News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

again can one person tell me the date when the judge must reach his option on the courts decision

This is not at all what this means. I think you are getting some skewed info based on your news sources.

Legislative branch - creates/passes the laws (can no longer create vague laws and leave it to Agency puppets to interpret/change based on politics)

Executive branch - enforces the laws (The President is not suddenly immune from breaking laws. Presidentially appointed officials cannot create regulations that bypass laws or interpret them differently than what was intended by Congress)

Judicial branch - determines if the above actions follow the constitution and are interpreted accordingly

Pretty much gets us closer to what our forefathers intended.

I think it was that the GSEs, the entities themselves, would need to bring direct not derivative suit against FHFA, as opposed to the shareholders. But of course the GSE's board is under direct control of FHFA so that will never happen. I think that's separate issue from Chevron however.

I think you are being hyperbolic. Chevron ruling does not create an imperial POTUS. The unitary executive does not create a king. The official acts with immunity is not the Chevron ruling. What these rulings do is set the boundaries back to what the constitution declares. They actually strip power from the imperial king. The Chevron doctrine means that unelected bureaucrats under the president can no longer legislate through the administrative actions and rule making of the executive branch. It means Congress can no longer pass overly broad open ended statutes. It means that Congress will have to compromise and vote on new laws that would cover “major questions of society”. They need to do their homework and draft statutes that tell the Executive branch exactly what they are to administer. Over all this is a check on the power of the unitary executive if that is how you want to describe it. Imagine if the unitary executive could continue with the deference of the courts under the old Chevron decision. That is how we got into Fanniegate in the first place. It doesnt mean any of the fear mongering that you are spouting. We now have 3 co-equal branches of government again as it was originally conceived.

No. No one knows because the date isn’t written in stone yet. Appeals take place first. And no don’t ask when those are done.

some back of the envelope scribbles ... "selling volume" from 6/10 or 6/11 (the downward slide from last time we reached $1.60) was around 45 million shares with the biggest sell off on 6/21 ... once no obvious news supporting the "sell-off" was determined we rebounded the following monday then came the presidential debate and Chevron ... since then "buy-back" volume has been close to 25 million ... but things are drying up until someone (uh em, Trump) makes c'ship, housing, release, or the GSEs top line news

does anyone know the date of the ruling by the judge would be entered?

There is a library full of cases that argued "Post Fact" law and impact

None of it matters anymore

Good luck trying to forecast or predict what is right or wrong --- doable or not doable

it will wind up in court - and the court will tell us - without looking at the majority opinion of that library as Stare Decisis is out

What??? No! It reels in the unabated, unconstitutional power of unelected bureaucrats … and returns that power to the courts, where it belongs. “In a major ruling, the Supreme Court on Friday cut back sharply on the power of federal agencies to interpret the laws they administer and ruled that courts should rely on their own interpretion of ambiguous laws.”

Guido

FHFA was castrated by the death of CHEVRON --- it in essence does not exist OTHER than at the whim and power of POTUS (alone) and SCOTUS to tell us if POTUS was right

Everything is new

We will know if good for F and F -- maybe soon - maybe with JOE or maybe with DJT. We know if Congress wants change they are out of the picture ---- so here we are

Beware of what you want --- for us right now - FHFA is castrated

Death of Cheveron simply means that unelected busybody bureaucrats can’t push people around, just because they want to. Apparently, that was lost on you.

Court and POTUS ----- not agencies in the Executive !!!! - will now tell us what is right and wrong

Serious question

The Unitary Executive theory sort of started with RR and has since grown and grown as each POTUS took more power. As I read it and understand it - it is the Unitary Executive (power) theory that is what is under the SCOTUS decisions that nothing can stand between POTUS and "his" agencies and thus the consumer and housing agencies were "unconstitutionally built" . Does that make sense? (For the 40 years or whatever before the growth of the Unitary - All Powerful - POTUS theory - CONGRESS would set laws that very often had commissions or regulatory groups or boards that hired and fired and directed the desires and WORDS of CONGRESS and not POTUS. Over time- post RR - SCOTUS stripped congress of more and more and most recently more again power. As I see it with CHEVRON DEAD and MQD in - and with Unitary Imperial POTUS - now COURTS and the PRESIDENT in a TWO POWER structure rule.

Now we have a new Official Acts Immunity doctrine (after the CHEVRON doctrine is tossed). What do the two together mean for F and F and then ....

SO ----- very seriously - what Bush and Paulson did can not be challenged ---- they were official acts and are chiseled in granite as correct ---- that is the bad news Why bother suing?

SO ---- (and not sure how one writes to as Congress as it is gone) --- if there ever was doubt that Biden could with one action correct things - now he can and an official act is not wrong. A riff on Nixon - "If the President does it - it is right" . So why all this talk of rules and laws and Acts in your excellent post. What meaning does it have ANYMORE? And the courts can do stuff with or without POTUS --- screw 4714f or whatever -- CHEVRON is dead. So the path is open to freedom by courts or POTUS ----- with no reference to law - IMO

We need more volume. I will now go outside and sound the whale horn multiple times. Should work. It is a new horn I got from Amazon.

way beyond me -- but the half I read and understood is strong IMO

Agree. But in our case the plaintiffs were repeatedly told by the courts that only FHFA could bring suits against itself during conservatorship. Tolling would begin when SCOTUS ruled on Collins and said that every US Citizen can file suits against the government.

So for us every quarterly sweep of profits and ratchet of the LP means lawsuits can still be drafted even though the action putting it in place was a long time ago.

I'm not sure it means when you "realize" as in a person just discovered something. I think it means that the harm is realized or comes to fruition. For example, a law is on the books for decades (eh hem... Charter Act), and at some point a Federal Agency (not Congress) decides to take an unusual interpretation of that law to implement or change a policy that affects a business or person. The 6 years would start from the point of that Agency action/interpretation/enforcement, not the date the original law went into effect. This is necessary when you have Federal Agencies that get whiplash from replacing their leadership for political bias and intentional misreading of the statutes to fit the political agenda.

separate from CHEVERON

death of CHEVRON --- is birth of a singular unitary court

Potus is King and Courts and = and congress in this construct is dead and over with

it is likely I did not read the first - and maybe second report

I did skim the BO and DJT report on "this" and found the answers solutions in BOTH --- BO and DJT to be multiple and across the board - to include what others might call 11 or 7 or wind down

Both seemed to want F and F SMALLER to allow more competition

And neither POTUS did shit

You'll be waiting a lot longer still.

If tha is a reference to where you think PPS will be after he eventually (if ever)_ certifies the verdict, you're only off by about $98.50 per share.

Yellow sticky please.

kthomp19,

Do NOT believe the JPS rank below the Seniors. A simple reading as well as the 'descriptive headers' make it appear that way, but Mnuchin looks to have a provision to make the Seniors & LP convertible which just might make the JPS the 'top' of the capital structure according to the CBO. Let's see if this in fact happens!

DeMarco was not wrong. There is no "abusive conservator".

With the no Chevron deference, the hedge funds want to bury the CFR 1237.12 that has already been covered up by their representatives in the U.S. courts (the plaintiffs), and enacted by the former FHFA Acting Director on his Time Limitation-day (July 20, 2011), to continue ((c) it supplements) the plan of deception with the capital distributions: "The Common Equity is gone!".

This way, as of that day, a capital distribution is authorized if (Exemption 1) it "enhances the ability to meet the Risk-Based Capital level and the Minimum Capital level of the enterprises", now seen in the ERCF. The exemptions 2, 3 and 4 are more of the same, because the whole thing "supplements" the restriction by statute, U.S. Code 4614(e), meant for the Recap too, even if the SPS are repaid (its exemption) at the same time, because the SPS are repaid with cash, whereas the Capital remains recorded on Equity (double-entry accounting).

That is, deplete capital in FnF (capital exits the Balance Sheet) if it recapitalizes FnF, which obviously refers to a Recap now outside their Balance Sheets (External Positions seen in the ECB's Payment Systems).

DeMarco understood that the capital distributions are restricted and it's been upheld during the entire conservatorshp:

-Capital sent to the UST. External Position or Separate Account ($301B in dividends, both the 10% and the NWS dividends), which repaid the SPS at the same time, estimated fully repaid at the end of 2014 in Fannie Mae and one year earlier in Freddie Mac (signature image below).

-Capital held in escrow ($132B through the offset -reduction of Retained Earnings account- attached to the $132B SPS LP increased for free since December 2017, both items absent from the Balance Sheets. Financial Statement fraud).

It's not that DeMarco went crazy and approved the NWS dividend ("unchecked decisions"), as you want us to believe under the orders of the hedge funds.

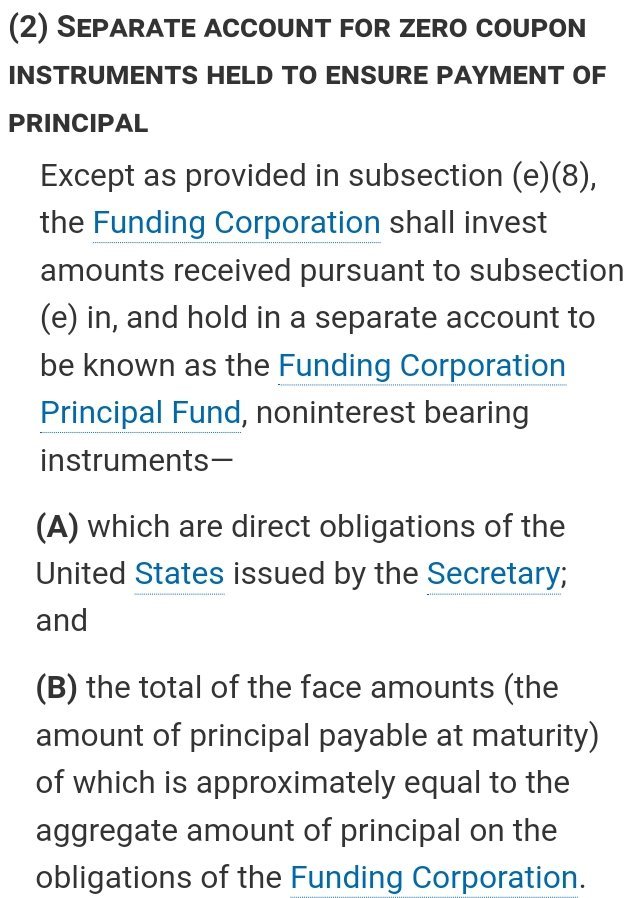

All the decisions were checked and well checked. The NWS dividend avoided the losses prompted by the 10% dividend (called death spiral), so that no capital is sent to the UST if FnF post losses (or the case when it's the very dividend the one that prompts the losses), the same premise seen in the 1989 bailout of the FHLBanks that was used as a template for FnF with the assessments sent to a "SEPARATE ACCOUNT TO ENSURE PAYMENT OF PRINCIPAL".

You are repeating the harassment to DeMarco that began in the Lamberth trials.

Anyone could have spotted the restriction, all the exceptions and an Incidental Power that allows the conservator to implement those actions ("authorized by this section") in a way that is in the best interests of the FHFA. A decision-making for the Privatized Housing Finance System endgame, with its desire to get rid of the AT1 Capital instruments (JPS) held mostly by hedge funds and Community Banks.

With this plan of deception, it also aims to get rid of the common shareholders, perplexed with the con operation in court with the collusion between the parties, that simply abandon the ship as we see in the annual data of number of shareholders of record in their Earnings reports.

Notice that, with the "FHLB membership cleansing" of 2016, the FHFA wanted to get rid of the hedge funds too, that used "captive insurers" with the objective to have access to the low cost borrowing from the FHLB System.

By the way, this 2016 Final Rule, not only gave the FHLB 5 years to "wind down their affairs with them", but also this rule was first proposed in 2010, which shows that the FHFA has been delaying it until FnF had built enough capital (2022), thinking of the Coop Model that would include the FHLB, already seen in the 2011 bill HR 1859 and the FHFA's pilot programs with the States' and Municipalities' Housing Finance Agencies (HFAs), using "Freddie Mac HFA Advantage Mortgage" to bundle their mortgages because at the time, Freddie Mac was already operating in the Common Securitization Platform, and at the time of Mel Watt (mid 2018).

Therefore, we see how the Membership is very important for the FHFA in a new Housing Finance System, and the reason of this overtime in the Conservatorships: you can only get rid of the AT1 Capital if FnF hold CET1 > 2.5% of ATA beforehand. Then, the Tier 1 Capital > 2.5% of ATA in the ERCF would be met.

T1 = CET1 + AT1.

This is harsh for the battered Non-Cumulative dividend JPS holders (Regulatory Risk: capital requirement from 0.45% to 2.5% of MBS), as it's been one year and a half without the resumption of dividend in the Fannie Mae JPS and one year more in the Freddie Mac JPS, under this Separate Account plan, but lawful (Conservator Risk), which is all that matters.

You mention Chevron with the same objective as others with other slogans.

As I replied yesterday to Bradford:

Quit repeating the PR campaigns from Bill Ackman and Pagliara, the peddlers of the Government theft story, who stick to

This is now 100% a Trump trade.

Still waiting for Lamberth's certification of the 8-0 verdict.

I want to sell 1000 shares at 100 dollars: any takers?

"i am always reminded 'nothing good lasts forever and nothing bad lasts forever'"

Death is bad and it's rather permanent, I am told!

Everyday investment analysts are wrong; doctors are wrong; politicians are wrong; scientists are wrong, and on and on, ad infinitum and, in this case (if Chevron will affect us) lawyers will be wrong. Often the case these various professionals are wrong is because they are supporting a man-made narrative in violation of either natural laws or long-standing laws or principles in the Constitution or established law. FHFA is a dictatorial, self-dealing, unelected, bureaucratic agency making unchecked decisions - the VERY REASON Chevron was overturned. This decision WILL impact us when the right case, set of principles, or the correct inappropriate activities of this c'ship are challenged OR, when the government moves to finalize the thievery.

Unless the legal system is entirely corrupt some enterprising law firm or deep pocket interested party will hold somebody's nose to this pile of dogshit known as the conservatorship. Under the guise of a conservatorship they created a financial commitment that cannot be repaid, created their own class of shares superceding all other classes, self-dealt between two government agencies, amended the so-called "agreements" numerous times to suit the needs of the agencies to the detriment of the very companies assets they were supposed to conserve, swiped the entire net worth of these companies - which continues to this day through the increase in the liquidation preference, and unconsitutionally prevented the companies from lobbying on their own behalf - just to name a few of the very things this conservative court has shown it WILL NO LONGER STAND FOR.

In spirit, this faux-conservatorship has made a mockery of contract law, shareholder rights, long-standing financial securities principles, the takings clause, and on and on and on. You cannot write one new law to circumvent every other principle the rights and laws of this country stands for. The Lamberth 8-0 shutout and this ruling - in recognition of the unchecked power of government agencies WILL eventually play a role in putting an end to the thievery. The courts have NOT given these agencies carte blanche with their previous decisions with regard to a final taking of all the companies assets, all shareholder rights and value in perpetuity. The end will come in one of two forms: 1. the government makes their final move to end the c'ships all thievery in tow, OR 2. new lawsuits pick up on the right track attacking the appropriate principles violated as outline above - in that case they will bank on the courts new found spine in overturning this Chevron nonsense that has held for too long!

Sad ending today up 3 cents. Hopefully tomorrow pops the top off.

Thanks Rodney, the snippet that I heard today on talk radio explained that the Supreme Court ruled in favor of a company that didn't even exist at the time that the "Regulation" was instituted. Said company, went into business and determined that this existing "regulation" was detrimental and filed a lawsuit. Initially the court ruled that the company didn't have standing because it was beyond the 6 years since the inception of the regulation. However, the Supreme Court "Amy Coney Barret" writes that the 6 years doesn't start until the harm is realized. So, if an individual/company invests in FNMA/FMCC tomorrow and next week they realize that the Governments tactics, self-dealing agreements, regulations, acts, etc. are harmful, couldn't they file suit? Maybe a new legal team can correct the errors that you believe were made.

EnoughAlready! I would think the next question after reading the two other post in this thread would be… Well, what part of the law did FHFA / Treasury violate ? I’m glad you asked.

Published October 9, 2023

FINANCIAL SERVICES

Committee

Committee Members

118th CONGRESS

The purpose of this letter is to bring attention to the Committee violations by the Federal Housing Finance Agency (FHFA) violating of the Charter Act, and the Federal Housing Enterprises Financial Safety and Soundness act of 1992 (FHEFSSA); Both as amended by the HOUSING AND ECONOMIC RECOVERY ACT OF 2008, (HERA). The Charter Acts are Fannie Mae and Freddie Mac's enabling statutes. FHEFSSA and HERA are regulatory statutes, governing the companies' regulators. All are laws passed by Congress.

The conservatorship of Fannie Mae and Freddie Mac has continued for over 15 years. I am not sure if Committee Members understand the history of the takeover of the companies and pray the Committee will of your clemency hear me in a few words.

Before the take down of the companies Treasury Secretary Paulson was unaware that the FHFA Regulator had sent both Fannie Mae and Freddie Mac letters saying the companies were safe and sound and exceeded their regulatory capital requirements. Paulson told FHFA Director Lockhart that he had to change his agency’s posture on the two companies, and FHFA did exactly that. FHFA sent each company an extremely harsh mid-year review letter, and two days later, Paulson, Lockhart and Fed chairman Bernanke met with the companies’ CEO's and directors to tell them they had no choice but to agree to conservatorship.

When Paulson met with the directors of Fannie Mae and Freddie Mac to inform them of his intent to take over their companies, neither entity met any of the twelve conditions for conservatorship spelled out in the newly passed HERA legislation. Paulson since has admitted he took the companies over by threat.

HOUSING AND ECONOMIC RECOVERY ACT OF 2008 Page 2734 Twelve Conditions

APPOINTMENT OF THE AGENCY AS CONSERVATOR OR RECEIVER

Link: https://www.congress.gov/110/plaws/publ289/PLAW-110publ289.pdf

The FHFA freely admitted the companies were adequately capitalized.

SECOND QUARTER CAPITAL RESULTS

Minimum Capital

Fannie Mae’s FHFA-directed capital requirement on June 30, 2008 was $37.5 billion and its statutory minimum capital requirement was $32.6 billion. Fannie Mae’s core capital of $47.0 billion exceeded the FHFA-directed capital requirement by $9.4 billion.

Freddie Mac’s FHFA-directed capital requirement on June 30, 2008 was $34.5 billion and its statutory minimum capital requirement was $28.7 billion. Freddie Mac’s core capital of $37.1 billion exceeded the FHFA-directed minimum capital requirement by $2.7 billion.

Link: https://www.fhfa.gov/Media/PublicAffairs/Pages/FHFA-Announces-Suspension-of-Capital-Classifications-During-Conservatorship-and-Discloses-Minimum-and-RiskBased-Cap.aspx#:~:text=During%20the%20conservatorship%2C%20FHFA%20will%20not%20issue%20a,submit%20capital%20reports%20to%20FHFA%20during%20the%20conservatorship.

The FHFA forced Fannie Mae and Freddie Mac into a contract with the United States Treasury by Senior Preferred Stock. The Senior Preferred Stock Purchase Agreement is not a law: The SPSPA is an illegal contract between Treasury and FHFA as conservator of the two companies. The Charter Act, FHEFSSA and HERA passed by Congress is the supreme law of the land that governs the two companies.

Fannie Mae and Freddie Mac's regulatory guidelines would have prohibited the companies form paying dividends to the Treasury while severely under-capitalized, but the FHFA suspended those guidelines because the regulator wanted the companies to have to draw more senior preferred stock from the Treasury to pay the annual dividends in cash, ballooning their outstanding senior preferred stock and increase their required annual dividends. FHFA and its Director are executive branch entities and can not make changes to federal laws. Only Congress can change the law. Neither the Charter Act nor did HERA authorize the Treasury to charge a commitment fee.

When Fannie Mae and Freddie Mac were taken over by the FHFA no emergency existed and the FHFA had no authority granted by Congress to take over the companies, no authority written in the Charter Act that gave the FHFA right to take down the companies.

Charter Act: SUBSECTION (g) TEMPORARY AUTHORITY OF TREASURY TO PURCHASE OBLIGATIONS AND SECURITIES; CONDITIONS.— EMERGENCY DETERMINATION REQUIRED. Page 16

Under this subsection no emergency existed.

This leads to the question, who authorized the appropriation of taxpayer debt to provide the 200 billion commitment? Certainly not Congress. Treasury took it upon themselves and authorized a 200 billion commitment available in exchange for One Million Shares (1,000,000) with an initial liquidation preference of $1,000 per share. Shares of senior equity illegal and unconstitutional.

Page 5

Link: https://www.fhfa.gov/Conservatorship/Documents/Senior-Preferred-Stock-Agree/FNM/SPSPA-amends/FNM-SPSPA_09-07-2008.pdf

Charter act prohibits the commitment fees (Seniors, warrants, variable liquidation preference). More importantly the actions of Treasury to appropriate 200 billion in taxpayer debt, take non regulatory control of the companies through the SPSPA (require Treasury permission at least 10 separate times) and ownership of more than 50% of the companies requires them under the GAO act and the CFO act to consolidate the GSEs onto the nations balance sheet. The fact that that hasn't happened means the Treasury has violated the 14th amendment to the Constitution by repudiating the 5 trillion plus in debt the Treasury has acquired through their actions since 2008. Their actions have resulted in a takings of the entire enterprise value of the formerly private companies. These actions have necessarily turned the GSEs back into agencies of the executive branch as they were originally created. This is the definition of a major question and also a separation of powers problem since Congress did not authorize the actions Treasury took and continues to take.

In addition 'Deferred Tax Assets' the Treasury forced the companies to write down and record these non-cash expenses making the companies appear bankrupted. Fannie Mae and Freddie Mac were no where near bankrupted.

Mr. Howard wrote below,

Quote: “Between the time Fannie and Freddie were put into conservatorship and the end of 2011, well over $300 billion in non-cash accounting expenses were recorded on their income statements. These non-cash expenses, most of which were discretionary, eliminated all of the Companies’ capital and forced them, together, to take $187 billion from Treasury. But because accelerated or exaggerated expenses cause losses that are only temporary, Fannie’s and Freddie’s non-cash losses began to reverse themselves in 2012. Coupled with profits resulting from a rebounding housing market, the reversal of these losses enabled both Companies to report in August 2012 sufficient second quarter income to not only pay their dividends to Treasury but also retain a total of $3.9 billion in capital. As soon as it became apparent that a large percentage of the non-cash accounting losses booked during the previous four years was about to come back into income, Treasury and FHFA entered into the Third Amendment to the PSPA. The Third Amendment substituted for the fixed dividend payment a requirement that all future earnings—including reversals of accounting-related expenses incurred earlier—be remitted to Treasury. From the time the Third Amendment took effect through the end of 2014, Fannie and Freddie paid Treasury $170 billion, $133 billion more than they would have owed absent the Amendment.” End of Quote

The United States was not obligated after 1968 to back debt of Fannie Mae. The United States Taxpayers became obligated when the government took over the two companies.

Originally, Fannie Mae had an explicit guarantee from the United States government; if the entity got into financial trouble the government promised to bail it out. This changed in 1968. Fannie Mae became a private stockholder owned company. Fannie Mae securities received no actual explicit or implicit government guarantee. This is clearly stated in the securities themselves, and in many public communications issued by Fannie Mae.

Quote: “Although we are a corporation chartered by the U.S. Congress, the U.S. Government does not guarantee, directly or indirectly, our securities or other obligations. We are a stockholder-owned corporation, and our business is self-sustaining and funded exclusively with private capital. Our common stock is listed on the New York Stock Exchange and traded under the symbol “FNM.” Our debt securities are actively traded in the over-the-counter market.” End of Quote.

Information from: Fannie Mae form 10K Dec 31, 2007

part I, page 1, item 1.

https://www.fanniemae.com/sites/g/files/koqyhd191/files/migrated-files/resources/file/ir/pdf/quarterly-annual-results/2007/form10k_022708.pdf

Where is "maximize profits for taxpayers" written in the Charter Act? Specifically, in this provision entitled Fee Limitation of the United States:

Neither the Charter Act nor did HERA authorize the Treasury to charge a commitment fee on a line of credit to be paid by the Enterprise. The United States prohibition on assessment or collection of fee or charge to Fannie Mae, (section 304 Fee Limitation). Only Federal Reserve Banks are authorized to be reimbursed of fees, (section 309).

SEC. 304. SECONDARY MARKET OPERATION

Fee Limitation

Quote: “(f) PROHIBITION ON ASSESSMENT OR COLLECTION OF FEE OR CHARGE BY UNITED STATES.—Except for fees paid pursuant to section 309(g) of this Act and assessments pursuant to section 1316 of the Federal Housing Enterprises Financial Safety and Soundness Act of 1992, no fee or charge may be assessed or collected by the United States (including any executive department, agency, or independent establishment of the United States) on or with regard to the purchase, acquisition, sale, pledge, issuance, guarantee, or redemption of any mortgage, asset, obligation, trust certificate of beneficial interest, or other security by the corporation. No provision of this subsection shall affect the purchase of any obligation by the Secretary of the Treasury pursuant to subsection (c) of this section.” End of Quote. Page 16

Only Federal Reserve Banks are authorized to be reimbursed of fees, (section 309).

SEC. 309. GENERAL POWERS OF GOVERNMENT NATIONAL MORTGAGE ASSOCIATION AND FEDERAL NATIONAL MORTGAGE ASSOCIATION

Federal Reserve Banks to Act as Fiscal Agents (Fannie Mae and GNMA)

Quote: “(g) DEPOSITARIES, CUSTODIANS, AND FISCAL AGENTS.—The Federal Reserve banks are authorized and directed to act as depositaries, custodians, and fiscal agents for each of the bodies corporate named in section 302(a)(2), for its own account or as fiduciary, and such banks shall be reimbursed for such services in such manner as may be agreed upon; and each of such bodies corporate may itself act in such capacities, for its own account or as fiduciary, and for the account of others.” End of Quote. Page 29

Link:

FEDERAL NATIONAL MORTGAGE ASSOCIATION CHARTER ACT

As amended through July 25, 2019

link: https://www.fanniemae.com/sites/g/files/koqyhd191/files/migrated-files/resources/file/aboutus/pdf/fm-amended-charter.pdf

The Senior Preferred Stock, with a variable liquidation preference outlined in the SPSPA and its amendments and share certificates is a new product for the purposes of the Safety and Soundness Act of 1992 as amended by HERA.

Congress directed the Director of FHFA to apply the Administrative Procedures Act to the new products sold to Treasury. The FHFA did not follow the administrative procedures congress required in the plain language of the safety and soundness act.

The Director of FHFA as regulator violated the safety and soundness act and the administrative procedures act by not following the statutory duty to approve new products issued by the GSEs to Treasury for the purpose of stabilizing the secondary mortgage market.

The law required the publication in the federal register of the SPS with their variable rate liquidation preference tied to the commitment. It requires a public comment period, and a rule making process to make the SPS legal. It is the same law that required the capital rule. And the same law that required FHFA a year ago issue the new products law for MBS products. They have ignored this requirement for 15 years.

Director Lockhart Regulator, and Director Lockhart Conservator. Holding both positions as Regulator and Conservator; Conservator Lockhart is required by law to file notice to himself as Regulator.

The Safety and Soundness Act required Director Lockhart as regulator not conservator to approve a new product issued by Director Lockhart acting as conservator FHFA-C (SPS with variable liquidation Preference) to Treasury under the terms of the SPSPA for the purpose of carrying out the secondary mortgage market. He was required as regulator to file notice in the federal register, seek public comment and issue federal regulations for the new product we call the Senior Preferred shares sold to Treasury.

HOUSING AND ECONOMIC RECOVERY ACT OF 2008

Page 2689

SEC. 1321. PRIOR APPROVAL AUTHORITY FOR PRODUCTS.

Link: https://www.congress.gov/110/plaws/publ289/PLAW-110publ289.pdf

The CFO act requires the Treasury department based on published accounting standards to determine if their actions of funding through appropriations, ownership of 100% of the GSEs net worth and non-regulatory control of the GSEs through the SPSPA require the consolidation of the GSEs liabilities onto the nations balance sheet. Do the actions of Treasury under the SPSPA require such consolidation under the plain language of the Chief Financial Officers Act?

The Congressional Budget Office publication states, “Federal Government effective ownership of Fannie Mae and Freddie Mac.”

The Enterprises have been Nationalized by the Government according to the CBO: The liabilities have not been added to the National Debt nor have the Shareholders been compensated by U.S. Law of the 5th Amendment.

Congressional Budget Office

From: Estimates of the Cost of Federal Credit Programs in 2023

Page 1, Foot Note 1.

Quote: “Fannie Mae and Freddie Mac have been in federal conservatorship since September 2008. CBO treats the two GSEs as government entities in its budget estimates because, under the terms of the conservatorships, the federal government retains operational control and effective ownership of Fannie Mae and Freddie Mac. For more discussion, see Congressional Budget Office, Effects of Recapitalizing Fannie Mae and Freddie Mac Through Administrative Actions (August 2020), www.cbo.gov/publication/56496; and Congressional Budget Office, The Effects of Increasing Fannie Mae’s and Freddie Mac’s Capital (October 2016), www.cbo.gov/ publication/52089” End of Quote

Link: https://www.cbo.gov/system/files/2022-06/58031-Federal-Credit-Programs.pdf

The United States Treasury in violation of the Charter Act has failed to treat as public debt the transactions of the United States when the FHFA placed Fannie Mae and Freddie Mac into conservatorship. This obligation was never recorded as public debt as required by law.

The Charter Act the Law of the Land.

Charter Act SEC. 304. SECONDARY MARKET OPERATIONS

(c) Terms and Rates

Quote: “All redemptions, purchases, and sales by the Secretary of the Treasury of such obligations under this subsection SHALL BE TREATED AS PUBLIC DEBT TRANSACTIONS of the United States.” End of Quote Page 14

Link: https://www.fanniemae.com/sites/g/files/koqyhd191/files/migrated-files/resources/file/aboutus/pdf/fm-amended-charter.pdf

IF THE FHFA / TREASURY are allowed to continue with the violations discussed in the above writing, and the illegal contract of the SPSPA agreement is allowed to stand the Committee should give consideration to the FHFA Breach of Contract Bad faith and Unfair Dealings actions of the government in litigation that took place in Judge Lamberth's Court. It took 8 random DC Jurors only 10 hours of deliberations to see right through the Government's false narratives.

It’s bad faith and unfair dealing when the Regulator is authorized to pay down the Senior Preferred Stock and sent the Net Worth without the pay down option. The FHFA Director doesn’t need the Treasury approval to pay down the Senior Preferred Stock the Director has the authority from Congress written in HERA:

HOUSING AND ECONOMIC RECOVERY ACT OF 2008

RESTRICTION ON CAPITAL DISTRIBUTIONS.— page 2731

‘‘(1) IN GENERAL.—A regulated entity shall make no capital distribution if, after making the distribution, the regulated entity would be undercapitalized. The exception.

Quote: “Page 2732

EXCEPTION.—Notwithstanding paragraph (1), the Director may permit a regulated entity, to the extent appropriate or applicable, to repurchase, redeem, retire, or otherwise acquire shares or ownership interests if the repurchase, redemption, retirement, or other acquisition— ‘‘(A) is made in connection with the issuance of additional shares or obligations of the regulated entity in at least an equivalent amount; and ‘‘(B) will reduce the financial obligations of the regulated entity or otherwise improve the financial condition of the entity.’’.

NOTE: REPURCHASE, REDEEM, RETIRE...

WILL REDUCE THE FINANCIAL OBLIGATIONS OF THE REGULATED ENTITY.

Link: https://www.congress.gov/110/plaws/publ289/PLAW-110publ289.pdf

In essence allows the trustees of Fannie and Freddie to go to the market at any time to raise new capital, including new capital with lower dividend coupons, to buy back the Treasury’s senior preferred. Any loyal conservator of Fannie and Freddie would take advantage of this refinancing option to end the bailout arrangement, by paying off the senior preferred in full. The Treasury did not take a Perpetual Equity Investment in the enterprises, the Treasury stated a temporary investment period!

The calculation of the pay down of the liquidation preference of the Senior Preferred Stock, I am asking this committee to apply the law written in the HERA legislation passed by Congress.

https://drive.google.com/file/d/15978NWfDcTtuClMBnwgWFmoPnwK94vWn/view

The liquidation preference has been paid and the Senior Preferred Stock should be canceled.

The law actually exists! FHFA and its Director are executive branch entities. They can not make changes to federal laws. Only Congress can change the law.

Therefore, the U.S. Congress did not give DeMarco the power to take all the future profits of their wards in conservatorship into perpetuity, thus Nationalizing the GSES, based on an Incidental Power in HERA: The Net Worth Sweep.

The U.S. Congress would have given the FHFA more explicit instructions to do so than merely drafting in the HERA to do whatever it feels is in its best interests. DeMarco, this non-elected bureaucrat, has been allowed to steal the companies for the Treasury.

The SCOTUS upholding the NWS does not change the fact the liquidation preference can be paid down and the Senior Preferred Stock redeemed under the terms of the law of HERA. The money kept by the Treasury by the NWS should be applied to principle and 10% interest and over payment should be returned to the companies. $301 billion is more than enough to pay the liquidation preference and redeem the Senior Preferred Stock.

I do not know the particulars of your cases

I can see the TIME advantage of cash --- v waiting for a loan to happen

Other than that --- I have no explanation - as your check is cash as is theirs --- but theirs is sooner and I guess 100% v 98%

(or maybe- you correctly require an inspection -- that the sale is subject to an inspection ---- and MAYBE MAYBE you have lost to those who do not make such demand. IF IF IF that is the case - I would encourage you to always make a purchase subject to inspection - you are right to do so and sellers should allow the time for it)

Summary - maybe you bit 500K in 30 days plus a subject to inspection and they bid --- 500K - in 3 days - and no inspection

AND --- interestingly - is some corporate entity is big and bigger and has that advantage - then our anti trust laws might just even the playing field

Good luck to you

Because elections have consequences in terms of driving federal policy which in this case is what will end the conservatorships. I think this continues. Fnmas new 52 week high

can you provide a more direct link?

Again, my understanding is any new lawsuit has to prove the FHFA / Treasury broke the law. The mistake of the current lawsuits the attorneys are going after the conservator! The lawyers failed to mention Federal Law. Treasury and FHFA violating Federal statutes. The Federal statutes are the Charter Act, the Safety and Soundness Act of 1992, as amended by HERA, Administrative Procedures Act, and potentially the Chief Financial Officers Act. None of the current litigation makes any claims of violation of these acts. They all challenge the actions of the Conservator and attempted to squeeze the APA and the 5th amendment takings into the Actions of the FHFA-C within the terms of the SPSPA. all have failed to this point.

The SPSPA is a contract between two government agencies which Fannie and Freddie had no say so. The only legal contract is the one with the U.S. Congress, called the Charter Act.

Charter Act, and the Federal Housing Enterprises Financial Safety and Soundness act of 1992 (FHEFSSA); Both as amended by the HOUSING AND ECONOMIC RECOVERY ACT OF 2008, (HERA).

The Charter Acts are Fannie Mae and Freddie Mac's enabling statutes. FHEFSSA and HERA are regulatory statutes, governing the companies' regulators. All are laws passed by Congress.

SENIOR PREFERRED STOCK PURCHASE AGREEMENT (this “Agreement”) dated as of September 7, 2008, between the UNITED STATES DEPARTMENT OF THE TREASURY (“Purchaser”) and FEDERAL NATIONAL MORTGAGE ASSOCIATION (“Seller”), acting through the Federal Housing Finance Agency (the “Agency”) as its duly appointed conservator (the Agency in such capacity, “Conservator”). Page 1

Link: https://www.fhfa.gov/sites/default/files/2023-07/FNM-SPSPA_09-07-2008.pdf

PUBLIC LAW 110–289—JULY 30, 2008

HOUSING AND ECONOMIC RECOVERY ACT

HERA is public law not a contract, the Senior Preferred Stock Purchase Agreement is a contract not the law.

FHEFSSA

Federal Housing Enterprises Financial Safety and Soundness Act of 1992 was amended to establish the Federal Housing Finance Agency. HERA amended certain parts of both FHEFSSA and the Charter Act. AMENDED not to do away with. Safety and Soundness still exists just as the Charter Act still exists.

Page 9 Title I

Establishment of the Federal Housing Finance Agency

FHFA is now the Regulator by reason of HERA.

Links:

FEDERAL NATIONAL MORTGAGE ASSOCIATION CHARTER ACT

As amended through July 25, 2019

link: https://www.fanniemae.com/sites/g/files/koqyhd191/files/migrated-files/resources/file/aboutus/pdf/fm-amended-charter.pdf

HOUSING AND ECONOMIC RECOVERY ACT OF 2008

Link: https://www.congress.gov/110/plaws/publ289/PLAW-110publ289.pdf

SENIOR PREFERRED STOCK PURCHASE AGREEMENT

Dated September 7, 2008.

link: https://www.fhfa.gov/sites/default/files/2023-07/FNM-SPSPA_09-07-2008.pdf

ALL THE AGREEMENTS

link: https://www.fhfa.gov/Conservatorship/Pages/Senior-Preferred-Stock-Purchase-Agreements.aspx

Federal Housing Enterprises Financial Safety and Soundness Act of 1992

https://www.congress.gov/bill/102nd-congress/house-bill/6094/subjects?overview=closed

This is my understanding: Statute of limitations would rely on DOJ guidance for recurring claims due to material changes introduced in the letter agreements. For example, the new increase of liquidation preference for free introduced within the last 6-years. The FHFA / Treasury continue to change the contract, letter agreement dated January 14, 2021, So, the Statute of Limitations are not up. PAGE 6 Liquidation Preference increases dollar for dollar for all the retained earnings of the enterprises.

Link: https://home.treasury.gov/system/files/136/Executed-Letter-Agreement-for-Fannie-Mae.pdf

I heard that the Chevron Decision wouldn't necessarily impact our situation, but it seems that it does impact the time that an individual/company has to challenge a regulation. "The Supreme Court on Monday gave companies more time to challenge many regulations, ruling that a six-year statute of limitations for filing lawsuits begins to run when a regulation first affects a company rather than when it is first issued."

Can any of the individuals on the board who have claimed that all future lawsuits are precluded based on the previous statute of limitations care to weight in(?) I'm curious if this helps to level the playing field. Are more lawsuits now on the table? The lawyers get paid to litigate so they are thrilled but does this change the mindset of the decision makers?

Correct. Congress not needed to end the c-ship. Could be done over a cup of coffee.

The chances of that happening were never at or above zero. Nothing lost (except all of the days gains) nothing gained.

Because they’ll be paid first

You could just play for both teams.

Preferred shares are doing much better than us today. Any reason ?

Its going to be a long slow climb ... there are plenty of people in this trade that are completely fed up who will continue to take profits with every next step up until someone comes out with real news or support for release ...

Goodbye gains from this morning. It was nice to meet you.

Like clockwork some fool shows up to regurgitate some stupid comment!

Vegas odds for today for FNMA

place your bets for closing price today

Odds for $1.49 are a -1 million favorite

meaning you have to bet 1 million to make 1 dollar

sponsored by SW, our favorite MM bankster

LOL

|

Followers

|

2331

|

Posters

|

|

|

Posts (Today)

|

10

|

Posts (Total)

|

802496

|

|

Created

|

07/14/08

|

Type

|

Free

|

| Moderators not one red cent ~NORC~ stockprofitter Ace Trader EternalPatience jeddiemack FOFreddie | |||

Fannie Mae (the Federal National Mortgage Association, or FNMA) is a government-sponsored enterprise (GSE) in the U.S. that was established in 1938. Its main purpose is to provide liquidity, stability, and affordability to the U.S. housing market. It does this by purchasing mortgages from lenders (like banks), packaging them into mortgage-backed securities (MBS), and selling those securities to investors. This process ensures that lenders have more capital to issue new home loans, helping more Americans get access to homeownership.

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |