News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Thanks

I'm thinking of some long term options LEAPs maybe.

all the big risk items are in place now

BEV production line humming

Phase 2 expansion underway

Share structure fixed

FCEV timetable published and beta1 tests were excellent

Short Interest

81,207,665

http://nasdaqtrader.com/Trader.aspx?id=shortinterest

Q) Which institutional investors are shorting Nikola?

A) As of the most recent reporting period, the following institutional investors, funds, and major shareholders have reported short positions of Nikola: Concourse Financial Group Securities Inc., Sculptor Capital LP, EMG Holdings L.P., Group One Trading L.P., Bank of Montreal Can, Teramo Advisors LLC, Walleye Trading LLC, Simplex Trading LLC, National Bank of Canada FI, Bank of America Corp DE, Sculptor Capital LP, Walleye Trading LLC, Jane Street Group LLC, Goldman Sachs Group Inc., and UBS Group AG. These positions are disclosed in Form 13F filings with the Securities and Exchange Commission.

Short Interest

81,207,665 or 29.7% of Float Shorted

https://www.marketbeat.com/stocks/NASDAQ/NKLA/short-interest/#:~:text=How%20often%20is%20Nikola%27s%20short%20interest%20reported%3F%20Short,for%20U.S.%20stocks%2C%20including%20NKLA%2C%20twice%20per%20month.

https://www.finra.org/filing-reporting/regulatory-filing-systems/short-interest

Will be fun to watch this grow over the next few months as deliveries ramp up and phase 2 is built. When the next FCEV truck are out being tested I think people will start to believe.

Nikola institutional ownership

https://fintel.io/so/us/nkla

well Mr businessman it isn't called the Consumer price index for a reason is it.

Consumer related items will start to fall in price following gas just like they rose.

Business aspects of the economy that go into overall inflation/recession calculations will take longer

In both areas there are very few things the government can control - especially this time around with the European war, politics and weather along with the hangover from Covid raising shipping costs astronomically which have hardly dropped.

I saw that German goods will cost more since they have to se smaller ships on the Rhine due to lowest river levels in memory, even using land transport instead.

Low and slow…. Scratch offs are available for those who need instant gratification. Lol

Adding every payday…. My future self thanks me. Ur too much! Lol

NKLA

all day long !!!!

NKLA

CPI report supposedly says less inflation which is a JOKE to this US businessman... NKLA stock lost over $2.00 in last 2 days, its earnings beat in fact, while Nasdaq soars even higher...???

Probably the lower CPI data today helps as expectations of interest rate hike fall.

seems the market likes the news that Mark Russell is stepping down at the end of the year:

https://ih.advfn.com/stock-market/NASDAQ/nikola-NKLA/stock-news/88804590/nikola-announces-leadership-succession-michael-lo

Given the history of that role I would have liked Mark to stay at least 6 more months - for successful FCEV production, although Michael was hired with a view he would take over.

It's load time still. Every big dip.

Markets stalled. Everything is coming down until economic data on wed. That data will determine direction. NKLA ran too high too fast. 7 is a good pause with no catalyst.

I just bought yesterday before close at $7.81. Wow, every time I buy this stock it goes down. I guess I should warn people so they can sell before I buy!

The Coming Silver Price Shock: Warning Everywhere - Keith Neumeyer | Silver Price Prediction

Jul 24, 2022

A U G U S T_ 4 , 2 0 2 2

Q 2_ 2 0 2 2_ E A R N I N G S_C A L L

https://d32st474bx6q5f.cloudfront.net/nikolamotor/uploads/investor/presentation/presentation_file/51/3._2022.08.03_Q2_2022_Earnings_Call_Deck_v23.pdf

https://investorshub.advfn.com/NIKOLA-MOTORS-NKLA-37678

Filing of Certain Prospectuses and Communications in Connection With Business Combination Transactions (425)

August 05 2022 - 06:07AM

Filed by Nikola Corporation

https://ih.advfn.com/stock-market/NYSE/romeo-power-RMO/stock-news/88769728/filing-of-certain-prospectuses-and-communications

[Transcript of CNBC interview with Mark Russell, August 4, 2022.]

Speaker 7:

Welcome back. A trio of EV stories to tell you about today. Tesla’s annual shareholder meeting kicking off in just a few hours, shareholders are voting there whether to approve more shares, so it can follow through on the three for one stock split, it’s up sharply over the last month. Meantime, Lucid Motors is under pressure after cutting its vehicle guidance for this year by 50%. And then there’s Nikola, which is higher today beating analyst assessment on both lines, delivering 48 trucks in the second quarter, also confirming it expects to deliver between 300 and 500 trucks by the end of the year. And joining me now to talk about all that is Nikola’s CEO Mark Russell. Mark, welcome back. Good to have you.

Speaker 4:

Good to be here.

Speaker 7:

So- so on the- on the production, you delivered 48. I think you expected to deliver 50. Previously expected 50 to 60. What are you learning about this process as you get it going?

Speaker 4:

Well that it takes, uh, 10,000- about 10,000 parts to build a truck and the number you need to build a truck is all of them. (laughs). And if you don’t have one, you can’t build the truck.

Speaker 7:

And that you’re having trouble getting them?

Speaker 4:

Well, there were a lot of parts short as we ramp this up. Around the world, this is the biggest supply chain crisis I’ve ever lived through. And so getting all those parts in the right place at the right time was hard.

Speaker 7:

Is it getting any better?

Speaker 4:

Yeah. Actually, I think we’re in such a better position now than we were, uh, a month or a quarter ago for sure. And we expect to keep being in stronger position going forward with control over our battery supply chain once the Romeo acquisition closes.

Speaker 7:

Is that why you are sticking with the 300 to 500 delivery expectation for the full year despite this supply chain crisis?

Speaker 4:

Exactly. We- we’re confident that we’re gonna overcome anything that comes up and we’re gonna be able to- to hit in that range.

Speaker 7:

What is- what is your perception of- of consumer demand at this point for- for the trucks that you’re producing? Both the batteries and your future plans around hydrogen fuel cell.

Speaker 4:

Well, we- we’re not direct to consumer of course, we’re business to business. And the businesses that we sell to, they- they really want and need these trucks. Um, many of our launch customers have objectives to help decarbonize commercial transportation. And the only way you do that is if you can convert from diesel trucks to clean, pure emission trucks, which we sell. And we provide the energy that powers them.

Speaker 7:

What about the regulatory environment? Is that a headwind or a tailwind at this point?

Speaker 4:

Well, I’d say it- it’s potentially about to become a- a big tailwind if the current proposed legislation passes. The- the so-called Manchin Deal, if that is signed into law, that’s gonna be a powerful incentive for us and everybody else in the space. Additional purchase incentives and additional incentives on the production of- of clean hydrogen.

Speaker 7:

Why? So I was wondering about- about how it affects you directly. ‘Cause a lot- a lot’s been told about the consumer incentives to buy EV cars, how- how does it affect you and what you’re trying to do?

Speaker 4:

Well if this legislation passes as is, as we understand it, you know, it’ll include an incentive of up to $40,000 for a commercial vehicle, um, heavy truck like ours. That’s in line with what’s been there for passenger cars for a number of years. So that finally puts commercial vehicles on an equal footing with passenger cars. And then unique to heavy duty transport and unique to Nikola’s business model and just a few other people in the world, is the hydrogen production tax credit, up to $3 a- a kilo for- for hydrogen kilo produced. Which would be a powerful incentive to get hydrogen, uh, clean hydrogen into the economy and powering things like heavy trucks.

Speaker 7:

So would it ch- would it change the- the economics for you? The calculus, the forecast?

Speaker 4:

It would make it better, you know, everything we do is based on pure economics with no incentives or anything like that. We wanna make sure it works without incentives. But if we do have incentives, we’re thrilled for- to- to have those and they make it even better. That would be the case here, makes it even better.

Speaker 7:

I ask because so the analyst consensus is that your revenues are five times higher than they are- five times higher in ‘23 than they are in ‘22. Can- at- at this point, can the production run rate handle that? Can- can you meet those ex- high expectations?

Speaker 4:

Yeah. What we’re projecting, we’re confident we can- we can meet. And we are gonna be growing rapidly from here. And we start slowly here and then we grow rapidly. That’s the plan. And we feel confident we can do that.

Speaker 7:

And finally, Mark, how- how big of a challenge at this point is Trevor Milton, your founder, he- he is of course the largest shareholder and has a lot of voting control, about 20%, you overcame that to- to issue more stock recently. He’s about to face trial in September. I know you don’t wanna comment on all of that, but just in terms of what it’s allowing you to do here, the- some of the headwinds you still deal with on the reputational side and obviously when- when you’re fighting to- to change the rules like issue more shares.

Speaker 4:

We’re super focused on going forward. We’re grateful to have additional shares authorized now, to- got that approved. That gives us the flexibility to continue our growth rate going forward. And we’re super excited about what’s coming down the pipe for us. Our milestones in the next couple of quarters of next year are just super exciting. We- we- we can’t wait.

Speaker 7:

Mark Russell, thanks for giving us a- a status report. We appreciate it.

Speaker 4:

Thanks for having me on.

====================================================

Nikola (NASDAQ: NKLA) Q2 2022 Earnings Call & Webcast

[First used August 4, 2022]

Company Participants:

- Mark Russell, President & Chief Executive Officer

- Kim Brady, Chief Financial Officer

- Henry Kwon, Director of Investor Relations

Prepared Remarks

Mark Russell, CEO

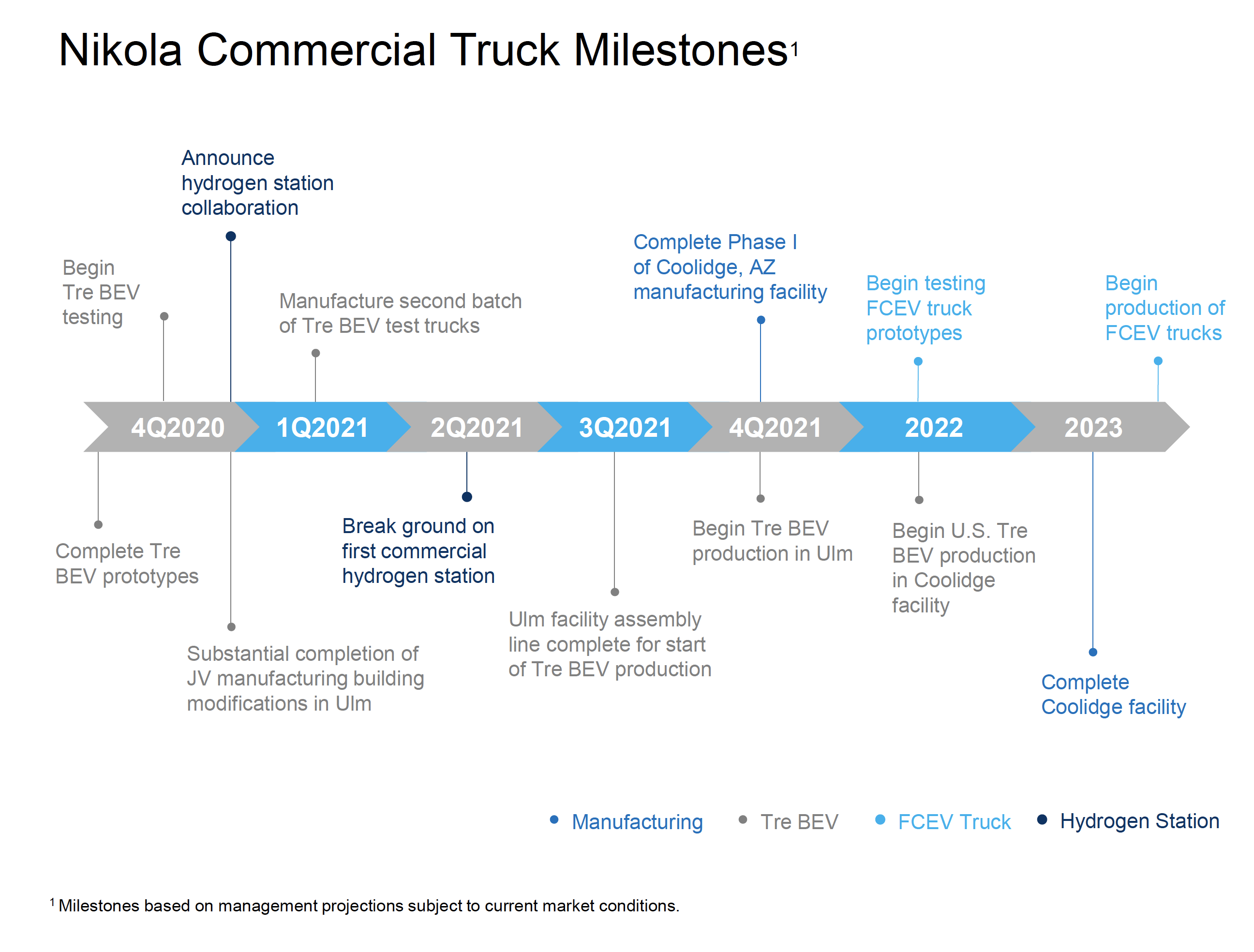

Thanks for joining us! Q2 was important for Nikola – our first quarter of generating revenue from the Nikola Tre BEV. We couldn’t have achieved this milestone without the extraordinary hard work and dedication of our outstanding team of people. We’re proud of what we’ve accomplished so far, and we’re so excited about continuing this drive to decarbonize heavy transport. Let’s start with things on the vehicle front.

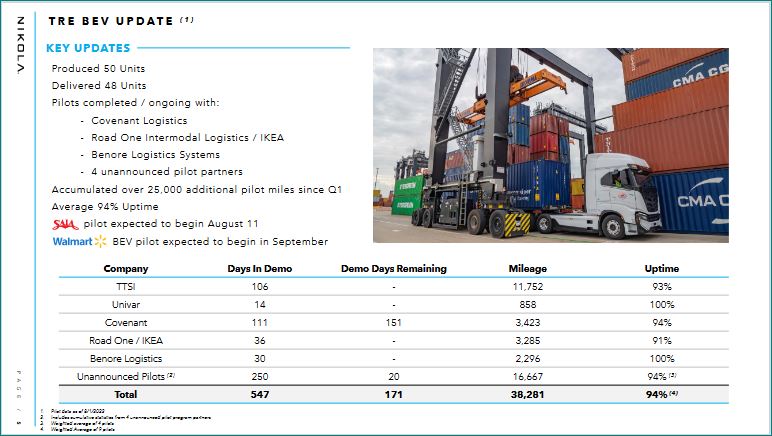

Tre BEV Update[Slide 4] We produced a total of 50 Nikola Tre BEVs in Coolidge, Arizona during the quarter, and we delivered 48 of those to our dealers around the country. Two were delivered just after the quarter end and they’ll be reported with Q3 shipments.

Our battery pack supplier Romeo continued to experience manufacturing challenges during the quarter, and we lost a total of 2 weeks of production at Coolidge due to delayed pack deliveries.

On the customer front, we have completed and we are continuing numerous successful pilot and demo programs, including several that have not been publicly announced. Notable among the public programs are TTSI, Biagi Brothers/Anheuser Busch, Univar, Road One/IKEA, Benore Logistics Systems, and Covenant, with SAIA starting this month, and Walmart in September. Average uptime for all Tre BEV’s in the field is an extraordinary 94% to date.

I’d like to highlight right now what it takes to actually takes to get a zero-emission truck into commercial service, hauling freight every day. I think this further validates Nikola’s long-standing focus on providing the total solution, including service, support and most importantly in this case, charging and fueling infrastructure.

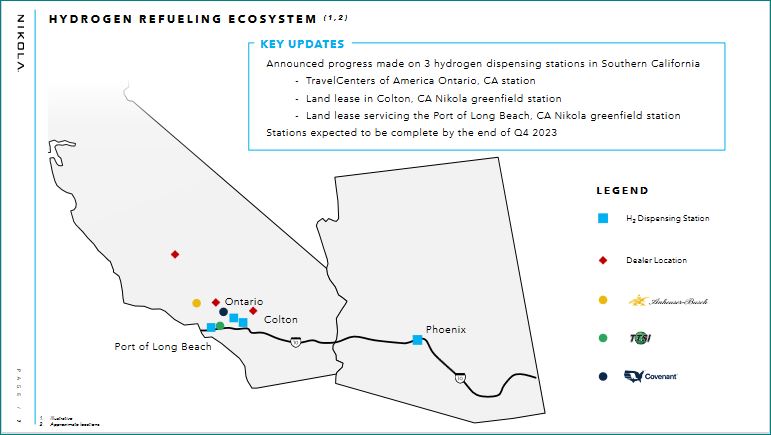

When you commit to using zero emission trucks you also are committing to the infrastructure they need to operate. Let’s use TTSI as an example. They’ve committed to a 100-truck fleet of 30 Tre BEV’s and 70 Tre FCEV’s. They are up and running with Tre BEVs and a Tre FCEV prototype by using mobile electric charging and mobile hydrogen fueling equipment that Nikola has helped provide. Nikola’s mobile charging trailers, and a temporary-to-permanent version that we call an E-Skid, as well as mobile hydrogen fueling systems we have helped develop, can get a customer started. But continuing to scale up to fleet-level infrastructure can require additional significant and permanent electric power for charging, and permanent heavy-duty infrastructure for hydrogen fueling, all located so that they work with existing operations. Here again, Nikola is helping to provide this critical and necessary infrastructure, as you saw in our announcement this morning of three commercial hydrogen dispensing station in Southern California. Lead time for this infrastructure varies by location, BUT it can be significant. For example, in addition to normal permitting and local approvals, if charging infrastructure at a given location requires an upgrade to power capacity, utility switchgear or substation infrastructure, the lead time can be up to a year or even longer. Lead times for hydrogen dispensing locations (mess up) similarly vary by location but generally are also more than a year. In some cases, this infrastructure lead time, along with any hesitancy or delay in committing to OR commencing construction, could be a limiting factor in the growth of customer zero-emission customer fleets.

Tre FCEV Update

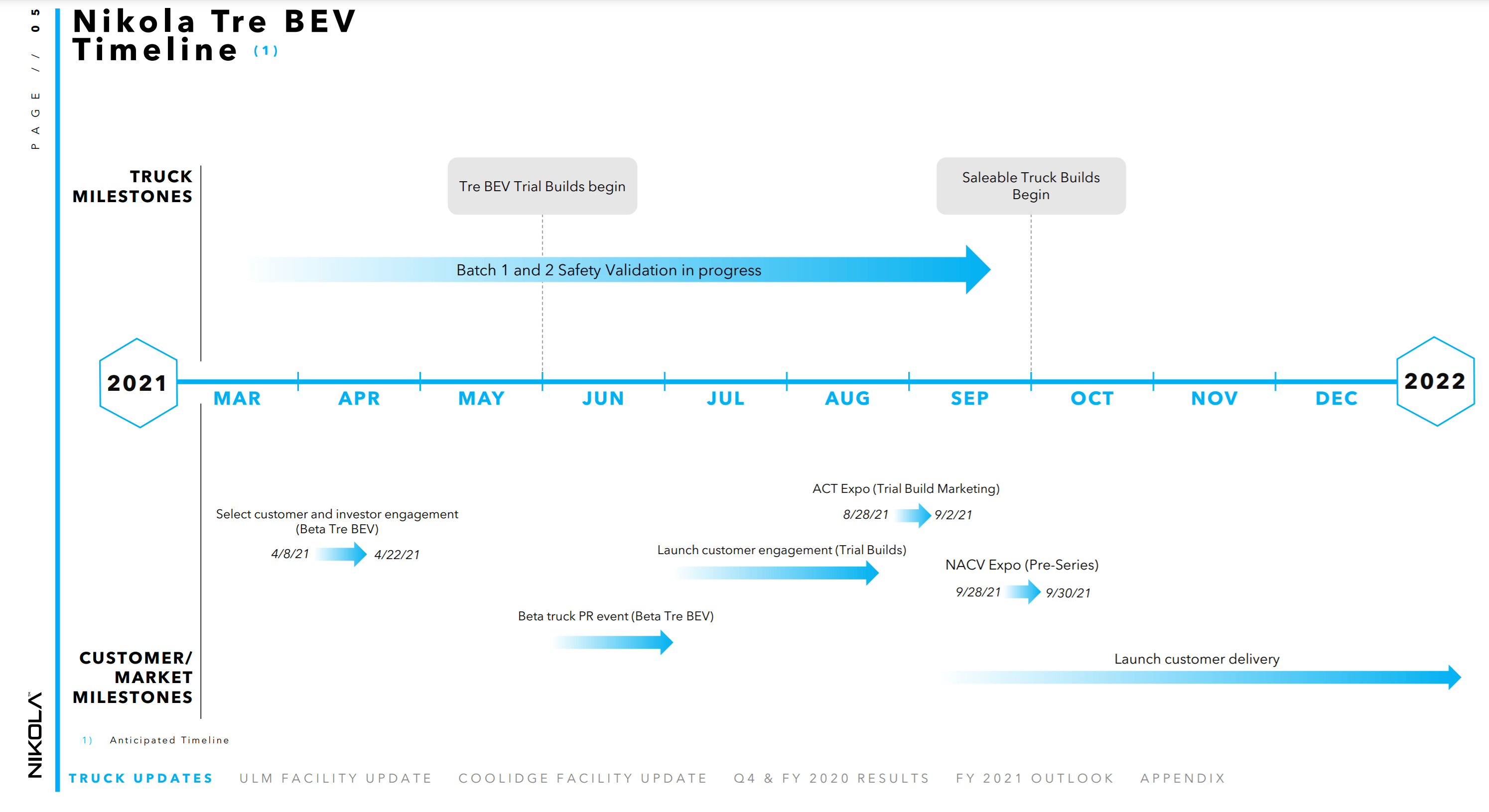

We began building the first batch of six Nikola Tre FCEV beta prototypes during Q2, which we expect to complete in August. The second batch of six Tre FCEV betas will start later this month and should finish by the end of Q3. The third batch will begin in Q3 and be completed by Q4 of this year according to plan. Specific changes from the alphas to betas include increased hydrogen storage capacity and improved efficiency of the fuel cell power module. These Beta trucks will enable further engineering development and performance validation testing. We’ll build THE gamma variants in Q1 for use in our own captive fleet and in additional customer pilots. We still expect to begin North American serial production of the Tre FCEV to begin in the second half of 2023.

Energy Business Commentary

[Slide 6] Moving on to the Energy. The land for our Arizona hydrogen hub is now under contract. We’ll announce the location after the closing, and then along with our partner TC Energy, we’ll break ground on Arizona’s first hydrogen production hub by the end of this quarter. Other hub locations we have announced so far including another partner project with TC Energy located in Crossfields, Alberta, and our project in partnership with Wabash Valley Resources in Indiana.

On the station and dispensing front, this morning we announced the progress made on 3 station locations in Ontario, Colton and Carson California. We’ve begun the permitting process and ordered long lead-time equipment for these stations. We expect they will be completed in Q4 2023.In addition to what we have publicly announced, there are numerous other production and dispensing projects in our development funnel that we will update you on when appropriate.

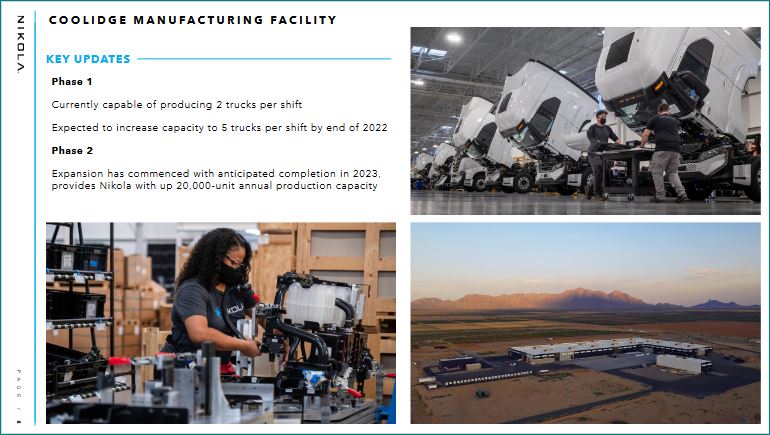

Progress Made at Nikola’s Coolidge, Arizona Manufacturing Facility

[Slide 7] We are on track to complete Phase 2 of our Coolidge, Arizona manufacturing facility by the end of Q1 2023, which will give us up to 20,000 units a year of nameplate capacity. The facility is capable of assembling both BEVs and FCEVs on the same line. We will also establish a line for assembly of our Bosch Fuel Cell Power Modules. Timing for Phase 3 of Coolidge will be announced at a future date, and that expansion will allow us to ramp production up to 45,000 units a year or more.

European JV Update

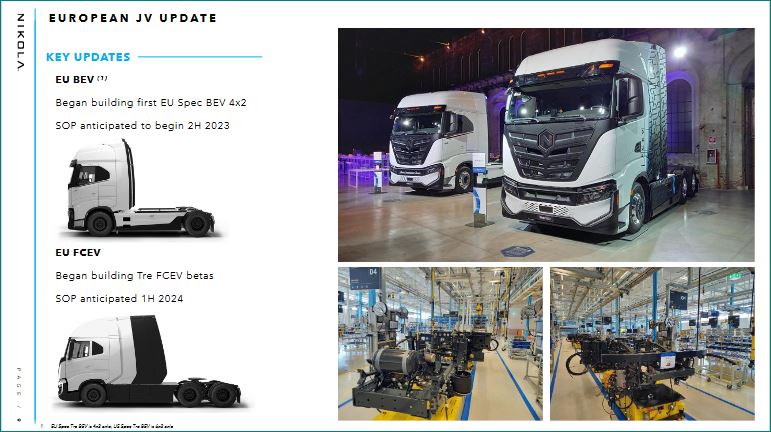

In June, our expanded European JV with IVECO began building the first EU Spec Tre BEVs. These are 4x2 variants that are targeted to the European market. The first 3 alpha builds are expected to be complete by Q3. We’ll then build 7 beta trucks during the third quarter for fourth quarter completion. Pre-series builds will take place during the second quarter of 2023, and we anticipate shipping the first production of EU Tre BEVs to customers in the second half of 2023.

During the second quarter, the JV also began building EU spec Tre FCEV betas. The build of the first batch of three trucks started in March and should be complete by the end of Q3. In July, we began building the second batch of 10 trucks, which should be complete by Q1 next year and EU spec Tre FCEV production is expected to begin in the first half of 2024.

The JV WITH IVECO originally was a contract manufacturing entity. However, Nikola and IVECO have now agreed to strategically expand the JV to include product development and vehicle engineering. This represents the maturing of our relationship with IVECO and the right next step for the JV to become more of an independent entity. Over to Kim now to take you through the numbers.

Kim Brady, CFO

Q2 Results

[Slide 12] Thanks, Mark, and good morning, everyone. There is a lot to cover today so let’s begin with the financial overview for the second quarter. In Q2, we reported revenues of $18.1 million on deliveries of 48 Tre BEVs and 4 MCTs. As Mark mentioned, we produced 50 Tre BEVs during the quarter at the lower end of our guidance, and two were delivered in the first week of July. The primary reason for our deliveries coming in at the low end of our guidance range was caused by two weeks of production losses in Q2 related to battery pack delivery delays from Romeo. Let’s go through the numbers, and I will outline what drove them and what we expect in the second half.

First, regarding Gross margin, the Tre Bev trucks we produced and delivered in Q2 are the most expensive battery trucks we will ever build. The objective was to do whatever it took to ensure the components were available at the assembly line to start the build of Tre Bev trucks. Nonetheless, there are a few items that we could have better foreseen in Q2 that we ultimately did not.

[Slide 14] There were two contributing factors to our gross margin guidance coming in lower than expected, the first being shipping and freight costs. We recorded $13.7 million in inbound shipping, freight, and duty expenses for the quarter, representing approximately 29% of our Cost of Revenues. Of this $13.7 million, $3.3 million represented duties and taxes, while $10.4 million came from freight expenses. Of the $10.4 million, roughly 80% of expenditures were expedited air freight. The impact on the Cost of Revenues was magnified because we purchased and received more components than we used in production due to the production delays that we referenced earlier. Thus, the impact of these two factors on our gross margin at our current revenue level was more pronounced than if we had already scaled. We had not budgeted this level of impact in our guidance, and it is something we will be better prepared for in future quarters.

To reduce our freight cost burdens going forward, we have started shifting the shipment of most components to ocean freight. We are also accelerating our localization efforts of certain components from the EU to North America. From these two actions, we expect a meaningful decrease in per unit inbound shipping and freight costs and a gradual easing of inbound freight cost pressure on our gross margin.

Next, let me provide some perspective on the quarterly inventory write-down of $7.5 million, representing a $4.1 million sequential increase. In 2Q, the Net Realizable Value, or “NRV”, adjustment represented 96% of the write-downs. As you may be aware, our inventory costs have risen in line with inflation and significantly more for battery cells, and Q2 was no exception. Under US GAAP, when our inventory value rises above a truck’s expected selling price or NRV, a reserve adjustment is required. This situation was compounded by holding more inventory than we would have held if no production delays occurred.

If you notice on the financial summary table in the deck, R&D expenses decreased by $11.5 million from Q1 to Q2. This is because prior to our commercial deliveries in Q2, manufacturing expense items, typically part of the Cost of revenues were recognized as R&D expenses, under US GAAP, including inbound shipping and freight, inventory write-downs, and D&A expenses.

Q2 EBITDA sequentially fell by $14.0 million to negative $163.6 million. We think it makes better sense to look at our results at the EBITDA level because of the reclassification items in Q2 regarding costs. We believe it is a better quarter-over-quarter comparison to focus on costs before interest and taxes this quarter given what they imply about our cash burn rate.

Equity in a net loss of affiliates decreased by $1.5 million in the second quarter to $1.3 million, driven by $1.2 million equity in net loss of Nikola IVECO Europe. As we shared in our Q1 earnings call, our European joint venture with IVECO now engages in product development and vehicle engineering in addition to its contract manufacturer role.

We recorded a $173.0 million net loss for the quarter, and basic and diluted Net Loss per share came to $0.41. Basic and diluted Non-GAAP Net Loss per share came to $0.25, beating consensus estimates.

On a Non-GAAP basis, adjusted EBITDA came to a negative $94.3 million. Adjusted EBITDA excludes (i) $54.8 million in stock-based compensation, (ii) $13.0 million for legal expenses to pay Mr. Milton’s attorneys’ fees under his indemnification agreement, (iii) $1.3 million for equity in net loss of affiliates, mainly from our IVECO JV in Europe, and (iv) a net $0.2 million loss for the revaluation of financial instruments including warrant liabilities and derivatives.

[Slide xx] On the Balance Sheet, we ended the second quarter with $529.2 in cash and equivalents, including restricted cash, up from $385.1 million at the end of Q1. The $144.1 million increase came from i) the $200 million private placement of convertible notes we placed in June with Antara Capital and ii) $50 million proceeds from the issuance of a promissory note collateralized by Nikola-owned equipment and restricted cash.

In addition to the $529.2 million in cash and equivalents, we still have $312.5 million available liquidity through our two equity lines with Tumin Capital. At the end of June, we have total liquidity of approximately $841.8 million, up from $794.0 million at the end of Q1. As of the end of June, we have sufficient capital to fund our business for the next 12 months of operations.

Given our target of keeping 12 months of liquidity on hand at the end of each quarter, we will continue to seek the right opportunities to replenish our liquidity on an ongoing basis while trying to minimize dilution to our shareholders. We are carefully considering how we can potentially spend less without compromising our critical programs and reduce cash requirements for 2023.

We will provide you with detailed guidance for 2023 on our Q4 2022 earnings call, but for now, a good way to think about how we can achieve our goals is to consider it in the context of our ongoing CAPEX requirements at the Coolidge plant.

For example, with the completion of Phase 2 by the end of Q1 2023, our Coolidge plant will achieve a design capacity of 20k units. While we have not made our 2023 production plans public, the 20k unit in annual capacity will be sufficient to allow us to achieve our 2023 and 2024 production targets. 2023 Coolidge manufacturing facility-related CAPEX for Phase 3 is approximately $345 million, including a paint line. Delaying this phase of our expansion to 2024 allows us to reduce our 2023 cash needs and fund-raising targets in 2022.We will continue to monitor market conditions and remain opportunistic about raising capital.

Q3 Guidance

Moving on to our Q3 guidance. We expect to deliver 65 – 75 Nikola Tre BEVs for $21.1 to $24.4 million in revenues in Q3. We anticipate our gross margin to be between -240% and -250%. As we explained in the Romeo merger call, we’ve agreed to provide Romeo with interim funding to ensure continued operations. The funding comes in two parts: i) up to $20 million in a temporary price increase for each pack delivered through transaction close, plus ii) $15 million in a senior secured note. The temporary price increase for the packs will weigh down our Q3 and Q4 gross margin. We expect, however, to make notable improvements in inbound shipping and freight costs and benefit from the operating leverage effect of delivering more vehicles on labor costs. Without the Romeo merger impact, the gross margin would approximate -150% to -160%.We anticipate a range of $80—$85 million in R&D expenses and $80 – $85 million in SG&A, including roughly $58 million in stock-based compensation. CAPEX for Q3 should be $85 to $90 million, as we expect station CAPEX, FCEV tooling, and Hydrogen Hub spending to catch up.

FY22 Guidance

Regarding fiscal 2022 guidance, we have not revised the existing 300-500 truck delivery. Still, given the battery charging infrastructure challenges Mark mentioned, we are more likely to hit the lower end of that guidance range.

The merger with Romeo will introduce new elements to our P&L in several ways, especially in the short run, which I will discuss in some detail. We plan to revise our full-year financial guidance post transaction close and share it with you in our Q3 earnings release.

We are currently working on the merger Pro-forma which will serve as the basis for our new full-year guidance. As many of you may anticipate, the merger with Romeo will cause our full-year guidance to change. This is because i) negative gross margin impact from the temporary pack price increase in Q3 and to a lesser extent in Q4, ii) negative gross margin impact from existing Romeo customer contract run-off, iii) incremental R&D and SG&A expenses of Romeo post-merger, and iv) transaction costs and purchase accounting adjustments that may further impact our Q3 and Q4 OPEX. We will come back to you with our revised full-year guidance at our Q3 earnings call.

While 2H will be challenging from a gross margin angle, we expect 30-40% cost reduction benefits for the non-battery cell-related pack cost by the end of 2023. Key cost-cutting initiatives will involve switching from machined to casted pack enclosures and using the combined purchasing power of the merged entity to optimize the supply chain. We believe this is achievable because we have had about 10 manufacturing engineers working on-site at Romeo since early 2022 to support Romeo’s production. With a good, accumulated understanding of Romeo’s operations, we have identified several areas of operational improvements that will begin to be implemented immediately following transaction closing. Longer term, we are targeting up to $350 million in annual battery pack cost savings by 2026.

Supply Chain

Regarding our supply chain, part shortage challenges still remain, although the visibility and availability of components have somewhat improved. But we are not out of the woods yet. We previously stated that one of our biggest constraints was a consistent supply of modules and packs from Romeo. Our proposed merger with Romeo takes us a step closer to ensuring a dedicated and consistent supply. Perhaps a more significant challenge that faces us and the industry is inflation and its impact on margins. We are subject to a commodities pricing increase from LG, which has increased our battery cell price by approximately 30%. The adjustment is calculated every six months based on the price movement of certain battery cell chemistry metals for the previous 6 months. We are uncertain when the critical metal prices for battery cells will normalize and come back down to the pre-Ukrainian War prices and how much of that increase we can successfully pass on to our customers. This is something we are actively grappling with, and unfortunately, we have no control when it comes to cell prices.

This concludes our prepared remarks. We will use the remainder of the time to address your questions. But before we open the line to analyst questions, we would like to take this opportunity to answer some questions from our retail shareholders. Henry?

Henry Kwon, Director, IR

Thank you, Kim. The first question from our individual investors is

When can I see Nikola on the road? I have never seen any of your vehicles on the street. Why?

Mark: It is exciting to see the trucks on the road! More and more are out there hauling freight and are being sighted every day. Pictures and video are increasingly showing up online. You have a better chance of seeing one if you are in one of our target launch geographies, such as California. Good luck with your Tre spotting.

Henry: The next question from our investors is

Considering the number of EVs entering the market in the next several years, how is Nikola planning to differentiate itself to ensure long-term success? Tesla was the first to market, Rivian secured a contract w/Amazon, and Ford has the capacity to ramp production quickly. Nikola has…?

Mark: First, we should clarify that unlike these companies we build only U.S. Class-8 and European Heavy Duty commercial trucks, addressing short, medium, and long-haul commercial freight segments. So that is an immediate difference. We are one of the first OEMs in the market for Class 8 BEVs, and We are likely be the first OEM to commercialize Class 8 FCEVs. But in the long run, what will really differentiate Nikola is energy infrastructure. On slide 3 of the deck, you can see that the total addressable market for just Hydrogen is bigger than the market for trucks.

Henry: Thank you, Mark. The next question coming from our individual investors addresses a similar topic…

What plans do you have to excite investors about what your company is bringing to the table? Do you have a plan to become profitable? If so, when?

Kim: I think Mark has already discussed Nikola’s value proposition, so let me share some thoughts about achieving profitability. During our Analyst Day in March, we stated that we are looking to achieve a positive gross margin for our Tre-BEVs by the end of 2023 and the end of 2024 for our FCEVs. Under our basic roadmap, we would like to get to positive EBITDA by the end of 2024.

The primary assumption behind this roadmap has been that as we continue to scale, we should be able to spread our fixed costs over a greater volume and reduce our BOM costs.

From our current vantage point, inflation remains a great unknown that makes our path to a positive gross margin a challenge, especially the cost of battery cells price. While OEMs have sought to raise the fee in line with inflation, it remains unclear to what extent we may be able to pass through that increase. So operating leverage will be one of the biggest factors driving our future gross margin, but potential headwinds from the impact of prolonged inflation could extend our existing timeline.

Henry: The next question from our individual investors is

If proposition 2 is passed, will you use the extra shares for capital immediately, diluting the stock, or on an as-needed basis?

Kim: A great question because it allows us to discuss something here on a topic on which many investors had asked us for clarification during the voting process. As you may know, Proposition 2 passed, but we feel that this is still a very relevant question because many people were not aware of what our committed share count was for coming into the end of Q2.

While our fully diluted number of shares stood at 495 million on June 30, if we included the committed shares of options, RSUs, and warrants as well as reserved shares for our ELOC and Convertible Notes, the share count came very close to 570 million shares. This left us with a sufficient number of shares to acquire Romeo without having to come to market so the increase in the authorized number of shares that was just approved will not be used to fund our merger with Romeo.

Having said that, the 200 million share increase in the authorized number of shares will leave us with the flexibility to pursue future capital raising opportunities.

NKLA, (Trade) has reported earnings of -0.25 per share versus last year's earnings of -0.2 per share.

/C O R R E C T I O N -- Nikola Corporation/

BY PR Newswire

— 9:05 AM ET 08/04/2022

In the news release, Nikola Corporation Reports Second Quarter 2022 Results, issued 04-Aug-2022 by Nikola Corporation (NKLA) over PR Newswire, we are advised by the company that the second bullet after the headline should read "Reported revenues of $18.1 million, GAAP net loss per share of $0.41, and non-GAAP net loss per share of $0.25" rather than "Reported revenues of $18.1 million and adjusted net loss per share of $0.25" as originally issued inadvertently. Additionally, the second paragraph of the H2 Dispensing Station Updates section has been updated to: "We also executed a land lease in Colton, California to build a greenfield hydrogen dispensing station, and identified a parcel servicing the Port of Long Beach to build a greenfield hydrogen dispensing station. We anticipate the stations will be complete by Q4 2023." The complete, corrected release follows:

https://eresearch.fidelity.com/eresearch/evaluate/news/basicNewsStory.jhtml?symbols=NKLA&pageno=&storyid=202208040905PR_NEWS_USPR_____LA36215

https://www.prnewswire.com/news-releases/nikola-corporation-reports-second-quarter-2022-results-301599821.html

right from the horse's mouth

A U G U S T 4 , 2 0 2 2

Q 2 -2 0 2 2- E A R N I N G S -CALL

KEY UPDATES

Announced progress made on 3 hydrogen dispensing stations in Southern California

- TravelCenters of America Ontario, CA station

- Land lease in Colton, CA Nikola greenfield station

- Land lease servicing the Port of Long Beach, CA Nikola greenfield station

Stations expected to be complete by the end of Q4 2023

P A G E / 1 8

2 0 2 2 - M I L E S T O N E S

Milestones

Deliver 300 – 500 production Nikola Tre BEVs to customers

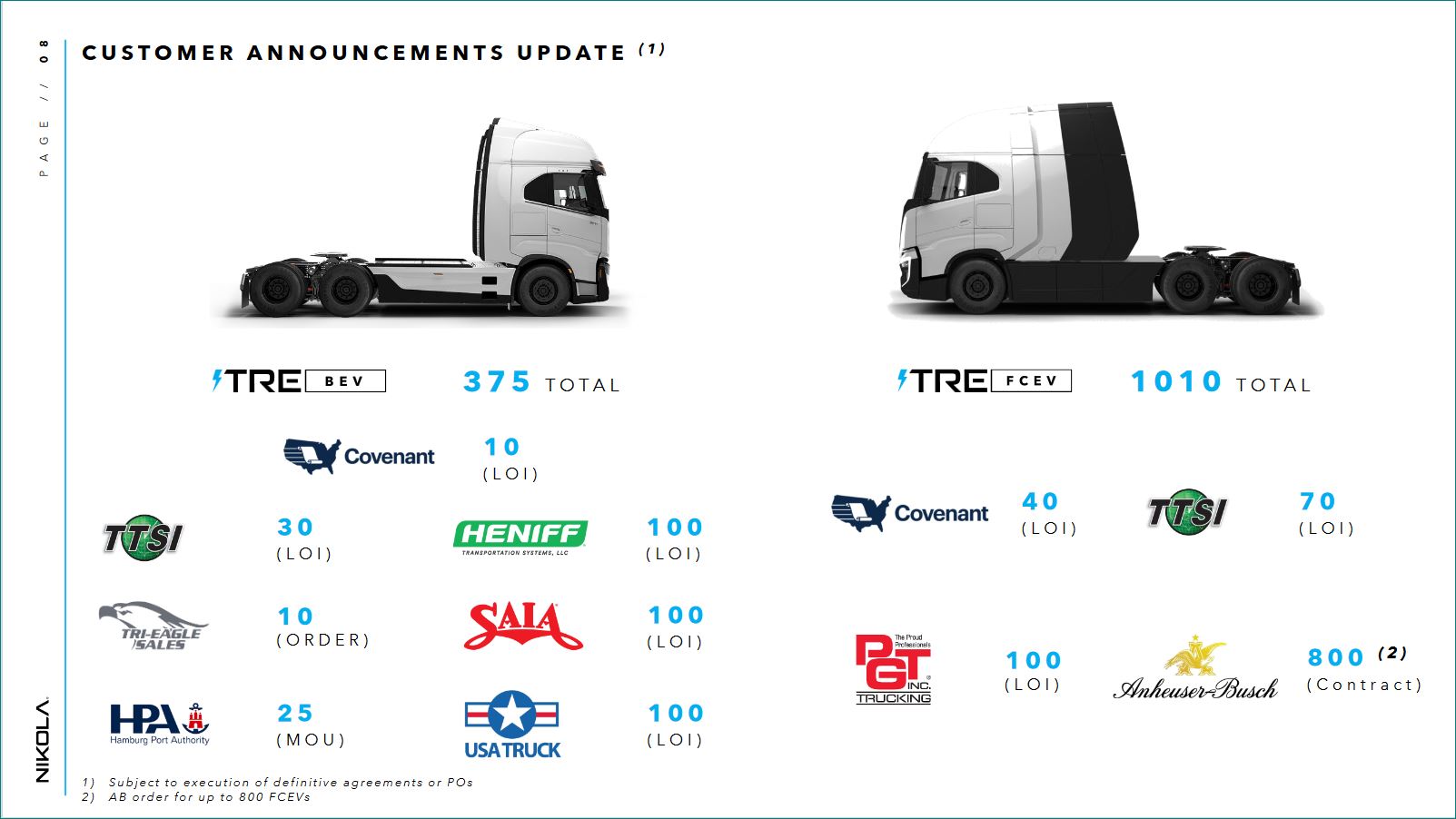

Successful pilot testing of Tre FCEV alpha trucks with customers (Anheuser-Busch, TTSI, and others)

Build, Test, and Validate FCEV beta trucks

Announce location, break ground, and commence construction of the first hydrogen production hub in Arizona

Announce two or more dispensing station partners in California

https://d32st474bx6q5f.cloudfront.net/nikolamotor/uploads/investor/presentation/presentation_file/51/3._2022.08.03_Q2_2022_Earnings_Call_Deck_v23.pdf

https://nikolamotor.com/investors

PHOENIX – May 5, 2022 -- Nikola Corporation (Nasdaq: NKLA), a global leader in zero-emissions transportation solutions, today reported financial results for the quarter ended March 31, 2022.

“During the first quarter, we reached a significant milestone with the start of serial production for the Nikola Tre BEV at our Coolidge, Arizona manufacturing facility and are currently delivering saleable trucks to dealers for customer deliveries,” said Mark Russell, Nikola’s Chief Executive Officer. “We look forward to scaling production and delivering 300 – 500 production vehicles to customers this year.”

Nikola Tre BEV Update

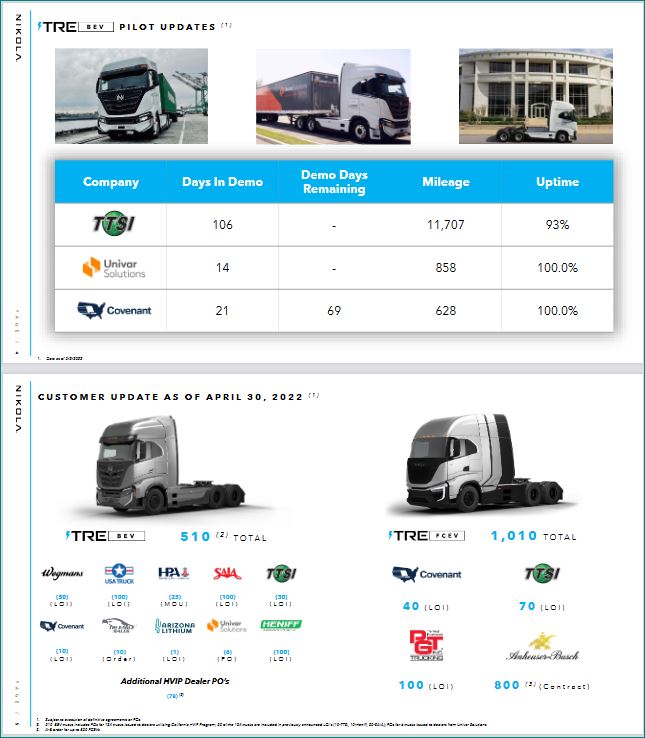

During the first quarter, the final 10 of a total fleet of 40 pre-series Tre BEVs came off the line in Coolidge, Arizona. Pre-series trucks continue to be used in customer pilots, dealer demos, and internal R&D testing. On April 29, we successfully completed our first Tre BEV customer pilot with TTSI. We also successfully completed a 14-day pilot with Univar Solutions (NYSE: UNVR). We are currently undergoing pilot testing with several other customers, including Covenant Logistics (Nasdaq: CVLG).

On March 21, 2022, we began serial production of the Nikola Tre BEV in Coolidge, Arizona. We began shipping saleable Tre BEVs to dealers in April for customer deliveries. Customer POs for 134 trucks have been issued to our dealers utilizing California HVIP. To date, we have received POs, LOIs, and MOUs for a total of 510 Nikola Tre BEVs.

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=169320139

Link to Nikola CEO, Mark Russell interview on CNBC Closing Bell earlier today https://www.cnbc.com/video/2022/08/04/the-hydrogen-production-tax-credit-would-be-make-our-forecasts-even-better-says-nikola-ceo.html

"Tax credit would make our forecasts even better" says Nikola CEO.

Mark Russell, Nikola CEO, joins ‘Closing Bell’ to discuss the vehicle production process, why Nikola is sticking with its current guidance and what the company’s seeing around consumer demand.

2 hrs ago

so 50 in Q2 60 in Q3 and then 200-400 in Q4 - Nice (including some FCEV)

at 10 per shift that is 600 per full quarter

Then in 2023 Phase 2 opens and they can really rock, I can't recall the target daily rate they expect with Phase 2 open but it will allow parallel FCEV and BEV I believe - need to look at Bears Workshop video again.

They reaffirmed guidance for 500-600 tre’s for 2022

5 Units a shift by November means their Q4 production target will be 3 or 4 times Q2 and Q3's.

and that's before Phase 2 opens but includes capability to put some FC models on the production line.

Nikola Corporation Reports Second Quarter 2022 Results

Published August 04, 2022

https://nikolamotor.com/press_releases/nikola-corporation-reports-second-quarter-2022-results-191

Nikola Corporation Reports Second Quarter 2022 Results

August 04 2022

https://ih.advfn.com/stock-market/NASDAQ/nikola-NKLA/stock-news/88760082/nikola-corporation-reports-second-quarter-2022-res

Summary

- Produced 50 Nikola Tre BEVs in Coolidge, Arizona, and delivered 48 to dealers

- Reported revenues of $18.1 million and adjusted net loss per share of $0.25

- Cash & Restricted Cash of $529.2 million and $312.5 million remaining ELOC commitment totaling $841.8 million in total liquidity at the end of Q2, up from $794.0 million in Q1

- Announced station progress in California in the cities of Ontario, Colton, and a location servicing the Port of Long Beach

- Stockholders approved proposal 2 increasing authorized shares from 600 million to 800 million

PHOENIX, Aug. 4, 2022 /PRNewswire/ -- Nikola Corporation (Nasdaq: NKLA), a global leader in zero-emissions transportation solutions, today reported financial results for the quarter ended June 30, 2022.

"Our momentum continued during the second quarter as we began delivering production vehicles to dealers and recognizing revenue from the sale of our Nikola Tre BEVs," said Mark Russell, Nikola's Chief Executive Officer. "We are committed to executing on our second half milestones."

We reported $18.1 million in revenues on deliveries of 48 Tre BEVs and four (4) Mobile Charging Trailers (MCT) in Q2. Two (2) additional Tre BEVs were delivered in the first week of July, which will be reported as part of Q3 revenues. We increased our total liquidity to $841.8 million in Q2 from $794.0 million at the end of Q1. As mentioned in May, we also successfully raised $200 million in a private placement of convertible notes during the quarter.

Nikola Tre BEV Update

During the second quarter, we produced 50 Nikola Tre BEVs and delivered 48 of those to dealers. We also continued pilot testing with a number of fleets to help facilitate additional orders and build our backlog. Pilots completed / ongoing include:

- TTSI (Complete) – 106 days / 11,752 miles / 93% uptime

- Univar Solutions (Complete) – 14 days / 858 miles / 100% uptime

- Covenant Logistics (Extended & Ongoing) – 111 days / 3,423 miles / 94% uptime

- RoadOne / IKEA (Complete) – 36 days / 3,285 miles / 91%

- Benore Logistics Systems (Complete) – 30 days / 2,296 miles / 100% uptime

*MCTs are merchandised goods sourced from external suppliers and therefore are not a part of our manufacturing costs.

Nikola Tre FCEV Program Update

In the second quarter, we began Tre FCEV alpha pilot testing with TTSI in Southern California. As of today, the trucks have accumulated over 3,800 miles. We expect to begin FCEV pilot testing with Walmart in Southern California on August 22.

During the second quarter, we began building the first Tre FCEV betas. The first batch of betas are scheduled to be complete by the end of August. We expect to build two additional batches of Tre FCEV betas by the end of the fourth quarter. Beta trucks incorporate learnings from the alpha trials and will be used for engineering and product development.

Coolidge, Arizona Manufacturing Facility Update

We are ramping up production capacity in Coolidge, Arizona. We expect to increase our throughput to five units per shift by November of this year. Phase 2 expansion is underway and on track to be completed by Q1 2023.

H2 Dispensing Station Updates

On August 3, we announced we had made significant progress in partnership with TravelCenters of America on the first hydrogen dispensing station in Ontario, California. We have executed the definitive agreement, agreed on the station design, and have ordered key equipment.

We also executed a land lease in Colton, California to build a greenfield hydrogen dispensing station, and entered into an agreement to lease a parcel servicing the Port of Long Beach to build a greenfield hydrogen dispensing station. We anticipate the stations will be complete by Q4 2023.

Nikola - IVECO European JV

In June, together with IVECO, we agreed to expand our 50/50 European JV to include engineering and product development. During the second quarter, the JV entity began building the first EU Tre 4x2 BEV alphas. Production for EU Tre BEV is expected to commence in the second half of 2023. The JV also started building EU Tre FCEV betas, which are expected to begin production in the first half of 2024.

Nikola Announces Locations of Three California Hydrogen Dispensing Stations, Continued Scaling of Infrastructure

August 04 2022

https://ih.advfn.com/stock-market/NASDAQ/nikola-NKLA/stock-news/88759179/nikola-announces-locations-of-three-california-hyd

PHOENIX, Aug. 4, 2022 /PRNewswire/ -- Nikola Corporation?(Nasdaq: NKLA), a global leader in zero-emissions transportation and energy infrastructure solutions,?today announced the locations of three California hydrogen stations to advance and scale up its long-term hydrogen distribution solutions to service market demand. Nikola's integrated energy and zero-emissions truck portfolio will be underpinned by developing hydrogen supply and refueling infrastructure, an essential step in helping to decarbonize the heavy-duty transport sector.

Through the combined efforts of Nikola’s truck and energy teams, the company links hydrogen fuel cell electric vehicles with hydrogen production hubs and dispensing stations. These stations are an important step in the delivery of a broader array of hydrogen fueling solutions to the heavy-duty trucking industry.

The three California refueling stations and logistics infrastructure will be located in the cities of Colton, Ontario and a location servicing the Port of Long Beach. To further support truck demand, plans for additional stations are in progress and will be announced in the near future.

California is a launch market for Nikola and these stations will support key customers and advance the state's efforts to decarbonize the transport sector.

"This marks an important step in Nikola's ability to deliver innovative solutions and the infrastructure needed to decarbonize the transportation industry," says President, Nikola Energy Pablo Koziner. "Our hydrogen refueling stations, along with a comprehensive energy supply, will provide customers the support needed to transition their fleets to zero-emissions."

The Ontario location is part of Nikola's previously announced collaboration with TravelCenters of America.

"TA is committed to providing viable infrastructure to support the nation's shift toward alternative fuels, and this collaboration with Nikola reflects our ongoing commitment to this goal," said Jon Pertchik, Chief Executive Officer of TravelCenters of America. "The success of the transportation industry's transition toward alternative fuel adoption is dependent, in part, on collaborations like this."

There are a number of distribution centers in the city of Colton, making it an ideal location for future Nikola FCEV customers.

"The establishment of a 'clean fuel' facility for heavy-duty commercial vehicles, such as semi-trucks, is a huge step forward in seeing the trucking industry move towards these types of vehicles. Actions like these are building blocks to cleaner air for Colton residents and the surrounding region and we are proud to support initiatives that align with our vision," said Mario Suarez, Planning Manager, City of Colton, California.

The ports of Long Beach and Los Angeles are major global commercial transportation hubs and are focused on leading decarbonization. Our station servicing port customers will be a critical anchor of our hydrogen dispensing infrastructure.

"The Nikola hydrogen refueling stations represent an important step forward to enable zero-emissions logistics solutions in Southern California. The Port of Long Beach station is an ideal location to support ocean drayage solutions for TTSI and other logistics providers," said Mike Bible, Chief Executive Officer of TTSI. "TTSI is excited about the prospects of hydrogen fuel cell technology as a viable solution to decarbonize the freight trucking industry."

Nikola is bringing comprehensive zero-emission heavy-duty trucking solutions to market. Through the combined efforts of Nikola's truck and energy teams, the company links hydrogen fuel cell electric vehicles with hydrogen production hubs and dispensing stations. These stations are an important step in the delivery of a broader array of hydrogen fueling solutions to the heavy-duty trucking industry.

ABOUT NIKOLA CORPORATION

Nikola Corporation is globally transforming the transportation industry. As a designer and manufacturer of zero-emission battery-electric and hydrogen-electric vehicles, electric vehicle drivetrains, vehicle components, energy storage systems, and hydrogen station infrastructure, Nikola is driven to revolutionize the economic and environmental impact of commerce as we know it today. Founded in 2015, Nikola Corporation is headquartered in Phoenix, Arizona. For more information, visit www.nikolamotor.com or Twitter @nikolamotor.

IS THIS REALLY A GLIMPSE OF THE FUTURE?

Posted Aug 3, 2022

Flint Creek Transport

Due to limitation on number of posts, I'll post the following two battery related articles in one post:

1) Nancy Pelosi’s trip to Taiwan creates tension with Tesla battery supplier

By Maria Merano

Posted on August 2, 2022

https://www.teslarati.com/tesla-catl-battery-factory/

Tesla battery supplier Contemporary Amperex Technology Co. Ltd (CATL) decided to delay its plans to build a battery factory in North America after Nancy Pelosi’s trip to Taiwan.

Earlier this year, CATL started scouting sites across North America for its $5 billion cell plant. The Chinese battery supplier was considering sites in Canada and Mexico, capable of producing up to 80 GWh per year. In July, Teslarati reported that CATL narrowed its choices to two locations in Mexico.

However, Bloomberg sources recently stated that CATL plans to delay its battery factory plans until September or October. According to people familiar with the matter, U.S. House Speaker Nancy Pelosi’s visit to Taiwan might have created tension amid sensitive times between the United States and China.

WHY IS PELOSI’S VISIT CREATED TENSION

China considers Taiwan as part of its territory. During her visit, Nancy Pelosi’s visit seemed to reaffirm Taiwan’s sovereignty as an independent nation. She also hinted at the political ties between Taiwan and the United States.

“Today, our delegation … came to Taiwan to make it unequivocally clear we will not abandon our commitment to Taiwan and we are proud of our enduring friendship,” Pelosi said while standing in the presidential office in Taipei.

The US House Speaker is the highest-ranking US politician to visit Taiwan in the last 25 years. China issued a statement saying that Pelosi’s visit would have “severe impact” on US-China relations. It considers her visit as “provacative.” China reportedly responded to Pelosi’s visit by launching exercises and targeted military operations around Taiwan.

======================================================

2) Romeo Power enters long-term supply agreement with LG Energy Solution for 8GWh of Li-ion cells through 2028

13 August 2021

https://www.greencarcongress.com/2021/08/20210813-romeo.html

Romeo Power, a developer of electrification solutions for complex commercial vehicle applications, has entered into a long-term supply agreement for lithium-ion battery cells with LG Energy Solution, Ltd., a Tier 1 battery cell and materials manufacturer.

Under the agreement, LG Energy has committed to supplying cells to Romeo Power that equal 8 GWh of energy through 2028. Romeo Power expects to use the allocated cells to manufacture battery packs for approximately 29,000 electric vehicles sold or operated by its customers.

Romeo Power will facilitate LG Energy’s build of an additional assembly line in Ochang, Korea through a recoupable pre-payment of $64.7 million. The agreement was approved by both Boards of Directors and became effective on 10 August 2021.

Romeo Power’s suite of advanced hardware, combined with its innovative battery management system, delivers safety, performance, reliability and configurability. Romeo Power’s 113,000 square-foot manufacturing facility brings its flexible design and development process inhouse to pack what it says are the most energy-dense modules on the market.

Electric semis might get up to $40,000 credit under reconciliation bill moving through Congress

By Stephen Edelstein

AUGUST 3, 2022 8

https://www.greencarreports.com/news/1136707_electric-semis-40-000-credit-reconciliation-bill-congress

As Congress moves to extend and expand the federal EV tax credit for passenger cars, it's also considering a bill that would add a first-ever tax credit for electric commercial vehicles.

As described in a blog post from the Union of Concerned Scientists (UCS), the current version of the bill includes a tax credit of up to $7,500 for vehicles with a gross vehicle weight rating (GVWR) of less than 14,000 pounds, including pickup trucks and vans, and up to $40,000 for larger vehicles like semi trucks and garbage trucks.

The bill also sets out a minimum battery-pack size of 7 kwh for sub-14,000-pound GVWR vehicles and 15 kwh for larger vehicles. As with the current passenger-car tax credit, vehicles with larger packs will likely receive a larger credit.

In addition to the incentives, which would run through 2032, the bill also includes $1 billion to fund electric heavy-duty commercial vehicles (including school buses) and infrastructure, and $3 billion for the electrification of the new United States Postal Service delivery fleet and associated charging infrastructure.

The commercial-truck incentives are part of the same bill and legislation package that might potentially re-up the EV tax credit to lift the 200,000-vehicle ceiling, make the $7,500 credit a point-of-sale one, and add $4,000 for used EVs. And it could have a comparably-large impact on emissions.

Despite accounting for only 10% of vehicles on U.S. roads, heavy-duty commercial vehicles are responsible for 28% of greenhouse gas emissions, 45% or nitrogen-oxide emissions, and 57% of fine particulate emissions, according to the UCS. California has already issued a mandate for electric trucks, aiming for 100% EV sales by 2045.

Some manufacturers have started marketing all-electric commercial trucks. Megawatt charging for big trucks has just been formalized, and models utilizing it might be available in the next year or two. Research suggests incentives could dramatically accelerate that market.

Real-world testing has verified the cost savings of electric trucks—and helped realize that electric trucks lower the level of driver fatigue. That's what Daimler found after a test fleet of electric trucks racked up one million miles with actual customers. Operating costs for electric trucks can be 14% to 52% lower, and repair costs 40% lower, than current diesel trucks, the UCS estimates.

Incentives or not, a broader coalition of states is preparing to mandate more zero-emission commercial vehicles. Seventeen states, the District of Columbia, and Canada's Quebec province recently stood by a plan to electrify 30% of trucks and buses by 2030—despite a legal challenge that's coming, partly, from inside the industry that's simultaneously talking up EVs and looking for the credit.

Teifhals, per the recent press release, the exchange rate is set at 0.1186 NKLA shares per RMO shares (Source https://nikolamotor.com/press_releases/nikola-agrees-to-acquire-romeo-power-to-bring-battery-pack-engineering-and-production-in-house-189). Also, I believe that the deal has high probability of going through, since the deal is mutually beneficial to both Nikola Motors and Romeo Power, as reflected by the fact that both have experienced a similar rise in share price (percentage wise) since the deal was announced.

Relevant excerpt from the press release:

Wouldn’t the RMO shares get converted at NKLA at a ratio. like 1 NKLA for every 7 RMO? At the trading price when the deal closes?

My strategy of selling NKLA and buying RMO shares, appears to be paying off so far. Ultimately, it will depend on whether or not the deal goes through, and I put a high probability that it does go through. Opinions are welcomed. Thank you in advance.

see what the extra 200m shares will help build out - phase 2 starting

Nikola Earnings Previews

Earnings Previews: Alibaba, ConocoPhillips, Nikola, Paramount Global

Paul Ausick

August 2, 2022 1:28 pm

Over the past 12 months, electric and hydrogen-powered truck maker Nikola Corp. (NASDAQ: NKLA) has seen its share price tumble by 37.8%. Since reaching a peak in early June of 2020, just a week after the IPO, Nikola stock is down by about 91%. The company announced Tuesday morning that it will acquire battery maker Romeo Power for $144 in Nikola stock. The company recently asked a federal judge to quash a subpoena from founder and former CEO Trevor Milton who is defending himself against criminal fraud charges.

Just eight analysts cover the stock and seven of those have given it a Hold rating. The other one rates the stock a Buy. At the current price of around $7.00, the upside potential based on a median price target of $8.00 is 14.3%. At the high price target of $15.00, the implied gain is 114.3%.

Analysts are forecasting second-quarter revenue at $16.58 million and expect Nikola to report a loss per share of $0.27. In the prior quarter, Nikola reported a loss of $0.21 per share and no revenue. For the full year, the company is expected to lose $1.09 per share, more than the loss per share of $0.79 in 2021. Analysts also expect Nikola to report $114.85 million in revenue for the full fiscal year. The company did not report any revenue last year.

Nikola is not expected to post a profit in 2022, 2023, or 2024. The enterprise value to sales multiple for 2022 is 22.8. For 2023 and 2024, the multiple is 4.2 and 1.7, respectively. The stock currently trades at an estimated sales to enterprise value multiple of 18.3 times for 2022 and 3.2 times for 2023. The stock’s 52-week range is $4.42 to $15.56. Nikola does not pay a dividend. The total shareholder return for the past 12 months is negative 37%.

https://247wallst.com/investing/2022/08/02/earnings-previews-alibaba-conocophillips-nikola-paramount-global/

Public Messages search for: NKLA

https://investorshub.advfn.com/boards/msgsearch.aspx?searchStr=NKLA

Nikola Q2 2022

Aug 04, 2022

09:30 AM EDT Nikola Q2 2022 Financial Results and Q&A Webcast

https://nikolamotor.com/investors

Getting exciting! The next few years will be a joy IMO.

Merger Agreement

On July 30, 2022, Nikola Corporation, a Delaware corporation (the “Company”), entered into an Agreement and Plan of Merger and Reorganization (the “Merger Agreement”) with Romeo Power, Inc., a Delaware corporation (“Romeo”), and J Purchaser Corp., a Delaware corporation and a wholly owned subsidiary of the Company (“Purchaser”). Pursuant to the Merger Agreement, and upon the terms and subject to the conditions thereof, Purchaser will commence an exchange offer (the “Offer”) to acquire all of the issued and outstanding shares of common stock, par value $0.0001 per share, of Romeo (“Romeo Common Stock”) for the right to receive 0.1186 of a share (the “Exchange Ratio”) of common stock, $0.0001 par value per share, of the Company (“Company Common Stock”).

https://www.sec.gov/ix?doc=/Archives/edgar/data/1731289/000119312522209149/d580862d8k.htm

https://www.sec.gov/Archives/edgar/data/1731289/000119312522210125/0001193125-22-210125-index.htm

https://www.sec.gov/cgi-bin/browse-edgar?CIK=0001731289&owner=exclude

https://nikolamotor.com/investors/sec?active=sec

Nikola Stockholder Meeting: Proposal 2 Passes

Stockholders approve increase in authorized number of shares from 600M to 800M

Published August 02, 2022

https://nikolamotor.com/press_releases/nikola-stockholder-meeting-proposal-2-passes-190?utm_source=Reddit&utm_medium=social&utm_campaign=proxy_release18

RMO closed @.71 today.....if you could have bought RMO shares @.5 or below a month ago or even last week imo it would have been well worth it

https://www.tradingview.com/chart/uZbZ0HkZ/

UK, as mentioned in a previous post, due to lack of funds to purchase new shares, I have been selling most of my NKLA shares and buying RMO shares, resulting in an effective 11% increase in my NKLA shares post the 0.1186 conversion of RMO to NKLA shares, assuming the deal goes through as expected before the end of October. I am putting a very low risk that the deal does not go through. Is this too risky a strategy in your opinion? Any other board member please feel free to chime in as well. Out of free posts for today and look forward to your responses.

Darkinvestor, note that the conversion rate is 0.1186, slightly higher than the 0.114 in your post (See https://investorplace.com/2022/08/nkla-stock-alert-what-to-know-about-nikolas-deal-for-romeo-power/)

each RMO share will yield you roughly 0.114 of NKLA shares.

If you do want to try this I would do it now since if they have the votes for the increase in shares I am expecting a nice increase in SP as funding phase 2 building will be cheap. News this pm.

Srm4u, in your opinion, does it make sense to buy RMO shares instead of NKLA to eventually get NKLA shares? It seems like a cheaper way to buy NKLA shares right now. Or is it too risky a strategy, in case the deal falls apart?

Nikola Corporation flair_name:"Hydrogen Fueling Stations"

https://www.reddit.com/r/NikolaCorporation/search?q=flair_name%3A%22Hydrogen%20Fueling%20Stations%22&restrict_sr=1

|

Followers

|

275

|

Posters

|

|

|

Posts (Today)

|

4

|

Posts (Total)

|

10913

|

|

Created

|

03/03/20

|

Type

|

Free

|

| Moderators WeTheMarket | |||

Nikola and VectoIQ Acquisition Corp. Announce Closing of Business Combination

Published June 03, 2020

https://nikolamotor.com/press_releases/nikola-and-vectoiq-acquisition-corp-announce-closing-of-business-combination-77

Steve Girsky

Girsky was GM Vice Chairman from March 2010 through January 2014. During that time he was responsible for several functional areas, including:

Global corporate strategy,

New business development,

Global product planning and program management,

Global connected customer/OnStar, and

GM Ventures LLC and global research & development.

Girsky also served as Chairman of the Adam Opel AG Supervisory Board and as interim President of GM Europe during this time frame, a critical period in

which the company established its current 'Drive Opel 2022' strategy. Girsky also held responsibility for GM's Global Purchasing and Supply Chain function

from 2011 to 2013, and served as Senior Advisor to General Motors from January 2014 to July 2014.

https://investor.gm.com/news-releases/news-release-details/gm-announces-stephen-girsky-retire-board-directors

https://www.freightwaves.com/news/shell-stuffing-how-nikola-became-vectoiqs-public-preference

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=165678224

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=165764942

Nikola and TC Energy Sign Joint Development Agreement

for Co-Development of Large-Scale Clean Hydrogen Hubs

October 7, 2021

Nikola and TC Energy sign joint development agreement for co-development of large-scale clean hydrogen hubs. Nikola Corporation (Nasdaq: NKLA), (Nikola),

a global leader in zero-emissions transportation and energy infrastructure solutions, and TC Energy Corporation (TSX,NYSE: TRP), (TC Energy), a leading

North American energy infrastructure company, have agreed to collaborate on co-developing, constructing, operating and owning large-scale hydrogen

production facilities (hubs) in the United States and Canada.

https://hydrogen-central.com/nikola-tc-energy-agreement-hydrogen-hubs/

#NationalHydrogenDay celebrations continue with a sneak peek of all things happeningat our Coolidge

manufacturing facility, including our Nikola Tre #FCEV, for our next episode of the #DrivingChange series!

1:57 PM · Oct 8, 2021

https://twitter.com/i/status/1446565427493044225

Hydrogen Heavy Duty Vehicle Industry Group Partners to Standardize Hydrogen Refueling,

Bringing Hydrogen Closer to Wide Scale Adoption

Published October 08, 2021

https://nikolamotor.com/press_releases/hydrogen-heavy-duty-vehicle-industry-group-partners-

to-standardize-hydrogen-refueling-bringing-hydrogen-closer-to-wide-scale-adoption-137

Gettin' it done. Season 2 of #DrivingChange starts with the continued journey

of the #NikolaTre FCEV alpha builds in Coolidge, Arizona.

November 3, 2021

https://www.facebook.com/nikolamotorcompany/videos/driving-change-season-2-episode-1-

get-it-done/1259891077770836/?__so__=permalink&__rv__=related_videos

https://www.youtube.com/watch?v=RokrKePeRrk

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |