News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Splinter, Look at the data not a fancy website and PR news about intent. That is not a reason to invest.

Experts say to call the company and see if you can buy any of the items they sell. That is why so many are in the mining industry (gold, Lithium, Uranium etc) because it’s a hot topic and you can’t buy the products so the pump is covered by a huge (fake) operation with no products.

You can see the reverse merger data, the debt, the float, the authorized; you can cross-reference the address and phone number (usually they are to lazy to switch addresses and also they know NO ONE looks at data).

If they have no debt, they cant be a pump and dump, If they HAVE DEBT, they turn that into huge revenue! $20-$250,000,000 or more!

ALL pump and dump schemes have debt and little to no revenue. The debt is their revenue!

When you connect the dots, the end result is Scheme pump and dump! The problem is finding one that IS NOT a scheme pump and dump.

You are looking at one now!

$GNGR

How do they turn debt into revenue?

"Debt is what makes them the money, you get rid of debt you lose your revenue."

Thank you

Apparently I have a lot to learn.

How do I learn it?

Splinter, Here is a perfect example of what is headed our way.

An abundance of new OTC AI tickers.

PMEDF a NEW artificial intelligence ticker just arrived. It was previously two different companies. Also the address in Canada is also the registered address of First Lithium Mining. When Marijuana stocks were the hot topic that switched to Lithium mines that are now switching to AI tickers because AI is HOT right now.

They have as authorized, UNLIMITED shares (more then 100 billion if they want). Since this looks like a new issue with the data not up to date yet, I see this price going UP before the crash back down. My reason is that they can’t make much money selling at the start at shares priced so cheap. Or can they?

They usually want to make the huge hit at $1 more or less before the debt conversion, and BOY do they have debt! But then again with unlimited shares, they don’t have to change the authorized so this may in fact be the scheme that just starts low and sells billions at $.07 on down to $.000001. Usually they add to the authorized after the high priced shares are sold but since they have unlimited, I would not risk too much betting it goes higher.

They will probably sell 20-100 million between $.02 and $.10 (because their float is only 68,000,000 also dated 2022). Since they have debt and unlimited shares already, they may just short the $.07 and sell 500,000,000 and take in $35,000,000 cash! Add the debt shares to cover the 500,000,000 short and that will be the new float (still low for a scheme) but then soon after that the decline to $.01 on down to $.0001 selling off another 2,500,000,000 at even $.01 is another $25,000,000 for a total of

$60,000,000 (Sixty million) all from $1000 in PR news releases.

You think with $60,000,000 they would just pay off the $1.5 million in debt? No way! Debt is what makes them the money, you get rid of debt you lose your revenue. And also because the $60,000,000 does not go to the company.

I guess that explains a lot.

You are aware their corporate headquarters is in a UPS store!

That ticker had a 15/1 split then a reversal of 1/85.

They have debt and little revenue. The shares are $3.28 but very few trade.

If the company has,

No revenue

LOTS of debt

Compensation members

And very few shares trading to justify enough capital to come in to pay debt and compensation, where is the money coming from?

They have a very low float and 300,000,000 authorized (similar to SGMD). Now here is the question you have to ask yourself.

How are they paying the employees, the overhead, paying off debt, compensating members?

All that takes CASH that they clearly show they do not have. Selling shares at $3 initially and only selling a few thousand is far from the capital needed to expand the operations and to be honest I read their data and still don’t know what it is they do. Usually is nothing.

The ONLY way they can make money at this point is to SELL SHARES! But they can’t sell many at $3+ so they must soon start the debt process. Thanks for the link, I may short this one as well at $3 and buy back at $.05

The 3 main people are listed as compensation committee members (debt holders eventually) or will just sell the $3 shares and take all that loot.

They cannot sustain the public entity with their business model and alleged revenue and with the $3 shares, there is just not enough cash coming in to keep things alive especially when compensated members are taking all the capital.

If they claim to have made $53,000 (and that is dated 2022) so my guess is a reverse merger soon into an AI company. But with no revenue data since 2022 and the float of 600,0000 is also dated 2022 so you don’t know what they are making or have in the float.

Great transparency!

They also have a 60% short interest that will likely remain open until the shares drop in price or they release debt shares to cover the shorts. You can’t make money on a company that has huge debt, no revenue and compensated board members with no real business operations. Money does not fall from the skies. But it is free when you legally take it from investors.

Remember this. It is their money; only theirs and investors get none of it. When others invest you think those who paid less will cash out? That is why they keep the price on a downward spiral so no one can sell except the schemers.

If the company sold 10,000 shares at $3 and they took in $30,000 and the stock went to $5 per share, most who paid $3 will sell, that means investors make money but when that happens, the scheme loses money and the schemes never lose money!

To keep the cash coming in for just themselves preventing anyone else from selling, they keep the price down and debt dilute further and end up dumping 5 billion at $.01 to make $50,000,000. No one can sell except at a loss while the schemes makes money even when the shares drop in price.

So far the ONLY ticker we can find with no debt, profitable and no debt dilution with a low float?

Your looking at it!

$GNGR

What you failed to notice is our plan only helps us not you. You are prevented from buying any more GNGR and that is how we want it. So I am not pumping to anyone to buy GNGR, I'm showing why others are bashing it and why good things happen to good companies regardless of share price or trading platform.

Choose your tickers structure.

Hot pumped intent plan (Bad but looks exciting)

Debt dilution (Bad)

Large float low price (Bad)

Large float high price (Even worse)

Audits (Legitimizes fraud, Bad)

Previous ticker change (Bad)

No products you can buy and have no operations (Very bad)

Vs.

Low float, No debt (Great)

Products you can buy and see sell (Great)

No hanky panky or questionable issues (Great)

Low share price on the above, low float and validity (Better then Great)

Do you choose Bad or Great?

Disagree Bar1080 is consistent. But you seem dangerous. Stating how bad it is and pumping a big plan you have for GNGR.

That seems more like a question for Bar1080 not me.

Mallenv

So with everything you post why would you be buying any OTC stock.

If the entire market is a scam what is your reason to buy

Do you just post how bad it is to save investors

Just wondering you spend a lot of time and effort on the boards

I have seen two CEO's agree to terms and they meet and sign all the contracts but at the last minute they switch to a new document with the last page altered. One day the CEO gets a court order to hand over controlling shares in his company.

I have seen wording that is so confusing it seems like a good thing. Little things to make the CEO excited I have seen are, "In the event the shares go higher then the agreed price, we would like to know that the company will allows us more options for shares at the higher price" and also if the opposite should happen. This is how we committed to great future with you company”. (The opposite is they can get more shares for their money as the price drops they end up owing the company).

Also many CEOs are so far into the failed ticker they just sign anything at that point.

As for audits? Some think audits means legitimacy? Look at all the pump and dumps that are audited. Audits mean NOTHING on any given ticker. The more a pump and dump adds audits, fake purchase orders, and fancy PR’s the more money they make.

If people say they only buy into an audited company then what do they look at to be convinced they are legit, if it’s just the audit you’re DOOMED!

You are better to buy shares in an EM market stock that has no audits but has the proper structure. Structure is REAL and tells the storey about a company that no audit, PR, intent news, or people pumping can. DO you buy into reality or the dream?

Since most dream stocks sell 1,000,000 shares for only $100, the LOTTO mentality kicks in not reality. The hope is they go to $1 and that dream negates reality and the schemes know very well how to sell the dream.

Look at

SGMD “Audited” stock hit $.000001

BRGO “Audited” stock his $.000001

And 100’s more!

All an audit does is make FRAUD LEGITIMATE! Period and 100% fact.

Some will be penny stock exempt so they don’t have to register with the SEC by achieving one of these requirements.

1) A price of over $5 per share, 2) the issuer has Average Revenue of at least $6 million for the last 3 years, or 3) the issuer has Net Tangible Assets in excess of $2 million if the issuer has been in continuous operations for at least 3 years or $5 million if less than 3 years. See: SEC Rule 3a51-1 - Definition of a Penny Stock

Look at GBTC, one of the biggest (over $2 billion) money raising schemes I have ever seen. Audit, penny stock exempt and still they post this on their disclaimer. IF you can make out what this means, please let us know.

Investments in the Products are speculative investments that involve high degrees of risk, including a partial or total loss of invested funds. Grayscale Products are not suitable for any investor that cannot afford loss of the entire investment. The shares of each Product are intended to reflect the price of the digital asset(s) held by such Product (based on digital asset(s) per share), less such Product’s expenses and other liabilities. Because each Product does not currently operate a redemption program, there can be no assurance that the value of such Product’s shares will reflect the value of the assets held by such Product, less such Product’s expenses and other liabilities, and the shares of such Product, if traded on any secondary market, may trade at a substantial premium over, or a substantial discount to, the value of the assets held by such Product, less such Product’s expenses and other liabilities, and such Product may be unable to meet its investment objective.

WHEW!

Audits are now used to legally tell lies only it’s certified. Audits are not a sure thing, and there are 100s of SEC (Questionable) lawyers that will issue an opinion letter for a few bucks knowing they may not be 100% accurate.

Look at the list of banned lawyers on the FINRA website, blow your mind! I guess some hacks can’t cut it as a litigator or smart enough to be an accident lawyer. Making few bucks as a per-hour hack is also not what they intended so they move to where the money is. OTC and helping the diluted schemes thrive.

So when you look for a ticker do not look at the trading tier NASDAQ or GRAYS. Do not look at the share price or what people say. You look up the company and see if they are real or an intent just information website with no operations.

You don’t look at the profits or EPS, that is what happens down the road. But you have to get in some time and early so you get in before all the compliance happens.

Low float, no debt, (Means debt diluting is IMPOSSIBLE)

No ticker changes (not a previous pumped ticker they reversed from)

No FINRA or SEC enforcement issues.

No debt and Profits no matter how small. $1 profits and a low share float is better then $10,000,000 in debt with a diluted float. Some say that is incorrect yet they keep losing on the big debt dilutes stocks.

They have to see they keep losing or just in denial. OTC current, even NASDAQ and also with Audits, Intent hot news, Penny Stock Exempt on a company that has no proven operations (Not just a PO BOX) no sales and is in debt up to their eyeballs and is too good to be true, Is a SUCKERS play.

Do not listen to anyone who hides behind a screen name, they are not your friend. They say what NOT TO BUY and there are reasons for that as well. No one bashes a bad stock!

Bashers only bash good stocks to keep the price down to accumulate or prevent a rinse in price to maybe expose fraud or expose short positions. You only see pumpers pumping a bad stock because they want to sell shares fast knowing the price will drop.

Bashers of a low priced stock know they can be affected by a rise in share price. If a stock is down the plan is to keep is down to not expose fraud. Bashing a stock is one thing but making others believe its bad when it’s actually a great company have other motives and investors need to look at data for themselves.

If someone wants to bash bad stocks all day and night for decades, that can’t be a real job or can it.

I never told you what to buy or pump some scheme. I don’t do that. I’m just posting how this all works. GNGR is a low float, no debt, profitable and great performing company with sales globally and they are expanding.

All proven and true, even without an audit. :)

$GNGR

Thank you -same to you and yours.

So you know you're buying junk. Good luck to you, and especially your family.

I have played the OTC for many years and while I have been naive at times I have done very well fortunately. Not only that but my P/L based on the amount invested happens to be excellent.

Yes I take the occasion hickey, in the scheme of things, its okay.

I appreciate your input.

If you bought this stock, you're certainly naïve. Never buy or hold a stock that isn't audited and audited by a respected CPA. By the way, I'm a retired lawyer and my son is a CPA for a major firm. I've been investing exclusively in rock-solid exchange-listed blue chips for decades and have done very nicely.

Skim thru all the old posts here and see how well GNGR sticks to its word, which is almost never from my long experience on this board. Naturally I never own rubbish like GNGR.

MallenNV,

THANK YOU VERY MUCH

What you wrote makes perfect sense and I greatly appreciate it.

I still have a few questions if you are willing to entertain them.

Has does the CEO of the company not know about the added share clause -dilution features?

Although this is the OTC and although 99.999% of the time the law and the rules of not apply to OTC tickers, isn't their supposed to be a filling for something like this?

In NNMX case, they are a SEC filer and fully audited. Perhaps I am still just too naive. I understand it. I really do. Still it is really hard to believe the rules and laws don't apply. Wouldn't be the first time LOL.

AGAIN, THANK YOU VERY MUCH FOR YOUR HELP!!!!!!!

Splinter; (You) Could you please read the following and explain how this person would buy 59,640 shares at a price of $1.17 when they could buy shares in the open market at .15, .17 and then .95 although I am sure there are shares for sale in between. They mention that he has bought shares like this in the past. Plus I don't see a filing for it.

Doesn't make sense - and since it doesn't make sense, something is missing.

In most cases the sale is an option or warrant to buy shares at that price so retail investors (The target of the pump) is made to believe that if someone is going to pay $1.17 you should buy some now for less so then when they rise to $1.17 you can sell.

Also do not look at the share count, look at the dollar amount. 59,640 shares at $1.17 is $69,000 but the small print says the investment of $69,000 has to be maintained by the bid price per share and at any time the price drops below $1.17 they are to receive more shares to match the $69,000 investment even before they pay the $69,000 on the option.

Since they all know (Sometimes the CEO is clueless) that the shares will drop in price on debt dilution or with a brokers help (And that ticker you are referring to has billions of shares and they are in debt $12,000,000) so that’s a good debt dilution indicator.

If the CEO is not in on it, the option holders agreement with the added shares clause will allow the schemer to tell brokers to kill the price to $.001 even temporarily. Once they do that, the option holder legally is now owed $69,000 worth of $.001 shares not at $.1.17 so instead of 59,000 shares for $69,000, they are now owed 69,000,000 shares. Soon after the shares will rise back up to $.01 maybe little more or less they dump them for $690,000 (netting $600,000).

Note: Data people look at when investing is if others or insiders are paying more as speculation that the confidence in insides shows it’s a good risk when it it’s not.

What I have seen first hand is that the CEO is often not aware of the small print that mentions the toxic issue. I have seen investors have options or warrants for $1.00 per share when the open market shares are $.20 or less. The fact they did not buy the open market shares is because they would have to pay money for them when a warrant or option cost them nothing until exercised.

I recall a term called submarine a stock. It’s when you are a CEO and agree to sell the 59,000 shares for $69,000 not knowing about the added shares if the price falls. The schemers will know the CEO owns 100,000,000 shares (51%) for example. They schemers work with brokers to drop the price to $.0001 and the investors use that fact they now are owed legally 690,000,000 shares, they file to vote out the CEO, take over the company and since the $69,000 is owed to the company and they take over its still their money and the CEO is out.

Once that is done the legit company is quickly merged into a new ticker and pump and dump. That is if the company they submarine was not a scam to begin with. If the company is a debt-selling scheme and you see large inside buyers at higher prices you can bet they did not pay that and likely never going to.

Although some could be higher price preferred stock but often its just smoke and mirrors to set up a debt dilution plan that looks legit before the fall.

The fact they claim to have paid $1.17 when they could have paid $.08 on the open market has no down price protection (added shares as the price falls) If they paid $.08 and the price falls, they lose. If they are owed shares at any price with more shares owed if the price falls, they are 100% protected and just keep getting more shares as they drop in price.

It’s really to get suckers to think things are happening or to scam a CEO out of control of the company by getting more shares as the price falls so they can change it to a debt dilution scheme.

Look at it this way, 99.999% of what people read or are told, is FALSE or LIES disguised as valid under the disclaimers. And 99.999% of the time the law and rules do not apply to OTC tickers. With all this allowed is why so many tickers come and go each year, tickers vanishing and new ones emerging and no one is making money on them buying hoping they go higher.

Sad and true. I met a 401K manager who had 250 people in his fund. He told them he was going to invest $1,000 of their money into a new stock. He told them he would watch it carefully and if he sees it head south he will get out fast. He told them that the $1,000 could turn onto $20,000 so they all agreed also knowing he would not let them risk the entire $1,000.

What he did was he bought $1,000 worth of a pump a dump scheme stock. He took $1000 from 250 accounts ($250,000) he emailed all the investors the buy order so each of the 250 investors though they each owned the shares. He then waited for the stock to drop in price (As most OTC tickers do) and he knew the schemer and the plan to kill the share price.

He then sold the shares for $800 and let everyone know that the stock dropped to almost $0 but he got them out losing only 20% not the entire $1,000. He took $250,000 spent only $1,000 then sold it back for $800 so he made $200 from 250 people. He put $50,000 in his pocket in just a few days and when everyone was told they got back $800 no one knew what he did except looking out for his managed fund investors interests.

No one was able to expose the scam because they did not know they were all scammed as a group. Even if two investors from the group met each other they would each confirm they each got back $800 not realizing the scam.

All scams even illegal go undetected simply because there are too many. And also when a scam is closed down even though it took place, there is no one to see it or question it. It's as if it did not exist.

It was a while ago when I spoke to him but can’t remember what he actually made but it was quite a bit.

Unfortunately a lot of what you wrote about is absolutely true.

Most shareholders lose everything, some who know how to play these make a little, and the scammers make millions if not billions overall.

Very sad.

Excellent points.

Hopefully what you write about GNGR will come true!!!!!

Dear Lord what a joke

It looks like one of the pictures is a basement bedroom.

People will actually buy that ring.

And the follow up->

Besao (from another board) also to note; when you see this kind of data (below) on a new pump launch, most think this is a good thing.

They see that stock options are being sold or issued for $.20 per share to give the appearance that major investors are jumping in at $.20 showing that stock option investors believe it will rise much higher, and notice it says to CONSULTANTS!

(The "Company") announces the grant of incentive stock options to acquire a total of 4,800,000 common shares of the Company at an exercise price of $0.20 per share, with such options to have vesting terms over a period of three years. The options expire three years from the date to grant. These options were granted to directors, officers and consultants of the Company.

Here is what happens (but rarely) in the small print that investors never get to see. 4,800,000 shares at $.20 come to; $960,000 you think the company will be receiving correct?

WRONG!

What happens soon will be those getting the options will soon convert them to debt shares. But 4,800,000 are not a lot of shares on a pump and dump. What the small print says is; if at any time the shares fall below $.20 the company has to make up the shortfall with more shares. This is an indicator of an impending drop in price. The option holders know paying $.20 ($960,000) will be tossing money into the garbage so they get the options and fool other investors into thinking lots of cash is headed to the company. Why even post the options in the first place?

What happens is the option holders will help kill the share price as these schemes always end up on a downward spiral. The option holders owe the company $960,000 for 4,800,000 shares. But not so fast! What happens is they only pay the $960,000 over time in tranches. and over time the stock keeps falling, this means that as the shares drop in price, the option holders get more shares for their $960,000.

The CEO does not get the $960,000 nor does the company. Debt is paid and they payments got right back to the debt the option holders own so they get back the debt money paid. The CEO will get some salary or bonus but its usually a small fraction of the capital made on the debt tranches and as the share price drops so too does the CEO's percentage of funds.

If the price falls to $.01, $960,000 divided by $.01 comes to 96,000,000 shares (not 4,800,000) when it falls to $.001 they get 960,000,000 shares. You will never see an options holder pay the agreed $.20 because the options holders are in on the debt dilution. Also the options are can be used as collateral. That means an options or warrant holder can work with a broker (Remember the broker is in on it) to sell not 4,800,000 shares at $.20 but 48,000,000 at $.20 or even 100,000,000 at $.20 with the brokers knowing full well debt shares will soon follow.

48,000,000 x $.20 on the initial low float set up comes to $9,600,000 (NICE!) and a short squeeze is all but eliminated because the debt shares are a sure thing. And the oversold is only exposed when the company increases the authorized and adds them to the debt diluted float after they dump the oversold shorts for the higher amount.

ALSO TO NOTE

There are two ways these options work. One is because the CEO is not involved in the pump and dump and the options holders sneak in the wording for toxic funding to debt dilute with out the CEO’s approval, knowledge or understanding.

The other is because the CEO is in on the scheme knowing full well the options will never be acted on and is just to fool investors. The willing CEO will allow the debt to happen and issue shares on the debt conversion while the unknowing CEO is forced into legally issuing toxic shares on a death spiral.

One factor to prove the CEO is in on it; is the company structure. You can bet a Uranium or Lithium or gold mine in Greenland is not the dream of an innovator legit businessman who wants it to see his vision come to fruition meaning the CEO is in on the scheme. And even with $960,000 on hand, you need 10’s million$ in equipment and also be approved to even mine in protected land. Not to mention years and millions in surveying the land by professionals then the health hazard compliance and processing of dangerous uranium or lithium and even gold requires toxic chemicals.

I said it many times; selling shares has more value then finding gold in them their hills. And selling shares takes one person and no costs or compliance. It can be done from the deck of their yacht or their $250,000 Mercedes at a red light. Why spend millions to find gold that may not exist and even if you find the gold, the shares are STILL worth more then the gold.

That is why the scheme has to be exciting not boring like Amazon books back when the stock was $2.00 per share. That is also why bigger investors made billions off Amazon stocks while the retailers were to busy buying into gold mine, marijuana schemes and losing their money. Books boring, Gold exciting!

In some cases the options are to show investors others are getting in at $.20 so it seems like a good risk. And in most cases the options are never acted on so the money never gets invested and the option shares never issued. Same with letters of “intent”. That means it’s not a fact or even will happen and on that note some tickers will say they got a $10,000,000 order and the 3rd party will issue them a check that bounces but the ticker never tells investors the order was cancelled. Instant revenue of $10,000,000 to post as news just for the fact they deposited a bad check. A $10,000,000 purchase order is real but so is the order being cancelled. All legal.

SO

Stock options at a high price? (Are likely not going to be exercised)

Letter of intent? (Means it’s just intent and likely never going to happen)

Sales of $10,000,000? (Just a scheme associate writing a bad check)

Always a hot topic and exciting like gold and diamonds. (That are never mined)

The proof is the scheme will post no revenue and add debt to the financials. With all those intent, checks, options you think they would have at least $100 in the bank but the data usually shows ($xxxx) and in CASE some do not know, ( ) means negative.

AGAIN ALSO TO NOTE

When you see a share price rise UP even after you short them you see the trade data is for not many shares, 1000, 1500 even as low as 100. Even if it is not a pump and dump those low trades are not really impacting liquidity or even value to investors. Just because the shares rise 200% on 100 shares being traded does not mean all shares are worth 200% more, so again its false data. The low volume means they scheme will soon make the liquidity explode just not at $.20 more like $.001, $.0001 and even $.000001.

Since shorts can stay open for decades it become a waiting game for the inevitable.

Some replies to questions->

If the same block of 10,000 shares gets sold ten times over how is there not a failure to deliver on 9 of the 10 sales?

Fail to deliver does not mean they never will be. It just means they will be eventually. Shorting these pump and dumps and the data they provide to me (publicly) is 100% proof they wont be around longer then the open short position. GUARANTEED! And even if they do remain trading longer, based on the data they provide the share will always end up in trip zeros or even less.

How is a short position registered as a long position?

There is what is called a mandatory reporting threshold. If you remain under that threshold the short position never shows up. Since a short can remain open for years or even decades and you short the stock under the reporting threshold they can be seen as long positions.

How is the $2.50 rule being circumvented as it seems to be in actual practice for you? I have IBKR and they have margin requirements for shorting penny stocks that match the $2.50 rule precisely.

It depends on the stock, the broker and who is just more willing to participate. If the store says bananas are $2.50 a bunch and the guy in the back shipping area says HAY PSSSST check it out you want the same bunch for $.10 cents? You say OK and no one knows about it.

Remember BROKERS are all in one it so when they let you short for cheap they know they will never be getting the stock back or have to call it back because they know you will just buy back diluted debt shares cheaper and never have to buy shares back from the float.

It’s FREE money for brokers and market makers and that is why they have associates short the stocks. They know they will never be called back or have to be returned to the lender. Any money they take to let you short the stocks $2.50 or even $.02 its free money they get to keep by continuing to lend what does not exist that soon will exist by the dilution.

You are confusing a legit short with a pump and dump short. A legit short, the shares have to be returned from open market inventory eventually. A pump and dump short you just buy back the diluted debt shares for less than 10% of the posted bid price.

Have you yourself ever experienced a short squeeze on a penny stock?

Pump and dumps don’t short squeeze because that would mean there are not enough shares to cover when the price rises. FACT! Pump and dumps make money only selling shares thus preventing any short squeeze because their are always unlimited shares available to buy from debt holders cheap to protect against any short squeeze.

If SGMD only kept the 200,000,000 float back in 2019 and sold them all for $.18 they took in $36,000,000. Once done and with no operations or revenue, they would have no choice but to close up. Why close the ticker when they can just over sell another 300,000,000 and make another $54,000,000 and protect the associates brokers, market makers, pumpers with debt shares soon to follow? Brokers would never have over sold unless they know for a fact the dilution is going to happen.

And also keep in mind those who set up the pump and dump do it over and over and if they let the brokers over sell and not cover the shorts with diluted debt shares, the brokers would never help those who create these schemes. Brokers make BILLIONS and so to the schemes so why mess with that.

So you can see why a pump and dump will never become a short squeeze. Or just maybe!

One company is being set up for this. The brokers and market makers that bet heavily on dilution and debt based on the trust they had for the ones setting up the pump, did not realizing the company was not part of the scheme but were told they company was.

This was done so the crooked attorney could dump 400,000,000 more shares at $.10 knowing full well there would not be any debt diluted shares to make up the shortfall leaving the brokers to be caught in a short squeeze. The company was not part of the scheme and kept the true DTC registered float at around 100,000,000 shares while over 800,000,000 traded hands with 400,000,000 over sold when some who attempted to attack the ticker failed to create the debt dilution shares and never told the brokers.

This caused a large over sold with a very low float. That is the storm of a short squeeze headed down the pipe. The shares now are $.002 means 100,000,000 shares will cost us $200,000 to accumulate the entire float. If we acquire all the float shares cheap and request the certificate from the broker (Minus 1,000 shares), once that certificate is issued, they are taken out of the lending pool, this would expose the massive naked shorts still open (maybe 400,000,000).

Think about this; You own 100,000 shares in your TD account and you now see the float is only 1,000 shares, you and 1000’s of others see the same, HOW can you own 100,000 if the float is only 1,000? Now 1000 investors call the SEC to complain and the brokers panic.

WHY WOULD A BROKER PANIC?

First of all there are NO diluted debt shares to buy cheap to cover the over sold and second, with only a float of 1,000 shares, what if the company issues a $10 CASH dividend?

The company only would have to pay out $10,000 to the TRUE float of only 1,000 shares and any over sold (your 100,000) that same $10 dividend would have to be paid to you by your broker and to those 1000’s of investors who own combined maybe 400,000,000 shares still open.

ANOTHER PROBLEM FOR BROKERS

They can’t just close the short by buying up diluted shares because there are NONE to buy, they MUST buy back all the 400,000,000 oversold. If the company issues a $10 cash dividend on a stock that you paid $.002 for (100,000 shares) and you paid $200, the brokers (not the company) owe you $1,000,000 and they LEGALLY HAVE TO PAY, just like they paid out $12,000,000,000 ($12 billion in one month for the GameStop squeeze).

IT GETS EVEN WORSE FOR BROKERS

If the cash dividend is $10 costing the company only $10,000, Millions of investors would rush to buy up the 1,000 float driving the price to as much as $1,000 per share. If brokers have to buy back the 400,000,000 under SEC LAW, to buy back the float at $1,000 per share x 400,000,000, the brokers would have to pay out $400 billion and anyone who paid $.002 would likely be BEGGED by the brokers to sell them for $100 per share just to reduce the huge short losses.

Even if you sold your 100,000 you paid $200 for at $100 per share you make a nice COOL $10,000,000! Now since we will own the float of about 100,000,000 shares paying only $200,000 at even $100 per share on a forced squeeze we would net $10.8 billion! Even the worst case, the company does not do a cash dividend and there are only 1,000 in the float. The SEC would force the brokers to close the open shorts and since they can only buy back and not resell what does not exist, they would cause a run on the stock as many won’t sell.

Even if they are forced to buy back the shorts and drive the price up to $1, we will still make $108,000,000 not to shabby I might add.

Heck even if they are forced to buy back what they sold them for $.10 we still net $10,800,000.

These are not assumptions like pump and dump stocks. These figures are real, valid and FACT period. No intent or ifs or could. When we buy the rest of the float we will make an offer to buy the 1,000 shares for $10 per share causing the bid to rise to $9.50 and the SEC forcing brokers to buy back the 400,000,000 for $9.50 per share.

The brokers will likely call the company to see if they will sell the public entity so the brokers can close the ticker and cancel the short squeeze and have all shares cancelled but so far the company CEO said NO SALE even to a 7 figure offer. That is the CEO you want running the company you invested in.

That is why we worked with him and his company because all the data points so far from being a pump and dump set up and the fact the (arrested) attorney lying to the brokers was the perfect set up for short squeeze not a diluted debt dump.

So there is your short squeeze answer.

It seems to me that once a penny stock company resorts to toxic convertible debt financing there is very little chance that the company could ever succeed. Company officers do get money for salary and bonuses, but the shareholders are wiped out. The toxic debt people and the penny stock company officers seem to be colluding to screw over the shareholders along with all the shorts.

CORRECT!

A ticker I’m shorting now has a women listed as CEO, CFO, secretary making $57,000, however in the filings, 10 others behind the scenes are making between $1,500,000 and $78,000 on a company that has no revenue. And it seems they bought the company that writes the PR’s, which is a serious conflict of interest. BUT no one cares. No one Look’s at data so it’s just the norms here on the sub penny markets.

They drive the price up by 30% by buying only 100 shares and people see that as a way to make money, if you did buy 100 shares you won’t be able to sell them and be profitable. As I said they do this to make people think it’s a good investment when its just being set up for debt dilution. A $100 stock buy can make the company market cap rise by $10,000,000 while at the same time one sell order can kill the share price. Smoke and mirrors.

For you a stock screen to search for prospective shorts might be to look for obvious scam companies with known corrupt officers, high amounts of convertible debt and no revenues. You would short them probably after a massive reverse split optimally or perhaps after a pumped run up in price.

YES, but those running the scheme are never on the filings or even the board of directors. They find a patsy CEO to run the scheme for not much money. Usually a CEO from a failed ticker with no products or revenue so those CEO’s have to end up a pump just to make some exit strategy money knowing that was not their initial plan, they just had a failed ticker and they needed some money to survive.

Once in a great while there might be a real company with honest officers that has a revolutionary product that has explosive growth potential. Have you ever witnessed such a success story? Was Microsoft or Apple once a penny stock on the OTC way back when they were starting out?

FACEBOOK was a gray market company and look what they did. The company we are targeting for the squeeze would like to move from Grays to NYSE and the hell with the OTC, however a simple fee to the OTC and they could up list right back to OTC Current. But the OTC is not an exchange or regulatory agency. They are a publicly traded ad platform.

Remember, Apple, Microsoft, Google and many fortune 500 Companies started in a garage or basement. NIKE CEO sold shoes out of his car trunk before his company took off. Amazon only sold books initially.

Wrigley’s gum started off as a laundry soap product that no one liked so they created GUM and said FREE CANDY in every box of detergent. People liked the gum so much they wanted the gum not the soap and the company emerged what is now a billion dollar corporation all from switching from horrible soap to chewing gum.

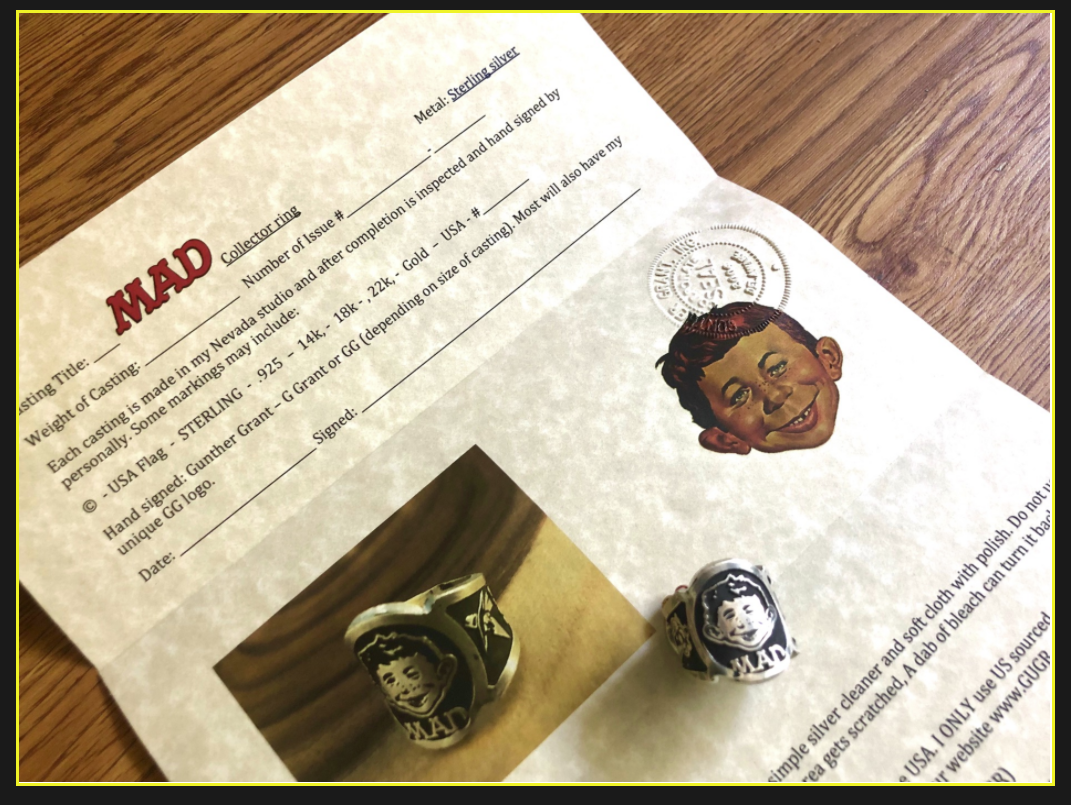

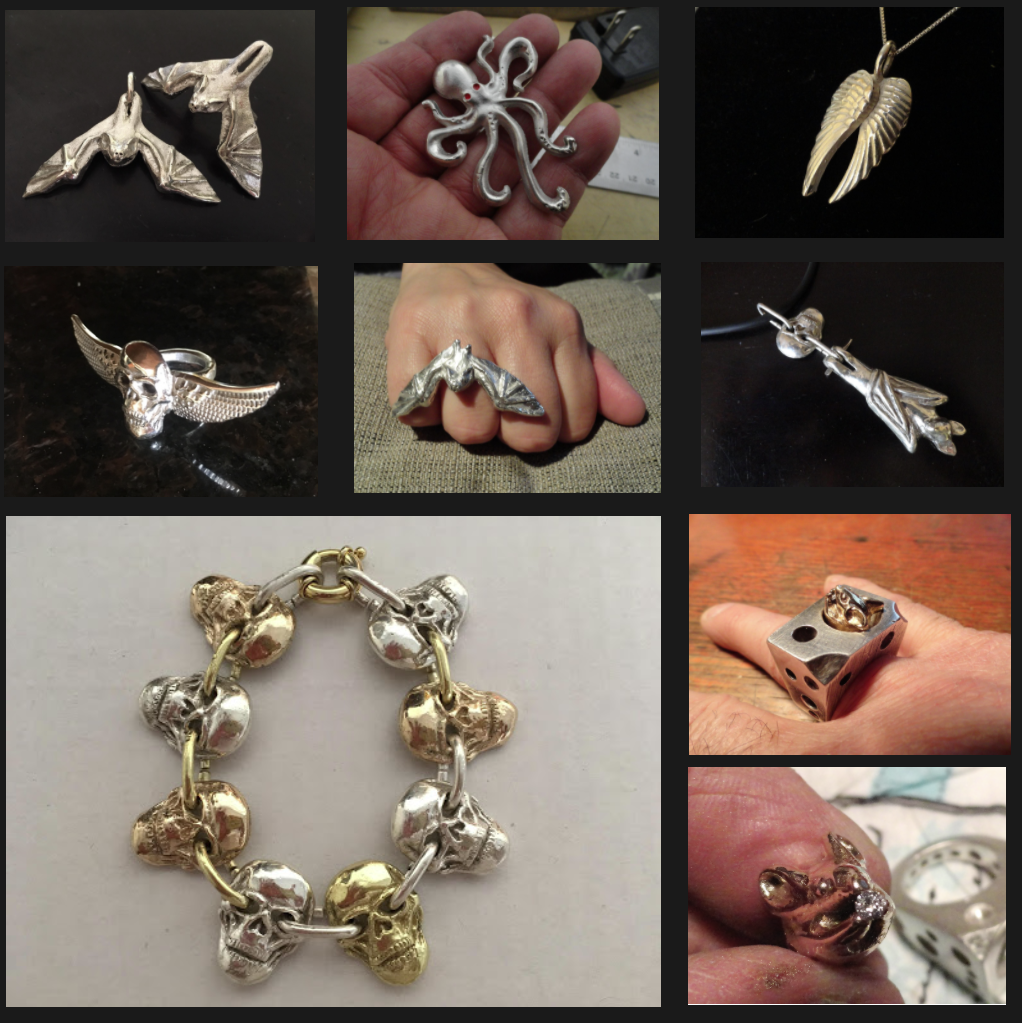

The company we see the impeding short squeeze coming has a similar story. They own a mold technology no one else has and used that in the confection industry. Then to increase sales, they offered a free custom 1/10-ounce silver ingot with every $15.00 purchase and more people wanted the custom silver ingots causing the change from confections to what is now a global silver and gold casting operation.

Change in a good proven company can be a great thing.

The most you see change in a pump and dump scheme is the diluted shares and eventually the ticker.

It's going to be a lean retirement without social Security or a pension. Pumping the stock may help... but not THIS stock.

You are awesome MallenNV

GNGR has done everything right. But they are on the expert market. In with the swill at .0001. So some not all investors made some good money on the scams if the got in and out. With GNGR everyone lost.

DID YOU KNOW!

GNGR went public in 2008 and the ticker is still active and trading publicly. And they are still a fully operating company with global sales and expanding. A Google search and proven sales is publicly available for all to review.

Garage, Cellar or Rented location? Anything is better then most OTC's that operate out of a $20 a month UPS store PO box. I always wondered? HOW can they fit all that gold mine or Marijuana equipment in that tiny little box?

Also as per FINRA data, since GNGR going public in 2008, “25,170” OTC listed companies changed their tickers. That’s almost twice the listed tickers today on the OTC (12,622).

That means most folded or changed from the normal pump and dump debt diluted mess into a new scheme to continue to dilute and move to a new ticker and that trend continues today. Like Locusts, they come eat and leave and move to the next crop of food, (For those who still don’t get it, FOOD is in reference to investors)

That may explain why no one can answer our question posted many times to name one OTC ticker investors have in their account that is still active and in operations since 2008. The answer is ZERO and I don’t mean that as a ticker symbol.

GNGR made a significant change for the better and is now a global operation with proven sales and they are expanding.

They may need a bigger cellar.

The only change for most other tickers is what looks to be a change to their float increase to diluted debt shares and change their tickers. (Not for the better for those who still have no clue how this works). The fact is that investors will never stop feeding the locusts. This is why only a few hundred of the 12,622 listed OTC tickers sell over $300,000,000 per day in cheap debt diluted shares, EACH DAY!

That comes to about $1.2 billion per week or more from tickers that are under $.001. $60 billion annually invested in under $.001 tickers with diluted debt shares. That is why OTC investors need to reset their thinking and it is why GNGR will likely never get ahead because they are of no interest to those investors who would rather invest in a lotto hot topic debt diluted scheme dream that is run out of a PO BOX then a successfully global company that may be in a cellar.

At least there is more headroom :)

GNGR’s securities and company structure is also why GNGR together with our group will do what needs to be done for the benefit of the company, our position and anyone else who is still in this ticker. I am sure that many may only have GNGR left in their accounts after all the cancelled tickers they invested in over the years that do not exist any more. I am 100% sure of it.

Better to have then have not.

$GNGR

So a valid company would have solid logic and facts to back it up. GNGR has had no factual information for over 5 years. It sits at the bottom of the OTC market because they have not shared any facts.

They have complained how they stock is naked shorted by the market makers. But you are telling a story of buying all the float and we will all see something we have never seen before

But if the CEO is right naked shorting will stop any movement.

So who is the crook you or the CEO?

In the music industry there is.

Blues, Jazz, Rock, Country, Soul, dance, Hip Hop, Rap, Pop, Folk, Classical, Heavy Metal, Punk Rock, dance, Disco, New wave, Electronic, Reggae, Funk, Techno, Grunge Rock, Swing, Gospel, Instrumental, Orchestra, Psychedelic, Baroque, Bossa Nova, Bluegrass, Holiday, Latin, New Age, Opera, Contemporary and many many more.

Which one do you listen to?

In the OTC industry there is

12,622 tickers with only one choice, an honest CEO, or a crooked CEO.

Which one do you listen to?

Since music is around forever one has to ask them selves how many tickers have vanished over all these years? And which tickers are still active and functioning as a valid company since they entered the marketplace?

Then you will have your answer, which CEO is the crook, or not.

$GNGR

Maybe we can get current before we start to pump the low float. You own 20 million plus and mallnv has at least 39 million for years and no short squeeze yet. I have a feeling the market makers are. It very nervous. Most companies in a basement make them nervous

GNGR is a different play now. A short squeeze play and who ever owns shares when the pressure is on will do very well. That is why when we control the float (coming soon) and we force the brokers to close out the open naked with no shares to buy back YIKES!

From your lips to God’s ears! Lol. Looking forward to see what happens…

Splinter, YES that last private email is 100% correct.

Splinter, I do not have access to private messages. If you email the company they will forward it to my Summerlin office. I am helping GNGR but not officially. We cannot buy the float as associates on paper.

;)

Since GNGR is not a confection company any more you have to compare apples to apples like GNGR with BRGO (jewelry) of even signet that is down from -50% from $140, while BRGO went from $2.00 down to $.000001.

GNGR is a different play now. A short squeeze play and who ever owns shares when the pressure is on will do very well. That is why when we control the float (coming soon) and we force the brokers to close out the open naked with no shares to buy back YIKES!

Gonna be something no OTC or Gray has ever done. Low float, no debt no dilution. Blue chips wont be able to even compete with the % gains on a short squeeze. Besides many blue chips are falling like a ROCK!

you should use some of your big bucks to clean the mold off your office window and fix your window shades.

I've been "having fun" with blue chips and index fund for decades. BTW, I see Hershey shares are at $256, an all time high, plus a nice dividend which GNGR apparently will never pay.

Plenty of fun there and right now. .

Good luck to anyone still holding GNGR

That seems a fair statement on most if not all OTC pump and dumps schemes. Since the CEO of most pumped tickers had to change to a pump in order to have an exit strategy for one of two reasons.

1) The CEO was part of the scheme before the debt dilution pump and dump and also walked away with a few million as the debt diluters made much more leaving the retailers with losses.

2) The CEO took their company public that did not achieve their goal or was able to get the plan in place that was the reason for going public in the first place.

Those CEOs who found going public were unable to get additional funding (No one funds OTC tickers), they are the ones that ended up with not much money and ended up working for minimum wage.

GNGR is one of those companies that did not go public to set up a scheme with others, If they had their would not be a company that was in production before going public and they would have had billions of shares added to the float on a pump and dump.

Some say GNGR was a pumped company but that is not so for the fact you can’t pump and dump a stock with out a large float or debt that allows a pump and dump to work.

GNGR has no debt and a very low float = Impossible to be a pump and dump.The falling share price is due to a low non liquid float and in a company that seems not exciting compared to a Lithium or gold mine and now many uranium mines are now entering the pumped market.

We want the shares cheap and with such a little float it will cost very little to acquire the entire float. Once obtained, the fun begins.

I wonder how the people behind penny stocks survive thru old age. Was GNGR paying into Social Security? At least Nevada casinos offer plenty of menial jobs. I guess one can wipe tables and empty ash trays deep into "the golden years."

So you are not part of the company

But you posted the following

Just be patient, Boarding the jet now to CA. To meet and make deals that will not flood the float or create debt financing

So you a marketing guy was doing a deal for the company. So strange. But started the pump.

rmc, I wont say it again. Your comments are not reaching the intended target (The Company). If you have any questions you need to email them. I am no longer working with GNGR and I don't even know what it is you are rambling about. No need to explain a 3rd time I put you on the blocked list. And I have other things to do than read the same posts like a broken record that are also 100% incorrect.

If the CEO is a crook and the company is a scam, SUE THEM! If you have any questions or concerns, email the company. Simple and easy! IHUB is not a place for solid valid information or answers and even when someone posts they are the CEO it’s probably not even them. I don’t know any CEO that even reads these public message boards. I just pop in sometimes and see what is a cookin.

Now I’m outta here. Taking the kids to get pizza.

Awesome thanks for the heads up. We are going to do the Overstock.com pump. GNGR will do a price release that they own all the shares. Then play up how they will go up when you uplist. Then. 4 months later you post you could no do anything because the big bad OTC said no!!!! Come up with something different. Do a press release that you are now an authorized merchant for F1. Or did you just use the logo with no approval.

I think a while ago the company posted that data on the website. Back when the news was posted, the dividend, which was (If I recall $20,000), divided into the issued shares came to about $.00001 per share, something like that.

I screen captured the post but it has been awhile and likely deleted it. We are not in this for the share price or dividends; we are accumulating the entire float for other reasons.

So FINRA cancelled the dividend? That's amusing. And the poor investors are just learning of that, long after the fact?

"Any cash dividend would have meant that over 90% of those funds would be directed back to the CEO and the associates. FINRA cancelled the approval for the dividend based on that fact it would not help anyone other then the CEO."

Ya it is all a joke when you have no response. Go back to the basement and run your international business with a stock price of .0001. Very successful.

You forgot to say April Fools!

So GNGR has hired you as a marketing firm?

I am still confused. Your current price on the public OTC shows .0001 they is public information. But I am to believe it is higher in a non public market where all the real big investors are loading up on GNGR. Sounds incredible So these large investors are putting money into a company out of a 500 square foot basement.

Sounds like GNGR is heading for another pump. Can not use the dividend. That’s has been done. Can not use you are selling that has been done.

I know you found a cure for cancer and are starting trials next month. Hope you have continued success marketing a fraud company with a criminal CEO

|

Followers

|

107

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

14462

|

|

Created

|

09/16/12

|

Type

|

Free

|

| Moderators | |||

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |