News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Saudi Arabia as a potential coal user?

Saudi Arabia, of all places, was apparently looking to displace some of the crude oil they burn for power generation with coal (https://ssrn.com/abstract=2749596). They have no coal domestically, and would have to import from other country. What's the potential of this? It seems economical when oil is valued at market prices and without any carbon prices.

If they care about their carbon emissions pledges post COP21, I would think they may forgo its import.

Biggest US coal plant closures of 2013

http://www.mining.com/biggest-us-coal-plant-closures-of-2013-87594/?utm_source=digest-en-coal-131223&utm_medium=email&utm_campaign=digest

Ana Komnenic | December 18, 2013

US coal plant closures

It's no secret that the US is abandoning coal in a big way: Over the next decade, US power companies have formalized plans to permanently retire nearly 28,000 megawatts (MW) of coal-fired generating capacity.

According to a report from SNL Financial, by 2015, US power plants will have to comply with the Environmental Protection Agency's (EPA) 'Mercury and Air Toxics Standards' which sets limits on plant emissions.

Coal-fired power plants – the biggest source of US electricity generation – are hit particularly hard by these standards. As a result, companies have been gradually retiring non-EPA-compliant plants, with the biggest spike in closures expected between 2014 and 2016.

Surprisingly, the pace of retirements has slowed in 2013 compared with 2012 when 8,800 MW of coal capacity was permanently shuttered.

This year's, the US will forsake just under 6,000 MW of coal power – 34% less than the previous year.

Source: SNL Energy, Aug 2013 | Map credit: Whit Varner

Here are the biggest US coal-fired power plant closures of 2013, grouped by company and based on data compiled by SNL Financial.

1 – FirstEnergy Corp

FirstEnergy Corp retired the largest amount of coal power in 2013 in terms of megawatts. By closing its Hatfield's Ferry Power Station and Mitchell Power Station in Courtney Pennsylvania, the company took nearly 2,000MW of coal out of the US power mix. In total, about 380 employees were affected, according to a FirstEnergy news release. The company decided to shutter the plants because the cost of EPA-compliance was too high.

2 – Duke Energy

Duke Energy – the largest electric power holding company in the US – shut down three coal units in North Carolina this year, totalling 1,342MW. Among the closures was Duke's first large-scale power plant, the 256-megawatt Buck Steam Station in Rowan County which began operating in 1926.

3 – Southern Company

Through its subsidiary Georgia Power, Southern Company shuttered two units of its Harllee Branch power plant as Georgia Power shifts toward nuclear power, 21st-century coal technology, natural gas and renewable energy. Combined, the units produced about 500MW.

Why Uranium and Coal Rank High for Energy Return on Energy Invested: Thomas Drolet

http://www.theenergyreport.com/pub/na/15729?utm_source=delivra&utm_medium=email&utm_campaign=FINAL+TMR+12-3-13

Coal Market Recovery To Boost Alpha Natural Resources Stock

http://seekingalpha.com/article/1725882-coal-market-recovery-to-boost-alpha-natural-resources-stock?source=google_news

Alpha Natural Resources (ANR) is a diversified coal producer with operations in Powder River Basin, Central Appalachia and Northern Appalachia. The company's earnings are sensitive to both thermal and met coal operations, as it produces and sells both thermal and met coal. The company has been going through difficult times due to soft coal market conditions, and has struggled to post a healthy financial performance recently. Due to the tough business conditions being faced by the U.S. coal industry, coal companies have lost a significant amount of market capitalization in the recent past. ANR's stock is down 38% year-to-date. Despite the ongoing soft coal market conditions, I believe the stock has the potential to offer investors attractive returns once coal markets strengthen. ANR has been improving upon its cost structure to support its feeble bottom line results. Also, the current depressed valuations and strong liquidity position make me bullish on the stock.

The U.S. coal industry has been going through tough times due to weak economic conditions, lower natural gas prices and an unfriendly political environment towards coal consumption. Also, over supplied coal markets have led to weak coal prices.

As business conditions for the company remain tough, it has been working to reduce its costs to support its bottom line results. ANR is committed to lowering its Western operation cost by nearly 3% to $10-$10.50 per ton. Also, to preserve cash and strengthen its liquidity, in the recent third quarter, the company lowered its capital expenditure (CapEx) by $25 million for the full year (2013). According to the last earnings release, ANR's liquidity stands at $1.9 billion, out of which $1 billion consists of cash and marketable securities. The healthy liquidity position bodes well for the company, as it provides a cushion to survive through the ongoing tough business conditions. Also, the company does not have any long term debt maturity until 2015.

As the company has been working to control its operations and capital expenditures, these efforts will help the company preserve cash to survive the current tough business conditions. According to BB&T Capital analyst, Mark Levin, ANR has 20,000 acres of the Marcellus Shale that the company can sell to improve its liquidity position. If the company plans to sell the property, it can generate $100 million-to-$140 million. Even though the sum is not that significant, it will certainly improve the company's financial flexibility to some extent.

An important driver for the company's future earnings potential remains a recovery in met coal prices. Met coal prices are likely to improve in the future, as more production cuts will be announced and demand will strengthen. Lately, met coal prices have improved, as the spot met coal price has increased 20% since July 2013. Also, the met coal benchmark price for the ongoing fourth quarter increased 5% QoQ to $152 per ton. I believe we will witness further improvement in coal prices, as more production cuts will be announced. ANR has already announced to reduce its annual met coal production by 1 million ton, in response to weak market conditions. ANR might announce further production cuts in the upcoming earnings releases to rationalize the over supplied coal markets. ANR is scheduled to announce its 3Q2013 financial results on October 28, 2013.

Conclusion

I believe, ANR has the potential to benefit from an upside in coal prices and demand. Also, ANR remains a good investment option for investors to play a coal market rebound, as the stock is currently trading at depressed valuations; it has Price/Sales of 0.20x and Price/Book of 0.25x. Moreover, ANR's cost control measures and strong liquidity position bode well for the stock price. Therefore, I reaffirm my bullish stance on the stock.

EPA's new carbon rules hurt coal, could accelerate shift to natural gas

Both critics and supporters of the new EPA draft regulations on CO2 emissions agree on one thing: This will be the final blow to many proposed coal plants.

The truth is, U.S. coal generation already was in decline not because of climate regulations, but because of good ol' free-market capitalism; the boom in natural gas production has dramatically increased supplies, sent prices plummeting and prompted a shift away from coal.

Among potential long-term winners: U.S. nat gas drillers such as CHK and XOM, drilling services firms such as HAL and BHI, pipeline companies such as SE and KMI, makers of gas-fired turbines such as GE and SI, power generators such as NRG and CPN if electricity prices rise.

Likely losers: Coal appears headed for a decline, and companies with large Appalachian operations such as JRCC and ANR could suffer most as more coal comes from cheaper-to-access deposits in the Illinois Basin and Wyoming; big industrial companies, which have used low U.S. power prices as a competitive advantage, are concerned.

ETFs: KOL, IDU, PUI, XLU, VPU, RYU, FXU, PSCU, UPW, SDP, UTLT.

EPA to set carbon limits on power plants

http://seekingalpha.com/currents/post/1290532?source=email_rt_mc_readmore

The Environmental Protection Agency is scheduled to today unveil restrictions on carbon emissions for new power plants, a key part of President Obama's policy to fight what many see as global warming.

The EPA will reportedly set CO2 limits at 1,100 pounds per megawatt hour for coal plants and 1,000 pounds for most natural gas plants. To meet those restrictions, coal plants would have to capture and store 20-40% of their CO2 emissions using technology that isn't yet being deployed on a commercial scale. The industry argues that the work would be so expensive that it would preclude the building of new plants.

More far-reaching limits for existing facilities are due to be proposed in June 2014.

Companies affected include Patriot Coal (PCXCQ.OB), Alpha Natural Resources (ANR), Arch Coal (ACI), Peabody Energy (BTU), James River (JRCC), Cliffs Natural (CLF), Rhino Resource Partners (RNO), CONSOL Energy (CNX), Oxford Resource Partners (OXF), Walter Energy (WLT) and Natural Resource Partners (NRP).

ETF - KOL.

King Coal: Industry Rebound Hinges On Production Cuts

http://seekingalpha.com/article/1661882-king-coal-industry-rebound-hinges-on-production-cuts?source=email_stocks_and_sectors&ifp=0

U.S. coal companies have been going through tough times, mainly due to oversupplied coal markets, weak economic conditions and lower prices for natural gas. However, I think the worst is already priced in for U.S. coal stocks and the only direction to go from here is up. In recent times, I believe excess supply in coal markets remains the most important factor that has led to lower coal prices and weak market conditions. For a recovery in coal prices, coal producers need to address the problem of an oversupplied coal market.

Lower Production Costs and Depreciation of Australian Dollar Has Kept Markets Oversupplied

To balance demand and supply in the coal markets, coal production cuts are essential. Two of the leading U.S. coal companies, Arch Coal (ACI) and Alpha Natural Resources (ANR), have already made plans to lower their production in response to depressed coal prices. ACI has idled several of its met coal mines, lowering its total met coal production by almost 2 million tons on an annualized basis. Earlier this quarter, ANR also announced plans to reduce its annual met coal production by 1 million tons. In the last two months, since the 3Q 2013 benchmark price settlement, approximately 6.5 million tons of coal production has been taken off the market. Analysts believe that to balance demand and supply in coal markets, additional and aggressive production cuts, between 15 to 25 million tons, are required.

Production cuts have been slow and less than expected in response to weak coal prices. Lower production costs and depreciation of the Australian dollar are limiting production cuts and quick price recovery. In 1H 2013, an improvement in the cost structure of the coal industry, of almost 8%-9%, as compared to the corresponding period last year, has kept coal markets oversupplied.

Also, the Australian dollar has depreciated 16.5% YTD, which has created a new headwind for U.S. met coal producers. As coal trade around the world is transacted in the U.S. dollar, Australian producers are getting paid in the stronger U.S. dollar which has offset the impact of a decrease in met coal benchmark prices of almost 16% for 3Q 2013 as compared to 2Q 2013. As currency movements offset the impact of lower coal prices, and Australian producers hardly lost any revenues, this has kept coal supply flowing, keeping coal markets oversupplied.

Excess coal supply in markets is not only due to international coal producers but also because of U.S. coal producers. In the recent second quarter, coal production at two major met coal mines in Alabama, mine No. 4 and No. 7, of Walter Energy (WLT) increased. In the recent second quarter, production at mine No.4 was up 80% YoY, while WLT mine No. 7 produced 1.4 million tons which was its highest output since 1983.

The following chart, published by the Energy Information Administration (EIA), displays that in recent months production cuts in the U.S. have been slow in response to weak coal prices.

(click to enlarge)

Source: eia.gov

Conclusion

As we move into the second half of 2013, I believe that aggressive production cuts are required to eliminate the excess supply in coal markets and for a recovery in coal prices. ACI and ANR have lowered their production in reply to the low 3Q 2013 benchmark price, but lower production costs and a weak Australian dollar have kept markets oversupplied. In the future, production cuts will determine the magnitude and timing for a recovery in the coal markets. As more production cuts would flow through the markets I believe coal prices will continue to move higher.

$WLB - Coal Without The Risk

Jhttp://seekingalpha.com/article/1585562-coal-without-the-risk?source=email_authors_alerts&ifp=0

Recently, I haven't been pointing out any near-term buying opportunities in the coal sector. Natural gas has been heading the wrong way, and simultaneously we've seen other significant emerging threats to the sector including a potential political drive to punish coal.

With these headwinds and coal companies carrying significant debt loads, it gets too risky to try and bet on a cyclical turnaround in coal. However, there might be a chance to get coal exposure with much lower risk and at a sensible valuation. The company I'll be talking about today, might be that chance.

Westmoreland Coal (WLB)

Westmoreland coal is a medium-sized coal company operating 6 surface mines in Montana, Wyoming, North Dakota, and Texas. The map below, from a company presentation, shows how these are positioned.

(click to enlarge)

Additionally, also shown in the map (in green), WLB operates a 2-unit coal-fired power plant with a 230MW capacity.

WLB's uniqueness starts here. With all mines being surface mines, low mining costs are already a certainty. Coal from these Western and PRB (Powder River Basin) locations is significantly cheaper on a per BTU basis. It's thus much less vulnerable to substitution by natural gas. The following chart from the same presentation tells us how it's positioned, cost-wise, versus other sources of U.S. coal:

(click to enlarge)

It's thus no surprise that WLB didn't suffer tremendously from natural gas substitution. After all, even in the darkest days of cheap natural gas during 2012, Wesmoreland's coal was still competitive:

(click to enlarge)

Westmoreland's competitiveness and stability doesn't end with per BTU cheapness, though. A further factor helping WLB happens due to WLB's mines' location, ensuring further cost advantages:

(click to enlarge)

One of WLB's mines has a significant shortened route to its main customers through rail. Another has the customers nearby and can service them with trucks, and finally 4 of the mines actually have the customers at mine-mouth, where these are fed through conveyor belt. Transportation costs are the main problem that PRB coal producers face, and for the most part WLB has these completely covered.

Finally, WLB's main customers are tied to it through long-term cost-plus or cost-indexed contracts. Cost competitiveness and these contracts ensure a rather low earnings volatility and low risk. Quite unlike most other coal operators.

(click to enlarge)

What does this all mean?

Overall, it all means a much more stable financial performance. Less risk, and revenue/EBITDA charts heading the right way, up and left.

(click to enlarge)

Even during 2013, in spite of an unfortunate event at one of WLB's plants, WLB kept its 2013 EBITDA guidance at $110-$120 million (what follows is from WLB's Q2 2013 earnings report):

"Unfortunately, Unit 4 at the Colstrip plant experienced a major equipment failure on July 1st and this unit is estimated to be down for at least 6 months. We anticipate that this will negatively impact our EBITDA in the second half of the year, but still expect 2013 EBITDA to fall in the range between $112 and $120 million, consistent with the guidance given last quarter. Our ability to maintain our guidance is, in part, due to the limited downside provided by our cost recovery business model."

This stable and cash-generative performance, on the other hand, is allowing WLB to quickly pay down its indebtedness, further reducing risk.

(click to enlarge)

Indeed, at the end of Q2 2013, WLB had already brought its net debt/EBITDA ratio down to just 2.5 times.

What does this all cost?

This brings us to another crucial matter. How much does this interestingly positive coal performance cost to an investor? It turns out it's massively cheap, when compared both to coal, and non-coal, companies.

WLB has a market capitalization of $184.3 million (at $12.71 per share). It carries net debt as of Q2 2013 of $299.6 million. This gives WLB an enterprise value of $483.9 million. At the midpoint of 2013 EBITDA guidance, the EV/EBITDA is thus a low 4.2 times. 4.2 times EV/EBITDA is low on absolute terms and relatively, when compared with other much riskier coal plays such as Arch Coal (ACI).

This profitability and cash generation is overshadowed by a high price/earnings ratio, due to WLB not yet being bottom-line profitable. Profitability is hindered by the debt load and resulting high interest costs. Given the high interest costs and falling leverage, it would seem possible for WLB to refinance these liabilities at a lower cost, with an immediate positive impact to profitability. Either way, in 2014 consensus estimates point towards an EPS of $1.01, giving it a 2014 P/E of 12.6.

Still, the very low EV/EBITDA is the main reason to believe WLB is very cheap from a valuation standpoint. Deleveraging will help both bottom-line profitability and equity, as it's likely that the EV/EBITDA won't trade much lower than where it stands now, so any deleverage is likely to be compensated by equity trading higher.

Acquisition

As a tribute to WLB's management, WLB undertook an acquisition - but it didn't do so during a market peak, like Arch Coal did when acquiring ICG. Instead, WLB acquired the Kemmerer mine for $179 million during one of the warmest winters on record. This allowed WLB to add another mine following its operating model (customer at mine-mouth) for a very sensible price, leading to a low EV/EBITDA acquisition multiple.

The Kemmerer mine added $43 million to WLB's 2012 EBITDA, so the effective EV/EBITDA multiple on the acquisition was also 4.2 times. Meanwhile, WLB has been able to produce measurable improvements in this acquired mine.

(click to enlarge)

The main problem

Not everything regarding WLB smells like roses, though. As always, there are some potential problems. The main problem regarding WLB rests on post-retirement pensions and health promises. These are recognized in the balance sheet, but lead to an ugly negative shareholder equity position of -$281.6 million.

This equity position can delay both a cheaper refinancing of WLB's debt and dividends. This is the one thing that's not to like regarding WLB.

Conclusion

Westmoreland Coal represents a very interesting operating model in the coal space. It's a low cost producer of sub-bituminous and lignite coal with added transport advantages, together with long-term contracts ensuring lower earnings volatility.

This lower-risk coal producer is available for a very low valuation, just 4.2 times EV/EBITDA. It thus represents a better way to get coal exposure than the other more-speculative coal producers.

There are also signs of a competent management team, in that it undertook an acquisition at the right timing, instead of the usual "buy at the peak" that's so common to see. This gives added confidence to an investor in WLB.

On the negative side, WLB still carries significant retirement and health-benefit liabilities and those lead to it having negative shareholder equity, which is never pretty and might make it harder for present shareholders to reap benefits in the short term.

All in all, WLB seems like an excellent buy, especially for those seeking coal exposure after the sector has been so punished.

$WLT - Buy This Coal Miner At A Deep Discount

http://seekingalpha.com/article/1547142-buy-this-coal-miner-at-a-deep-discount?source=email_stocks_and_sectors&ifp=0

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More...)

By Adam Fischbaum

Beleaguered shareholders of this coal miner probably feel like Lee Dorsey in the classic 1966 song "Working in the Coal Mine":

"Lord! I'm so tired! How long can this go on?"

That's a good question. It's been a wild ride for Walter Energy (NYSE: WLT) over the past seven years.

The share price is lower than it was during the apex of the financial crisis. But while there was a massive sell-off of all types of assets in 2008 and 2009, current conditions seem much more stable.

So what gives?

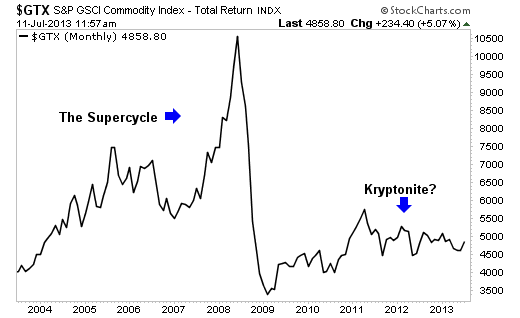

The End Of The Supercycle

With explosive economic growth in emerging markets such as the BRIC nations (Brazil, Russia, India and China) has come a rapid escalation in commodity prices based on what has seemed like an insatiable need for raw materials. Commodity producers and investors have enjoyed very good returns. How good? This 10-year chart of the S&P GSCI Commodity Index says it all.

But these days? Not so much.

As the U.S. dollar strengthens, commodity prices (contracts are priced in dollars) soften internationally by sheer market mechanics.

However, the psychological reasons for the downturn stem mainly from the fear of an economic slowdown in the emerging markets (primarily China) and the continued weakness in global demand due to the slow recovery in the U.S. and the persistent malaise in the eurozone economies.

But what does all of this have to do with a coal producer in Birmingham, Alabama? Plenty.

The Other "Clean Coal"?

An important input commodity, coal -- especially U.S.-produced coal -- has seen its price rise and fall violently in recent years. The first part of the 21st century saw thermal coal prices rise nearly fourfold from around $40 per short ton to $140 in 2008, which coincided with the global financial crisis. Since then, prices have settled back to around $55 per short ton.

In the industrialized world, coal is primarily used for two things: as fuel to help generate electricity and to make coke for steel manufacturing.

A large, fast-growing economy such as China uses a lot of coal for both purposes. However, China is also the world's largest coal producer, with the United States a distant second.

Should a slowdown in China affect what happens to coal domestically? Not really, but federal government regulation can.

Since both Bush administrations and the first Obama administration, the U.S. has had virtually no concrete energy policy. It's no secret that the current administration is no fan of coal from an environmental standpoint.

Compounding those worries, large power producers have switched en masse to natural gas as a cheap, clean fuel source. Obviously, that doesn't help prop up prices. So it makes sense that the stocks of domestic coal producers have been beaten up over the past few years.

However, Walter produces primarily high-quality metallurgical coal that is used in steelmaking. Is the market throwing the baby out with the bathwater?

Buried Treasure

The company's numbers look terrible: negative earnings for 2013 with an analyst consensus of a loss of $1.43 a share; weak Chinese demand (although China is a large coal producer, they produce very little high-quality metallurgical coal); and coking coal prices down 18% to a recent price of around $140.

To give the market even less confidence, Walter recently postponed proposed refinancing of $1.6 billion in term loans, citing market conditions. Most investors wouldn't touch this idea with a 10-foot pole. But look beneath the surface.

Walter Energy is in a fairly simple business: It owns and produces a tangible asset. Conservative estimates put Walter Energy's tangible book value at around $16 a share. Much of that is tied to the company's coal reserves (coal in the ground). That wasn't a big deal when shares were trading north of $100, but with shares staggering around $11.50, it's a different story -- that's 45% upside. The value is literally buried in the ground. But the story gets better.

As far as the metallurgical segment -- Walter's bread and butter -- goes, demand has stabilized, albeit at lower levels. According to the U.S. Energy Information Administration, coking coal domestic demand for 2013 should slip about 1.4% from last year, to 20.5 million tons. Not a disaster.

Imports are a different story. Last year, import demand stood at 125.7 million tons. This year's forecast is pretty grim at 107.1 million tons, a 14.8% drop. However, the 2014 forecast for coking coal imports appears stable at 108.4 million tons. A modest increase of just 1.2% leaves some room for an upside surprise.

As far as Walter Energy is concerned, the picture, believe it or not, is getting brighter. Forget about 2013: Sales should come in at around $2.1 billion versus $2.5 billion last year, which would be an ugly 16% drop. However, forecasts for 2014 call for sales of $2.3 billion, which would be an impressive 9.5% improvement over 2013.

Cash flow is also improving. After a negative 98 cents per share last year, free cash flow has turned positive to about 48 cents per share. That's expected to climb more than 170% next year to a projected $1.31 per share. The company will accomplish this through tighter capital controls and eliminating the dividend.

While I normally don't like to see dividend cuts, this is necessary for the survival of the company and actually adds more value to a deeply undervalued stock.

Last, the hope of all stock investors: Walter Energy is rumored to be a takeover candidate. Whenever certain sectors become depressed, consolidation often follows. Possible suitors have included Alpha Natural Resources (NYSE: ANR), Brazilian miner Companhia Siderurgica Nacional (NYSE: SID) and Warren Buffett's Berkshire Hathaway (NYSE: BRK.A). Based on the unlocked assets at Walter, that idea is right up the Oracle of Omaha's alley.

Risks to consider: By its nature, contrarian deep-value investing is extremely risky. As an investor, you're buying into an idea or event that may very well fail to materialize. As a business, Walter Energy is in a precarious position. One way to protect yourself would be to use a stop-loss order 15% to 20% below your purchase price. Another way would be to use options to hedge your long position. (My colleague Amber Hestla-Barnhart covered this in great depth.) Finally, the coal industry is depressed and very sensitive economically. Continued global economic weakness would likely suppress this idea.

Walter Energy is clearly undervalued, based on the company's improving internals and improving macro conditions, a 12-month price target of $16 would bring the company back to its book value. Shares currently trade around $11.50. This would represent a 40% return. The annual 50-cent-a-share dividend gives the stock a yield of about 4.4%. Don't count on it being that high forever, but this will help the company in the long run.

$JRCC - James River Coal: How Its Debt Swap Affects Valuation And Bankruptcy Risk

http://seekingalpha.com/article/1462851-james-river-coal-how-its-debt-swap-affects-valuation-and-bankruptcy-risk?source=email_rt_article_readmore

... "James River Coal has continued to make impressive strides to improve their balance sheet, reducing their long term debt load by around $180 million over the last year due to these note exchanges plus additional repurchases. The current note exchanges somewhat limits the maximum upside due to dilution, but also makes James River Coal more valuable in a moderate recovery scenario due to the reduced debt loads. However, their situation is unchanged if the metallurgical coal market fails to make a meaningful recovery. In such a scenario bankruptcy remains a serious possibility in 2014, although management has proven to be resourceful in managing financing. James River Coal remains a high risk and a high reward stock, although with slightly reduced reward now, and reduced long-term risk if they can weather the next year or so." ...

$JRCC - An Update On James River Coal's Risk

http://seekingalpha.com/article/1265061-an-update-on-james-river-coal-s-risk?source=email_rt_article_readmore

... "We can draw three main conclusions from this work:

First, the Z-Score would have been useful to predict James River's bankruptcy back in 2003;

Second, the Z-Score would have been useful to show, in May 30 2012, that James River's near-term solvency risk was similar to that of Arch Coal and Alpha Natural Resources and much lower than that of Patriot Coal. This would have been useful both to avoid Patriot Coal's demise, and to take some temporary long trades in JRCC;

Finally, now we can now conclude that James River Coal risk is greatly increased and indeed, if the coal market does not recover, James River might at some point face solvency risk. It would thus perhaps be advisable not to take long trades in it.

On a side note, James River Coal management of working capital still seems sound enough that very near-term insolvency is not yet at hand. Indeed, James River still holds $127.4 million in cash plus $36.5 million in restricted cash. Still, I believe the increased risk at this point should override speculative long endeavors." ...

Domestic Coal Investments

http://www.energyandcapital.com/report/domestic-coal-investments/876

... "In 2004, coal was a major part of U.S. electricity generation, accounting for 51% of all generated power. The U.S. was one of the largest producers of the resource, second only to China, and though it was a top ten coal exporter, six other nations preceded it. Between 2005 and 2010, only 5% of domestically produced coal was exported.

But last year, coal-generated electricity dropped to 42%. The U.S. became the fourth-largest coal exporter, doubling exports from 5% to 10% of domestically produced coal.

The thing is, the U.S. has a lot of coal. But environmental concerns over the carbon emissions that come from burning fossil fuels like coal have sparked rounds of regulations and restrictions.

In March 2012, an Environmental Protection Agency (EPA) ruling put a limit of 1,000 pounds of CO2 per megawatt-hour on output-based emissions, requiring coal-fired plants to add enough carbon-capture and sequestration technologies to reduce their emissions output by 50%.

And though around 70% of U.S. coal plants are more than thirty years old, new ones aren't being built. With ever-tightening regulations in place, it just isn't feasible.

This year, another competitor factored in. Natural gas prices fell below $2 per mmBtu for the first time in ten years.

Unlike the use of coal, the use of natural gas has been lauded, particularly when it comes to emissions reduction. By the end of 2012, U.S. carbon emissions are expected to have fallen to 5.2 billion metric tons – down from a high of 6 billion metric tons in 2007 and moving ever closer to the 1990 level of 5 billion metric tons—a drop that has been attributed, in large part, to a switch by utilities and power companies from coal to the much cheaper, much less regulated natural gas.

Coal consumption has taken a hit, and with increased regulations and alternative power sources taking its place, it seems U.S. coal is headed out.

But don't give up on the sector too soon, because there are plenty of reasons for it to keep on going...

We Want Coal!

Just because coal demand is beginning to wane in the United States (and I said beginning – it still accounts for almost half of electricity generation) doesn't mean that the rest of the world has decided to reduce consumption.

First of all, natural gas may be cheap right now in the United States, but that doesn't say anything for other nations. Though it's a topic of discussion, the U.S. still doesn't export any of its cheap LNG abroad. And natural gas prices are as much as three times higher than U.S. prices in some parts of the world, so in those countries it's not displacing cheaper coal.

Second of all, developing nations have a growing electricity demand. Nations like China, the world's largest importer of coal, and India, the world's fourth-largest, have populations much more massive than the U.S. and require higher volumes of resources to even brush close to the demand level.

In 2011, the U.S. didn't even make the top ten for highest percentage of electricity generated from coal. South Africa had the highest percentage with 93%; Poland followed with 90%. China received 79% of its electricity from coal and India, which has been facing massive power outages and is still unable to provide power to all of its citizens, uses the resource for 69% of its power.

It's possible that nations like India could increase their coal consumption in years to come; after all, Indian citizens are demanding power the utilities can't provide.

The U.S. and China are still the world's biggest producers of the resource, with China taking the lead. Other major producers are India, Australia, Indonesia, Russia, South Africa, Germany, Poland, and Kazakhstan.

But China burns much more coal than the U.S., so it's also the biggest importer. The U.S., on the other hand, sends this production back out in exports.

Even if domestic demand is waning, exports are rising. After a decade steady at 5%, exports jumped to 10%.

Though the domestic coal market is not what it once was, the U.S. still has plenty of the resource, and there's always somewhere for it to go.

Where to Profit

Many domestic coal companies are involved in supplying the product for these rising exports. Some of the biggest even have headquarters in other nations, dealing on five or six continents.

Peabody Energy Corporation (NYSE: BTU)

Peabody is the largest coal company in the world, serving 25 nations and boasting over 9 billion tons of proven and probable reserves.

Headquartered in St. Louis, Missouri, the company also has offices in China, Australia, the UK, Singapore, Indonesia, Germany, and the U.S.

It's mining interests are located at 29 locations in the U.S. and Australia, and it has direct access to Asian and European markets with its international trading headquarters.

Last year it secured or advanced joint ventures in Australia, China, Mongolia, and Indonesia, bringing in revenue over $7.97 billion.

Shares lost 31% over the first six months of the year, when natural gas prices hit their cheapest. In the three months following, however, they jumped back up 19%.

Arch Coal (NYSE: ACI)

Arch Coal is one of the five largest coal producers in the world. The company has mines in Wyoming, Utah, Colorado, Illinois, West Virginia, Kentucky, Virginia, and Maryland, accounting for 15% of the nation's total coal production.

Arch Coal's business is focused on providing low-sulfur and cleaner-burning coal. Also headquartered in St. Louis, Missouri, the company has customers on five continents and sold 157 million tons of coal last year.

It has an annual revenue of $4.5 billion, with $4.58 billion in debt and $512 million in cash.

The company's shares lost 53% over the first ten months of 2012, but between July and October, shares picked back up again, gaining as much as 31%.

Arch Coal received the Conservation Legacy Award from the National Museum of Forest Service History in September for “outstanding actions” in restoring operating locations.

CONSOL Energy Inc. (NYSE: CNX)

CONSOL is a unique company in that it is involved in the production of both coal and natural gas—energy sources that, when combined, account for two-thirds of U.S. power generation.

This strategy has helped the company to stay in the energy game even when natural gas prices dipped to become more attractive than coal.

The company is headquartered in Canonsburg, Pennsylvania, and it's one of the nation's biggest coal producers and the largest producer of underground mines, with 96% of its production coming from underground. Its longwall mining technology helps improve production.

CONSOL has 4.5 billion tons of proven and probable reserves, with 18 mining complexes in Kentucky, Ohio, Pennsylvania, Utah, Virginia, and West Virginia. The company's coal production powers 6.5% of the nation's total demand.

The company's shares lost 22% in the first six months of the year, climbing back up 15% in the following three months.

Coal Outlook

The future of coal in the United States is not doomed simply because demand has been decreasing. Though coal prices will likely average $2.40 per mmBtu in 2012, higher than natural gas's low of around $1.80 in April, the EIA estimates that they will only rise to an average of $2.42 per mmBtu in 2013.

Natural gas prices, on the other hand, have not stayed at these ten-year lows they hit in the spring. Prices were back up to around $2.40 per mmBtu by May, and in the beginning of October, they were circling $3.20.

The prices, as with most things, are dependent on demand—and as it starts to get colder and the heating clicks on, demand is climbing. Last winter was unusually mild, followed by one of the hottest summers in recorded history, so the drop in demand, coupled with a rise in production, contributed to the dip in prices.

But once natural gas prices get even more expensive, coal will start to look attractive again. Even if coal's percentage of power generation doesn't hit levels it once touched, coal-fired plants will start up again.

The EIA expects coal production to decline about 6% in 2012 due to the falling rates of consumption, though exports will remain strong through the end of the year.

However, exports could taper off slightly in 2013, the EIA said, if international coal prices fall and demand from China slows, which is likely to happen as a result of slowed growth.

U.S. coal is also dependent on the party in the White House, as was evident from stock trends during the 2012 presidential election.

Following the first presidential debate during the election, where Mitt Romney voiced his support for coal, coal stocks shot up. Arch Coal received a boost of 6.7%, CONSOL Energy jumped 4.9%, Alpha Natural Resources (NYSE: ANR) went up 5.2%, and Peabody Energy moved up 4.2%.

Stocks were also up after the second debate, where Romney again put coal in a positive light. Peabody shares were up 3.63% by the day's close, Arch Coal was up 4.5%, Alpha Natural Resources jumped 8.3%, and CONSOL closed up 2.99%.

Investors showed their faith in both the Republican party and coal after the candidate added his faith in the resource to his energy policy.

But investors seem to believe the Democratic party will hurt domestic coal production. President Barack Obama's crackdown in regulations on the coal industry made the construction of new coal plants extremely difficult. And the Democratic party will likely push to further these strict regulations.

The future of domestic coal lies in the hands of the domestic energy plan. Regulations will play a big role in restricting the domestic use, though international growth could spur domestic production and exports.

Investors should watch the progression of policies here in the U.S. and abroad, as well as coal and natural gas prices, to stay informed on the future of coal.

You can download the PDF version here: Domestic Coal Investments" ...

Excellent boards Tommy. I saw your Potash board too. Great information. Nice going!

Coal mining companies in the USA

http://www.miningfeeds.com/coal-mining-report-united-states-of-america

Coal Mining

http://en.wikipedia.org/wiki/Coal_mining

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |