News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

This is not even close to over. Its clear from the article below, the Trump admin is keeping its position a secret. Wonder why.... ·

https://www.nationalmortgagenews.com/news/fannie-and-freddie-should-they-stay-or-should-they-go

Us as shareholders have been here dealing with this for so long and led on. I truly believe we should have had some sort of notification not publicly made as to the direction of this and these entities. It is another taking and they have allowed us to invest and trade in it when this should not be allowed. It is rape!

HOWARD ON MORTGAGE FINANCE - The Path Forward

JUNE 6, 2017 ~ JTIMOTHYHOWARD

At the beginning of this year, in a post titled “Economics Trumping Politics,” I wrote: “For the past eight years, what I refer to as the Financial Establishment—large banks and Wall Street firms, and their advocates and alumni at Treasury and elsewhere—has been engaged in a well designed, carefully scripted and highly orchestrated political campaign to convince Congress to replace Fannie Mae and Freddie Mac with a mechanism more financially beneficial to themselves. Then, seemingly out of nowhere, five weeks ago Treasury Secretary-designate Steven Mnuchin announced his intention to “get [Fannie and Freddie] out of government control…reasonably fast.” With this statement, the odds immediately flipped to favor the prospect that the fates of Fannie and Freddie will be determined not by a misinformation-based political process likely to benefit banks, but by a fact-based economic process likely to benefit borrowers.”

Based on the Mnuchin comments, my expectation had been for a relatively quick settlement of the lawsuits against the government for its handling of Fannie and Freddie in conservatorship, followed by a reform and recapitalization plan for the companies that would have provided them with regulatory and capitalization schemes designed to maximize their effectiveness as mortgage guarantors. Such a result would have been driven both by the interests of shareholders behind the lawsuits and the interests of Treasury, which holds warrants for 79.9 percent of the companies’ common shares, and would have been in the best interest of mortgage borrowers. While the large banks and the political opponents of Fannie and Freddie would have objected to keeping the companies alive, without a workable legislative alternative they would not have been able to prevent it.

On February 21, however, the U.S. Court of Appeals for the D.C. Circuit in the Perry Capital case unexpectedly (and inexplicably) held that plaintiffs’ statutory claims against the net worth sweep were barred by the anti-injunction provision of the Housing and Economic Recovery Act. Shortly afterwards two suits challenging the sweep in lower courts—Roberts in Illinois on March 20 and Saxton in Northern Iowa on March 27—were dismissed in opinions citing the Perry Capital decision. Still another lower court case, Collins in Texas, challenging not only the net worth sweep but also the constitutionality of the Federal Housing Finance Agency (FHFA) as a federal agency headed by a single director removable by the president only for cause, was dismissed on May 22.

The Perry Capital ruling and the subsequent dismissals of other net worth sweep cases in lower courts halted whatever near-term momentum administrative mortgage reform might have had. Treasury had no justification for initiating settlement of a case it so evidently was winning—and that was bringing over $15 billion per year into its coffers—and without resolution of the sweep Fannie and Freddie cannot be removed from conservatorship.

With administrative reform efforts stalled, the spotlight returned to the legislative side. On April 20 the Mortgage Bankers Association put out a white paper arguing (incorrectly, in my view) that legislation was essential to achieve the consensus objectives of “protecting taxpayers, attracting capital to Guarantors, and ensuring consumers and borrowers have access to affordable housing.” Then, on May 23, the American Bankers Association sent Secretary Mnuchin a paper (“Reforming the Housing Enterprises—Sustaining Homeownership and Protecting Taxpayers”) taking virtually the same position, while also advocating additional restrictions on credit guarantors and more benefits or flexibilities for primary market originators.

Yet while the focus of mortgage reform may have changed, what hasn’t changed are the relative degrees of difficulty of legislating something new and untested versus administratively fixing something that already exists and has been proven to work.

Legislative reform efforts never have been about devising a secondary market system that produces the lowest cost and most available mortgage financing for homebuyers; their core objective instead has been to remove or restrict two companies—Fannie and Freddie—whose operations have made it more difficult for large commercial and investment banks to exercise the control over and make the amount of money they wish to from the $10 trillion single-family residential mortgage market. For that reason proponents of legislative reform have as an unconditional requirement that Fannie and Freddie either be eliminated or altered to a degree that they no longer can operate as effectively and efficiently as they once did. Advocates for these changes may say publicly that they are remedies for a “failed business model,” but the reality is that they end up having to propose secondary market credit guaranty mechanisms that work less well than Fannie and Freddie now do, or have a risk of not working at all.

Legislating the replacement of the known and proven with the unknown and uncertain always is difficult, and there are four factors that make it even more so in the current environment. The first is the extreme partisanship and divisiveness in both houses of Congress today. Second, setbacks to attempts by the Trump administration to replace the Affordable Care Act and achieve consensus on an approach to tax reform further complicate the task of knitting together a coalition capable of agreeing on and passing reform legislation. Third, there are fundamental, and seemingly irreconcilable, philosophical differences between the Senate and the House on whether there should be an explicit government guaranty on securities issued by the envisioned successors to Fannie and Freddie: the Senate supports one, whereas a significant number of members in the House insist that the future secondary market be “fully private,” with no government support at all.

Finally, to put and keep the companies in conservatorship Treasury has had to single out their shareholders for unprecedentedly punitive treatment—forcing the companies into conservatorship, having FHFA add massive temporary or artificial accounting expenses to make them take unneeded and non-repayable senior preferred stock, and then, when the effects of the accounting expenses reversed, taking all of their net income in perpetuity. Advocates of “winding down and replacing” Fannie and Freddie through legislation seem to be wishing away the challenge of convincing investors to put up $150-$200 billion in capital for new and untested credit guarantors at the same time as the government is expropriating the capital previously invested in the two existing secondary market entities.

For these reasons I believe it is highly unlikely that mortgage reform legislation can pass before the 2018 midterm elections (beyond which time prediction is foolhardy because of possible changes in the political landscape). It is tempting to conclude that the status quo will continue indefinitely, since it will be favored by Congress—whose leaders see it as preferable to administrative reform preserving Fannie and Freddie—and it also benefits the administration, which can keep the companies’ net income while publicly exhorting Congress to end the legislative impasse. Ultimately, though, the lawsuits make the status quo unsustainable.

A number of cases related to the net worth sweep are still pending. There is the Jacobs-Hindes case in Delaware District Court, asserting that the sweep violates Delaware and Virginia law applicable to Fannie and Freddie and thus is void and unenforceable. An appellate court decision in favor of the plaintiffs in any one of four cases—Robinson in Kentucky, or Roberts, Saxton or Collins—would conflict with the finding of the D.C. District Court Appeals in Perry and trigger “a split in the circuit,” making it likely that the Supreme Court would hear and decide the issue. And just this past Thursday (June 1), a new suit challenging the constitutionality of FHFA was filed in the District Court in Western Michigan. While the timing on the final disposition of all of these cases is uncertain, and the appellate decision in Perry has reduced the odds of the sweep eventually being overturned, as long as any suit remains outstanding the government is at risk of losing it.

Moreover, if the net worth sweep is upheld across the board the government still must contend with the breach of contract claims remanded to the Lamberth court in the Perry Capital case, as well as the regulatory takings charges in the Federal Court of Claims under Judge Sweeney. Breach of contract and takings are constitutional claims, the remedy for which is monetary damages. In the absence of legislation eliminating Fannie and Freddie they will remain at the center of the secondary market and become increasingly profitable. Were plaintiffs to prevail in one of the constitutional cases, particularly the takings case, requested damages could be staggeringly (and appropriately) large.

I believe Secretary Mnuchin sees and understands this bigger picture. Even if he hadn’t already pledged to remove Fannie and Freddie from government control, he knows he has to take the initiative on mortgage reform while he still has some control over the outcome. With his path to administrative reform blocked for the moment by the Perry Capital decision, his only practical option is to work with industry leaders, lobbyists and members of Congress on the legislative efforts they now are pursuing. In doing so, however, he should and I think will set a high bar for what he deems to be an acceptable reform package. Treasury has a 79.9 percent stake in the two companies that have the best past record of secondary market performance and the best prospects for future success, but which Congress, under the influence of the banking lobby, is intent on phasing out or re-chartering. Politically motivated reform that replaces Fannie and Freddie with a less effective alternative would eliminate Treasury’s payments from the net worth sweep (for as long as they remain legal), make its warrants for the companies’ common stock worthless, and raise the cost and reduce the availability of mortgage credit for homebuyers. Those are not outcomes Mnuchin wants.

While Congress tinkers with legislative reform, therefore, Mnuchin will continue to assess his options for administrative reform. In this regard, a plan released late last week by the investment bank Moelis & Company, which describes itself as “financial advisers to certain non-litigating preferred stockholders of Fannie Mae and Freddie Mac,” may well gain traction. The Moelis plan, titled “Blueprint for Restoring Safety and Soundness to the GSEs,” relies on Treasury and FHFA’s existing authorities to set new capital standards for Fannie and Freddie, strengthen their regulation, and prepare them for exit from conservatorship following a series of equity issuances over a four-year period. Moelis contends that its plan also would net taxpayers $75 to $100 billion from sale of Fannie and Freddie stock acquired upon exercise of Treasury’s warrants.

I will have more to say about the Moelis plan in a future post; overall I find it to be very promising, but believe its fixed, bank-like capital standard needs to be refined in order to produce the business results Moelis is projecting, and to enable Fannie and Freddie to price their guarantees in a way that offers affordable financing to a broader range of borrowers. For now, though, the important point to make about the “Blueprint” is that it puts a concrete, third-party administrative proposal into the public domain for evaluation against the multitude of competing plans for legislative reform.

A significant weakness of the many legislative reform plans that have been offered over the last few years has been a lack of operational detail on how their proposed new credit guaranty mechanisms would work, and vagueness about the transition of $5 trillion in mortgage guarantees from the books of Fannie and Freddie to the envisioned new credit guaranty mechanisms or companies. The Moelis proposal, in contrast, uses an existing and proven infrastructure, includes detailed financial projections and a timeline for achieving its capitalization objectives and, in its words, “does not require a winding down of the existing GSEs, or use of market-destabilizing legal constructs like receivership, as envisioned by the MBA” that also would “[fail] to resolve existing shareholder litigation and would likely lead to new legal claims…that increase the prospect of a court-imposed solution rather than a policy-led solution.”

The president of the Mortgage Bankers Association, David Stevens, immediately responded to the Moelis plan by saying, “This proposal is clearly self-serving and designed to confuse unsuspecting, innocent taxpayers into supporting a plan that is intended to line the pockets of hedge funds who invested in Fannie and Freddie.” Tellingly, however, Stevens offered no specific criticism of the plan. Instead, he fairly begged critics of the MBA’s plan to respond by calling it “clearly self-serving and designed to confuse unsuspecting, innocent homebuyers into supporting a plan that is intended to line the pockets of banks who want the business of Fannie and Freddie.”

To date there has very little substance in the debate about what to do with Fannie and Freddie going forward. Together with the interest and participation of the Mnuchin Treasury, the Moelis proposal should help change that, by serving as a catalyst to shift the mortgage reform discussion in Washington from inaccuracies, political rhetoric and name-calling to a serious analysis of the competing plans on their merits. When and as that occurs—as I believe it will—the optimism in my “Economics Trumping Politics” post about a fact-based administrative reform process prevailing over a misinformation-based political process should again seem justified, although it will take longer to play out than I expected originally.

these really arent swings.

The big swings were back in the old days when the stock would gain/drop 1.00 in less than an hour.

No. Why would anyone expect any different. No other reason to go after the CFPB the way they have.

Getting tough with Wells Fargo while totally ignoring Fannie Mae and Freddie Mac.

I'm sure that his tweet means a lot!

Dear Judge Steele,

Tell your former colleagues to grow a set and do the right and lawful thing. The public reads these ridiculous rulings coming out of the courts which only lowers the abysmal opinions the public has about the current judicial system. To do so, you might have to grow a set yourself.

A downtrodden Fannie and Freddie shareholder

My optimism tanked yesterday and today sold over a 1/3. In attempt to keep up with my failure :-[... maybe get back in later

300,000 in the sale column!!!

Meaning that they won't appeal?

e-mail reply from Delaware Case .....

*******************************************************

usnavycmdr@gmail.com> 6:41 AM (54 minutes ago) to Myron

Good Mornin' Judge Steele ...

What is Gary Hindes next move ? Appeal ?

Which pending Circuit Court Case stands a "better chance"

in prevailing against the HERA anit-injunction clause ?

Thanks ...

******************************************************

Steele, Myron T. <msteele@potteranderson.com>

7:31 AM (3 minutes ago) to me

If we appeal, it would be the 3rd

Sent from my iPad

300,000 share block trade. Someone is blasting out. Eject! Eject!

LOVING the VERY TRADEABLE Volatility ....

if you prefer to jus watch the ACTION ... no worries

enjoy the JOURNEY ....

Loving the short!!!!

the Bollinger Band TRADE ... BUY outside Below ... Take Profits outside ABOVE

the GSE "Conga line Dance"

on the OTCBB cesspool exchange

TRADE ACCORDNGLY ... GOOD TRADING ALL !!!

$Mega Dittos .... $

....

....

FNMAS HAS A HUUUUUUUUUUUGE GAPPPPPPP LOLOLOL

Mr. Thompson sent a similar letter to the Eighth Circuit today,

and a copy of that letter is attached to this e-mail message.

http://www.glenbradford.com/wp-content/uploads/2017/12/17-1727-0024.pdf

Mr. Thompson continued his letter writing campaign today

by telling the Fifth Circuit to follow Judge Brown’s reasoning,

and a copy of that letter is attached to this e-mail message.

http://www.glenbradford.com/wp-content/uploads/2017/12/17-20364-00514265203.pdf

David Thompson at Cooper & Kirk, representing the Roberts Plaintiffs,

tells the Seventh Circuit in a letter filed today that the Sixth Circuit

and Judge Sleet read HERA way too expansively.

“HERA confers on FHFA a limited set of enumerated powers . . . and

pillaging the Companies’ balance sheets is not among them,”

Mr. Thompson says.

Mr. Thompson urges the Seventh Circuit to tell

FHFA it’s gone too far and follow Judge Brown’s dissent.

ONAMA STOLE $500B FROM FNF!

Get what I'm saying?

Sure did and a very BIG CHUNK.

I think this is a base valuation. if you apply this numbers at freddie, the valuation is more high because there is less shares outstanding and the cushion for an hipotetical rescue is smallest. my bet is for freddie!!

Did you BUY the foolish LEMMING DIP ?

realtime LEVEL II ...

Federal guarantee of MBS is a twofer for big banks

BY GLEN CORSO, — 12/07/17 03:20 PM EST

Federal guarantee of MBS is a twofer for big banks

A proposal to provide a federal guarantee only on mortgage-backed securities (MBS) issued through Fannie Mae and Freddie Mac (or their successors) as part of mortgage market reform will leave small lenders and their customers out in the cold and hand the mortgage market back to the big bank lenders.

A federal guarantee only on MBS further tilts the competitive field in the mortgage market to the big bank lenders in two ways. First, borrowing costs for Fannie/Freddie, known formally as government sponsored enterprises (GSEs), will increase and that increase will be disproportionately borne by small lenders selling their loans to the GSEs.

Second, a federal guarantee on MBS means that they become assets that carry a zero capital charge for the big banks, which means they can purchase and hold those MBS at highly favorable prices, a competitive advantage that is beyond the reach of small lenders.

As the House Financial Services Committee continues its preparatory work for a full-blown consideration of GSE reform in 2018, it appears that there is a gathering consensus that a federal guarantee will be necessary for the housing finance system to operate.

Currently, the preferred stock purchase agreements between the U.S. Treasury and Fannie and Freddie are an implicit federal guarantee for each organization. That implicit guarantee favorably affects both the borrowing costs for the GSEs and the MBS they issue, resulting in lower costs for consumers, both those whose mortgages are sold to the GSEs through the cash window and those whose mortgages are financed through direct placement in MBS.

Small and mid-size lenders who typically sell to the GSEs through the cash window thus are able to remain competitive with larger lenders who place their mortgages directly in MBS that they issue through the GSEs.

The consumers served by smaller lenders get the benefit of those competitive rates.

If the federal guarantee only extends to the MBS issued by the GSEs, then small lenders and their customers would lose their direct access to those competitive rates as borrowing costs for the GSEs would increase, including the borrowing costs associated with financing mortgages purchased through their cash windows.

The prices offered to small lenders selling to the cash window would decline to offset those increased costs.

Now you might think that small and mid-size lenders could side-step this competitive disadvantage by accumulating mortgages in order to place them directly in federally guaranteed MBS that they would issue through the GSEs.

But that ignores the twofer that favors the big banks in the MBS federal guaranty proposal. The big banks will have an advantage, thanks to their capital rules, over midsize and small lenders. An advantage that some analysts have pegged at $200 billion+.

They will be able to use that advantage to regain the dominant position they enjoyed in the pre-2011 days when the GSEs extended discounted guarantee fees only to big lenders, forcing midsize and small lenders to sell their loans to the big guys.

The advantage the big banks will have is that they can own securities issued or guaranteed by their national government without holding any capital against those securities, nor would they have minimum liquidity requirements for those investments.

They would be able to extend that advantage to the primary market as well, where their mortgage subsidiaries operate.

The big banks could decide how much of their advantage they want to share with borrowers in the primary market by offering discounted interest rates.

Those rates could not be matched by midsize and small lenders either through sales to the cash window or by issuing their own MBS, since small and midsize lenders lack the ability to purchase and hold their own MBS with zero capital costs and no liquidity requirements.

So presto chango, we are back to the pre-2011 days when the only way midsize and small lenders can serve the home financing needs of their customers is to go hat-in-hand to the big bank lenders and sell them their mortgages and the servicing rights to those mortgages at a price set by the big banks.

For these reasons, the proposal to place a federal guarantee only on MBS as part of mortgage market reform is a bad idea. It puts a big, fat thumb on the scale in favor of the big bank lenders and leads to fewer choices for consumers. It should be rejected by Congress.

Glen Corso is the executive director of the Community Mortgage Lenders of America, which is a trade association that represents lenders who originate mortgage loans, sell mortgage loans to permanent investors and who service those loans.

Yes it appears that there is an unfilled gap at 2.45.

That morning pump is like clockwork

How about this?

H.R. 4560: To suspend contributions by Fannie Mae and Freddie Mac to the Housing Trust Fund during any period that the full required dividend payments under the Senior Preferred Stock Purchase Agreements for such enterprises are not made, and for other purposes.

Another gap to fill, what a racket.

You will agree with me that if the warrants are exercised to capitalize the gse and have a cushion of 100b, all this money is real and has to be counted as assets. then the value of the company must have at least this value. $ 100b / 5b shares = pps $ 20

* * $FNMA Video Chart 12-07-17 * *

Link to Video - click here to watch the technical chart video

Senator Heitkamp, Thank You! Fannie & Freddie Are The Only Game In Town; & AverageJoe Plan Is Fair And Balanced.

Make America Great Again!

Let's Rock!

https://twitter.com/nsfraudbuster/status/938986987049984008

National debt accounting

The on- or off-balance sheet obligations of the two GSEs,

which are "independent" corporations rather than federal agencies,

are just over $5 trillion, a significant amount when compared to

the $9.5 trillion of officially reported United States public debt

at the time of the takeover.

The September 6, 2008 conservatorship and the subsequent planned

Treasury infusion of capital support the senior liabilities, subordinated

indebtedness, and mortgage guarantees of the two firms.

Some observers see this as an effective nationalization of the companies

that ultimately places taxpayers at risk for all their liabilities. The federal government follows specialized accounting standards set by the

Federal Accounting Standards Advisory Board.

The net exposure to taxpayers is difficult to determine at the time

of the takeover and depends on several factors, such as declines

in housing prices and losses on mortgage assets in the future.

The Congressional Budget Office director Peter R. Orszag announced

on September 9, 2008 that the CBO intended to incorporate the assets

and liabilities of the two companies into their federal budget planning,

due to the degree of government control over the entities.

The White House Budget Director Jim Nussle, on September 12, 2008

indicated their budget plans would not incorporate the GSE debt into

the budget because of the "temporary nature" of the conservator

intervention.

GSE can raise $100B by same dilution % as if warrant is exercised

Government may not exercise 79.9% warrant but Gov can force GSE to raise $100B by same dilution. That will be easy with no lawsuits. That's why Mnuchin say, "When we reform GSE, make sure GSEs do not require bailout again."

He can put this $100B in the treasury bond generating $3B per year.

Use $3B to as fee for LOC and trust fund.

You will see mother of all wild ride in following scenario:

1. GSE will be recap, release and relisted with warrant being exercised - going $60

2. Dilution by 5 times same as warrant to raise $100B - Back to $20.

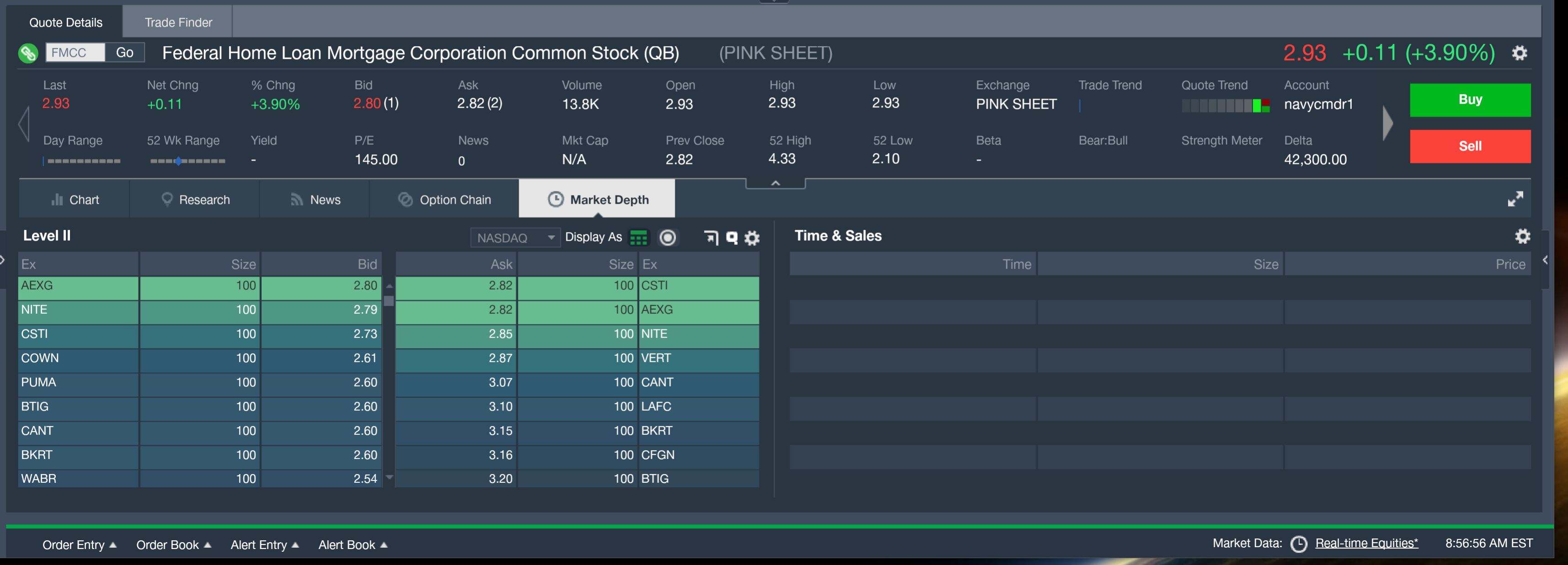

pre-mkt LEVEL II ... 13,800 Freddie Trade $2.93 _+.11

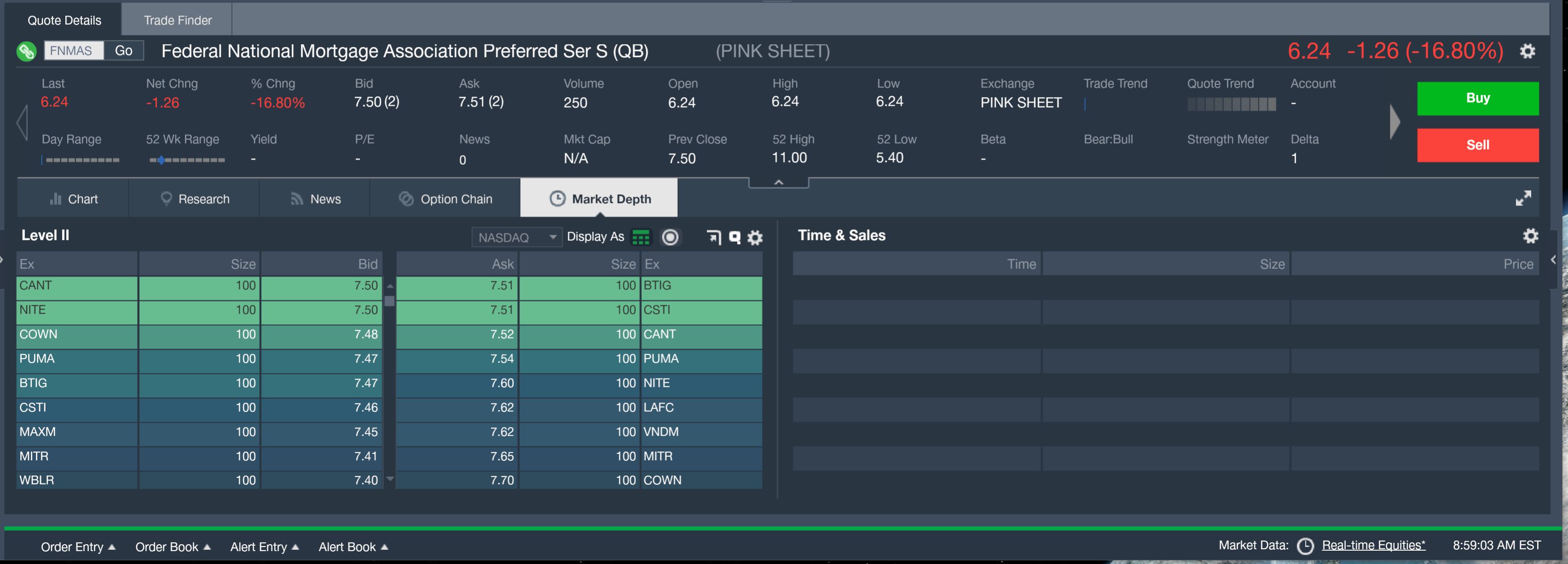

pre-mkt FNMAS _-$1.26 _250 shares

Exactly what about Dodd Frank places a burden on these banks. Give me an example. Curious to know because I have never heard anyone with specifics.

Financial condition of Fannie and Freddie prior to takeover

Over 98% of Fannie's loans were paying timely during 2008.

Both Fannie and Freddie had positive net worth as of the date

of the takeover, meaning the value of their assets exceeded

their liabilities.

As of March 31, 2009, seriously delinquent loans accounted for 2.3%

of single-family mortgages owned or guaranteed for Freddie Mac and

3.2% for Fannie Mae.

While those are historically high levels, they compare favorably to

industry averages of 4.7% for all prime loans, 7.2% for all single-family

mortgages, 24.9% for all subprime mortgages, and 36.5%

for subprime adjustable rate mortgages

all their money counted as assets

these are warrants at a penny or so - not options at a buck or more?

agree ... $23-$47 very reasonable valuation at this point

are ya ready for a new 52-wk Hi ?

|

Followers

|

2353

|

Posters

|

|

|

Posts (Today)

|

7

|

Posts (Total)

|

804079

|

|

Created

|

07/14/08

|

Type

|

Free

|

| Moderators not one red cent ~NORC~ stockprofitter Ace Trader EternalPatience jeddiemack FOFreddie | |||

Fannie Mae (the Federal National Mortgage Association, or FNMA) is a government-sponsored enterprise (GSE) in the U.S. that was established in 1938. Its main purpose is to provide liquidity, stability, and affordability to the U.S. housing market. It does this by purchasing mortgages from lenders (like banks), packaging them into mortgage-backed securities (MBS), and selling those securities to investors. This process ensures that lenders have more capital to issue new home loans, helping more Americans get access to homeownership.

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |