News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

http://www.prophecyplatinum.com/lp_20130927.php

800 possible meters, wow

just letting those that actually understand width and depth of a deposit by studying rocks know that you should hide these shares from your family members...cuz

I was able to catch up with billionaire Ivanhoe Mines (TSX:IVN) Executive Chairman Robert Friedland in Toronto yesterday. The Singapore-based mining legend was in Toronto this week to announce the launch of Ivanhoe Pictures, a new film and TV finance and production company, and to host the first investor presentations for his Ivanhoe Mines after a summer spent relaxing and reflecting on the Italian coast, where Mr. Friedland acquired a hotel property earlier this year.

Friedland says that the Chinese are determined to fight air pollution. “I have a home in Beijing but I’ve been avoiding it in recent years because the air pollution has become absolutely diabolical,” Friedland commented. This alone would be enough to drive the conventional Platinum market crazy, he added, noting that catalytic converters which reduce toxic emissions in automobiles use substantial amounts of platinum and palladium.

There is a revolution coming to the automobile industry via the Japanese, according to Friedland. Senior officials in Japan tell him that the Toyota Motor Company will announce hydrogen fuel cell automobiles later this year with a commercial roll out coming in 2015. “These cars will use ounces, not tenths of ounces of platinum,” Friedland said. This is why the Japanese government bought 10% of Ivanhoe’s Platreef project for $300 million, Friedland believes.

The Japanese will also spend as much as $100 billion upgrading their high speed trains, requiring massive amounts of metals, said the always enthusiastic Ivanhoe chairman.

“You will need a telescope to see how high the price of Platinum will go.”

On the subject of quantitative easing in the US, Mr. Friedland commented, “Now we have this new word written by idiots called tapering which is basically the breast of your mother is being taken out of your mouth but just for a few minutes and slowly, and while you’re getting deprived of your mother’s milk, they’re going to give you baby formula instead, and assure you at the same time that money’s going to be free forever. All of the world’s central banks are printing capital. We are not going into a deflationary meltdown. It’s not going to happen. Europe is starting to recover.. The US is clearly in a recovery… Growth in the developing world continues at pace.”

Friedland thinks the sacking of CEOs at major mining companies was a mistake by the boards and chairman at these companies. “Mr. Munk dispensed of Aaron Regent, which was a ridiculous decision, in my considered opinion… The new personage in the CEO positions are risk averse. They’re cutting costs and selling assets, sticking their heads in the sand… What do you think is going to happen in the mining industry where at the top all of the major mining companies are downsizing or shrinking?”

Copper

Friedland says that a growing global economy, coupled with a downsizing mining industry, and constricted exploration finance markets are contributing to a very bullish setup in commodities, in particular copper.

Electrical energy consumption per person on planet earth has never done anything but go up, said the mining legend, and power takes copper. “Copper is the king of metals.”

“These old mines are dying, and their grades are declining, and we’re going to have to have a much higher copper price.”

Friedland believes $4.50 – $4.75 per pound copper prices are necessary to justify the construction of new mines, with one exception, Ivanhoe’s high grade Kamoa project in the DRC, one of two copper development projects in that challenged but resource rich African nation which Ivanhoe owns stakes in. “Did you know the Katanga province [in the DRC] now produces more copper than all of Canada?” Friedland asked rhetorically.

“I think copper is going to hang around $3-$3.25, maybe for a nano second $2.75, but 5 years from now it’s definitely $4-$5 per pound, and this is what a bottom looks like.”

Friedland also suggested a new use for copper. Because of its antiviral and antibacterial properties, the mineral could replace stainless steel as a surface material in hospitals. Silver is another anti-bacterial alternative, albeit more expensive than copper. Whether we’ll be seeing copper counters in hospitals soon is unknown.

On the subject of Iron ore, Friedland commented, “Iron, I’m sorry to say it, but WE’RE FLOATING ON AN IRON BALL, THE EARTH. Iron is either the first or second most common element on the periodic table and everyone and his brother are building iron mines. But copper is rare and hard to find and without it we don’t have a modern world.”

Friedland Track Record

Mr. Friedland is considered to be the most successful mining entrepreneur of our time (Rick Rule to CEO.CA). In the early 1990’s one of Friedland’s companies discovered and developed the Fort Knox gold mine in Alaska, now owned by Kinross. According to Friedland, the project cost investors $7 million and was sold for approximately $600 million.

Friedland’s Diamond Fields International then discovered the Voisey’s Bay nickel project in Newfoundland, Canada, which sent his Diamond Fields stock from $1 to $161 in 13 months adjusted for splits in 1995. “So many trees died to generate the wood pulp in the Globe and Mail to gloat about the fact that Inco paid too much for Voisey’s Bay, $4.3 billion. But actually when the Brazilian’s came to buy Inco they ascribed $12 billion to the value of this asset, so I just want to remind you that the real wealth in the mining industry is generated by FINDING something,” Friedland emphasized.

Friedland turned his attention to Mongolia in 1999. With only $100,000 remaining in Ivanhoe Mines bank account, on the 153rd drill hole, the company discovered a massive copper gold ore body in the Gobi Desert at Oyu Tolgoi. Ivanhoe Mines then executed the largest drilling campaign in the history of the mining industry, over 1 million meters of diamond drill core, to delineate over $400 billion worth of reserves, which Friedland described as giving birth to a 100 kilogram baby.

Oyu Tolgoi mine in Mongolia (Company)

Robert Friedland’s 100 kilogram baby, the Oyu Tolgoi mine in Mongolia (Company)

Over $7 billion was spent developing a mine at Oyu Tolgoi and a $5 billion expansion is now under way, however the market capitalization of the company which owns the mine (Turquoise Hill Resources – TSX:TRQ) is only $5.25 billion. Turquoise Hill will be producing copper at a negative cash cost (thanks to the gold) for over 100 years, Friedland said.

“All the drama about the Mongolian government and the investment agreement is long forgotten. This is the largest lowest cost new copper and gold mine in the world trading at a discount of the capital cost of building the plant right here on the Toronto Stock Exchange right under your nose because we have a bubble in panic.”

Friedland didn’t stop there. “Consider picking up a few shares as a speculation… Pack them away for your favourite nephew.”

Friedland says that he still holds some 80-90 million shares in Turquoise Hill, despite no longer being officially involved with the company, having relinquished control to Rio Tinto, one of the world’s largest mining companies, in 2012.

Ivanhoe 2.0

The team who discovered and built the mine at Oyu Tolgoi are still with Friedland at his Ivanhoe Mines 2.0 (TSX:IVN), and Friedland says that the company now has the three best undeveloped mines in the world, Kamoa, Kipushi and Platreef.

“These are world class mines opening soon at a theatre near you in one package trading at a radical discount to the price the Japanese government was willing to pay.”

Mr. Friedland did not discuss his plans for Ivanhoe Pictures, although rumours are circulating that Ivanhoe’s first film could be a biopic of Friedland himself. The legend’s life does deserve to be told on the silver screen, but who will they cast to play the man?

On the subject of junior mining stocks, Friedland thinks they are extremely undervalued. “We’re much closer to the bottom of this cycle than you imagine. This is not the end of the super-cycle… The financial markets are like a school of fish, they all head in one direction until all of a sudden, they turn on a dime.”

Quad est

Lenghy discussion...= worth at the end (at today's trading "value")

Some of the previoue posts talk of frustration...from us retail investors...totally understandable...however imagine if you were the accredited investors that bought in last year at 2.70 with warrants not "in the money" which is why I am aiming to discuss some of the reasons we are here and trading here.

we are here because we all know that we USE 38,212 pounds of new minerals Every Year

http://www.mineralseducationcoalition.org/sites/default/files/uploads/per_capita_2013.pdf

and we invest in this understanding

trying to understand the forces inside and outside of this company in respect to where we are is complex, but here goes...the past internal issues are beyond a year now...with the experience management team now in place we are good to go moving forward with an updated M & I and PEA . The outside forces are multiple: with the many issues created by the greed on wall street about 5 years ago, the fallout has been many governments taking over companies and social programs to keep their economies from imploding, in return, they have had to look at avenues to keep money coming into their coffers. Thus in relation to mining: resource nationalism

the more stable economies like Canada not so much, but looking at much more of the world and we read of it weekly. The unstable areas in Africa are really loud in the press. The one that perplexes many is how Mongolia has treated a Major mining(RIO) company, 3 million population, all could be millionares by 2020, if they do not screw it up much more...headlines are getting better as they have seen the world turn on their country for this attitude...on the bright side ...mining companies are figuring out a more open conversation planning process as they mine:

Resource nationalism retains the number one risk ranking with many governments around the world going beyond taxation in seeking a greater take from the sector, with a wave of requirements introduced around mandated beneficiation, export levies and limits on foreign ownership.

The uncertainty and destruction of value caused by sudden changes in policy by the governments of resource-rich nations cannot be understated.

We are observing three key trends of resource nationalism:

Imposition/increasing of royalties or mining taxes

The announcement in 2010 of a proposed new ‘super profits’ mining tax in Australia had a significant ripple effect around the world. Many mining and metals jurisdictions announced increases in taxes and royalties during the course of 2011–12 and many looked at Australia’s action as commercial cover for proposed changes.

Amendments to mining and tax laws can result in changes to capitalallocation based on a weaker risk/reward profile.

Mandated beneficiation/export levies

Many governments are now seeking to have minerals beneficiated in-country prior to export. South Africa has announced a beneficiation strategy, as has Zimbabwe, Indonesia, Brazil and Vietnam. In order to better ensure in-country beneficiation, governments are imposing new steep export levies on unrefined ores.

Retaining state or national ownership of resources

Governments are also seeking to ensure that they retain ownership of their minerals, which is not a new phenomenon. These changes in ownership laws can have a significant impact on the reward miners’ expect to receive for the risk they have taken as they have paid for 100% of the investment but will receive only a percentage of the future investment return.

There is no doubt projects around the world have been deferred and delayed, and in some cases investment withdrawn altogether because of the changed risk/reward equation.

Miners should continue to engage with governments to foster a greater understanding of the value a project brings to the host government and be better able to negotiate appropriate trade-offs that preserve the value to both mining and metal companies and governments.

This includes encouraging governments to take a broader view of the return from natural resource development, as well as negotiating tax incentives and offsets.

Steps mining and metals companies can take to respond to this risk:

Invest in transparent relationships with host governments to foster a greater understanding of the value of the project to the host

Align with the host government’s long-term economic and political incentives and thereby become an invaluable part of the infrastructure in the host country

Focus on generating direct and sustainable benefits for the host community through pro-active and well organized social and community development programs

Align with multi-lateral agencies, such as the World Bank, to achieve a ‘prominent victim’ status in the face of mounting resources nationalism

Partner with state owned enterprises that have strong Government-to-Government relationships

Encourage direct government participation

Because of the above, many investors have ran from the mineral sector...like we are not going mine, and moreover not use 38,212 pounds per year...we are only going to need more minerals as the "rest of the world" continues to grow...you have to realize that the WWW. has allowed the masses to see what many have...and they want it too!!

So let's get to trading valuation.

We all know we have had selling pressure for about 2 years...well, so have all the rest of miners, bar a couple, but overall...hammered. Even the ones below have not been spared, all with solid resouces like NKL.

Platreef of Ivanhoe mines in South Africa, 28.5 million PGM's in the M&I. well know salesman at the helm there, Japan firm bought 10% of the deposit for 280 million. Underground starting at 700 metres on down...entire mills concentrators,etc will be underground as well to soften their footprint as they say...good pitch...but it is smarter more cost effective to take out the 1% of the rock you will use and keep the 99% waste rock or tailings down there...rather than taking 100 percent out and returning 99%,,,from an environmental perspective it makes it easy to sell...out of sight out of mind, so to speak...in reality...they have no choice at those depths...kinda of like Duluth Metals in MN. We are at surface, almost sticking out of the Earth, kind of like Polymet in MN. Back to Platreef and the amount of shares that make up this company.

http://www.ivanhoemines.com/s/StockInfo.asp

Shares have been nailed this year...they have 529,061,000 million shares...wow

and they have about 9% shares short!! From a Mr Friedland deposit?

http://finance.yahoo.com/news/ivanhoe-mines-begin-sinking-bulk-112247119.html

underground mines cost billions to fire up

heading to Canada: Platinum Group Metals 17.5 million PGM's at Waterberg

they have 419,000,000 shares trading on the NYSE just over a dollar

http://platinumgroupmetals.net/news_releases/2013/index.php?&content_id=398

for the discussion here, estimating the M&I will possibly get to 14-16 million PGM's by spring...would you rather have a company with 99,000,000 shares, and a near surface deposit, in a mining juristiction?

or in this neighborhood I grew up in that every environMental-ist on the planet is fighting?

http://www.polymetmining.com/wp-content/uploads/2013/02/2012_panels_coppernickelpgm_september2012.pdf

I own property in this region, I do not want my lakes, drinking water and planet destroyed...but I understand mining will happen with a lessor footprint than we did years back...mine closure plans and up front funds for cleanup are required...no brainer...next.

NKL management is looking at a staged production of higher grades with a lower CAPEX at startup of 300-400 million. This is solid reasoning and the bankers down the road these days want to see this type of mining...less risk for them with a faster payback.

to add one situation, acute skills shortage: Many areas around the planet are having issues finding quality skilled workers...We are in the Yukon and the company has expressed that they have a good working relationship with the local First Nations Group. This is mining country!!

Steps mining and metals companies can take to respond to this risk:

Source skills from aligned sectors and a broader demographic

Account for demographic and diversity factors when making investment decisions

Initiate programs that encourage semi-skilled and retired workers to re-enter the work-force

Target initiatives to retain critical skills held by older workers close to retirement

Create employment packages focused on career development opportunities

Implement early labor scheduling and sourcing within mine planning

Develop sustainable skills development programs to fill these gaps

Develop strategic alliances with institutions and communities

go to pages 9 & 10 of the latest presentation

http://www.prophecyplat.com/pdf/Prophecy_Platinum_Corporate_Presentation.pdf

glad I got a nap in with the NASCAR rain delay...

seriously, when the investment world 'wakes' up again to mining the minerals we consumers use daily and the miners that dig em up...this company is one to recon with.

New Presentation

pages 13-18 especially 17 & 18

http://www.prophecyplat.com/pdf/Prophecy_Platinum_Corporate_Presentation.pdf

and page 24

Why go to South Africa Mr Frieland? When you could have it in a mining friendly juristiction.

expressed in platinum equivalent and 3E PGM (platinum + palladium + gold) (see definitions below):

WS-154 intersected five intervals totaling 501.2 metres grading 1.84 g/t Pt Eq. (0.55 g/t 3E PGMs with 0.26% Ni and 0.19% Cu) for a total Pt Eq. grade thickness of 922 g/t-m

WS-160 intersected two intervals totaling 443.6 metres grading 2.46 g/t Pt Eq. (0.84 g/t 3E PGMs with 0.31% Ni and 0.30% Cu) and including 352.7 metres of 2.62 g/t Pt Eq. (0.93 g/t 3E PGMs with 0.31% Ni and 0.33% Cu) for a total Pt Eq. grade thickness of 1,094 g/t-m

WS-165 intersected two intervals totaling 194.1 metres grading 2.99 g/t Pt Eq. (1.24 g/t 3E PGMs with 0.26% Ni and 0.55% Cu) and including 60.7 metres of 4.24 g/t Pt Eq. (2.02 g/t 3E PGMs with 0.24% Ni and 0.99% Cu) for a total Pt Eq. grade thickness of 581 g/t-m

WS-193 intersected two intervals totaling 410.7 metres grading 1.77 g/t Pt Eq. (0.46 g/t 3E PGMs with 0.29% Ni and 0.10% Cu) and including 357.7 metres of 1.84 g/t Pt Eq. (0.49 g/t 3E PGMs with 0.30% Ni and 0.11% Cu) for a total Pt Eq. grade thickness of 726 g/t-m

These results indicate the potential for the Far East Zone to be laterally extensive with broad zones of significantly higher grades than the average of the Wellgreen deposit. Several of these holes contain Pt Eq. grade thickness values of 1,000 g/t-m, which are some of the best intersections to date on the project.

Prophecy Platinum Corp. President and CEO, Greg Johnson, said:

We are excited about the implications of these drill holes and the potential to define a large block of new mineralization within the existing pit model. We are also encouraged with the presence of the wide zones of significantly higher grade, such as in hole 165 which intersected 60.7 metres of 2.01 g/t 3E PGMs with 0.24% Ni and 0.99% Cu for a total platinum equivalent grade of 4.24 g/t Pt Eq. In our current drilling, we are testing the total width of this zone with a step out to the east designed to intercept both the historic tabular Wellgreen deposit and to drill into this Far East Zone to the north. Though the assay results of this offset drill hole are pending, it has already intercepted more than 750 metres of continuous ultramafic host rock containing disseminated sulphide mineralization. In light of this new interpretation, the Company is also reviewing and assessing additional historic drilling several hundred metres east of the Far East Zone and believes that these holes may have also intercepted this new zone of mineralization.

and...

In addition, the Company is drilling a series of shallow drill hole targets in areas with potential for higher grade starter pits, particularly in the Far West and West Zones. Five such drill holes have been drilled this year as part of the 2013 field program, with assay results pending.

We are also excited to report that in our review of historical information, some of which has not previously been published, we have noted areas of strongly enriched rare platinum group metals ("PGMs"), rhodium (Rh), osmium (Os), iridium (Ir) and ruthenium (Ru).

these rare PGM's will be in 2014 PEA as: inclusion in economics

ah, the fun starts today!!

Thank you. Interesting company.

What are we to expect this summer from the company?

I think that we may try to get a few shares on a price dip soon.

latest fundraising at 12% higher than she trades...cool

http://www.prophecyplat.com/news_2013_jun_20_prophecy_platinum_completes_equity_financing.php

all good stuff

CEO

Ellis Martin Report with Greg Johnson of Prophecy Platinum

posted today on youtube

we are at the levels of when it first started trading once the split happened...she should run again

Wellgreen Emerges

Prophecy Platinum Passes a Milestone with its First Yukon PEA

By Kevin Michael Grace

Throughout a 50-year history with numerous owners, the Wellgreen Project has never lacked for promise. Extensively drilled, it briefly produced high-grade nickel and copper in the Yukon 30 years ago. The property has been owned since 2011 by Prophecy Platinum TSXV:NKL, which has added gold and platinum group metals (PGMs) to the traditional resource base. With the June 18 release of a positive preliminary economic assessment, that promise has begun to emerge. Wellgreen could, in the words of Chairman John Lee, “potentially reach of the size of the some of the world’s largest nickel-sulphide projects.”

Lee calls Wellgreen “humungous.” It measures 22.1 square kilometres precisely, with “up to almost 18 kilometers of known mineralization. We’ve only explored two kilometers. The existing resource, which is at 450 million tonnes, is entirely encapsulated in that two-kilometer strike.” The project is located in the southwest of the Yukon, 317 kilometres northwest of Whitehorse, 35 kilometres northwest of the Burwash Landing airstrip, 15 kilometres from the Alaska Highway and 402 kilometres from the deepsea port of Haines, Alaska.

Read more about this gold play in the Yukon. http://resourceclips.com/2012/06/22/wellgreen-emerges/

Thanks for the post, but is that supposed to be a joke on the part of the reporter ?

Prophecy‘s Wellgreen Project and its newly found potential to host a rare PGE resource in addition to nickel, copper and gold

Newly found ? It takes a creature with a thousand year lifespan to say that!

News releases

May 28 = initial drill results from 2012 underground program

May 25 = exotic Pt/Pd family metals Ir/Rh/Ru/Os analyses released

May 10 = flowsheet study update

Visit company website for releases with full graphics

South of Klondike

Prophecy adds PGEs to its Yukon Nickel-Copper-Gold Project

By Greg Klein

Long after the Gold Rush that such inspired characters as Sam McGee, Blasphemous Bill and Dangerous Dan McGrew, Yukon is again coming to international prominence as a new gold play matures. In the territory’s southwest, Prophecy Platinum Corp TSXV:NKL is developing one of the world’s largest undeveloped resources of nickel-copper-platinum group elements towards PEA and prefeasibility.

Unlike Russia and South Africa, producers of 85% of world PGE supply, Robert Service’s old stomping ground has settled into a stable, mining-friendly jurisdiction. That bodes well for Prophecy‘s Wellgreen Project and its newly found potential to host a rare PGE resource in addition to nickel, copper and gold.

Read more about Prophecy in the Yukon. http://resourceclips.com/2012/05/28/south-of-klondike/

prpcf

http://seekingalpha.com/article/435841-crucial-coal-powering-mongolia-s-future?source=yahoo

parent company

cheers

closed financing...2 million dollars more than originally planned...restricted for 6 months...go to the web site for the news release

Cheers

Somebody didn't like what they heard. Too coincidental in timing to be anything else.

So does anyone figure the major drop in PNIKD after the conference call ? The $2M cash sufficient through September bothered me, but that is close to the end of the Yukon field season. So obviously there is dilution ahead. It is hard to value their in-the-ground and their unexplored potential, but obviously that is others problem, having seen my Prophecy Resources spin out shares fall around 40-50%, pause their briefly, then go a little more than +1000% in a few days, then back what -40% Monday.

This is one of the best investment opportunities I've seen in a while. Prophecy Coal is SEVERELY undervalued based upon their coal that they have just started shipping alone. Never mind the easily open pit mining of platinum, gold, cobalt, nickel, rare earths?, that they own a 45% stake in with their spin off Prophecy Platinum company. $20 a share should be an easily attainable price for this company.

press release

July 21, 2011, 11:19 p.m. EDT

Prophecy Platinum Files Wellgreen Mineral Resource Technical Report and Sets Investor Conference Call for Monday, July 25 at 1:30 pm EST

VANCOUVER, BRITISH COLUMBIA, Jul 21, 2011 (MARKETWIRE via COMTEX) -- Prophecy Platinum Corp. ("Prophecy Platinum" or the "Company") (tsx venture:NKL)(frankfurt:P94P) announces it has filed on SEDAR, the independent National Instrument (NI) 43-101 compliant report prepared by Todd McCracken, P. Geo. of Wardrop Engineering Inc., a Tetra Tech Company, relating to a mineral resource estimate for its Wellgreen PGE-Ni-Cu property located in the Yukon Territory, Canada, following announcements made by the Company in a news release dated July 14, 2011.

Prophecy Platinum will hold an investor conference call on Monday, July 25, 2011 at 1:30 pm EST (10:30 am PST). Mr. John Lee, chairman and Mr. Danniel Oosterman, P.Geo., senior geologist, will lead the conference call to discuss the Wellgreen project.

Prophecy Coal feels vulnerable, adopts defense against hostile takeover bids

By: The Canadian Press

Posted: 07/20/2011 7:29 PM

VANCOUVER - The board of Prophecy Coal Corp. (TSXV:PCY) has adopted a defensive plan to give the company's shareholders and directors time to consider alternatives should a hostile takeover attempt emerge.

"Prophecy management believes the company is very undervalued, thus vulnerable given the rise in value of its equity holding in Prophecy Platinum," John Lee, chairman of Prophecy Coal, said in an announcement Wednesday.

Prophecy Coal shares closed Wednesday at 72 cents. That was unchanged from Tuesday's close but up 36 per cent from July 13, a day before the platinum company released a new resource estimate for its Wellgreen property in Yukon.

Shares of Prophecy Platinum jumped 114 per cent to $1.59 and Prophecy Coal shares gained 26 per cent to 67 cents on July 14. The two companies were the most active on the TSX Venture Exchange on July 15, a day after the estimate.

Prophecy Platinum's shares closed Wednesday at $3.52, making Prophecy Coal's 22.5 million shares in that company worth about $79 million — compared with a total market value of about $137 million for the coal company.

Apart from its shares in the metals miner, Prophecy Coal controls more than 1.4 billion tonnes of thermal coal on two properties in Mongolia. Thermal coal is used primarily as fuel for power stations.

|

Followers

|

17

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

78

|

|

Created

|

07/25/11

|

Type

|

Free

|

| Moderators | |||

The 100% owned Wellgreen project hosts a large PGM-Ni-Cu deposit located just off the Alaska Highway in the southwest of Canada’s mining-friendly Yukon Territory. A 2012 Preliminary Economic Assessment (“PEA”) on Wellgreen estimated open pit production potential of 7 million ounces of PGM + gold, 2 billion pounds of nickel and 2 billion pounds of copper over a 37 year mine life (please refer to footnote disclosure on the PEA below)1. The Wellgreen property features excellent access and transportation infrastructure and the deposit is just 15 kilometres by all-weather road from the paved Alaska Highway, a major all-season trucking route leading to deep sea ports at Haines and Skagway, Alaska. Ranked in the top 20 mining jurisdictions globally in the 2013/2014 Fraser Institute Survey of Mining Companies, the Yukon has a rich mining heritage that dates back to the Klondike gold rush of the late 1800s.

Wellgreen Platinum is focused on the advancement of the Wellgreen project toward production, with current efforts underway designed to further define the mineral resource, evaluate overall project economics, simplify project financing requirements and complete environmental permit applications.

The Company expects to release the results from an updated PEA by the end of Q2 2014.

The Company anticipates releasing the results of an updated PEA on the Wellgreen project in Q2 2014 and associated engineering studies on pit designs, the location and general arrangements of the mill, tailings pond, waste piles, water treatment system, accommodations, and water (domestic, potable and process) are in progress. The updated PEA will consider Liquefied Natural Gas (LNG) as a primary power source rather than higher cost diesel, which was the primary power source in the 2012 PEA. The project team is investigating a staged capex approach with a lower production rate than the 2012 PEA during the initial years of operation with the goal of decreasing pre-production capital expenditures. The Company will also evaluate the economics of larger production scenarios in the PEA update.

The Company has continued environmental baseline studies and First Nations consultation in order to begin the environmental assessment process in 2015.

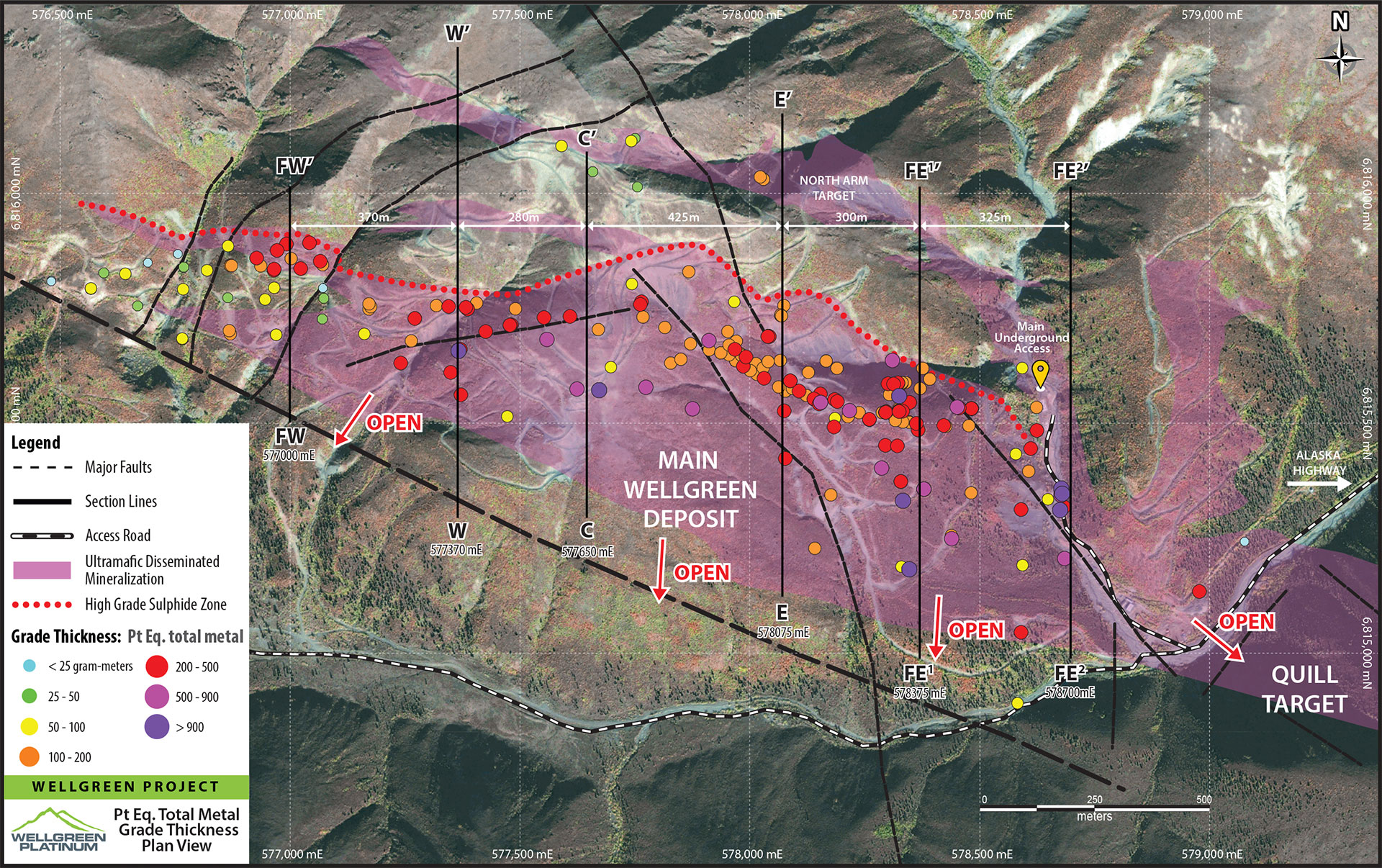

Mineralization at Wellgreen has been defined over a strike length of approximately 2.5 km and is open in most directions. Drilling conducted since 2012 has identified a nearly continuous zone of disseminated PGM, nickel and copper mineralization in ultramafic intrusive rocks, starting from surface and continuing down to 200-500 metres, with a higher grade package of ultramafics lower in the section of up to 150-300 metres with substantially higher PGM grades.

An updated geologic model for the project that integrates all existing geologic information is being developed as part of work to provide an updated resource estimate for the PEA update and which allows for the development of priority targets for future testing.

The 2013 Project Activities are summarized as follows:

The Company has conducted a thorough technical review of the Wellgreen project, including a comprehensive assessment of exploration results back to the 1950’s. With the historic focus on high grade massive sulphide occurrences amenable to narrow seem underground mining many of the historic drill holes were only selectively assayed for high grade mineralization. With a focus on the bulk mining potential of the deposit the Company has re-logged and completed continuous assays where possible sampling all of the material within the mineralized ultramafic host rocks.

On July 17, 2013, the Company announced the commencement of the 2013 exploration field program. Metallurgical test work and engineering initiatives had also commenced at that time. Comprehensive re-logging and cataloging as well as re-sampling of historic drill holes has now been completed and is being integrated and interpreted. The total re-logging and re-testing program completed to date is 18, 377m.

RE-ASSAYING PLAN VIEW

A targeted surface exploration drilling program, designed to upgrade a portion of the Inferred resource as well as test potential higher grade zones also commenced in July 2013. This drill program was completed near the end of November 2013. The program included deeper holes from surface designed to pursue higher grade PGM mineral resources as well as a number of shorter holes designed to increase confidence in the model and upgrade portions of the resource to Measured & Indicated resources from Inferred.

All of the historical exploration data that was re-evaluated along with most recent drilling programs will be utilized in an updated deposit model that is projected to be completed by Q2 2014 and will be part of a PEA update. The above image shows the locations of the historic holes that were re-logged and assayed in 2013 and early 2014.

As noted above, extensive work conducted on the geologic modeling of Wellgreen revealed some exciting new potential developments. The modeling work started in the center of the deposit with the most concentrated drill information and moved out from there to both the easternmost and westernmost ends where less information was available. This work has been aimed at increasing confidence in the resource model, defining new bulk mineable zones of mineralization that have not been previously recognized as well as better defining the geometry and distribution of higher grade material in the resource.

2.5Km Strike: Open East / West and at Depth

Work to date has allowed the Company to identify three promising target areas with wide intervals of higher grades:

Market conditions in the resource sector have led major institutional investors to focus on projects with lower pre-production capital requirements over those with large scale high initial capex expenditures. To address this, the Company is analyzing first-stage operations targeting a lower production rate and a significantly reduced capex scenario as compared to the 2012 PEA1. The full text of the 2012 Wellgreen PEA is available here and under the Company’s SEDAR profile at www.sedar.com.

The metallurgical test work upon which the 2012 PEA was based was preliminary in nature and attained the initial objective of demonstrating the material would report to a conventional sulfide flotation circuit bulk concentrate. Subsequent metallurgical testing has supports the potential of using conventional sulphide flotation methods to produce separate nickel and copper concentrates (click here to view the 2012 metallurgy report). The metallurgical testing also indicated opportunities to optimize recoveries, improve concentrate quality, and pursue recovery of rhodium, ruthenium, osmium and iridium.

Mr. Mason began his career and traditional training with Deloitte LLP as a Chartered Accountant, followed by Homestake Mining Company (merged with Barrick Gold Corporation) in mineral exploration, construction and operations reporting.

COMPANY WEBSITE

http://www.wellgreenplatinum.com/

4/14 JAMES WEST INTERVIEW

CEO Greg Johnson provides an overview of Wellgreen’s renewed focus on bringing its flagship platinum-nickel-gold project into production with a revised (and smaller) capex approach, and the moves the company has made to strengthen both its management team and its share structure. Transcript: Greg Johnson: Well, it’s been a fairly busy period for the company. Our new management team all joined about 15 months ago, in late 2012 and at that point the Board brought in a new technically focused management group. We undertook a couple of important things over the last year plus. One was to comprehensively go back and compile all of the existing information on the project back to the 1950s to bring all that into a single database and systematize it and allow our geologists and team to really dive in, engage some of the leading experts in PGMs who helped us to be able to understand the Wellgreen system in context with other world class systems like Norilsk in Russia, the Bushveld down in South Africa.

So our work with the new drilling, we have got almost 40,000 meters of new drill information that’s gone into the program since the 2011 resource estimate has really built our confidence in terms of understanding of the system. The early work in 2011 demonstrated that we had a very large system, mostly inferred, and the work that we’re doing now is really reinforcing the scale of the system, in fact, it’s demonstrating that we’ve got what’s effectively becoming a porphyry scale PGM System here, that’s open-pitable. In addition, there were some pretty important structural changes at the corporate level. We had a controlling shareholder that was around a 30% position that we placed entirely in 2013, in new hands, and that restructuring of the company resulted in new Board of Directors and effectively taking that over-hang from those stock sales from that financially distressed investor out of the way so that we would be in a position to be able to take the story out.

James West: Okay, was that a Prophecy Coal you are referencing there? Greg Johnson: Prophecy Coal was the original control and shareholder in Wellgreen and they are now effectively completely out of the shares. James West: Okay. So what’s been happening since your new team has taken over? Greg Johnson: Well, in addition to the drilling, the development of the new geologic model, we have been undertaking as well, engineering and metallurgical test work. We’ve got a couple of major milestones here in the second quarter. We are looking to deliver an updated concept on the engineering and production for the project. We are looking at a smaller capital project focused on higher grade material, potentially an open-pit and underground combination operation, and we’re targeting an operation that could be the largest producer of PGMs in the first world, potentially larger than Stillwater; as our target for this project, and clearly the resource that’s coming together is demonstrating that this is a system that could be a very large producer for a very long period of time. In addition, we are getting set up to look at pre-feasibility activities, they are going to get kicked off in the second half of this year and we are targeting to be able to move into feasibility in 2015.

James West: Hey, well that’s interesting. Have you been drilling all through the winter this year? Greg Johnson: We drilled up in through November and we’ve been releasing the results of a combination program, it was about 5000 metres of new drilling, including one of the widest intercepts ever hit on the property, 756 meters at almost 2 grams per ton, platinum equivalent. In addition, we had the benefit of being able to go back into historic drilling. Particularly drilling that was done in the 1980s, and we were able to re-log and resample many of it for the very first time, about 20,000 meters of historic drilling. So our combined program was about 25,000 meter program. And all of that is going to go into this new resource estimate that’s going to be coming out in the second quarter and the new preliminary economic assessment.

James West: I see! Okay, so then — I had actually visited the Wellgreen project back in 2011 and at the time there was some discussion about a 16-17 kilometer strike length for the whole Wellgreen project. Is that still something that you feel comfortable sort of putting out there? Greg Johnson: Yeah, our property is about 18 kilometers long that we control a 100%. The main focus — we’ve got almost 800 drill-holes in the Wellgreen deposit proper, and that’s about a ten million ounce platinum equivalent resource for platinum, palladium and gold. Along trend of that, we have got a series of other deposits that are also associated with these ultramatic systems. (00:05:12) Most of the work on those was done in the 1980s. There really hasn’t been much more modern work done since that time. But we undertook some surveys on project, both of magnetics as well as surface sampling and we have identified two very high priorities areas. One that is the continuation of the Wellgreen to the East called Quill and that’s about a two-and-a-half kilometer long anomaly combination of soils and magnetics. And then the second is the Burwash area which historically was actually a separate property that was optioned by INCO and others looking for high grade massive sulfide deposits. And that deposit has a very strong signature similar in scale to Wellgreen itself, with historic drilling shallow holes, but some interesting results in some of that historic work. And with the new surveys that we have, we’ve got some very large targets that we’re hoping to be able to test this year. All of this is on the road. So all of this, if we can develop additional open-pitable resources could be processed through a centralized facility and all of it could be looked at as kind of a single coherent district.

James West: I see! Interesting! So those discrete deposits to the East that you mentioned in Burwash and Quill, are those — you don’t think those are contiguous possibly connected to the main Wellgreen deposit? Greg Johnson: Well, the geology is mapped as continuous. But we don’t have a lot of information on there yet. A lot of that is based on outcrop mapping and magnetics in particular. The Ultramatic Host Rocks for the deposits do have a high degree of magnetic minerals in them. So magnetics can be a very good tool, but until we actually have a series of drill-holes across those, it’s hard to say whether or not this is going to be continuous. Certainly when you look at Quill, and you look at the strength of the magnetic signature at Wellgreen, and the fact, that that runs unbroken into the Quill target, one could argue that there is a strong probability that there is continuation of Wellgreen into Quill. Burwash, it almost appears that there is a — the area that our main access road comes in and the Quill creek drains out of — it looks like there may be some kind of important structure; geologic structure that goes through there. And sometimes in geology and ore deposits, big structures can be important. So it looks like we may have a little different geometry as we get across into Burwash. And we don’t know what level we’re looking at in the system, we could be looking deeper than we are at Wellgreen. So we’re pretty excited to take a look at that and see what comes out of it. James West: Sure! Okay, so what is the drilling budget for 2014 in terms of dollars and metrage? Greg Johnson: So we’re basically looking to start a pre-feasibility level program in the second half of the year. So that’s probably going to kick off sometime in June. We are talking of $5-$10 million program, and actually that’s likely to be something that’s going to be in the 5,000-10,000 meter program combination, probably of reverse circulation and core drilling. We haven’t finalized, right now we’re going through and developing our priority target list, and I can tell you that our target list is probably going to be longer than what we’re going to be able to go after, so you know we’ll clearly be prioritizing within our priority list. But there are some very exciting targets. Some of the very best holes at Wellgreen have not had the natural step-out adjacent to them, and so, were going to want to test some of these targets at Quill and Burwash look like, very promising targets. So I think we would want to test some of those. So it’s going to be a combination of both, infill confirmatory work, as well as step out and expansion work and testing some of these new targets.

James West: And I assume that’s all in support of an updated revised resource calculation? Greg Johnson: Yeah, so we’ll have an updated resource out this second quarter along with the updated economic approach looking at this smaller capital, higher grade start-up concept. And then, we would look to put out a pre-feasibility update to that probably early in 2015 and then begin the feasibility work in the remainder of 2015, with potentially permits could be completed by late 2016 on the projects. (00:10:03) So, we do have the opportunity that this thing can move quite rapidly, particularly mining is the industry in the Yukon, as you know. So they’ve got a good process in terms of going through environmental assessment, The Kluane First Nations are strong supporters of the project and we see the project being able to move fairly quickly through that process. James West: Sure! Okay, so in terms of financing a $10 million drill program in 2014, does Wellgreen have that capital in the bank? Greg Johnson: We are going to need to raise some money, and so we’re basically going to be looking to raise, probably something in the $5-$10 million range. It’s depending on the outcome of that investment round, that’s going to kind of set the plans in terms of how much work will be done in the summer or into the fall. But that work would be specifically targeted towards that next major milestone of the completion of the pre-feasibility studies. James West: I see. And at this point do you have as an investor any major mining corporations or large mineral funds that will sort of provide the role of lead order in that financing? Greg Johnson: Yeah, we’ve got — a number of our existing shareholders have invested in each round of financing, including, putting in lead orders. We’ve got a number of new funds that are looking at the company in terms of new investment. These are names that are also invested in other platinum names and are groups that are putting capital to work today. In addition, we are already discussing the project and potential investment from a number of more strategic type investment groups. These could be groups that are affiliated with smelting groups, or some of the producers. I think we’ve got a number of irons in the fire that we’re pursuing. It is still fairly early days at Wellgreen, but there are so few assets of scale in the platinum space, particularly that would likely have an open pit mining cost structure and scalability, and I think as we get out this next set of studies on the resource and on the engineering, and as we’re advancing that we’re likely to see a lot of attention from those groups over the next couple of quarters and years.

James West: Sure! Okay, now what about infrastructure? It seems to me that there were some challenges there in terms of energy, electricity etcetera. Has there been any progress on that front since 2011? Greg Johnson: I mean the Yukon energy is one of the main issues for all projects. Now fortunately, we’ve got the highway that goes past the project and we’ve got our year round access road and the two ports. The one at Skagway and the one at Haines are already in place with capacity to be able to handle our concentrates. So really when we talk infrastructure, for our project, it mostly is about energy with the access roads and things already there. The Yukon has about 20 MW of capacity on the grid. There is a high capacity line near Haines junction which is a about 100 kilometers from the project down the highway. LNG is definitely coming to the Yukon; there is a couple of initiatives that are underway now. The State of Alaska’s Industrial Development Bank is putting in place an LNG facility in Fairbanks, Alaska. They’ve completed their feasibility and they’ve gone to tender for the groups that’s going to construct that, and that’s supposed to be up and running by late 2015. So that’s a possible source for us, and in fact, we are in discussions with the Alaska Industrial Development and Export Authority right now about a potential MoU on that source of LNG. In addition, about 95% of the Yukon grid is hydroelectric, about 5% of their power comes from diesel and they are upgrading those sets to become LNG and are actually in the construction phase on their first LNG plant that would be tied into the grid now in Watson Lake. So the Yukon Energy Corporation is going to be bringing LNG to the territory for that. So we are going to be looking for this next study, the PEA that was done in 2012, we used diesel as its assumed power source. We are likely to be looking at an LNG-base case, which could be a significant reduction in the cost assumptions for power and it looks like we’ve got two or three different potential sources along with investigating whether or not it may make sense to extend the power line from the main Yukon Energy Corporation Grid. James West: Oh well, great! So it sounds like you’ve got options there.

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |