News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

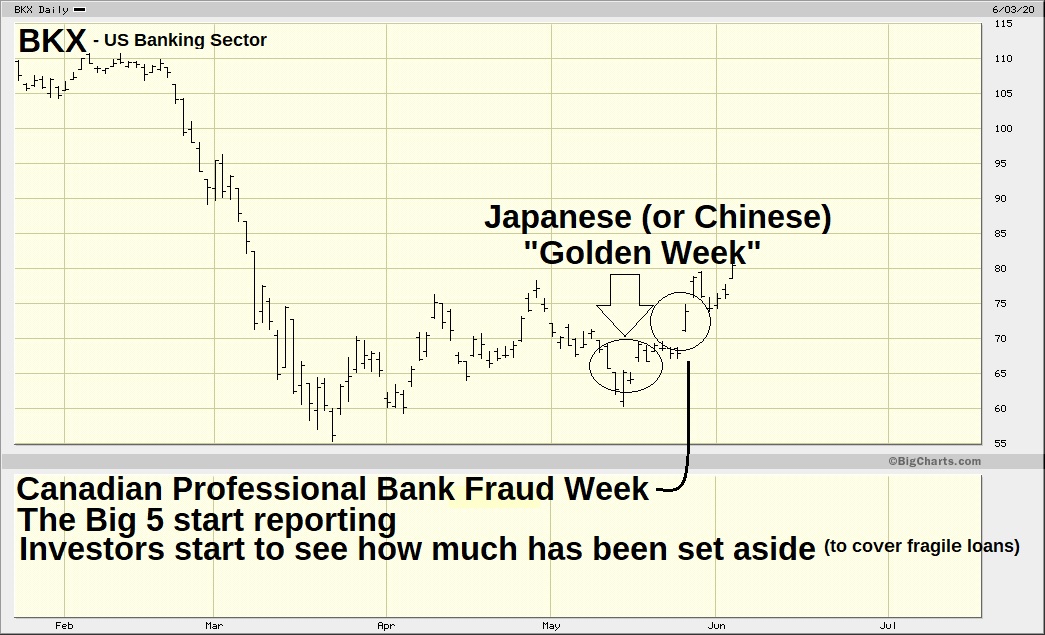

CPBFW (happens every quarter).....

Canadian Banks have always seemed to have an uncanny ability to come out with their earnings agt critical junctures.....

ALL of their CEO's are Harvard grads frequently winding up at (or coming from) Goldman Sachs, etc.

Some very important and something else questions :

Please check out the post to which this one replied to (in order to view some proper charts) :

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=35362794

Do you have any thoughts about where it might go ?

Because whatever it does may prove quite influential.

I'd like to know where it will be on May 12th.

Corruption: re Hedge Fund Paid Summers $5.2 Million in Past Year

No wonder why banking industry is hyperventilating. This article shows one more corruption among other unfair practices in the financial markets.

___________________________________________________________

Hedge Fund Paid Summers $5.2 Million in Past Year

By JOHN D. MCKINNON and T.W. FARNAM

WASHINGTON -- Top White House economic adviser Lawrence Summers received about $5.2 million over the past year in compensation from hedge fund D.E. Shaw, and also received hundreds of thousands of dollars in speaking fees from major financial institutions.

A financial disclosure form released by the White House Friday afternoon shows that Mr. Summers made frequent appearances before Wall Street firms including J.P. Morgan, Citigroup, Goldman Sachs and Lehman Brothers. He also received significant income from Harvard University and from investments, the form shows.

Financial Disclosures

In total, Mr. Summers made a total of about 40 speaking appearances to financial sector firms and other places, with fees totaling about $2.77 million. Fees ranged from $10,000 for a Yale University speech to $135,000 for an appearance paid for by Goldman Sachs & Co.

http://online.wsj.com/article/SB123879462053487927.html

Hedge Funds, Buyout Firms Say Regulation Unstoppable (Update1)

By Katherine Burton and Rebecca Christie

March 27 (Bloomberg) -- Hedge funds and private-equity firms, after opposing increased federal oversight for years, said they can’t escape the Obama administration’s plan to include them in an overhaul of U.S. financial regulation.

http://bloomberg.com/apps/news?pid=20601087&sid=ajq8MuPTxQy8&refer=home#

Bubble/Crash manipulation ~ Rates on the 30-Year Mortgage Drop to Record Low of 4.85%

FREDDIE MAC, MORTGAGE RATES, DECREASE, FEDERAL RESERVE,

Reuters

| 26 Mar 2009 | 02:27 PM ET

U.S. mortgage rates fell to record lows again this week, feeding demand for refinancings, as a result of government efforts to reduce rates to levels that will help the hard-hit housing market begin to recover.

Interest rates on 30-year fixed-rate mortgages averaged 4.85 percent for the week ending March 26, down from the previous week's 4.98 percent.

The rate broke the previous record low of 4.96 percent set 10 weeks earlier, according to Freddie Mac.

The 30-year fixed-rate mortgage is the lowest since Freddie Mac started the Primary Mortgage Market Survey in 1971.

"The Federal Reserve's announcement that it intends to purchase Treasury securities over the next six months caused bond yields to drop and mortgage rates followed," Frank Nothaft, Freddie Mac vice president and chief economist, said in a statement.

Low mortgage rates have spurred a surge in home refinancing loans, and resulting lower monthly payments should provide a bit of relief to strapped consumers amid rising unemployment and a shrinking economy.

But the precipitous drop in mortgage rates has made only a marginal impact on demand for loans to purchase a home, offering little sign of a recovery from the worst housing downturn since the Great Depression.

"Everything helps when it comes to the U.S. housing market and lower interest rates on mortgages should make it easier for buyers to enter the market and absorb supply, which is still quite high," said Lawrence J. White, professor of economics at New York University's Stern School of Business.

"For existing homeowners who are able to refinance, it should help prevent foreclosures and free up cash," he said.

Other rates drop

Freddie Mac said the 15-year fixed-rate mortgage averaged 4.58 percent in the latest week, down from 4.61 the prior week.

The 15-year fixed-rate mortgage also reached a record low.

One-year adjustable-rate mortgages, or ARMs, fell to an average of 4.85 percent from 4.91 percent last week.

Freddie Mac said the "5/1" ARM, set at a fixed rate for five years and adjustable each following year, averaged 4.96 percent, compared with 4.98 percent a week earlier.

The 5/1 ARM has never been lower since the span of Freddie Mac's weekly survey, which dates back to 2005 for the 5/1 ARM.

A year ago, 30-year mortgage rates averaged 5.85 percent, 15-year mortgages were at 5.34 percent and the one-year ARM was at 5.24 percent.

A year ago, the 5/1 ARM averaged 5.67 percent.

Lenders charged an average of 0.7 percent in fees and points on 30-year mortgages, unchanged from the previous week, while they charged an average 0.7 percent in fees and points on 15-year mortgages, unchanged from the previous week.

The 5/1 ARM fees and points were 0.7 percent, unchanged from the previous week.

The one-year ARM fees and points were 0.6 percent, down from 0.7 percent the previous week.

Freddie Mac and its larger sibling, Fannie Mae, were placed under government conservatorship in early September.

Freddie Mac is a mortgage finance company chartered by Congress that buys mortgages from lenders and packages them into securities to sell to investors or to hold in its own portfolio.

Copyright 2009 Reuters. Click for restrictions.

URL: http://www.cnbc.com/id/29894995/

US Must Lead Regulatory Improvements: Summers

ECONOMY, LARRY SUMMERS, WHITE HOUSE, POLITICS, BARACK OBAMA, TIMOTHY GEITHNER,

Reuters

| 13 Mar 2009 | 11:43 AM ET

Top White House economic adviser Lawrence Summers on Friday called for the United States to lead a global effort to improve regulatory standards and warned against allowing regulators to compete against one another.

Summers, speaking to a Brookings Institution forum in Washington, said there should be no substantially interconnected institution or market that escapes regulatory scrutiny.

"Globally, the United States must lead a leveling-up of regulatory standards, not as has happened all too often in the recent past, trying to win a race to the bottom," Summers said.

Summers said U.S. Treasury Secretary Timothy Geithner in coming weeks will lay out the Obama administration's regulatory reform approach, which will be taken up at an April 2 meeting of the Group of 20 wealthy and major developing economies.

Summers said regulatory agencies should never be allowed to compete "for the privilege of regulating particular financial institutions."

He said reforms should include requirements on levels of capital and liquidity that help to protect the overall financial system, even in very difficult times.

"And there must be far more vigorous and serious efforts to discourage improper risk taking through transparency and accountability for errors," Summers said.

# Slideshow: Surprising Stock Market Indicators

Copyright 2009 Reuters. Click for restrictions.

URL: http://www.cnbc.com/id/29676910/

$BKX 26.47 after 12 + trillions to hedge funds

The market manipulation and fight with the Obama admin.

Markets down 7 days in a row -- selling off 12.50% since the Geithner speech. It seems that the hedge funds are fighting against the Gov as well because the Gov is planning to regulate the industry.

WallStreet against Obama and mainstreet ~ US Regulators Stand Ready With More Bank Capital

TREASURY, GOVERNMENT, FINANCIAL SERVICES, CITIBANK, BANK OF AMERICA, BANKING, BANKS

Reuters

| 23 Feb 2009 | 08:44 AM ET

U.S. banking regulators Monday pledged to provide more capital to banks as needed and keep large institutions viable through a new capital assessment program to be launched Wednesday.

"The U.S. government stands firmly behind the banking system during this period of financial strain to ensure it will be able to perform its key function of providing credit to households and businesses," the regulators said in a statement issued by the U.S. Treasury that named no individual banks.

"The government will ensure that banks have the capital and liquidity they need to provide the credit necessary to restore economic growth," the regulators said. "Moreover, we reiterate our determination to preserve the viability of systemically important financial institutions so that they are able to meet their commitments."

The program to be launched Wednesday -- the Capital Assistance Program -- was announced Feb. 10 by U.S. Treasury Secretary Timothy Geithner as part of a larger bank rescue plan that will include the creation of a public-private partnership to mop up toxic assets on bank books.

Under the Capital Assistance Program, regulators will conduct "stress tests" to evaluate the potential capital needs of major U.S. banks should the economy perform more poorly than expected.

"Should that assessment indicate that an additional capital buffer is warranted, institutions will have an opportunity to turn first to private sources of capital," the regulators said.

"Otherwise, the temporary capital buffer will be made available from the government.

The announcement followed a report on Sunday night that Citigroup was in talks on the U.S. government taking a bigger stake in the bank. The Wall Street Journal said taxpayers could end up owning as much as 40 percent of the ailing lender's common stock. The announcement did not mention Citigroup or any other institution.

Any government capital under the new program will come in the form of mandatory convertible preferred shares, which would be converted into common equity shares only as needed over time to keep banks well capitalized, the regulators said. These can be retired before conversion if conditions improve.

Banks that previously received preferred stock capital injections under the Troubled Asset Relief Program can exchange these shares for the mandatory convertible preferred stock, "to enhance the quality of their capital."

The regulators stressed, however, that major institutions currently have more than enough capital to be considered well capitalized.

The Capital Assistance Program aims to ensure that they have sufficient capital to support economic recovery, even if conditions worsen.

"Because our economy functions better when financial institutions are well managed in the private sector, the strong presumption of the Capital Assistance Program is that banks should remain in private hands," the regulators said.

In addition to the Treasury, these regulators include the Federal Reserve Board, the Federal Deposit Insurance Corp., the Office of the Comptroller of the Currency and the Office of Thrift Supervision.

# Read the Full Text of the Treasury's Statement

Copyright 2009 Reuters. Click for restrictions.

URL: http://www.cnbc.com/id/29347340/

Geithner is better than, and no worse than Paulson: all would know that Paulson was nothing but a wolfman who ate up millions of sheepsters.

I am referring to the debate in the video.

http://www.cnbc.com/id/29163525

Geithner's Bank Plan Led Goldman to Call Meeting

BOFA, BANK, JETS, CORPORATE, APARTMENT, LEWIS

Posted By: Charlie Gasparino | On-Air Editor

CNBC.com

| 12 Feb 2009 | 04:17 PM ET

How worried was Wall Street about a lack of clarity in Treasury Secretary Tim Geithner’s plan to save the banking system by buying toxic debt? So worried that Goldman Sachs called a meeting to figure out how to fix the problem.

—This meeting known as the “Goldman Sachs roundtable” took place just hours after Geithner’s speech (and the dismal market reaction) on Tuesday at the headquarters of Goldman Sachs in lower Manhattan.

—Around 20 of the firm’s biggest hedge fund and private equity clients from around the country showed up—a testament to just how concerned financial industry insiders are about what few details Geithner presented.

—They included representatives of KKR, Fortress Investment Group , Bain Capital, Perry Capital, Capital Research, Putnam and Citadel.

Goldman sachs says the meeting was planned well in advance. But people who attended tell CNBC that they received the invitation after the speech and decided to attend because of the speech. Goldman Sachs initially denied that the meeting, hosted by co-presidents John Winkelried and Gary Cohn, took place.

Here are some of the upshots from that meeting:

1. While it is better to wait for a good plan as opposed to quick-and-dirty bad one, time is important. What the group concluded was that the longer the plan takes to produce, the more difficult the situation becomes. That's because reviving the securitization market is key toward reviving the economy and it’s a vicious cycle: The longer it takes to revive securitization, the worse the economy becomes and the securitized products held by the banks lose more value.

2. Ken Griffen, the founder of Citadel, stressed the need not merely to fix the prices of the securitized bonds, but also that any plan must stabilize the root cause of the problem—the mortgages themselves. And he came up with several ideas to spur homeownership that could revive the housing market.

3. Also some worry over speculation that Obama economic adviser Paul Volker doesn’t have a more formal role in the process of coming up with a bailout plan.

4. Some actually had met with officials at the New York Federal Reserve after Geithner's speech and were told the plan is still weeks away. That wasn’t received well.

© 2009 CNBC.com

URL: http://www.cnbc.com/id/29163525/

"Financial 911 by the Bush Admin": Disgusted public is a correctly described state of mind for many who still have jobs, cash out of markets, and house; however, we have many who are financially demolished feeling desperate, unquenchable stomach-twisting pain financially and emotionally -- equivalent of financial 911 experience.

We need to have "Full accountability hearing on the Bush Amin" in the light of our Economic Crisis.

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=35518789

___________________________________________________________

Bank CEOs Need to Win Public Over: Lawmakers

The Associated Press

| 11 Feb 2009 | 10:48 AM ET

The top members of a key House panel told banking leaders Wednesday they must win over <<< a disgusted public >>> and work with Congress without hesitation to right the deeply troubled financial system.

"I urge you going forward to be ungrudgingly cooperative," said Rep. Barney Frank, the Democratic chairman of the House Financial Services Committee. "There has to be a sense of the American people that you understand their anger...and that you're willing to make some sacrifices to get this working."

http://www.cnbc.com/id/29137594/

To restore financial market, we need to have "Full accountability hearing on the Bush Amin" in the light of our Economic Crisis. We need to see further investigation including R.E. bubble/bust manipulations which is the crime against Americans using market manipulation.

I don't think that the CEOs are going through much pain even though those Q/A sessions are not pleasant experience. Many Americans are financially demolished because of many who abused their positions to deceive many unethically even though the actions may not be illegal. While some may have committed illegal acts, many conduct themselves unethically.

---------------------------------------------------------------

Facing Oversight, Banks Go on Offense

Wall Street Executives Say They're Looking to Improve Risk Management

By Amit R. Paley

Washington Post Staff Writer

Wednesday, February 11, 2009; Page D02

Wall Street is trying to move out of its defensive crouch.

The chieftains of eight of the nation's largest banks could receive a tongue-lashing when they testify before a House committee today, but some on Wall Street have moved to preempt the withering criticism by proposing their own solutions to the economic meltdown.

Earlier this week, Goldman Sachs chief executive Lloyd Blankfein urged tougher regulation of the financial sector and tighter limits on lavish compensation for executives. His comments echoed previous proposals by Wall Street's main lobbying association to expand oversight and regulation of the industry.

The banks helmed by Blankfein and the other seven chief executives called to appear before the House Financial Services Committee this morning received $165 billion from the $700 billion government bailout. Lawmakers are furious at the executives over accounts of their lavish spending since receiving the taxpayer funds, and have attacked them for hoarding the money instead of using it to boost lending.

"This is going to be a torture session for them; they know they are going to be pilloried, particularly by the Democrats on the committee," said Anne Mathias, director of policy research for Stanford Group, a financial services firm. "They know that they have to reframe the debate on their own terms and show that they understand the public frustration."

Analysts said the Wall Street executives are hoping to go on the offensive and embrace some degree of regulation before it is forced on them.

"For policymakers and regulators, it should be clear that self-regulation has its limits," Blankfein wrote in the Financial Times on Monday. "All pools of capital that depend on the smooth functioning of the financial system and are large enough to be a burden on it in a crisis should be subject to some degree of regulation."

Blankfein, whose firm received $10 billion in the bailout, also called for limits on executive compensation that could be more stringent in some circumstances than President Obama has proposed. Blankfein said senior executives should be paid a large portion of their bonuses in equity that they must retain until they retire. He also said it was critical that companies put a priority on reducing the risk of losses, arguing that it is necessary to prevent another crisis.

Mark T. Williams, an expert on risk management and a former Federal Reserve Bank examiner, said Wall Street has recently begun to elevate the importance of risk management as a good business practice, a trend that is typical once banks sustain enormous losses. He cited the increasing number of chief risk officers in financial firms.

"I call it the return of the nerds," said Williams, a professor at Boston University's School of Management and a consultant for Deutsche Bank. "We used to be the nerdy group that was just pushed aside into the back offices to crunch our numbers. Now risk managers are really at the tops of these banks."

Bank executives hope their adoption of risk management will soften the anger from lawmakers, according to Williams. He said it is similar to a move by J.P. Morgan in the early 1990s to develop a risk-management approach for the industry before the government did. "They were very proactive in anticipating and heading off additional regulation," he said. "They realized if they didn't develop it then regulators would."

Analysts expect that today's hearing will be much like when hedge fund managers appeared before the House Oversight Committee in the fall and, under serious questioning, agreed to support further oversight.

"I think the bank executives are going to cry uncle and finally say: We will accept more regulation," Williams said.

Blankfein's emphasis on the importance of more market oversight follows a similar proposal from the Securities Industry and Financial Markets Association.

"Today no regulator has a 30,000-foot perspective of the system," group spokesman Travis Larson said. "A financial markets stability regulator with oversight of systemically important insurance companies, private-equity firms, hedge funds and other financial firms is absolutely key to building a stronger, more robust and resilient financial system."

Spokesmen for the eight executives appearing today declined to comment or did not respond to requests for comment.

But in previous statements, the executives have tried to strike a careful balance between acknowledging the need for more regulation and being reluctant to have rules stifling innovation. In a speech last year, Citigroup chief executive Vikram Pandit said there was a need for better regulatory oversight of systemic risk.

But he quickly added: "This doesn't mean deluging oversight agencies with data. That serves the opposite goal. We need transparency with a purpose."

http://www.washingtonpost.com/wp-dyn/content/article/2009/02/10/AR2009021003302.html?hpid=topnews

Sell-off manipulation for coming Hedge Fund Regulation ~ Obviously markets sold off to spite TS Geithner. The sell off was ruthless so markets must be expecting "tight control" regulation for Hedge Fund industry. Unregulated hedge fund industry is ruining our economy, many people wealth, and nation's wealth with massive financial wealth drain with colluded funds as well.

___________

Did Sell-Off Create Trading Opportunity?

Posted By: Lee Brodie | Web Editor

CNBC staff and wire reports

| 10 Feb 2009 | 05:39 PM ET

LACK OF DETAILS IN RESCUE PLAN DOOM MARKET

The Dow fell sharply on Tuesday after Treasury Secretary Tim Geithner rolled out a reworked financial rescue plan but did not provide enough details to satisfy investors.

Wall Street was hoping to hear specifics about how to mop up bad bank assets and revive consumer lending.

Main Points Of The Geithner Financial Stability Plan

1. Public-Private Fund to Buy $1 Trillion in Toxic Assets

2. Additional Capital for Banks

3. $50 Billion to Prevent Foreclosures

The Problems

1. Vague: Which Banks Get What?

2. Vague: Which Homeowners Get What?

3. Nationalizing the Losses, But Not the Profits?

4. Private Capital Has No Idea What the Plan Is

With the Geithner plan triggering more questions than answers, investors once again turned to the flight to quality trade -- and bid gold and Treasuries higher.

Considering the steep drop in financials, should you buy bank stocks on the dip?

The Fast Money Trades

If you want to play financials look at the book value of Wells Fargo versus JP Morgan , counsels Pete Najarian. Wells Fargo is still trading above its book value and JP Morgan still trades at a big discount. Consider a pairs trade, he says. And look at Visa and Mastercard . They’re not really affected by the new TARP.

In the materials space nothing has changed since yesterday, adds Tim Seymour. I see the underpinnings of increased demand in the space.

I think the sell-off presents an opportunity, says Guy Adami. I would look to Intel on the dip or even Bank of America as a trade, he says.

Bank stocks are trading vehicles only, reminds Jeff Macke. If you go to bed with Bank of America you’ll wake up with fleas. If you want a trade buy Morgan Stanley on the dip. Otherwise let things come back to you.

Musings From The Fast Money Traders

A centerpiece of the TARP now renamed "Financial Stability Plan" is a proposal to set up a public-private investment fund, in partnership with the Federal Deposit Insurance Corp, a bank watchdog, and the Federal Reserve, the U.S. central bank.

The traders like the concept but don't understand how the government intends to value toxic assets.

Private capital will bid on anything if they can figure out a way to price it but the plan has no way of pricing anything, says Jeff Macke’s. That’s what sent the market tumbling.

I wish they’d use Morgan Stanley as a test case, muses Guy Adami. They took their lumps and they’ve come out the other side. I think the message here is that banks need to take their lumps.

I agree, says Pete Najarian. Morgan Stanley and Goldman have taken their write-offs. Those are the stocks to put on your radar. Stay away from them money-center banks

I’m concerned that in his testimony Geithner told Congress that there are banks that are too big to fail, observes Dylan Ratigan.

I think we need to allow some banks to fail, adds Macke. Ultimately, people will step in and the markets will work.

And why can’t we let the bond holders fail too, adds Tim Seymour. Bond holders know they’re taking risk and with that risk comes failure.

We’re spending too much time propping up banks that are on the brink of failure, adds Macke. We’ve got to start thinking about other industries such as the automakers.

We don’t need these banks, adds Ratigan. We just need banks. Others will do.

What I think the feds should do is put a bottom on the toxic assets, says Guy Adami. For example, for every dollar of toxic assets, price them at 40 cents and let the chips fall where they may.

CNBC.com with wires

© 2009 CNBC

URL: http://www.cnbc.com/id/29119230/

U.S. Treasury Secretary Timothy Geithner announcing a new financial stability plan Feb. 10

Best of Luck and God bless ~ May God strengthen you that all the speech and the belief will not be trampled by massive manipulation.

U.S. Treasury Secretary Timothy Geithner outlined the first phase of the Obama administration’s economic recovery plan Feb. 10. The plan is fairly orthodox, even though its scope is vast. It might even prove profitable for the government.

Analysis

After three weeks in office, U.S. President Barack Obama’s administration outlined the first phase of its economic recovery effort Feb. 10. The plan at present requires no new actions or money from Congress. Instead, it relies purely on existing legal frameworks governing the Treasury Department and the Federal Reserve System, as well as authority and funding obtained by the Bush administration from Congress. The stimulus plan before Congress is another ball of wax completely, and if adopted, it would be the second leg of the administration’s anti-recession efforts.

While the numbers freshman Treasury Secretary Timothy Geithner provided as he sketched out the Obama administration’s plan Feb. 10 are certainly large — even mammoth — a deeper look reveals that the plan is neither creative nor new. This is not meant as a criticism of the Obama team — while the devil, of course, is in the details, the plan as announced looks quite sound. But not only does it look like a natural extension of, and a minor course correction from, the Bush administration’s bailout policies; it also is revolutionary neither in concept nor reach — only in scope.

Credit Crunches vs. Liquidity Crises

As Geithner stated, subprime mortgages lie at the heart of the crisis’ genesis, a diagnosis that is neither new nor controversial. People who should never have qualified for mortgages were encouraged to buy. The brokers who provided the mortgages in turn sold the loans to others, who packaged them together into tradable securities and sold them yet again. When the market functions normally, this secondary market allows investors to flood money into the system, dropping borrowing costs. But when home prices fall or foreclosures mount — both of which have happened in spades in recent months — it is impossible to separate the good loans from the bad in the securities. Shorn of the ability to assess how much any particular security is worth, no one wants to purchase them, so the entire housing credit system seizes up.

In September 2008, the problem broke out of housing and affected the broader financial system. Suddenly, banks were unwilling to lend not just to homebuyers, but also to each other. This proceeded on the reasoning that, lacking the ability to assess the stability of a prospective borrower’s asset sheet, lenders cannot in good conscience lend. Money thus stopped flowing completely. The accompanying graph demonstrates how the cost of lending between banks shot up during that time.

At this point, a technical distinction is required for clarity. When banks stop lending to each other, the economy does not face a traditional credit crunch, but a liquidity crunch. The money is there, it is just unable to flow to where it is needed. A liquidity crunch is perhaps the most damaging thing that can happen to a modern economy. Western banking systems exist to allocate capital to entities that will use it most efficiently and effectively. When banks stop doing that, everything in the affected economy that depends upon credit at all simply stops. Most of what the Bush administration did during the final four months of its term — and nearly everything it did in September and October 2008 — was aimed at mitigating this liquidity crisis. (For a thorough discussion of how it all went down, click here.)

Graph: 3-Month USD Libor

This liquidity crisis is pretty much over — in fact, it has been for several weeks. Interbank costs have plummeted, and interbank lending has broadly picked up again, as the graph demonstrates.

In contrast, the problem of today is a credit crunch. Liquidity is back in the system, but lending from banks to consumers and companies has yet to recover. Banks remain risk-averse not necessarily because they are worried about access to capital or the creditworthiness of their peers (the problem in a liquidity crunch), but because they are concerned about the creditworthiness of their potential customers. Credit checks have become more thorough, marginal borrowers have been declined, and loans on the whole have become harder to get.

While such circumstances are obviously recessionary, they are hardly unprecedented. In fact, what is happening now with the credit markets is the same thing that happens in every recession. Unlike the liquidity situation that the Bush administration struggled with in October and November 2008, the credit situation of 2009 is not extraordinary. Thus, the Obama plan for dealing with it is rather orthodox.

In essence, the worst is over for the United States. But we mean neither to belittle the pain of the recession, nor to wave away concerns for the future. Instead, we want to point out that the systemic danger has passed, and that the nature of the current problem lies within a more well-understood framework for which mitigation and recovery tools already exist. Some of these tools are simply part of the government’s normal tool kit; those that are not were crafted through congressional cooperation with the Bush administration within the last year.

The Obama Strategy

The Obama strategy can be broken into three pieces.

First, the Treasury Department, Federal Reserve, Federal Deposit Insurance Corp. and other government entities that touch upon the banking sector will run a “stress test” of every bank that seeks any sort of assistance. This test will focus on lending practices and balance sheets; qualifying banks can tap the Treasury for loans to help rationalize their balance sheets. The government will require banks receiving such loans to prove regularly that the government assistance is being used exclusively to extend credit to consumers. There must not be any excessive executive compensation (defined by the Treasury as an annual salary of more than $500,000), and the funds cannot be used to purchase other banks.

For funding, this program will use the final half of the $700 billion that Congress authorized to the Bush administration back in September under the Troubled Assets Relief Program (TARP). The primary difference between how the Obama and Bush administrations carried out the TARP is that the Bush administration simply wanted to shove as much cash into the system as quickly as possible to reliquify the system. As such, the Bush administration’s $350 billion simply went directly to the banks with few strings attached.

But the Obama administration does not have to deal with a liquidity crisis, so it is putting into place the safeguards, “stress tests” and lending requirements to minimize graft and maximize overall lending. The Bush team administered its half of the TARP money within a few short weeks; the Obama team’s controls mean it will take months to loan out its half. But bear in mind that the Obama team is addressing a fundamentally different issue than the Bush team was. Liquidity crises are economy killers, while credit crises are “merely” recession-causers. For the Obama team, there is not the same level of urgency the Bush team faced, so the Obama team can afford to take the time to apply its package more comprehensively.

In the second part of the Obama plan, the Treasury will set up a public/private investment fund to manage and dispose of the questionable mortgage-backed securities that touched off all of this in the first place (often referred to as a “bad bank”). The plan is to work with the private sector to set a price for the securities that is somewhere between what they were worth when they were originally formulated and their current near-worthlessness. (Remember, all of these securities are backed by actual homes with values that are far more than zero.) The Treasury will provide the initial funds to purchase the securities from banks, and the Fed will provide whatever financing is necessary. The plan is to clean the banks’ books while injecting capital, allowing the banks to make loans with more confidence. The government plans to provide $500 billion in financing immediately, and could apply $1 trillion before all is said and done.

Third, the government will participate in the secondary debt market for everything from car to college loans. Secondary debt is like the mortgage-backed securities discussed previously, e.g., loans that have been packaged together for trading. Geithner estimates that 40 percent of the capital that supports lending in the United States participates only in the secondary market. As long as banks and investors are skittish, this market does not operate smoothly. Up to $1 trillion will be applied to this via the Term Asset-Backed Securities Loan Facility (TALF), largely through Fed financing.

A Profitable Bailout?

Altogether this sounds like a lot of cash, and it is. The total price tag comes in at roughly $2.4 trillion, more than the entire government budget in a normal year. But this is not nearly as bad as it sounds. In fact, the government is likely to make money on this over time.

First of all, the TARP money is all loans. Banks that received the first batch from the Bush administration have to pay 8 percent interest annually. Additionally, under the terms of TARP, the banks had to give the government the right to veto policy decisions. So the Obama administration enters its time with TARP with all the tools in place to change bank policy to match national policy. Specific terms as to how the Obama team will rejigger TARP remain to be seen, but if anything, the terms of the TARP loans will be tightened — making it more likely that the government will come out ahead — rather than loosened.

Second, the public/private debt management effort almost certainly will produce a fat profit for the government. The government will be buying up the distressed securities at well below market prices, and then will sell them at a time and place — and most important, a price — of its choosing down the line, ostensibly after the housing market recovers. The problem is not that the money will disappear; it is instead an issue of opportunity cost and time frame. With a potential $1 trillion in assets under management, this program could well take more than a decade to flush out completely. The closest comparison in American financial history is the Resolution Trust Corp. (RTC), a federal program of the 1980s and 1990s designed to help the country recover from mass bankruptcies in the savings and loan sector. Once one adjusts for the change in the size of the economy from then to now, the RTC program was about half the size of Geithner’s public/private program, and it still took six years to complete.

Third and last, participating in the secondary debt market is a temporary measure, and the government fully intends to pull back from that market as soon as the private sector’s appetite for investment resumes. This is the only part of the program announced thus far that Stratfor anticipates will operate at a loss once all the accounting in finished. Debt trading works on the idea that private investors are better than the government at reducing costs and directing capital. So not only would government employees (albeit very knowledgeable and financially experienced employees) be playing the market, they will be doing so with the intent of keeping things moving rather than making money. That will generate losses. But even here, the price tag is not as bad as it sounds. While the Treasury will use up to $1 trillion to run this program, every asset purchased will be sold, so the cost will be largely administrative.

This does not mean that all of the Obama team’s policies will be cost-neutral. As noted in the first paragraph, this is only the first step of the Obama administration’s plans for dealing with the recession. Each of these steps deals with the financial aspects of the recession, and none actually changes anything directly related to how much trouble homeowners are having making their mortgage payments.

All of the spending and tax cuts in the stimulus package before Congress are funded with deficit spending — very real costs that will create very real debt that will definitely need to be paid back. Additionally, Geithner gave notice in his presentation that the administration will announce a fourth effort in the weeks ahead. That effort aims to provide debt relief to homeowners and small businesses, primarily to help prevent foreclosures. Stratfor does not wish to judge that effort before it is announced, but anything that uses the phrase “debt relief” normally has a lot of costs attached.

Sen. Richard Shelby has a well-paying job, and must be in cash or short and must be waiting for financial mass destruction.

__________

OK, That's Your Plan—Now Where's The Money?

Posted By: Albert Bozzo | Senior Features Editor

CNBC.com

| 10 Feb 2009 | 04:18 PM ET

The much-anticipated financial-rescue plan drew some positive reviews from business and Democrats in Congress, but failed to impress Wall Street.

Though some say the measures were a marked departure from the Bush administration’s efforts to prop up the financial system, critics say Treasury Secretary Timothy Geithner's financial plan doesn't offer a convincing strategy on how to deal with toxic assets and generally leaves funding questions unanswered.

“Its all generalities—it's more of the same,” said Lawrence White, a former White House economist and savings and loan regulator, now with NYU’s Stern School of Business "They don't seem to be able to go out with specifics. That’s what killed (former Treasury Secretary Henry) Paulson.”

"I think we need more information," Sen. Richard Shelby (R-Ala.) told Geithner during a Senate Banking Committee hearing on the plan on Tuesday. "We dealing with maybe trillions of dollars."

The plan did not, as many had hoped and expected, call for the creation of a free-standing entity—known as a "bad bank"—that would buy toxic assets from financial firms and then sell them back into the marketplace.

Instead, the plan calls for what some consider a murky, private-public partnership in the form of a fund to buy the assets, through some combination of capital and guarantee assistance.

Even opponents of the "bad bank" model were unimpressed.

“I am dubious about the cost to taxpayers of the vehicle that will facilitate sales of assets. “ said William Isaac, former FDIC Chairman. “It is a better approach than a bad bank, but depending on the amount and structure of government support, it could be extraordinarily expensive to taxpayers."

The plan calls for a public-private financing component, which could involve putting public or private capital side-by-side and using public financing to leverage private capital on an initial scale of up to $500 billion, with the potential to expand up to $1 trillion.

By most estimates, there are $1.5 trillion to $2 trillion in assets that fall into the troubled category, either in that they illiquid or non-performing.

Two key financial industry trade groups, the Financial Services Roundtable and American Securitization Forum, issued statements saying that supported virtually all of the financial stability plan's measures.

The Geither plan assumes that there’s adequate private sector capital available. There’s some agreement about that in Washington and on Wall Street.

Rep. Jeb Hensarling (R-Texas), who was among those in Congress pushing for a private capital component in the original TARP legislation, called the current idea "feasible" because there's a lot of money "sitting on the sidelines,” but still favors the insurance-based model he proposed, wherein firms participating in the asset transactions pay fees.

For Investors

# Plan Ahead: Buy Small-Cap Consumer Stocks

# Gold Seen Jumping to $1,200 as Bailouts Mount

# Time to Sell or Go Bargain-Hunting?

Carlye Group co-founder David Rubenstein, for one, recently told CNBC that “private equity does have capital.”

The fund, however, appears no more likely to solve the riddle of pricing, such that buyers don’t overpay and sellers don’t accept fire sale prices, even though the intent is to have private sector buyers essentially establish market prices rather than a government entity.

Rubenstein considers pricing the principal problem because “many people who own assets don't yet want to recognize that their value has gone down so much that when they sell they’re going to take a bigger write down than they would want to take.”

Rubenstein estimates it could take six to none months before sellers are willing to enter the market and accept a proper haircut.

What’s unclear, however, is how much government money such an approach will entail.

The Geithner plan doesn’t address that, nor does it indicate where the funding would come from. About $350 billion remains in the TARP, but given all the other measures in the plan, that might not leave much available, which would require another source of funding.

In a recent interview, Rep. Brad Sherman D-Calif.) shared his concerns about the government purchases or guarantees of bad asset purchase, saying if the Fed got involved "it would clearly give the government more money to work with.”

It’s no small matter because as Fed Chairman Ben Bernanke told a Congressional panel Tuesday, while the TARP authorized the Treasury to inject capital into banks, the Fed is only allowed to make loans under the Federal Reserve Act.

There were already questions about whether the administration plans to use a multiplier method in dealing with the troubled assets through the ring fence model rather than a virtual dollar-for-dollar approach. Those will probably also apply to new private-public fund model.

"There is an attempt as I sense of Treasury and the federal Reserve to find other conduit .for funds to be used or guarantees to be put in place that really do represent commitments, that don't have to be passed by Congress or openly declared,” Rep. Paul Kanjorski (D. Pa.) told Bernanke during the hearing.

The Fed has been loaning billions of dollars under section 13.3 of the Act, which authorizes it to do so under “unusual and exigent circumstances.”

By Bernanke’s count, the Fed now has a $2 trillion balance sheet, 95 percent of is devoted to supporting the credit markets but is "extremely safe, overly-collateralized” and raising money for the government.

Under the Treasury’s plan, the current TALF program could be expanded by up to $1 trillion to support business and consumer lending in the secondary markets.

When asked by one Congressman if the Fed could extend its balance sheet to $5-10 trillion, Bernanke didn’t rule it out, but was quick to add it depended on the length of loans, especially if they were short-term, as in over-night loans.

Hensarling told CNBC.com there "appears to be little check" over the Fed using its balance sheet and that if concerns remain “Congress would have to explore statutory authority to limit that

Sherman took a bolder approach Tuesday, telling Bernanke: “I cannot think of the words that will really limit you in terms of the quality of the loans you make.” If we're going to limit your power at all we could do so in terms off quantity

© 2009 CNBC.com

URL: http://www.cnbc.com/id/29124642/

This must be an attack against TS Geithner for an effort to regulate the hedge fund industry.

BKX ~ FAS/FAZ used Geithner to trash markets with huge volume right after 11 am.

Markets are using TS Geithner as a market manipulation toy -- The drop at 11 am when he started to speak. It will likely be the same in the future.

~~~

Treasury Secretary Geithner Outlines Financial Stability Plan

BKX ~ FAS/FAZ used Geithner to trash markets with huge volume right after 11 am.

Markets are using TS Geithner as a market manipulation toy -- The drop at 11 am when he started to speak. It will likely be the same in the future.

~~~

Treasury Secretary Geithner Outlines Financial Stability Plan

Markets are trashed and also at the same time running up deficit -- the worst of the combination -- big hedge funds are trashing mass.

WASHINGTON, Feb. 10, 2009(CBS/ AP) The Obama administration promised an aggressive effort to combat America's worst financial crisis in seven decades, unveiling a program that could mobilize well over $1 trillion in public and private support to get the frozen credit markets functioning again.

Treasury Secretary Timothy Geithner said Tuesday the new plan would bring the full force of the federal government to bear in a partnership with the private sector.

Obviously, markets are using Obama and Geithner as manipulation toys as market reaction has shown.

~~~

Geithner unveils new bank rescue plan

At long last, the Treasury Secretary has announced how the Obama administration will try to stabilize the financial sector.

Colin Barr, senior writer

Last Updated: February 10, 2009: 11:46 AM ET

NEW YORK (Fortune) -- Treasury Secretary Tim Geithner sketched out the broad strokes of the latest government attempt to stabilize the financial sector Tuesday morning.

Speaking in the Cash Room at the Treasury Department in Washington, D.C., Geithner introduced a four-point plan that aims to restart the flow of credit to businesses and consumers.

And markets said:

![]()

Geithner Unveils New Plan To Bail Out US Banks

BANKS, GEITHNER, TREASURY, SUMMERS, ECONOMY, BAD BANKS

CNBC.com

| 10 Feb 2009 | 11:14 AM ET

The US Treasury Department unveiled a revamped financial rescue plan to cleanse up to $500 billion in spoiled assets from banks' books and support $1 trillion in new lending through an expanded Federal Reserve program.

The renamed "Financial Stability Plan," rolled out by Treasury Secretary Timothy Geithner at the Treasury, will also devote $50 billion in federal rescue funds to try to stem home foreclosures and soften the crushing impact of the deep housing crisis now afflicting the entire economy.

TS Geithner, Obviously not effective as markets are using TS Geithner as a market manipulation toy -- The drop at 11 am when he started to speak. It will likely be the same in the future.

He could not be very effective as he is just used to manipulate markets -- the same as what he is planning to do.

~~~

Treasury Secretary Geithner Outlines Financial Stability Plan

Treasury Secretary Tim Geithner is expected to announce Tuesday the Obama administration's long-awaited plans to address the foreclosure crisis.

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=35479387

Bad Bank 2.0 package will be unveiled Tuesday by Treasury Secretary Timothy Geithner at 11 am EST. CNBC.com will carry the speech live.

CNBC will also interview Geithner after the speech at 12 Noon EST. It will be his first television interview since becoming Treasury Secretary

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=35472525

$BKX retesting the 25 bottom with positive divergence.

Obama: Wall Street Bonuses 'Outrageous'

The Associated Press

| 29 Jan 2009 | 03:57 PM ET

President Barack Obama says it is irresponsible and shameful for Wall Street bankers to be paid huge bonuses at a time when the American public is dealing with economic hardship.

The president reacted harshly Thursday to reports that corporate employees got paid more than $18 billion in bonuses last year. Obama said, "That is the height of irresponsibility. It is shameful. It's outrageous."

The president said he and new Treasury Secretary Timothy Geithner will have direct conversations with corporate leaders to make the point.

URL: http://www.cnbc.com/id/28917969/

TARP Panel Report Cites Regulatory Failures In Crisis

Posted By: Albert Bozzo | Senior Features Editor

CNBC.com

| 29 Jan 2009 | 08:27 AM ET

The Congressionally-appointed panel overseeing the TARP program today will release a stinging report of the regulatory failures that led to the current financial crisis.

A copy of the draft report, which will be presented to Congress, was obtained by CNBC.com.

“The regulatory system not only failed to manage risk, but also failed to require disclosure of risk through sufficient transparency,” the report concludes.

Among the report’s recommendations are that future regulation include better oversight of systemic risk, reducing the potential impact of “too-big-to-fail” institutions; improved transparency through “better, more accurate credit ratings” and better regulation of consumer products, which would “curb excesses in mortgage lending.”

The panel’s report also calls for the creation of executive pay structures “that discourage excessive risk taking.”

The panel was created under the Economic Emergency Stabilization Act, which was signed into law in October and authorized the Treasury to spend up to $700 billion in propping up the financial system.

The panel, known as COP (Congressional Oversight Panel), is headed by Harvard University professor Elizabeth Warren, who has been consistently critical of the TARP program’s administration under former Treasury Secretary Henry Paulson.

The 78-page report includes so-called “alternate views” from one panel member, which include making the Federal Reserve the “systemic regulator.”

The COP report also identifies three “highly technical issues” that have had a key role in the regulatory structure that need serious review by the agencies with oversight: accounting rules, securitization of debt and short selling. The report says COP also plans to “address financial architecture” in a future report.

© 2009 CNBC.com

URL: http://www.cnbc.com/id/28910947/

Treasury Aims To Keep Lobbyists Off TARP

WASHINGTON, Jan. 27, 2009 (CBS/AP) Treasury Secretary Timothy Geithner, in his first full day on the job, announced new rules Tuesday to limit special-interest influence on the government's $700 billion financial rescue program.

The new rules are designed to crack down on lobbyist influence over the rescue program and make sure that political clout in not a factor in awarding rescue money.

Obama administration officials said they go farther than the lobbying rules imposed by the Bush administration and are designed to ensure that bailout money is distributed with the goal of promoting the health and stability of the financial system.

"American taxpayers deserve to know that their money is spent in the most effective way to stabilize the financial system," Geithner said in a statement. "Today's actions reaffirm our commitment toward that goal."

Treasury's new rules restrict the contact officials can have with lobbyists in connection with applications for funds from the bailout program. The new restrictions are modeled on the limits that are imposed on political lobbying of Treasury Department officials on tax matters.

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=35119490

Geithner was sworn in shortly after 7:30 p.m. President Barack Obama attended the ceremony, Vice President Joe Biden Administered the oath of office.

(AP Photo/Ian Barrett)

Timothy Geithner, the New York Federal Reserve Bank president whose failure to pay tens of thousands of dollars in taxes threw his nomination as Treasury secretary into jeopardy, was today confirmed for the job by the Senate.

The vote was 60-34. Geithner earlier cleared the Senate Finance Committee with an 18 to 5 vote; one of the dissenters, Mike Enzi, said that "in previous years, nominees who made less serious errors in their taxes than this nominee have been forced to withdraw."

The Obama administration backed Geithner despite his tax problems, however, and consensus formed in Washington that the country's economic problems were too significant for Geithner's "careless mistakes" to derail his nomination.

The 47-year-old is seen by many as the best candidate for the job, and there was concern that rejecting him would mean a delay in confirming a replacement that the country could not afford.

"The economic situation is so tense right now and I don't want see us go back to square one and wait several weeks or longer for the process to bring in a new treasury secretary," Republican Sen. Arlen Specter said today, according to the Associated Press, in explaining his support for Geithner.

Geithner will oversee the Internal Revenue Service and oversee President Obama's efforts to stimulate the economy.

http://www.cbsnews.com/blogs/2009/01/26/politics/politicalhotsheet/entry4754254.shtml

Geithner: Strengthen Derivatives, Hedge Fund Rules

Reuters

| 23 Jan 2009 | 12:10 PM ET

U.S. Treasury Secretary-nominee Timothy Geithner Friday pledged to strengthen regulation of over-the-counter derivatives and pursue registration of hedge funds to improve market transparency.

In written responses to questions from Sen. Carl Levin, a Michigan Democrat, Geithner said the current regulatory system for derivatives and complex structured financial products failed to adapt to new risks.

"We are going to need sweeping changes, in regulatory policy, the oversight structure and in our tools for crisis management," Geithner said in his responses.

Geithner faces a confirmation vote by the full Senate on Monday amid controversy over his underpayment of self-employment taxes.

He said if confirmed, he would pursue a stronger and more comprehensive framework for regulating derivatives markets to bring greater transparency, accountability and safety to these markets, which have been blamed for deepening the current financial crisis and recession.

# Geithner signals tougher stance on China

"There may be a number of ways to achieve this, but steps to be taken in the short-term include bringing standardized products within centralized clearing mechanisms and setting an effective statutory and regulatory framework for regulating all derivatives," Geithner said.

He added that he would also consider the consolidation of financial regulatory agencies—a goal proposed by the previous Treasury secretary Henry Paulson.

Regarding hedge funds, Geithner said he believes better federal oversight was needed for hedge funds, whose destabilization could seriously disrupt markets and credit flows. "I support the goal of having a registration regime for hedge funds because we need greater information and better disclosure in the marketplace. I believe that we should also establish an effective regulatory framework for derivatives dealers."

Geithner also endorsed continuation of mark-to-market accounting rules, saying they help protect investors and promote transparency.

Copyright 2009 Reuters. Click for restrictions.

URL: http://www.cnbc.com/id/28813934/

Geithner Is Sworn In as Treasury Secretary

Reuters

| 26 Jan 2009 | 06:38 PM ET

Timothy Geithner was sworn in as U.S.Treasury secretary on Monday a little more than an hour after the Senate approved him, and he vowed to move quickly to aid the distressed U.S. economy.

"We are at a moment of maximum challenge for our economy and our country," Geithner said at a swearing-in ceremony as he stood by the President Barack Obama's side. "Our agenda is to move quickly to help you do what the country asked you to do," he told the president.

http://trend-signals.blogspot.com/2009/01/ts-geithner.html

Who are concerned about the news on Geithner.

Market manipulation ~ re Geithner Confirmation as Treasury Secretary Likely Next Week

__________________________________________________________________

Who are concerned about the news.

TS Paulson role was really nothing more than market manipulation.

Geithner's Statement

Reuters

| 21 Jan 2009 | 10:23 AM ET

http://www.cnbc.com/id/28770843

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=34966495

$BKX 3 peaks & Domed house ~ decade old massive financial scam using all kinds of financial instruments, repealing and forming bills such as Glass-Steagall, and naked short-sellings, etc. -- completed on the Bush last day.

Bombing hell out of $BKX to 25.34, near to all time low, just same as bombing hell out of Gaza. It's absolutely robbing massive wealth around the world.

http://trend-signals.blogspot.com/2009/01/bkx-2534.html

How to judge if your credit-card issuer is being unfair or deceptive

By Gail Liberman and Alan Lavine

Last update: 7:00 p.m. EST Jan. 19, 2009

PALM BEACH GARDENS, Fla. (MarketWatch) -- Ever wonder whether a credit-card issuer's offer to you or treatment of your account is "unfair" or "deceptive?"

If it is, your lender could suffer a penalty, which can vary dramatically from a maximum civil penalty of $11,000, to more than $1 million per violation -- per day. Whether you get reimbursed and by how much depends upon the regulator involved and state and federal rules.

The FDIC has detailed how to detect unfair or deceptive credit-card practices in its winter "Supervisory Insights" letter to banks.

Here, according to the FDIC, is a three-pronged test to assess whether a credit card representation, omission or practice is "deceptive." All three of the following conditions must be met:

1.

It must mislead or be likely to mislead the consumer. Example: The phrase "6% cash back" appears 13 times in a credit-card solicitation, but the bank failed to prominently disclose that the actual "cash back" bonus was tiered. Only purchases between $40,001 and $50,000 actually earn that 6% cash back. Plus, no reward is paid until the earned rewards for the year totaled $50. "The likelihood of a consumer being misled by an advertisement or direct solicitation increases with the repetitiveness of the unqualified representation," the FDIC warns.

2.

For a practice to be deceptive, the consumer's interpretation of credit card offers must be reasonable under the circumstances. The FDIC details one woman's "reasonable" interpretation of a solicitation from a bank offering zero percent interest for 12 months on balance transfers. The problem: The bank never disclosed -- either in its solicitation or in the credit card agreement -- the actual date the promotional rate expired. Upon her own interpretation of that date, the woman, despite faithfully making minimum monthly payments, was zapped with a charge of $19.89 in interest. Reason: The bank posted her final payment at a later date than she had calculated. The FDIC says the woman's interpretation of when the promotional rate expired was reasonable, given conflicting representations or repeated omissions in the solicitation and the card member agreement. The FDIC also warns that in marketing materials to the elderly, students or the financially unsophisticated, the "reasonableness" of a consumer's interpretation must be judged from the vantage point of a reasonable member of the targeted group.

3.

The misleading representation, omission or practice must be material. Examples of material information: Costs, benefits or restrictions on the use or availability of a product or service. For example, radio ads invite you to call for a free credit report, with no qualifications or conditions. Suddenly you apply for credit, obtain it, but are charged the cost of the credit report at closing. Problem: Nothing in the bank's records or promotions suggests consumers would be charged a fee for the credit report upon acceptance of a loan. This fee is "material," because it influences your decision.

To determine whether a credit-card practice is "unfair," all three of the following conditions must be met:

1.

The act or practice must cause or be likely to cause substantial injury, which usually involves monetary harm, to consumers. Trivia or speculative harms are typically insufficient. Example: Your bank charges multiple rates, but applies card payments so that the lower rates are paid off first. This leaves your higher-rate balances to accumulate more interest. While one customer may not have been substantially impacted by this practice, the FDIC says it may judge injury caused to a group of consumers "substantial."

2.

Consumers must not reasonably be able to avoid the injury. Example: A check bounces only because the bank, unbeknownst to the customer, reduced the customer's credit limit after the customer had already issued the check. This unavoidable situation led to a host of possible fees.

3.

The injury must not be outweighed by offsetting benefits. Take the common practice mentioned above of charging multiple interest rates, but applying card payments so that lower rates are paid off first. The substantial injury caused by this practice may be outweighed by the offer of low promotional rates for balance transfers. In that case, the practice may not be judged "unfair."

The FDIC stresses that other regulations may be cited in determining whether an act or practice is unfair.

Score update

In another matter, Fair Isaac Corp., the provider of the dominant FICO credit score, says 1.5 million customers who have a bank account can check FICO credit scores online for free. Its "Scores on Statements" program is offered by Pennsylvania state Employees Credit Union, Chase and HSBC banks.

What about free scores for those who more desperately need a FICO score because they can't qualify for a bank account? Craig Watts, spokesman for the Minneapolis-based company, says that's being worked on. The hang-up, he says, lies with the three major credit bureaus -- Equifax, Experian and Trans Union.

Spouses Gail Liberman and Alan Lavine are syndicated columnists. Their latest book is "Quick Steps to Financial Stability" (Que/Penguin). You can contact them at www.moneycouple.com.

Citigroup Splits Into Two After Losing $8.3 Billion

CITIGROUP, BANKS, FINANCIALS, EARNINGS, CREDIT, STOCK MARKET

Reuters

| 16 Jan 2009 | 10:21 AM ET

Citigroup, scrambling to survive losses triggered by the credit crunch, unveiled plans to split in two and shed troubled assets, and reported a quarterly loss of $8.29 billion.

The banking giant also said it expected more departures from its embattled board, which is losing former Treasury Secretary Robert Rubin as a director later this year.

URL: http://www.cnbc.com/id/28688568/

Geithner Faces Questions On Housekeeper, Taxes

CNBC staff and wire reports

| 13 Jan 2009 | 04:39 PM ET

Treasury Secretary nominee Timothy Geithner is facing questions over the immigration status of a former housekeeper and whether he paid Social Security and Medicare taxes.

Sen. Charles E. Grassley, the ranking Republican on the Senate Finance Committee, has raised questions about both issues, the Wall Street Journal reported, though Senate Democrats told CNBC that they don't think this will derail the nomination. Geithner's confirmation hearing is scheduled for Thursday.

According to the Journal, the former housekeeper's immigration papers expired while working for Geithner, though she later received a green card and became legal. The second question involved employment taxes while Geitner was working for the International Monetary Fund from 2001 to 2004.

# Click Here to See Geithner's Tax Documents

Senate Finance Committee Chairman Max Baucus (D-Mont.) has summoned committee members to his office this afternoon to discuss the matter.

Geithner informed the Senate panel that he had made a common tax mistake while working for the IMF, an official with the Obama transition team told Reuters. The official said the error stemmed from an unusual payroll system that U.S. employees of the IMF and other international organizations must use.

"This unusual payroll system commonly creates confusion among U.S. employees,' the official said. Geithner realized the error in November during the review process for his nomination and immediately corrected it, the official added.

"All of his taxes have now been paid in full, and at no time was there any intention on Mr.Geithner's part to avoid taxes,' the official said.

Geithner's nomination to replace Henry Paulson as Treasury secretary has been widely praised in Washington and on Wall Street.

"Geithner is a solid choice. He has shown more independent thinking," said Former Sen. Don Riegle, who chaired the Senate Banking Committee during the savings and loan crisis. "He has also seen this financial system meltdown from the inside ... he can offer highly skilled and pragmatic advice to Obama."

Geithner's task will be enormous, however. The US is facing a worsening economy, prolonged credit and housing crises as well as rising unemployment. Geithner, however, has been closely involved in federal efforts to deal with the financial crisis, having worked with Treasury Secretary Henry Paulson and Fed Chairman Ben Bernanke

Some, however, think that Geithner might be too closely linked to the highly criticized management of the $700 Wall Street bailout fund, known as the Troubled Asset Relief Program, or TARP.

"There's a little bit of a question because he's associated with the bailout," said James Awad, managing director of Zephyr Capital. "And that's still a work in progress and not totally successful. There will be a few who'll be upset because he's associated with the TARP."

Still, "I would think the market is going to like it," Awad added. "People will view it as a safe choice, an experienced guy."

According to the New York Fed Web site, Geithner graduated from Dartmouth with a bachelor’s degree in government and Asian studies in 1983 and from the Johns Hopkins School of Advanced International Studies with a master’s in International Economics and East Asian Studies in 1985.

He joined the Treasury in 1988 and worked in three administrations, serving as Under Secretary of the Treasury for International Affairs from 1999 to 2001 under Rubin and Summers.

He become New York Fed president in 2003. In that capacity, he worked as the vice chairman and a permanent member of the Federal Open Market Committee, the group responsible for formulating the nation's monetary policy.

© 2009 CNBC

URL: http://www.cnbc.com/id/28641283/

Citigroup, Morgan Stanley Agree to Merge Brokerages

C, MS, BANKS, SMITH BARNEY, CITIGROUP, MORGAN STANLEY

Posted By: Charlie Gasparino | On-Air Editor

CNBC.com

| 13 Jan 2009 | 03:51 PM ET

Citigroup has agreed to merge its Smith Barney brokerage unit into Morgan Stanely's brokerage operations, the first step in ultimately shedding Smith Barney and a move away from the financial supermarket model that Citigroup has followed for the past decade.

The boards of both Citigroup and Morgan Stanley have approved the joint venture, CNBC has learned.

Under the agreement, Morgan Stanely will control 51% of the joint venture with the right to increase its share in future years. In effect, the deal will give Morgan Stanley control the nation's largest brokerage firm, with 18,000 financial advisers, compared to the 16,000 at the Merrill Lynch subsidiary of Bank of America .

The deal would provide a capital boost for Citigroup, but it will also be the first step toward the break up of the massive investment bank, which is under pressure to raise capital to stem losses. Citigroup is expected to announce another massive loss for its fourth quarter.

As reported earlier Tuesday, Citigroup CEO Vikram Pandit plans to announce in the coming days a major shift away from the "financial supermarket" model that has guided the bank for the last decade.

Video: CNBC's Charlie Gasparino discusses Citi's plan to focus on its core business.

The breakup of the supermarket model—in which a bank handled a client's every financial need, from investing to insurance—would mean that Citigroup would become more of a traditional bank like JP Morgan Chase .

The core of the remaining company would be a global wholesale bank with some investment banking capability and include private and regional banking.

Citigroup's former CEO Sandy Weill developed the financial supermarket model in 1998 when he fought successfully to allow the merger of Travelers with Citibank.

The merger circumvented the Depression-era Glass-Steagall Act that separated commercial and investment banking and helped pave the way for the banking behemoths that have been crumbling during the credit crisis. Glass Steagall was repealed in 1999.

The dismantling of Citigroup's supermarket model is being made under pressure from the federal government, which has loaned Citigroup $45 billion in recent months and agreed to absorb the losses on a huge pool of mortgages and other assets.

URL: http://www.cnbc.com/id/28642133/

re Pull out all stops for grim economy

The same madness which robbed U.S. especially during the last several years with spend, spend, and spend theme.

We have speculations that USA can not last more than a few years with escalating national debt.

We need to stop this madness before detrimental debt blows up.

http://www.pgpf.org/resources/PGPFCitizensGuide.pdf

http://www.brillig.com/debt_clock/

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

By Ros Krasny Ros Krasny 2 hrs 39 mins ago

SAN FRANCISCO (Reuters) – The U.S. economy faces a potentially long period of weak growth and a rising risk of deflation, making it worth "pulling out all the stops" with a big fiscal spending program, Janet Yellen, president of the San Francisco Federal Reserve Bank, said on Sunday.

"The financial and economic firestorm we face today poses a serious risk of an extended period of stagnation -- a very grim outcome," Yellen said on a panel discussion at the American Economics Association's annual meeting in San Francisco.

"If ever, in my professional career, there was a time for active, discretionary fiscal stimulus, it is now."

Yellen said she was skeptical about suggestions for broad-based, permanent tax cuts and backed the "diversified package of policies" suggested recently by the International Monetary Fund.

Specifically, Yellen urged "spending on goods and services with higher rather than lower social value," but said measures should be consistent with "long-term fiscal discipline" to be the most effective.

If the public doesn't believe that spending increases are temporary, then long-term interest rates are likely to rise in response, "undercutting, conceivably even overwhelming, the short-term stimulus," Yellen said.

President-elect Barack Obama has said that signing a major economic stimulus package will be his first priority when he takes office, with a goal of creating or saving 3 million jobs over two years.

Speaking on the same panel as Yellen, renowned economist Martin Feldstein said that $300 billion to $400 billion in fiscal measures in 2009 and 2010 seemed justified.

Feldstein, former head of the National Bureau of Economic Research, also warned that the current recession, with its roots in a financial crisis rather than restrictive Fed interest rate policy, could easily drag on for the rest of 2009.

DEFLATION RISK

With the United States already bogged down by a year-long recession, Yellen said there is a rising risk of deflation, or a persistent decline in prices that could cause consumers to delay purchases, dragging down the economy further.

"With an extended period of abnormally high unemployment in the forecast, it is increasingly likely that inflation will fall to undesirably low levels," she said.

That, in turn, would risk pushing up real interest rates as inflation expectations decline at a time the Fed has already reached the "zero bound" on official rates.

Yellen said the trigger for the current recession, the eruption of a severe financial crisis, suggested U.S. growth would remain weak "for an extended period."

"The current downturn is likely to be far longer and deeper than the 'garden-variety' recession in which GDP bounces back quickly," she said. "Many forecasters expect this to be one of the longest and deepest recessions since the Great Depression."

Yellen said the Fed has not run out of monetary policy options, despite having set its official lending rate at a rock-bottom range of zero to 0.25 percent in December.

The Fed's "nonconventional measures" would likely remain focused on improving the functioning of credit markets, complementing the actions of the Treasury and the Federal Deposit Insurance Corp.

A "thoroughgoing report of the financial system" is essential for a sustained economic recovery but will be "a long, drawn-out process," she said.

(Editing by Leslie Adler)

http://news.yahoo.com/s/nm/20090104/bs_nm/us_usa_fed_3

re: Oil Falls to $37, Down 60% in '08

Oil at this price is certainly helping financial markets in check.

~~~~~~~~~~~~~~~

Reuters

| 31 Dec 2008 | 07:22 AM ET

Oil slid below $37 a barrel on Wednesday, heading for a fall of more than 60 percent in 2008 as

the global economic slowdown bit deep into energy demand.

Crude oil hit an all-time high of more than $147 in July but rices have collapsed in the last six months as the credit risis has pushed the industrialized world into recession.

Dismal data from the United States on Tuesday added to pessimism that oil demand would suffer further in 2009, countering any support from Middle East tensions and hopes for another Saudi output cut.

Analysts forecast an average of $49 a barrel for U.S. crude in the first quarter, and an average of $58.48 for next year, down $14 from their previous forecasts, the latest Reuters poll showed.

U.S. crude oil futures for February dropped. London Brent also fell .

"We expect energy prices to remain on the defensive through the early weeks of the New Year, presuming of course that the fighting in the Middle East does not spill over into other countries," MF Global said in a note to clients.

Deteriorating Economy

A dealer with a large U.S. broker agreed:

"The fundamentals of this oil market are horrible. Demand is falling and there seems no reason to buy," he said. "There is still plenty of room to go lower."

Oil jumped as much as 12 percent on Monday after Israel launched its air offensive on Gaza but prices slipped back quickly and analysts said they saw very little risk of the conflict disrupting oil supplies from the Gulf.

Foreign powers have stepped up calls on the warring parties to call an immediate ceasefire.

The market focus is on the deteriorating economy.

For Investors:

# Get Latest News from Oil and Gas Sector

# Get After-the-Bell Dow 30 Quotes

# Credit Spreads and Libor Data

# Futures and Pre-Market Data

The United States saw its worst job market in 16 years hammer consumer confidence to a record low in December, the shopping season was the worst since at least 1970, and prices of

U.S. single-family homes in October fell a record 18 percent from a year earlier.

U.S. retail gasoline demand for the week ending Dec. 26 dropped 3.8 percent from the same week a year ago, as drivers tightened their belts over Christmas, a MasterCard survey

showed.

Weekly U.S. inventory data due later on Wednesday will give more clues on the impact on oil use.

A poll of analysts forecast U.S. crude stocks fell by 1.5 million barrels last week, while distillate inventories rose by 1.1 million and gasoline increased by 1.5 million.

Top OPEC exporter Saudi Arabia is set to cut oil supplies further in February, market sources said on Tuesday, potentially taking output below its agreed OPEC target.

With oil coming off more than $100 from its record peak mid-year, the Organization of the Petroleum Exporting Countries has announced its biggest-ever production cut of 2.2 million barrels per day to fight the price slide.

The group already has cut output three times in an effort to remove about 5 percent of world supply.

Copyright 2008 Reuters. Click for restrictions.

URL: http://www.cnbc.com/id/28439470/

With tamed energy/oil price, so far, after initial market hype by some, we are in recession - depression outlook unless Obama comes up with some good idea to stimulate economy and unless markets provide some stability.

Oil staying around 40 +/- is certainly fair.

We r in deflationary period now! Only recession! or chronic stagnation..