News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Ask the CEO:

To submit a question to the CEO, please send it to asktheCEO@edrsilver.com

http://edrsilver.com/investors/ask_ceo/

$248M total assets ($22M cash) vs. $63M total liabilities...

http://edrsilver.com/_resources/financials/Q3_2015_Financial_Statements.pdf

New November 2015 EXK Fact Sheet:

http://edrsilver.com/_resources/november_2015_factsheet.pdf

Gold/Silver falling during the past 2 weeks but... that could completely change coming into 2016...

Endeavour Silver Announces Revised Date for Release of Third Quarter, 2015 Financial Results; Provides Emergency Supplies to Small Towns Near San Sebastian del Oeste, Jalisco, Mexico to Assist in Recovery From Hurricane Patricia

more here

Greetings from Fred & EntendanceInvestors Beach!

EXK October 8, 2015

Endeavour Silver Produces 1,820,282 oz Silver and 15,319 oz Gold (2.9 Million oz Silver Equivalent) in the Third Quarter, 2015

VANCOUVER, BC--(Marketwired - October 08, 2015) - Endeavour Silver Corp. (TSX: EDR) (NYSE: EXK) announces that silver and gold production from the Company’s three operating silver mines in Mexico was on plan in the Third Quarter, 2015. Endeavour owns and operates the Guanaceví mine in Durango State and the Bolañitos and El Cubo mines in Guanajuato State.

Silver production in the Third Quarter, 2015 was slightly above guidance at 1,820,282 ounces (oz) and gold production was slightly below guidance at 15,319 oz. Silver equivalent production was on plan at 2.9 million oz using a 70:1 silver gold ratio. Silver, gold and silver equivalent production were each up quarter-on-quarter compared to Q2, 2015 and up year-on-year compared to Q3, 2014.

Production Highlights for Third Quarter, 2015 (Compared to Third Quarter, 2014)

•Silver production increased 11% to 1,820,282 oz

•Gold production increased 9% to 15,319 oz

•Silver equivalent production increased 10% to 2.9 million oz (at a 70:1 silver: gold ratio)

•Silver oz sold up 50% to 1,844,556 oz

•Gold oz sold up 7% to 14,599 oz

•Bullion inventory at quarter-end included 97,654 oz silver and 223 oz gold

•Concentrate inventory at quarter-end included 99,555 oz silver and 1,497 oz gold

More here

EXK

Endeavour Silver reports Q3 silver production was slightly above guidance at 1,820,282 ounces and gold production was slightly below guidance at 15,319 oz.

Silver equivalent production was on plan at 2.9 million oz using a 70:1 silver gold ratio.Lower than planned mill feed from the El Cubo mine allowed Bolaitos to mill just under 1,200 tpd of Bolaitos ore in Q3, 2015. Grades and recoveries were both lower in the third quarter but are expected to rise according to plan in Q4, 2015.

Greetings from EntndanceInvestors, EXK Long-Term Investors.

Endeavour Silver Drilling Extends Three Zones of High Grade, Gold-Silver Mineralization in Santa Cruz Vein, Guanaceví Mine, Durango State, Mexico

VANCOUVER, BC--(Marketwired - September 09, 2015) - Endeavour Silver Corp. (TSX: EDR) (NYSE: EXK) announces that drilling at the Guanaceví Mine in Durango State, Mexico has extended high grade, gold-silver mineralization within three zones in the Santa Cruz vein. The Shallow Porvenir, Deep Porvenir and Santa Cruz mineralized zones are each adjacent to historic mine workings, readily accessible for future mine development.

Recent drilling highlights are summarized in the table below and include 351 grams per tonne (gpt) silver and 0.41 gpt gold (379 gpt silver equivalent (AgEq)) over 4.6 metres (m) true width, or 11.0 ounces per ton (opT) AgEq over 15.1 feet (ft), including 2,960 gpt silver and 1.8 gpt gold (3,086 gpt AgEq) over 0.23 m true width, or 90.0 opT AgEq over 0.8 ft in hole UNP9-3.

More here

Silver equivalents are calculated at a ratio of 70:1 silver:gold.

Luis Castro, Vice President of Exploration, commented, “Each of the three new zones of mineralization are in areas of the Santa Cruz vein we thought had low potential due to some widely spaced, low grade holes drilled in previous years. These results show that high grade mineralization can be found in such areas, even adjacent to historic mine workings readily accessible for future mine development.”

Godfrey Walton, M.Sc., P.Geo., Endeavour’s President and COO, is the Qualified Person who reviewed and approved this news release and supervised the drilling programs in Mexico. A Quality Control sampling program of reference standards, blanks and duplicates has been instituted to monitor the integrity of all assay results. All samples are split at the local field office and shipped to ALS-Chemex Labs, where they are dried, crushed, split and 50 gram pulp samples are prepared for analysis. Gold and silver are determined by fire assay with an atomic absorption (AA) finish.

Greetings from E!

Pretty cheap but my favorite is CDE. Bought recently at $2.75

I absolutely love CDE at $2.75

I am still holding to my opinion that SILVER may touch $13's briefly, but will not spend anytime in the $13's

$14.00 is support and a great place to buy anything SILVER.

Buy, buy, buy CDE in the $2's

Usually you're pumping this one.

CDE over EXK. Or if you don't mind higher SP ... SLW is good.

Looky here... Run on Silver Developing As Demand EXPLODES!

Posted on August 28, 2015 by The Doc

http://www.silverdoctors.com/run-on-silver-developing-as-demand-explodes/

In the Wake of “Black Monday” and the Past Week’s Crash of Historic Proportions, Alasdair Macleod Joins the Show to Break Down All the Market Action and What’s Coming This Fall, Discussing:

- After a Brief Rally, Bear Market Likely to Resume With a Vengeance- the END GAME IS APPROACHING!

- Run On Silver Developing As Physical Demand Goes THROUGH THE ROOF

- Is the Bond Market About to Find Religion?

- Alasdair Explains Why the Next Crisis (Which He Believes is Likely to Begin in About a Month) Will Spread From A Banking Crisis to a CURRENCY CRISIS

- In the Words of Eric Dubin: Its Going to Get REALLY UGLY

- The SD Weekly Metals & Markets With The Doc, Eric Dubin, & Alasdair Macleod is Below:

Gold miners up across the board on crisis' in global financing

Endeavour Silver Drilling Intersects High Grade, Gold-Silver Mineralization in Three Historic Veins on Bolanitos Property, Guanajuato State, Mexico

VANCOUVER, BC--(Marketwired - August 17, 2015) - Endeavour Silver Corp. (TSX: EDR) (NYSE: EXK) announces that drilling on the Bolanitos property in Guanajuato State, Mexico has intersected high grade, gold-silver mineralization within three historic veins, San Ignacio-San Miguel, La Joya and Gabriela. Gabriela mineralization is adjacent to historic mine workings that are readily accessible for development.

Silver equivalents are calculated at a ratio of 70:1 silver:gold.

Luis Castro, Vice President of Exploration, commented, "We are encouraged that our exploration drilling continues to find new zones of high grade mineralization at relatively shallow depths within historic veins on the Bolanitos property. The Gabriela mineralization sits adjacent to historic mine workings that should provide easy access for future mining if a large enough block of mineral can be outlined."

Godfrey Walton, M.Sc., P.Geo., Endeavour's President and COO, is the Qualified Person who reviewed and approved this news release and supervised the drilling programs in Mexico. A Quality Control sampling program of reference standards, blanks and duplicates has been instituted to monitor the integrity of all assay results. All samples are split at the local field office and shipped to ALS-Chemex Labs, where they are dried, crushed, split and 50 gram pulp samples are prepared for analysis. Gold and silver are determined by fire assay with an atomic absorption (AA) finish.

I hope you already have joined us at our beach and thus you read the 2 new EXK articles.

Greetings from E.

Nows the time to start buying

Endeavour Silver (NYSE:EXK): Q2 EPS of -$0.01 beats by $0.03.

Revenue of $47.72M (-12.9% Y/Y)

Endeavour Silver Reports Financial Results for Second Quarter, 2015; LOC Debt Reduced by $4 Million, Cash Holdings Increased by $5.5 Million; Conference Call at 10am PDT (1pm EDT) on August 6, 2015

VANCOUVER, BC--(Marketwired - August 06, 2015)

- Endeavour Silver Corp. (NYSE: EXK) (TSX: EDR) released today its financial results for the second quarter ended June 30, 2015. Endeavour owns and operates three underground silver-gold mines in Mexico: the Guanaceví mine in Durango state, and the Bolañitos and El Cubo mines in Guanajuato state.

The Company's financial performance in the Second Quarter, 2015 was lower compared to both the First Quarter, 2015 and the Second Quarter, 2014 as a result of lower precious metal prices and lower gold production. Operating costs were slightly higher quarter-on-quarter compared to the First Quarter, 2015 but substantially lower year-on-year compared to the Second Quarter, 2014.

Highlights of Second Quarter 2015 (Compared to Second Quarter 2014)

Financial

•Net loss of $1.0 million(1) ($0.01 per share) compared to $0.3 million ($0.00 per share)

•EBITDA(2) decreased 19% to $10.9 million

•Cash flow from operations before working capital changes decreased 8% to $11.0 million

•Mine operating cash flow before taxes(1) decreased 17% to $16.4 million

•Revenue decreased 13% to $47.7 million

•Realized silver price decreased 19% to $16.34 per ounce (oz) sold

•Realized gold price decreased 9% to $1,191 per oz sold

•Cash costs(2) decreased 13% to $8.60 per oz silver payable (net of gold credits)

•All-in sustaining (AIS) costs decreased 18% to $16.86 per oz silver payable (net of gold credits)

•On track to beat cash cost and AIS cost guidance for 2015

•Working capital of $26.7 million after using free cash flow to reduce LOC debt by $4 million to $25 million and increase cash holdings by $5.5 million to $31.8 million

Operations

•Silver production increased 8% to 1,805,569 oz, 35,828 oz more than previously reported

•Gold production decreased 11% to 13,430 oz, 383 oz more than previously reported

•Silver equivalent production increased 1% to 2.7 million oz (at a 70:1 silver:gold ratio)

•On track to meet high end of silver production and low end of gold production guidance for 2015

•Bullion inventory at quarter-end included 187,954 oz silver and 399 oz gold

•Concentrate inventory at quarter-end included 76,099 oz silver and 926 oz gold

•El Cubo mine expansion to 2,200 tpd completed on time and budget by the end of Q2, 2015

•El Cubo production below plan at mid-year but expected to meet guidance by year-end

•Guanaceví production above plan at mid-year and expected to beat guidance

•Bolañitos production on plan at mid-year and expected to meet guidance

•Terronera positive PEA published in May, PFS postponed until January 2016

•El Cubo wins first place, Bolañitos wins second place in first aid and benchman mine rescue competitions out of 14 teams; El Cubo and Guanaceví move on to Mexican national competition

1.The Consolidated Interim Financial Statements and Management's Discussion & Analysis can be viewed on the Company's website at www.edrsilver.com, on SEDAR at www.sedar.com and EDGAR at www.sec.gov. All amounts are reported in US$.

2.Mine operating cash flow, EBITDA, cash costs and all-in sustaining costs are non-IFRS measures. Please refer to the definitions in the Company's Management Discussion & Analysis.

Endeavour CEO Bradford Cooke commented, "Our strong operational and financial performance in the Second Quarter, notwithstanding lower metal prices, allowed us to add $9.5 million in net cash to the balance sheet. We are also on track to meet our production guidance and beat cash cost and AIS cost guidance for 2015.

"Congratulations once again to our El Cubo management and workforce for delivering the 50% El Cubo mine expansion to 2,200 tpd in Q2, 2015 on time and budget! Q3, 2015 should see a decline in operating costs now that the mine expansion is complete. I would also like to recognize the stellar performances of all three of our mine rescue teams in the recent regional competitions in Mexico.

"We released a robust preliminary economic assessment in May for our new, high-grade Terronera mine project in Jalisco state. But with the metal prices still falling in July, management felt it prudent to slow our growth spending at Terronera so the pre-feasibility study has been postponed until January 2016."

Operating Results

Conference Call

A conference call to discuss the results will be held on Thursday, August 6 at 10am PDT (1pm EDT). To participate in the conference call, please dial the following:

Toll-free in Canada and the US: 1-800-319-4610 FREE

Local Vancouver: 604-638-5340

Outside of Canada and the US: 1-604-638-5340

No pass-code is necessary to participate in the conference call.

A replay of the conference call will be available by dialing 1-800-319-6413 FREE in Canada and the US (toll-free) or 1-604-638-9010 outside of Canada and the US. The required pass-code is 4890 followed by the # sign. The audio replay and a written transcript will also be made available on the Company's website at www.edrsilver.com

Greetings from Entendance!

Well...

Have a look

here

and draw your own conclusions...

E.

I have a small position but looking to accumulate. EXK has great properties and good management. I added at 1.44 but I am getting beaten up overall. Question is....when will metals and metal miners turn around? It is hard to imagine prices falling much further. If the FED raises rates (and i don't think they can) i just don't know how miners stock will react.....wont be a good thing. Any thoughts as I am taking a wait and see position.

EXK Summary

•EXK remains profitable even in a weak silver market.

•This year’s Q2 production implies EXK will have a great 2015.

•EXK’s previously unprofitable mine is now looking profitable.

•EXK should be reporting strong earnings but might be purposefully underestimating their projected revenue.

•EXK is the safest silver investment at the moment...

Endeavour Silver Corp. - Successful While Silver Is Low Implies Long-Term Prospects

Greetings from Fred & EntendanceInvestors Beach!

Hard Asset Investments: ...Endeavor looks like it is doing everything it can here to increase production and lower its cash costs. This is what the company can control. It can't control silver prices...

Endeavor Silver Reports Decent Q2 Production Numbers And Shares Look Oversold Here

Greetings from EntendanceInvestors!

Sooner or later EXK will stop falling. We are at $14/15 SILVER.

I think we can all go heavy on everything silver here ...

SLW

EXK

USLV

PAAS

FMS

SSRI

IMO

silver manipulation:

Silver Thursday: How Two Wealthy Traders Cornered The Market

http://www.investopedia.com/articles/optioninvestor/09/silver-thursday-hunt-brothers.asp

EXK gets no love ...

The Investment Doctor: "... the Mexican Peso depreciated really fast at the end of 2014 resulting in an average USD/MXN exchange rate of around 15 in the first quarter of this year. The Mexican Peso continued to weaken in the second quarter and it looks like the average USD/MXN exchange rate will be 2-3% more advantageous to Endeavour Silver compared to the first quarter.

This will obviously have a positive impact on the company's financials as a weaker Peso should increase the company's operating margins. It's definitely something to keep an eye on, and I will be looking forward to the next quarterly update to hear if Endeavour Silver has any plans at all to start hedging its currency.

Investment thesis

Despite the lower silver-equivalent production rate, Endeavour Silver seems to be performing better than I expected at the beginning of this year. The lower production rate was mainly due to a lower gold production as the production of pure silver actually increased.

I'm impressed by the production rate at the Guanacevi mine, as the mine already produced 57% of its expected full year production in just six months time. The discovery of the new high-grade zone is very positive and I hope this will contribute to increasing the reserve-based mine life at Guanacevi."

Greetings from Fred & EntendanceInvestors Beach!

Fred & EntendanceInvestors Beach advice to buyers of physical precious metals is the same as always: if you purchased it and you can't hold it in your hand, it isn't yours.

I hold a small position and have gotten beat up, watching and waiting for right timing to buy more and wondering the same Phatlander...it is at 1.80 now....time to pull the trigger or hope for 1.70 ish?

$1.82 is looking interesting. What are your thoughts here?

I like the idea ...

Should be able to easily buy $2.00 and sell $3.00

I picked up USLV this morning for a sell at $20.00

We are in accumulation mode for long swing trade

$EXK building a base down here around it's 50 day moving average? I'm seeing more than a few subtly strong miners on my scans, could be a positive sign for the sector?

http://chartdiligence.com/exk-silver-miner-trying-to-bottom-building-a-base/

I have my father down huge in EXK. It was not my idea. Back awhile ago.

While I would not average down, I would tend to say hold on to your position here.

The expansion and production are amazing.

Ball Mill Repaired and Plant Operations Back to Normal at Bolanitos Mine; Second Mine Contractor Commences Work at El Cubo Mine

VANCOUVER, BC--(Marketwired - June 15, 2015) - Endeavour Silver Corp. (TSX: EDR) (NYSE: EXK) announces that the 1,000 tonne per day (tpd) ball mill at the 1,600 tpd Bolañitos mine was repaired earlier than expected and plant operations returned to normal last Friday, June 12. No material impact on production is anticipated from the mill downtime as the mine continued to produce ore to the stockpile.

The outage will have a minor impact on forecast production in the second quarter from the El Cubo mine, located in the same district of Guanajuato as Bolañitos, because El Cubo is currently in the middle of a mine expansion from 1,500 tpd to 2,200 tpd. The additional mine tonnes were planned to be trucked for processing to the Bolañitos plant to take advantage of its available capacity. Instead, these additional El Cubo tonnes during the mill downtime were stockpiled for processing in the third quarter.

The El Cubo mine expansion is well under way and a second mining contractor commenced work last Friday, June 12 to help facilitate the mine expansion to 2,200 tpd. The El Cubo plant was optimized in the first quarter and is now operating well above its original design capacity of 1,500 tpd.

About Endeavour Silver - Endeavour Silver is a mid-tier silver mining company focused on growing production, reserves and resources in Mexico. Since start-up in 2004, Endeavour has posted ten consecutive years of accretive growth of its silver mining operations. Endeavour's three silver-gold mines in Mexico combined with its strategic acquisition and exploration programs should facilitate Endeavour's goal to become a premier senior silver producer.

Accumulate

Silver Manipulation May Be The Most Extreme In History

Never in the history of the commodities markets has the amount of futures outstanding for any commodity been this extraordinarily disconnected from the amount of the physical supply produced and available for delivery...

Greetings from Fred & IntendanceInvestors Beach

Loading up for swing

Endeavour Silver Infill Drilling Confirms Thick, High Grade, Silver-Gold Mineralization at Terronera Property, Jalisco State, Mexico

Marketwired - June 01, 2015

More news on Terronera

Greetings from Entendance!

Q1 news is out. Production is up and ahead of projection for Q1. While it is lower than Q1 2014, it is ahead of Q4 and ahead of Q1 projection. This stock still has a long-term price projection of $3.80

Even a small move from RSI(14) 30 to 50 can yield a nice little gain.

I am hanging on for at least $4.00

I would love to see SILVER over $20.00 again.

When that day comes, I can only pray that I hold SLW and USLV.

I do hold CDE, SSRI and EXK.

Sold yesterday at 2.24 and glad i did

now trying to get in at 1.95

thanks for the posting john!

Endeavour Silver's Short-Term Issues Mask A Long-Term Opportunity

Mar. 25, 2015 8:51 AM ET

By Ben Kramer-Miller

Endeavour Silver has seen high production costs and declining production, which is contrary to the story that drove the stock to new highs in 2010-11.

Bearish investors are assuming temporary issues are actually more permanent, yet production growth is coming and high costs were short-lived.

Endeavour Silver's woes have made it cheap relative to its peer group.

As investors realize that growth is coming while costs will decline Endeavour shares should play catch-up, and thereby offer a compelling opportunity for silver bulls.

Overview

Endeavour Silver (NYSE:EXK) is a mid-tier silver producer with three operations in Mexico - Guanacevi, Bolanitos, and El Cubo. This had been one of the best-performing silver stocks as silver rose from $9/oz. to nearly $50/oz. from 2008 - 2011 given its history of production and resource growth and its relatively low production costs. However, it has been one of the hardest hit of late given that 2014 was the first year in a decade in which we didn't see this growth. The company's poor performance was exacerbated as its all-in production costs at El Cubo came in at ~$35/oz., and in the fourth quarter the company took a write-down of $83 million on this project.

The company's 2015 guidance wasn't exactly promising either, since production at Guanacevi and Bolanitos is expected to decline. Investors should note, however, that this is mostly due to these mine's showing an especially strong performance in 2014 given their higher ore grades and silver recovery rates (although this was masked by the high production costs at El Cubo and a falling silver price).

In short what we've seen is that those attributes of Endeavour Silver that have made it an attractive investment in the past have seemingly dissipated, and the stock has fallen to reflect that.

But have the company's fundamentals really shifted? Sure, we have seen some short-term issues, but to argue that a few rocky quarters negate a decade of exceptional performance by Brad Cooke and his team is short-sighted. Furthermore, this short-sightedness has created a compelling opportunity for those willing to take the other side of a trade that has become decidedly bearish. I cite the following points to support my thesis.

Endeavour Silver has become incredibly inexpensive compared with its peers. I specifically have in mind Fortuna Silver (NYSE:FSM) and First Majestic Silver (NYSE:AG). My readers know that these are two companies that I like and have owned (I still own First Majestic), given their regular production growth, resource growth, and low costs. These three companies all have the same attributes that make them excellent vehicle through which to express a bullish silver position, yet Endeavour's 2014 issues have made it the least expensive option by far using key metrics.

Endeavour Silver may not grow its production substantially (if at all) this year or next but it does have near-term growth potential in its Terronera Project, which has the potential to become the company's largest through a 2-stage development.

The recently announced ramp-up of production at El Cubo should keep production relatively flat on a year/year basis with a minimal capital expenditure.

Weakness in the Mexican Peso should reduce production costs on a USD basis.

Before I get into these points in greater depth I must point out that Endeavour Silver is hardly out of the woods considering its production costs relative to the current silver price. The silver price is incredibly low relative to the cost of production for all but a handful of company's (e.g. Tahoe Resources (NYSE:TAHO)) which trade at a significant premium to the value of their discounted cash-flow as a result. This has led to project postponements (e.g. Pitarrilla) and temporary suspensions (e.g. Velardena). While the low silver price may lead to a supply reduction that ultimately pushes prices higher investors need to keep in mind that ~70% of global silver production is by-product production, meaning that the companies that mine most of the world's silver don't really care what the silver price is. There are certainly reasons to be bullish of silver given a rise in investment demand along side gold and given a rise in industrial applications (e.g. photovoltaic cells in solar panels), but this won't necessarily lead to an increase in the silver price in the near term. As a result, silver miners such as Endeavour Silver could continue to lose money, and this will clearly put pressure on the stock price. This means that there is inevitably a speculative aspect to an investment in Endeavour Silver. But once the silver market recovers Endeavour Silver will be among the best positioned companies to profit from this.

Endeavour Silver's Relative Valuation

Endeavour Silver is not the cheapest silver mining company, but if we compare it only with companies in its peer group I would argue that it is. Fortuna Silver and First Majestic Silver share similarities with Endeavour Silver.

They all have multiple projects in Mexico.

They all have histories of production and resource growth.

They all have histories of low production costs.

If we look at their relative valuations compared with their annual silver equivalent production we will find that Endeavour Silver is incredibly inexpensive. Endeavour Silver should produce ~11 million ounces of silver with a valuation of just $208 million. Meanwhile Fortuna will produce just 9 million ounces in spite of its $488 million valuation. Finally First Majestic will produce 16 million ounces with a $656 million valuation. This gives the three companies respective market cap/annual AgEq. production ratios of $19.oz., $54/oz., and $40/oz.

Investors should note that the disparity in valuations between First Majestic and Endeavour is offset by the former company's production costs, which are expected to be ~$2/oz. lower than Endeavour's placing that company in the black in 2015 assuming the silver price remains relatively flat. But Fortuna expects to have similar production costs to Endeavour and the valuation disparity has no validation (despite Fortuna's stronger balance sheet and larger working capital position) unless we assume tremendous growth for Fortuna vs. no growth or even production declines for Endeavour while Endeavour is slated to grow longer term. In fact, while I think Fortuna Silver is an excellent company pair, traders may want to consider going long Endeavour vs. going short Fortuna.

2 - Endeavour Silver's Growth (Terronera)

As I've mentioned, Endeavour Silver's growth streak has ended in 2014 as production declined.

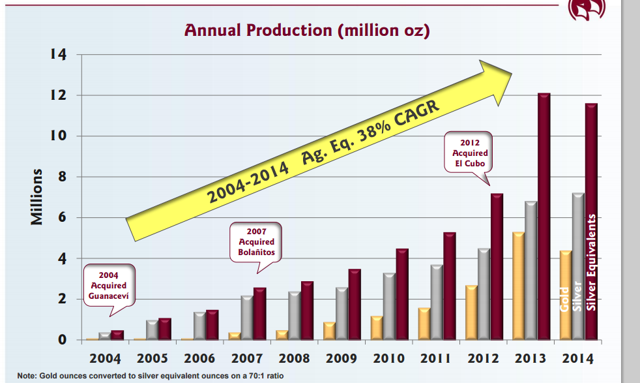

(Source: Endeavour Silver's Presentation)

Endeavour Silver is also not slated to grow production in 2015, which should be roughly flat. Still, growth in 9 out of 11 years at a significant double-digit clip is nothing short of phenomenal. Investors giving up on Endeavour Silver - especially at the current valuation - are far too concerned with the current lack of growth to realize that Endeavour's management has made astute acquisitions and has demonstrated an ability to exploit opportunities at its acquired projects. Furthermore, such investors seem to be assuming that just because Endeavour Silver isn't growing its production now that its team isn't working towards growing production, when it is actually pursuing multiple opportunities that will take a couple of years to execute.

The biggest opportunity is at the Terronera Project - acquired in 2013. The Terronera property contains multiple small historic mines and ore veiins that a company such as Endeavour can consolidate into a significant mine - the company's largest in fact if management can execute its longer-term plan.

The maiden Terronera resource estimate shows a project with 29 million ounces of silver and 225,000 oz. of gold (44 million AgEq oz. assuming a 70:1 gold:silver ratio with the company). Management plans on completing the drilling needed in order to convert some of these resources into reserves in preparation for a pre-feasibility study. Assuming this PFS is promising we should see the company develop the project in preparation for a 2016 production commencement. The company is targeting a 2-stage development, with the first stage reaching ~4 million ounces of AgEq. production in the mine's first full year (2017). Stage two should lead to a doubling of production to 8 million AgEq. oz. which means tremendous growth for the company. While we don't know the initial capital costs the company's $20 million in working capital (as of December 31st) and its $50 million credit line (soon to be $25 million in July) should be sufficient to develop the project, especially given that this development will take place over time.

Furthermore, assuming the company can generate flat production at its 3 producing projects combined (recent discoveries at Bolanitos and El Cubo suggest that this is a probable scenario) we should be able to see production grow at a CAGR of nearly 15% as the Terronera Project matures. This doesn't take into consideration potential growth from acquisitions. In my discussion with Brad Cooke, he told me that the company is exploring opportunities in both gold and silver throughout North America. Investors who follow the junior space know that there are several opportunities - juniors that have compelling projects, but which lack the capital with which to develop them. While this opportunity is open to other mid-tier producers, it flies in the face of the market's apparent belief that Endeavour Silver's growth is behind it.

3 - Expansion At El Cubo

Until Endeavour Silver's recent announcement that it is going to be expanding production at El Cubo, 2015 was supposed to be another year of declining production. The El Cubo expansion announcement along with a turn in gold and silver prices last week sent shares bounding off of a multi-year low, as the implication is that production will not decline in 2015. Rather, it will be flat.

Before I get into the El Cubo expansion, note again that 2014 was expected to be weaker than it was, yet high grades/recoveries at Guanacevi and Bolanitos meant that the company surprised to the upside. 2015 guidance calls for a "normalization" of grades and recoveries, but we could very well see upside surprises at these two projects again. That being said the production decline was in comparison to these better than expected figures.

Investors should note also that expansion at El Cubo is a far cry from what management was suggesting a few months ago, namely that the mine might be put into care and maintenance (cf. Endeavour's Q3 MD&A). Yet opex came down in Q4 while silver and gold prices seem to have stabilized, both of which bode well for El Cubo.

Production at El Cubo is expected to rise from 1,550 tpd. up to 2,200 tpd. Production guidance was for 3.5-3.8 million AgEq. oz., and this figure is expected to rise to 4.3-4.8 million AgEq. oz. making El Cubo the company's largest producing mine. This increased production should also lower the company's overall AISC to $16-$17.5/oz. on a by-product basis. Meanwhile, the added capex is just $3.8 million, which is minimal compared with the company's original ~$33 million allocation towards capital expenditures for 2015.

Overall we should see production growth come in flat year over year, although another outperformance at the company's Guanacevi and Bolanitos Projects could push production to a higher level than what we saw last year.

4 - Mexican Peso Weakness

Given recent weakness in the value of the Mexican Peso Endeavour Silver's input costs should come down in US dollar terms. With the USDMXN cross at 15.1 and Endeavour Silver's expectations for 14.5 the company has a fair amount of wiggle room, and investors should expect production costs to come in towards the lower end of guidance should the Peso remain weak or weaken further. With that in mind Endeavour is likely generating positive cash-flow relative to its AISC estimates at $16.8/oz. silver, although the margin is razor thin.

The Bottom Line

As is often the case in the mining industry, short-term phenomena can have a tremendous impact on market sentiment and on a given mining company's share price. Endeavour Silver saw its Ripkenesque growth stream come to a halt last year. It also saw its average production costs come in high relative to its peers thanks to high costs at El Cubo. The second and third points that I bring up should demonstrate to investors that these are temporary issues. Endeavour Silver has the potential to grow long term, and it has the potential to bring its costs down so that it is competitive with its peers.

Yet the market doesn't see it this way. As point #1 reveals, Endeavour Silver is unjustifiably cheap relative to its peers. This relative value is the result of near-term issues. Therefore, investors looking for a growth company leveraged to the silver price have a unique opportunity in Endeavour Silver to buy this growth at a price that assumes none.

silverspot $17.4 DH now when writing $17.2 and rising nicely

in on 1.77 next stop 2.35

happy trading folks!

I would have but I did not like the way it was trading.... It may react deferent today but all I know is there is and I watched better opps pass by yesterday and I'd rather exit a trade I didn't like then hold in hopes of any difference.... But I do see a lot of potential to the upside here with pms getting a boost... Glty thanx Exk

shoulda held bro..its @2.25 after hours..and shouldnt stop running till the 2.40 area in wich we should have a pull back then on to 3.00

Chit would move if people would lay off the ask.... Exk

Looking like PMs may make a little comeback next week.... Dollar tanking... We shall see... Held some exk till then.... Exk

|

Followers

|

88

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

1410

|

|

Created

|

10/30/06

|

Type

|

Free

|

| Moderators | |||

![]()

LISTED ON THE NYSE:EXK AND TSX:EDR

http://www.edrsilver.com/s/Home.asp

| The Daily View | The Weekly View | |

The Point & Figure Chart

|

|

SILVER IN DEPTHSilver links from LinksMine - InfoMine's Library of Mining Web Sites Site Listings

Associations

Exploration

History

Investment

Publications

Please boardmark us if this i-Message is helpful... Thanks in advance!!! |

![]()

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |