News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

RECENT TOUT $600 PPO SILVER; BAC SAID $3,000 GOLD PPO;

Coeur d'Alene Mines Corp. (CDE)'

$CDE, 1-1/2 X'S BOOK, Book/sh 2.79, Cash/sh 0.23

https://finviz.com/quote.ashx?t=CDE&ty=c&ta=1&p=d

$CDE , LIGHT DEBT;Debt/Eq 0.44,LT Debt/Eq 0.41

https://finviz.com/quote.ashx?t=CDE&ty=c&ta=1&p=d

insiders; $CDE

https://finviz.com/quote.ashx?t=CDE&ty=c&ta=1&p=d

RE;

Coeur Mining, Inc. explores for, develops, and produces gold, silver, zinc, and lead properties. The company holds 100% interests in the Palmarejo gold and silver mine covering an area of approximately 112,520 net acres located in Mexico; the Rochester silver and gold mine covers an area of approximately 16,494 net acres situated in Nevada; the Kensington gold mine comprising 12,336 net acres located in Alaska; the Wharf gold mine covering an area of approximately 7,852 net acres situated in South Dakota; and the Silvertip silver-zinc-lead mine comprising 90,156 net acres located in British Columbia, Canada. It also owns interests in the Sterling gold project and the Crown Block of deposits located in the Walker Lane trend in Nevada; and the La Preciosa silver-gold exploration project located in the State of Durango, Mexico. The company markets its concentrates to third-party refiners and smelters in the United States, Switzerland, and Japan. The company was formerly known as Coeur d'Alene Mines Corporation and changed its name to Coeur Mining, Inc. in May 2013. Coeur Mining, Inc. was founded in 1928 and is headquartered in Chicago, Illinois.

Insider Trading Relationship Date Transaction Cost #Shares Value ($) #Shares Total SEC Form 4

Smith Terrence F. SVP, Operations Mar 16 Buy 2.06 12,000 24,720 178,130 Mar 19 04:51 PM

Sandoval Brian E Director Mar 16 Buy 2.18 1,130 2,458 39,012 Mar 17 05:20 PM

Rasmussen Hans John SVP, Exploration Mar 16 Buy 2.00 17,500 35,000 350,655 Mar 17 05:19 PM

THOMPSON J KENNETH Director Mar 16 Buy 2.61 10,000 26,100 178,223 Mar 17 05:17 PM

Whelan Thomas S SVP & CFO Mar 13 Buy 2.58 6,000 15,480 6,000 Mar 17 05:14 PM

Gress Randy Director Mar 13 Buy 2.61 17,062 44,556 157,483 Mar 16 04:27 PM

Gress Randy Director Mar 12 Buy 2.73 12,938 35,321 140,421 Mar 16 04:27 PM

Whelan Thomas S SVP & CFO Mar 12 Buy 2.95 15,000 44,250 275,494 Mar 12 06:10 PM

Sandoval Brian E Director Feb 28 Buy 3.99 1,233 4,920 37,882 Feb 28 05:02 PM

Whelan Thomas S SVP & CFO Feb 28 Buy 4.11 25,000 102,625 260,494 Feb 28 05:02 PM

Sandoval Brian E Director Feb 25 Buy 5.00 984 4,920 36,649 Feb 26 05:26 PM

Edwards Sebastian Director Feb 25 Sale 5.21 21,423 111,528 111,053 Feb 26 05:06 PM

Watkinson Kenneth J VP, Corporate Controller & CAO Feb 21 Sale 6.38 10,378 66,212 31,768 Feb 21 05:29 PM

Nault Casey M. SVP & General Counsel Dec 03 Sale 7.00 20,000 140,060 357,744 Dec 04 04:16 PM

Watkinson Kenneth J VP, Corporate Controller & CAO Aug 13 Sale 5.48 9,891 54,213 47,638 Aug 14 04:16 PM

Nault Casey M. SVP & General Counsel Aug 05 Sale 5.01 30,000 150,300 377,744 Aug 07 05:14 PM

Whelan Thomas S SVP & CFO May 31 Buy 2.84 25,000 71,000 183,464 Jun 03 05:47 PM

Sandoval Brian E Director May 23 Buy 3.00 1,750 5,245 18,087 May 23 04:38 PM

THOMPSON J KENNETH Director May 21 Buy 2.93 15,000 43,935 150,645 May 21 05:12 PM

STILL BUSINESS; Q1 2020 Coeur Mining Inc Earnings Call

https://finance.yahoo.com/news/edited-transcript-cde-earnings-conference-080600501.html

COEUR D'ALENE Apr 24, 2020 (Thomson StreetEvents) -- Edited Transcript of Coeur Mining Inc earnings conference call or presentation Thursday, April 23, 2020 at 3:00:00pm GMT

TEXT version of Transcript

================================================================================

Corporate Participants

================================================================================

* Hans John Rasmussen

Coeur Mining, Inc. - SVP of Exploration

* Mitchell J. Krebs

Coeur Mining, Inc. - President, CEO & Director

* Paul DePartout

Coeur Mining, Inc. - Director of IR

* Terrence F. D. Smith

Coeur Mining, Inc. - SVP of Operations

* Thomas S. Whelan

Coeur Mining, Inc. - Senior VP & CFO

================================================================================

Conference Call Participants

================================================================================

* Adam Philip Graf

B. Riley FBR, Inc., Research Division - Senior Mining Analyst & MD

* Brian MacArthur

Raymond James Ltd., Research Division - MD & Head of Mining Research

* Joseph George Reagor

Roth Capital Partners, LLC, Research Division - MD & Senior Research Analyst

* Michael Stephan Dudas

Vertical Research Partners, LLC - Partner

================================================================================

Presentation

--------------------------------------------------------------------------------

Operator [1]

--------------------------------------------------------------------------------

Good morning, and welcome to the Coeur Mining First Quarter 2020 Financial Results Conference Call. (Operator Instructions) Please note, this event is being recorded. I now like to turn the conference over to Paul DePartout, Director of Investor Relations. Please go ahead.

--------------------------------------------------------------------------------

Paul DePartout, Coeur Mining, Inc. - Director of IR [2]

--------------------------------------------------------------------------------

Thank you, and good morning. Welcome to Coeur Mining's first quarter earnings conference call.

Our results were released after yesterday's market close, and a copy of the press release and slides are available on our website. I would like to remind everyone that our press release, slides and some of our comments today include forward-looking statements from which actual results may differ. Please review the cautionary statements included in our press release and presentation as well as the risk factors described in our first quarter 10-Q and 2019 10-K.

Now I'll turn it over to Mitch.

--------------------------------------------------------------------------------

Mitchell J. Krebs, Coeur Mining, Inc. - President, CEO & Director [3]

--------------------------------------------------------------------------------

Thanks, Paul. Joining me on the line are Tom Whelan and Terry Smith, along with several other members of the management team. Before discussing the quarter, I'd like to provide a brief COVID-19 update. Since early March, our 2 objectives for navigating through the impacts of this global pandemic have been to protect the health and well-being of our fellow employees, their families, our contractors and our communities where we operate and to ensure the continuity of our business operations as best we can. To date, we have had no positive COVID-19 cases anywhere in the company. Early last month, we put a series of controls and procedures in place, focused on controlling and limiting access to our operations, thoroughly screening employees and visitors and reducing exposure and transmission risk through a range of social distancing protocols and sanitizing and cleaning procedures. Office employees are all working from home and nonessential travel has been eliminated.

We are continually reassessing these procedures as the situation evolves and as we gain additional information. The level of engagement, support and outreach by our employees to the communities in Western South Dakota, Northern Nevada, Southeast Alaska, Chihuahua, Mexico and British Columbia has been truly inspiring. Slides 15 through 17 highlights several of the efforts being made by our employees.

In terms of business continuity, our 3 U.S. assets remain in operation with minimal adjustments or disruptions. Our Palmarejo mine suspended operating and exploration activities in accordance with the decree issued by Mexico in late March.

Our Silvertip operation in British Columbia safely suspended mining and processing activities just ahead of the COVID-19 outbreak and all ongoing site activities, along with our drilling program are continuing there. We remain in close contact with our suppliers and with our smelter and refinery customers, and we have not experienced any significant disruptions to date.

Like many companies, we have taken steps to increase our frequency and methods of communication, bolster our liquidity levels and be as prepared as possible for a wide range of potential scenarios going forward. Overall, I think our strategy is serving us well during these unprecedented times. Our focus on operating a balanced portfolio of assets located in North America with a particular focus on the U.S. is helping us reduce our overall risk profile.

Our shift over the past several years towards more gold and less silver has removed a significant amount of volatility and has us well positioned for the current environment. Our collection of organic growth projects offers investors compelling near-, medium- and long-term growth and our commitment to a higher sustained level of exploration, particularly near our existing assets, provides our stockholders with exposure to the upside potential associated with new discoveries and to opportunities for high-return mine life extensions from successful reserve and resource growth.

And finally, our U.S. listing and location as well as our liquidity and access to capital are key differentiators, especially during times like this.

Now turning to our results. Overall, the quarter was in line with our expectations, mostly due to strong performances from Palmarejo and our Kensington gold mine in Alaska. Those 2 operations offset a lighter quarter from both Wharf and Rochester as anticipated, both of which are expected to deliver stronger results during the remainder of the year.

I mentioned our collection of growth projects. The 2 most impactful near-term opportunities are the expansion of Rochester and a potential restart of Silvertip. At Rochester, we achieved a major milestone on schedule for the POA 11 expansion project when we received the record of decision from the Bureau of Land Management last month. We plan to accelerate work later this year and complete this important project by late 2022. We are also on track to issue an updated technical report in the fourth quarter incorporating an updated capital estimate, optimized mine plan and economic analysis.

And at Silvertip, a prefeasibility study for a potential mill expansion is now underway, and we expect to have some results midyear. The drilling program at Silvertip kicked off last month, and we remain optimistic about what this program will deliver. And finally, speaking of exploration, other key elements of our 2020 exploration program, the largest in our company's 92-year history are off to good starts. The bulk of our near-mine exploration investment during the first quarter went to Palmarejo and Kensington, while our single largest allocation of resource expansion drilling went to the Sterling and Crown deposits in Southern Nevada. We plan to provide a midyear exploration update later this year, given the size and importance of these programs for the company.

And with that, I'll go ahead and turn it over to Terry.

--------------------------------------------------------------------------------

Terrence F. D. Smith, Coeur Mining, Inc. - SVP of Operations [4]

--------------------------------------------------------------------------------

Thanks, Mitch, and good morning, everyone. Slide 6 highlights our production performance at each operation during the quarter and provides an outlook for the remainder of the year. Starting with Palmarejo. Throughput increased by over 25% year-over-year and improved recovery rates from several optimization initiatives helped drive higher gold production quarter-over-quarter. As anticipated, silver production decreased due to lower grades in our mine plan during the first quarter. Higher gold recoveries and throughput, along with a slightly higher gold price combined to generate over $20 million of free cash flow at Palmarejo. It's also worth pointing out that we'll be well positioned to safely and efficiently ramp back up once the suspension in Mexico is lifted.

Switching over to Rochester. We mentioned on the last call that crusher production was hitting its stride early in the year. I'm happy to report that crusher performance during the quarter was 11% higher than our target and 33% higher than the fourth quarter. We have now rebuilt momentum on our leach pad that we lost late last year, but have not yet seen the benefit of improved ore placement rates and restocked metal inventories as we were operating on deeper sections of the pad in the first quarter.

We expect production to improve during the second quarter and climb steadily through the remainder of the year. Before moving on to Kensington, I'll add some color to Mitch's earlier comments on our expansion plans at Rochester. We plan to spend roughly $30 million to $35 million on the expansion this year, which includes a mix of procurement and early stage earthworks. We have several purchase agreements already in place for long-lead items, including crushing and process equipment. At SNC-Lavalin, our third-party EPCM contractor has progressed detailed design to around 50% completion to date.

We are also conducting a targeted drilling program, which we are optimistic will help us upgrade our mine plan as we work towards an updated technical report at the end of the year. Now switching over to Kensington. Production was on budget for the quarter as we saw positive grade reconciliation from the Kensington Main deposit.

Financial performance remained strong as unit costs decreased by 5% to under $930 per ounce, helping to generate just over $14 million in free cash flow during the quarter. We were able to produce just over 2,500 ounces from Jualin at an average grade of 0.33 ounce per ton or 11.3 grams per ton. And now expect to add into account for 15% to 20% of Kensington's production for the full year.

We expect a slightly weaker second quarter due to fewer anticipated Jualin tons but expect Kensington will deliver another strong year for the company. At Wharf, adverse weather impacted first quarter crusher performance, leading to weaker-than-expected production levels.

We have mobilized a third-party crusher contractor to accelerate our placement rates and help us catch up on and deliver on our full year plan. As a reminder, we are planning to increase our strip throughout the year, but we expect it to revert to historical levels in 2021.

Before passing the call over to Tom, I'd like to thank our workforce for stepping up during this difficult period. We had a solid quarter of safety performance despite this additional time of stress and distraction. Please continue to be mindful and focus on the task at hand. We appreciate everything you are doing and your continued dedication to the company. Next, Tom will cover the financial highlights for the quarter.

--------------------------------------------------------------------------------

Thomas S. Whelan, Coeur Mining, Inc. - Senior VP & CFO [5]

--------------------------------------------------------------------------------

Thanks, Terry. As presented on Slide 10, we have a very sound balance sheet, with no near-term maturities and over $250 million of liquidity.

With improved margins, our LTM EBITDA increased 44% to $195 million versus the $135 million just 12 months ago. Higher EBITDA, along with our 2019 debt reduction initiatives led to total and net debt leverage ratios at the quarter end of 1.8x and 1.5x, respectively. We have been completing various scenario-planning analysis to consider the potential impacts of COVID-19 on our business, specifically focusing on liquidity.

From volatile gold and silver prices to estimating the impact of the temporary suspension at Palmarejo and other potential downside scenarios, we have modeled numerous cases to determine a range of financial impacts. We believe it is prudent to have a wide variety of options available to maximize our financial flexibility during these unprecedented times of volatility and uncertainty. Based on our analysis, we've taken the following key actions to be well positioned under various potential downside scenarios. First, we've added foreign currency hedges to lock in operating cash flow gains relative to our budget.

Secondly, we drew down an additional $100 million after quarter end on our revolving credit facility. Third, we developed an internal list of opportunities where CapEx and exploration could be deferred. And fourth, we have also put a $100 million at the market equity program in place, which is available as a source of liquidity, if needed. To date, we have not begun the deferral of any capital projects or exploration investments and would not expect to reduce these key internal growth initiatives unless certain downside scenarios became likely.

Looking at our financial results on Slide 5. We expected the first quarter to be our weakest quarter of 2020 and are pleased to be ahead of our internal budget on operating and free cash flow. Digging into the numbers. Our first quarter results include $47 million of adjusted EBITDA, which is a 79% improvement over Q1 2019. We had strong kickoff to our 2020 exploration programs. And we had modest negative operating cash flow of $8 million which was impacted by the timing of the annual Mexican EBITDA tax, the payment of the annual -- of our annual bonuses across the company and the buildup of inventory on the leach pads at Wharf and Rochester. The temporary cessation of active mining and processing activities at Silvertip also had a notable impact on our Q1 2020 results. Silvertip used $32 million of free cash flow during the quarter. A figure we will expect will be much smaller going forward as the site focuses on exploration, prefeasibility work and ongoing maintenance activities. We forecast that ongoing carrying costs will be $4.5 million per quarter, down from the $6 million figure that we guided towards at the beginning of the year. Exploration and prefeasibility costs remain in line with our previous estimates. One additional note on silvertip. Given the precipitous drop in zinc and lead prices during Q1 2020 and the significant increase in the 2020 benchmark treatment charges for zinc and lead concentrates, which were finalized during March 2020, we remain confident that the temporary cessation was a sound decision. Before handing the call back to Mitch, I wanted to draw everyone's attention to Slide 11, where we summarize our hedging program. We continue to take advantage of the stronger gold price by implementing additional price protection.

You'll see that we've extended our zero-cost collar gold hedges to cover a portion of our production in 2020 with a $1,600 floor. As I mentioned earlier, we also laid in some forward currency hedges over the next 2 years. Our hedging strategy is designed to support cash flow generation and help fund key internal growth projects, most notably the POA 11 expansion at Rochester, which we anticipate funding with a combination of internally generated cash flow and borrowings from our revolving credit facility.

I'll now pass the call back to Mitch.

--------------------------------------------------------------------------------

Mitchell J. Krebs, Coeur Mining, Inc. - President, CEO & Director [6]

--------------------------------------------------------------------------------

Thanks, Tom. Just to quickly wrap up, Slide 12 hits several of our key priorities for the remainder of the year. Of course, our top priority remains the health of our employees, their families and members of our communities as we continue to manage our way through the COVID-19 crisis.

We remain optimistic about our exploration programs and the results we expect to see over the course of the year. We're also looking forward to seeing Rochester's production levels rise based on the higher crushing and placement rates the team has been delivering. All of us are excited about the operations future growth potential as POA 11 is set up to gain momentum during the second half.

I'm also enthusiastic about the work that is now underway on the prefeasibility study at Silvertip, and we look forward to sharing results with you later in the year. And finally, we will continue to further improve upon our strong safety and environmental performance as we strive to deliver consistent operating and financial results. Okay. With that, let's go ahead and open it up for any questions.

================================================================================

Questions and Answers

--------------------------------------------------------------------------------

Operator [1]

--------------------------------------------------------------------------------

(Operator Instructions) Our first question will come from Michael Dudas with Vertical Research Partners.

--------------------------------------------------------------------------------

Michael Stephan Dudas, Vertical Research Partners, LLC - Partner [2]

--------------------------------------------------------------------------------

I'm glad to hear things are going safely and healthy for everyone.

--------------------------------------------------------------------------------

Mitchell J. Krebs, Coeur Mining, Inc. - President, CEO & Director [3]

--------------------------------------------------------------------------------

Thanks, Mike. Good to hear from you.

--------------------------------------------------------------------------------

Michael Stephan Dudas, Vertical Research Partners, LLC - Partner [4]

--------------------------------------------------------------------------------

So first question regarding Palmarejo. Maybe you can share some additional thoughts on expectations on some of the government in the news we're hearing about continued expansion of the COVID situation, what maybe other angles are being worked on down there to kind of alleviate that and how -- and for first? And then secondly, how quickly do you think you can ramp up once you get the green light? And third, what are some of the carrying costs that we should anticipate into Q2, given the cessation of the mining down there?

--------------------------------------------------------------------------------

Mitchell J. Krebs, Coeur Mining, Inc. - President, CEO & Director [5]

--------------------------------------------------------------------------------

Yes, sure. Thanks, Mike. I'll start and then Tom, I'll ask you to step in as well. Just in terms of the overall status in Mexico, just to rewind the clock, March 31, the Mexican government issued the emergency decree regarding restrictions on nonessential businesses. And then we received some further clarification on April 6 that made it clear that precious metals mining was not an essential business according to the decree. So then on the 7th of April, we announced that we were going to begin the process of temporarily suspending operating activities at Palmarejo. That decree earlier this week was officially extended out to May 30, however, there are areas with little COVID-19 impact that will be allowed to reopen on May 18. And currently, Palmarejo sits in one of those zones of little-to-no COVID-19 impact. So we'll kind of circle the 18th of May. But meanwhile, on a kind of a separate path, we submitted an application for exemption to the decree under guidelines published by the Undersecretary of Mines. And that's kind of a case-by-case process where they'll take the applications, discuss it with public health officials to determine whether or not mines can restart sooner than those May date.

So we'll keep pushing on that angle as well as kind of gearing ourselves up for a restart kind of worst case, hopefully, in the middle of May, kind of like the ramp down that takes 2 or 3 weeks. There'll be a similar kind of 2- or 3-week ramp-up process to get ourselves back up and going whenever we do get the green light, whether it's the 18th of May or sooner. And so that's how we're kind of thinking about it. In terms of impact on cost, obviously, that depends heavily on when we are able to restart so that we can measure how many days we were not producing. But Tom, do you want to go into another level of detail there as far as potential impact?

--------------------------------------------------------------------------------

Thomas S. Whelan, Coeur Mining, Inc. - Senior VP & CFO [6]

--------------------------------------------------------------------------------

Yes, sure. Yes, Mike, as we talked about, we've been thinking about tons of scenarios around this and the number that I would use for kind of a 30-day shutdown, which kind of feels like our best estimate at this stage be about $10 million in terms of less free cash flow for the year for Palmarejo.

We really want to grind into how we came up with that, just an estimate of 1/12 of the revenue lost. We think we can reduce our operating cost by about 50%. We've obviously stopped the drilling and there'll be less CapEx. So that's kind of to give you some numbers about how to get to that $10 million. But the other thing I would just remind everybody is that -- I mean, the peso is really devalued here. And as mentioned, we put on some hedges. The peso, about 50% to 60% of our costs are denominated in Mexican peso. So with those hedges, we've kind of locked in roughly the same amount of lost free cash flow from operations. So anyway, just to give you a sense, we'll come back with obviously a clearer picture as Q2, but hopefully, that gives you some numbers to play around with.

--------------------------------------------------------------------------------

Michael Stephan Dudas, Vertical Research Partners, LLC - Partner [7]

--------------------------------------------------------------------------------

Tom, that's perfect. And hopefully, the 18th is sooner rather than later. Second question is turning to Kensington. So just to clarify. So it sounds like second half, you're getting a lot more ore processed through Jualin. So is that mix going to be -- you said 15%, 20%, is that over the 12-month period? Or -- so therefore to be maybe a much higher mix in the second half of the year? Is that how I should think about it?

--------------------------------------------------------------------------------

Mitchell J. Krebs, Coeur Mining, Inc. - President, CEO & Director [8]

--------------------------------------------------------------------------------

That's right. First quarter, Terry, remind me, it was single digits, right? In terms of...

--------------------------------------------------------------------------------

Terrence F. D. Smith, Coeur Mining, Inc. - SVP of Operations [9]

--------------------------------------------------------------------------------

Yes.

--------------------------------------------------------------------------------

Mitchell J. Krebs, Coeur Mining, Inc. - President, CEO & Director [10]

--------------------------------------------------------------------------------

Contribution. And a lot of that, Mike, had to do back to COVID-19 in terms of workforce availability, a decent amount of our workforce at Kensington flies up from the Lower 48 to work their scheduled rotations and that had impacted in the first quarter and in particular, in March, availability of workers in Jualin. And so that is a reason why we were a little lower in the first quarter than we expect to be in subsequent quarters. I kind of look at it as a positive that with only 9% or whatever of the tons coming from Jualin, it had a great quarter on its own. So hopefully, with a little bit higher contribution through the rest of the year, we'll see the results reflect that.

--------------------------------------------------------------------------------

Michael Stephan Dudas, Vertical Research Partners, LLC - Partner [11]

--------------------------------------------------------------------------------

That's great. I appreciate that, Mitch. And just finally, maybe back to Terry on the scenario analysis or maybe the hedging front.

So I assume since you've been putting through this hedge program on gold over the last few quarters, you're going to continue to think through that as the markets move forward and with higher collar balances, I would assume. And from a -- and from I guess on the scenario concept, looking at the potential spend on the deferrals and such. It seems -- it seems like you feel like you have enough liquidity to kind of crush through this and not have to defer some of the important work that you're doing, but what -- would it be just price change or concerns about that? Or Palmarejo would be out for several months? Would that be some of the negative scenarios that would impact that?

--------------------------------------------------------------------------------

Mitchell J. Krebs, Coeur Mining, Inc. - President, CEO & Director [12]

--------------------------------------------------------------------------------

Yes. I'll start and then Tom, you can chime in with our thoughts on the market and the hedging program that we've been carrying out. Having a $1,600 floor under a good chunk of our gold production goes a long way toward helping to ensure that we've got sufficient cash flow from Rochester and elsewhere to fund that expansion project. That's a project that doesn't have a lot of room to be deferred or moved because as we stack on the Stage IV leach pad, there's a point at which that pad is full, and we need to have this new pad down and ready to start stacking on. And that is sort of late 2022. So we're working on that basis and on that schedule in between our revolver and cash flow, especially feeling better about that downside of $1,600 gives us a lot of comfort that that's sufficient. Now if Mexico continues on more -- longer than what we all hope and expect that makes the numbers, obviously, a little bit tighter, but we still feel comfortable that we'll have sufficient liquidity.

And then just, Mike, on separate but related point. I mentioned Silvertip and the prefeasibility study and a potential scenario of a restart. That's a project that we have a lot of flexibility on in terms of if and when we would ever pursue that. And so obviously, we're thinking through and mindful of not only relative returns on these projects, but how do they sequence and slot in to our financial capacity to deliver on them. And -- but Rochester is clearly the one that has the highest priority. Tom, anything on the hedging that you want to add?

--------------------------------------------------------------------------------

Thomas S. Whelan, Coeur Mining, Inc. - Senior VP & CFO [13]

--------------------------------------------------------------------------------

Yes, I just -- I'd reiterate, Mitch, that $1,600 floor is definitely a target. And the beauty of doing it in layering is we're not trying to time the market. And obviously, where the more patient you are, the higher the ceiling that we're able to achieve. And just as a reminder, I mean, in March, we did see gold drop below $1,500 and silver went below $12. So we definitely want to protect the downside to ensure that we've got sufficient funding for POA 11, as Mitch mentioned, I mean, that timing is we really don't have that much flexibility to move around that capital spend.

--------------------------------------------------------------------------------

Operator [14]

--------------------------------------------------------------------------------

Our next question will come from Joseph Reagor with Roth Capital Partners.

--------------------------------------------------------------------------------

Joseph George Reagor, Roth Capital Partners, LLC, Research Division - MD & Senior Research Analyst [15]

--------------------------------------------------------------------------------

So I guess first thing, thinking about the scenario with Rochester with building out the additional leach pads. Would you need to have all of like the capital to do that in hand when you embarked on that? Or is that something where you can kind of have a certain portion day 1 that would make you feel comfortable?

--------------------------------------------------------------------------------

Mitchell J. Krebs, Coeur Mining, Inc. - President, CEO & Director [16]

--------------------------------------------------------------------------------

Yes. I think it's the latter, Joe, in terms of -- we have the revolver balance day 1 but with the cash flow from Rochester and then from the other operations, that, of course, will come over time during 2021 and 2022 to act as a another key source of the funding. So that would come sort of as we go. Tom, anything to add to that?

--------------------------------------------------------------------------------

Thomas S. Whelan, Coeur Mining, Inc. - Senior VP & CFO [17]

--------------------------------------------------------------------------------

No, you've nailed it again. We -- Joe, we think we've got between the internally generated operating -- free cash flow from our mines as well as the revolver capacity. Based on the scenarios that we've run, we're feeling pretty good about our ability to fund POA 11.

--------------------------------------------------------------------------------

Joseph George Reagor, Roth Capital Partners, LLC, Research Division - MD & Senior Research Analyst [18]

--------------------------------------------------------------------------------

Okay. Also, Rochester, a big portion of kind of the decline in production there has been related to tonnage. And then that step back up in Q1, but that probably won't flow through until Q2, just as you rebuild inventory. But is there any difference in the ore makeup from, say, mid-last year to now?

Like are you guys experiencing any changes even though maybe the model says it should be fine? But like is there anything geologically different about the ore that you're mining today?

--------------------------------------------------------------------------------

Mitchell J. Krebs, Coeur Mining, Inc. - President, CEO & Director [19]

--------------------------------------------------------------------------------

Terry, do you want to cover that?

--------------------------------------------------------------------------------

Terrence F. D. Smith, Coeur Mining, Inc. - SVP of Operations [20]

--------------------------------------------------------------------------------

Joe, yes, thanks for the question. No, there's nothing significantly different over that time period that you're thinking about. One of the things that we benefit from and Rochester is just uniformity. I think there's some differences in terms of hardness. We see drilling differences and crushing impacts from hardness, but nothing geologically or mineralogically that is different.

--------------------------------------------------------------------------------

Joseph George Reagor, Roth Capital Partners, LLC, Research Division - MD & Senior Research Analyst [21]

--------------------------------------------------------------------------------

Okay. So given that, and given my layman's terms understanding of the high-pressure grinding you're doing. There's really nothing but time standing between you guys and getting to where you want to be?

--------------------------------------------------------------------------------

Mitchell J. Krebs, Coeur Mining, Inc. - President, CEO & Director [22]

--------------------------------------------------------------------------------

I think that's fair. Every time we put HPGR-crushed ore on or near liner, we see the kind of recovery results that all the test work had indicated. So that's certainly comforting and validating. It's really about the timing, like you said, Joe, of getting not only ounces down through deeper sections of that Stage IV pad, but building up that tonnage, those stacking rates and placement rates that the guys out there have done a good job of reestablishing. In large part, is blasting in the pit has gone a long way toward helping improve the crusher performance. But we're -- we like what we see at HPGR, and you're right, it's more of a time -- function of time than anything.

--------------------------------------------------------------------------------

Joseph George Reagor, Roth Capital Partners, LLC, Research Division - MD & Senior Research Analyst [23]

--------------------------------------------------------------------------------

Okay. I just wanted to confirm and cross all the Ts. One last one, just at Silvertip, are there any remaining payments? Or did you guys make the final contingent payments in Q1?

--------------------------------------------------------------------------------

Mitchell J. Krebs, Coeur Mining, Inc. - President, CEO & Director [24]

--------------------------------------------------------------------------------

Yes. We made that no more now to go.

--------------------------------------------------------------------------------

Operator [25]

--------------------------------------------------------------------------------

(Operator Instructions) Our next question will come from Brian MacArthur with Raymond James.

--------------------------------------------------------------------------------

Brian MacArthur, Raymond James Ltd., Research Division - MD & Head of Mining Research [26]

--------------------------------------------------------------------------------

I have 3 quick questions. Just back to Tom's point about layering. You said you had 99,000 ounces in 2021. And in the press release, you sort of gave us 56,500 with the first half and the second half. Can I assume those other ounces were sort of layered in, in the first half and the second half equally?

--------------------------------------------------------------------------------

Mitchell J. Krebs, Coeur Mining, Inc. - President, CEO & Director [27]

--------------------------------------------------------------------------------

Tom, you want to cover that?

--------------------------------------------------------------------------------

Thomas S. Whelan, Coeur Mining, Inc. - Senior VP & CFO [28]

--------------------------------------------------------------------------------

Yes is the answer. There's probably a little bit more weighting to the first half of the year, but the goal would be to have them spread out evenly when we complete the program.

--------------------------------------------------------------------------------

Brian MacArthur, Raymond James Ltd., Research Division - MD & Head of Mining Research [29]

--------------------------------------------------------------------------------

Okay. Great. It's just there are only 56 -- you kindly gave us 56,500 ounces of prices in the press release, and I saw you got up to 99,000 ounces as you said in your presentation. Second thing, just the $100 million draw on the revolver, I mean, I get it. If you draw $200 million, you're going to pay more under fees or whatever. Is there any math -- I assume that $100 million was sort of -- in the context of guaranteeing cash to finance Rochester, obviously, you'd want to have a buffer just in case things didn't go wrong. Is that kind of just the way you came up with $100 million. You did all your testing, you made analysis and $100 million sort of seem like the right number. And I mean you could have taken, I presume, $150 million or $200 million and maxed it out, and then you'd had more cash on the balance sheet. Is that kind of the thinking that went into where the $100 million came from?

--------------------------------------------------------------------------------

Mitchell J. Krebs, Coeur Mining, Inc. - President, CEO & Director [30]

--------------------------------------------------------------------------------

You're on the -- definitely on the right track there. Tom, you want to provide some color?

--------------------------------------------------------------------------------

Thomas S. Whelan, Coeur Mining, Inc. - Senior VP & CFO [31]

--------------------------------------------------------------------------------

Yes. Thanks, Brian. Look, the -- we went through a bunch of different scenarios. And the last -- so a couple of comments. One is this is a different crisis than '08. It's not a a banking crisis. It's an economic crisis. So we chatted with all the banks and just made sure that there is no restrictions to be able to draw on the revolver. And so this had nothing to do with that. But it was just -- we thought a precautionary measure just to make sure that we had some cash on hand, if some of these downside scenarios were to come together. I mean the hope is that we'll never need to draw on it. And again, I'd just reiterate as -- right as of this moment, we have no intentions to stop any CapEx or exploration.

And again, at $1,700 gold, we're feeling actually pretty good. But last thing you want to do is rest on your laurels and get caught short in a time like this. We've never seen times like this. And so we just thought it was the prudent thing to do.

--------------------------------------------------------------------------------

Brian MacArthur, Raymond James Ltd., Research Division - MD & Head of Mining Research [32]

--------------------------------------------------------------------------------

Yes, it makes total sense. And a lot of other companies have done that, too. I would just I figured that's where that number came from as opposed to -- I mean, I could argue, just to be really sure you take the whole $200 million, I guess, is the debate.

--------------------------------------------------------------------------------

Thomas S. Whelan, Coeur Mining, Inc. - Senior VP & CFO [33]

--------------------------------------------------------------------------------

Yes. We just -- sorry, and just to, we also thought, again, we've talked about all the responses that -- our response to COVID-19. And we just didn't think drawing all of it was commensurate with all of the risk mitigation that has happened. And we thought it would probably send the wrong signal. The third -- as you point out, we could have done the whole thing, but -- it just didn't feel right to us.

--------------------------------------------------------------------------------

Brian MacArthur, Raymond James Ltd., Research Division - MD & Head of Mining Research [34]

--------------------------------------------------------------------------------

Now, it makes sense. And I guess just my third question, just with Silvertip. And as you mentioned, with TCRCs up, zinc prices down, you put in the final payment of $25 million. I guess the stress testing for a writedown, what's the general thought process on that? I assume you're going to wait until you get the new study because then you sort of have an adjusted long-term plan as -- and maybe you don't need to do, what I'm not saying you do or don't. I was just kind of curious whether that had to be stress-tested this quarter.

--------------------------------------------------------------------------------

Mitchell J. Krebs, Coeur Mining, Inc. - President, CEO & Director [35]

--------------------------------------------------------------------------------

Tom, you want to cover that, please?

--------------------------------------------------------------------------------

Thomas S. Whelan, Coeur Mining, Inc. - Senior VP & CFO [36]

------------------------------------------------------------------------

Sure. Yes. Again, the assumptions that we used in the impairment analysis contemplated a restart in 2022. And so again, looking out to where long-term prices would be, I think it was disclosed in the 10-K, what we used in terms of zinc and lead prices sort of back to more long term. And so again, whatever happens to the zinc and lead price here over the next 18 months is not going to impact the amount of the impairment?

--------------------------------------------------------------------------------

Operator [37]

--------------------------------------------------------------------------------

Our next question will come from Adam Graf with B. Riley FBR.

--------------------------------------------------------------------------------

Adam Philip Graf, B. Riley FBR, Inc., Research Division - Senior Mining Analyst & MD [38]

--------------------------------------------------------------------------------

Just a couple of quick questions. One at Rochester, the study that you guys are targeting for the end of the year. Can you just remind us if that's going to include Lincoln or Wilco? Or is that the next study for Rochester?

--------------------------------------------------------------------------------

Mitchell J. Krebs, Coeur Mining, Inc. - President, CEO & Director [39]

--------------------------------------------------------------------------------

No, Adam, it's Mitch. The plan would be updated capital and then a mine plan that would be optimized and expanded to hopefully include some of those East Rochester ounces that sit underneath the old Stage I and Stage II pads and then some additional material from Lincoln Hill, but nothing from Wilco or Gold Ridge further to the west of Lincoln Hill.

--------------------------------------------------------------------------------

Adam Philip Graf, B. Riley FBR, Inc., Research Division - Senior Mining Analyst & MD [40]

--------------------------------------------------------------------------------

Got it. And then could you guys just give us maybe some color on any progress in the first quarter exploration at Preciosa and at Sterling and Crown?

--------------------------------------------------------------------------------

Mitchell J. Krebs, Coeur Mining, Inc. - President, CEO & Director [41]

--------------------------------------------------------------------------------

Yes. Hans, do you want to cover that?

--------------------------------------------------------------------------------

Hans John Rasmussen, Coeur Mining, Inc. - SVP of Exploration [42]

--------------------------------------------------------------------------------

Adam, La Preciosa continues with the engineers looking at our updated geologic and resource model. We'll get -- actually a meeting at the end of next week, we'll review it. So sometime in May, we'll have a much better idea of what we're going to do there. The Crown and Sterling projects started out with 3 rigs turning, 2 up at the Crown area, 1 down at the Sterling. The Crown area had a large truck rig, is one of the rigs testing a new geophysical target. Because of the success of that target, now we've moved our smaller RC rig up there and continued drilling on this target. It's called Seahorse. I'm not sure if we've shown that in any of our maps, but it's up about 1.5 miles north of the SNA resource in an area that was -- where no prior drilling was, it's a geophysical target. So we've been quite busy with one rig up there. We sent the truck rig home, and we're continuing to drill around the Sterling area.

At Sterling, we'll move a core rig in, starting on Sunday. And the core rig will start doing the infill large diameter core that we're going to use for metallurgical work, engineering work and look at a pit design at Sterling itself. Both Crown and Sterling have had some nice upside hits in the drill results, which we're going to talk about in our midyear updates in places we didn't expect. So these will be results that I can disclose, and we put that news release out. And hopefully, by that news release, we'll have somewhere around between 5 and 10 holes to report in those new zones. So it's going really well at Crown and Silvertip.

--------------------------------------------------------------------------------

Mitchell J. Krebs, Coeur Mining, Inc. - President, CEO & Director [43]

--------------------------------------------------------------------------------

And Hans, just in terms of the biggest components of the program this year, Palmarejo and Kensington, obviously, Palmarejo right now is -- drills aren't turning, but we have 10 rigs there ready to get back into action. And so we're looking forward to that. That program and the results from there. Kensington also will have some good results to talk about in a midyear update. And then Rochester and Wharf are both more kind of middle to the second half of the year weighted. So we've got a lot of good things going on in a lot of places.

--------------------------------------------------------------------------------

Hans John Rasmussen, Coeur Mining, Inc. - SVP of Exploration [44]

--------------------------------------------------------------------------------

Yes. Silvertip just got started nearly mid- to end of March and is up to 3 rigs now. We'll have 5 rigs by the middle of second quarter. Visually, things are looking really good there, too.

--------------------------------------------------------------------------------

Adam Philip Graf, B. Riley FBR, Inc., Research Division - Senior Mining Analyst & MD [45]

--------------------------------------------------------------------------------

And Hans, can you remind us at Palmarejo, is the focus more resource conversion or resource expansion?

--------------------------------------------------------------------------------

Hans John Rasmussen, Coeur Mining, Inc. - SVP of Exploration [46]

--------------------------------------------------------------------------------

We started out the year with a bit more resource conversion just because of our annual resources and reserves calculations. Typically, we have a data cutoff end of June. So if you look at our money spent and feet drilled or meters drilled, they're a bit more in the infill resource conversion category right now. However, it's super important that we find some new veins, new clavos to expand into in a couple of years. And so you'll see for the remainder of the year, that the focus will be dominantly expansion. And we're finding some interesting looking stuff that we're going to end up like Mitch said, we've got 10 rigs queued up to start-up and aggressively drill some new areas north of Independencia and east of Independencia, where we've got some good intercepts that we'll talk about in the midyear report. Great.

--------------------------------------------------------------------------------

Operator [47]

--------------------------------------------------------------------------------

This concludes our question-and-answer session. I would like to turn the conference back over to Mitchell Krebs for any closing remarks.

--------------------------------------------------------------------------------

Mitchell J. Krebs, Coeur Mining, Inc. - President, CEO & Director [48]

--------------------------------------------------------------------------------

Okay. Thanks. Well, we appreciate everyone's time this morning, and we look forward to speaking with you again in the summer when things are hopefully returning to normal to discuss our second quarter results. In the meantime, I hope you all stay healthy and safe. And thanks again for your time. Bye.

--------------------------------------------------------------------------------

Operator [49]

--------------------------------------------------------------------------------

The conference has now concluded. Thank you for attending today's presentation. You may now disconnect.

Coeur Mining Inc (CDE)

3.6 ? -0.05 (-1.37%)

Volume: 8,655,051 @04/24/20 7:59:58 PM EDT

Bid Ask Day's Range

- - 3.42 - 3.84

CDE Detailed Quote

Current Report Filing (8-k) Edgar (US Regulatory) - 4/23/2020 8:47:57 AM

Prospectus Filed Pursuant to Rule 424(b)(5) (424b5) Edgar (US Regulatory) - 4/23/2020 8:42:25 AM

Quarterly Report (10-q) Edgar (US Regulatory) - 4/22/2020 4:43:24 PM

Current Report Filing (8-k) Edgar (US Regulatory) - 4/22/2020 4:36:02 PM

Coeur Reports First Quarter 2020 Results Business Wire - 4/22/2020 4:30:00 PM

Additional Proxy Soliciting Materials (definitive) (defa14a) Edgar (US Regulatory) - 4/21/2020 4:31:32 PM

Coeur Announces Move to Virtual Platform for 2020 Annual Stockholders’ Meeting Business Wire - 4/21/2020 4:30:00 PM

http://www.barchart.com/quotes/stocks/CDE

[-chart]www.stockta.com/cgi-bin/candle.pl?cobrand=&symb=CDE&size=analysis&support=0.00,15,0.00,66,0.00,38,0.00,14,0.00,12,0.00,15,0.00,3,0.00,2,0.00,4,0.00,6,0.00,2&trend=[/chart]

http://www.barchart.com/quotes/stocks/CDE

http://www.barchart.com/quotes/stocks/CDE

[-chart]www.stockta.com/cgi-bin/candle.pl?cobrand=&symb=CDE&size=analysis&support=0.00,15,0.00,66,0.00,38,0.00,14,0.00,12,0.00,15,0.00,3,0.00,2,0.00,4,0.00,6,0.00,2&trend=[/chart]

http://www.barchart.com/quotes/stocks/CDE

Is Coeur d’Alene Mines Corporation (CDE) A Good Stock To Buy?

April 7, 2020

by DEBASIS SAHA

Insider Monkey

We hate to say this but, we told you so. On February 27th we published an article with the title Recession is Imminent: We Need A Travel Ban NOW and predicted a US recession when the S&P 500 Index was trading at the 3150 level. We also told you to short the market and buy long-term Treasury bonds. Our article also called for a total international travel ban. While we were warning you, President Trump minimized the threat and failed to act promptly. As a result of his inaction, we will now experience a deeper recession (see why hell is coming).

In these volatile markets we scrutinize hedge fund filings to get a reading on which direction each stock might be going. The 800+ hedge funds and famous money managers tracked by Insider Monkey have already compiled and submitted their 13F filings for the fourth quarter, which unveil their equity positions as of December 31. We went through these filings, fixed typos and other more significant errors and identified the changes in hedge fund portfolios. Our extensive review of these public filings is finally over, so this article is set to reveal the smart money sentiment towards Coeur d’Alene Mines Corporation (NYSE:CDE).

Hedge fund interest in Coeur d’Alene Mines Corporation (NYSE:CDE) shares was flat at the end of last quarter. This is usually a negative indicator. The level and the change in hedge fund popularity aren’t the only variables you need to analyze to decipher hedge funds’ perspectives. A stock may witness a boost in popularity but it may still be less popular than similarly priced stocks.

That’s why at the end of this article we will examine companies such as Harmony Gold Mining Co. (NYSE:HMY), United States Steel Corporation (NYSE:X), and Capitol Federal Financial, Inc. (NASDAQ:CFFN) to gather more data points. Our calculations also showed that CDE isn’t among the 30 most popular stocks among hedge funds (click for Q4 rankings and see the video at the end of this article for Q3 rankings).

In the financial world there are numerous methods market participants have at their disposal to evaluate publicly traded companies. A duo of the most useful methods are hedge fund and insider trading interest. Our experts have shown that, historically, those who follow the best picks of the elite money managers can trounce the S&P 500 by a superb margin (see the details here).

GOTHAM ASSET MANAGEMENT

Joel Greenblatt of Gotham Asset Management

We leave no stone unturned when looking for the next great investment idea. For example, we believe electric vehicles and energy storage are set to become giant markets, and we want to take advantage of the declining lithium prices amid the COVID-19 pandemic. So we are checking out investment opportunities like this one.

We read hedge fund investor letters and listen to stock pitches at hedge fund conferences. Our best call in 2020 was shorting the market when S&P 500 was trading at 3150 after realizing the coronavirus pandemic’s significance before most investors. Keeping this in mind we’re going to take a look at the key hedge fund action surrounding Coeur d’Alene Mines Corporation (NYSE:CDE).

Hedge fund activity in Coeur d’Alene Mines Corporation (NYSE:CDE)

At the end of the fourth quarter, a total of 15 of the hedge funds tracked by Insider Monkey were long this stock, a change of 0% from the previous quarter. The graph below displays the number of hedge funds with bullish position in CDE over the last 18 quarters. So, let’s check out which hedge funds were among the top holders of the stock and which hedge funds were making big moves.

Is CDE A Good Stock To Buy?

The largest stake in Coeur d’Alene Mines Corporation (NYSE:CDE) was held by Renaissance Technologies, which reported holding $42.7 million worth of stock at the end of September. It was followed by Sprott Asset Management with a $11.3 million position. Other investors bullish on the company included Millennium Management, Citadel Investment Group, and Winton Capital Management.

In terms of the portfolio weights assigned to each position Sprott Asset Management allocated the biggest weight to Coeur d’Alene Mines Corporation (NYSE:CDE), around 2.34% of its 13F portfolio. Sloane Robinson Investment Management is also relatively very bullish on the stock, earmarking 1.09 percent of its 13F equity portfolio to CDE.

Due to the fact that Coeur d’Alene Mines Corporation (NYSE:CDE) has experienced declining sentiment from the entirety of the hedge funds we track, we can see that there lies a certain “tier” of hedgies that elected to cut their positions entirely heading into Q4. Intriguingly, Jonathan Soros’s JS Capital cut the biggest position of the “upper crust” of funds watched by Insider Monkey, totaling about $0.4 million in stock, and Mike Vranos’s Ellington was right behind this move, as the fund said goodbye to about $0.2 million worth. These transactions are important to note, as aggregate hedge fund interest stayed the same (this is a bearish signal in our experience).

Let’s also examine hedge fund activity in other stocks – not necessarily in the same industry as Coeur d’Alene Mines Corporation (NYSE:CDE) but similarly valued. These stocks are Harmony Gold Mining Co. (NYSE:HMY), United States Steel Corporation (NYSE:X), Capitol Federal Financial, Inc. (NASDAQ:CFFN), and Pacific Premier Bancorp, Inc. (NASDAQ:PPBI). This group of stocks’ market caps match CDE’s market cap.

Ticker No of HFs with positions Total Value of HF Positions (x1000) Change in HF Position

HMY 12 79446 2

X 26 179182 6

CFFN 16 142701 2

PPBI 12 47542 4

Average 16.5 112218 3.5

As you can see these stocks had an average of 16.5 hedge funds with bullish positions and the average amount invested in these stocks was $112 million. That figure was $74 million in CDE’s case. United States Steel Corporation (NYSE:X) is the most popular stock in this table. On the other hand Harmony Gold Mining Co. (NYSE:HMY) is the least popular one with only 12 bullish hedge fund positions.

Coeur d’Alene Mines Corporation (NYSE:CDE) is not the least popular stock in this group but hedge fund interest is still below average. This is a slightly negative signal and we’d rather spend our time researching stocks that hedge funds are piling on. Our calculations showed that top 20 most popular stocks among hedge funds returned 41.3% in 2019 and outperformed the S&P 500 ETF (SPY) by 10.1 percentage points.

These stocks lost 13.0% in 2020 through April 6th but beat the market by 4.2 percentage points. Unfortunately CDE wasn’t nearly as popular as these 20 stocks (hedge fund sentiment was quite bearish); CDE investors were disappointed as the stock returned -56.9% during the same time period and underperformed the market. If you are interested in investing in large cap stocks with huge upside potential, you should check out the top 20 most popular stocks among hedge funds as most of these stocks already outperformed the market in 2020.

Nice move 22 percent.

#CDE: The Gold Signal, Just Like 2008

First came the gold price take-down, and then came the Sunday night announcement. It’s just like late October, 2008…

by Dave Kranzler of Investment Research Dynamics

In 35 years of active participation in several diverse aspects of the financial aspects, I’ve never seen a more obvious investment set-up than long gold, silver and mining stocks:

https://investmentresearchdynamics.com/the-gold-signal-just-like-2008/

#CDE: Load'em up..:-} $4.00

#CDE: More FUEL for lift off...;-}

https://www.zerohedge.com/commodities/bullion-bank-nightmare-lbma-comex-spread-blows-again

Bullion Bank Nightmare As LBMA-COMEX Spread Blows Up Again

Submitted by Ronan Manly, BullionStar.com

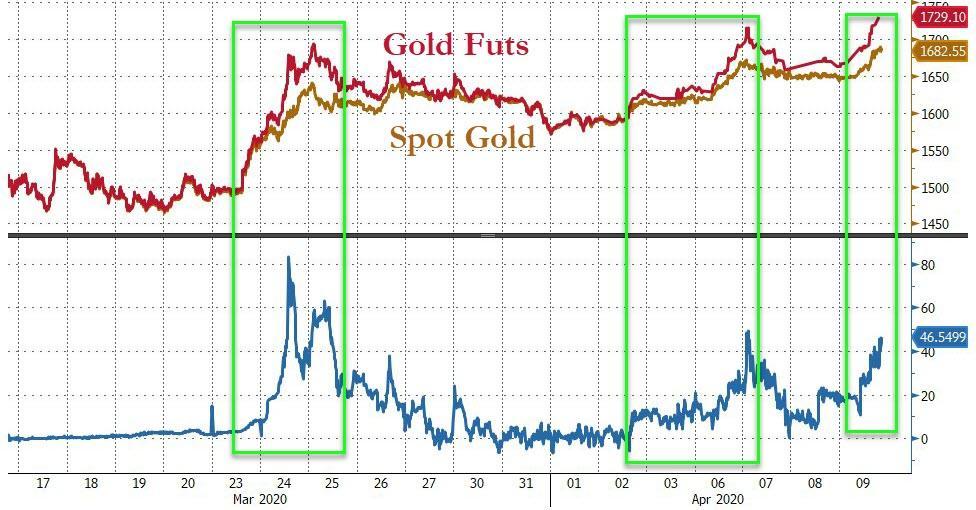

The gaping price differential between spot gold and gold futures that has been plaguing the paper gold markets in London and New York for the last three weeks shows no signs of abating and is continuing to flare up.

In essence, the contango phenomenon we are seeing is one of gold futures prices trading far above spot gold prices, a sign of liquidity problems in the London gold market and a signal that something is completely broken between the world‘s two predominant “gold price discovery" trading venues – which both, by the way, trade paper gold.

As a reminder, London LBMA trades unallocated gold over the counter (OTC), a form of synthetic fractional gold derivative. The vast quantities of unallocated gold which are traded in London are then netted and cleared in an electronic clearing engine called Aurum by 5 LBMA bullion banks that comprices London Precious Metals Clearing Limited (LPMCL), namely JP Morgan, HSBC, UBS, Scotia, and ICBC Standard Bank). Allocation of physical gold is a totally separate process beyond clearing in Aurum.

COMEX trades predominantly cash-settled gold futures contracts on exchange and facilitates the trading of these contracts bilaterally. COMEX futures are 99.9% cash-settled and even those that result in delivery really result in warehouse warrants changing hands but the gold staying in the New York vaults of JP Morgan, HSBC and Scotia.

That the wide-open spread continues to persist is even more remarkable, despite the best efforts of the London Bullion Market Association (LBMA), CME Group (operator of COMEX) and the powerful London-New York bullion bank syndicate to throw all they have at the problem.

At the time of writing, spot gold was trading at US$ 1696 against US$ 1753 for the front-month (most actively traded) COMEX gold futures contract, a $36 spread with futures over 3.44% over spot. The spread we‘re referring to can be seen in the below 3-day chart, which plots June 2020 gold futures (red and green line) against spot XAUUSD (blue line) from 6 April to 8 April. Notice that over this time the futures price has stayed far above spot, and more importantly, it has persistently done so.

The spot-futures spread blow out that has been running into its third week now can vividly be seen by zooming out and looking at a similar chart but this time from 24 March until 9 April, the first day that the price spread between London and New York gaped open. Notice the big gaps between futures and spot over 24-25 March, the persistence of the gap over the remainder of the week, and the subsequent re-explosion of the divergence since early April, particularly over the last few days.

Three Weeks and Counting

Its instructive to review a short timeline of some of the events which have contributed to this ongoing saga over the last three weeks, because it shows that no matter what the LBMA and CME do, the spread between London and COMEX continues to stay out there.

Week 1

23 March – COMEX gold futures (April contract) begin trading noticeably above LBMA bullion bank spot gold prices.

24 March – Spreads between COMEX futures and London spot blew out to $100 at one point during the day, while bid – ask spreads within London spot widened substantially.

24 March – Rumors in the gold market suggested that bullion banks that were required to deliver physical gold for COMEX Exchange for Physical (EFP) transactions failed to do so, suffered losses and exited the market, and that this caused the Spread between COMEX and London to widen substantially.

The bullion bank controlled LBMA releases its first control statement, deflecting attention away from London, saying it will help (essentially collude with) the CME-COMEX in the gold market – The official language is that the LBMA “is working closely with COMEX and other key stakeholders to ensure the efficient running of the global gold market."

Note – Who are these other key stakeholders, what do they mean by efficient running, and what gives them the right to think they can “run“ the global gold market?

24 March – LBMA and its bullion banks pressure CME to launch a gold futures contract with a deliverable clause in London 400 oz gold bars.

24 March – At end of day, CME announces the launch of a new gold futures contract that can theoretically deliver 400 oz bars, 100 oz bars and kg bars but that uses a fractional paper concept called Accumulated Certificates of Exchange (ACEs) to divide 400 oz deliverable bars into 100 oz bars, and that critically includes all refiner brands on the LBMA Good Delivery List (current and former Good Delivery refiners). This contract will be called 4GC (See here and here).

See BullionStar article “LBMA colludes with the COMEX – To lockdown the global gold market?" for background to the above.

25 March until end of March – For the rest of the week, disinformation from bullion banks to mainstream media about flight cancellations and refinery closures preventing bullion banks delivering gold from London to New York thus causing prices on COMEX and London to diverge. See here, here, here and here for examples. From the below chart you can see that there is never any gold exported from London to New York.

Week 2

30 March – CME published its daily gold vault stocks report (for Friday 27 March) with a new category for “400 oz AND eligible brands", but with all vaults showing zero stocks of 400 oz gold bars. And notably, that the JP Morgan vault in New York had zero holdings.

30 March – When Bullionstar draws attention to this new CME vault report, in “COMEX can’t find a 400 oz bar for its new 400 oz gold futures contract“, the CME then deletes the new report from its website on the morning of 31 March, and replaces it intra-day with a report which reverted to the original version.

1 April – LBMA and CME publish an unprecedented second control statement titled “LBMA and CME group comment on healthy gold stocks in New York and London”, saying that “CME Group and LBMA..will continue to coordinate efforts as market circumstances evolve”. See “LBMA and COMEX try to Reassure the Market – Twice in One Week“ for background.

Note – If LBMA and CME are trading gold bars, why would they need to coordinate efforts, and more importantly, coordinate efforts to what end?

LBMA disingenuously refers to 8326 tonnes of gold in London, a figure that is from 3 months ago, and nearly all of this total tonnage is central bank gold, gold held in ETFs, and allocated gold held by other investors. The real float of physical gold in the london LBMA gold vaults controlled by the LBMA bullion banks is less than 1000 tonnes and some estimates from sources in the bullion banks say it could be between 300 and 500 tonnes.

In the same statement, CME refers to 9.2 million ozs ( 287 tonnes) of gold held in its approved vaults, with irrelevant claims that 5.6 million ozs of this is eligible gold. Eligible gold is gold which just happens to be in the form that satisfies the deliverable unit of the contracts (1 kg bars or 100 oz bars). The rest of this figure is registered gold, which already has warehouse warrants attached.

2 April – The spread between COMEX gold futures prices and London spot gold prices starts to gap up strongly again.

Rest of week – CME Group releases publicly a PowerPoint slide presentation titled “Precious Metals Physical Delivery Process”, which includes the new 4GC contract and explains how to get an electronic warrant if standing for delivery of COMEX gold futures contracts, but that explains nothing about withdrawing gold from the COMEX vaults.

The COMEX presentation also features a slide discussing the COMEX New York approved vaults but unbelievably instead of showing photos of one of its approved New York vaults, this slide contains photos of a HSBC gold vault in London showing gold bars belonging to the exchange traded fund, the SPDR Gold Trust (GLD). This GLD gold has nothing to do with COMEX gold vaults in New York (or does it?).

Week 3

6 April – The spread between the COMEX June gold futures contract and the LBMA spot gold price blows out again very widely to over $80 at one point in the day.

6 April – CME adds back the category “Enhanced Delivery (400 oz AND eligible brands)" to its New York daily vault report. Of the 9 vaults on the report, 5 have 0 holdings in this 400 oz category, 2 (Brinks & Loomis) have a combined 2 tonnes, HSBC claims 21.5 tonnes, JP Morgan appears for the second time, claiming 126.8 tonnes. The first time being 30 January when JP Morgan was listed as having zero tonnes of 400 oz bars.

Note – “400 oz AND Eligible Brands" will be the subject of another article soon, but for now it means as follows. For the new 4GC contract, CME added all LBMA Good Delivery gold bar Brands (Current and Former) as Eligible brands. That’s 68 brands from the existing GC100 contract + 71 brands from the LBMA current Good Delivery List + another 113 LBMA former Good Delivery List.

As another aside, where did the JP Morgan New York vault suddenly get 126.8 tonnes of gold suddenly to add to Eligible category for the COMEX 4 GC contract? Was this 126.8 tonnes of gold suddenly shipped in to the JP Morgan vault from London? Hardly. Were 126.8 of London Good Delivery gold bars already sitting in its New York vault. Probably not as its London and not New York which is the center of 400 oz gold bar storage. Was there some type of gold swap involved between London and New York. Possibly.

Another intriguing possibility is that now that former LBMA Good Delivery List gold bars are eligible for the new 400 oz contract, that JP Morgan borrowed Old US Assay Office gold bars from the New York Fed (their two gold vaults are beside each other), and then added these to the Eligible category for the new 4GC gold contract.

Root Cause of Spot vs Futures Gold Price Discrepancy

So what is the cause of this dislocation in pricing between the lower ‘spot’ price and the higher ‘futures’ price, i.e. between the London LBMA gold spot market and the New York COMEX gold futures market? The answer in general is that the problem is with the spot price. And where is the spot price? London.

Ironically, the LBMA bullion banks are trying to shift the attention away from London, when London is exactly where the problem is. The spot price problem appears to be due to liquidity problems of the LBMA market makers in London where they are suspicious of trading with each other. This is despite the fact that these LBMA market makers are obliged to constantly make a market and offer two way price quotations to each other. These market makers are BNP Paribas, Citibank, Goldman Sachs, HSBC, ICBC Standard, JP Morgan Chase, Merrill Lynch, Morgan Stanley, Standard Chartered, Bank of Nova Scotia, Toronto-Dominion and UBS.

The spot price problem has nothing to do with air travel cancellations or shipments of 100 oz gold bars from London to New York. These market makers do not make markets in physical gold. The unit of trading in London is not real gold anyway, its unallocated gold or gold credit which is issued by a bullion bank and which has counterparty risk.

Something has spooked these market makers and caused a drop in liquidity in the London market. These banks, which normally trade with each other, now do not want to trade with each other due to heightened counterparty risk. Unallocated trading volumes in the London gold market have fallen over the last three weeks. See chart below.

Likewise, according to Bloomberg, COMEX gold futures trading volume last week was 80.6 million ounces, a 72% drop compared to the end of February. From the same Bloomberg article, there is an intriguing and obviously dramatic quote from commodities broker Marex Spectron, saying:

“You have a bunch of shell-shocked market makers who are literally hiding under their desks and do not and possibly can not make markets in any size, shape or form,” said David Govett, head of precious metals trading at Marex Spectron. “Hence we have the lack of liquidity, the small volumes and the wide spreads.”

Marex is a broker for EFPs, so maybe the LBMA market makers are not answering calls. Then they are failing in their duty and obligations as market makers. But why would market makers not want to trade and how does this relate to EFP spreads? If banks suffered EFP problems and then the EFP spread between London and New York blew up, and then they use the excuse that the EFP spread is too large for them to make a market in spot because they don’t want to take on risk, then that’s just circular logic and a pathetic excuse. But what causes LBMA market makers to become shell shocked and literally hide under their desks?

Could it be that the gold trading activities of some of these LBMA bullion banks have blown up and they have ceased their market making activities, but have not publicly stated this, and covered it up? Stranger things have happened. All the while, as trading volumes continue to fall in the paper gold markets of London and New York, the opposite is the case in physical gold markets, where BullionStar and other bullion dealers – those that continue to have inventory – see unprecedented demand and increasing trading volumes.

This article was originally published on the BullionStar.com website with the same title "Bullion Bank Nightmare as LBMA-COMEX Spread Blows Up Again".

Good stock but will need to come much lower.

Panic will resume here soon.

Trade accordingly.

glty

#CDE; Finding the Cream...:-}

https://www.coeur.com

That's for dang right.

I also felt way with $12.00 SILVER

So far so good USLV.

There are no guarantees in life, however, CDE going under 2 seems like a done deal.

CDE under $2.00??

Space some buys out down under $2 see if you get any drops over the next 60.

Tecno Trader current analysis of CDE price action.

CDE as well as most of the stocks in the mining sector.

have had a sharp drop off in share price.Sector analysis

show show that the mining stocks both gold and silver

had a large fall on the sector ladder as well as a

fall on relative strength as well.The market sell off

hit the gold and silver markets as well.Although there

is a great demand for physical silver it not reflected

in the price at this time.I looked at several charts

in the mining sector and things don;t look good at this

point in time.Technical damage has been done and it

make take a period of time before things reverse.

This is my viewpoint at this time and construe a

buy or sell in CDE stock

time for another trade close to establishing double bottom here been a nice trader.

CDE down $.93 just a few minutes ago, ouch. Still bullish on CDE. Have a great day.

$CDE The Sterling Gold Project located near Beatty, Nevada, consists of four, high-grade, heap-leachable deposits with a total inferred gold resource of approximately 709,000 ounces, averaging 0.066 oz/t located on a 35,000-acre land package approximately 115 miles north of Las Vegas, Nevada.

The high-grade Sterling gold deposit is a fully-permitted, past producing mine with near-term, low-cost, low-capital production potential. The remaining deposits include Daisy, Secret Pass and SNA collectively known as the Crown Block, which contain significant exploration potential. The land package also includes multiple new, undrilled targets that remain untested.

https://www.coeur.com/operations/project/sterling-gold-nevada/

$CDE The Palmarejo silver & gold complex consists of (1) the Palmarejo mine and processing facility; (2) the Guadalupe underground mine, located about 8 kilometers southeast of the Palmarejo mine; (3) the Independencia underground mine, located approximately 800 meters northeast of the Guadalupe underground mine; and (4) other nearby deposits and exploration targets. The Palmarejo complex is located in the state of Chihuahua, Mexico

https://www.coeur.com/operations/mines/palmarejo-mexico/

Came across this stock over the weekend and I liked the look of the chart so I picked up some shares yesterday. I look at long range charts, not the intraday charts. I am willing to wait 3 months or 3 years for a nice profit. Best to all and hoped you all had a great day.

I try we've got a lot more to go.

This hasn't scratched the surface.

Nice dip here loadimg tomorrow

Unless your TSLA and a host of others, ofcourse

Investors do not like financials.

Listen. You have had a couple opportunities to buy at $3. Then a run up to $15 and $8.

Would be nice to see 15 again and silver topping 20.