News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Oh, it's just a bump in the road. Dye only has 100 million dollars at risk, lol

Weird as though Dye and his minion make it sound like their is absolutely nothing wrong here. Yet the price share languishes between .01 to .20

Any thoughts? Honestly I really dont know what to think.

...and even then they didn't have much volume. lol

There will be no real volume until they are back trading OTC

So much for the volume pump. Back to scratch.

22.5 k traded today. Interesting. Keep an eye on this.

Good points, I like the CYA measures. SHWZ should be thinking of ways to protect themselves and it would be wise for them to cover this with their attorney.

Agreed, but now realizing that, even though there are 1000+ dispensaries in NM, that, as the largest MSO in the state we are probably the most suseptible to the (misleading) negativity/fallout from state/product recalls. It makes you wonder of the company's product selection/offering policy and whether or not they will change/update the policy to try and better protect against these issues in the future? I get that cannabis is a 'live' product, and therefore suseptible to any produce related recalls, but THIS -- a prohibited pesticide -- is preventable. The downfall is that a dispensary is supposed to be a gatekeeper when it comes to product safety...and this product managed to get on so many shelves. It makes you wonder the COA that was provided to the dispensary to get it on the shelves...did it contain a pesticide test, and what did it say (probably misleading, cause you might not be able to 'catch' everything, which is where the state comes into play)? And if it didn't contain a pesticide test, it is probably time SHWZ update their standards to include several layers as a CYA.

I am just glad it was not a Schwazze product as there could be serious liability consequences. I do get the initial reaction but we dodge a bullet on this one.

Yes. Thank you for clarifying! Huge difference. I didnt watch the video, I just totally misinterpreted the article. I guess it makes sense that the retail outlets would have/sell the contaminated products...and need to pull them from the shelves...but dang that article was poorly written making it seem like it was retailer, in-house, product.

Thanks for that clarification.

Looks like Maggie's Farm is the producer/packager of the products that were contaminated. Maggie's Farm owned by Bill Conkling and to my knowledge not associated with Schwazze or its investors. So thankfully it's not a product produced and packaged by any of Schwazze House of Brands.

https://tracxn.com/d/companies/maggies-farm/__ipz-yQyr7qTa9YwF_sl34lWO_bss9pvglIdCpbxizZc

https://kfoxtv.com/amp/newsletter-daily/bad-trip-contaminated-cannabis-makes-its-way-to-sunland-park-dispensary-r-greenleaf-organics-dispensary-new-mexico-cannabis-control-division-weed-recall-pyrethrins

https://www.santafenewmexican.com/news/local_news/recall-ordered-for-cannabis-products-over-contamination-concerns/article_cfd57d2e-6c8d-11ef-b9b1-8b2fd23707c6.html

https://www.elpasotimes.com/story/news/health/2024/09/06/new-mexico-recalls-marijuana-over-excessive-pesticide-contamination/75107016007/

Way to go SHWZ, you dominate the list! Too bad it is product recalls for testing positive for a prohibited pesticide!

https://www.krqe.com/news/recalls/dozens-of-marijuana-products-in-new-mexico-recalled-over-contamination-concerns/

Up 172% today on 3550 shares? Must be getting ready to file some financials

No, not grim at all. Still positive cash flows, the debt can be managed and the creditors are friendly. They just need to get the filings current and get back on OTCQX. I do believe they now understand how important the stock price is and will manage the company accordingly.

Does anyone have a path that doesn't involve bankruptcy? 12 million cash with approximately 160 million in debt due Nov 2025 is pretty grim.. I own 400,000 shares at an avg cost of 0.59..I would love to hear from anyone what that path would be. I think we need a legislative and scheduling hail mary at this point.

Good, now Canadian investors can't grab all these underpriced shares off the expert market either. Let's see some filings updated, Justin...

I don't see any movement on MJ at the fed level until at least a month or two after inauguration. The question will be, would passage (safe banking, rescheduling) be one of those "In the first 100 days" items for either president/king/queen that gets elected for the next four years. It could be an easy win to chalk up and prove some competency, progress, action in either administration. But perhaps sniping will rule the day next year rather than doing anything meaningful in congress. I see another impeachment attempt of Biden is afoot for when congress comes back from summer recess - more time and dollars well spent by congress rather than doing their job.

If SHWZ can consistently show net profits between now and then, yes, a bump is possible. And with the stock in the gutter, getting back to sixty cents would be a big percentage bump for traders.

Of course the politicians won't do a thing this year, as nothing will happen with weed before the November elections now. But just maybe.... next year as either party at least passes safe banking, and the company implements cost cutting measures, the markets in Colorado and New Mexico at least stabilize, and the company reports NET PROFITS for at least a few quarters. If that happens and they regain OTCQX trading status, I can see the Marijuana funds scrambling to add these cheap shares, and we have already seen how just their buying can move this stock. Ok... it's a waiting game now.

Right Doc, languishes probably through the end of the year, easily. They best hope they don't find any irregularities missed prior as well. But even if it all gets resolved next year, no surprises, and SHWZ says, "Hey everybody, we're back!" they may be saying that to an even emptier room than the one they are in now. They couldn't get people to care about the stock before, now, that's a steep hill they will need to climb to even get penny traders to take interest again. Beyond someone buying them for peanuts, I don't see a compelling upside for quite some time.

No it's not, lol. It was anticipated and expected. I posted that it might happen, months ago.

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=174735518

The filing rules require that, like stepping stones over a flowing river, that the financials have to be audited and accepted, to be used for subsequent filings starting points. So if the 2023 filings are not re-completed then they can't be used as a basis for inclusion as a starting point for 2024 filings, even though they have the numbers for the quarter. But once the old filings are resubmitted, then we will likely see a fast process for the 2024 filings to be filed. It's a tedious process, but obviously one they are working very diligently upon, and will get completed, hopefully by the end of this year.

Here we go! This is a sign of a slow death for sure .

OMG - NT10Q filed  State below in reasonable detail the reasons why Forms 10-K, 20-F, 11-K, 10-Q, N-SAR, N-CSR, or the transition report or portion thereof, could not be filed within the prescribed time period.

State below in reasonable detail the reasons why Forms 10-K, 20-F, 11-K, 10-Q, N-SAR, N-CSR, or the transition report or portion thereof, could not be filed within the prescribed time period.

Medicine Man Technologies, Inc. (the “Company”) is unable to file its Quarterly Report on Form 10-Q for the quarter ended June 30, 2024 (the “Quarterly Report on Form 10-Q”) on or prior to August 14, 2024, without unreasonable effort and expense for the reasons stated below.

The ongoing impact of the May 3, 2024, U.S. Securities Exchange Commission (“SEC”) order (the “SEC Order”) against B.F. Borgers CPA PC and Benjamin F. Borgers (individually and together, “Borgers”), pursuant to which the SEC suspended Borgers from appearing or practicing before the SEC as an accountant has been significantly challenging for the Company. Borgers was the Company’s independent auditor for the fiscal year ending December 31, 2023, during which time Borgers reviewed Company financial statements and performed reviews of interim financial statements.

In April, the Company engaged Baker Tilly to provide a re-audit of the Company’s year-end December 31, 2023 financial statements as filed on the Annual Report on Form 10-K and the interim quarterly statement for the three-months ending March 31, 2023, as filed in the Quarterly Report on Form 10-Q and the interim quarterly statement for the six-months ending June 30, 2023. The extent of the SEC Order’s impact has been significant on the Company’s financial statements as of and for the fiscal quarters ending March 31, 2024 and June 30, 2024, to be included in the Quarterly Report filed on Form 10-Q, and its financial statements as of and for the year ended December 31, 2023 included in its Annual Report on Form 10-K.

The impact of the SEC Order has required the Company to undergo a re-audit of the Company’s; (i) year-end December 31, 2023, financial statements as filed on the Annual Report on Form 10-K; (ii) the interim quarterly statement for the three-months ending March 31, 2023, as filed in the Quarterly Report on Form 10-Q, in order to file our Quarterly Report on Form 10-Q for the three-months ending March 31, 2024; and (iii) the interim quarterly statement for the six-months ending June 30, 2023, as filed in the Quarterly Report on Form 10-Q, in order to file our Quarterly Report on Form 10-Q for the six-months ended June 30, 2024. As stated in the SEC Order, Form 10-Q filings on or after the date of the SEC Order may not present financial information that has been reviewed by Borgers. Each quarterly period presented in Form 10-Q filings on or after the date of the SEC Order must be reviewed by a qualified, independent, PCAOB-registered public accountant that is permitted to appear or practice before the Commission.

Based on the scope of the re-audit of the Company’s financials noted above, Baker Tilly has had insufficient time to re-audit the Company’s financials by the required filing date of the Quarterly Report on Form 10-Q for the quarter ended June 30, 2024. The Company will use its best efforts to file its Quarterly Report on Form 10-Q for the quarter ended June 30, 2024 within the extension period provided under rule 12b-25, however there can be no assurances as the timing of the filing is contingent on Baker Tilly’s re-audit of the Company’s financials noted above.

I'd be ecstatic with a buck twenty five!

He's dreaming. $2.50? The stock hasn't seen 2.50 since 2021.

10:29 AM EDT, August 14, 2024 (Benzinga Newswire)

Benchmark analyst Mike Hickey reiterates Medicine Man Technologies (OTC:SHWZ) with a Buy and maintains $2.5 price target.

Yep, lots of us hope the enthusiasm will be low when they resume trading, so we can scoop up cheapies in the .20's...

Nice to see the revenue uptick but unless they get a better handle on debt and expenses, I don't share his optimism. Nice to hear outreach to the investor community may be in the picture, but why did it take this crisis to get to that point? This company's differential initially was the "stellar" management team, there no longer is that confidence in the management team, and Dye stepping back in demonstrates he shares the same concern. They have a lot of proving to do over the next 6 months to warrant anything but flipping by traders if/when they return to trading. Not seeing this ER having any real effect on the stock or people's perceptions of the company to create a shift in sentiment.

Obviously, the cost of the overhead of the distribution center was not enough to pay for itself in cost savings, and became a drain on earnings. I predicted that they would start closing weaker locations, months ago. And that is a good thing, as you can't continue to support and try to turn around locations that just aren't performing. My biggest concern is why they allowed themselves to get into the situation in the first place. Why did they take their finger off the pulse.

All those analysis and projections they were making, but they missed their targets?

I think Justin was hoping he could back away and let Nirup and the people that were running the company last year, continue to build the company, but they obviously were not capable of keeping up with the trends and were spending cash like it would never end.

Now Justin seems to be back in charge, as Dye Capital is hurting badly with the stock debacle, and I believe they will get it fixed by the end of 2024. I also believe he sees the need to report POSITIVE EARNINGS to support the stock, thus the closing of the cash bleeding distribution center. We as investors seem to have forgotten how we thought management was the greatest team in Cannabis, and they could do no wrong for years.

Some of us saw the debts spiraling out of control and the interest payments on the loans and PREFERRED STOCKS eating up all the profits. I don't think there will be anything that Dye can do about the debts coming due in 2025 except try to continue to pay interest on them, but he could SUSPEND THE PREFERRED DIVIDENDS for awhile and that would allow the company to become instantly profitable and likely would raise the stock price back into DOLLARLAND.

With the share price higher again, then he could use stock again to acquire more dispensaries and continue to build the store count as will be necessary to continue as a growing company. He knows he and his team fumbled, but it does appear he now has his finger on the pulse again, and hopefully we will see a much better outcome in 2025.

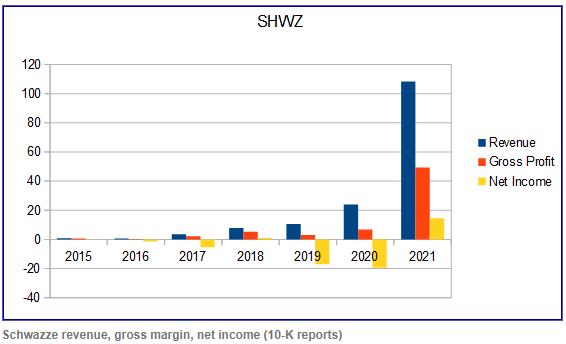

The real positive is they were finally able to turn the revenue positive. I believe it was a hard lesson for management. Also wholesale starting to pick up steam.

Closed the Colorado distribution center...I thought a centralized location was one of the plans that was going to set them apart from their competition by allowing for more product depth and better inventory management across their retail outlets?

I listened to the conference call. Dye is optimistic that they will be back on OTCQX, and is planning investor conferences and increased investor relations activities after getting back on the trading exchange.

Small increase in revenue with large increase in expenses, thus losses reported again. I hope someone asks when they think they will be off expert market again.

Hope all is well Doc. Any thoughts on new auditor? Tilley something. I would suspect on an operating basis e.r. Will be similar to last one in regards to revenues.

I just hope I'm around when it starts trading again!

I admire your optimism, but .75 is over double where this trading even before all this audit news broke. I think they'd need some really stellar news to go back over 30 or 35. Especially after this recent headwind.

It totally depends on the state of the company as they get reinstated. If they were extremely profitable, (unlikely) and announced that NEWS while trading was on th e expert market, likely there would be a huge rally. Regardless, the share price would likely be back over .75, imo, just because they came back...

Doc,

Any experience with what happens when a stock like this comes back out of the expert market? Let's assume SHWZ gets their house in order and gets moved out of purgatory. The only folks who can be set for that move are the experts. Bagholders just sit and wait for a move to get close to where they were in the past. I'm assuming we can't place a buy order at a low price ahead of its return to trading. So any flip trades for that first day have to be both nimble and lucky?

Today's PRESS RELEASE confirming the earnings date and conference call is frankly GREAT NEWS for shareholders. What it means is that the audit process is intact and not hampered by the Borgers audits that were deemed unreliable and must be refiled. A very positive sign that the company will come back into compliance later this year, and resume trading.

So is their some fiduciary issues here? Certainly appears so. This is getting very interesting. Sure hope to see some heads roll. It all started with the good old boy network imo. I look for the rats to start jumping soon.

No need to pay any attention to the expert market day to day trading. The volume and prices you see are totally meaningless and unrelated to the value of the company now. What the company needs to do is to make sure they stay on top of the re-audits and try to provide the best financial results possible in the interim period until they get relisted. Then the stock will trade based on potential and on value again, and will likely rise very very fast back to pre-expert market levels and even higher. Meanwhile we wait...

They've done such a great job of alienating investors, even a good ER will struggle to overcome that. There are other stocks, better managed companies, who didn't step in it and get moved to the Expert Market. So I would not expect anyone rushing back into this when it resumes trading, except flippers betting on a potential move when trading resumes and cashing out as soon as it does. IMHO, this rises only when someone makes an offer to buy it above where it's trading price. It's now a stock waiting on a hero, they've ruined any and all good will with investors.

At least it seems like it will be better than the previous one.

|

Followers

|

128

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

21347

|

|

Created

|

01/10/16

|

Type

|

Free

|

| Moderators StevenRisk Drugdoctor damAcon1 | |||

Instagram: https://www.instagram.com/schwazze/

Facebook: https://www.facebook.com/Schwazze/

Meet the "Steve Jobs of Cannabis" and Schwazze's Chief Cultivation Officer, Josh Haupt:

https://www.youtube.com/watch?v=s36OIBT4XiQ&t=1s

Star Buds is one of the Most Recognized and Successful Retail Cannabis Operators in North America

Company Projects Pro Forma Revenue for Schwazze and its Two Acquisitions (Mesa Organics and Star Buds) of $95 Million in 2020

Company Expects to Be Cash Flow Positive Beginning in January 2021

Company Anticipates Acquiring Remaining Seven Star Buds Retail Dispensaries in Colorado during the First Quarter 2021

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |