash as difficult as possible, in order to force a "conversion of the debt" into freely trading shares of the issueer at a dramatic discount-to-market. Such returns grossly exceed the legal usury law limitations in all states, and this general business practice is operating in a legally dubious space. JSJ, for instance, refused to accept repayment from HHSE via a bank wire transfer (including all applicable, legal interest per the note), preferring instead to file a lawsuit (in Texas?!), in order to try to force repayment via shares at 200% or more interest. These predatory lenders generally prey on companies that are unable to defend themselves, and therefore are forced to allow the lenders to squeeze out profits far in excess of lending laws through toxic-conversions; most of the time, these small borrowers are ultimately forced out of business. However, this was not the case with Hannover House - as the company has a operating business that is unaffected by fluctuations of our stock price and not dependent on the issuance of shares for capital. These toxic dilutions from 2013 and 2014 definitely hurt our shareholders, and hurt our "market cap," as demonstrated in the charts. So, the Board voted to cease such forms of borrowing, and as a result, HHSE has not issued any new shares in 2.5-years. Anyone predicting on a chat board or anywhere else that a "big dilution is coming" is mistaken.

2). It Doesn't Take Much to Double or Triple the HHSE Share Price - Look at the market-cap spike for HHSE stock earlier this year (seen as June, 2017). This increase in PPS was due to shareholder excitement about the prospect that a merger with Crimson Forest would provide HHSE with high-profile films to distribute. The growth in PPS was not based on any increase in revenues (in fact, the time-distraction of the Crimson merger caused many 2017 releases to be delayed). The PPS spike was driven solely by enthusiasm.

3). Does HHSE Need a Merger Partner? - If the right opportunity came along that would provide HHSE with a reliable source of high-end theatrical titles, we would be responsive to consider such opportunities. However, the programing philosphy ultimately revealed by Crimson Forest did not conform to North American market conditions, in HHSE's opinion. When the promised operating funding didn't materialize, the promised high-end productions turned into low-end films, and the promised "big" releases all turned out to be Mandarin-language releases, we knew that the partnership would not deliver what HHSE wanted for our step-up to major independent status.

4). What's in Store for the first half of 2018?

a). Release Activities: January will see the theatrical release of "BLOODFEAST" - delayed since July due to MPAA re-cut needs. February will see a massive placement of DVDs and BluRays for "BATTLECREEK" (street date Feb. 6). That same week, on Friday (Feb. 9), HHSE will commence the initla theatrical launch of "DEATH HOUSE" to theatres. In April, three titles will be released via Sony Pictures Home Entertainment (including "DAISY WINTERS" ; in May, HHSE will release "THE RIOT ACT" to theatres and Cinedigm will release DVD's and BluRays of "THE LENNON PROJECT" for the Company. Other titles in queue for theatrical and / or home video during the first half of 2018 include "MUSE", "INSOMNIUM", "IDENTITY CRISIS", "SLEEPER CELL", "DINOSAURS OF THE JURASSIC" and "SACRED HEARTS" (all but the last title were planned for 2017, but delayed during the Crimson merger pursuit).

b). Corporate Governance: HHSE will be re-filing a Form 10 Registration with two full years of audits (2016 and 2017) early this coming year, during the first few weeks; the CPA review is already underway and much of the documentation and procedural steps for the audit were already assembled during 2017 while planning for the Crimson merger. We feel that a registration of the shares and the subsequent uplist to OTC:QB will attract more investors and some institutional funds... resulting in a higher anticipated daily trading volume, and a predicted much higher HHSE stock price (based on business results, industry fundamentals and the proven power of Shareholder Enthusiasm).

c). New Ventures - With Sony and Cinedigm handling selected HHSE releases, our management time can be redirected towards theatrical releases, higher-end acquisitions (including productions) and our VODWIZ streaming venture. As will be seen in our 2017 filings, theatrical release activities are the engine that is now driving HHSE revenues in all other arenas. Theatrical titles get more shelf space and priority placement when released to home video; theatrical titles get larger license fees from Netflix and Television licensors; and theatrical titles provide two direct revenue streams for HHSE in the form of both servicing fees and revenue participations. The current mass merchant and key video retail support for "BATTLECREEK" evidences the sales boost that a targeted, limited theatrical release can deliver for the subsequent home video release.

5). Thoughts on the HHSE Stock Chart: (abbreviated) The company did very little in share issuances for the first two years... and none for the past 2.5-years - as seen by the flat-line of total shares in issue.

The next interesting item of note is the tremendous PPS Spike that occurred earlier this year, at which time the Market Cap jumped from $5.4-MM to $24-MM in just a few month's time. What's interesting about this result is that the company was functionally frozen from new releases during that time, so the sudden shareholder enthusiasm cannot be attributed to improved revenues... it can only be viewed as a reaction to the prospective merger with Crimson. The current Market Cap of $12.4-MM has been stable for quite a few months now.

A third observation can be seen during the "heavy dilution" time-frames of 2013 to the end of 2015, when TCA (via MAGNA) and JSJ were flooding the market with toxic-conversion shares. What is interesting about this? Well, the market cap stayed surprisingly stable during this dilution... meaning that the average PPS went DOWN while the total float went UP, but the overall Market Cap remained steady. HHSE Management believes that the Market Cap remained relatively steady during these dilution times due to Investor Relations / Stock Promotions. As the toxic-lenders dumped their HHSE shares onto the market, some effort was being expended (by them or third parties) to create an investor market for their share dumps... which is another reason why HHSE management hates the concept of these toxic-conversion notes. It also answers the question that some shareholders have posted to HHSE management over the past few years about "why aren't you doing IR / Stock PR now?" The answer is that we are are focused on building the fundamentals of the business rather than on creating a momentary spike in PPS interest while some third party lender dumps out shares. We are not philosophically opposed to I.R. and new investor outreach. We just feel that the cost of such promotions would be best utilized after our Registration and other major events in the works.

There are more thoughts and developments to share... watch this blog over the holidays, and watch for news releases occuring between Christmas and New Years, as well as during the first week of January. Happy Holidays / Merry Christmas / Happy New Year and Best Wishes to all our HHSE shareholders!

http://hannoverhousemovies.blogspot.com/2017/...w-and.html

HHSE -- NO DILUTION in over 2.5 years!

1). Hannover House has Not Issued any Shares in 2.5-years. See the chart below. For the company's first two years as a public equity, the stock structure was quite stable. For the past 2-1/2 years, the stock structure has also been stable. But in 2013 and 2014, the company got involved in some ugly predatory lender situations, most notably TCA Global and JSJ, which precipitated a rapid growth in share issuances. The business model for both TCA and JSJ - as exercised against HHSE and many other borrowers - is to make repayment with cash as difficult as possible, in order to force a "conversion of the debt" into freely trading shares of the issueer at a dramatic discount-to-market. Such returns grossly exceed the legal usury law limitations in all states, and this general business practice is operating in a legally dubious space. JSJ, for instance, refused to accept repayment from HHSE via a bank wire transfer (including all applicable, legal interest per the note), preferring instead to file a lawsuit (in Texas?!), in order to try to force repayment via shares at 200% or more interest. These predatory lenders generally prey on companies that are unable to defend themselves, and therefore are forced to allow the lenders to squeeze out profits far in excess of lending laws through toxic-conversions; most of the time, these small borrowers are ultimately forced out of business. However, this was not the case with Hannover House - as the company has a operating business that is unaffected by fluctuations of our stock price and not dependent on the issuance of shares for capital. These toxic dilutions from 2013 and 2014 definitely hurt our shareholders, and hurt our "market cap," as demonstrated in the charts. So, the Board voted to cease such forms of borrowing, and as a result, HHSE has not issued any new shares in 2.5-years. Anyone predicting on a chat board or anywhere else that a "big dilution is coming" is mistaken.

|

Followers

|

6

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

40

|

|

Created

|

01/07/16

|

Type

|

Free

|

| Moderator Head Clown | |||

| Assistants justincase | |||

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |