News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Beacon Roofing Supply - >>> Small-cap fund manager tunes out market ‘noise’ in bid to find quality companies

By Philip van Doorn

Feb 18, 2017

http://www.marketwatch.com/story/small-cap-fund-manager-tunes-out-market-noise-in-bid-to-find-quality-companies-2017-02-16?siteid=yhoof2

Bassett, who helps manage the $1.7 billion Aberdeen U.S. Small Cap Equity Fund from Philadelphia, shared three of his favorite stocks held by the fund in an interview Feb. 14:

Beacon Roofing Supply

Beacon Roofing Supply Inc. BECN, of Herndon, Va., has a market value of $2.7 billion. The company grew its sales per share by 36% during 2016, according to FactSet.

“We have always liked how they were able to consolidate a fragmented industry,” Bassett said. In October 2015, the company completed the acquisition of Roofing Supply Group, which Bassett said was its largest private competitor.

“That has given them the ability to leverage back-office costs, distribution, technology, etc., allowing them to [improve] economies of scale,” he said, adding that a reduction in debt has set up further margin improvement. This makes the company “slightly less dependent on macro factors” over the next two years, Bassett said.

Beacon’s shares closed at $45.32 on Feb. 14 and traded for 16.9 times the consensus 2018 earnings estimate of $2.69 a share, among analysts polled by FactSet.

<<<

>>> Beacon Roofing Supply, Inc., together with its subsidiaries, distributes residential and non-residential roofing materials, and other complementary building materials to contractors, home builders, retailers, and building materials suppliers. The company?s residential roofing products include asphalt shingles, synthetic slates and tiles, clay and concrete tiles, slates, nail base insulations, metal roofing, felts, synthetic underlayment, wood shingles and shakes, nails and fasteners, metal edgings and flashings, prefabricated flashings, ridges and soffit vents, and other accessories. Its non-residential roofing products comprise single-ply roofing, asphalt, metal, modified bitumen, and build-up roofing products; cements and coatings; flat stock and tapered insulations; commercial fasteners; metal edges and flashings; smoke/roof hatches; roofing tools; sheet metal products, including copper, aluminum, and steel; and PVC, thermoplastic olefin, and ethylene propylene diene monomer membrane products. The company also provides complementary building products, such as vinyl, wood, and fiber cement sidings; and stone veneers, windows, doors, skylights, and gutters and downspouts, as well as decking and railing, water proofing, building insulation, and millwork products. In addition, it offers value-added services primarily, including advice and assistance on product identification, specification, and technical support; job site delivery, rooftop loading, and logistical services; tapered insulation design and related layout services; metal fabrication and related metal roofing design and layout services; trade credit; and marketing support for contractors. As of September 30, 2016, the company operated through a network of 368 branches in 46 states of the United States and 6 provinces in Canada. Beacon Roofing Supply, Inc. was founded in 1928 and is headquartered in Herndon, Virginia. <<<

>>> Apogee Enterprises, Inc. designs and develops glass solutions for enclosing commercial buildings and framing art in the United States, Canada, and Brazil. The company operates through four segments: Architectural Glass, Architectural Services, Architectural Framing Systems, and Large-Scale Optical Technologies (LSO). The Architectural Glass segment fabricates coated and high-performance glass used in customized windows and wall systems comprising the outside skin of commercial, institutional, and multi-family residential buildings. The Architectural Services segment designs, engineers, fabricates, and installs the walls of glass, windows, and other curtain wall products making up the outside skin of commercial and institutional buildings. The Architectural Framing Systems segment designs, engineers, fabricates, and finishes the aluminum frames used in customized aluminum and glass windows, curtain walls, storefronts, and entrance systems comprising the outside skin, as well as entrances of commercial, institutional, and multi-family residential buildings. The LSO segment manufactures value-added glass and acrylic products for the custom picture framing and fine art markets. The company?s products and services are primarily used in commercial buildings, such as office towers, hotels, and retail centers; and institutional buildings, including education facilities and dormitories, health care facilities, and government buildings, as well as multi-family buildings. It markets its architectural products and services through direct sales force, independent sales representatives, and distributors to general contractors and glazing subcontractors, architects, and building owners; and value-added glass and acrylics through retail chains, picture framing shops, and independent distributors to museums, and public and private galleries. Apogee Enterprises, Inc. was founded in 1949 and is headquartered in Minneapolis, Minnesota <<<

>>> Evictions by Wall-Street Mega-Landlords Soar, Financialization of Rents Cause “Housing Instability”: Atlanta Fed

by Wolf Richter

Jan 7, 2017

http://wolfstreet.com/2017/01/07/evictions-by-wall-street-mega-landlords-soar-financialization-of-rents-cause-housing-instability-atlanta-fed/

It blames the Fed & Bernanke; the dark side of “healing” the housing market.

The housing collapse during the Financial Crisis keeps on giving. On Friday, Invitation Homes, a creature of private-equity firm Blackstone, and largest landlord of single-family rental homes in the US, filed with the SEC to raise up to $1.5 billion in an IPO. Deutsche Bank, JP Morgan, BofA Merrill Lynch, Goldman Sachs, Wells Fargo, Credit Suisse, Morgan Stanley, and RBC Capital Markets are the joint bookrunners and get to cash in on the fees.

Invitation Homes, founded in 2012, now owns 48,431 single-family homes, according to the filing. It bought them out of foreclosure and turned them into rental properties, concentrated in 12 urban areas. Revenues for the nine months through September 30 rose 11.4% to $655 million, producing a net loss of $52 million. It lists $9.7 billion in single-family properties and $7.7 billion in debt.

Blackstone was a pioneer in the post-Financial Crisis buy-to-rent scheme, including issuing the first rent-backed structured securities in November 2013. The collateral for the $479-million deal was rental income from 3,207 homes. Blackstone paid rating agencies Moody’s, Kroll, and Morningstar to rate the bonds; so nearly 60% of the debt was rated AAA. Other tranches carried lower ratings. The overall cost of capital to Blackstone from the securitization of these rents was about 2.01%. Cheap money! Thank you hallelujah QE and ZIRP.

Rent-backed securities have since become a common funding mechanism.

Other players in the buy-to-rent scheme have already gone public. American Homes 4 Rent, which owns about 48,000 rental houses in 22 states, went public in August 2013. It has produced a net loss every year since, sports negative EPS of -25 cents and a negative PE ratio of -84.

Starwood Waypoint Residential Trust was spun off from Starwood Property Trust Inc. and started trading in February 2014. In 2016, it merged with Thomas Barrack’s Colony Capital and changed its name to Colony Starwood Homes. Colony is now the third-largest single-family landlord. It too has lost money every year since going public, has negative EPS of -47 cents and a negative PE ratio of -62. Colony founder Barrack is now chairman of Trump’s inauguration committee.

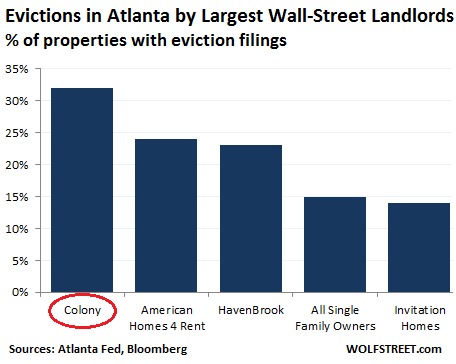

But there’s a drawback: 32% of Colony’s properties in Atlanta and adjacent suburbs have eviction filings, by far the highest rate among the Wall Street landlords, according to a study by the Atlanta Fed on the impact of Wall Street landlords on surging “housing instability.”

The report doesn’t name names, but Ben Miller, co-author of the report, filled in the blanks for Bloomberg. Next in line in eviction rates: American Homes 4 Rent, HavenBrook, owned by Pimco, and Invitations Homes. The percentage of properties with eviction filings in Atlanta by the largest Wall-Street landlords:

The report indicated that eviction rates in some other cities are lower. But this being the Atlanta Fed, it focused on Atlanta, one of the hotbeds of the buy-to-rent scheme. And it focused on single-family rentals because Wall Street’s muscling into this space is new and perhaps a generational shift in the US housing market.

So how did this Wall Street landlord nirvana – and the ensuing “housing instability” – come about after the housing bust? The report blames the Fed, and Fed Chairman Ben Bernanke:

In unwinding their bank-owned properties, the GSEs [Fannie Mae, Freddy Mac, etc.], U.S. Treasury, and Federal Reserve innovated new structured transactions for disposing of hundreds of thousands of bank-owned homes, also known as real estate owned (REO). The Federal Reserve was the first to suggest that private equity firms were the one group with cash on hand to invest in foreclosed homes (Bernanke, 2012).

In 2012, the Federal Housing Finance Agency (FHFA), conservator of the GSEs, issued a pilot to develop structured transactions that could be used to sell its REO homes in bulk. The private market followed by developing and standardizing financial instruments to allow broader market investment in converting foreclosed homes into single-family rentals. Rental housing, traditionally the purview of mom-and-pop landlords, caught the attention of large financial firms.

Nationwide, an estimated 350,000 homes were purchased by institutional investors from 2011 to 2013, and these were spatially concentrated in cities like Atlanta with high numbers of bank-owned homes and the prospect of future home price appreciation. Today there is high concentration in the single-family rental business, with an estimated 170,000 single-family rental homes owned by the seven largest firms.

“My hope was that these private equity firms would provide a new kind of rental housing for people who couldn’t – or didn’t want to – buy during the housing recovery,” Elora Raymond, the report’s lead author, told Bloomberg. “Instead, it seems like they’re contributing to housing instability in Atlanta, and possibly other places.”

Evictions are cheap in Atlanta: about $85 in court fees and another $20 to have the tenant ejected, report co-author Michael Lucas told Bloomberg, which added: “With few of the tenant protections of places like New York, a family can find itself homeless in less than a month.”

The report points at the broader implications beyond poor neighborhoods: While “evictions are highly correlated with neighborhood characteristics such as education levels, change in the employment-population rate, and racial composition,” Wall Street landlords still filed for evictions at higher rates than smaller landlords after accounting for “property and neighborhood characteristics.” Why? The report:

One possible reason large corporate landlords backed by institutional investors may have higher eviction filing notices is that they may routinely use eviction notices as a rent collection strategy.

Bloomberg adds:

In interviews and court filings, renters and housing advocates said that some investment firms are impersonal and unresponsive, slow to make necessary repairs and quick to evict tenants who withhold rent because of complaints about maintenance.

“They want to get them out quickly if they can’t pay,” explained Aaron Kuney, a former executive of HavenBrook and now CEO of PE landlord Piedmont Asset Management in Atlanta. “Finding people these days to rent your homes is not a problem.”

Then there’s the expense of housing, which has soared, thanks to the Fed’s efforts to “heal” the housing market. According to the report, 53.4% of renters were “cost burdened in Atlanta” in 2014. More generally, homeownership has declined to a 51-year low, and “demand for rentals has caused urban rents to increase sharply”:

During the 2010 to 2014 period, low-cost rentals in Atlanta declined by more than 15%. Gentrification, or the influx of wealthier residents accompanied by rising property prices and the displacement of existing, lower-income residents, can be a factor in evictions.

The effect of evictions is “housing instability or insecurity”:

Families with insecure or unstable housing may move frequently, suffer eviction, or otherwise be at increased risk of homelessness.

Evictions can result in personal loss of property, trigger job loss, and lead to underperforming schools and poor student outcomes. Even an eviction filing that is resolved can mar a tenant’s credit record and bar that person from renting elsewhere or accessing public assistance.

At the neighborhood level, high eviction rates are associated with poor housing conditions, high rates of school turnover, and neighborhood and community instability.

But it’s not just Atlanta, according to the Atlanta Fed: “There is increasing documentation of an ensuing high rate of evictions in U.S. cities, partly due to tenants’ inability to afford higher rents.”

So is the Fed having second thoughts about its efforts to encourage Wall Street to muscle into the single-family home market in big urban areas, drive up housing costs around the country, and turn rents in to a finanzialized product? I doubt it. Bernanke, the engineer of all this, has moved on; and the Fed, credited with “healing” the housing market, never has second thoughts about its actions.

But the Fed is worried about “real wage” increases. It’s about cheap labor. Read… The Thing in the Jobs Report that Gives the Fed the Willies

57 comments -

Jim Smith

Jan 7, 2017 at 12:54 pm

How do these firms stay in business with negative earnings, is it because they are booking profits on the price increase of their assets-homes.

And as rates go back up, which they will do if their is wage inflation will all these firms have to sell?

Reply

Wolf Richter

Jan 7, 2017 at 1:04

They stay in business because they have access to cheap capital that they can burn with their money-losing operations. Investors support them on the hope that they’re sitting on big capital gains from their home purchases in 2011-2014.

<<<

>>> Top funds for real estate stocks

http://m.kiplinger.com/article/investing/T044-C008-S003-5-reits-to-buy-now-for-income-and-growth.html

If you prefer to buy real estate investment trusts through a fund, you have plenty of choices. One good one is Manning & Napier Real Estate S (symbol MNREX), which holds 56 real estate stocks—mainly REITs such as mall owner Simon Property Group and storage firm Prologis. Over the past five years through June 10, the fund returned 12.4% annualized, beating 93% of its peers. One drawback: annual fees, at 1.09%, are above average.

Fidelity Real Estate Investment (FRESX) returned 12.5% annualized over the past five years. Veteran manager Steve Buller looks for REITs that offer growth at a reasonable price and says he’s emphasizing health care and triple-net-lease REITs these days. The fund yields 2.5% and costs 0.78% in annual expenses.

If you simply want to track the REIT market, buy Schwab U.S. REIT ETF (SCHH), an exchange-traded fund that follows the Dow Jones U.S. Select REIT index, a basket of 96 stocks weighted by market value. Yielding 3.1%, the ETF pays out more than most mutual funds, thanks to a rock-bottom expense ratio of 0.07%.

For ultra-high income, consider iShares Mortgage Real Estate Capped ETF (REM). The fund, which yields 11.0%, invests in mortgage REITs—firms that own real-estate-backed loans. Mortgage REITs could tumble if short-term interest rates climb sharply while long-term rates stay flat or decline (squeezing the REIT’s profit margins). But that looks unlikely over the next year. Annual expenses are 0.48%.

<<<

>>> Sovran Self Storage

http://m.kiplinger.com/article/investing/T044-C008-S003-5-reits-to-buy-now-for-income-and-growth.html

Sales are going strong for Sovran (SSS, $101.91, P/E 18, 3.1%), a self-storage REIT that owns more than 550 properties in 26 states under the Uncle Bob’s brand. The firm is landing customers with its modernized, climate-controlled facilities, many of which are located in high-traffic urban and suburban areas. Occupancy hit 90.5% in the first quarter, up one percentage point from a year earlier. Sovran is also expanding with a $1.3 billion deal, announced in April, to acquire 84 properties from LifeStorage, a privately held firm whose buildings generate higher average rents per square foot than Sovran’s real estate.

Sovran issued 6.9 million shares of stock to finance the LifeStorage deal. That could dilute FFO per share in the near term and lower the REIT’s net asset value per share (the estimated market value of Sovran’s properties, less outstanding debt). Still, analysts see Sovran’s revenue jumping a healthy 17% this year, to $430 million. Sovran recently hiked its annual dividend rate by 11.8%, to $3.80 per share, and it ramped up its 2016 FFO forecast to as much as $5.55 per share, up 14.4% from 2015. Although the stock looks pricey at 18 times FFO, it has room to climb. Bank of America Merrill Lynch, which rates the stock a buy, expects the shares to hit $120 a year from now.

<<<

>>> Realty Income

http://m.kiplinger.com/article/investing/T044-C008-S003-5-reits-to-buy-now-for-income-and-growth.html

Most REITs pay quarterly dividends, but Realty (O, $64.30, P/E 22, 3.5%) shells out cash monthly, paying about 20 cents per share like clockwork. That income arises from Realty’s vast collection of properties: 4,615 buildings, leased mainly to big retailers such as Walgreens and Dollar General. These firms sign long-term triple-net, or NNN, leases with Realty, requiring them to pay for all property taxes, maintenance and insurance.

Although Realty isn’t a high-growth REIT, it’s a solid earner. The firm has paid dividends for a stunning 550 consecutive months. Its 98% property occupancy rate has never slipped below 96%, and revenues are climbing thanks to rent increases built into leases and a steady stream of property acquisitions. Realty expects FFO to rise by as much as 4.3% this year. That should support more growth in the dividend, which Realty has increased at an annualized rate of 4.7% since going public in 1994.

At 22 times FFO, Realty is one of the pricier REITs, and its stock may stay flat in the near term. But stick with it: You can scoop up steady monthly dividends while waiting for the shares to edge higher over the long run.

<<<

>>> Omega Healthcare Investors Inc

http://m.kiplinger.com/article/investing/T044-C000-S015-looking-for-a-high-yield-try-these-3-reits.html?rid=SYN-yahoo&rpageid=15273

High Yield: 6.95%

Investors looking for higher-than-average dividend yields may want to consider REITs that specialize in a niche area. Omega Healthcare Investors Inc (OHI) is one such specialized REIT.

As its name implies, OHI focuses its attention on healthcare-related real estate. Demand for healthcare continues to rise, and as that demand has expanded so has the number of facilities needed to conduct that medical business. That’s were OHI comes in.

Omega provides capital to property owners in order to build their facilities. However, many of OHI’s loans have been in the sale-lease-back style, meaning after a period of time, OHI will buy the building back and the tenant will continue to lease the property from Omega.

The added bonus is that OHI has specialized even further by only focusing on skilled nursing facilities and assisted living facilities. Today, the REIT owns 932 skilled nursing facilities in the United States and the United Kingdom. The vast bulk of its rents come from the U.S. government by way of Medicare and Medicaid. While the government won’t pay much, it always pays on time.

That steady nature has allowed OHI to continue with its dividend growth, fund future expansions and provided investors with a high yield of nearly 7%.

<<<

Realty Income, Sovran -- >>> 5 High-Yielding REITs for Dividend Investors

Kiplinger

By Daren Fonda

http://finance.yahoo.com/news/5-high-yielding-reits-dividend-142001629.html

If you're a small-time landlord, real estate can be a ton of work, with an uncertain payoff. But stick with real estate investment trusts and you're likely to be rewarded. Over the past 15 years, property-owning REITs have generated an average annual total return of 11.2% a year, doubling the 5.5% annualized gain of Standard & Poor's 500-stock index.

As giant landlords, REITs (rhymes with treats) own everything from apartment buildings to offices, malls, warehouses and hotels. Regardless of what they hold, they're required to shell out at least 90% of taxable income to shareholders. That makes them gravy trains for dividends. REIT stocks today yield 3.8%, on average, well above the 2.2% yield of the S&P 500.

REITs could get a lift, too, from a new buying wave by mutual funds. Until now, S&P has classified REITs as financial stocks, along with banks, brokers and other such firms. That was always an odd fit for real estate developers and landlords. But starting in September, two big index providers--MSCI and S&P Dow Jones Indices--plan to carve out REITs and real estate operating companies into a stand-alone sector. Real estate will be the eighth-largest group in the S&P 500--bigger than materials, telecommunications and utilities. Many mutual funds ignore REITs, and the change could prompt more interest in the stocks, propping up the sector.

Of course, REITs could take some lumps, too. After returning 10.6% in the past year, the stocks have edged into pricey territory, trading, on average, at 103% of their net asset values, slightly above their historical average. REIT stocks could face pressure, moreover, if long-term interest rates climb. That would make REIT yields less attractive than bonds and other fixed-income investments.

Yet Kiplinger's doesn't expect big rate hikes over the coming year, partly because inflation expectations remain muted. REITs continue to offer yields that are greater than those of investment-grade bonds. And their payouts are likely to climb more than those of utilities or other income investments, making them a better bet long term.

Below are five REITs we like for their dividend yields, growth prospects and reasonable share prices. Note that price-earnings ratios are based on estimated year-ahead funds from operations, a common REIT measure that represents net income plus depreciation expenses. (Returns, prices and related data are through June 10).

Gaming and Leisure Properties

Visit a casino and you'll probably lose money at the slot machines or table games. A better bet: Gaming and Leisure Properties (symbol GLPI, $34.07, P/E ratio 11, yield 6.4%). The REIT recently bought 14 casinos from Pinnacle Entertainment in a deal worth about $5 billion. Gaming issued $1.1 billion worth of stock to help finance the acquisition, and it now carries a hefty $4.9 billion in long-term debt on its balance sheet.

Overall, though, the purchase is a good deal for shareholders. With revenue now flowing from 35 casino and hotel properties in 14 states, Gaming and Leisure should generate ample cash to fund its dividend and raise it as rental income climbs gradually. Jeffrey Kolitch, manager of Baron Real Estate Fund (BREFX), figures that within a year the firm will bump its annual payout from $2.24 per share to $2.45. At 11 times estimated FFO, the stock trades well below the average of 18 for all property-owning REITs. The shares look "mispriced," says Kolitch, who sees the stock hitting $41 over the next year.

Host Hotels & Resorts

Lodging REITs such as Host Hotels (HST, $15.40, P/E 9, yield 5.2%) have hit the bargain bin. Investors worry that hotel revenues, after climbing for years, appear to be peaking, and they fear that competition from Airbnb and other home-rental websites will cut into occupancy rates and hotel profits. All this has taken a toll on Host's stock, which has sunk 17% over the past year. Yet at just 9 times projected FFO, the shares look compelling.

The largest U.S. lodging REIT, Host owns 92 upscale hotels and resorts, including luxury properties such as the Hyatt Regency Maui Resort and Spa, and the W Hotel in New York City's Union Square. Demand for its hotels, which other companies manage, appears to be healthy, with average revenue per available room (a common lodging REIT measure) climbing 3.6% in the first quarter compared with the same period in 2015. For Host's core clientele--upscale business and leisure travelers--competition from the likes of Airbnb isn't likely to pose a major threat.

Granted, Host's revenues would slump if the economy weakens and business travelers spend less on lodging. Yet that would likely be a temporary setback. Host's balance sheet looks strong, with a manageable debt level relative to its income. Its dividend should be secure, too, says Mike Underhill, manager of RidgeWorth Capital Innovations Global Resources and Infrastructure =Fund (INNNX). Over the next year, he expects the stock to hit $19.

Realty Income

Most REITs pay quarterly dividends, but Realty (O, $64.30, P/E 22, 3.5%) shells out cash monthly, paying about 20 cents per share like clockwork. That income arises from Realty's vast collection of properties: 4,615 buildings, leased mainly to big retailers such as Walgreens and Dollar General. These firms sign long-term triple-net, or NNN, leases with Realty, requiring them to pay for all property taxes, maintenance and insurance.

Although Realty isn't a high-growth REIT, it's a solid earner. The firm has paid dividends for a stunning 550 consecutive months. Its 98% property occupancy rate has never slipped below 96%, and revenues are climbing thanks to rent increases built into leases and a steady stream of property acquisitions. Realty expects FFO to rise by as much as 4.3% this year. That should support more growth in the dividend, which Realty has increased at an annualized rate of 4.7% since going public in 1994.

At 22 times FFO, Realty is one of the pricier REITs, and its stock may stay flat in the near term. But stick with it: You can scoop up steady monthly dividends while waiting for the shares to edge higher over the long run.

Sovran Self Storage

Sales are going strong for Sovran (SSS, $101.91, P/E 18, 3.1%), a self-storage REIT that owns more than 550 properties in 26 states under the Uncle Bob's brand. The firm is landing customers with its modernized, climate-controlled facilities, many of which are located in high-traffic urban and suburban areas. Occupancy hit 90.5% in the first quarter, up one percentage point from a year earlier. Sovran is also expanding with a $1.3 billion deal, announced in April, to acquire 84 properties from LifeStorage, a privately held firm whose buildings generate higher average rents per square foot than Sovran's real estate.

Sovran issued 6.9 million shares of stock to finance the LifeStorage deal. That could dilute FFO per share in the near term and lower the REIT's net asset value per share (the estimated market value of Sovran's properties, less outstanding debt). Still, analysts see Sovran's revenue jumping a healthy 17% this year, to $430 million. Sovran recently hiked its annual dividend rate by 11.8%, to $3.80 per share, and it ramped up its 2016 FFO forecast to as much as $5.55 per share, up 14.4% from 2015. Although the stock looks pricey at 18 times FFO, it has room to climb. Bank of America Merrill Lynch, which rates the stock a buy, expects the shares to hit $120 a year from now.

STAG Industrial

Leasing warehouses to auto-parts makers and other industrial firms, STAG (STAG, $22.72, P/E 14, 6%) has been snapping up properties since going public in 2011, amassing 223 buildings with more than 40 million square feet of space. Demand for warehouses should stay healthy as long as the economy keeps expanding. And STAG aims to keep up its growth, planning to acquire or develop $1.7 billion worth of properties over the next few years.

Spending heavily to buy warehouses has pushed STAG's debt load to 36% of its property values, according to brokerage firm Baird. That's slightly above average for industrial REITs. But it isn't excessive relative to STAG's income, and it shouldn't prevent the firm from acquiring more real estate. Meanwhile, rental income is rolling in. First-quarter FFO rose by 11.4% from the same period a year earlier, and STAG generates plenty of cash to support its dividend, which, Baird says, it should be able to hike at an annual clip of 7% to 8%. Trading about 20% below STAG's net asset value of $28.30 a share, the stock looks like a good value, says Baird, which expects it to hit $24 over the next year.

Top funds for real estate stocks

If you prefer to buy real estate investment trusts through a fund, you have plenty of choices. One good one is Manning & Napier Real Estate S (symbol MNREX), which holds 56 real estate stocks--mainly REITs such as mall owner Simon Property Group and storage firm Prologis. Over the past five years through June 10, the fund returned 12.4% annualized, beating 93% of its peers. One drawback: annual fees, at 1.09%, are above average.

Fidelity Real Estate Investment (FRESX) returned 12.5% annualized over the past five years. Veteran manager Steve Buller looks for REITs that offer growth at a reasonable price and says he's emphasizing health care and triple-net-lease REITs these days. The fund yields 2.5% and costs 0.78% in annual expenses.

If you simply want to track the REIT market, buy Schwab U.S. REIT ETF (SCHH), an exchange-traded fund that follows the Dow Jones U.S. Select REIT index, a basket of 96 stocks weighted by market value. Yielding 3.1%, the ETF pays out more than most mutual funds, thanks to a rock-bottom expense ratio of 0.07%.

For ultra-high income, consider iShares Mortgage Real Estate Capped ETF (REM). The fund, which yields 11.0%, invests in mortgage REITs--firms that own real-estate-backed loans. Mortgage REITs could tumble if short-term interest rates climb sharply while long-term rates stay flat or decline (squeezing the REIT's profit margins). But that looks unlikely over the next year. Annual expenses are 0.48%.

<<<

>>> Get real: Billions set to pour into real-estate investments

The Standard & Poor's 500 and other big stock indexes will soon carve out real estate investments from the financial sector and give them their own category

Associated Press

By Stan Choe

http://finance.yahoo.com/news/real-billions-set-pour-real-161651503.html

NEW YORK (AP) -- Mutual funds are about to get much more real.

A big change is coming in how stock indexes measure the market, one that's likely to push tens of billions of dollars into real-estate investments, according to estimates. All that cash could drive further gains for a group of stocks that's already done quite well since the financial crisis. Critics say it could also make an area of the market that they call overvalued even more so.

The deluge of cash is the result of a re-think by index providers about how they see the market's construction. The Standard & Poor's 500 and other indexes have long split the market into 10 main sectors, such as technology companies or utilities or industrials. After the market closes on Aug. 31, S&P Dow Jones Indices and MSCI will carve out real estate to become the 11th sector.

For investors who own only broad index funds, the change won't mean much. Real-estate investment trusts, which own apartments, office buildings and shopping malls, will still make up about 3 percent of the S&P 500, and they'll make up the same percentage of S&P 500 index funds.

The change is much more than housekeeping for actively managed mutual funds, which still control more dollars than their index-fund rivals.

It's a stock picker's job to be different from the index. That's why they charge more in expenses than S&P 500 funds, for the opportunity to do better than the index. Even so, active managers pay close attention to how indexes are constructed. If their portfolios are very different, they'll need to explain why to their investors.

Many mutual funds have nothing at all invested in real estate. Nearly 40 percent of large-cap core fund managers have zilch, according to a review by Goldman Sachs strategists. But that's not obvious from a quick glance at funds' marketing materials, which generally show how much is invested in each of the 10 big sectors.

REITs are currently categorized as part of the financial sector. So an actively managed fund could have 16 percent of its investments in financial stocks, the same as the S&P 500, but with no real estate. At first glance, such a fund could look like it's built similarly to the S&P 500 index. But come September, that same fund would suddenly appear as if it's optimistic about banks, insurers and other financial companies — and pessimistic about real estate — because it will hold more financials and less REITs than the index.

THE WAVE HAS ALREADY BEGUN

Estimates vary widely on how much REIT buying the index changes will drive, but most are big. They range from about $10 billion to 10 times that.

"It's a tsunami," says Mike Underhill, portfolio manager at the RidgeWorth Capital Innovations Global Resources and Infrastructure fund, which owns several REITs. And he says the buying has already started.

He's recently noticed prices doing better than he'd typically expect for REITs that operate in areas where renters are falling behind on rents. He attributes that to mutual funds buying REITs in advance of the index shift.

ALREADY STRONG PERFORMANCE

The expected jump in demand could help keep REIT prices high, even after their strong performance both this year and since the stock market bottomed in March 2009. An index of REITs by MSCI has returned a cumulative 434 percent since March 9, 2009, versus 265 percent for the S&P 500.

Investors have been buying REITs in part because they offer relatively big dividends. Bond yields are low, so investors have gone searching elsewhere for yield. And REITs can avoid taxes if they pass on 90 percent of their profit to shareholders as dividends.

That's drawn investors to REITs like Simon Property Group, which owns shopping malls around the country, or Public Storage, which runs self-storage units.

The jump for REITs mean they make up about 3 percent of the S&P 500 index now, up from 0.1 percent in 2003, according to Goldman Sachs. When it becomes the 11th sector, real estate will be roughly the same size as the utilities, raw materials and telecom services sectors. The largest component in the S&P 500 is technology, which makes up 21 percent of the index.

WORRIES AND CONSEQUENCES

All the demand for REITs in recent years, though, means their prices have climbed not only on an absolute level but also relative to how much cash their businesses are producing. The jumps have been big enough that some investors call REITs overly expensive, while others say they're fairly valued. Most fund managers agree that REITs are no longer cheap.

The index changes could have particularly big impacts on investors with funds that focus on just financial stocks, which control a total of about $39 billion in assets.

The largest such exchange-traded fund, the Financial Select Sector SPDR fund, has already laid out its plans. It will pay out a special dividend to investors in September, one made up entirely of shares of an ETF created in October that focuses exclusively on REITs.

But the index shifts will likely reverberate across the market. S&P Dow Jones Indices and MSCI say they're upgrading real estate to stand-alone "sector" status because they want to acknowledge its importance to the global economy. That may push lay investors to give the sector a closer look.

<<<

>>> Trump: His early rise into fame and wealth, his near fatal end and his resilient comeback

Iliana E. Perez

December 2000

http://www.nyu.edu/classes/keefer/ww1/perez.html

Trump: His early rise into fame and wealth, his near fatal end and his resilient comeback

The weird thing about Donald Trump is, as much as he tried to be a figure of ridiculous fun and shrug of gossip, lie as he did about things large and small, Trump appears to be an enormously skilled developer even though he has very poor investment strategies. Donald Trump’s early rise came about as the result of timely speculation and not because of his deal making strategies. During the early eighties the Real Estate market was hot and gave Trump the window of opportunity he needed. Donald Trump possesses the ability to identify profitable ventures a mile away. His aggression and one-sided focus are what allowed him to break down the existing barriers to obtain his goals of becoming successful as a developer. With all that said there is a sad and dark side to Donald Trump, I believe he suffers from an obsessive compulsive disorder. His OCD is to buy and build whatever comes to his mind is just plain crazy. His actions time and time again have proven that when he sets his sights on something; he just goes for it no matter what. Trump does not have any set strategies. Donald Trump’s impulsiveness is what many times does not let him see what will happen after he makes that first pivotal step in any direction. His OCD is best seen in his impulsive purchase of a bankrupt Eastern Airlines and a huge yacht he was never able to put into profitable use.

Donald Trump is the third generation of an entrepreneurial family. His family’s achievements and success reflect one of the biggest changes America has ever seen, from the Gold Rush in Colorado to affordable housing in Queens. Donald Trump was born in Queens, New York on June 14,1946, the day the nation united to celebrate its flag, Flag Day. Donald Trump has added to his parent’s legacy of finding the demand in the market and infusing the supply it needs. The name Donald Trump has made for himself is unsurpassed to this day.

Donald Trump grew up assisting his father in his business ventures. Trump had a very comfortable childhood and was sent to a military academy where he learned discipline and completed his middle education. In military school he learned the true meaning of competition and how aggressive you must be to get what you want. While assisting his father Trump realized he did not like the rougher aspects of his father's business. Some of the jobs he did not like included rent collecting and the physical labor involved. Trump had a great interest in real estate and decided he would like to be involved in the Real Estate business but at a larger scale than his father had ever been. He studied finance at the prestigious University of Pennsylvania's Wharton School because of this.

During his college years, Donald Trump and his father decided to purchase an apartment complex in Ohio which was in bankruptcy. The purchase of this complex is striking because they obtained financing above the purchase price so they could do the necessary remodeling to the run down complex. The development purchased by Donald Trump with his father’s aid was called Swifton Village, a 1,200 unit apartment in Cincinnati, Ohio. It was purchased at a foreclosure sale for less than $6 million and sold within a year and half for about $12 million dollars. Without a penny of their own invested they were able to turn the apartment complex around by taking a strict approach at rent collection and by remodeling the appearance of the complex. Trump was able to see how the government would assist buyers in purchasing property with little or no financial backing. and best of all how do get such aid. This incident was the beginnings of the Donald Trump we know today. This event proved to be the single most important lesson Donald Trump learned

Donald Trump is known as the all American real estate developer. Donald Trump has shaped New York City into the likes of a modern impressionist painting. All his developments and projects have been new, original, modern, and awe inspiring. Donald Trump was one of the first developers to incorporate an indoor waterfall as a back wall to a restaurant which can be found at the Trump Plaza. Donald Trump breaks the rules of construction and development but always seems to manage to do the right thing. Trump’s actions have always proven to be one of the most reckless and aggressive approaches a real estate developer has ever shown. Is he crazy or does he have an incredible amount of foresight? Buying buildings, casinos, and property just because he can conceive the idea of ownership in his head proves he may be a little bit crazy. This proves Trump’s personal self gratification and not his intelligence is what has made him millions. This strange quality which Trump possesses has given him the edge he has needed and needs to keep going. Trump’s strive for greatness has pushed him to become the national emblem that represents cocky wealth.

Donald Trump didn’t always have it this easy. Even though Trump’s first investment had great success he was not satisfied. Donald decided it was important for him to be on his own. Trump always had his sights set on New York City. Trump believed New York City would be his gold mine. He rented an apartment in Manhattan. The apartment was dingy and old by his standards and he was embarrassed to bring people there. This move to Manhattan brought him into the heart of New York City and he was able to become familiar with all of the properties in his area. He would walk the streets to make note of the buildings and their condition. Always keeping his eyes open for the right investment. He decided these steps would be very important in making a name for himself.

His first attempts at becoming a developer in the early eighties in New York City went unnoticed. Even though his bids were lower and offered more then his contractors he lost out every time. Even when Donald Trump offered his advice the city would not accept it. It seemed his earlier acclaimed fame and luck had diminished. Why? Could it have been because he was the young new face in town? Donald Trump’s youth and inexperience put doubts into the minds of other older more experienced developer. Surprisingly, this did not deter Donald; he became even more determined and aggressive similar to the likes of a spoiled child throwing a tantrum when he does not get what he wants.

Trump’s goal, was to make his mark on New York City. His persistence proved fruitful. At the age of 28 New York City finally gave Trump his chance. He had convinced the city to build a convention center on what use to be the defunct Penn Central Rail yards, which he had secured for his own benefit with options. But, that was not all Trump was able to do, he also convinced the city and the Hyatt Corporation to renovate the Commodore Hotel, which later became known as the Grand Hyatt Hotel. Finally, after these two projects were accomplished Donald Trump’s presence and skill was known. He had proved that he was someone to be reckoned with and was rapidly becoming New York’s newest real estate tycoon.

Donald Trump’s ultimate show of power was when he built the Trump Tower, on Fifth Avenue. This project was what finally provided him with the national attention he had dreamed of for so many years. It contained a mixture of stores and million-dollar apartments; this building became Donald Trump’s trademark. Trump Tower brought forth masses of tourist and was his final show of what great financial success is. When competitors tried to beat him out of the market and lowered their prices he simply raised them. Donald did not once lower his prices. He felt that affluent people, which was the market he was trying to attract would not be concerned with price. This proved he had the ability to understand the psychology of the wealthy. Donald Trump had found his niche and was going to exploit if for as long as he could.

At the peak of his wealth in the year 1989, Trump's billion dollar empire included Trump Parc which contained more than 24,000 rental and co-op apartments, the Trump Shuttle Airline, ownership of the New Jersey Generals of the United States Football league, casinos in Atlantic City, Trump Castle, and his luxurious private homes. Trump's The Art of the Deal was his way of educating the public on business dealings and how to achieve success. I believe this was his conceded attempt to lecture America and rub his financial success in the faces of all who snubbed him. Trump states his style is very basic, in his own words he describes his approach by saying, "I aim very high, and then I just keep pushing to get what I am after" (The Art of the Deal). Donald Trump is a firm believer the deal making is an ability you are born with, it is in the genes. But obviously it was his personal whims, which played a major role in the reasoning behind his acquisitions and their management.

Trump was flying high and finally felt he had achieved everything he wanted. At the speed of light he acquired and developed assets that he had no experience in managing. This caused him to soon lose sight of it all. He was unable to balance his current assets against his outstanding debts that were rapidly coming due. The real estate market boom was heading toward a bust and the rampant tidal waves of the declining market claimed the investments of many and now Donald Trump was directly in its path of destruction. The first sight that something was wrong in Donald's glittery glamorous life started surfacing at the same time the press began reporting his personal problems to the world. Once the break up with his wife and Trump’s reported affair with Marla Maples came to light it distracted him even further from his already crumbling empire. Where were his investment strategies now? They were nowhere to be found. The reality was, Trump was stretched so thin using his name and his persona as a personal guarantee that the foundation of all of his project might as well been made out of sawdust. Donald Trump had no idea what to do. His empire was slipping through his fingertips and the most powerful man in New York was helpless.

During Trump’s near bankruptcy problems the big New York banks were not too far behind. They had lent fortunes to Trump, without paying sufficient attention to where profits would be coming from or how tight an operation Trump was really running. Banks that never lent money for gambling businesses before lined up to fund Trump's empire, more for his name, his golden touch and because of his earlier estate deals than something more concrete. Trump built huge casinos and gleaming apartment buildings, brought world-famous hotels and a fleet of planes and plastered his name over everything. Is this the sign of a man with great business or an over inflated ego? The banks were so blinded by Trump’s charm and past achievements that they felt it would be the easiest buck they would ever make. This later proved to be the worst mistake the Banks could have made. It was as if the Banks had signed their souls to the devil. They were in such an awkward position, if Trump went down so would they.

By 1990 Trump was facing bankruptcy, unable to meet payments on more than $2 billion in loans that were owed to the banks. He was able to secure some emergency financing on various occasions but in return he had to give up the operation and control of most of his real estate to the creditor banks as well as 10 percent of all revenue earned. Trump gradually gave up control of considerable parts of his empire including the Trump Shuttle, casinos, and The Plaza in order to secure more favorable debt financing to cushion his near bankruptcy situation. The lenders were cracking down hard and it had become a tug of war over whose name would be more tarnished, theirs or Donald Trump's. The banks wanted to lend Trump more money but they too had become constrained. The savings and loan crises had caused federal regulators to monitor banks closely, which led to them ending practices with Trump very abruptly.

What lead to Trump's downfall and near catastrophic ending in the early nineties? I believe it was in part because of his non existent strategies. For example by putting the word "Trump" on a building or an airplane he thought this would immediately make him money. There was no concrete backing to his notions and what made it worse was the public bought into it. This proved what a great sales person Trump was in selling and displaying his image to the public but never proved that he was the wonderful business savvy person he portrayed himself to be. Trump was no magician nor was he born with an instinct for real estate as he believed. Donald Trump was simply a speculator who was bound to eventually get knocked down by debt and the normal business cycle. Forbes magazine had charted Trump's rise and estimated that his increased debt and a drop in real-estate values caused Trump to lose more than two thirds of his net worth, from $17 billion in 1989 to $500 million in 1990 (Forbes April 3, 2000).

Donald Trump I believe has helped the arrival of a new age and has brought forth the most unforgettable era in real estate but the cost was almost to high for him to pay. He wanted to accomplish too much too soon with very little planning ahead. Not being able to place proper thought on things is not the best way to start of any type of project especially not multimillion dollar ones. Donald Trump was very smart with dealing with people but until he learns to control himself and focus history may repeat itself. Trump’s aura and image lures many people to invest in his ventures. This blinding affect although great for Trump and his ventures can be deadly to investors.

Trump is the perfect example of how fast a heavily borrowed fortune and the fame that comes with it can very easily disappear if one is not careful. Despite all his misfortunes, Trump at the age of 53, a good decade and a half after he came to national prominence, Donald Trump is possibly the most famous businessman in America. According to the Gallup Organization, 98% of Americans know who he is. None of the other masters of American business like Jack Welch, or Warren Buffett, and Steve Jobs, or even Ted Turner come close. The most impressive aspect of Trump's celebrity status is not his grandeur but its durability. Donald Trump will be a name that will resonate through time. This is best illustrated in this quote, "He has far outlasted the decade that produced him, but--unlike other products of the 1980s who've managed to stay in the limelight through self-reinvention like Michael Milken "the junk bond king". Trump has done this without any discernible personal growth. Like a cryogenically frozen body, he stands as a perfectly preserved specimen of the era (Forbes)." In this new age where wealth is paper, and most assets move electronically Donald Trump's tastes and love of money can be looked upon as a refreshing change. His love of money, success and fame will always keep Donald Trump thinking of bigger and better projects to surprise the public and have the city pull its hair out.

Among Trump's peers, other rich business people like himself, the situation is very different. When Fortune magazine asked several thousand of them to rank 469 companies for its 1999 list of Most Admired Companies, they put Trump's casino company last. They ranked it worst in quality of management, in use of its corporate assets, employee talent, long-term investment value, and social responsibility. This again proves Donald Trump does not use any business strategies in his purchases. He just speculates as to what will be hot and what will not. Trump’s wealth allows him to invest in many places and usually one out five investments will be a hit which will cover all his other loosing assets. Trump tries to shrug off such opinions, in one of his books, The America We Deserve he states, "Rich people who don't know me never like me. Rich people who know me like me." Does this mean he doesn't get the recognition he deserves as a businessman? "I don't think anybody knows how big my business is," Trump replied. "People would rather talk about my social life than the fact that I'm building a 90-story building next to the U.N. ... They cover me for all sorts of wrong reasons (The America We Deserve)."

Donald Trump’s Associates describe his uncanny ability for spotting and sorting out waste as well as his outstanding memory. Trump is so detailed that he routinely requires the city to close loopholes only he had the guts to exploit. What is true for Donald Trump is that he will not usually play it safe. Because of this insecurity Trump walks the construction sites every day, yelling that the concrete is the wrong kind, that the marble isn't flat enough, that the ceiling should be ripped out and redone. Trump must be in every part of the deal. He literally believes, if you want the job done right you do it yourself. Because of this you see Trump always brings the sheer power of his persona forth. He negotiates with subcontractors himself instead of relying on a purchasing department and isn't opposed to using his celebrity status to better the terms wherever he can. To seal one deal, Trump agreed to call the subcontractor's mother and wish her a happy birthday. "He has this ability to relate to the doorman, to the guy who's carrying the iron or steel, and make that guy feel good and important (Colony Capital CEO Tom Barrack).

While Trump's lifestyle hasn't changed much since the 1980s, his dealmaking approach has. He has become a bit more cautious of the sort of leverage that pushed him close to bankruptcy in the early 1990s, he refrains from putting up large sums, instead he tries to partner with financial backers among them is General Electric's pension fund. Many of who want to tap the power of his name as well and also retain him as a sort of jungle guide. In one instance, developers paid Trump a flat $5 million licensing fee for the right to brand a Trump Tower in Seoul. Trump's opponents will usually seize these opportunities to label him as a mere front man for financial interests. Trump has become to them a brand slapped on buildings he doesn't own, which in turn many times sends Trump into spasms of outrage. "I own at least 50% of everything I do," he says, not quite accurately. Trump is always defending himself by saying, "I'm the biggest developer in the hottest city in the world."

In truth, Trump's strategy resembles a village than a fast-expanding game of SimCity, which is to say he has a lot of big projects in the works. On Manhattan's East Side, he and partner Daewoo are putting up Trump World Tower, the 90-story massive building that is going to cast a shadow on the United. Over on the West Side, he and a group of Hong Kong investors have two buildings into an 18-building residential project along the Hudson River, which again creatively is titled Trump Place. This project will fill up on of Manhattan's last big parcel of undeveloped land. Condo sales from both are benefiting from the hottest real estate market anyone can remember once again the advantage Trump had in the eighties. As for the three trophy properties Trump calls "my other children" Trump Tower, 40 Wall Street, and the General Motors Building, which he purchased in 1998 with insurance company Conseco, he has successfully succeeded in jacking up rents. His attention to detail and to what potential tenants will want has remained impeccable.

Even though in some aspects he is doing well still Trump's self-defeating tendencies are evident with his casino company, Trump Hotels & Casino Resorts. Trump took it public in 1995 under the ticker symbol DJT. It was Trump's salvation at the time, raising $140 million that he used to pay off his creditors. Without the casino company, Donald would most likely not be alive today in the way we know him. Surprisingly after near bankruptcy and downright dumb investments his underlying assets are in decent shape. Trump's three New Jersey casinos command nearly a third of all gaming revenues in Atlantic City and a slow-growing market has withstood challenges from new megacasinos. All are well-run operations which have top skilled management; the New Jersey Casino Control Commission says they all have clean records. The Taj Mahal which has about 4,500 slot machines, throws off nearly $100 million in cash annually; the smaller Trump Marina has doubled its own cash flow to $53 million in just three years. If you add in Trump Plaza and a riverboat outside Gary, Ind., the company generates more than $240 million in cash a year. Donald Trump is not just blowing smoke when he says there is a lot of money to be made in this type of business.

True, some of his investments may be a cash cow, but most of the revenues earned goes toward the care and feeding of another beast. The $1.8 billion in high-yield debt that has weighed the company down almost since its inception. The debt servicing eats up $216 million of the cash flow, leaving the company with very little capital to reinvest in its properties and even less in earnings for shareholders. The company lost $134 million after depreciation and special items in 1999, and the S&P recently lowered Trump's bond rating from junk to junkier.

The most unnerving thing about Trump has been the accusations in the press about Trump's tendency to use the casino company as his own personal piggy bank. If you look at the $5 million bonus he drew one year, or the fact that the pilots of his personal 727 are on the casino company's payroll this little bit of gossip can hardly be overlooked. In 1996 he sold the Trump Marina to the company for what many shareholders considered to be a very high price. Trump insists it was a "good deal." Trump has angered investors in 1998 when he had the already cash-strapped company lend him $26 million to pay off a personal loan from Donaldson Lufkin & Jenrette. The weird thing is Trump denies misusing company funds and says he'll repay the $26 million when it comes due May 15. What does this say about Trump’s character? Donald Trump knows how to use the situation to the best of its ability. As if all this weren't enough to rubs Trump's Street credibility in the mud, the company was also accused of overstating last year's third-quarter results when it failed to disclose that $17 million in revenues came from a one time event.

A couple of people close to Trump which hold him at high regards suggest that he's unfit to be running a public company. Given that the low stock price seems partly a function of Wall Street's allergic response to Trump's showiness analysts have named it "the Donald factor." Many believe the solution is obvious, it would be better for Trump to remove himself from management. Industry executives speculate that this step alone would bring a 30% bump up in the stock. But Trump has always chosen the opposite track. To macho to prove he may be out of his league even after having paid little attention to the casinos for several years, Donald Trump now promises to become more involved with them. Now it appears Trump will attempt to deleverage the company by unloading one of the casinos within the next six months.

Another puzzling aspect of Trump's public image is that even though he runs two companies which employ 22,000 people together, you never get the sense of an organization underneath him. It is easy to come to the conclusion that he's not only a sole proprietor but a sole employee. Both current and former employees describe Trump as a loyal but not especially well-paying boss, citing stories of birthdays remembered, of sick relatives visited in the hospital. Yet some of them shrug at the popular perception of Trump as a one-man show.

Oddly enough for a man who all but lives in the media, Trump has no public relations to speak of. In a day when even petty tycoons protect themselves with platoons of spokespeople and media people, he relies only on his longtime assistant Norma Foederer and returns most reporters' calls personally, making him one of the most accessible businessmen anywhere. How ironic a man of his statue and money has to prove himself to the world everyday. Donald Trump is a very goal-driven person and I believe will always resurface no matter how his investments turn out. Trump summed his future in these few words, "Anyone who thinks my story is anywhere near over is sadly mistaken."

<<<

>>> Retail Opportunity Investments Corp., a real estate investment trust (REIT), engages in the acquisition, ownership, and management of necessity-based community and neighborhood shopping centers in the eastern and western regions of the United States. As of December 31, 2011, its portfolio consisted of 30 owned retail properties totaling approximately 3.2 million square feet of gross leasable area. The company has elected to be taxed as a REIT, for U.S. federal income tax purposes. The company is based in San Diego, California with additional offices in New York City; Rancho Cordova, California; West Linn, Oregon; and Federal Way, Washington. <<<

>>> Attention America's Suburbs: You Have Just Been Annexed

by Tyler Durden

07/24/2015

http://www.zerohedge.com/news/2015-07-24/attention-americas-suburbs-you-have-just-been-annexed

Submitted by Stanley Kurtz via NationalReview.com,

It’s difficult to say what’s more striking about President Obama’s Affirmatively Furthering Fair Housing (AFFH) regulation: its breathtaking radicalism, the refusal of the press to cover it, or its potential political ramifications. The danger AFFH poses to Democrats explains why the press barely mentions it. This lack of curiosity, in turn, explains why the revolutionary nature of the rule has not been properly understood. Ultimately, the regulation amounts to back-door annexation, a way of turning America’s suburbs into tributaries of nearby cities.

This has been Obama’s purpose from the start. In Spreading the Wealth: How Obama Is Robbing the Suburbs to Pay for the Cities, I explain how a young Barack Obama turned against the suburbs and threw in his lot with a group of Alinsky-style community organizers who blamed suburban tax-flight for urban decay. Their bible was Cities Without Suburbs, by former Albuquerque mayor David Rusk. Rusk, who works closely with Obama’s Alinskyite mentors and now advises the Obama administration, initially called on cities to annex their surrounding suburbs. When it became clear that outright annexation was a political non-starter, Rusk and his followers settled on a series of measures designed to achieve de facto annexation over time.

The plan has three elements: 1) Inhibit suburban growth, and when possible encourage suburban re-migration to cities. This can be achieved, for example, through regional growth boundaries (as in Portland), or by relative neglect of highway-building and repair in favor of public transportation. 2) Force the urban poor into the suburbs through the imposition of low-income housing quotas. 3) Institute “regional tax-base sharing,” where a state forces upper-middle-class suburbs to transfer tax revenue to nearby cities and less-well-off inner-ring suburbs (as in Minneapolis/St. Paul).

If you press suburbanites into cities, transfer urbanites to the suburbs, and redistribute suburban tax money to cities, you have effectively abolished the suburbs. For all practical purposes, the suburbs would then be co-opted into a single metropolitan region. Advocates of these policy prescriptions call themselves “regionalists.”

AFFH goes a long way toward achieving the regionalist program of Obama and his organizing mentors. In significant measure, the rule amounts to a de facto regional annexation of America’s suburbs. To see why, let’s have a look at the rule.

AFFH obligates any local jurisdiction that receives HUD funding to conduct a detailed analysis of its housing occupancy by race, ethnicity, national origin, English proficiency, and class (among other categories). Grantees must identify factors (such as zoning laws, public-housing admissions criteria, and “lack of regional collaboration”) that account for any imbalance in living patterns. Localities must also list “community assets” (such as quality schools, transportation hubs, parks, and jobs) and explain any disparities in access to such assets by race, ethnicity, national origin, English proficiency, class, and more. Localities must then develop a plan to remedy these imbalances, subject to approval by HUD.

By itself, this amounts to an extraordinary takeover of America’s cities and towns by the federal government. There is more, however.

AFFH obligates grantees to conduct all of these analyses at both the local and regional levels. In other words, it’s not enough for, say, Philadelphia’s “Mainline” Montgomery County suburbs to analyze their own populations by race, ethnicity, and class to determine whether there are any imbalances in where groups live, or in access to schools, parks, transportation, and jobs. Those suburbs are also obligated to compare their own housing situations to the Greater Philadelphia region as a whole.

So if some Montgomery County’s suburbs are predominantly upper-middle-class, white, and zoned for single-family housing, while the Philadelphia region as a whole is dotted with concentrations of less-well-off African Americans, Hispanics, or Asians, those suburbs could be obligated to nullify their zoning ordinances and build high-density, low-income housing at their own expense. At that point, those suburbs would have to direct advertising to potential minority occupants in the Greater Philadelphia region. Essentially, this is what HUD has imposed on Westchester County, New York, the most famous dry-run for AFFH.

In other words, by obligating all localities receiving HUD funding to compare their demographics to the region as a whole, AFFH effectively nullifies municipal boundaries. Even with no allegation or evidence of intentional discrimination, the mere existence of a demographic imbalance in the region as a whole must be remedied by a given suburb. Suburbs will literally be forced to import population from elsewhere, at their own expense and in violation of their own laws. In effect, suburbs will have been annexed by a city-dominated region, their laws suspended and their tax money transferred to erstwhile non-residents. And to make sure the new high-density housing developments are close to “community assets” such as schools, transportation, parks, and jobs, bedroom suburbs will be forced to develop mini-downtowns. In effect, they will become more like the cities their residents chose to leave in the first place.

It’s easy to miss the de facto absorption of local governments into their surrounding regions by AFFH, because the rule disguises it. AFFH does contain a provision that allows individual jurisdictions to formally join a regional consortium. Yet the rule leaves it up to local authorities to decide whether to enter regional groupings — or at least the rule appears to make participation in regional decision-making voluntary. In truth, however, just by obligating grantees to compare their housing to the demographics of the greater metropolitan area, and remedy any disparities, HUD has effectively turned every suburban jurisdiction into a helpless satellite of its nearby city and region.

We can see this, because the final version of AFFH includes much more than just the provisions of the rule itself. The final text of the regulation incorporates summaries of the many public comments on the preliminary rule, along with replies to those comments by HUD. This amounts to a running dialogue between leftist housing activists trying to make the rule more controlling, local bureaucrats overwhelmed by paperwork, a public outraged by federal overreach, and HUD itself.

Read carefully, the section of the rule on “Regional Collaboration and Regional Analysis” (especially pages 188–203), reveals one of AFFH’s key secrets: It doesn’t really matter whether a local government decides to formally join a regional consortium or not. HUD can effectively draft any suburb into its surrounding region, just by forcing it to compare its demographics with the metropolitan area as a whole.

At one point (pages 189–191), for example, commenters directly note that the obligation to compare local and regional data, and remedy any disparities, amounts to forcing a jurisdiction to ignore its own boundaries. Without contradicting this assertion, HUD then insists that all jurisdictions will have to engage in exactly such regional analysis.

Comments from leftist housing activists repeatedly call on HUD to pressure local jurisdictions into regional planning consortia. At every point, however, HUD declines to demand that local governments formally join such regional collaborations. Yet each time the issue comes up, HUD assures the housing activists that just by compelling local jurisdictions to compare their demographics with the region as a whole, suburbs will effectively be forced to address demographic disparities at the total metropolitan level (e.g., page 196).

When housing activists worry that a suburb with few poor or minority residents will argue that it has no need to develop low-income housing, HUD makes it clear that the regulation as written already effectively forces all suburbs to accommodate the needs of non-residents (pages 198–199). Again, HUD stresses that the mere obligation to analyze, compare, and remedy demographic disparities at the local and regional levels amounts to a kind of compulsory regionalism.

HUD’s language is coy and careful. The Obama administration clearly wants to avoid alarming local governments, so it underplays the extent to which they have been effectively dissolved and regionalized by AFFH. At the same time, HUD wants to tip off its leftist allies that this is exactly what has happened.

At one level, then, the apparatus of formal and voluntary collaboration in a regional consortium is a bit of a ruse. AFFH amounts to an annexation of suburbs by cities, whether the suburbs like it or not. Yet the formal, regional groupings enabled by the rule are far from harmless.

Comments from housing advocates (pages 194–197), for example, chide HUD for failing to include a mention in AFFH of the hundreds of federally-funded regional plans already being developed by leftist activists across the country (the “Sustainable Communities Regional Planning Grant” program). These plans entail far more than imposing low-income housing quotas on the suburbs. They embody the regionalist program of densifying housing in suburb and city alike, and they structure transportation spending in such a way as to make suburban living far less convenient and workable. HUD replies that these plans can indeed be used by regional consortia to fulfill their obligations under AFFH.

So a city could formally join with some less-well-off inner-ring suburbs and present one of these comprehensive regionalist dream-plans as the product of its consortium. At that point, HUD could pressure reluctant upper-middle-class suburbs to embrace the entire plan on pain of losing their federal funds. In this way, AFFH could force the full menu of regionalist policies—not just low-income housing quotas—onto the suburbs.

There are plenty of ways in which HUD can pressure a suburb to bend to its will. The techniques go far beyond threats to withhold federal funds. The recent Supreme Court decision in Texas Department of Housing and Community Affairs v. Inclusive Communities Project has opened the door to “disparate impact” suits against suburbs by HUD and private groups alike. That is, any demographic imbalance, whether intentional or not, can be treated by the courts as de facto discrimination.

Just by completing the obligatory demographic analysis demanded by AFFH—with HUD-provided data, and structured according to HUD requirements—a suburb could be handing the government evidence to be used in such a lawsuit. Worse, AFFH demands that suburbs account for their demographic disparities, and forces them to choose from a menu of HUD-provided explanations. So if a suburb follows HUD’s lead and formally attributes demographic “imbalances” to its zoning laws, the federal government has what amounts to a signed confession to present in a disparate-impact suit seeking to nullify local zoning regulations. With a (forced) paper “confession” from nearly every suburb in the country in hand, HUD can use the threat of lawsuits to press reluctant municipalities to buy into a regional consortium’s every plan.

Regionalists consider the entire city-suburb system bigoted and illegitimate, so there are few local governments that HUD would not be able to slap with a disparate-impact suit on regionalist premises. It’s unlikely that any suburb has a perfect demographic and “asset” balance in every category. All HUD has to do is decide which suburban governments it wants to lean on. With every locality vulnerable to a suit, every locality can be made to play the regionalist game.

Leftist housing activists worry that AFFH never specifies the penalties a suburb will face for imbalances in its housing patterns. These activists just don’t get it. A thoughtful reading of AFFH, including its extraordinary “dialogue” section, makes it clear that HUD can go after any suburb, any time it wants to. The controlling consideration will be politics. HUD has got to boil the frog slowly enough to prevent him from jumping.

It will take time for the truth to emerge. Just by issuing AFFH, the Obama administration has effectively annexed America’s suburbs to its cities. The old American practice of local self-rule is gone. We’ve switched over to a federally controlled regionalist system. Now it’s strictly a question of how obvious Obama and the Democrats want to make this change — and when they intend to bring the hammer down. The only thing that can restore local control is joint action by a Republican president and a Republican congress to rescind AFFH and restrict the reach of disparate impact litigation. We’ll know after November 8, 2016.

<<<

$SPF Standard Pacific Sees Big January Orders Growth

Add upscale #homebuilder Standard Pacific (SPF) to those reporting strong January order growth, which some economists and builders say bodes well for the coming spring selling season. SPF says during the 4Q conference call had a net 463 contracts signed last month, up 27% from a year earlier and faster than 4Q's 11% order growth. "Sales trends were positive in nearly all of our markets in January," notes CEO Scott Stowell. "2015 is off to a strong start, and we're looking forward to the spring selling season." Shares rise 4.1% to $7.54, moving shares back into the green for 2015.

http://seekingalpha.com/article/2894876-standard-pacifics-spf-ceo-scott-stowell-on-q4-2014-results-earnings-call-transcript?auth_param=21hhj:1adai9a:1cc3cf0705313b05dc841355772c93ac&uprof=45

>>> Sovran Self Storage, Inc. operates as a real estate investment trust (REIT). It engages in the acquisition, ownership, and management of self-storage properties in the United States. The company?s self-storage properties offer storage space to residential and commercial users, as well as offer outside storage for automobiles, recreational vehicles, and boats. As of February 15, 2007, it owned and managed 328 properties, consisting of approximately 20.3 million net rentable square feet in 22 states. Sovran Self Storage has elected to be treated as a REIT for federal income tax purposes and would not be subject to income tax to the extent it distributes at least 90% of taxable income to its stockholders. The company was founded in 1982 and is headquartered in Williamsville, New York. <<<

>>> Extra Space Storage, Inc. operates as a real estate investment trust (REIT) in the United States. It engages in property management and development activities that include acquiring, managing, developing, and selling, as well as the rental of self-storage facilities. As of December 31, 2006, Extra Space Storage owned interests in 567 properties located in 32 states and Washington, D.C., as well as managed 74 properties owned by franchisees or third parties. As a REIT, the company would not be subject to federal corporate income taxes if it distributes at least 90% of its taxable income to its stockholders. The company was founded in 1977 and is based in Salt Lake City, Utah. <<<

Storage REITS -- >>> An alternative place to store your money with a 483% return...

By Nicole Goodkind

Yahoo Finance

http://finance.yahoo.com/news/the-number-one-alternative-investment--storage-space-164102530.html

The number one alternative investment according to Bloomberg Markets is … storage space. Yes, you read that correctly.

According to the magazine’s annual ranking of alternative and exotic investments, storage units (specifically storage facility REITs) have been having a great few years.

Storage REITs such as Extra Space (EXR), Public Storage (PSA), CubeSmart (CUBE) and Sovran Self Storage (SSS) have seen gains between 142% and 483% in the past five years. Storage as a category has returned 101% from 2008 through 2011, outperforming all other REIT categories. There are now 52,000 storage properties in the United States, up from just under 20,000 in 1990. Nearly 11 million Americans rent storage units each year.

“Homeownership in the U.S. is at its lowest point in 19 years,” says Devin Banerjee, U.S. investing reporter at Bloomberg News, "and people aren’t upsizing [moving into larger homes] as much as they used to. if you’re not upsizing, then you need a place to put all of that stuff. You’re going into storage.”

Now that the economy seems headed toward recovery, however, it may be too late to get in on these gains.

“There are some warnings signs across the markets," he says. “The industry is consolidating, these large players are going into small towns, trying to expand geographically and acquiring local players."