News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Gold & Silver Index - Philadelphia ($XAU)xau-xau:gold wkly - bull waves will be plenty to come -

Gold & Silver Index - Philadelphia ($XAU)xau-gold wkly - its a long hike back UP - Gold bull just started new run UP -

ME - Au 10mil. oz + + + + best location on earth -

http://www.monetaporcupine.com/s/Projects.asp

ME traded more than 100 year on TSE -

one of the oldest longest traded company on TSE -

lots of great hidden Au hard asset values and

old mining properties in ME - MPUCF -  )

)

http://www.monetaporcupine.com/i/maps/Regional_Geo_20121024_Rev1.pdf

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=123346496

Potentially Sending Gold Prices Haywire -

To as much as $14,454 per Ounce (Or More) -

call it “G-Day.”

http://research.agorafinancial.com/research/html/rgs_pennygold_0516/?code=ERGSS638&n=RGS_pennygold_0516&email=rbalc%40yahoo.com&a=13&o=38810&s=42543&u=1630580&l=218984&r=MC2&vid=FQl-8u&g=0&ver=8

http://www.kitconet.com/images/live/au0001wb.gif

Gold & Silver is the only REAL Legal Tender -

by The Founding Fathers for your -

Rights, Liberty and Freedom -

http://www.biblebelievers.org.au/monie.htm

- God Bless -

Watch for the Production release for Primero Mining. Badly beaten down by the last Q and the Tax Questions in Mexico. Nafta appeal and huge production improvements at both mines JMHO PPP will jump.

CQR / CQRLF - for the Gold mining -

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=123055673

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=123000795

- God Bless -

Here’s Why I Just Launched A $1,000,000 “Secret” Gold Project -

ex....

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=122291502

https://www.youtube.com/watch?v=N9pK9wBxgag&feature=youtu.be

Why Donald Trump’s Popularity Might Be Boosting Gold Prices -

Hold on to the hats - Gold’s Current Market a 1970’s Deja vu Times 10 | -

McAlvany Commentary 2016 -

) ) -

RBYCF (Rubicon) clear breakout today.

Nevada Exploration

A Canadian explorer. American symbol is NVDEF

Hold on to the hats - CALVF Au - we going to FLY *~(()

http://www.plata.com.mx/mplata/articulos/articlesFilt.asp?fiidarticulo=281

http://www.caledoniamining.com

- God Bless -

Here is some of the old ruins and protected -

ex...

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=67548765

CALVF sold 51% of Blanket Mine for $30 million and is still

collecting 10% interest on the debt which still is 30 mil. -

CALVF manage the production and still own 49% + ( in praxis

the 51% to the debt of $30 mil is payed off -

- God Bless -

Montanore thank you, its stable - low taxes -

low cost - happy workers who got 10% of the mine -

they living in good housing - good community which

also got 10% of the mine and CALVF is one very low cost

producer of gold @ about $600/oz and has NO DEBT -

last I heard they had >$20million in London bank -

paying about 6-8% in dividend -

http://www.caledoniamining.com/index.php/dividends

1100 workers and the mine goes 24hrs/day -

sorry - I have not found a better producer -

to redevelop the mine would cost a few billion -

the mill cap. is about 3800ton/day and they

only mine about 1000t/day so don't need to pay out

much to expand it - they have 19 old mines

Falconbridge used to mine and they only mine

the main mine but 3 mines within short trucking distance

are under re-commission etc.

they found about 268 old mines hand-dug since 1000yrs back -

historic ruins of ex.

Q-Sheba capital close by -

its not hard to to do dd on CALVF -

many videos often a few / month etc.

http://www.caledoniamining.com -

http://investorshub.advfn.com/Caledonia-Mining-Corporation-CALVF-5294/

God Bless -

I used to know a lot more about CALVF years ago and I've forgotten he details. Mostly I shied away because it was in an unstable part of Africa--Zimbabwe. Maybe I was wrong, but why not look for producers in a more stable region?

Caledonia Mining Corporation (CALVF) - The Coming Revaluation of Gold -

E.g. -

http://www.plata.com.mx/mplata/articulos/articlesFilt.asp?fiidarticulo=281

http://investorshub.advfn.com/Caledonia-Mining-Corporation-CALVF-5294/

Gold & Silver is the only REAL Legal Tender -

by The Founding Fathers for your -

Rights, Liberty and Freedom -

http://www.biblebelievers.org.au/monie.htm

God Bless

Found this board after posting on the ITEC board for a while now. Take a look at ITEC - they are in the financing and gold mining production/engineering assistance business getting started with their first project any day now with West Port Energy in Arizona and a second mine Hunter Creek in Alaska. You can be sure they have other opportunities up their sleeves as well. I cannot see how they can lose, baring not getting fully permitted which they are on the verge of doing, or there not being the gold they expect in the ground, which test show there certainly is. The stock is trading at 5 cents a share, with a market cap of 4.6 million - that's not a typo. Imagine what this is going to look like a year from now.

carl thanks, Caledonia Mining IG Interview Television Interview -

just added to the website -

https://www.youtube.com/embed/Jo-0DMYj_FE

http://www.caledoniamining.com/

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=113031300

God Bless

Montanore thank you HL excellent - UK To Join China-led World Bank To Protect Itself From The Collapsing Dollar - Episode 615 -

South Africa Gross $Gold & Forex Reserve dipped from previous $49.1B to $47.611B in January -

Fri, Feb 06 2015, 06:00 GMT | FXStreet

http://www.fxstreet.com/news/forex-news/article.aspx?storyid=35f30ad0-6d50-41a3-bc05-9fa4baf4d8f4

Another 71 tonnes of gold withdrawn from China’s SGE in week 3 Withdrawals

from the SGE for the first 3 weeks of the year have totalled 202 tonnes –

comfortably more than world new mined gold supply for the period.

Lawrence Williams | 1 February 2015 20:58

http://www.mineweb.com/news/gold/another-71-tonnes-gold-withdrawn-chinas-sge-week-3/

gold bars and granules

Despite some talk that India may have re-overtaken China as the World’s

largest gold consumer, gold withdrawals out of the Shanghai Gold Exchange

(SGE) continue to contradict this enormously.

The Chinese themselves have stated that SGE withdrawals – all physical gold

which, under SGE rules, cannot be returned to the Exchange for resale –

are totally representative of Chinese gold demand.

So the SGE figures, which are published weekly, in our view remain as

the most readily available measure of true Chinese gold demand.

As SGE figures nowadays include withdrawals from the Exchange’s

international section, the SGEI, (which are not necessarily landed in

China at all) the actual Chinese mainland demand figure may be a little

lower than the overall total may suggest, but the SGEI withdrawals are

believed to be a very small maximum of up to 5 tonnes, probably less),

so the latest overall SGE withdrawals, which are running at a huge level,

indicate massive internal demand running up to this year’s Chinese New

Year, which is still nearly 3 weeks away (on February 19th).

The latest total withdrawals figure from the SGE, for the week ending

January 23rd, was a huge 70.62 tonnes – even larger than the previous

week’s 70.00 tonnes which was until now the third highest weekly figure

ever.

This means that withdrawals from the Exchange for the first 3 weeks of the

year have come to over 200 tonnes – and with total global new mined gold

production running at around 60 tonnes a week according to the latest

GFMS estimates, this shows that the SGE on its own is accounting for

comfortably more than this so far this year.

GFMS has also seen a fall in global scrap supplies –

the other main contributor to the total world gold supply – which

it sees as continuing through 2015 so the Chinese SGE withdrawal figures

so far are, on their own, accounting for around 85% of ALL new gold

available to the market.

So where’s the rest of the world’s (including India) gold supply coming

from?

January is usually a particularly strong month for Chinese gold demand

in the period immediately prior to the Chinese New Year holiday which

is accompanied by gift giving in which gold ornaments and

jewellery play an important part.

But what is particularly significant about this year’s apparent demand is

that it has occurred within a rising gold price scenario.

That demand remains particularly strong is also shown by the fact that

Shanghai gold premiums have stayed positive throughout according to

reports, while gold-buying business at Chinese shopping malls has seen

some ‘stampede’ situations arising according to the Chinese press.

Historic Revolt Against Corrupt Western Banksters Now Underway - ? -

February 02, 2015

http://kingworldnews.com/historic-revolt-corrupt-western-banksters-now-underway/

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=110493459

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=110491528

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=110512815

The Only Legal Tender is Gold and Silver the rest is fiat 666 poncy schemes -

http://www.biblebelievers.org.au/monie.htm

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=110491528

imo. -

God Bless

GOLD Repricing by CHINA -

Sutter Gold Mining Inc. (SGM) -

http://web.tmxmoney.com/article.php?newsid=68818795&qm_symbol=SGM

God Bless

SKIPPACK, PA., August 18, 2014 – North Bay Resources Inc. (OTCQB: NBRI) (“North Bay” or the “Company”) is pleased to issue the follow progress report on our exploration efforts at the Ruby Mine in Sierra County, California, where mining is set to begin in the Black Channel this week.

Underground work at the Ruby Mine is presently focused on four concurrent headings. These include continued mining in the White Channel, driving the South Terrace Raise to the recently discovered terrace gravels, reinforcing and securing the entryway to the recently-constructed Big Bend Bypass Raise to the old workings upstream of the Big Bend, and the start of mining as well as continued exploration in the old workings downstream of the Big Bend in the southern extent of the Black Channel.

Mining in the Black Channel will begin this week, and will be initiated by driving a crosscut through pillars near the China Chute. The crosscut will allow easier access to the old workings, and will cut through some of the richest channel gravels downstream of the Big Bend. The crosscut will start at the top of the China Chute and run upstream for approximately 60 to 100 feet, cutting through 2 or 3 pillars. It is anticipated that the crosscut will produce significant gold. This area of the channel was extensively mined by previous operators, but large pillars up to 40 feet thick were left between old workings.

Also within the Black Channel, an ongoing exploration effort to locate additional mining targets has been underway within the old workings. Compressed air pipe and water lines have been extended and installed that allow for a portable sluice box to be moved from place to place. The miners locate prospective areas by metal detector or clues gained from experience and excavate the rock by pick or, at times, blasting. Gold recovered from specific locations is photographed and cataloged for the purpose of identifying the number of types and sources of gold.

The Company also reports that new gravels have been successfully intersected above the Black Channel as a result of a drill program that began two weeks ago and which is yielding positive results. This effort consists of long hole drilling with a standard air leg drill. These short holes, generally up to the 30 to 34 foot limit of the drill, are exploring for terrace gravels on the south rim of the Black Channel. At the Big Bend, terrace gravels were present 15 to 25 feet above the outer or south rim of the channel. We are attempting to locate the continuation of these terraces downstream, between the Big Bend and the China Chute. Six holes have been drilled to date, three of which successfully penetrated gravels. The elevation of the gravels indicates they are high gravels within the main Black Channel, not terrace gravels. The drilling will continue concurrent with the crosscut mining underway this week

Mr. C. Gary Clifton, P.Geo., is the Company’s independent consulting geologist for the Ruby Gold Project. Mr. Clifton is a Qualified Person as defined by National Instrument 43-101, and has reviewed this press release for technical accuracy.

About The Ruby Gold Project

The Ruby Mine, a/k/a the Ruby Gold Project, is a fully-permitted underground placer and lode mine located near Downieville in Sierra County, California that is known to have produced over 350,000 ounces of gold since the 1850’s, and which is considered to be part of the northern extension of the historic Mother Lode system. The Ruby Property covers approximately 2,312 contiguous acres, only a small portion of which has been explored to date. The property consists of the subsurface mineral rights of two patented claims totaling approximately 435 acres and 59 unpatented claims containing approximately 1,877 acres. The equipment, fixed assets, and infrastructure in place include a 1,000 yard per day placer wash plant, 50-ton per day quartz mill, 6,000 feet of tracked haulage, and related support equipment needed for underground mining operations. The property also features an excellent system of roads, is accessible via paved highway from Reno or Sacramento, has abundant water and timber available for mining purposes, and has PG&E power available on-site. For further information on the Ruby Mine, ple

Sutter Gold Announces New Major Shareholder and Restructures Debt

Vancouver, British Columbia (July 4, 2014) -

Sutter Gold Mining Inc.

(SGM:TSX-V) (SGMNF:OTCQX) ("Sutter" or the "Company") is pleased

to report that Sutter and

Tyhee Gold Corp.

(TSXV:TDC) have entered into an agreement

(the "Implementation Agreement") with RMB Australia Holdings

Limited ("RMB") whereby, subject to certain conditions,

Tyhee will acquire:

all of the issued and outstanding shares of Sutter currently

held by RMB and/or its affiliates;

all of the issued and outstanding shares of Sutter that are

to be issued to RMB by Sutter upon the proposed conversion of

US$8 million of RMB's current debt exposure to Sutter; and

approximately US$17 million of RMB's additional debt exposure to

Sutter (the "Transaction").

Upon completion of the Transaction, Tyhee will hold

approximately 73% of Sutter's issued and

outstanding shares (on a non-fully diluted basis).

Sutter Gold

Sutter currently holds a number of precious metals properties in California, USA, including the permitted Lincoln underground mine near Sutter Creek, California, as well as a new, permitted processing facility, located near the entrance to the Lincoln Mine. In March 2014, the project was put on care and maintenance while certain production issues are being evaluated and the Company reduced costs due to capital constraints.

Sutter's assets cover 3.2 miles of what has been described as "the most productive portion" of California's famed, 120 mile long Mother Lode District. Sutter has established a National Instrument 43-101 compliant gold resource that reflects only a small area of the gold mineralization identified to date.

RMB

RMB Australia Holds Limited is a wholly-owned subsidiary of FirstRand Limited, a South African-based financial services group. RMB currently holds approximately US$40 million in debt from Sutter as well as approximately 58.2 million (47%) of Sutter's approximately 123 million outstanding shares.

The Agreement

The Implementation Agreement, which will be filed under Sutter's profile on SEDAR, follows one year of extensive due diligence by Tyhee's management and technical team, including comprehensive discussions, site inspections and a review of Sutter's financial situation.

Upon consideration of Sutter's current financial difficulty and the determination that the Transaction will be financially beneficial to Sutter's operations, the board of directors of Sutter, upon recommendation of a special committee of independent directors, has approved the Transaction.

The Transaction would benefit both Tyhee and Sutter shareholders. In particular, benefits include:

For Sutter, improved financial standing, with significantly improved liquidity and access to capital to properly capitalize completion of development of the Lincoln mine and mill to achieve commercial production. For Tyhee, enabling the execution of its strategy of building its production profile through additional acquisitions with near-term production potential;

For Tyhee and Sutter, being transformed into a developing precious metals production company with gold production planned from Lincoln;

or Tyhee and Sutter, significantly enhanced development and exploration upside across a diverse portfolio of precious metals properties, including the Keystone deposit in California as well as the large undeveloped gold resources (Feasibility Study -- August 2012) at the Yellowknife Gold Project, NWT;

For Tyhee and Sutter, utilizing Tyhee's highly experienced underground mining team that will be key to successful operations at Lincoln; and

For Sutter, access to an expanded management team that includes complementary experience in exploration, development, operations, and financing.

The Transaction

Tyhee proposes to acquire certain of RMB's current interests in Sutter pursuant to the Implementation Agreement as follows:

Tyhee will acquire the current stock position of RMB and/or its affiliates in Sutter (58,216,820 common shares) at C$0.02 per share, paid in cash on closing of the Transaction;

RMB will reduce its debt exposure to Sutter by US$8 million, from no more than US$40 million to no more than US$32 million by converting the US$8 million into 108,454,603 Sutter common shares at a deemed price of $0.0788 per share. Tyhee will then acquire such shares at C$0.02 per share, paid in cash on closing of the Transaction; and,

RMB will assign to Tyhee up to US$17 million of RMB's debt exposure, with RMB continuing to retain a US$15 million loan to Sutter, in consideration for the following:

90 million Tyhee common shares issued from treasury;

US$4 million in cash;

a covenant by Tyhee to consummate an additional financing to raise the remaining balance necessary to achieve commercial production of Sutter' s Lincoln-Comet mine, to a maximum of US$17 million; and

a covenant by Tyhee to cause Sutter to make interest payments, principal repayments, and mandatory prepayments on the retained US$15 million loan from RMB to Sutter on a first ranking basis.

The Transaction does not require a shareholder approval of either Tyhee or Sutter.

Closing of the Transaction is subject to customary closing conditions, including receipt of the approval of the TSX Venture Exchange and any other regulatory approvals. In addition, the closing of the Transaction is subject to the completion of certain debt restructurings by Sutter, noted below, and the completion of a minimum of US$15 million financing by Tyhee, also discussed below.

The Implementation Agreement contains a non-solicitation covenant on the part of RMB and Sutter, subject to customary fiduciary out provisions. The Implementation Agreement also provides Tyhee with the right to match any potential third party proposal. Sutter is permitted to terminate the Implementation Agreement under certain conditions, including the payment of a $1.5 million break fee to Tyhee. In addition, Tyhee has agreed to pay a $750,000 fee to RMB, if the concurrent financing is not completed on or before August 15, 2014.

Concurrent Financing

In connection with the Transaction, Tyhee intends to complete, through a previously announced (see Tyhee release dated November 26, 2013) special purpose vehicle (the "SPV"), a concurrent financing of a minimum of US$15 million. The SPV would provide a loan or loans to Tyhee or its wholly owned US subsidiary (the "SPV Loan"). The SPV would issue convertible debentures having the following terms:

Face value: US$1,000 denominations.

Term: Five (5) years.

Interest Rate: Eight (8) percent per annum, payable annually in cash or in ounces of gold, at the election of the holder of the convertible debenture.

Security: Secured against the assets of Tyhee NWT Inc., Tyhee's wholly owned Northwest Territories subsidiary.

Conversion: Principal to be convertible to Tyhee common shares at $0.30 per Tyhee common share.

Redemption: Principal amount to be redeemable by Tyhee after 24 months, subject to payment of premium.

In addition, if at any time after 24 months from the issuance of the convertible debentures gold trades at greater than US$2,000 per ounce for a period of 30 consecutive business days or more, the holder would have the option, subject to additional conditions to be determined, to convert the principal amount outstanding on the SPV Loan to gold, at the rate of one ounce for each US$2,000 outstanding (delivery terms and timing of repayment remain to be determined), or payment in cash of an amount equal to the principal owing.

Terms of Loans to Sutter

US$15 million loan from RMB to Sutter - RMB will retain a secured US$15 million amortizing loan to Sutter. RMB and Sutter would amend and restate the terms of its existing US$40 million debt facility to provide for the following terms:

US$15 million principal amount;

interest at 12% per annum, capitalising until July 31, 2015 and paid monthly commencing on August 31, 2015;

repayment in up to 48 consecutive monthly installments of equal amounts, subject to certain conditions and adjustments, commencing on August 31, 2015; and

such loan would be senior secured debt to Sutter and any other Sutter debt would be fully subordinated on terms satisfactory to RMB.

Approximately US$17 million note payable by Sutter to Tyhee - RMB will assign to Tyhee US$17 of existing indebtedness owing under the promissory note dated December 31, 2013 issued by Sutter to RMB and Tyhee and Sutter will enter into a new promissory note on terms similar to RMB.

Funds to Restart Production - Further advances ("Tyhee Advances") to Sutter by Tyhee or its related entities would be made up to US$17 million on the same terms as the SPV Loan that would be provided to Tyhee, except that (i) interest on Tyhee Advances would accrue at 12% per annum; and (ii) security for the Tyhee Advances will be equal ranking to the Tyhee note described above.

Denis Taschuk, Tyhee's Chairman of the Board, said, "Given the many challenges facing the junior resource sector, we are particularly pleased with both the potential we see with this agreement and the support for our company's capabilities from both RMB and Sutter's Board. This has taken a great deal of work to get us to this point and we are confident that this represents a tremendous opportunity to generate significant value for all of the stakeholders involved."

Mark T. Brown, Sutter's Chairman of the Board, said, "Despite the issues we have had with an orderly development and the difficulties of raising funding given Sutter's financial position, we have always had confidence in the Lincoln project. Our number one priority over the last many months has been to secure the additional investment needed to achieve commercial production. We are supportive of RMB and Tyhee's transaction, which will provide both the funding and technical/operational expertise to make Lincoln a success, aligning all parties' interests. We look forward to working with Tyhee to meet our common objectives."

Tyhee CEO, Brian Briggs stated, "The blending of Tyhee's operational talent and the remaining management at Sutter will provide an excellent team capable of executing our comprehensive turn-around plan and to bringing the Lincoln Mine into production in the coming months. In addition to the near term potential of Sutter's assets, we see the opportunity to build the next, long term gold producer in one of the richest trends in America."

About Sutter

Sutter has two projects: the Lincoln Project located in Amador County, on the California Mother Lode Gold Belt, and the Santa Theresa Project located in the Northern Baja region of Mexico. Currently, the Company is completing the mill construction and underground development of the Lincoln Mine Project, beginning with the shallow portion of the Lincoln-Comet ore zone. The Lincoln-Comet and Keystone zones have a NI 43-101 compliant Indicated Resource estimate (completed in February 2008). Sutter currently controls approximately 3.6 miles of the Mother Lode of Amador County, with 90% of the property still unexplored.

In Mexico, Sutter holds the rights to the geologically similar, high-grade El Alamo district of northern Baja.

For further information, please contact:

Amanda Miller,

Chief Financial Officer

T:303 238 1438 ext. 223

amiller@suttergoldmining.com

http://www.suttergoldmining.com

Greg Taylor

GT Investor Relations Inc.

O: 905 337-7673 C: 416 605-5120

gtaylor@tyhee.com

http://www.tyhee.com

Brian Briggs

President -- Tyhee Gold

T: 604 681-2877

info@tyhee.com

http://www.suttergoldmining.com/s/NewsReleases.asp?ReportID=663112&_Type=News-Releases&_Title=Sutter-Gold-Announces-New-Major-Shareholder-and-Restructures-Debt

God Bless

QMX Reports Revenue of $9.1 Million and Operational Cash Flow of $2.28 Million for Q1 2014

06/03/2014

http://www.qmxgold.ca/English/Investor-Centre/News/News-Details/2014/QMX-Reports-Revenue-of-91-Million-and-Operational-Cash-Flow-of-228-Million-for-Q1-2014/default.aspx

http://www.qmxgold.ca/files/QMX%20Marketing%20Presentation%20May%202014.pdf

http://www.alexisminerals.com/

http://investorshub.advfn.com/QMX-Gold-Corp-QMXGF-17662/

God Bless

ST. ANDREW GOLDFIELDS (TSX:SAS) reports 2014 first quarter results,

with an eighth consecutive quarter of

positive cash flow from operations -

http://www.sasgoldmines.com/i/pdf/Presentation-AGM-13May14.pdf

http://www.sasgoldmines.com/s/FinancialStatements.asp?ReportID=653208&_Type=Annual-and-Interim-Reports&_Title=2014-First-Quarter-Results

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=101596215

http://www.sasgoldmines.com/s/Home.asp

God Bless

Q1 2014 results in - Excellon reports net earnings of $1.9 million from first quarter 2014

Excellon Resources Inc. (PC) (USOTC:EXLLF)

Today : Wednesday 30 April 2014

TORONTO, April 29, 2014 /CNW/ - Excellon Resources Inc. (TSX:EXN; OTC:EXLLF) ("Excellon" or the "Company"), Mexico's highest grade silver producer, is pleased to report financial results for the three-month period ended March 31, 2014.

Q1 2014 Highlights

Revenue of $10.5 million (Q1 2013 – $10.1 million)

Sales of 624,953 AgEq ounces (Q1 2013 – 476,281 AgEq ounces), including 383,782 oz Ag, 2,482,210 lbs Pb and 2,877,156 lbs Zn

Mine operating earnings of $2.7 million (Q1 2013 – $4.1 million)

Net income of $1.9 million or $0.03/share (Q1 2013 – net loss of $0.6 million or $0.01/share)

Cash flow from operations of $2.1 million or $0.04/share before changes in working capital (Q1 2013 – loss of $0.6 million or $0.01/share)

Total cash cost per silver ounce payable of $11.76 (Q1 2013 – $9.09)

All-in sustaining cost ("AISC") per silver ounce payable of $17.28 (Q1 2013 – $24.06)

Cash, marketable securities and current accounts receivable totaled $9.1 million at March 31, 2014 ($7.0 million at December 31, 2013)

Working capital totaled $11.8 million at March 31, 2014 ($10.3 million at December 31, 2013

".....During the first quarter, we demonstrated positive cash flow and profits, even while producing from relatively lower grade mantos at Platosa and at currently low silver prices," stated Brendan Cahill, President and Chief Executive Officer. "With years of significantly higher grade resource ahead of us, we are well positioned to grow even in this subdued silver price environment. Starting this quarter, we are reporting in accordance with the World Gold Council's all-in sustaining cost ("AISC") standards, which will provide investors with a clearer perspective on our cash flow per payable ounce of silver.........."

(Cont.)

http://ih.advfn.com/p.php?pid=nmona&article=62012675&symbol=EXLLF

Claude Announces Q1 Production Results

April 23, 2014 - Saskatoon, Saskatchewan, Canada: Claude Resources Inc. (“Claude” and or the “Company”) today announced first quarter production results of

11,344 ounces, representing a 40% increase from the 8,082 ounces produced in the first quarter in 2013. The grade in the first quarter also increased significantly by 34% to 5.76 grams per tonne from the first quarter in 2013.

Mike Sylvestre, Interim President and CEO stated, “Historically, our first quarter has always been a challenge and 2014 was no different. While we faced severe and abnormal winter conditions, we were able to complete the winter re-supply program and have our best first quarter production results in the last ten years. We have focused on improving our grades and that initiative is starting to pay off. We expect this trend to continue and we are confident that the mine grades will reconcile more closely to our reserve grade for the remainder of the year.”

The Company remains confident in meeting its 2014 production guidance of 47,000 to 51,000 ounces of gold. In addition, the Company continues to make progress in advancing the Santoy Gap towards production by the fourth quarter of 2014 by completing the fresh-air vent raise in the second quarter and continued mine development. The Santoy Gap currently hosts 266,100 ounces of gold in Mineral Reserves at 5.68 grams per tonne and is expected to increase production and margins by the beginning of 2015.

Claude Resources Inc. is a publicly traded gold exploration and mining company based in Saskatoon, Saskatchewan, whose shares trade on the Toronto Stock Exchange (TSX: CRJ) and the OTCQB (OTCQB: CLGRF). Its asset base is located entirely in Canada and since 1991, Claude has produced over 1,000,000 ounces of gold from its Seabee Gold Operation in northeastern Saskatchewan. The Company also owns 100 percent of the Amisk Gold Project in northeastern Saskatchewan.

For further information please contact:

Mike Sylvestre, Interim President & CEO

Phone: (306) 668-7505

or

Marc Lepage, Manager, Investor Relations

Phone: (306) 668-7501

Email:ir@clauderesources.com

Website: www.clauderesources.com

http://www.clauderesources.com/html/news/press-releases/index.cfm?ReportID=203321

St. Andrew Goldfields (.29) owns and operates the Holt, Holloway and Hislop mines in North America, and produced approximately 100,000 ounces of gold in 2013. The Company is also advancing the Taylor Project and is conducting aggressive exploration across 120km of land straddling the Porcupine-Destor Fault Zone.

Apr 14, 2014 - SAS reports Q1 2014 production results of 24,361 ounces of gold http://www.sasgoldmines.com/s/NewsDetails.asp?id=122570

Website: http://www.sasgoldmines.com/s/Home.asp

TSX: http://web.tmxmoney.com/quote.php?qm_symbol=SAS

Claude Resources Inc. Reports Full Year 2013 Results

http://www.prnewswire.com/news-releases/claude-resources-inc-reports-full-year-2013-results-253186771.html

* Revenue of $63.8 million from the sale of 44,823 ounces of gold.

* Total cash cost per ounce of gold (1) was $983 (U.S. $954).

* Net cash margin of $440 per ounce.

Claude Resources (.178) http://www.clauderesources.com/index.cfm

Excellon reports 2013 annual and fourth quarter financial results

Thursday 27 March 2014

TORONTO, March 27, 2014 /CNW/ - Excellon Resources Inc. (TSX:EXN; OTC:EXLLF) ("Excellon" or the "Company"), Mexico's highest grade silver producer, is pleased to report financial results for three and twelve month periods ended December 31, 2013.

2013 Annual and Q4 Highlights

Revenue of $33.3 million (Q4 - $7.4 million)

Sales of 2,038,295 AgEq ounces (Q4 - 545,428 AgEq ounces), including 1,403,783 oz Ag, 7,237,003 lb Pb and 9,683,329 lb Zn

Mine operating earnings of $8.7 million (Q4 - $0.2 million)

Net loss of $5.0 million or $0.09/share (Q4 - net loss of $2.4 million or $0.04/share), including a deferred tax accounting adjustment of $0.8 million recognized in Q4 as a result of the recently enacted Mexican tax reforms

Cash flow from operations of $1.7 million or $0.03/share before changes in working capital (Q4 - $0.8 million or $0.01/share)

Net cash costs per payable silver ounce of $10.51 (Q4 - $13.02)

All-in costs per payable AgEq ounce of $17.29 (Q4 - $16.09)

Cash corporate administrative costs reduced by $2.2 million or 36% relative to 2012

Cash, marketable securities and current accounts receivable totaled $7 million at December 31, 2013

Working capital totaled $10.3 million at December 31, 2013

"During 2013, and particularly during the third quarter, we demonstrated our ability to generate cash flow at Platosa despite the significant decrease in silver prices," stated Brendan Cahill, President and Chief Executive Officer. "The biggest impact on our profitability was the significant volatility in the silver price, particularly during the second and fourth quarters. We have now taken steps to reduce the effect of these fluctuations and we are confident that these adjustments will improve cash flow and profitability going forward. Additionally, just as we realized cost reductions throughout the year, we will continue to further reduce costs at the mine site level through 2014."

"Our strong, dedicated and valuable operations team should be proud of producing the most ounces from Platosa since 2009 and the most tonnes in the mine's history. In 2014, we aim to build on this improved production profile, while continuing to enhance our commitment to the highest levels of health and safety protocols and training."

Financial and Operating Highlights

Financial results for the three and twelve month periods ended December 31, 2013 and 2012 are as follows:

('000's of USD, except amounts per share

and per ounce) Q4 2013 Q4 2012 2013 2012

Revenue 7,445 9,113 33,332 36,273

Production costs (5,987) (4,153) (20,692) (16,401)

Depletion and amortization (1,260) (860) (3,910) 2,788

Cost of sales (7,247) (5,013) (24,602) (19,189)

Gross profit (loss) 198 4,100 8,730 17,084

Corporate administration (1,448) (1,854) (5,831) (7,338)

Exploration (212) (3,650) (6,718) (9,907)

Other (incl. finance cost) 512 (417) 202 685

Income tax recovery (expense) (1,457) 8,481 (1,423) 7,884

Net income (loss) (2,406) 6,660 (5,041) 8,408

Earnings per share - basic (0.04) 0.12 (0.09) 0.15

Cash flow from operations (1) 790 124 1,699 3,631

Cash flow from operations per share - basic 0.01 0.00 0.03 0.07

Net cash cost per payable silver ounce ($/Ag oz) 13.02 9.88 10.51 6.80

All-in cost per payable silver equivalent ounce

($/AgEq oz) 16.09 18.85 17.29 16.78

(1) Cash flow from operations before changes in working capital

Revenues during 2013 decreased 8% from 2012, despite a 52% increase in tonnes produced, due to a 33% decrease in the average realized silver price from $31.03 to $20.93. The decrease in the silver price resulted in lower revenues as well as significant charges against revenue during 2013, both of which affected income and cash flow (as further described below). Total revenues for 2013 were also lower than anticipated due to inclement weather at year-end on the west coast of Mexico delaying the delivery of $1.0 million in concentrate until early 2014. Costs of sales increased 28% during 2013 due to the significant increase in produced tonnage during the year.

The Company's net losses during 2013 and Q4 were primarily the result of $2.0 million (Q4 - $0.9 million) in negative price adjustments relating to decreases in the price of silver between the deliver date and final settlement date (up to four months later) of concentrate sold during the periods (including $0.6 million of unsettled deliveries marked-to-market at the end of Q4 2013).

The Q4 revenue adjustments of $0.9 million were the major contributor to the relatively low mine operating earnings of $0.2 million during the quarter. The Company has entered into new concentrate purchase terms, which are expected to reduce the effect of similar revenue adjustments in 2014/2015.

Other significant items contributing to the Company's net losses during 2013 and Q4 include: (i) a one-time non-cash income tax provision of $0.8 million resulting from the initial recognition of the Mexican mining tax reform; (ii) expensed drilling and exploration totaling $6.7 million during the year; (iii) an unrealized loss of $1.5 million (Q4 - $0.4 million) from a decrease in the fair value of 344,000 units of the Sprott Physical Silver Trust held by the Company, representing an underlying investment in 134,732 ounces of silver; and (iv) non-cash charges totaling $1.6 million (Q4 - $0.5 million) in respect of share based compensation.

Net working capital decreased $5 million during 2013 to $10.3 million (December 31, 2012 - $15.3 million), primarily due to exploration expenditures of $6.7 million and cash repayments of $4.5 million during the year related to the negative revenue reductions discussed above. Cash, marketable securities and current accounts receivable decreased to $7 million at December 31, 2013 ($15.3 million at December 31, 2012).

Cash corporate administration expenses decreased by approximately $2.2 million or 36% during 2013 relative to 2012 as the Company implemented cost reduction measures in the Toronto office. Cash compensation, in particular, was $1.4 million or 45% lower in 2013 than in 2011 and 2012.

During the first two quarters of 2013, the Company expended $6.2 million in drilling and exploration expenditures at Platosa and the Beschefer and DeSantis properties. Subsequent to May 2013, exploration expenses were reduced significantly. Due to current silver prices and market conditions, the Company has suspended drilling at La Platosa, though drill rigs remain on site and available to resume exploration at short notice.

The Company has committed going forward to providing costs per silver equivalent ounce on a "payable" basis, rather than on a "produced" or "sold" basis, as the payable basis provides a more accurate measure of the cash income received from each silver equivalent ounce sold by the Company. On the payable metric, costs per ounce appear higher than they may historically have appeared when reported on a produced or sold basis.

Cash cost per payable silver ounce net of by-products increased during 2013 to $10.51 (2012 - $6.80). This increase was primarily attributable to lower grades of silver (-15%) and zinc (-32%) in the mantos mined during 2013 relative to 2012, lower recoveries in respect of lead and zinc (as discussed in Operating Highlights, below) and related lower by-product credits on silver production, as well as higher costs in respect of certain consumables that are not expected to recur in 2014. All-in cost per payable silver equivalent ounce was slightly higher relative to 2012 at $17.29 versus $16.78.

Relative to Q3 2013, net cash costs and all-in costs increased, primarily due to lower grades mined during Q4 (684 g/t Ag in Q4 versus 975 g/t Ag in Q3) offsetting the increased tonnage milled (21,186 tonnes in Q4 versus 16,707 tonnes in Q3). As in Q3, during Q4 (i) significant expenditures were made on electricity to manage water inflows in the 6A Manto (which were resolved in late February 2014), (ii) the areas mined during the quarter contained lower lead and zinc grades, reducing by-product credits and silver equivalent ounces, and (iii) recoveries were lower than in previous periods (see Operating Highlights for a further discussion). The Company realized significant improvements in each of these respects in early 2014.

All financial information is prepared in accordance with IFRS, and all dollar amounts are expressed in U.S. dollars unless otherwise specified. The information in this news release should be read in conjunction with the Company's unaudited consolidated financial statements for the year ended December 31, 2013 and associated management discussion and analysis ("MD&A") which are available from the Company's website at www.excellonresources.com and under the Company's profile on SEDAR at www.sedar.com.

The discussion of financial results in this press release includes reference to "cash flows from operations before changes in working capital items", "cash cost per payable silver equivalent ounce net of byproducts" and "all-in cost per payable silver equivalent ounce," which are non-IFRS performance measures. The Company presents these measures to provide additional information regarding the Company's financial results and performance. Please refer to the Company's MD&A for the year ended December 31, 2013, for a reconciliation of these measures to reported IFRS results.

Production Highlights

Mine production for the three and twelve months periods ended December 31, 2013 and 2012 was as follows:

Q4 Q4 Year Year

2013* 2012 2013* 2012

Tonnes of ore produced 20,481 11,139 70,490 46,495

Tonnes of ore processed 21,186 11,452 69,862 48,199

Ore grades:

Silver (g/t) 684 751 718 846

Silver (oz/T) 19.96 21.89 20.94 24.67

Lead (%) 5.27 6.59 6.14 6.75

Zinc (%) 5.08 11.21 8.00 11.81

Recoveries:

Silver (%) 89.9 94.4 92.6 93.4

Lead (%) 71.2 85.7 79.4 82.1

Zinc (%) 75.8 83.7 80.2 84.8

Production:

Silver - (oz) 411,277 251,065 1,409,852 1,081,165

Silver equivalent ounces (oz) (1) 545,428 360,831 2,055,567 1,550,964

Lead - (lb) 1,720,303 1,393,067 7,342,108 5,731,160

Zinc - (lb) 1,857,066 2,387,785 9,876,955 10,450,813

Sales:

Silver ounces - (oz) 393,908 233,773 1,403,783 1,060,211

Silver equivalent ounces (oz) (1) 513,568 337,642 2,038,295 1,523,422

Lead - (lb) 1,530,833 1,324,026 7,237,003 5,638,330

Zinc - (lb) 1,660,102 2,253,698 9,683,329 10,316,726

Payable:

Silver ounces - (oz) 360,285 208,702 1,279,364 951,707

Silver equivalent ounces (oz) (1) 466,391 326,729 1,841,335 1,476,413

Lead - (lb) 1,453,171 1,254,681 6,868,685 5,331,554

Zinc - (lb) 1,376,336 1,892,706 8,117,208 8,660,607

Realized prices: (2)

Silver - ($US/oz) 20.02 35.56 20.93 31.03

Lead - ($US/lb) 0.96 1.03 0.94 0.91

Zinc - ($US/lb) 0.87 0.93 0.86 0.90

* Q4 data remains subject to adjustment following settlement with concentrate purchaser, Q3, Q2 and Q1 data has been adjusted to reflect settlement with concentrate purchaser.

(1) Silver equivalent ounces established for each period using prices of US$24 per oz Ag, US$0.90 per lb Pb, and US$0.90 per lb Zn applied to the recovered metal content of the concentrates.

(2) Average realized price is calculated on current period sale deliveries and does not include prior period provisional adjustments in the period. A complete reconciliation of net realized prices is set out in the Company's 2013 MD&A.

Note: "t"= tonne; "T"= ton

Production of over 1.4 million ounces of silver was the Company's highest annual production at La Platosa since 2009. The Company realized a significant improvement in tonnes per day ("tpd") of production during the latter half of the year from ~175 tpd during Q1/Q2 to ~210 tpd in Q3/Q4 (including 223 tpd in Q4) as the benefits of underground development work during the first half of the year were realized and the Company began identifying further operational efficiencies and improving water management. Production of 2.1 million silver equivalent ounces during the year was in line with the Company's revised target (announced September 17, 2013) and silver grades were generally in line with budget (718 g/t Ag versus 728 g/t Ag budgeted).

During the fourth quarter, ore was produced primarily from the 5A, 6A and Guadalupe North mantos. Tonnes milled represented a 27% increase on the previous quarter for a total of 21,186 tonnes. Grades were in line with estimates for the La Platosa resources mined during the period. As in the third quarter, recoveries were slightly lower due to (i) significant remnant grouting from historical water management measures in certain areas mined, (ii) oxide mineralization in the 5A manto, and (iii) similar lead and zinc grades affecting the mill's differential separation of each metal. Recoveries of all metals have exceeded budget to date in 2014.

Outlook

Excellon is targeting 2014 production of 1.4 to 1.6 million ounces of silver, 7.5 to 8.5 million pounds of lead and 9.0 to 10 million pounds of zinc or 2.1 to 2.3 million silver equivalent ounces (based on $24 silver, $0.90 lead and $0.90 zinc).

In December 2013, Mexico passed tax reform legislation that took effect January 1, 2014. The reform includes, among other items, cancellation of the reduction in the Mexican corporate tax rate from 30 per cent to 28 per cent by 2015, a special mining duty of 7.5% on taxable mining profits, fewer allowable deductions excluding interest and capital depreciation, and a 0.5-per-cent environmental tax on gold and silver revenue. The tax reform is expected to impact the Company's future earnings and cash flows. The Company intends to minimize the impact of these reforms to the full extent possible and, additionally, still holds significant loss carry forwards from its acquisition of Silver Eagle Mines Inc. in 2009, which may be applied against profits going forward.

Corporate Governance Updates

The Board of Directors of the Company is also pleased to announce the implementation of a Majority Voting Policy and the approval of an Advance Notice Bylaw, each as further described below.

Advance Notice Bylaw

The Advance Notice Bylaw requires that advance notice be provided to the Company in circumstances where nominations of persons for election to the Board are made by shareholders other than pursuant to: (i) a requisition to call a shareholders meeting; or (ii) a shareholder proposal, in each case as made in accordance with the provisions of the Business Corporations Act (Ontario) (the "Act"). Among other things, the Advance Notice Bylaw fixes a deadline by which shareholders must notify the Company of nominations of persons for election to the Board and provide that the same information about the proposed nominee as one would be required to include in a dissident proxy circular under applicable securities laws must be provided to the Company by the deadline.

In the case of an annual meeting of shareholders, notice to the Company must be made not less than 30 and not more than 65 days prior to the date of the annual meeting; provided however, that in the event that the annual meeting is to be held on a date that is less than 40 days after the date on which the first public announcement of the date of the annual meeting was made, notice may be made not later than the close of business on the 10th day following such public announcement.

In the case of a special meeting of shareholders (which is not also an annual meeting) notice to the Company must be made no later than the close of business on the 15th day following the day on which the first public announcement of the date of the special meeting was made.

The Advance Notice Bylaw provides a clear process for shareholders to follow to nominate directors and set out a reasonable timeframe for nominee submissions along with a requirement for accompanying information. The purpose of the Advance Notice Bylaw is to treat all shareholders fairly by ensuring that all shareholders, including those participating in a meeting by proxy rather than in person, receive adequate notice of the nominations to be considered at a meeting and can thereby exercise their voting rights in an informed manner. In addition, the Advance Notice Bylaw should assist in facilitating an orderly and efficient meeting process.

In accordance with the provisions of the Act, the Advance Notice Bylaw will be subject to confirmation by shareholders at the next annual meeting of shareholders of the Company. A copy of the by-law has been filed under the Company's profile on SEDAR at www.sedar.com.

Majority Voting Policy

Under the Majority Voting Policy, any nominee for director of the Company who receives a greater number of votes "withheld" from his or her election than votes "for" such election shall immediately following the shareholders' meeting tender his or her resignation from the Board for consideration by the nominating and corporate governance committee of the Board (the "Committee"). The Committee shall consider the resignation and recommend to the Board the action to be taken with respect to such resignation, which may include acceptance of the resignation or rejection of the resignation. The Committee shall be expected to recommend acceptance of the resignation unless exceptional circumstances exist that would warrant the applicable director continuing to serve on the Board. The Board has 90 days following the date of the shareholders' meeting at which the election occurred to decide whether to accept the resignation. Promptly after the Board's decision, the Company will disseminate a press release disclosing whether or not the director's resignation was accepted. If the Board determined not to accept the resignation, the press release must disclose reason or reasons for rejecting the tendered resignation. The Majority Voting Policy is accessible on the Company's website at www.excellonresources.com.

Annual Meeting

The annual meeting of Excellon shareholders will be held at 4:00 p.m. (ET) on April 29, 2014 at 330 Bay Street in Toronto, Ontario. Excellon shareholders as of March 11, 2014 are entitled to attend and vote their shares at the annual meeting. Materials outlining the matters to be approved at the annual meeting will be mailed in early April 2014.

About Excellon

Excellon's 100%-owned and royalty-free La Platosa Mine in Durango is Mexico's highest grade silver mine, with lead and zinc by-products making it one of the lowest cash cost silver mines in the country. The Company is positioning itself to capitalize on undervalued projects by focusing on increasing La Platosa's profitable silver production and near-term mineable resources.

Additional details on the La Platosa Mine and Excellon's exploration properties are available at www.excellonresources.com.

Forward-Looking Statements

The Toronto Stock Exchange has not reviewed and does not accept responsibility for the adequacy or accuracy of the content of this Press Release, which has been prepared by management. This press release contains forward-looking statements within the meaning of Section 27A of the Securities Act and Section 27E of the Exchange Act.

SOURCE Excellon Resources Inc.

Copyright 2014 Canada NewsWire

http://ih.advfn.com/p.php?pid=nmona&article=61610071&symbol=EXLLF

NUSMF

I remain fascinated by the idea...but it has gone nowhere. (so far)

http://news.nationalgeographic.com/news/2013/13/130201-underwater-mining-gold-precious-metals-oceans-environment/?source=hp_dl2_news_in_focus_deepsea_mining_20130201

EXLLF Excellon Resources (1.39) http://www.excellonresources.com/ a mining company operating in Durango and Zacatecas States, Mexico, and Ontario and Quebec, Canada. Excellon's 100%-owned La Platosa Mine in Durango is Mexico's highest grade silver mine, with lead and zinc by-products making it one of the lowest cash cost silver mines in the country.

Excellon produced 2.1 million silver equivalent ounces in 2013.

Never heard of that one and I thought I had heard of most of 'em.

Another brutal smack down of gold the past two days. As long as the crooks have a printing press and the dollar has value, they can continue to do the slam downs.

Thanks NYBob! I've liked QMX for a long time!

welcome to QMX Gold -

http://investorshub.advfn.com/QMX-Gold-Corp-QMXGF-17662/

God Bless

QMX Gold Corp is another good one. I found it (then Alexis) 3 years "too early" but that's three years they have had to get further along. Always liked their milling capacity.

Website: http://www.alexisminerals.com/

QMX doing the milling for Kerr Mines -

The Aurbel Gold Mill

http://investorshub.advfn.com/QMX-Gold-Corp-QMXGF-17662/

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=98660148

God Bless

Yes! We want the wheat! Would that be "hole" wheat LoL !?!

ATL Atlatsa Resources (.485) Atlatsa Resources is a platinum group metals mining, exploration and development company, controlling the third largest PGM resource base in South Africa. They produced in excess of 100,000 4E ounces ((platinum, palladium, rhodium and gold) in 2012.

Website: http://www.atlatsaresources.co.za/

Pink sheets: http://www.otcmarkets.com/stock/ATL/quote

There has been a restructuring. Been watching these guys since .20 and they appear to be the real deal.

I remember Bonanza getting bought out. If it's the same company I'm remembering.

I'm going to look into the others you posted once I get a chance.

Here's another old one I forgot about. They are bouncing off the lows...

CRCUF

http://investorshub.advfn.com/boards/board.aspx?board_id=19701

Opinions, as always, are welcome.

There are way too many penny mining scams. A lot of chaff and little wheat. We want the wheat!

SOLTERA MINING CORP. (SLTA) (.22)Files SEC form 8-K, Entry into a Material Definitive Agreement

Kerr Mines AISCF (.0396) the reincarnation of the old Armistice Resources. http://kerrmines.com/

Do you remember the old BZA ABGFF American Bonanza Gold ? They were supposedly a near term producer back in 2011 or so. Apparently they were acquired by an outfit now called Kerr Mines AISCF (formerly Armistice) around the first of the year.

Kerr appears to be assembling a portfolio of projects through M+A, judging by their 2014 PR's.

Don't know anything about Kerr since my thread started with a company they acquired, but they appear to be assembling value.

Decent candidate for further research.

GALKF Galantas Gold Corporation (.017) Galantas owns and operates a producing open pit gold mine near Omagh, County Tyrone, Northern Ireland. The mine also produces by-product silver and lead. A metals concentrate is produced by safe, low-toxicity processing and sold under contract to Xstrata Corporation

They're small but they are a producer. For the three months ending September 30, 2013 Galantas produced 500 ounces of Gold, 1,000 ounces of silver, and 15.5 tons of lead. http://www.galantas.com/

Looks like the miserable SOB's are gonna get Ukraine's gold next. All they can do is buy time. Sooner or later the last of the low hanging fruit, the "easy" gold to steal, ... will be gone. Gonna hang loose, buy physical, and prepare.

HL--the old reliable with one of the oldest histories. I remember visiting some of their old properties in Idaho many years ago. I am also waiting to buy US Silver back...be we need to see much higher silver prices before it's worthwhile...production costs being what they are. When Parker left the operation it sort of took the wind out of my sails.

It's sad what the banksters are still able to do with PMs...especially gold. All that paper gold and rigging. Stealing the gold from other countries and dumping it....or leasing it out multiple times Fractional reserve banking and fractional gold. I just read the Fed banks stole UKraine's gold and shipped it to their NY vault. They already swiped Gaddafi's gold. And Saddam's of course...a sick and sordid world at the top with criminal who set rules for us but break them freely on their own.

But I digress. I still watch a great many penny golds...some are legit (like Claude Resources) but they've been so shellacked they were turned into pennies. I avoid the micro pennies now as most of them are scams run by pumper crews. I should get my list together and post them here so we can all trade notes. There seems to be a lot of bargains out there still. I can't imagine they can suppress gold forever--or maybe they can.

One gold stock I've done well on is ANV--It is still consolidating over $5. Used to be $55 a few years back...

You Bet Montanore! I got a bunch of them squirreled away. I'm probably not going to use them but maybe somebody can. I'll dig through the notes and park that stuff here.

The good thing about a "well seasoned" list is, if they are going to take the easy way out and screw the shareholders, they usually do it fairly early on in the process. Some of these guys I've been watching for 2 or 3 years.

The machinations of the market have lead me to concentrate my holdings into fewer companies. Even with the recent take downs, I'm still green with Hecla and Metanor and if they try to push us around I'll just buy more of those two.

Hecla is a steal right now too. Pushing 10 million ounces of silver a year and over 100,000 ounces of gold, not to mention the lead and zinc. Not bad!

CLGRF Claude Resources Inc. (.2128)- 2013 Gold production of 43,850 ounces

http://www.clauderesources.com/index.cfm

Claude Announces 2013 Annual Production

http://www.clauderesources.com/html/news/press-releases/index.cfm?ReportID=203312

Metanor Resources (.20) has cash cost of US$766/oz Gold - financial results for its initial period as commercial Gold producer (12,751 gold ounces produced Q4 2013) http://www.metanor.ca/en/

Metanor Resources Inc. (TSX VENTURE:MTO) (Pink Sheets:MEAOF) (Frankfurt:M3R) has released financial results for its initial period as commercial Gold producer at its newly refurbished Bachelor Gold Mine and Mill in Quebec. It appears Metanor has hit the mark it had projected in corporate presentations in which it anticipated initial $800/oz cash costs - it delivered US$766/oz.

In reviewing Metanor's numbers for the first quarter ending as a commercial Gold producer we note several important points that show good health; 1) The P&L bottom line of $410,000 net loss is extremely positive after factoring out depreciation (a non cash item) of $1.07 million and the fact it had to include two months of expenses that were not in the commercial gold production period. 2) Even though Metanor produced 4,514 oz Gold in December it could only show 2,863 ounces of that as sales in the quarter because 2,375 ounces of Gold (representing ~$2 million at cost to Metanor and ~$3 million in terms of sales) was on deposit at the mint. 3) Cash-wise Metanor should be currently sitting well with somewhere between CDN$4 million - $5 million as it would have received that aforementioned $3 million from the mint in early January + it already had ~$1 million cash closing out the period + it is understood to have had an abnormally large GST(sales tax) refund (receivable) of an extra $700,000. 4) Also important to note is MTO.V announced earlier this week the amendment of a ~$5.3 million note with the Quebec Government, pushing the note back over a year and thus negating the potential cash call in April 2014.

Excerpt Metanor's February 28, 2014 release:

Metanor Reports its Financial Results for the Quarter Ending December 31st 2013 with a Cash Cost of US$766/oz

February 28, 2014 - Val-d'Or, Quebec, Canada: Metanor Resources Inc. ("Metanor") (TSX - V: MTO) is pleased to report on its financial results for the quarter ending December 31st 2013 (Q2). This press release should be read in conjunction with Metanor’s interim consolidated financial statement for the three month period ended December 31st 2013 and related Management’s Discussion and Analysis (MD&A), which can be found on the company website www.metanor.ca or on SEDAR www.sedar.com. All amounts are in Canadian dollars unless otherwise stated.

Q2 2014 Highlights

- Metanor achieves Commercial production November 2nd 2013 (declared December 1st 2013).

- Gold production of 12,751 ounces for the quarter which 4,514 oz were produced in December.

- Gold sales of 10,427 ounces for the quarter of which 2,863 oz were sold in December.

- Gross Margin of $149,128 for the quarter after depreciation and depletion of $1,070,138.

- Net Loss for the quarter of $410,174 which includes revenues and cost of sales for December and three months of expenses.

- Milled 62,033 tonnes of ore at a feed grade of 6.6 g/T and a recovery of 97.5%.

- Total of $3,556,885 in gold sales in December (commercial production period) at an average selling price of $1,242/oz (US$1,167/oz at an exchange rate of US$0.94/CA$1.00).

- Cash Cost of $815 per ounce sold in December (US$766/oz at an exchange rate of US$0.94/CA$1.00).

- Began the payment on the capital totaling $933,333 during Q2 on the loan provided by Ressources Québec.

- Subsequent to December 31st, Ressources Québec and Métanor concluded an amendment distributing the balance of the loan until March 2015. (See the press release issued February 27th 2013)

Ghislain Morin, president and chief executive officer, and Serge Roy, executive chairman of the board, declared: « We are very pleased with our quarterly results which show that Metanor can already generate a positive gross margin at the onset of commercial production. We plan to improve these results during the coming quarters as we attain full production capacity.

The full financial release from source with P&L statement may be viewed at http://goo.gl/2cwUcw online.

Metanor will continue to develop new drifts to the west which will allow access to new zones and increase the production toward a full capacity. Additionally, Metanor will increase the diamond drilling in the coming months in order to eventually add new resources and reserves.

Metanor recently announced Gold production numbers for January holding steady above 4000 ounces, this while still processing development ore. Recent development work to open new stopes at Metanor's Bachelor mine appear to have translated into results, allowing MTO.V to have stabilized Gold production over 4,000 oz per month. The stage is now set for a cash flow positive scenario, and a push to stabilize in the higher range of a 4000 - 5000 oz per month Gold target (at 800 TPD). Managements near-term plan is to increase the mill capacity by ~50% at low capex (~$4 million) and target 6,500 - 7,500 oz Gold production per month in late 2015 (contingent of obtaining additional electricity from Hydro-Quebec planned for 2015). MTO.V with ~267 million shares outstanding provides an ideal vehicle for investors seeking exposure to precious metals. Shares of MTO.V are currently trading near C$0.20 and the time to pay attention is now while MTO.V is trading at a fraction (less than 1/4) of its infrastructure (replacement) value alone, ignoring the ~1.6 million oz Gold resource in all categories (on all properties), and ignoring the large resource growth potential. Metanor is also actively advancing on a second front, it's Barry Mine deposit, that many believe has a the potential to translate to a large increase of gold ounces in the ground and a significant percentage increase in production ounces on top of the >6,500 ounces Gold production per month target expected at Bachelor sometime in 2015.

Market Equities Research Group has identified the following related research links on Metanor:

- Mining Expert Jay Taylor's interview with Metanor's VP and recommendation to clientele:

http://jaytaylormedia.com/media/MetanorResources20140128.mp3 [Audio]

- Mining Expert Lawrence Roulston initiates coverage http://sectornewswire.com/RoulstonMTO02-2014.pdf [PDF]

- Ronald Perry, Vice-President of MTO.V, November 15, 2013 Business News Network interview: http://watch.bnn.ca/#clip1044420 [Video]

- Recent Q4 2013 Analysts Report (C$0.47 price target): http://sectornewswire.com/MTOanalystOct2013.pdf [PDF]

- Metanor Resources Inc. Corporate Website: http://www.metanor.ca/en [Website]

- SEDAR Filings for Metanor Resources Inc.: http://goo.gl/fpbR3Z [Website]

- Recent Mining Journal article: http://miningmarketwatch.net/mto.htm [Website]

This release may contain forward-looking statements regarding future events that involve risk and uncertainties. Readers are cautioned that these forward-looking statements are only predictions and may differ materially from actual events or results.

Contact information:

Simon Levinson, Editor in Chief

Market Equities Research Group

s.levinson@marketequitiesresearch.com

Accesswire IA

February 28, 2014 - 6:38 PM EST

Read more at http://www.stockhouse.com/news/press-releases/2014/02/28/metanor-resources-has-cash-cost-of-us-766-oz-gold-financial-results-for-its#6YfDEW2TWk0MoXkO.99

|

Followers

|

63

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

1994

|

|

Created

|

07/30/11

|

Type

|

Free

|

| Moderators NYBob RBKissMyAs | |||

We're looking for legit penny miners that have the possibilty to become (or already are) REAL producers. NO SCAMS!

http://investorshub.advfn.com/boards/board.aspx?board_id=22034

Fun Fact: The US dollar is worth ~3% of what $1 was worth in 1913, the year

the Fed was created.

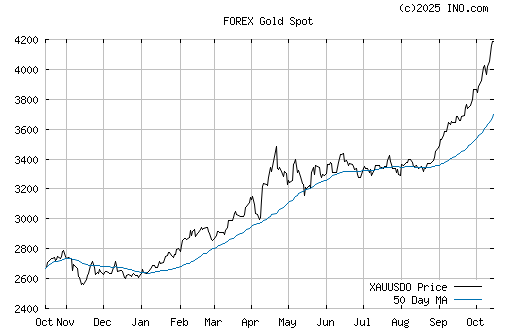

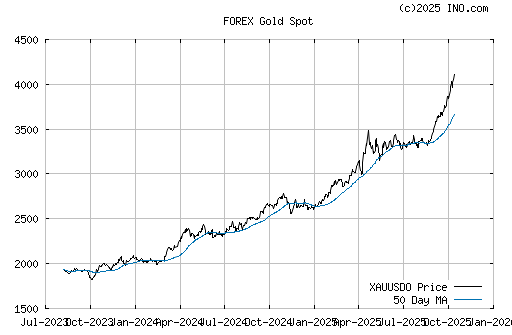

GOLD Higher lows and Higher Highs - REAL GOLDEN MONEY -

The super red banksters cults -

Rothschilds World Part 1 "Glen, Rush, Michael...Here's to you boy's"

http://www.youtube.com/watch?v=yhKHwrUA5SM&feature=related

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |