Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

LXP bought @ 8.16 today Lexington Realty Trust Announces quarterly Common Share Dividend 5:00 pm ET September 13, 2018 (Globe Newswire) Print Lexington Realty Trust (NYSE:LXP) ("Lexington"), a real estate investment trust (REIT) focused on single-tenant real estate investments, today announced that it declared a regular common share/unit dividend/distribution for the quarter ending September 30, 2018 of $0.1775 per common share/unit payable on or about October 15, 2018 to common shareholders/unitholders of record as of September 28, 2018.

Lexington also declared a cash dividend of $0.8125 per share of Series C Cumulative Convertible Preferred Stock ("Series C Preferred Shares") for the quarter ending September 30, 2018, which is payable on or about November 15, 2018, to holders of Series C Preferred Shares of record as of October 31, 201.

Contact:

Investor or Media Inquiries for Lexington Realty Trust:

Lexington Realty Trust (Lexington) is a self-managed and self-administered real estate investment trust (REIT). The Company’s primary business is the acquisition, ownership and management of portfolios of net-leased office, industrial and retail properties. It conducts all of its property operations through property owner subsidiaries. As of December 31, 2010, Lexington had ownership interests in approximately 195 consolidated real estate properties, located in 39 states and containing an aggregate of approximately 36.9 million square feet of space, approximately 93% of which was subject to a lease. During the year ended December 31, 2010, no tenant/guarantor represented greater than 10% of its annual base rental revenue. The Company is structured as an umbrella partnership REIT (UPREIT), and a portion of its business is conducted through its three operating partnership subsidiaries. In January 2012, the Company acquired a build-to-suit office facility in Huntington.

The chart of Lexington Realty Trust (LXP) shows a double top with $13.56 target or 58.00% above today’s $8.58 share price. The 5 months chart pattern indicates low risk for the $2.06 billion company. It was reported on Apr, 11 by Finviz.com. If the $13.56 price target is reached, the company will be worth $1.19B more. Double tops are rare but powerful chart patterns. The stock increased 2.02% or $0.17 on April 8, hitting $8.58. Lexington Realty Trust (NYSE:LXP) has risen 9.30% since September 2, 2015 and is uptrending. It has outperformed by 4.23% the S&P500.

Its alright, happy trading, I have invested for long term for retirement income in 30 or 40 years; all about diversifying my portfolio for the long term.

NEW YORK, Feb. 19, 2015 (GLOBE NEWSWIRE) -- Lexington Realty Trust ("Lexington") (NYSE:LXP), a real estate investment trust focused on single-tenant real estate investments, today announced results for the fourth quarter ended December 31, 2014.

Fourth Quarter 2014 Highlights -- Generated Company Funds From Operations ("Company FFO") of $66.3 million, or $0.27 per diluted common share.

-- Acquired three properties for $70.4 million.

-- Invested $24.5 million in on-going build-to-suit projects and loan investments.

-- Generated gross disposition proceeds of $167.2 million from the sale of four office buildings.

-- Received $32.8 million from maturing loan investment.

-- Retired $59.0 million of debt.

-- Completed 1.9 million square feet of new leases and lease extensions, raising cash and GAAP renewal rents by 4.6%.

T. Wilson Eglin, President and Chief Executive Officer of Lexington, stated "The execution of our stated strategies in 2014 has resulted in a strong balance sheet with a large cash position, which we believe positions us to capitalize on growth opportunities in 2015. We are already committed to fund approximately $325 million in growth initiatives this year. We believe our pipeline remains strong with additional opportunities for growth as the year progresses. We also expect to continue to take advantage of refinancing opportunities in 2015, to reduce interest expense and extend our debt maturities."

FINANCIAL RESULTS

Revenues

For the quarter ended December 31, 2014, total gross revenues were $108.0 million, compared with total gross revenues of $100.5 million for the quarter ended December 31, 2013. The increase is primarily due to property acquisitions.

Company FFO

For the quarter ended December 31, 2014, Lexington generated Company FFO of $66.3 million, or $0.27 per diluted share, compared to Company FFO for the quarter ended December 31, 2013 of $65.7 million, or $0.28 per diluted share. The calculation of Company FFO and a reconciliation to net income (loss) attributable to common shareholders is included later in this press release.

Dividends/Distributions

Lexington declared a regular quarterly common share/unit dividend/distribution for the quarter ended December 31, 2014 of $0.17 per common share/unit, which was paid on January 15, 2015 to common shareholders/unitholders of record as of December 31, 2014, and a dividend of $0.8125 per share on its Series C Cumulative Convertible Preferred Stock ("Series C Preferred Shares"), which was paid on February 17, 2015 to Series C Preferred Shareholders of record as of January 30, 2015.

Net Income (Loss) Attributable to Common Shareholders

For the quarter ended December 31, 2014, net income attributable to common shareholders was $35.7 million, or $0.15 per diluted share, compared with net loss attributable to common shareholders for the quarter ended December 31, 2013 of $(8.9) million, or $(0.04) per diluted share.

OPERATING ACTIVITIES

Investment Activity

Acquisitions

Initial Initial Annualized Initial Estimated Lease Property Basis Cash Rent Cash GAAP Term Tenant/Guarantor Location Type ($000) ($000) Yield Yield (Yrs) ----------------- ---------- ----------- --------- ---------- ------- --------- ------ ZE-45 Ground New York, Tenant LLC NY Land $ 30,426 $ 1,500 4.9% 15.2% 99 Vineland, Rehab HealthSouth Corp. NJ Hospital 19,100 1,113 5.8% 5.8%(1) 28 International Automotive Components Group Anniston, North America AL Industrial 20,907 1,572 7.5% 8.3% 15 --------- ---------- ------- --------- $ 70,433 $ 4,185 5.9% 10.6% ========= ========== ======= ========= 1. Lease contains annual CPI increases.

On-going Build-to-Suit Projects

GAAP Investment Maximum Balance as Lease Commitment/Estimated of Estimated Property Term Completion Cost 12/31/2014 Completion Location Sq. Ft. Type (Years) ($000) ($000) Date ---------- --------- ---------- ------- -------------------- ---------- ------------ Oak Creek, WI 164,000 Industrial 20 $ 22,609 $ 11,860 2Q 15 Thomson, GA 208,000 Industrial 15 10,245 3,428 2Q 15 Richmond, VA 330,000 Office 15 110,137 62,225 3Q 15 Lake Jackson, TX 664,000 Office/R&D 20 166,164 28,225 4Q 16 Houston, Private TX(1) 274,000 School 20 86,491 11,795 3Q 16 --------- -------------------- ---------- 1,640,000 $ 395,646 $ 117,533 ========= ==================== ========== 1. Lexington has a 25% interest as of December 31, 2014. Lexington may provide construction financing up to $56.7 million to the joint venture.

Forward Commitments Estimated Estimated Acquisition Estimated Initial Estimated Lease Property Cost Completion Cash GAAP Term Location Type ($000) Date Yield Yield (Years) ------------ ----------- ----------- ---------- --------- --------- ------- Auburn Hills, MI Office $ 40,025 1Q 15 7.9% 9.0% 14 Richland, WA Industrial 155,000 4Q 15 7.1% 8.6% 20 ----------- --------- --------- $ 195,025 7.3% 8.7% =========== ========= =========

Capital Recycling

Property Dispositions

Gross Disposition Annualized Property Price NOI Month of Tenant Location Type ($000) ($000) Disposition ------------ ------------- --------- ------------ ---------- ------------ Bank of America, National Association Brea, CA Office $ 110,000 $ 8,096 Nov-14 Vacant(1) Chicago, IL Office 34,150 -- Nov-14 Canal Insurance Greenville, Company SC Office 11,550 991 Dec-14 Vacant(2) Houston, TX Office 11,486 -- Dec-14 ------------ ---------- $ 167,186 $ 9,087 ============ ========== 1. $29.9 million secured debt satisfied at closing. 2. Purchaser assumed an $11.5 million secured debt.

Loan Investments

Lexington collected $32.8 million in full satisfaction of the Norwalk, Connecticut loan investment.

Balance Sheet

During the fourth quarter of 2014, Lexington satisfied $50.5 million of secured debt, which had a weighted-average interest rate of 5.5%, including the $41.4 million of aggregate secured debt encumbering properties which were disposed.

In December 2014, holders converted approximately $8.6 million original principal amount 6.00% Convertible Guaranteed Notes due 2030 ("6.00% Notes") for 1,280,439 common shares and a cash payment of $171 thousand plus accrued interest, reducing the outstanding balance of this note issuance to $16.2 million at December 31, 2014. All common shares that are issuable upon conversion of the 6.00% Notes are treated as outstanding for diluted Company FFO calculations.

During the fourth quarter of 2014, Lexington locked rate on the following secured loans:

Property Amount Term Tenant/Guarantor Location Type ($000) Fixed Rate (approx.) ----------------- ----------- ----------- --------- ---------- ---------- ZE-45 Ground New York, Tenant LLC(1) NY Land $ 29,193 4.1% 10 years Federal Express Long Island Corporation(2) City, NY Industrial 51,650 3.5% 13 years --------- ---------- $ 80,843 3.7% ========= ========== 1. Loan closed in first quarter of 2015. 2. No assurances can be given that the loan will be funded on these terms or at all.

Leasing During the fourth quarter of 2014, Lexington executed the following new and extended leases:

LEASE EXTENSIONS

Location Prior Term Lease Expiration Date Sq. Ft. ------------------------ ---------- --------------------- ---------

Office/Multi-Tenant

1 Little Rock AR 10/2015 10/2020 36,311 2 Pine Bluff AR 10/2015 10/2017 27,189 3 Phoenix AZ 11/2016 11/2021 6,982 ------------------------ ---------

~ Thursday! $LXP ~ Earnings posted, pending or coming soon! In Charts and Links Below!

~ $LXP ~ Earnings expected on Thursday * Want more like this? Search Keyword:MACMONEY >>> http://tinyurl.com/MACMONEY <<< One or more of many earnings sites has alerted this security has or will be posting earnings on or around the day of this message.

Lexington Realty Trust (Lexington) is a self-managed and self-administered real estate investment trust (REIT). The Company’s primary business is the acquisition, ownership and management of portfolios of net-leased office, industrial and retail properties. It conducts all of its property operations through property owner subsidiaries. As of December 31, 2010, Lexington had ownership interests in approximately 195 consolidated real estate properties, located in 39 states and containing an aggregate of approximately 36.9 million square feet of space, approximately 93% of which was subject to a lease. During the year ended December 31, 2010, no tenant/guarantor represented greater than 10% of its annual base rental revenue. The Company is structured as an umbrella partnership REIT (UPREIT), and a portion of its business is conducted through its three operating partnership subsidiaries. In January 2012, the Company acquired a build-to-suit office facility in Huntington.

Lexington Realty Trust (Lexington) is a self-managed and self-administered real estate investment trust (REIT). The Company’s primary business is the acquisition, ownership and management of portfolios of net-leased office, industrial and retail properties. It conducts all of its property operations through property owner subsidiaries. As of December 31, 2010, Lexington had ownership interests in approximately 195 consolidated real estate properties, located in 39 states and containing an aggregate of approximately 36.9 million square feet of space, approximately 93% of which was subject to a lease. During the year ended December 31, 2010, no tenant/guarantor represented greater than 10% of its annual base rental revenue. The Company is structured as an umbrella partnership REIT (UPREIT), and a portion of its business is conducted through its three operating partnership subsidiaries. In January 2012, the Company acquired a build-to-suit office facility in Huntington.

Currently, LXP has around $200 million of cash on hand with only 19.3% secured debt to total debt. Also, LXP has an unused $400 million credit facility and expects to continue to unencumber the shorter-term debt. Like most Net Lease REITs, LXP has continued locking-in fixed rates and going long term.

What Do I Expect on May 7th?

In anticipation of LXP's first-quarter results next week (May 7th), I am expecting to gain more clarity and I'm hoping that the market will soon rally behind the mis-priced REIT. Although I have enjoyed the higher than average dividend, I am looking forward to seeing shares begin to trade closer to their deserved course of action. Here's a few things I'm looking for next week:

Acquisitions: LXP has already closed on $197.3 million of new properties in Q1-15 with an initial cash yield of 6.9% (8.1% GAAP). The properties have a weighted-average lease term of 17 years. This is a positive announcement and I expect LXP to move ahead of its 2015 acquisition guidance (and of course that means FFO will grow).

Tenant Retention Should Improve in 2016: LXP has eight lease expirations in 2015 and the company expects five tenants to move out. I'm not too concerned with the rent reduction (around $7 million), but I would like to see how the company addresses the leasing of the vacated assets. Looking ahead to 2016 and beyond, LXP's lease roll should result in more stable and consistent NOI and AFFO growth. Hopefully, the worst is in the rear view mirror.

Private School Deal: I did see that LXP is co-investing in a for-profit private school build-to-suit in Texas. It's a small deal (around $7 million by LXP capital) but the news of Corinthian shutting down this week made me blink. It appears that LXP's tenant is stable (strong parent guarantee) and the lease is 20 years. I suspect there will be questions arising on the earnings call since this is a new net lease category for LXP.

Build-To-Suit Business: The BTS business has become a core part of LXP's asset aggregation model. There are around five BTS deals that LXP has in various stages with funds committed of around $400 million. Completion dates are from Q2-15 to Q4-16. It takes time for the rent checks to hit the earnings statement so I'm sure that LXP will address this capital strategy to determine whether the projects are on budget and on time.

Earnings Results: LXP's 2015 FFO guidance is $1.00 to $1.05 per share. Given the weaker (FFO) growth forecast (this year) I expect to see mediocre performance in Q1 with accelerated progress in the next 3 quarters. The Q1 acquisitions provide me with comfort that the cash is being deployed accretively and as the BTS deals (start paying rent) I expect that LXP would move closer to the top-end of guidance (in 2015).

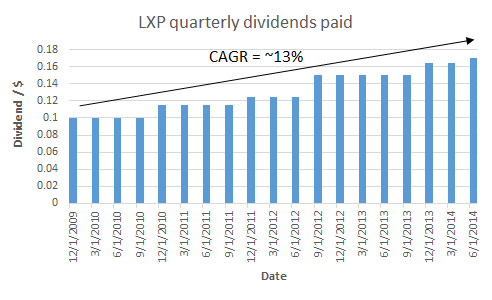

Dividend Growth: The quarterly dividend is $.17 per share ($.68 annualized) and while I view the payout as sustainable, I'm not expecting a big boost in 2016. The dividend yield is already above average so I expect to see Mr. Market move the yield closer to the peer group.

News

News  Market Data

Market Data  Discover

Discover