News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

You’re being generous with $.05 lol

Commons keep going up. Preferreds keep going down. Commons headed to $325. Preferreds headed to $0.05.

That’s what scares me, we’re playing poker with our cards facing the corrupt Govt. Very sad indeed !

"3 years old by a guy no longer President. Not sure he would remember this anyway. I haven't seen that he's mentioned the GSEs since that 3 year old letter. Has he?"

So what about Rand Paul? In one ear and out the other?

"I guess I am just trying to figure out why this is taking so long. "

Two reasons:

1) The judge and his staff know NOTHING about finance and are struggling with the division.

2) The judge, a government employee, NEVER wanted the plaintiffs to win, and they did, so he is dragging his feet as much as humanly possible (and doing a good job).

Lamberth will not rule in any way here that will benefit shareholders or harm the defendant. Company man.

Thompson talks abt eventual exit from conservatorship, as if it will magically happen.

— Chris Roberts (@RobertsChris6) April 18, 2024

She needs to work with Yellen to move ahead. Always the excuse, "waiting for Congress", Yellen is silent.

Mnuchin & Calabria knew a) HERA allows them to act, b) took steps to act on their own.

My potential profit on GSE holdings is not enough reason to vote for DJT or JOE

There are major issues on the table

Pick and Choose but voting on GSE profit - unless you own 1,000,000 shares I guess - is missing the forest for the tree

Did not read

but

tons of corporations - like Oil companies and Builders are absolutely looking 10-20 years out to what climate change will have done to our USA land and such

it is smart -- and does not need to be political just good BUSINESS

e.g. it is my understanding that oil companies have major difficulty issuing 30 year bonds without a big boost on interest paid --- it just is the market (Same IMO if Tesla tried to issue 30 year bonds --- into the haze around EV)

oops

I tried to think but had no time ?

792454

why not have Freddie and FNMA for JPS pay to equity holders ?

such payment - if it ever where to occur goes to equity holders AND the decrease of cash or surplus at the GSE is meaningless ---- until there is freedom

This tiny payment does zero damage to the value of F and F that equity holders wish to get back IMO

Mortgage rate manipulation:

Homeowners in the US filed a class action lawsuit in October 2012 against twelve of the largest banks which alleged that Libor manipulation made mortgage repayments more expensive than they should have been from loans including Fannie Mae and Freddie Mac.

Statistical analysis indicated that the Libor rose consistently on the first day of each month between 2000 and 2009 on the day that most adjustable-rate mortgages had as a change date on which new repayment rates would "reset". An email referenced in the lawsuit from the Barclay's settlement, showed a trader asking for a higher Libor rate because "We're getting killed on our three-month resets. During the analysed period, the Libor rate rose on average more than two basis points above the average on the first day of the month, and between 2007 and 2009, the Libor rate rose on average more than seven and one-half basis points above the average on the first day of the month.

The fifteen lead plaintiffs included a pensioner whose home was repossessed after her subprime mortgage was securitised into Libor-based collateralised debt obligations, sold by banks to investors, and foreclosed. The plaintiffs could number 100,000, each of whom has lost thousands of dollars. The complaint estimates that the banks earned hundreds of millions, if not tens of billions of dollars, in wrongful profits as a result of artificially inflating Libor rates on the first day of each month during the complaint period.

Punitive damages…hahaha!!

Can we just be happy with a cup and handle?

Why would you even respond to him?

If I’m wrong so be it

See you on the other side lol

Let’s go Fannie!

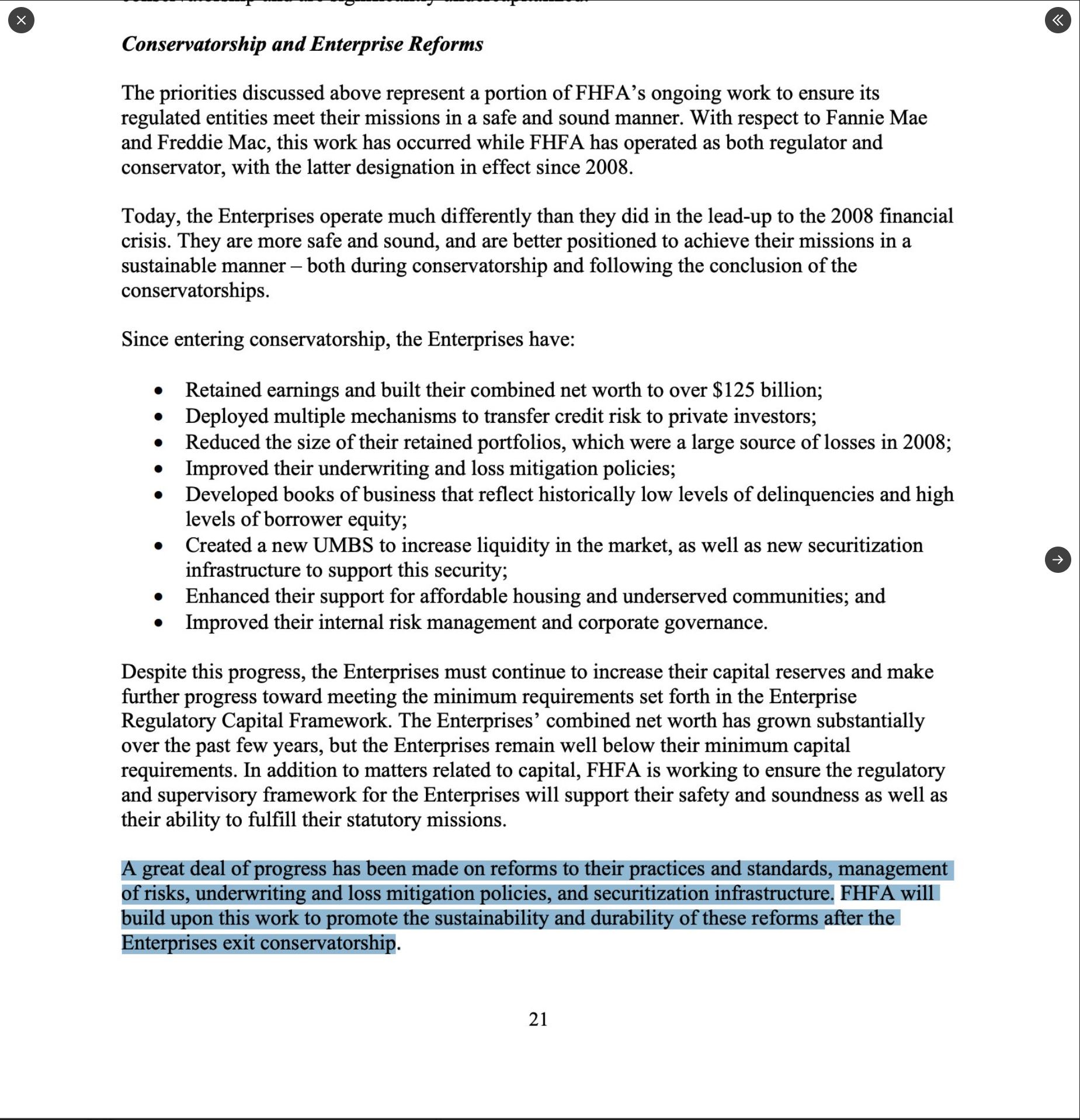

Rood mentions page 28.

Your post shows page 21.

Is there more info on page 28?

Page 21 you highlighted shows an intended Fhfa job description for after conservatorship has ended.

Interesting that she writes this.

Thx again for the info

Agreed

— D.L. (@outerspace987) April 23, 2024

The very last sentence of a 28 page written testimony on the GSEs mentioned getting the GSEs ready for an exit from conservatorship. Judge for yourself what that means.

— Tim Rood (@tim_rood_) April 23, 2024

Fascinating trend in legislating and fiscal spending - find ways for the private sector to pay for or just finance the policy and outcomes the gov wants. CARES Act (servicers and mom and pop investors - “you mind covering those missed payments?” Or the GSEs - (opportunistic…

— Tim Rood (@tim_rood_) April 23, 2024

You’re wrong I don’t defend the SPS LP increased for free. And I don’t support the Treasury confiscation of over $301 billion eluding to keep it in their coffer!

The separate account plan you are advocating the Treasury returns the money confiscated returns it back to the shareholders?? And will you kindly tell us the date this will happen??

You are absolutely correct on Sandra. I urge everyone here to ask your family and friends to vote for Trump. Else I can bet NWS will start after they reach $200b capital as per Calabria/mnuchin agreement.

Parrot wanted to turn around calabria ship and he did that by installing dumb Sandra.

That's related to a LIBOR settlement approved in 2020. Hello?

The LIBOR case comprises several litigation alleging the existence of an international conspiracy, better known as "The Allies".

Your are talking about the brief filed yesterday by one plaintiff of those awarded a settlement, the Exchange-based Plaintiffs that transacted in LIBOR-based Eurodollar futures or options on exchanges, and regarding a dispute with his lawyer.

https://www.usdliboreurodollarsettlements.com/

As far as I know, FnF are in a different group of plaintiffs: The OTC Plaintiffs, basically those that used swaps for hedging interest rates.

There is also a Class Action for those with investments Libor-based.

You want to pass it off as a settlement with FnF using multiple aliases, "Hi Ron!", because you've been ordered to post court news no matter what.

You even post the estimation of calendar for the release of the first quarter of 2024 Earnings report wrong, because all the financial websites I checked out, provide an estimation of April 30th. At least, tell us your source.

Although we have to wait for the official announcement of the scheduled release by the managements a few days earlier.

Looks like Libor settlement will be announced in conjunction with earnings May 5-6, 2024.

By the way, Hamish, as part of a Takings case, not as part of the Separate Account plan (SPS LP increased for free is the Phase 3) in accordance with the law.

Another one crying out loud: "We've been robbed!"

Fanniegate will be an "inverse settlement" case with all the frivolous litigation.

The litigants and company will have to pay Punitive Damages to the Equity holders, accused of stock price manipulation, abuse of court process and Making False Statements for the cover-up of many statutory provisions and rules, like the Restriction on Capital Distributions, besides financial concepts.

There is a 6-box checklist for scrutiny of the plotters and to levy a penalty for punitive damages.

Although the checklist is extended to 9 boxes to see the extent of their involvement in the Fanniegate scandal.

It was posted here.

It's you who defends the SPS LP increased for free along with the rest of plaintiffs and other plotters (Ackman, Berkowitz, etc.), because you haven't brought it up to court in your lawsuit.

Only the attorney Hamish Hume just a few months ago in the Wazee case and with a 3rd amended complaint. But he is covering it up in the Lamberth court where he is a party too, because it would blast his case and the claim of damages of one-day share price drop on the 3rd amendment-day, as it is the same Common Equity Sweep as before with the NWS dividend, and also, it blasts the Class Action altogether, as it wouldn't put an end to the controversy as a prerequisite to authorize Class Actions.

We even have the case of the attorney for Berkowitz, the almighty and omnipresent David Thompson, who even claims in court in the Rop case that with the SPS LP increased for free, it has achieved a Wonderland scenario based on the Financial Statement fraud in FnF (these gifted SPS LP and its offset, reduction of Retained Earnings account, are absent from the Balance Sheets), where the UST gets rich with gifted SPS and, at the same time, FnF are recapitalized, and thus, he requested constitutional damages, arguing that the "for cause" removal restriction prevented this scenario from happening sooner, sacking Mel Watt before.

On the other hand, the Separate Account plan, that states that the SPS LP increased for free as compensation to the UST in the absence of dividend payments, is a capital distribution (Definition number 1: 12 U.S.Code §4502(5)(A)) restricted (U.S.Code §4614(e)), and therefore, it's applied towards the exception to the restriction in order to legalize it.

In this case, the exception added to the one the statute posted before, enacted in a July 20, 2011 Final Rule "for the transparency of the conservatorships", and also with the objective to uphold the FHFA-C's "PUT FnF IN A SOUND CONDITION" power: recapitalization in a separate account (12 CFR 1237.12, in either of the 4 exceptions, because it supplements and shall not replace or affect the restriction by statute posted before, that also means recapitalization at the same time the SPS LP is reduced, with assessments sent to UST under the guise of dividend payments, as they are restricted too -Number 1 in the definition of capital distribution-, besides unavailable Earnings for distribution as dividend, out of an Accumulated Deficit Retained Earnings accounts.)

Therefore, the way to comply with the law is simply: the Common Equity is held in escrow, pending unwinding the operations. Other theme is that it's unnecessary to do it in the Balance Sheet if the operations haven't been recorded in the first place.

We can see how it's held in escrow in this image:

Actions have consequences and now, no one can pretend that it didn't happen: It needs a settlement of this Securities Law violation (7 in total during conservatorship: SPS LP increased instead of issued, to skip the December 2009 deadline on purchases by UST of high yield SPS, etc.), that the S.E.C. is aware of:

S.E.C. complaint 15976-876-848 submitted on August 2020.

Important clarification: the charge on the Income Statement that makes FnF post $0 EPS every quarter, is correct.

Finally, it gets better. The Lamberth rebate is another capital distribution and thus, restricted, included in the definition of capital distribution in an amendment inserted by the FHFA Final Rule of July 20, 2011, thanks to an express grant of authority to do it in the FHEFSSA posted above (Definition number 3: CFR 1229.13)

The Liquidation Preference continues to increase. And this is okay?

Yes we will make it to the 20th anniversary sadly. We are at $125B but need $200B per the capital rule. I doubt very much this rule will be amended by Thompson. She knows nothing. She is incapable of writing a new rule. I doubt she can read or write. I firmly believe she is illiterate. She should be cleaning and dusting the FHFA offices every night not running the place. The irony of it all. I am WhaleBalls.

What is it, the 16th Anniversary coming up? Will we make it to the 20th :/

We are in excellent position better than ever before. Soft bashers will always pop up here and try and spread fear to scare you into selling and snap up your shares

Don’t get suckered

Strong Buy

FNMA

What is it, the 16th Anniversary coming up? Will we make it to the 20th :/

Now as in next 0-4 years? May be..

possible.

Chances exist

Hopefully

Feasible

Probable

Might happen

Cannot say 4 sure

The government has milked the gses for as much as it could now there going to release them 🛹🌵🇺🇸

If you go back and click on the link from my post from stockprofiter has you’ll see that’s the real McCoy

Yep ! low volume and short % way down here's to the next leg up !! Even the Fullstoc's line has crossed. This one's easy to predict !

3 years old by a guy no longer President. Not sure he would remember this anyway. I haven't seen that he's mentioned the GSEs since that 3 year old letter. Has he?

Lol...

Are we speaking with..

Arnold or Benedict

right now?

The Freddie Mac and Fannie mae board Risk Committee has primary oversight of climate related risks....and have no acknowledgement of stealing shareholders retirement investment?

So the sky is falling?

Thieves will get their justice. I fret not over those who do evil...and envy not those that do wrong...they will wither...wither quite quickly.

Shareholders want justice...reparations!

Stop being the weather reporter and give back our money!

Yeah, but that's from 4/20. Someone was smoking something! 🤣

It just means case has gotten a verdict. Doesn’t mean appeals are through though.

Toonie Tuesday!!

Twooooooooooo!

Spot on as usual. Thanks for posting!

Thank you @imbellish I guess I am just trying to figure out why this is taking so long. I think I was just getting hopeful that they are finally giving the rightful owners some of their money back.

Sounds good AlongZ take your own advice and go away!

The website archive has status Pending in July 2023 and Recently Settled in September 2023.

FHFA : Incorporating Climate-Related Risks into Governance ...

Published: 4/22/2024

https://www.fhfa.gov//Media/Blog/Pages/Incorporating-Climate-Related-Risks-into-Governance.aspx

Following FHFA’s Conservatorship Scorecard guidance, Fannie Mae and Freddie Mac have made progress on developing foundational climate risk frameworks, integrating climate risk considerations into their strategic planning, incorporating climate risk considerations into their management and board reporting structures, and developing educational resources for their workforce. The Federal Home Loan Banks are continuing to individually develop their decision-making processes and governance structures in consideration of climate change.

Background

In October 2021, the Financial Stability Oversight Council (FSOC) released a report1 identifying climate change as an emerging and increasing threat to financial stability. Several international organizations and standard-setting bodies have recently developed frameworks to understand, assess, and manage climate-related risks to the entities or markets within their statutory jurisdictions. These include frameworks established by the Task Force on Climate-Related Financial Disclosures,2 Bank for International Settlements (BIS),3 and U.S. regulators (Office of the Comptroller of the Currency, Board of Governors of the Federal Reserve System, and Federal Deposit Insurance Corporation),4 as well as guidance5 and hypothetical scenarios6 developed by the Network for Greening the Financial System (NGFS).7

Federal Housing Finance Agency (FHFA)

FHFA, the conservator and regulator of Fannie Mae and Freddie Mac, and regulator of the Federal Home Loan Banks (collectively, the regulated entities), recognizes the emerging and increasing threat to all stakeholders in the housing system due to climate risk and the increased frequency and intensity of major natural disasters. Strong governance is foundational to managing an institution’s risk profile, particularly when the institution must address a constantly evolving landscape of risks. Accordingly, FHFA included the need to identify ways to incorporate climate change into regulated entity governance in its 2022-2026 Strategic Plan.8 Since 2022, FHFA has established goals for Fannie Mae and Freddie Mac (the Enterprises) to develop company-wide frameworks that incorporate climate risk into existing governance and risk management structures and decision-making, and to incorporate both short- and long-term strategies into the Enterprises’ strategic planning processes.

FHFA established an internal Climate Change and ESG9 Governance Working Group (Working Group) to evaluate the integration of climate risk into the corporate governance, risk management, and strategic planning structures of the regulated entities, and incorporation into operational and business decision-making. The Working Group meets regularly with the Enterprises and evaluates their progress through the annual Conservatorship Scorecard process, reviewing the establishment of foundational governance structures, decision-making processes, and risk management practices around climate risk. The Working Group also reviews progress made by the Federal Home Loan Banks in these areas.

Enterprises

Since 2022, the Enterprises have made distinct progress towards these goals and have been focused on: developing foundational climate risk frameworks, integrating climate risk considerations into strategic planning, incorporating climate risk considerations into management and board reporting structures, and establishing training and educational resources for their workforce.

Developing ?Climate Risk Frameworks

The Enterprises have developed initial climate risk frameworks that are incorporated in their enterprise risk management frameworks in consideration of the impact that climate change could have on the achievement of their mission, strategy, and business objectives.

The Enterprises continue to make progress and develop their capacity to measure the effects of climate risks and integrate climate-related risks into risk management structures:

Freddie Mac has developed climate scenario methodologies to better quantify the impact of climate events on housing affordability, property values, and credit risk;

Fannie Mae is working on finalizing climate scenario design and methodology for intended reporting in 2024; and

Both Ent?erprises completed exploratory climate scenario analysis exercises on flood risk in 2023.

Strategic Plan Integration

To assess and address climate-related risks and opportunities that could affect their businesses, the Enterprises have been incorporating climate issues into their corporate strategic plans and planning processes.

Each Enterprise has completed ESG materiality assessments that inform their ESG and climate strategic planning processes.

Fannie Mae’s 2023-2025 Strategic Plan includes climate risk management and supporting the housing ecosystem’s adaptation to climate change as priorities.10

Board and Management-level Reporting

Fannie Mae

The board Risk Policy and Capital Committee has primary oversight of climate-related risks.

The board Audit Committee provides oversight of ESG-related reporting, which includes climate risk.

The board Community Responsibility and Sustainability Committee oversees the development and implementation of Fannie Mae’s climate risk strategy.

There is a newly established Climate Risk Committee at the management level, and Fannie Mae has designated senior executive officers to oversee climate and ESG.

Freddie Mac

The board Risk Committee has primary oversight of climate related risks.

The board Audit Committee provides oversight of ESG-related reporting, which includes climate risk.

The board Mission and Housing Sustainability Committee provides oversight responsibilities for the development, planning, implementation, performance, and execution of Freddie Mac’s mission strategies and significant initiatives, including the review of sustainability initiatives with climate change implications or impacts.

Freddie Mac has also established several advisory and steering committees at the management level for ESG and climate risk reporting.

Training and Education

Over the last few years, the Enterprises have begun educating staff on the potential impacts of climate-related risks, taking into consideration the interconnectedness and multi-dimensional nature of climate-related topics that could reach all aspects of the organization.

Federal Home Loan Banks

The Federal Home Loan Banks also continue to develop their decision-making processes and governance structures in consideration of climate change. In June 2023, the Federal Home Loan Banks released an inaugural Corporate Social Responsibility Report11 highlighting governance and risk management as foundational to their ability to meet the needs of their members and districts.

FHLBank Mission and Foundational Principles

?

?Individually, each Federal Home Loan Bank is addressing climate-related risks in accordance with its own governance and management structures. For example, the Federal Home Loan Bank of Dallas’s 2022 ESG Report12?? highlights the formation of an ESG Committee providing oversight of the FHLBank’s ESG activities. The committee assists the executive management team and board with setting ESG strategy and reviewing reports and recommendations from subcommittees, including the Climate Risk Subcommittee. At the Federal Home Loan Bank of New York, “Climate and Natural Disaster” risks have been included into the scope of the board’s Risk Committee charter.

Summary

The work undertaken by the Enterprises and Federal Home Loan Banks in managing climate risks continues to be iterative and ongoing. For 2024, FHFA established priorities for the Enterprises in the Conservatorship Scorecard related to climate risks. For the governance area, this includes strengthening risk management capabilities in identifying, assessing, controlling, monitoring, and reporting on climate risk and incorporating these capabilities into the Enterprises’ overall risk frameworks.

Responsibilities of the FHFA Climate Change and ESG Governance Working Group:

Evaluate the integration of climate risk into the corporate governance, risk management, and strategic planning structures of the regulated entities, and incorporation into operational and business decision-making.

Monitor the development and maturation of the regulated entities’ climate risk frameworks and strategic planning processes.

??

Readers are encouraged to explore the FHFA Climate Change & ESG homepage for additional blogs and information related to climate risk.

1 Financial Stability Oversight Council, Report on Climate-Related Financial Risk, 2021, https://home.treasury.gov/system/files/261/FSOC-Climate-Report.pdf.

2 The Financial Stability Board, established to coordinate at the international level the work of national financial authorities and international standard-setting bodies in order to develop and promote the implementation of effective regulatory, supervisory and other financial sector policies, created the Task Force on Climate-Related Financial Disclosures in 2015 to improve and increase reporting of climate-related financial information.

3 The Bank for International Settlements is an international consortium of central banks and monetary authorities whose mission is to support central banks' pursuit of monetary and financial stability through international cooperation, and to act as a bank for central banks. See https://www.bis.org/about/index.htm. In 2022, the Basel Committee on Banking Supervision issued principles for the effective management and supervision of climate-related financial risks. See https://www.bis.org/press/p220615.htm.

4 On October 30, 2023, the Office of the Comptroller of the Currency, Board of Governors of the Federal Reserve System, and Federal Deposit Insurance Corporation jointly issued principles that provide a high-level framework for the safe and sound management of exposures to climate-related financial risks. See https://www.federalregister.gov/documents/2023/10/30/2023-23844/principles-for-climate-related-financial-risk-management-for-large-financial-institutions.

5 See https://www.ngfs.net/en/liste-chronologique/ngfs-publications.

6 See https://www.ngfs.net/ngfs-scenarios-portal/.

7 The NGFS is a voluntary group of central banks and supervisors that work together to contribute to the development of environment and climate risk management guidance and best practices in the financial sector for use both within and outside its membership.

8 See https://www.fhfa.gov/AboutUs/Reports/ReportDocuments/FHFA_StrategicPlan_2022-2026_Final.pdf.

9 ESG encompasses considerations of environmental, social, and governance factors. For the Enterprises, ESG covers their work to enhance environmental sustainability within the homes they finance, to advance consumer access to safe, resilient, and affordable housing opportunities in a sustainable manner, and to embed climate considerations within their board and management processes.

10 Fannie Mae’s 2023-2025 Strategic Plan is referenced in its 2022 Annual Report on Form 10-K (pp. 4) at https://www.fanniemae.com/media/46276/display.

11 See https://fhlbanks.com/the-federal-home-loan-banks-inaugural-corporate-social-responsibility-report/.?

12 See https://www.fhlb.com/getmedia/9cd26f43-96eb-4ac0-9dad-e109fd4abdb5/FHLBank-ESG-Report.pdf.

Authored by: Eric Kelley

Senior Strategic Analyst, Division of Conservatorship Oversight and Readiness

Authored by: Anne Marie Pippin

Deputy Director, Division of Conservatorship Oversight and Readiness

Authored by: La’Toya Holt

Senior Risk Analyst, Governance and Management Risk Branch, Office of Risk Analysis, Policy and Guidance and Development, Division of Enterprise Regulation

Editor: Varun Joshi

Economist, Climate Change and ESG Branch

https://www.ktmc.com/current-cases

Does anyone know why the recent court case is being listed as settled on the Attorneys website?

About 170K buy order at $1.43 just printed.

Free info from top trader

(Click here )

Rules pro trader uses for selecting stocks:

Avoid stocks in conservatorship

Stay away from stock that has all profits swept.

Run away from stock that is Billions in debt.

Follow these basic (FNMA ) rules to help improve chance of successful trader .

you said, "I was thinking"

no thinking allowed here...just LOAD UP and don't look back

?

he listens to DOJ?

he listens to POTUS

he listens to Congress

what is a judge who is a company man --- as Lamberth has a long history -- and I am sure has decided against GOV in many many cases

Indeed

I was thinking about how one replaced a CEO - of an agency - where there is no oversight panel or committee

Indeed - point well taken

Still the question --- on GOV overreach

Congress overreached when they wrote it this way

POTUS overreached when they followed the legislation

Agency overreached when they followed the financing dictated by law

Indeed - self funding - if that is the issue - is not typical and seems wrong ---- but I simply do not include this in the category of overreach which is an interesting point of view in many many cases where IMO the EO is over reach or an agency goes to far with regulation ? or Congress passes law where it should not venture per the constitution

Freddie pulls off low of $1.24 now at $ !.31.5

Fannie pulls off low of $1.35 now at $1.42.5

Raise The Ask - Raise The Ask - Raise The Ask - Raise The Ask -

|

Followers

|

2331

|

Posters

|

|

|

Posts (Today)

|

27

|

Posts (Total)

|

802380

|

|

Created

|

07/14/08

|

Type

|

Free

|

| Moderators not one red cent ~NORC~ stockprofitter Ace Trader EternalPatience jeddiemack FOFreddie | |||

Fannie Mae (the Federal National Mortgage Association, or FNMA) is a government-sponsored enterprise (GSE) in the U.S. that was established in 1938. Its main purpose is to provide liquidity, stability, and affordability to the U.S. housing market. It does this by purchasing mortgages from lenders (like banks), packaging them into mortgage-backed securities (MBS), and selling those securities to investors. This process ensures that lenders have more capital to issue new home loans, helping more Americans get access to homeownership.

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |