News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Prologis - >>> Warehouse Giant Seeing Insatiable Demand From Amazon, Walmart

Bloomberg

By Natalie Wong

May 5, 2020

https://www.bloomberg.com/news/articles/2020-05-05/warehouse-giant-seeing-insatiable-demand-from-amazon-walmart

Prologis Inc., the largest owner of warehouses in the U.S., is getting a boost as social-distancing pushes consumers deeper into the embrace of e-commerce.

Companies including Amazon.com Inc. and Walmart Inc. have an “almost insatiable” appetite for more warehouse space, Chief Executive Officer Hamid Moghadam said in an interview on Tuesday.

“We’re not seeing those guys slow down, they continue to be very active in making new deals,” Moghadam said. “The strong continue to be taking a lot of space.”

Prologis and Blackstone Group Inc. have gobbled up warehouses in recent years, betting in part that more and more shopping will move online. Still, e-commerce is a relatively a small piece of the warehouse business, which is more tightly tethered to the overall economy.

Even as the pandemic fuels job losses and batters the economy, the surge in online shopping, including for groceries, is keeping vacancy rates low at Prologis properties.

The company has grown rapidly through acquisitions, but Moghadam doesn’t see buying many opportunities amid the current turmoil.

“I don’t expect anywhere near the kind of opportunities that came in other cycles,” he said. “I don’t expect fire sales.”

<<<

>>> Cell Tower REITs: 5G's True Killer App

Seeking Alpha

Apr. 22, 2019

https://seekingalpha.com/article/4255831-cell-tower-reits-5gs-true-killer-app

Summary

With 5G on the horizon, Cell Tower REITs have outperformed the broader real estate sector in each of the past four years. 5G technology will fundamentally disrupt the communications sector.

The true “killer app” for 5G will be fixed wireless broadband internet. Dense small cell networks will allow carriers to deliver fiber-like speeds without the last-mile wires into each home.

The technological limitations of 5G – notably the very small coverage area per antenna – mean that 5G small cell networks will complement, not replace, macro cell tower networks.

The Sprint/T-Mobile merger saga continues. Just when a deal appeared imminent, a new curveball emerges. We think that Sprint’s troubles are overstated and that no-deal outcome would benefit tower REITs.

Cell tower REITs continue to benefit from a favorable competitive positioning within the telecommunication sector. Concentrated ownership and strong demand have translated into substantial pricing power for cell tower operators.

This idea was discussed in more depth with members of my private investing community,iREIT on Alpha.

REIT Rankings: Cell Towers

In our REIT Rankings series, we introduce and update readers to each of the commercial and residential real estate sectors. We analyze REITs within the sectors based on both common and unique valuation metrics, presenting investors with numerous options that fit their own investing style and risk/return objectives. We update these rankings every quarter with new developments.

cell tower REIT overview

We encourage readers to follow our Seeking Alpha page (click "Follow" at the top) to continue to stay up to date on our REIT rankings, weekly recaps, and analysis on the REIT and broader real estate sector.

Cell Tower Sector Overview

Cell tower REITs comprise roughly 10% of the REIT ETFs (VNQ and IYR). Within the Hoya Capital Cell Tower REIT Index, we track the three cell tower REITs which account for roughly $160 billion in market value: American Tower (AMT), Crown Castle (CCI), and SBA Communications (SBAC). Cell tower REITs are on the "growth" side of the real estate spectrum and generally pay a low dividend yield but have achieved some of the highest internal and external growth rates across the real estate sector over the past decade. Investors seeking focused but diversified exposure to this sector should consider the Benchmark Data & Infrastructure Real Estate ETF (SRVR).

cell tower REITs

More than any other real estate sector, cell tower ownership is highly concentrated. Cell tower REITs own roughly 50-80% of the 100-150k investment-grade macro cell towers in the United States. For this reason, while cell towers may constitute only a tiny portion of total real estate asset value in the United States, they constitute a disproportionally high importance in the market capitalization-weighted investible real estate indexes and in fact, American Tower and Crown Castle are the two single largest REITs. Strong performance from cell tower REITs over the past two years have explained much of the underperformance of the traditional "core" real estate sectors.

cell tower REIT overview

Consumers want both speed and mobility, but because of the physics and economics of data transmission, there is often a tradeoff between the two. For pure speed and low-latency, a robust fiber-based or dense 5G small-cell network is ideal. This requires laying thousands of miles of underground cables and/or having hundreds of thousands of small-cell base stations using high-band spectrum. For pure mobility, a wide-reaching macro cellular network using high-powered transmitters at lower and farther-reaching spectrum is ideal. This requires having a network of macro towers, but each tower is capable of servicing tens of thousands of devices each, rather than several dozen or hundreds of customer per small-cell antenna.

cell tower networks

Since consumers need both speed and mobility and none of the players are able to fully satisfy both of these needs, a blend of different technologies- including macro cell networks- will continue to be used to meet the growing demand for data connectivity. It’s important to note that both AMT and SBAC have significant international operations, while CCI is a pure-play US operator. AMT and SBAC focus on the macro tower business, while CCI has made significant investments in fiber and small-cell networks in addition to their primary tower business.

Bull & Bear Thesis for Cell Tower REITs

Our research continues to indicate that macro cell towers provide the most economical mix of coverage and capacity, and recent challenges with dense small-cell network deployment have affirmed our belief that macro towers will continue to be the "hub" of next-generation networks for the foreseeable future. While communications technology does change very rapidly, it appears that the physical and economic limitations of the alternative technologies (low-orbit satellites, wide-spread small cell networks, and outdoor Wifi) are unlikely to abate anytime soon and the risk of technological obsolescence in the 5G-era is often overstated.

5G vs. 4G

Cell tower REITs continue to command strong competitive positioning in the telecommunications sector. Cell carriers sold off their tower assets beginning in the mid-2000s to de-lever their balance sheet and free-up capital to expand their networks. Supply growth is almost non-existent in the US as there are significant barriers to entry through the local permitting process. The relative scarcity of cell towers, combined with the absolute necessity of these towers for cell networks, has given these REITs substantial pricing power. While cell carriers have tried to make moves to establish leverage over tower owners by building or acquiring towers themselves, carriers have limited available capital to spend on these initiatives, especially in light of the capital-intensive 5G rollout.

bullish cell towers

The four-year run of strong performance, however, has pushed cell tower REIT valuations to elevated levels compared with the rest of the real estate sector. The land under cell towers, of course, is worth very little without a functioning macro cell site. While we don’t believe there is an immediate risk of technological obsolesce, it is impossible to predict technological innovation in a decade, much less over multiple decades. Further, there are only four major players in the US carrier industry (and potentially three if the Sprint /T-Mobile merger gets approved), limiting the number of potential tenants for these REITs. Carriers are incentivized to invest capital in alternative technologies like small-cells and DAS to try to reduce the competitive position of cell towers. Perhaps the most significant risk relates to the fact that these REITs own just 30% of the land under their structures and lease the other 70% through (typically long-term) ground leases.

bearish cell towers 2019

Potential Outcomes of Sprint/T-Mobile Deal

The cell tower REIT industry continues to await the outcome of the Sprint/T-Mobile merger, which has the potential to alter the competitive dynamics within the telecommunications space. Earlier this year, the third and fourth largest US wireless carriers announced a long-awaited merger agreement that would consolidate the industry into three nearly-equal competitors along with AT&T (NYSE:T) and Verizon (NYSE:VZ). Following years of discussions and a failed attempt at a merger in 2014 that was blocked by US regulators, the two firms finally came to terms on the potential $26-billion deal. The combined entity would command a roughly 35% share of total retail wireless connections, including 25% of postpaid phone subscribers and nearly 60% of prepaid phone subscribers.

While revenues from Sprint (NYSE:S) and T-Mobile (NASDAQ:TMUS) comprise a combined 26% of total industry revenues, the “overlap” between Sprint and T-Mobile cell tower sites is roughly 4% of total industry revenues. This 4% represents a "worst-case-scenario" in which T-Mobile completely shuts down the Sprint network on redundant towers and does not subsequently need to upgrade their equipment to handle the increased capacity. Crown Castle, which is US-focused, would be most affected, while American Tower, which has a significant international presence, would be relatively unscathed.

Last week, The Wall Street Journal reported that the Department of Justice informed T-Mobile and Sprint that the deal is “unlikely to be approved as currently structured.” The general consensus among analysts is that the odds of approval have now decreased from above 75% late last year to below 50% currently. As we discussed during our last update, we believe that the merger approval will likely hinge on the regulator's assessment of the likelihood and forecast of four key unknown factors, ranked in order of importance.

1) Can Sprint survive without a merger?

2) Would Sprint have other suitors (cable companies, tech companies)?

3) Would a merger help or hurt the growth of 5G?

4) Is wireless broadband a competitor to the home broadband providers?

Given the uncertain answers to these four questions and a wide range of permutations of possible outcomes, analysts are generally split as to whether cell tower REIT investors should be rooting for or against the potential merger. Our assessment is that cell tower REITs would ultimately benefit from a no-deal outcome, but that the downside risk is more significant if Sprint were to indeed fail as a result. We outline our assessment through an analysis of the three possible outcomes.

Scenario 1: Merger Approved

The cellular carrier industry would be consolidated into three players of roughly equal size. With more balance sheet capacity, the merged T-Mobile would likely ramp up network spending in line with Verizon and AT&T, which would translate into an immediate boost to cell tower REIT revenues. With one less competitor, the 5G rollout begins sooner but is focused on higher-value markets and consumer pricing would likely become less competitive, translating into higher margins for carriers, but potentially fueling further network investment. Over time, however, the competitive positioning of cell tower REITs would be diminished. Carrier initiatives to gain leverage over cell tower REITs, including building their own towers or taking over leases from REITs, would be incrementally more successful and growth would moderate but remain at above-inflation levels due to the still-favorable competitive positioning of cell tower REITs.

Probability: 50%. For Cell Tower REITs: Decent/Default Outcome.

Scenario 2: Merger Rejected. Sprint Finds Third-Party Partner

The merger gets rejected, but Sprint's underpriced and valuable network and spectrum assets are attractive to cable broadband providers (Comcast (NASDAQ:CMCSA), Charter Altice) who recognize the mounting and legitimate threat from 5G fixed wireless broadband, which we believe to be underappreciated by the market. Alternatively, a cash-flush technology company (Amazon (NASDAQ:AMZN), Google (NASDAQ:GOOG) (NASDAQ:GOOGL), or Microsoft (NASDAQ:MSFT)) sees the assets as an underpriced compliment to their existing data center infrastructure and a new source of distribution to mitigate the competitive threats from the incumbent broadband providers. Sprint is able to leverage this partnership to become a legitimate competitor in the space. Meanwhile, T-Mobile continues its strong run of adding customers at sector-leading rates. The carrier industry remains at four players with T-Mobile and Sprint close behind and consumer pricing competition remains intense. The four carriers battle to become leaders in 5G and access is widespread. Initiatives to gain leverage over cell tower REITs are largely unsuccessful and pricing power remains strong.

Probability 35%. For Cell Tower REITs: Best Outcome.

Scenario 3: Merger Rejected. Sprint Fails

The merger gets rejected Sprint is unable to find a suitable partner. Sprint's investors, including SoftBank (OTCPK:SFTBY), scale back their investment and the network falls further behind the other three carriers and continues to lose customers until being unable to operate any longer. In bankruptcy, Sprint's assets are distributed around the telecom sector including to AT&T and Verizon, further strengthening their grip on the emerging duopoly. T-Mobile's strong run of performance slows down and cannot keep up with the network spending of the two major players without the complementary asset of Sprint. The carrier industry becomes a de-facto duopoly and cell tower REIT competitive positioning is significantly diminished. Consumer pricing becomes significantly less competitive and the 5G rollout continues but is isolated only to the most high-margin deployments. Carrier initiatives to gain leverage over tower REITs are largely successful and the industry becomes more akin to the data center REIT sector over the past several years with below-inflation internal growth rates and weak pricing power over increasingly dominant tenants.

Probability 15%. For Cell Tower REITs: Worst Outcome.

Recent Cell Tower REIT Fundamental Performance

2018 was another strong year for the cell tower sector as the early effects of network densification to fuel 5G networks powered above-trend organic growth. Organic tower revenue, effectively the same-store NOI equivalent, continues to grow at a sector-leading 6%+ rate as carriers continue to invest heavily in network densification and equipment upgrades. With the high degree of operating leverage inherent with the co-location tower model, tower REITs are seeing amplified benefits increased network spending.

cell tower REIT AFFO

These REITs are forecasting an average 8% rise in AFFO per share in 2019, among the strongest rates of growth in the real estate sector. Along with robust organic growth, external growth via strategic acquisitions remains a central focus of cell tower REITs, aided by the cost of capital advantage enjoyed by these firms. As we'll discuss shortly, cell tower REITs trade at an estimated 30-50% premium to private market-implied net asset values, meaning that external acquisitions, though somewhat limited, are easily accretive to earnings.

REIT tower sites

The combination of strong organic growth and continued external growth fueled a 16% rise in total property revenues in 2018, rising from the 13% rate achieved in 2017, boosted by the effects of Crown Castle's merger with small-cell operator Lightower. While appearing to be very conservative, these REITs offered guidance that projects a 5% rise in property revenues in 2019.

Carrier Performance & Capital Spending

Cell tower REITs are inexorably linked with the underlying performance of their cell carrier tenants, who delivered another very strong year. AT&T, Verizon, T-Mobile, and Sprint combined to add more than 4.5 million post-paid wireless customers in 2018, a sharp increase from the 3.8 million added in 2017, and the strongest year ever for cell carriers. Pricing remains highly competitive with customers effectively seeing an average 3% drop in their phone bills.

cell carrier pricing

Capital spending by cell carriers is a key driver of growth for tower REITs. Capex among US carriers had been in a lull for the past two years as much of the available capital has been put towards spectrum acquisition which will power the next generation 5G networks. Capital spending is expected to ramp up again as carriers begin to deploy 5G networks over the next five to ten years.

network spending cell

Recent & Long-Term Stock Performance

Since NAREIT began tracking the sector in 2012, cell tower REITs have outperformed the REIT index in every year besides 2014. Cell towers continue to be one of the few remaining growth engines of the REIT sector and, considering the positive operating environment forecast for 2018-2020, don't appear to be slowing down anytime soon.

REIT sectors

The good times have continued for the cell tower REIT sector this year despite the merger uncertainties. The Hoya Capital Cell Tower REIT Index has gained more than 19% this year compared to a 14% gain in the broader REIT index. Receding interest rates and signs of moderating global growth have lifted REIT valuations across the sector following the worst year since the recession.

cell tower REIT performance

American Tower has led the way over the last two years, followed by SBA Communications. Investors remain somewhat skeptical on the economic returns from Crown Castle's significant investment in fiber and small cells over the last several years, explaining some of the underperformance since 2016.

cell tower REIT stocks

Valuation of Cell Tower REITs

Strong performance over the past four years has pushed cell tower REIT valuations towards the most expensive end of the real estate sector. Cell towers trade at a sizable Free Cash Flow premium (aka AFFO, FAD, CAD) to the REIT average, but after accounting for the sector-leading expected growth rates, cell tower REITs very quite attractively valued based on the FCF/G metric. As discussed above, cell tower REITs trade at some of the widest NAV premiums in the real estate sector, giving these companies the "cheap" equity capital to fuel further external growth.

cell tower REIT valuation

Cell Tower REIT Dividend Yield

Cell tower REITs are among the lowest-yielding REIT sectors, paying out just 53% of their free cash flow and instead of plowing that capital back into the business to fuel external growth. The sector pays an average 2.2% dividend yield, among the lowest among REITs.

cell tower REIT dividend yield

Within the sector, only Crown Castle acts like a typical REIT when it comes to distributions. CCI pays a healthy 3.7% dividend yield, while AMT pays 1.9%, and SBAC does not yet pay a dividend.

cell tower dividends

Cell Tower REITs & Interest Rates

Cell tower REITs skew towards the "growth" side of the real estate sector, reacting more to economic growth expectations than to changes in interest rates. Among US REIT sectors, cell towers are the third least interest rate sensitive sector and could provide balance to an otherwise rate-sensitive REIT portfolio.

REITs interest rates

Within the sector, AMT and SBAC are classified as Growth REITs. CCI, which pays a 4% dividend, is a Hybrid REIT and has characteristics that are more aligned with the REIT averages.

interest rates REITs

Bottom Line: Wireless Broadband is 5G's Killer App

With 5G on the horizon, Cell Tower REITs have outperformed the broader real estate sector in each of the past four years. 5G technology will fundamentally disrupt the telecommunications industry. We believe that the true “killer app” for 5G will be fixed wireless broadband internet, as dense small cell networks will allow carriers to deliver fiber-like speeds without the wires.

The technological limitations of 5G – notably the small coverage area – mean that macro towers will continue to be the primary hub of cellular networks. Network densification drives cell tower revenues. The Sprint/T-Mobile merger saga continues. Just when a deal appeared imminent, a new curveball emerges. We think that Sprint’s troubles are overstated and that no-deal outcome would benefit tower REITs.

Cell tower REITs continue to benefit from a favorable competitive positioning within the telecommunication sector. Low supply and high demand have translated into substantial pricing power for cell tower operators. We analyzed the three potential merger outcomes and believe that a no-deal scenario would be the best-case scenario for these companies. This analysis, however, is contingent upon our view that wireless broadband does indeed become the "killer app" of 5G and that Sprint is a valuable partner or acquisition target from a third-party (cable or technology) company as a result.

The risk of a no-deal outcome is that the carrier industry devolves into an effective duopoly, which would translate into significant downside risk to the competitive positioning of the cell tower REIT sector. The success of the early 5G fixed wireless broadband tests in a handful of US cities will be closely monitored by all players in the industry and the ultimate fate of Sprint may hinge on its relative success. If wireless broadband is indeed the 5G "killer app" we think it could be, the future looks bright for cell tower REITs and carriers alike.

<<<

>>> Here's Why You Should Buy SBA Communications (SBAC) Stock Now

Zacks Equity Research

April 17, 2020

https://finance.yahoo.com/news/heres-why-buy-sba-communications-144102324.html

It seems to be a wise decision to add SBA Communications Corporation SBAC, given its efforts to extend business in select international markets with high growth characteristics. Moreover, amid growing demand for data volume and deployment of 5G network, wireless carriers are expanding and enhancing their networks. These positive trends are expected to drive demand for the company’s communications infrastructure assets.

SBA Communications is expected to witness year-over-year growth in funds from operations (FFO) per share in 2020. The company also beat estimates in the last four reported quarter, the average positive surprise being 2.8%.

Its price performance also seems impressive. In fact, this Zacks Rank #2 (Buy) stock has gained 28.1% in the year-to-date period against the industry’s decline of 13.9%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Notably, SBA Communications has a number of other aspects that make it a solid investment choice.

Why the Stock is an Attractive Pick

Favorable industry tailwinds: Mobile subscriber growth has significantly boosted the wireless tower industry. Next-generation 4G LTE networks and increased usage of smartphones and tablets are creating impressive demand for the company’s site leasing business. With increasing smartphone adoption, greater broadband demand and plans for 4G service worldwide, the company is set to pursue international wireless infrastructure opportunities. Furthermore, wireless consumer demand is expected to considerably increase in the upcoming years supported by innovation and accelerated adoption of data-driven mobile devices and applications such as machine-to-machine connections, social networking and streaming of video.SBA Communications’ extensive infrastructure portfolio is well-positioned to meet such demands.

Encouraging FFO picture: SBA Communications’ projected FFO growth rate is 10.3% for 2020. This is higher than the industry average of 0.5%. Further, management expects 2020 AFFO per share in the range of $9.07-$9.47.

Strategic Portfolio Expansion: With decent presence in the United Sates and its territories, SBA Communications has developed or acquired thousands of towers throughout Central and South America and across Canada over the years. Presently, the company continues to expand its tower portfolio and seek new growth opportunities. Supported by strong industry fundamentals, the company is identifying international markets with high growth characteristics and extending its business in these regions. In fact, during the December-end quarter, it acquired 1,336 communication sites for a total cash consideration of $471.7 million.

Encouraging Dividend Payout: Solid dividend payouts remain the biggest attraction for REIT investors, and SBA Communications is boosting shareholder wealth through dividend hikes. Specifically, concurrent with its fourth-quarter 2019 earnings release, the company announced a quarterly cash dividend of 46.5 cents on its Class A common stock, indicating a 25.7% hike from its October-December quarter payout. Given the company’s financial position compared with the industry’s, this dividend rate is anticipated to be sustainable.

<<<

Interesting. As for European real estate market, there is current downturn in property prices for property in Germany https://tranio.com/germany/ etc. Developed countries like Germany, France or the USA have already taken extensive and effective measures to curb the spread of the pandemic. As reported by CNBC, the outbreak in China is under control and economic activity is slowly recovering.

Interesting. As for European real estate market, there is current downturn in property prices for property in Germany https://tranio.com/germany/ etc. Developed countries like Germany, France or the USA have already taken extensive and effective measures to curb the spread of the pandemic. As reported by CNBC, the outbreak in China is under control and economic activity is slowly recovering.

>>> Beware the Big Price Tag for a Mall REIT With Roots in Sears

Barron's

By Bill Alpert

March 6, 2020

https://www.barrons.com/articles/beware-the-big-price-tag-for-a-mall-reit-with-roots-in-sears-51583548833?siteid=yhoof2&yptr=yahoo

Real estate was the ace in the hole in Eddie Lampert’s investment strategy for Sears Holdings. So in 2015—a decade after the hedge fund manager’s ESL Investments took over the struggling retail chain— Sears spun off its interests in some 260 shopping mall properties into a real estate investment trust called Seritage Growth Properties.

Before that year was out, Berkshire Hathaway CEO Warren Buffett used his own money to buy a 7% stake in Seritage (SRG) for about $35 a share. The stock hit $57 the next year amid enthusiasm that Seritage would replace the bargain rents paid by Sears with market-rate tenants. The real estate play looked like a winner to Barron’s in early 2017.

But Sears was still Seritage’s main tenant. When Sears Holdings (SHLDQ) filed for bankruptcy protection in 2018, the retailer still filled 70% of Seritage’s space.

Seritage stock now goes for about $31 a share. That prices the enterprise at $3 billion and, by most measures, values Seritage on a par with the better mall REITs. Looking closely at Seritage’s recent results, it is hard to understand why its stock deserves that generosity. Seritage and Lampert declined our requests for comment, while Buffett didn’t respond to our query.

After Sears’ bankruptcy, the chain vacated over 200 Seritage properties. Its contribution to the REIT’s rental income has dropped to 5% of the total. Revenue at Seritage in 2019 was $169 million, down sharply from the 2016 level of $250 million. Its net loss in 2019 was $64 million, or 1.77 cents a share. REITs use an operating cash-flow measure called funds from operations, or FFO, and that number sank at Seritage from a positive $16 million in 2018 to a negative $34 million in 2019, or minus 61 cents a share. It pays no dividends on its common stock.

The red ink will be about as deep this year, Wall Street says. One has to look to 2021 to find a positive forecast for Seritage funds from operations. The sole analyst polled by FactSet projects about $20 million in FFO for next year, or 38 cents a share, on revenue of $260 million. That means today’s stock price for Seritage is 80 times next year’s forecast for FFO.

By way of comparison, the classiest of the class-A mall operators, Simon Property Group (SPG)—at its current stock price of $119—trades for just nine times the consensus forecast for 2021 funds from operations. Macerich (MAC) trades for six times. A well-regarded shopping center REIT, such as Regency Centers (REG), trades for 15 times next year’s FFO.

Malls are a forlorn sector these days, but even in its unhappy class, Seritage stands out for how many of its properties stand vacant. The company’s annual report makes painful reading, with a six-page list of wholly owned properties studded with empty malls in towns like Burnsville, Minn., and Lebanon, Pa. In all, only 43% of Seritage’s 29 million square feet of space was leased at the end of December. At Simon Property, 95% of retail space was occupied.

A main theme in the Seritage strategy has been the re-leasing of Sears locations to new tenants, at rents several-fold higher. But many retail tenants are struggling, these days. In addition to the 6% of its rent roll still paid by Sears and Kmart at year end, Seritage’s top tenants included the arcade chain Dave & Buster’s Entertainment (PLAY), the At Home Group (HOME) furnishings chain, and the clothing discounter Burlington Stores (BURL)—totaling 18% of the REIT’s annual rent and all causing angst in their own investors lately, amid faltering revenue.

Seritage’s other strategy is to redevelop its retail space and parking lots as fitness centers, restaurants, medical offices, or multifamily dwellings. In recent visits with investors, Seritage executives called attention to mixed-use projects near Seattle, Dallas, and Chicago that will together cost over $325 million in just the initial phase.

The REIT has good reason for staying in touch with institutional investors. Seritage has some remaining credit facilities, but without operating cash flow, it will have to fund its billions of dollars worth of redevelopment ambitions by selling off property and by selling stock. So shareholders should brace for dilution.

Meanwhile, if you’ve got a clever use for an empty Sears store, give Seritage a call.

<<<

Buffett - >>> Seritage Growth Properties (SRG) is a publicly-traded, self-administered and self-managed REIT with 184 wholly-owned properties and 28 joint venture properties totaling approximately 33.4 million square feet of space across 44 states and Puerto Rico. The Company was formed to unlock the underlying real estate value of a high-quality retail portfolio it acquired from Sears Holdings in July 2015. The Company's mission is to create and own revitalized shopping, dining, entertainment and mixed-use destinations that provide enriched experiences for consumers and local communities, and create long-term value for our shareholders. <<<

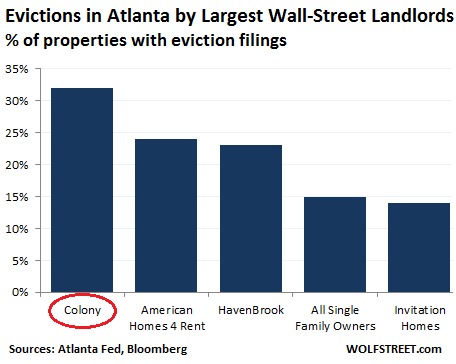

>>> Real Estate Billionaire Barrack Says Commercial Mortgages on Brink of Collapse

Bloomberg

By Erik Schatzker

March 22, 2020

https://www.bloomberg.com/news/articles/2020-03-22/colony-s-barrack-says-commercial-mortgages-on-brink-of-collapse?srnd=premium

Warns of cascade of margin calls, foreclosures, bank failures

White paper calls for banks, government to coordinate relief

Real estate billionaire Tom Barrack said the U.S. commercial-mortgage market is on the brink of collapse and predicted a “domino effect” of catastrophic economic consequences if banks and government don’t take prompt action to keep borrowers from defaulting.

Barrack, chairman and chief executive officer of Colony Capital Inc., warns in a white paper of a chain reaction of margin calls, mass foreclosures, evictions and, potentially, bank failures due to the coronavirus pandemic and consequent shutdown of much of the U.S. economy. The paper was posted late Sunday on online publishing platform Medium.

“Loan repayment demands are likely to escalate on a systemic level, triggering a domino effect of borrower defaults that will swiftly and severely impact the broad range of stakeholders in the entire real estate market, including property and home owners, landlords, developers, hotel operators and their respective tenants and employees,” he wrote.

Barrack said the impact could dwarf that of the Great Depression.

Rescue Plan

Specifically, his paper highlights the fragility of mortgage real estate investment trusts, or REITs, and credit funds and the lenders that provide them with liquidity via repurchase financing. He argues for a rescue plan coordinated by banks and supported by government that includes the following:

$500 billion of taxpayer funds to provide liquidity to the financial system, including for loans and repurchase contract

Temporary suspensions of both mark-to-market accounting and certain loan-modification rules

Delaying until 2024 a new accounting rule governing the recognition of credit losses

Leeway for banks to provide loan forbearance without triggering bank-capital rule violations

Barrack, a longtime friend of President Donald Trump, has much at stake in the outcome. Most of Colony’s investments are in or connected to real estate. The Los Angeles-based firm’s year-end financial report lists $3.54 billion of assets in hospitality real estate and $725 million of debt and equity investments at Colony Credit Real Estate Inc., its publicly traded commercial mortgage REIT.

<<<

>>> Commercial real estate booms in cannabis-friendly states

Yahoo Finance

Sarah Paynter

February 12, 2020

https://finance.yahoo.com/news/commercial-real-estate-booms-in-cannabisfriendly-states-164314252.html

Investors are buying up warehouses and retail space in cannabis-friendly states.

In a reversal from 2018 trends, cannabis investors are buying up commercial property, particularly warehouses, in states where recreational cannabis use has been legalized for more than three years, according to a new study by the National Association of Realtors, based on a September 2019 survey of over 600 commercial brokers in states like Colorado, where recreational cannabis use is legalized, and in states, like Florida, where medical marijuana use is legal.

The U.S. has a patchwork of marijuana legalization laws by state, despite federal laws against the drug. Graphic by the National Association of Realtors.

“It is very important to understand the supply and demand, and the regulatory dynamic, in each state. Focusing on states with higher barriers to entry makes a license more valuable and makes that real estate more valuable,” said Katie Barthmaier, chief executive officer of Green Acreage, a cannabis-focused real estate investment trust.

Warehouse demand increased in 42% of the markets with longstanding (over three years) recreational legalization, and 34% of markets that legalized recreational use since 2016 also saw increased demand from the previous year. Only 18% of markets without recreational marijuana legalization claimed warehouse demand growth.

In 2018, warehouse demand in states with only medical use outpaced demand in states with recreational use, 34% to 27%, respectively, according to last year’s study.

In a reversal from 2018 trends, cannabis investors are buying up commercial property in states where recreational cannabis use has been legalized for more than three years. Graphic by the National Association of Realtors.

“In states that have a longstanding legal [cannabis] industry, warehouses have especially been of interest to commercial investors. That increased demand, I suspect is not just for storage but for growing,” said Dr. Jessica Lautz, vice president of demographics and behavioral insights for the National Association of Realtors.

Meanwhile, demand for retail space increased in 27% of longstanding recreation-friendly markets (before 2016), compared to 19% of recently-legalized markets or 18% of prescription-only markets. The trend is a reversal from 2018, when storefronts saw greater growth in medical use-only markets than in markets with recreational use.

“Investors knew folks would need space to cultivate and manufacture cannabis. A lot of unused space was rented up and bought by investors,” said Jack Nichols, general counsel and chief operating officer of Harborside, a Calif.-based marijuana company. Nichols said that cannabis investor interest has inflated real estate prices as demand for commercial space grows.

Cannabis companies are held back

Because cannabis companies cannot turn to traditional banks, buying or leasing property can be difficult. Financing is usually supplied by specialized venture capitalists, private real estate investment funds and publicly-traded companies.

“On the investment side, banks cannot loan you money, insurance companies cannot deal with you and few funds can enter the space. There is no institutional capital in the space,” said Ori Bytton, founder of California-based real estate management company for cannabis operators, WeGrow CA, and founder and chief executive officer of Natura Life + Science, the largest vertically-integrated grow and processing facility in California.

Cannabis companies say that investor-driven capital offers loans at high interest rates and with hefty restrictions.

“Everybody thinks cannabis is the most profitable business, and they try to take advantage of it… They all wanted me to personally put up my house as a guarantee on a lease… It’s egregious,” said Heidi Adams, chief marketing officer at Calif.-based Henry’s Original cannabis company, which she said searched a year and a half before finding a “reasonable” lease.

Restrictions could soon lift, however, if the Senate passes the SAFE Banking Act, which would give cannabis companies access to traditional banking. The act was passed by the U.S. House of Representatives in September 2019.

<<<

>>> Pacer Benchmark Industrial Real Estate SCTR ETF (INDS)

Expense Ratio: 0.6%

https://investorplace.com/2019/02/5-of-the-best-thematic-etfs-to-consider/

Some of the best ETFs provide access to the real estate sector and do so in unique fashion. The Pacer Benchmark Industrial Real Estate SCTR ETF (NYSEARCA:INDS) hails from a family of unique, thematic ETFs with real estate exposure. INDS offers exposure to one of the real estate industry’s most compelling growth segments.

Industrial real estate investment trusts (REITs), including those residing in INDS, own facilities and warehouses used to store goods for the e-commerce boom. Industrial REITs are “important because investing in this space is a roundabout way to play the e-commerce sector without exposure to volatile and expensive retail equities like Amazon, Walmart and more,” according to Pacer.

INDS is beating the largest U.S. REIT ETF by nearly 360 basis points this years and this thematic ETF, which will be one year old in May, does not skimp on yield, as highlighted by a 30-day SEC yield of 3%.

<<<

>>>2 Investments To 'Load Up' Before The Recession

Nov. 28, 2019

Jussi Askola

REITs, real estate, research analyst

https://seekingalpha.com/article/4308392-2-investments-load-up-recession

Summary

The investment world is faced with an unprecedented challenge: both stocks and bonds have simultaneously become overvalued and risky.

Investors are quickly seeking refuge in real assets such as commercial properties, pipelines, farmland, airports, timberland, and other.

While investing in real assets may have been reserved to high net worth individuals in the past, today there exists a lot of publicly-traded alternatives.

Below we present 2 of our favorite real assets and explain why their cash flows are resilient to recessions.

Looking for a portfolio of ideas like this one? Members of High Yield Landlord get exclusive access to our model portfolio. Get started today »

Investors are today faced with a big challenge:

"There is nothing interesting to buy."

On one hand, stocks are trading at a 30% premium to historical averages – despite slowing growth in a late cycle economy:

And on the other hand, bonds pay historically low interest rates that may not even cover inflation in the long run.

This creates two major problems to investors:

Stocks: With high valuations in a late cycle, risks are very high and investors could suffer significant capital losses from a return to historic valuation multiples.

Bonds: Not enough income is earned to meet investor's immediate needs. This is particularly dangerous to large institutions and retirees.

What is then the solution to deal with these challenges?

Our preferred strategy is to invest in Real Assets. Commercial properties, farmland, timberland, energy pipelines and other similar real assets are the only remaining investments that can still provide high income and inflation protection – without taking an enormous amount of risk.

These are not just the empty words of a Seeking Alpha author. Over the past 10 years, institutional capital in the real asset space has grown by $30 trillion. Yes that’s trillion with a “t”. Over the coming 10 years, another $50 trillion is expected to shift to real asset investments.

real asset allocations on the rise

Stocks and bonds are not providing the needed returns and professional investors are quickly changing portfolio allocations. By 2030, the allocations to real assets are expected to reach up to 40% of intuitions portfolios:

So far, individual investors have been slow to react. With poorer access to research and no expertise in real asset investing, individual investors continue to overexpose themselves to the risks of owning traditional stocks and bonds.

Fortunately, you do not need to be a multi-billion-dollar institution to invest in real assets. At High Yield Landlord, we specialize in liquid alternatives to gain exposure to high yielding real assets. This includes REITs, MLPs, Utilities, and other listed infrastructure companies.

If you've read until here, we want to share with you two of our "Top Picks" among high-yielding REIT opportunities. These two REITs are particularly well-positioned in today’s late cycle economy because of their more defensive nature, steady cash flow growth, and high level of dividend security.

INVESTMENT #1 – Medical Properties Trust (MPW)

MPW is our one and only Healthcare REIT investment at the moment.

The Buy Thesis in 3 Bullet Points:

Superior Cap Rates: Most REITs compete for properties in the 5-7% cap rate range. MPW is able to target greater cap rates at closer to 8% by specializing in hospitals - a property type that is mostly ignored by the investment community.

Resilience in Late Cycle: People need hospitals - regardless of economic conditions. MPW's tenants are healthy and enjoy strong rent coverage ratios. If we were to go into a recession tomorrow, we would expect the cash flow to remain stable - allowing it to pay a sustainable 5.3% dividend yield.

Strong Acquisition Pipeline: As the only "pure-play" Hospital REIT, MPW enjoys valuable relationships with operators to conduct sale and leaseback transactions. With a strong acquisition pipeline and the capital to fund it, we expect 5-8% annual growth in the coming years.

You can read our full investment thesis here:

Investing In Hospitals: Recession Resilience, High Growth, And 5.6% Yield

Recap of 3rd Quarter Results:

This company is doing absolutely amazing:

It beat on FFO and revenue expectations. It also reaffirmed its full year guidance – which it already boosted during the last quarter.

The CEO talks about a “record-breaking year” with “monumental results”. This is because year-to-date, the company has grown its assets by 40%!

Its new acquisitions are done at ~8% cap rates – which results in immediately accretive growth.

They note that they have a pipeline of up to $5 billion for transactions in the coming quarters. The company is not slowing down.

The investment story was already strong in MPW, but with these new acquisitions, the story is only getting better. We also love the recent expansion to more global markets including the UK and Switzerland which have very favorable demographics for hospitals. With such healthy spreads, and defensive properties, we believe that MPW is a near certain future outperformer. If the share price remains around $20 per share, we will buy more shares in the near term.

INVESTMENT #2 – EPR Properties (EPR)

EPR Properties (EPR) is one of our oldest investments. We invested heavily when it traded at mid-$50 and have a large capital gain at $77 today. To this day, it remains our Favorite net lease REIT investment idea.

The Buy Thesis in 3 Bullet Points:

Alpha-Rich Strategy: EPR targets specialty net lease assets that are ignored by most other investors. These include movie theaters, golf complexes, ski resorts, and other entertainment assets. They come with greater cap rates, longer leases, and higher rent increases.

History of Successful Execution: EPR has historically been a massive outperformer and everything points out to further outperformance in the long run.

Simple Story: The company beats its peers on all fronts. It pays a higher yield (6%), it grows faster (5-8%), and it has more upside potential due to its discounted multiple (14x FFO).

You can read our full investment thesis here:

A New Opportunity Has Emerged In EPR Properties

Recap of 3rd Quarter Results:

EPR has a long history of consistently beating expectations and surprising to the upside. The last quarter was no different:

It beat FFO and revenue expectations for the quarter. It also boosted its full year guidance.

It invested $118 million in new properties over the past 3 months alone. A big portion went into golf complexes such as the one illustrated above.

EPR is currently enjoying historically high spreads on its new investments and the guidance for further acquisitions is very strong.

EPR also issued $500 million in senior unsecured notes with a 10-year term at a 3.75% interest rate during the quarter. This cheap capital was used to refinance its previous notes that were yielding 5.75%.

The dividend is up by 4.2% as compared to same quarter last year.

We expect another dividend increase sometime in the coming quarters, likely in early 2020. We are very bullish and recently upgraded EPR into a Strong Buy. The discount to peers is historically high and the company is stronger than ever before. We expect ~15% upside from repricing to a higher FFO multiple and 5-8% annual FFO growth. Add to that a 6% dividend yield, and you have a recipe for consistent and predictable outperformance.

It's by targeting this type of defensive, yet undervalued REITs that we aim to outperform in today's volatile and uncertain environment.

As of today, our Core Portfolio has a 7.4% dividend yield with a conservative 68% payout ratio. Beyond the dividends, the core holdings are trading substantially below intrinsic value at just 9.2x Cash Flow - providing both margin of safety and capital appreciation potential.

<<<

>>> EPR Properties (EPR) is a specialty real estate investment trust (REIT) that invests in properties in select market segments which require unique industry knowledge, while offering the potential for stable and attractive returns. Our total investments are nearly $7.2 billion and our primary investment segments are Entertainment, Recreation and Education. We adhere to rigorous underwriting and investing criteria centered on key industry and property level cash flow standards. We believe our focused niche approach provides a competitive advantage, and the potential for higher growth and better yields. <<<

>>> Medical Properties Trust, Inc. (MPW) is a self-advised real estate investment trust formed to acquire and develop net-leased hospital facilities. The Company's financing model facilitates acquisitions and recapitalizations and allows operators of hospitals to unlock the value of their real estate assets to fund facility improvements, technology upgrades and other investments in operations. <<<

>>> California Bans Private Prisons, Immigrant Detention Centers

Newly signed law will force federal government to shut down four facilities for migrants in state

Bloomberg

By Alejandro Lazo in Sacramento, Calif., and Michelle Hackman in Washington

Oct. 11, 2019

https://www.wsj.com/articles/california-bans-private-prisons-immigrant-detention-centers-11570820873

California will work to end the use of private prisons within its borders, including for-profit immigrant detention facilities, under a law signed Friday by Gov. Gavin Newsom.

The measure, originally focused only on prisons, was expanded late in the legislative session this year to include jails that hold migrants, as they became a polarizing political issue in left-leaning California.

The new law prohibits the state from entering into or renewing contracts with private prison companies after Jan. 1 and bans their use by the state after Jan. 1, 2028. It also forbids the operation of private facilities contracted by the federal government to hold migrants in California starting next year, or whenever their current contracts expire.

“During my inaugural address, I vowed to end private prisons, because they contribute to over-incarceration, including those that incarcerate California inmates and those that detain immigrants and asylum seekers,” Mr. Newsom said in a statement. “These for-profit prisons do not reflect our values.”

An analysis earlier this year by the state Senate said the Trump administration would likely challenge the law but concluded California would likely prevail in court. A Federal Bureau of Prisons spokeswoman declined to comment.

A spokesman for Immigration and Customs Enforcement, which oversees detention centers for adult migrants, said once the law goes into effect, the agency would move detainees currently in California to facilities elsewhere in the country.

Four large detention centers could be shut down by the new law. All are operated by private prison companies, which have seen increased business from the Trump administration’s stepped-up immigration enforcement and now account for the bulk of migrant detentions in the state of California.

Two of those facilities are run by GEO Group Inc., while CoreCivic Inc. and the Management and Training Corp. run the other two. A GEO Group spokeswoman said she believed most or all of the new law will be found unconstitutional by a court. CoreCivic said the state’s ban conflicts with its stated goal to reduce prison overcrowding. A spokesman for MTC said the company provides “a valuable service to our customers and a safe and humane environment for those in our care.”

ICE detention centers will again be in the spotlight this fall as some liberal members of Congress and activists plan to inject a demand to defund the agency into federal spending talks. Activists also hope California’s ban will spur similar action in other states.

“It’s going to really set an example for other communities,” said Alejandra Pablos, an activist and Mexican national who traveled to Sacramento from Tucson last month to attend a rally in support of the law. “People are going to recognize that this could be done.”

In 2017, California passed a law blocking local governments and law enforcement from making new contracts or expanding existing contracts with the federal government to detain undocumented immigrants.

Despite those efforts, ICE in April said it was seeking to expand its capacity in the state by 5,600 detainees, according to public documents. Currently ICE has a total capacity in California of about 4,000 beds, which represents less than 10% of the agency’s national detention capacity, a spokeswoman said.

In the 2018 fiscal year that ended Sept. 30, 396,448 people were booked into ICE detention facilities, some of which are operated privately. That is 22.5% more than during the previous 12 months, according to the Department of Homeland Security.

Three other states, New York, Illinois and Iowa, have prohibited their prison systems from using private facilities. In addition, Illinois earlier this year passed a law aimed at halting a proposed detention center in Dwight, Ill., effectively banning for-profit detention centers there. New York and Iowa laws don’t ban such facilities.

The law marks a rapid shift for California, which until recently relied on private prison operators to help relieve overcrowding in state facilities. California currently has four private prisons under contract, all run by the GEO Group, which house about 1,400 of the state’s 125,000 inmates.

The GEO Group’s prison contracts with the state run through 2023, and can’t be renewed under the new law except under a possible court order to relieve overcrowding.

Some experts question whether the law will go as far as intended in light of the court-order exemption and other exceptions in the law.

<<<

>>> Prologis, Inc. (PLD) is the global leader in logistics real estate with a focus on high-barrier, high-growth markets. As of June 30, 2019, the company owned or had investments in, on a wholly owned basis or through co-investment ventures, properties and development projects expected to total approximately 786 million square feet (73 million square meters) in 19 countries. Prologis leases modern distribution facilities to a diverse base of approximately 5,100 customers principally across two major categories: business-to-business and retail/online fulfillment. <<<

LTC Properties (LTC) - >>> 3 Monthly Dividend Stocks to Buy Today

by Aaron Levitt

InvestorPlace

June 21, 2019

https://finance.yahoo.com/news/3-monthly-dividend-stocks-buy-185123145.html

Retirement: It’s all about one thing and that’s income … replacing a steady paycheck with your savings. With that, dividend stocks have plenty of appeal for retirees. Not only can you score higher yields than bonds, but you have the ability to grow those payouts over time as well. However, dividend stocks do have one major drawback.

Their payment schedules.

Most dividend stocks pay on a quarterly or even semi-annual basis. And while that may not seem like a problem, for many retirees used to a monthly or bi-weekly paycheck balancing cash flows can be a hard pill to swallow. After all, your mortgage, cable bill and car payments are due each month. To that end, getting a monthly dividend could be the answer to budgeting issues.

Luckily, there are plenty of dividend stocks that do happen to payout monthly. Here are three of the best.

Main Street Capital Corp (MAIN)

Dividend Yield: 5.89%

Most investors have never heard of businesses development companies (BDCs). That’s a shame because they can be some of the biggest yielding stocks around. BDCs are set up as pass-through entities much like real estate investment trusts, and similarly must pay out at least 90% of their earnings as dividends. How they earn that income is by loaning cash to mid-sized firms — companies too big to ask the local bank for a loan, but not big enough to launch a significant bond offering — at competitive rates. The best way to really think of them is like public-private equity firms.

And when it comes to BDCs, Main Street Capital (NASDAQ:MAIN) could be one of the best.

MAIN has provided capital to more than 200 private companies and thanks to its underwriting and deal standards, it has been very successful at turning a big profit on those loans. Just for the first quarter of this year, MAIN has already seen its investment income rise by 10% year-over-year. Those sorts of gains have allowed the firm to become a great dividend stock since its IPO in 2007. The BDC has managed to grow its payout by 127% since then.

Today, you can score a great recurring monthly dividend with a current yield of 5.89%. The best part is that MAIN’s management likes to reward shareholders further with extra supplemental dividends. This allows the BDC to use excess capital if a great deal can be had or for dividends. Adding those extra payouts in, and investors are looking at closer to 7.2% yield.

BDCs like MAIN provide a much-needed service to many firms. And thanks to its underwriting skill and focus on quality firms, MAIN has quickly become one heck of a dividend stock.

Shaw Communications (SJR)

Dividend Yield: 4.5%

One sector that can be a fertile hunting ground for dividend stocks, and is also known for its stability, is the telecommunications industry. Top stocks like AT&T (NYSE:T) and Verizon (NYSE:VZ) are in plenty of income portfolios. The reason is easy to see. Predictable fixed costs and demand allow telcos to pay out reliably healthy dividends. The problem is T and VZ aren’t monthly dividend stocks.

But Canada’s Shaw Communications (NYSE:SJR) is.

Shaw remains one of Canada’s largest telecoms and offers the usual bundle of services, including cable, internet and wireless phone services. It has been doing this for decades just like T and VZ here at home. And SJR has also tackled the problem of cord cutting head on. The telecom has been able to successfully convert customers to faster internet service to overcome lower cable subscriptions. This has helped boost revenues. At the same time, SJR has been one of the first movers in Canada for new 5G networks. That will give it a heads-up in bringing faster mobile internet, IoT and other applications to the nation.

As Shaw moves forward in these areas, investors can sit back and collect a hefty monthly yield. Currently, SJR pays 4.5%. Now, that dividend will fluctuate based on changes to the U.S./Canadian dollar. However, given Shaw’s stability and potential growth, it’s a small price to pay for a great dividend stock.

LTC Properties (LTC)

Dividend Yield: 4.89%

Honing in on so-called mega-trends is a great way to find dividend stocks that will stand the test of time. For monthly-dividend payer LTC Properties (NYSE:LTC) that mega-trend is the “Graying of America.”

Thanks to advances in medicine, lifespans are only increasing and longevity is almost assured at this point. LTC is uniquely positioned to take advantage of this fact. The firm invests in the senior housing and assisted living facility sectors of the healthcare property market. Currently, the firm owns/invests in roughly 200 properties that are right in the sweet spot for the nation’s aging baby boomers. Demand for these facilities continues to grow as more seniors need aid to get along.

The key is that LTC doesn’t operate the facilities or even own the buildings in many cases. What it does is provide financing for owner/operators to construct and renovate their properties or it buys properties from owners in a sale-leaseback transaction. It’s basically a mortgage lender that collects a monthly rent check. This position in the sector allows it to avoid some of the profitability issues that can result in senior living and assisted living facilities.

It also allows for some safety and steady profits on its end. Year-over-year, LTC saw a gain in FFO for the first quarter of 2019. Steady FFO gains have allowed it to raise its dividend over 46% since 2008. Currently, LTC yields 4.89%.

All in all, LTC is in the right area at the right time. And that makes it a great monthly dividend stock to own.

<<<

>>> CareTrust REIT, Inc. is a self-administered, publicly-traded real estate investment trust engaged in the ownership, acquisition and leasing of seniors housing and healthcare-related properties. With 212 net-leased healthcare properties and three operated seniors housing properties in 28 states, CareTrust is pursuing opportunities across the nation to acquire properties that will be leased to a diverse group of local, regional and national seniors housing operators, healthcare services providers, and other healthcare-related businesses.

<<<

>>> More trouble for malls: A new wave of closures from Gap, Victoria's Secret and others

11-30-18

CNBC

https://www.msn.com/en-us/money/topstocks/more-trouble-for-malls-a-new-wave-of-closures-from-gap-victorias-secret-and-others/ar-BBQgr3j?li=BBnb7Kz&ocid=mailsignout

Mall and shopping center owners across the U.S. are preparing to be hit by more store closures, following a brutal year that included department store chains like Bon-Ton and Sears going bankrupt, Toys R Us liquidating and even Walmart shutting dozens of its club stores.

Now, a slew of specialty retailers like Gap and L Brands are getting serious about downsizing, which will leave more vacant storefronts within malls until landlords are able to replace tenants.

And if retailers are not shutting stores, the focus is on negotiating with landlords over how to cut rent and other expenses. Real estate analysts say it's the retailers, not the mall and shopping center owners, that still have the upper hand in most negotiations today.

"Our early read on 2019 is more of the same ... with both malls and [shopping centers] facing another year of tepid earnings growth and store closure-related headwinds," Mizuho analyst Haendel St. Juste said.

Related video: Malls compete for shoppers from e-commerce ahead of holidays

The CEO of clothing retailer Express, David Kornberg, told analysts Thursday morning the company is "benefiting from reduced occupancy costs, which are expected to continue based on recent lease negotiations."

Express has 60 percent of its leases up for renewal over the next three years, and will be in a position to argue for slashed rents because of that, he said. Express currently has more than 600 stores, including outlets, across the U.S. and Puerto Rico.

The comments come after Gap earlier this month warned it could shut hundreds of stores for its namesake brand "quickly" and "aggressively."

"There are hundreds of other stores that likely don't fit our vision for the future of Gap brand specialty store, whether in terms of profitability, customer experience, traffic trends," CEO Art Peck said.

Then, L Brands CFO Stuart Burgdoerfer told analysts earlier in November the company is going to "take a hard look" at its real estate "over the next several months." He said L Brands hasn't had much flexibility to shut stores of late, without incurring a penalty, as leases in the U.S. typically last for 10 years, and can be 15 years in the U.K. But he hinted the company hopes to take a more aggressive stance, moving forward.

"We're doing some more purposed testing for Victoria's [Secret] around closing some stores that may not be as obvious financially, but really observing the sales transfer effects," Burgdoerfer said. Victoria's Secret has been viewed as dragging down Bath & Body Works, which is also owned by L Brands and is seeing improved sales trends for its lotions and candles as its stores are being remodeled.

Bucking the trend, Abercrombie & Fitch said Thursday morning it plans to close fewer stores this year than it previously anticipated, based on a regained momentum of its apparel business. It's now planning to shut just 40 locations in malls, compared with a prior target of 60. But it also still has 60 percent of its leases expiring by 2020, giving the company more flexibility in the coming months to ink better deals with property owners. Abercrombie currently has more than 850 stores globally, including those under the Hollister banner.

"I would say, we retain a lot of flexibility with our leases ... based on lease expiration," CEO Fran Horowitz told CNBC. "We work with our landlords. We negotiate with them."

All things considered, U.S. mall owners like Simon, Macerich, Taubman, Seritage, Brookfield and Unibail-Rodamco-Westfield must look for new ways to fill these gaps, as there aren't many retailers today opening new stores at the same size and scale as before the Great Recession.

Some are turning to co-working spaces, apartment complexes and health facilities to replace department stores. Others are building spaces that house multiple e-commerce brands on a rotating basis. There's a wave of digital brands like Casper, Warby Parker and Untuckit opening bricks-and-mortar locations.

"We continue to believe that we're still in the earlier stages of the reshaping of the retail landscape and facing a challenging backdrop marked by defensive landlords/weak pricing power, more anticipated store closures, and selective capital," St. Juste said.

<<<

>>> Mortgages fast approaching 5 percent, a fresh blow to housing market

Wall St Journal

10-11-18

https://www.msn.com/en-us/money/realestate/mortgages-fast-approaching-5-percent-a-fresh-blow-to-housing-market/ar-BBOeBHg

Mortgage rates hit their highest level in more than seven years this week at nearly 5%, a level that could deter many home buyers and represents another setback for the slumping housing market.

The average rate for a 30-year fixed-rate mortgage rose to 4.9%—the largest weekly jump in about two years—according to data released Thursday by mortgage-finance giant Freddie Mac.

Lenders and real-estate agents say that, even now, all but the most qualified buyers making large down payments face borrowing rates of 5%.

Rates have been edging higher in recent months, but during “the last week we’ve seen an explosion higher in mortgage rates,” said Rodney Anderson, a mortgage lender in the Dallas area.

A 5% mortgage rate isn’t that high by historic standards. During much of the decade before the financial crisis, these rates hovered between 5% and 7%. But a return to more normal lending rates won’t feel normal to many buyers who have become accustomed to getting a mortgage loan at 4% or lower, and they could experience sticker shock at what they would have to pay now for a home loan.

“There’s almost a generation that has been used to seeing 3% or 4% rates that’s now seeing 5% rates,” said Vishal Garg, founder and chief executive of Better Mortgage.

For a house with a $250,000 mortgage, rates of 5% add about $150 to the monthly payments compared with the rate of 4% that borrowers could have had less than a year ago, according to LendingTree Inc., an online loan information site. That excludes taxes and insurance.

With rates hitting recent highs at a time when housing prices have been going up, too, some economists suggest sellers may need to lower prices if borrowers can’t afford high prices in a higher rate environment.

Higher mortgage rates have also slowed the housing market more than many expected. That’s a potentially troubling sign for the broader economy, since housing is often a bellwether for how rising interest rates could affect growth overall.

Many buyers who are struggling to find a home they can afford because of high prices are more sensitive to rising rates than they have been in the past.

Existing home sales fell in August from a year earlier, the sixth straight month of declines. Many would-be buyers sat out the buying season because of high housing prices, a historic shortage of homes to buy, and a tax bill that reduced some incentives for homeownership. Higher mortgage rates will likely compound their hesitation.

“With the escalation of prices, it could be that borrowers are running out of breath,” said Sam Khater, chief economist at Freddie Mac.

Once-hot markets are showing signs of cooling down. Bill Nelson, president of Your Home Free, a Dallas-based real-estate brokerage, said that in the neighborhoods where he works, the number of homes experiencing price cuts is more than double the number that are going into contract.

Brad and Virginia Reitinger closed on a new home in Dallas two weeks ago, and opted for an adjustable-rate mortgage so they could get a 4% rate. With a fixed-rate 30-year loan, they would have had to pay 4.5% to 5%, Mr. Reitinger said.

He added that the prospect of rates going even higher motivated them to move quickly on buying the new home. And if they had opted for a fixed-rate mortgage, he estimates, their monthly payment would have been higher by a couple hundred dollars. “When you run the numbers, it makes a big difference,” he said.

Adjustable-rate mortgages, which reset to market rates after a certain number of years, typically offer lower rates than fixed-rate mortgages at the beginning of their term. Some lenders say they have seen a surge of customer inquiries into the product as rates rise. They remain a relatively small part of the mortgage market, though: They made up about 12% of mortgage originations in the second quarter, according to industry research group Inside Mortgage Finance.

The rise in rates could have far-reaching effects for the mortgage industry. Some lenders—particularly nonbanks that don’t have other lines of business —could take on riskier customers to keep up their level of loan volume, or be forced to sell themselves. Many U.S. mortgage lenders, including some of the biggest players, didn’t exist a decade ago and only know a low-rate environment.

Long-term mortgage rates now have climbed nearly a full percentage point from 3.95% at the beginning of this year. House hunters who started searching months ago are acutely aware of the rise in rates.

“We have some people who prepared themselves early, and bless their heart for doing it—that’s what I’ve been preaching,” said Rick Bechtel, head of U.S. mortgage banking at TD Bank. “And they’re the ones who are most pained.”

A spate of recent positive economic news helped drive the 10-year Treasury note, to which mortgage rates are closely tied, to a seven-year high last week. The Federal Reserve, which has raised its key policy rate three times this year, is expected to do so again in December.

And higher rates will likely kill off any lingering possibility of a refinancing boom, which bailed out the mortgage industry in the years right after the 2008 financial crisis. If rates hit 5%, the pool of homeowners who would qualify for and benefit from a refinance will shrink to 1.55 million, according to mortgage-data and technology firm Black Knight Inc. That would be down about 64% since the start of the year, and the smallest pool since 2008.

Higher rates will be hardest on first-time buyers, who tend to make smaller down payments than older buyers who have built up equity in their previous homes, and middle-income buyers, who can least afford the extra cost. Mr. Khater said that about 45% of the loans that Freddie Mac is backing are to first-time buyers, up from about 30% normally, which also means that rising rates could have an even bigger impact on the market than usual.

“Affordability has already been an issue for consumers across the country,” said Sanjiv Das, CEO of Caliber Home Loans Inc., one of the biggest mortgage lenders in the country. “Now it becomes an even bigger issue.”

>>>

>>> Why Realty Income Corp. (O) is a Great Dividend Stock Right Now

Zacks Equity Research

October 5, 2018

https://finance.yahoo.com/news/why-realty-income-corp-o-131501911.html

Why Realty Income Corp. (O) is a Great Dividend Stock Right Now

Dividends are one of the best benefits to being a shareholder, but finding a great dividend stock is no easy task. Does Realty Income Corp. (O) have what it takes? Let's find out.

Getting big returns from financial portfolios, whether through stocks, bonds, ETFs, other securities, or a combination of all, is an investor's dream. But when you're an income investor, your primary focus is generating consistent cash flow from each of your liquid investments.

Cash flow can come from bond interest, interest from other types of investments, and of course, dividends. A dividend is the distribution of a company's earnings paid out to shareholders; it's often viewed by its dividend yield, a metric that measures a dividend as a percent of the current stock price. Many academic studies show that dividends make up large portions of long-term returns, and in many cases, dividend contributions surpass one-third of total returns.

Realty Income Corp. In Focus

Realty Income Corp. (O) is headquartered in San Diego, and is in the Finance sector. The stock has seen a price change of -0.84% since the start of the year. The real estate investment trust is paying out a dividend of $0.66 per share at the moment, with a dividend yield of 4.68% compared to the REIT and Equity Trust - Retail industry's yield of 5.07% and the S&P 500's yield of 1.81%.

Taking a look at the company's dividend growth, its current annualized dividend of $2.65 is up 4.5% from last year. Over the last 5 years, Realty Income Corp. has increased its dividend 5 times on a year-over-year basis for an average annual increase of 4.70%. Future dividend growth will depend on earnings growth as well as payout ratio, which is the proportion of a company's annual earnings per share that it pays out as a dividend. Realty Income Corp.'s current payout ratio is 85%, meaning it paid out 85% of its trailing 12-month EPS as dividend.

Looking at this fiscal year, O expects solid earnings growth. The Zacks Consensus Estimate for 2018 is $3.18 per share, with earnings expected to increase 3.92% from the year ago period.

Bottom Line

Investors like dividends for many reasons; they greatly improve stock investing profits, decrease overall portfolio risk, and carry tax advantages, among others. However, not all companies offer a quarterly payout.

Big, established firms that have more secure profits are often seen as the best dividend options, but it's fairly uncommon to see high-growth businesses or tech start-ups offer their stockholders a dividend. Income investors have to be mindful of the fact that high-yielding stocks tend to struggle during periods of rising interest rates. With that in mind, O presents a compelling investment opportunity; it's not only an attractive dividend play, but the stock also boasts a strong Zacks Rank of #2 (Buy).

<<<

>>> Equinix, Inc. (Nasdaq: EQIX) connects the world's leading businesses to their customers, employees and partners inside the most-interconnected data centers. In 52 markets across five continents, Equinix is where companies come together to realize new opportunities and accelerate their business, IT and cloud strategies. <<<

https://finance.yahoo.com/quote/EQIX/profile?p=EQIX

Equinix EQIX, -0.62% runs data centers in the U.S., Japan and Europe, providing cloud services to more than 9,800 companies.

>>> Is the REIT bloodbath finally a buying opportunity?

By Andrea Riquier

Apr 2, 2018

Malls are a ‘distressed’ play for some investors, while jumping on the housing shortage attracts others

Buying opportunity or value trap?

https://www.marketwatch.com/story/is-the-reit-bloodbath-finally-a-buying-opportunity-2018-03-28?siteid=bigcharts&dist=bigcharts

In December MarketWatch took a balanced view on investing in real estate investment trusts. REITs may be “cheap enough to warrant another look,” we wrote then.

The pro-REIT camp liked the macro fundamentals underpinning the investment — not to mention their cheap relative valuations — believing that those factors outweighed concerns about rising interest rates, investor disinterest and the Amazon AMZN, +1.33% effect that’s been clearing out the traditional shopping malls that anchor many of these funds.

Since then REITs have gotten even cheaper, and are now luring some analysts who’d shied away before.

The Vanguard Real Estate ETF VNQ, +1.05% is down about 9% for the year to date, worse than the 2% decline for the S&P 500 SPX, +1.16% . Shares of the PowerShares KBW Premium Yield ETF, meanwhile, have lost more than 12% so far in 2018.

REITs have been beaten down enough that Rick Daskin, an investor who in December told MarketWatch he was staying away, is now interested. Back then, Daskin, who serves as president of RSD Advisors, and subadvises Cumberland Advisors on MLP strategy, thought interest-rate risk was just too strong to make REITs, which depend on borrowing, attractive.

Now, he said, “relative to bonds and other things it looks to me like they present some opportunity. Retail REITs have gotten absolutely destroyed, and some are at a level where they’re near-distressed. And they may be superior to bonds because you’re scraping up more yield. The risk-reward might be coming more into focus.”

Within the retail sector, Daskin said, he’d concentrate on class “A” malls, those with higher foot traffic than lower-rated properties and with strong tenants.

“I don’t think you want to play at the bottom of the barrel,” he said.

A mall REIT that fits that description and is popular among analysts surveyed by FactSet is Simon Property Group, Inc. SPG, +1.33% , which has a mean overweight rating and a price target about 19% higher than current trading levels.

Another area he’d consider is health care, which is less sensitive to the economic cycle.

But as with so many considerations surrounding REITs, the specific details seem to trump the logic of the fundamentals.

Sabra Health Care REIT, Inc. SBRA, +2.23% , down about 7.5% for the year to date, has an overweight rating among FactSet analysts and a target price of $20.60, nearly 20% higher than current trading levels. Sabra has strong geographic diversification across the U.S., and properties in senior living, skilled nursing and specialty hospitals. It also boasts a dividend yield of 10.3%.