News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

300,000 in the sale column!!!

Meaning that they won't appeal?

e-mail reply from Delaware Case .....

*******************************************************

usnavycmdr@gmail.com> 6:41 AM (54 minutes ago) to Myron

Good Mornin' Judge Steele ...

What is Gary Hindes next move ? Appeal ?

Which pending Circuit Court Case stands a "better chance"

in prevailing against the HERA anit-injunction clause ?

Thanks ...

******************************************************

Steele, Myron T. <msteele@potteranderson.com>

7:31 AM (3 minutes ago) to me

If we appeal, it would be the 3rd

Sent from my iPad

300,000 share block trade. Someone is blasting out. Eject! Eject!

LOVING the VERY TRADEABLE Volatility ....

if you prefer to jus watch the ACTION ... no worries

enjoy the JOURNEY ....

Loving the short!!!!

the Bollinger Band TRADE ... BUY outside Below ... Take Profits outside ABOVE

the GSE "Conga line Dance"

on the OTCBB cesspool exchange

TRADE ACCORDNGLY ... GOOD TRADING ALL !!!

$Mega Dittos .... $

....

....

FNMAS HAS A HUUUUUUUUUUUGE GAPPPPPPP LOLOLOL

Mr. Thompson sent a similar letter to the Eighth Circuit today,

and a copy of that letter is attached to this e-mail message.

http://www.glenbradford.com/wp-content/uploads/2017/12/17-1727-0024.pdf

Mr. Thompson continued his letter writing campaign today

by telling the Fifth Circuit to follow Judge Brown’s reasoning,

and a copy of that letter is attached to this e-mail message.

http://www.glenbradford.com/wp-content/uploads/2017/12/17-20364-00514265203.pdf

David Thompson at Cooper & Kirk, representing the Roberts Plaintiffs,

tells the Seventh Circuit in a letter filed today that the Sixth Circuit

and Judge Sleet read HERA way too expansively.

“HERA confers on FHFA a limited set of enumerated powers . . . and

pillaging the Companies’ balance sheets is not among them,”

Mr. Thompson says.

Mr. Thompson urges the Seventh Circuit to tell

FHFA it’s gone too far and follow Judge Brown’s dissent.

ONAMA STOLE $500B FROM FNF!

Get what I'm saying?

Sure did and a very BIG CHUNK.

I think this is a base valuation. if you apply this numbers at freddie, the valuation is more high because there is less shares outstanding and the cushion for an hipotetical rescue is smallest. my bet is for freddie!!

Did you BUY the foolish LEMMING DIP ?

realtime LEVEL II ...

Federal guarantee of MBS is a twofer for big banks

BY GLEN CORSO, — 12/07/17 03:20 PM EST

Federal guarantee of MBS is a twofer for big banks

A proposal to provide a federal guarantee only on mortgage-backed securities (MBS) issued through Fannie Mae and Freddie Mac (or their successors) as part of mortgage market reform will leave small lenders and their customers out in the cold and hand the mortgage market back to the big bank lenders.

A federal guarantee only on MBS further tilts the competitive field in the mortgage market to the big bank lenders in two ways. First, borrowing costs for Fannie/Freddie, known formally as government sponsored enterprises (GSEs), will increase and that increase will be disproportionately borne by small lenders selling their loans to the GSEs.

Second, a federal guarantee on MBS means that they become assets that carry a zero capital charge for the big banks, which means they can purchase and hold those MBS at highly favorable prices, a competitive advantage that is beyond the reach of small lenders.

As the House Financial Services Committee continues its preparatory work for a full-blown consideration of GSE reform in 2018, it appears that there is a gathering consensus that a federal guarantee will be necessary for the housing finance system to operate.

Currently, the preferred stock purchase agreements between the U.S. Treasury and Fannie and Freddie are an implicit federal guarantee for each organization. That implicit guarantee favorably affects both the borrowing costs for the GSEs and the MBS they issue, resulting in lower costs for consumers, both those whose mortgages are sold to the GSEs through the cash window and those whose mortgages are financed through direct placement in MBS.

Small and mid-size lenders who typically sell to the GSEs through the cash window thus are able to remain competitive with larger lenders who place their mortgages directly in MBS that they issue through the GSEs.

The consumers served by smaller lenders get the benefit of those competitive rates.

If the federal guarantee only extends to the MBS issued by the GSEs, then small lenders and their customers would lose their direct access to those competitive rates as borrowing costs for the GSEs would increase, including the borrowing costs associated with financing mortgages purchased through their cash windows.

The prices offered to small lenders selling to the cash window would decline to offset those increased costs.

Now you might think that small and mid-size lenders could side-step this competitive disadvantage by accumulating mortgages in order to place them directly in federally guaranteed MBS that they would issue through the GSEs.

But that ignores the twofer that favors the big banks in the MBS federal guaranty proposal. The big banks will have an advantage, thanks to their capital rules, over midsize and small lenders. An advantage that some analysts have pegged at $200 billion+.

They will be able to use that advantage to regain the dominant position they enjoyed in the pre-2011 days when the GSEs extended discounted guarantee fees only to big lenders, forcing midsize and small lenders to sell their loans to the big guys.

The advantage the big banks will have is that they can own securities issued or guaranteed by their national government without holding any capital against those securities, nor would they have minimum liquidity requirements for those investments.

They would be able to extend that advantage to the primary market as well, where their mortgage subsidiaries operate.

The big banks could decide how much of their advantage they want to share with borrowers in the primary market by offering discounted interest rates.

Those rates could not be matched by midsize and small lenders either through sales to the cash window or by issuing their own MBS, since small and midsize lenders lack the ability to purchase and hold their own MBS with zero capital costs and no liquidity requirements.

So presto chango, we are back to the pre-2011 days when the only way midsize and small lenders can serve the home financing needs of their customers is to go hat-in-hand to the big bank lenders and sell them their mortgages and the servicing rights to those mortgages at a price set by the big banks.

For these reasons, the proposal to place a federal guarantee only on MBS as part of mortgage market reform is a bad idea. It puts a big, fat thumb on the scale in favor of the big bank lenders and leads to fewer choices for consumers. It should be rejected by Congress.

Glen Corso is the executive director of the Community Mortgage Lenders of America, which is a trade association that represents lenders who originate mortgage loans, sell mortgage loans to permanent investors and who service those loans.

Yes it appears that there is an unfilled gap at 2.45.

That morning pump is like clockwork

How about this?

H.R. 4560: To suspend contributions by Fannie Mae and Freddie Mac to the Housing Trust Fund during any period that the full required dividend payments under the Senior Preferred Stock Purchase Agreements for such enterprises are not made, and for other purposes.

Another gap to fill, what a racket.

You will agree with me that if the warrants are exercised to capitalize the gse and have a cushion of 100b, all this money is real and has to be counted as assets. then the value of the company must have at least this value. $ 100b / 5b shares = pps $ 20

* * $FNMA Video Chart 12-07-17 * *

Link to Video - click here to watch the technical chart video

Senator Heitkamp, Thank You! Fannie & Freddie Are The Only Game In Town; & AverageJoe Plan Is Fair And Balanced.

Make America Great Again!

Let's Rock!

https://twitter.com/nsfraudbuster/status/938986987049984008

National debt accounting

The on- or off-balance sheet obligations of the two GSEs,

which are "independent" corporations rather than federal agencies,

are just over $5 trillion, a significant amount when compared to

the $9.5 trillion of officially reported United States public debt

at the time of the takeover.

The September 6, 2008 conservatorship and the subsequent planned

Treasury infusion of capital support the senior liabilities, subordinated

indebtedness, and mortgage guarantees of the two firms.

Some observers see this as an effective nationalization of the companies

that ultimately places taxpayers at risk for all their liabilities. The federal government follows specialized accounting standards set by the

Federal Accounting Standards Advisory Board.

The net exposure to taxpayers is difficult to determine at the time

of the takeover and depends on several factors, such as declines

in housing prices and losses on mortgage assets in the future.

The Congressional Budget Office director Peter R. Orszag announced

on September 9, 2008 that the CBO intended to incorporate the assets

and liabilities of the two companies into their federal budget planning,

due to the degree of government control over the entities.

The White House Budget Director Jim Nussle, on September 12, 2008

indicated their budget plans would not incorporate the GSE debt into

the budget because of the "temporary nature" of the conservator

intervention.

GSE can raise $100B by same dilution % as if warrant is exercised

Government may not exercise 79.9% warrant but Gov can force GSE to raise $100B by same dilution. That will be easy with no lawsuits. That's why Mnuchin say, "When we reform GSE, make sure GSEs do not require bailout again."

He can put this $100B in the treasury bond generating $3B per year.

Use $3B to as fee for LOC and trust fund.

You will see mother of all wild ride in following scenario:

1. GSE will be recap, release and relisted with warrant being exercised - going $60

2. Dilution by 5 times same as warrant to raise $100B - Back to $20.

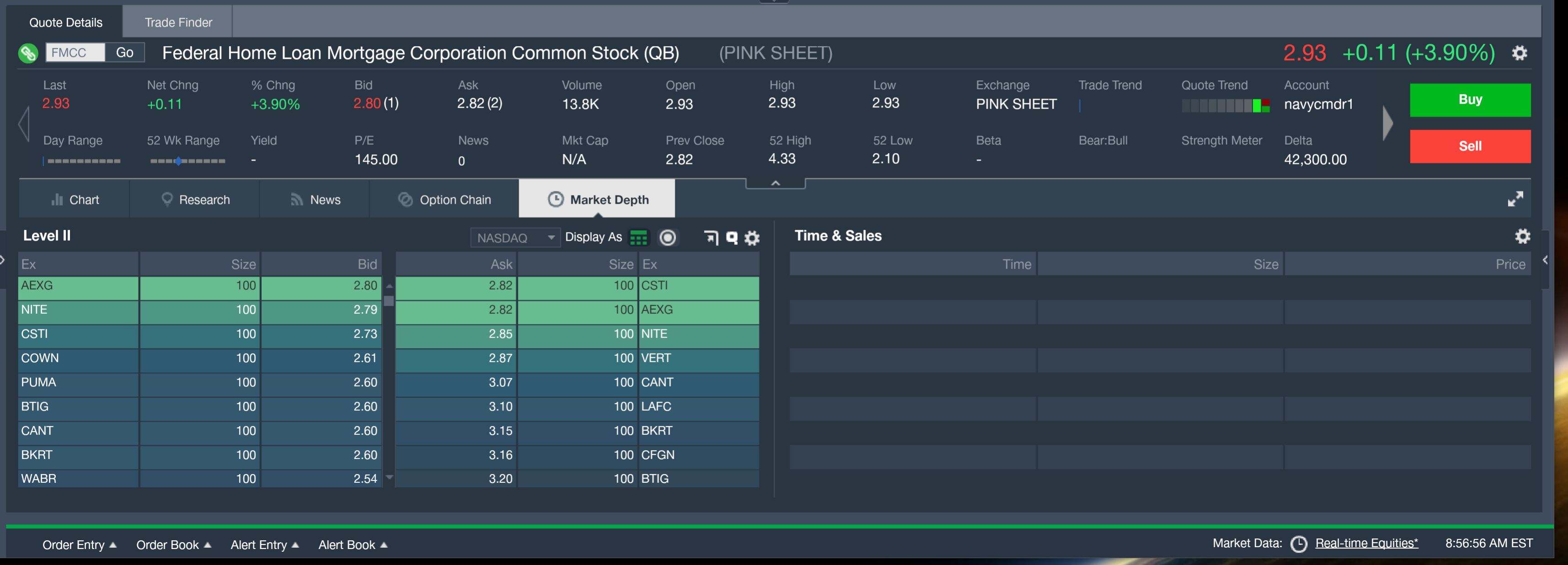

pre-mkt LEVEL II ... 13,800 Freddie Trade $2.93 _+.11

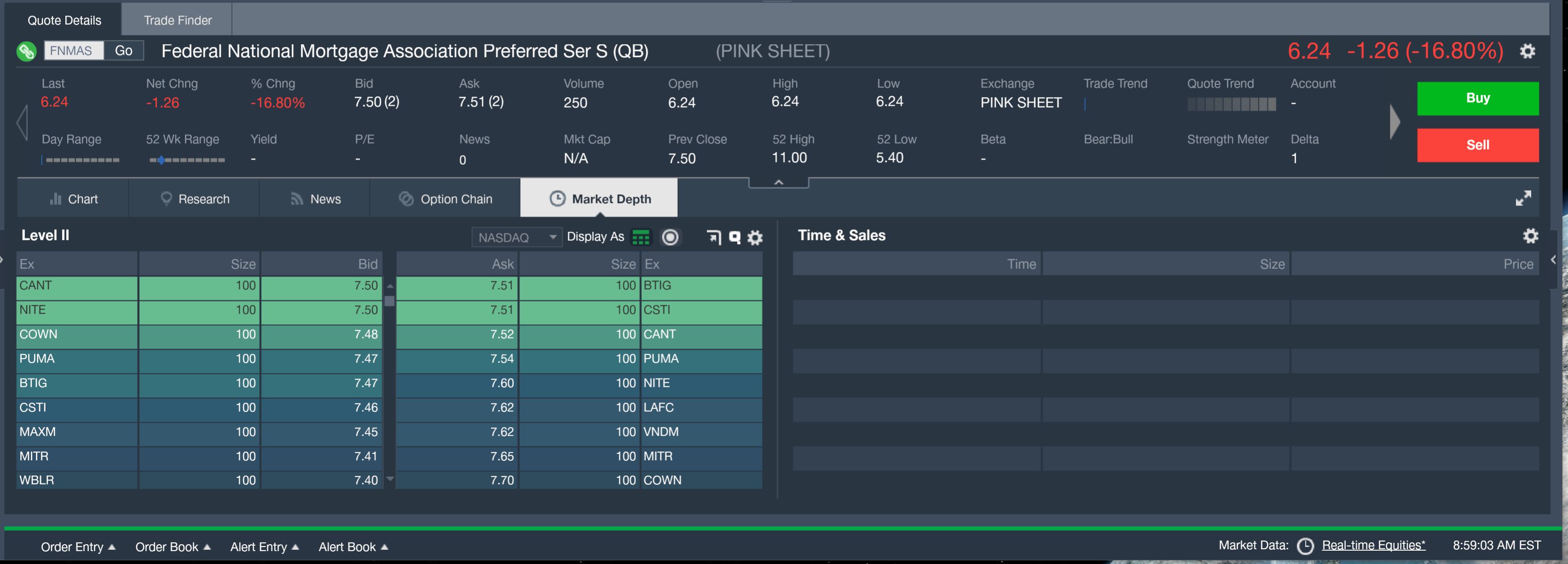

pre-mkt FNMAS _-$1.26 _250 shares

Exactly what about Dodd Frank places a burden on these banks. Give me an example. Curious to know because I have never heard anyone with specifics.

Financial condition of Fannie and Freddie prior to takeover

Over 98% of Fannie's loans were paying timely during 2008.

Both Fannie and Freddie had positive net worth as of the date

of the takeover, meaning the value of their assets exceeded

their liabilities.

As of March 31, 2009, seriously delinquent loans accounted for 2.3%

of single-family mortgages owned or guaranteed for Freddie Mac and

3.2% for Fannie Mae.

While those are historically high levels, they compare favorably to

industry averages of 4.7% for all prime loans, 7.2% for all single-family

mortgages, 24.9% for all subprime mortgages, and 36.5%

for subprime adjustable rate mortgages

all their money counted as assets

these are warrants at a penny or so - not options at a buck or more?

agree ... $23-$47 very reasonable valuation at this point

are ya ready for a new 52-wk Hi ?

the Warrants "are" ILLEGAL but the GOVT still OWNS them

unless the Courts Rule otherwise I expect the GOVT

to Convert them to Common & SELL them for additional TAXPAYER Profit

Agreed.

And they will shake the tree every now and then while we are OTC, I have seen it hapen with some many news-driven stocks on the OTC.

In my opinion, the projection of the ackman pps is correct, if the warrants are executed (complicated thing because the debt has been paid with interests) all there money must be counted as assets, making the value of the company rise considerably and consequently the value of the 'diluted' shares. if we add an annual net income of about 10b to all this, we will have annual profits of $2/share more or less. for all that I have exposed I think that the estimate of $25-45 made by ackman is quite prudent

Need I remind you that you have specifically posted that the warrants are illegal and would not be executed?

I fully expect the warrants to be executed, just curious why your posts change depending on the month.

GSE YIELDS FOREVER

Gaps have always filled with FNMA. That probably is not a gap. What is the date.

the GOVT OWNs 79.9% of the Common shares

the GSEs and the Common AIN'T GOIN' ANYWHWERE !!!

When the Treasury took over in 2008,

it maintained warrants on 79.9% of their

common shares. The remaining 20%

continued to trade in the public market,

where they soon fell under $1 a share.

(They had peaked at $86 in 2000.)

This high volatility confirms that we are at the last stage of conservatoship. i think it's a bad moment to trade, you can be out at there moment and you'll can't react. the smartest position is 'buy as you can' don't matter commons or prefd at the end everyone will win.

?

You do know that financial institutions had their most profitable year ever last year?

But they are dying under the burdens

There should be relief for the smaller and medium size banks

But the top 10 banks - which control most of the action in every way - need to be regulated. They are all Wells Fargo if you remove the veneer

Someone will looks with a silly face on the day that doesn't cover that gap and keep going up ...

Yes I think so, also trump mortgage LLC in 25 states had failed .

|

Followers

|

2353

|

Posters

|

|

|

Posts (Today)

|

18

|

Posts (Total)

|

804090

|

|

Created

|

07/14/08

|

Type

|

Free

|

| Moderators not one red cent ~NORC~ stockprofitter Ace Trader EternalPatience jeddiemack FOFreddie | |||

Fannie Mae (the Federal National Mortgage Association, or FNMA) is a government-sponsored enterprise (GSE) in the U.S. that was established in 1938. Its main purpose is to provide liquidity, stability, and affordability to the U.S. housing market. It does this by purchasing mortgages from lenders (like banks), packaging them into mortgage-backed securities (MBS), and selling those securities to investors. This process ensures that lenders have more capital to issue new home loans, helping more Americans get access to homeownership.

https://www.cbo.gov/publication/60190

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |