News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Cisco Systems (CSCO) - Daily Chart

By: finviz | December 18, 2019

Read More »»»

DiscoverGold

DiscoverGold

Cisco stock has been becalmed in 2019 as it retools its networking product line

By: InvestorPlace | December 17, 2019

• Why I Just Bought More Cisco Systems Stock

I recently compounded my biggest investment mistake of 2019 by buying more stock in Cisco Systems (NASDAQ:CSCO).

This has not been a good year for the maker of networking gear. The shares are little changed from where they were a year ago. Over the last six months they have plunged from the high-$50 range to their Dec. 17 opening price of $46.22 per share.

There are analysts warning of dark days ahead. Proceed with caution, says one. Is CSCO the next International Business Machines (NYSE:IBM), asks another? It’s a legacy tech company being left behind, suggests a third.

Why, Cisco has even lost its leadership position in Gartner’s (NYSE:IT) “Magic Quadrant” to privately held Aruba Networks.

What Cisco Is Doing

The story CEO Chuck Robbins had been spinning, between fawning interviews about his upbringing in the Atlanta exurbs, is that Cisco wants the regular income of software subscriptions over the choppy results of hardware wins.

But that’s not entirely true. Behind the scenes, Cisco has been refreshing its main product line for the Internet of Things, a world where wireless connectivity is ubiquitous, and where anything that can collect data uses it.

At the center of it is a chip dubbed Cisco Silicon 1, developed by Leaba Semiconductor, an Israeli company Cisco acquired in 2016.

The chip is at the heart of a “pluggable” optical router that can move 10.8 terabytes of data per second. That’s 10,800 gigabytes, the equivalent of 25,000 feature films. This will connect to a new standard dubbed OpenRoaming, which can log devices to Wi-Fi 6 services automatically. The company has also been remaking its monitoring software.

Cisco is also buying Exablaze, whose low-latency routers are built with field programmable gate arrays, hardware pre-loaded with software. Exablaze has been winning traction in stock trading and other financial niches. It’s Cisco’s sixth acquisition this year.

Better Days Ahead

Bears have been comparing Cisco with companies that missed the cloud like IBM, Oracle (NYSE:ORCL), and with Intel (NASDAQ:INTC), which missed the mobile revolution. But as its recent product announcements show, Cisco has not been left behind in the networking arena.

The machine networking revolution has only been delayed over concerns about data privacy and whether computers can be trusted. There has been little incentive for companies to move away from the cloud-and-device paradigm, which continues to deliver growth and profits.

The result, assuming that Cisco isn’t blowing smoke, is that it looks like the rarest of birds in technology — a bargain. The trailing price-to-earnings ratio is 18.4 and the yield on the 35 cent per-share dividend is 3%. Cisco earned $2.63 per share over the last year, so that dividend looks sustainable.

Under Robbins, who became CEO in 2015, succeeding industry legend John Chambers, Cisco has been managed for income rather than big capital gains. The dividend has nearly doubled. Until this year, the stock was averaging a 15% gain per year, in line with other S&P 500 stocks.

The Bottom Line on Cisco Stock

Cisco stock is not for everyone.

It’s not a “high beta” name. It won’t outperform the market during boom times. It’s a conservative investment for those who want to protect what they have and earn a modest income.

My personal portfolio still has some risky assets in it, as I’m still not feeling my age (I turn 65 next month). But I need downside protection. I’m too old to start over.

Cisco is part of that downside protection. I think it’s ready for the next technology revolution, and meanwhile it should continue to perform. There are a lot of stocks I’ll sell ahead of it.

Read Full Story »»»

DiscoverGold

A Billion-Dollar Bet Could Be the Spark Cisco Stock Needs to Move Higher

By: InvestorPlace | December 17, 2019

• Several years in the making, this move is great for Cisco stock

Cisco (NASDAQ:CSCO) needed a spark to get Cisco stock moving again. The company’s December 11 announcement of its ‘Internet of the Future’ technology strategy could be just the ticket.

Cisco shareholders have a year to date (through Dec. 12) total return of 8.6%, less than one-third the performance of the U.S. total market.

Although the announcement failed to move CSCO stock immediately, the news it would begin selling networking chips to the likes of Microsoft (NASDAQ:MSFT) and Amazon (NASDAQ:AMZN) ought to persuade investors to give Cisco a second look.

Here’s why.

The Big Picture

Rather than blather on about the various tech specifications of the company’s new products revolving around Cisco’s new Silicon One chip series, I’ll focus on how this will change the way it does business.

While Cisco spent five years and more than $1 billion developing Silicon One, it is CEO Chuck Robbins’ vision for the future that makes the announcement so interesting (and possibly, down the road, extremely rewarding for shareholders).

What’s changed?

Well, it will still sell lots of routers and switches, now it will also sell specialized networking chips to power the hardware for Microsoft Azure and Amazon AWS and other operators of big data centers.

Customer Needs and Cisco Stock

But don’t think Cisco is suddenly entering the chip business to take on the Intel’s (NASDAQ:INTC) of the world. It’s merely responding to customer demands.

“We didn’t say, ‘Let’s go build a semiconductor business.’ This was driven because our customers asked us to do this,” Robbins said. “We don’t have a big proactive strategy to build some large-scale semiconductor business.”

“I have to worry about what my customers want. I can’t worry about Wall Street, how they interpret this.”

One thing is clear: the future internet is going to look a lot different than the internet of today. Robbins is merely trying to get a head start on the technology changes required to operate in a 5G world.

“I think the bottom line is we have to embrace every transition, every trend that’s happening,” Robbins said. “If you sit around and deny and hope that things won’t happen, that’s when you die.”

Perhaps this is a bit of blind optimism. Still, for those who’ve followed the company in recent years, its Silicon One architecture represents a significant change in the way it does business.

It is taking a significant risk that it will alienate some of the companies it’s already doing business with, including Intel and Broadcom (NASDAQ:AVGO).

Too Much Power

Raymond James analyst Simon Leopold believes Cisco’s entry into the chip market comes as a result of concerns from Microsoft, Amazon, and the rest of the big data companies that Broadcom’s sway over this market was getting too powerful.

“We think Cisco aspires to address operators’ concerns about Broadcom securing too much market power,” Leopold said in a recent note to clients.

In recent years, Cisco’s acquisitions have pivoted it away from routers and switches toward software and services. The introduction of the Silicon One chip series would be an extension of this move.

Now all Cisco has to do is execute its plan.

The Bottom Line on Cisco Stock

InvestorPlace contributors Ian Bezek and Josh Enomoto recently discussed why Cisco is a great value play.

Bezek believes that except for sales growth, Cisco is an excellent investment. At 13 times forward earnings, Silicon One success could easily translate into a $15 bump over the next 12 months.

Enomoto believes the only thing standing in the way of a higher Cisco stock price is the ongoing trade war with China. Also, election years tend to do funny things to an economy, so that has the potential to act as a significant headwind to its share price in 2020.

However, there’s no question Cisco is one of the cheaper large-cap tech stocks available today.

While I can’t tell you if the latest move from Chuck Robbins delivers the growth Cisco envisions, I can tell you that you don’t get ahead by standing in place.

If you own CSCO stock, this latest move is a major positive for the company. That doesn’t mean it will translate into a higher stock price, but it’s a start.

I’ll continue to watch Cisco’s progress with interest.

Read Full Story »»»

DiscoverGold

7 Greatly Undervalued Dow Stocks for Upside and Dividends in 2020

By: 24/7 Wall St. | December 17, 2019

It has been undeniable that stocks have enjoyed more than an impressive recovery and continued rally to all-time highs in 2019. The Dow Jones industrial average was up about 21% on a total return basis so far in 2019, and that great gain is even less impressive than almost a 27% gain for the S&P 500 and more than 34% gain for the tech-heavy Nasdaq-100 Index. What is now more important than looking backward is looking ahead. That brings 2020 into prime focus.

Investors have a lot to consider as 2020 gets closer. There is an impeachment process, an announced but unsigned phase-one trade deal with China, and an upcoming election that is likely to be quite nasty. There may even be some new tax changes coming in 2020 as well. 24/7 Wall St. has already tracked the forecasts from top firms calling for 3,300 to 3,400 on the S&P 500 in 2020. That would imply another 6% gain or so, without considering dividends on individual stocks.

One thing that is changing ahead is that many investors now believe it’s time to go back to individual picks rather than solely betting on the rising tide of the indexes to lift all ships. Some strategists see value finally winning the day, while other strategists want to be more aggressive. Chasing the stock market for 6% gains after a 200% rally since the change of the last decade might be too much risk for some investors. After all, a rapid change in government policies or an unexpected geopolitical event could do far more damage to the indexes now that they have risen so much.

24/7 Wall St. has identified seven of the 30 Dow stocks to which value investors and others may flock. These are either cheap on a relative valuation basis or they may be cheap against prior highs or against their Refinitiv consensus analyst target prices. We have identified why each name may be too cheap to ignore, but any seasoned investor knows that 1) cheap stocks are cheap for a good reason and 2) that there is no reason they cannot get even cheaper.

Some investors choose to go to the Dogs of the Dow for dividends and value, but this strategy has frequently not performed well. Other investors like to look solely at price-to-earnings (P/E) ratios or other traditional metrics. And some investors just cannot help themselves by looking for Dow stocks that are down handily from their former highs. There is opportunity and risk in any of these strategies, and no investor should buy a stock solely because an analyst, seasoned investor or even a drinking buddy says it’s too cheap to ignore.

If history holds true, some of the down and out Dow stocks are likely to recover. Unfortunately, history also dictates that some of the losers of the Dow are likely to keep disappointing investors and holding back the index’s gains. We have provided some candid criticism on each company, as well as what the implied returns would be, dividend yields and other metrics. Here are seven Dow stocks that are viewed as undervalued for 2020.

Cisco Systems

Cisco Systems Inc. (NASDAQ: CSCO) has been one of the largest leaders in the technology space for years. It has made endless acquisitions and has bought back so much stock over time that some wonder how it hadn’t just taken itself private. Still, Cisco is a slow grower that has a business now more in line with GDP growth than growth of the internet and technology. It also has migrated away from just a sales-stringent environment to more of a recurring revenue model that now includes security and other services more than ever. Cisco has been volatile around earnings, and it has been all but shut out of new business in China, despite having made up with Huawei in years past.

At $46.00 a share, Cisco is down from a 52-week high of $58.26, and its consensus target price is $52.16. That would imply a 13% gain to the analyst’s target, and its shares would have to rise about 27% to hit a new 52-week high. Total return investors can also look at Cisco’s 3.05% dividend yield to add to whatever upside expectations they are looking for.

Read Full Story »»»

DiscoverGold

Enterprise Tech Names Such as HPE and Cisco Are Facing an Existential Crisis

By: TheStreet | December 16, 2019

• Enterprise computing vendors have had a rough year, and the future doesn't bode well for them, either.

The tough year for computer and networking stocks such as Cisco Systems (CSCO), Hewlett Packard Enterprise (HPE), and Pure Storage (PSTG) won’t be quickly remedied in 2019 by anything the companies can do. The fact is, they are up against a broad change in the structure of their markets that is simply unstoppable.

Cloud computing operators Amazon (AMZN), Microsoft (MSFT), and Alphabet’s (GOOGL) Google several years ago became among the biggest buyers of computer equipment in the world. And that’s a problem for Cisco and the rest.

Shares of HPE are actually one of the less-bad performers this year: at least they’re up 22.5%, though that significantly trails the 32% return of the Nasdaq this year. VMware (VMW), a software vendor, is also one of the brighter lights, up 11.7%.

More muted, single-digit percentage gains can be seen at Cisco and at Dell Technologies (DELL), and at storage networking vendor NetApp (NTAP). Several, including Pure Storage, are basically flat for the year. But some newer companies, such as Nutanix (NTNX), which is transitioning from being a hardware vendor to a software company, have had a harder time of it. Nutanix is down 20% this year.

What’s happening to all these companies is a crisis that has been a long time in the making. Their traditional sales to corporations of computers and software as the bedrock of IT systems is being replaced by the cloud.

As more and more companies run their operations inside of the cloud facilities of Amazon and its competitors, the cloud operators have become oligopsonists, meaning a handful of buyers who dominate purchasing (versus oligopolists, in which a handful of sellers dominate.)

Purchases by Amazon, Microsoft and Google replace some of the purchases that used to be made by smaller, individual companies. The shift to cloud is not entirely a zero-sum game: companies will still buy computing equipment, and there is a phenomenon called “hybrid cloud,” in which a company’s IT is split between its own data centers and what it runs in the cloud. That can help to balance things.

But the over-arching trend is for cloud to replace IT buying by companies, and it is playing havoc with the results of the vendors. The concentration of buying by cloud oligopsonists leads to pressure on prices, wild swings in order patterns and ultimately, some contraction in overall orders as cloud vendors either use machines more efficiently or displace some commercial systems with their own home-built computing equipment.

The impact can be seen in the results of Hewlett-Packard Enterprise, which reported fiscal Q4 results last month. Hewlett’s sales growth has collapsed from an increase of 4% in the fourth quarter of last year to a drop of 9% in the most recent quarter. Hewlett says it is adjusting its product portfolio to exit less valuable equipment sales and focus on higher-growth product lines -- what CEO Antonio Neri refers to as becoming a “a more streamlined and focused company.”

But despite growth of 21% in certain newer segments (what Hewlett calls “Composable Cloud” products) and even after backing out the sales of low-end server equipment, sales on an adjusted basis still fell 7% in the quarter.

The best that can be said is that Hewlett is treading water, keeping its head up and not drowning. And remember, Hewlett is actually one of the less-bad examples.

For almost all these companies, the revenue forecasts of analysts have been declining for the past year. Growth for the older companies such as Cisco, HPE, NetApp and Dell is in the low- to mid-single-digit percentage range. There’s simply no growth to speak of. While younger companies such as Pure and Nutanix have double-digit revenue growth to look forward to, estimates have been coming down for them, too.

If one wanted to pick a name that could show upside, it might be VMware, which has projected sales growth of 11.8% for fiscal 2021, is solidly profitable and whose estimates have been on the rise. But Dell is VMware's majority owner, holding 80.5% of the stock. Although VMware is not cheap, per se — it trades for 21 times projected earnings of $7 a share in 2021 — it probably would trade for a bit more if it weren’t getting the customary discount that happens with stocks that are majority-owned by a larger public company.

While VMware may be a special case, the trends at Hewlett and the rest show that what is happening is in the case of the older companies, a vast breakdown in sales, and for younger companies such as Pure and Nutanix, persistent uncertainty in forecast sales. This uncertainty is the effect of the cloud operators’ oligopsony on equipment purchases. It is a years’ long trend, perhaps a decades-long trend.

As such, it is an existential crisis for these equipment vendors. No one knows how they will puzzle their way out of it, and that means the shares will be trouble for investors for the foreseeable future.

Read Full Story »»»

DiscoverGold

Why Old-School Legacy Tech Stocks May Be Big 2020 Winners

By: 24/7 Wall St. | December 13, 2019

Some of the biggest moves in technology this year have been from the new giants in the industry. Apple Inc. (NASDAQ: AAPL) has almost doubled, and there were big moves in the software as a service (SaaS) and cloud computing stocks. So the real question for investors is where the good values are after such a red-hot year.

The answer may lie with the old-school, “legacy” technology stocks, as some of them, while solid this year, certainly haven’t doubled in price. We screened the Merrill Lynch technology research universe for legacy technology leaders that have solid upside potential for 2020. We found five that look like great additions to aggressive growth portfolios, and are all rated Buy at Merrill Lynch.

Cisco

Cybersecurity is a growing silo for this long-time networking mega-cap tech leader. Cisco Systems Inc. (NASDAQ: CSCO) designs, manufactures and sells internet protocol (IP) based networking products and services related to the communications and information technology industry worldwide.

It provides switching products, including fixed-configuration and modular switches, and storage products that provide connectivity to end users, workstations, IP phones, wireless access points and servers, as well as next-generation network routing products that interconnect public and private wireline and mobile networks for mobile, data, voice and video applications.

Cisco cybersecurity products give clients the scope, scale and capabilities to keep up with the complexity and volume of threats. Putting security above everything helps corporations innovate while keeping their assets safe.

Cisco shareholders receive a 3.10% dividend. Merrill Lynch has a target price of $56, while the posted consensus target was last seen at $55.58. The stock closed at $45.67 a share on Thursday.

Read Full Story »»»

DiscoverGold

Why This Analyst Is Staying on the Sidelines on Cisco

By: 24/7 Wall St. | December 12, 2019

Cisco Systems Inc. (NASDAQ: CSCO) has been one of the weakest components of the Dow Jones industrial average so far in 2019, and according to one analyst this might not change anytime soon. A Nomura Instinet report is somewhat ambivalent on the stock despite Cisco’s recent unveiling of a new chipset family.

At its “Future of the Internet” launch event, Cisco unveiled a new chipset family and new operating system. According to Nomura, Cisco’s arguably overdue vision includes a single chipset family and a new software stack, and ultimately integrated optics will be a best-in-class platform across routing, switching and optical markets.

In a daring shift, Cisco will sell components directly on the merchant market. Nomura points out that it is generally skeptical of the link between announced technical leaps and financial performance. However, the firm also acknowledged the broad technical vision, bold new sales motion and strong customer partnership (including webscale) evident in the launch.

Nomura detailed in its report:

Five years of effort led to a chip family with leading performance and power metrics across switching and all routing classes (access, edge, core) for webscalers and operators. Cisco said many thought it impossible. It may well be, at least on a single chip; Cisco will have many variants of the Silicon One family. Nevertheless, Cisco’s suite is a commanding vision. The first chip, the Q100, will power the new Cisco 8000 router, which is due in early 2020.

Accordingly, a single software development kit across the chipset family should reduce future development time and customer operating expenses. Cisco said that it expects 39% lower operating expenditures and a 66% lower total cost ownership from the new 8000. The new software suite, IOS XR7, is different from what runs Cisco’s installed equipment and thus benefits should accrue slowly.

The earliest applications of the Q100/Cisco 8000 appear likely to be within service providers, though Nomura does not expect this to reverse Cisco’s sales declines in its Service Provider segment.

Nomura concluded by reiterating a Neutral rating with a $45 price target, implying miniscule upside from the most recent closing price of $44.28.

Shares of Cisco traded up about 2.5% to $45.40 on Thursday, in a 52-week range of $40.25 to $58.26. The consensus price target is $52.12.

Read Full Story »»»

DiscoverGold

Cisco Systems is Oversold

By: Dividend Channel | December 5, 2019

The DividendRank formula at Dividend Channel ranks a coverage universe of thousands of dividend stocks, according to a proprietary formula designed to identify those stocks that combine two important characteristics — strong fundamentals and a valuation that looks inexpensive. Cisco Systems Inc (NASDAQ:CSCO) presently has an excellent rank, in the top 25% of the coverage universe, which suggests it is among the top most "interesting" ideas that merit further research by investors.

But making Cisco Systems Inc an even more interesting and timely stock to look at, is the fact that in trading on Thursday, shares of CSCO entered into oversold territory, changing hands as low as $43.46 per share. We define oversold territory using the Relative Strength Index, or RSI, which is a technical analysis indicator used to measure momentum on a scale of zero to 100. A stock is considered to be oversold if the RSI reading falls below 30.

In the case of Cisco Systems Inc, the RSI reading has hit 28.9 — by comparison, the universe of dividend stocks covered by Dividend Channel currently has an average RSI of 51.9. A falling stock price — all else being equal — creates a better opportunity for dividend investors to capture a higher yield. Indeed, CSCO's recent annualized dividend of 1.4/share (currently paid in quarterly installments) works out to an annual yield of 3.19% based upon the recent $43.89 share price.

A bullish investor could look at CSCO's 28.9 RSI reading today as a sign that the recent heavy selling is in the process of exhausting itself, and begin to look for entry point opportunities on the buy side. Among the fundamental datapoints dividend investors should investigate to decide if they are bullish on CSCO is its dividend history. In general, dividends are not always predictable; but, looking at the history chart below can help in judging whether the most recent dividend is likely to continue.

Read Full Story »»»

DiscoverGold

Never Confuse the Bottom of the Page With Support

By: David Keller | November 22, 2019

* (Click Read Full Story »»» at the bottom of the page for the charts to appear on the post)

When I worked for a large asset management firm, we had a number of fantastic digital displays that allowed us to view stock charts on a massive scale. The size of the screens made the work of identifying trends and inflection points much easier - and also way more fun.

We often joked that, when a stock would be in an extended downtrend and the price reached the bottom of the monitor, the bottom edge of the display was not a legitimate support level. To phrase it as one of my early mentors once said, “Never confuse the bottom of the page with support!”.

Novice technical analysts will often get excited when a stock price is down, with the hope that they can identify “the bottom” and anticipate an inflection point before it happens. As exciting as that sounds, actually identifying a market bottom as it’s happening is incredibly difficult. Doing it once is coincidence. Doing it consistently across markets and cycles is downright impossible. This is why most long-term technical analysts (as well as quantitative models and hedge funds) employ more of a trend-following or “momentum” approach, with the goal of confirming when a new trend is in place and sticking with existing trends until signals start to suggest otherwise.

This brings me to the chart of Cisco Systems (CSCO), which remained in the mid-$40 range this week. That is down over 20% from its peak of just below $58 back in July.

After trading down to its 200-day moving average in August, CSCO gapped down to find support around $46, which lined up perfectly with a 61.8% Fibonacci level based on the 2019 rally.

The next three months saw Cisco bounce repeatedly off this key support level, with every new retest serving to solidify the importance of this line in the sand.

CSCO finally broke down through that resistance last week, with another gap down to around $44.50. This week saw further distribution, with most days seeing a close lower than the opening price.

At this point, we have a stock forming a consistent pattern of lower lows and lower highs - that is, a downtrend. The relative strength made another new low in recent weeks and continues to slope downward. The RSI is not yet oversold, suggesting there is plenty of potential for further downside.

To summarize, Cisco is in a downtrend with no real technical indication of anything changing soon. And to summarize that summarization, don’t confuse the bottom of the page with support.

RR#6,

Dave

Read Full Story »»»

DiscoverGold

After Cisco Stock’s Post-Results Battering, is it Time for a Long-Term Buy?

By: InvestorPlace | November 21, 2019

A tough macroeconomic environment is likely to make CSCO stock volatile in the short-run

Cisco Systems (NASDAQ:CSCO) stock has been punished since the release of Q1 FY20 earnings results that beat on the top and bottom lines for the quarter, which ended Oct. 26. What’s battered CSCO stock since the Nov. 13 results is management’s forecast for revenue declines in the fiscal second quarter.

So far CSCO shareholders have not had a great 2019. Year-to-date the shares are up about 4%. Let us now take a look if long-term shareholders should consider buying into Cisco stock at current price levels.

Guidance Failed to Impress

Cisco remains is a global heavyweight in the networking and communications equipment market. Revenue and earnings came at $13.2 billion and 84 cents per share, respectively, vs. $13.09 billion and 81 cents per share as expected by Wall Street. During the quarter, revenue grew 1% on an annualized basis.

The group reports revenue under two headings: Product (about 75% of revenue) and Service (about 25%). Cisco makes products and provides services that help customers transport data, voice and video traffic. Under its Product business, Cisco has infrastructure platforms, networking applications, as well as security products. Service revenue comes from providing technical consulting and related support services.

For Q2 the networking giant now expects 75 cents-77 cents in earnings per share and an annualized revenue decline of 3%-5%. Analysts were instead expecting 79 cents in earnings per share and about 2.6% revenue growth. Management’s discussion hinted a decline in corporate tech spending, which investors did not regard as a positive sign for the next quarter.

In late October, rival Arista Networks (NYSE:ANET) also warned about the next quarter as a large customer was cutting orders. Maybe investors should have already expected a similar dismal outlook form Cisco.

Ahead of the after-market Nov. 13 release of the quarterly results, CSCO stock price closed at $48.46. The next day, it gapped down to open at $45.56. On Nov. 18, it saw a recent low of $44.44.

Tailwinds Behind CSCO Stock

Despite worries over the tech market and spending levels, not everyone is pessimistic about the future of Cisco shares. In September, Evercore ISI analyst Amit Daryanani initiated CSCO stock coverage with a price target of $60, citing multiple catalysts that could help the share price go higher.

Cisco, which has long been known for its networking and communications hardware, such as routers and switches, has lately been diversifying into software and cloud support services. Many analysts and investors have welcomed this strategic move that is likely to add revenues, primarily from reoccurring cloud-related subscription services.

The company offers its products and services to a wide range of customers, including service providers, such as telecommunication carriers and and wireless service providers, public sector, and commercial businesses of different sizes.

A recent thesis by Apoorva Parikh of Massachusetts Institute of Technology highlights that “Cisco’s security business segment with over $2 billion in revenue in fiscal 2018, makes Cisco one of the largest enterprise security players in the market.”

Parikh continues, “[c]ybersecurity market is huge. Research firm IDC estimates security solutions spending will hit $92 billion in 2018 and continue to grow at CAGR of 10% to reach over $130 billion by 2022 … Cisco is well positioned to capture this massive market.”

As CSCO’s global geographical reach is rather broad, the company may be spared any further damage that may be caused by the ongoing trade war with China. For example, the company is expecting to triple its India customer base, where about two-thirds of all small- and- medium enterprises (SMEs) have no online presence.

Cisco is Cash Rich

CSCO’s reserves of over $33 billion in cash and short-term investments enables it to be flexible, especially when it comes to potential acquisitions that may help the company increase revenue through software and subscription-based business. During the quarter, management completed the acquisition of customer experience management company CloudCherry and speech recognition company Voicea.

Earlier in 2019, the group bought Acacia Communications for $2.6 billion. Cisco management is hopeful that this purchase will help the group meet customer demand for more robust networks and contribute to revenue growth soon.

All that followed 2018, CSCO had acquired a young start-up, Duo Security, to strengthen its offering of integrated cybersecurity products and solutions to customers, especially in multi-cloud computing and storage environments. Previously, there had been ongoing rumors that Cisco may eventually acquire Red Hat with which it had partnered for many years. However, Red Hat was finally acquired by International Business Machines (NYSE:IBM).

The Q1 earnings statement also showed that Cisco had managed to repay more than $6 billion in debt. Going forward, this debt reduction will translate into less interest expenses.

Despite the strength of Cisco’s balance sheet and the management’s strategic moves to increase the revenue base, it may be several weeks before CSCO stock may stabilize.

Where CSCO Stock Price is Now

If you have not looked at the price chart over the past year, you would not have known that it had been a volatile one for CSCO shareholders. In the past 12 months, Cisco stock is down about 1%.

Yet its 52-week range has been $40.25 (Jan. 24, 2018) – $58.26 (July 16, 2019). CSCO stock is currently hovering around $45.

Although Cisco stock may look quite appealing at this lower price from a fundamental basis, I’m expecting some short-term volatility and profit taking in the broader tech sector.

Therefore, the setback in CSCO shares are likely to continue for several more weeks. Cisco stock may be one of the first tech stocks to test its 52- week low at $40.25 and make a double bottom around that level where it has strong support.

Those investors who pay attention to moving averages and oscillators should note that the technical message has become a “sell.” CSCO shares will need to stabilize and build a base again before a long-term sustained leg up can occur.

Bottom Line on Cisco Systems Stock

Although Cisco Systems stock offers long-term investment opportunities on a strong fundamental basis, rest of the year may bring more volatility in technology stocks like CSCO. However, investors may regard any further decline in the stock price as an opportunity to buy into the shares. I expect Cisco to bounce back from the recent sell-off before too long.

Furthermore, CSCO’s current annual average dividend yield of 3.1% makes it an attractive buy for dividend growth investors. On Sept. 20, CSCO declared a quarterly stock dividend of 35 cents per share, payable on Oct. 23 to shareholders of record on Oct. 4. Cisco stock’s next ex-dividend date is expected in early January 2020.

Read Full Story »»»

DiscoverGold

Cisco accuses three former employees of stealing trade secrets and taking them to Poly

By: Business Journals | November 19, 2019

Cisco Systems has filed a lawsuit against three former employees, alleging that the trio stole thousands of pages of trade secrets on their way to join Poly, a Santa Cruz-based competitor in the audio and video conferencing space.

The San Jose networking hardware giant filed the lawsuit Monday against Poly Distinguished Engineer Wilson Chung, Poly Director James He and Poly Vice President of New Product Introduction Jedd Williams.

Williams declined to comment, and attorneys for He and Chung couldn’t be reached for comment.

Poly spokeswoman Edie Kissko said the company would not be commenting on the lawsuit.

"As reflected in the allegations in the complaint, we took the unusual step of filing a legal case against former employees for egregious intellectual property violations," Cisco spokeswoman Robyn Blum said in an email. "Our goal is to protect our significant (research and development) investments and valuable intellectual property."

Cisco claims that Chung and He, both former high-level engineers in the company’s Unified Communications Technology Group, downloaded thousands of Cisco’s confidential documents related to the design, manufacture, pricing and market opportunities for Cisco products shortly before leaving for jobs at Poly earlier this year.

Both are accused of destroying evidence after Cisco discovered the alleged misappropriation.

Williams, a former Cisco managing director of global collaboration sales who left the company last month after 21 years, allegedly misappropriated confidential material related to Cisco’s sales forecasts and business development opportunities, including spending commitments and potential upsides, immediately before leaving Cisco.

Williams is also accused of proposing to Poly a go-to-market strategy that he called “Project X,” which he had developed at Cisco.

Poly’s stock was trading almost 2 percent lower on Tuesday, closing at $25.76. The company’s shares plunged 25 percent earlier this month after reporting disappointing earnings results. The company has a market cap of just over $1 billion, compared to Cisco at nearly $193 billion.

Cisco’s stock was trading almost 1 percent higher Tuesday, closing at $45.47. The tech giant’s share price has been on a declining trend since July, when shares hit $57.95.

Read Full Story »»»

DiscoverGold

Cisco Shares Look Cheap After Their Selloff

By: TheStreet | November 15, 2019

Cisco shares fell nearly 8% in response to disappointing Q2 guidance. However, I believe that this selloff gives long-term investors a chance to buy shares at a discount.

Cisco (CSCO - Get Report) reported its Q1 earnings after the bell on Wednesday and while the numbers beat on both the top and bottom lines, shares sold off in response to the report due to negative Q2 guidance. The guidance that Cisco gave during its prior quarter sparked a selloff as well.

These negative outlooks are becoming a theme for this company as management continues to highlight macro problems that had led to decreased business and CEO confidence which put pressure on enterprise spend. Investors are fearful of secular pressures leading to a prolonged growth slump for Cisco. This is why the stock is being priced so cheaply.

However, when I look at the underlying fundamentals, I don't see a disaster here. To me, Cisco shares are being priced irrationally low, giving long-term investors a great chance to pick up shares of a blue chip technology name while it's in the bargain bin.

Q1 Results

Cisco's Q1 revenue came in at $13.2 billion, up 2% year-over-year. The company's non-GAAP earnings-per-share came in at $0.84, up 12% year-over-year. For a mature name like Cisco, double digit bottom-line growth is great. But, whether it is completely rational or not, the market places outsized focus on forward growth prospects, which is why the Q2 guidance was the star of the Q1 report.

Cisco guided for year over year revenues declines of 3-5% in Q2. And, they lowered their non-GAAP earnings-per-share guidance range to $0.75-$0.77. At the mid-point of this earnings guidance, Cisco would generate year-over-year bottom-line growth of 4.1%.

During the conference call, management seemed to compound the negative sentiment surrounding the Q2 guidance. Rather than turn the narrative towards the strong margins that the company continues to generate (implying that market share is not being lost) or the fact that Cisco is still on track to meet, and even exceed, its prior guidance regarding its continued transition away from legacy hardware and into the software space, throughout the Q&A session much of the focus was on slowing enterprise spend.

Cisco's non-GAAP total gross margin came in at 65.9% in Q1, up from 64.2% during the same quarter one year ago.

The company continues to believe that software sales will make up roughly 30% of its total revenue pie by the end of fiscal 2020, with upwards of 70% of those sales coming in the form of high margin, reoccurring SaaS based subscriptions.

In recent years, the market has shown a penchant for paying high premiums for companies adopting this more predictable and reliable reoccurring sales model. However, when CEO Chuck Robbins says things like, "We saw some large deals get done but got done smaller," or "And then we just saw deals that slipped, and so we saw little bit of all that," there's no wonder the narrative was negatively skewed.

Granted, I don't want to be too hard on Robbins because he is the architect of Cisco's turnaround towards growth and growth markets. I continue to be bullish on the direction the company is headed. Management appears appears to be bullish too, I just wish they had done a better job of portraying that sentiment during the Q&A session of the conference call.

This morning, Robbins came on air for a CNBC exclusive interview with Jim Cramer and tried to change the narrative.

While noting that it would be impossible to model progress with regard to macro concerns until the outlook on trade is more clear, the did highlighted the fact that Cisco was controlling what it could control in the face of macro headwinds with regard to things like margins.

With regard to the cautious stance of CEOs regarding their capital, Robbins said that Cisco's technology "is fundamental to how they're running their organizations" and "there is only so long that they can actually pause."

Robbins concluded the interview by saying, "Quarters come and go and we're not too worried about it."

At this point, the selloff had already begun and it was probably too late to stave off much of the negative sentiment in the short-term, but I think Robbins is right here and investors who can't see the forest for the trees are running the risk of missing out on a great deal.

Valuation

While it's true that the $0.76 mid-point EPS guidance was below analyst consensus, I find it curious that the stock sold off to 52-week lows on the news. At Thursday's $44.70 share price, Wall Street has slapped a 13.5x forward multiple on shares (based upon the current analyst estimate of $3.31 for full-year 2020 earnings). This is down significantly from the nearly 19x multiple that investors proved willing to pay for Cisco earlier in 2019. It's also below Cisco's 5-year average trailing twelve-month price-to-earnings multiple of 14.1x.

In spite of the top-line weakness, Cisco remains incredibly profitable. During the quarter, non-GAAP operating income totaled $4.4 billion, up 6% year-over-year. Cash flow from operations came in at $3.6b. This was down 5% year-over-year, though the figure includes a $0.4 billion receipt with relation to the Arista (ANET - Get Report) litigation settlement. Normalized with this one-time item in mind, cash flows from operations would have been up 7% year-over-year.

Cisco ended the quarter with $28 billion dollar's worth on cash on the balance sheet. This affords the company continued flexibility in the M&A space and signals more shareholder returns. During Q1, Cisco paid $1.5 billion to shareholders in dividends and returned $768 million in the form of stock buybacks (at an average share price of $48.91). The company has $12.7 billion remaining on its current buyback authorization and I expect to see the company continue to retire shares into this share price weakness.

In today's low interest rate environment, a company like Cisco, offering a 3.1% dividend yield, mid-single-digit earnings growth, and mid to high single-digit dividend growth prospects remains exceedingly attractive.

With the market near all-time highs, it's difficult to find blue chip equities trading with attractive multiples attached to them. Cisco certainly fits this bill. And, due to the company's generous shareholder return policies, investors buying into weakness will be paid handsomely while they wait for the stock to rebound. Cisco remains one of my favorite technology names in today's market. It's a defensive pick in a late-cycle market environment that I feel comfortable holding over the long-term.

Read Full Story »»»

DiscoverGold

Cisco (CSCO) Deja Vu

By: Bespoke Investment Group | November 14, 2019

Call it deja vu, but Cisco (CSCO) is seeing a repeat of its August earnings report. Back in the summer, CSCO beat on the top and bottom line but lowered guidance leading the stock to fall 8.61% the following day. Fast-forwarding to today, CSCO reported after yesterday's close with the same results. The company once again lowered guidance while beating EPS by 3 cents and revenues by $69.4 million. Although the stock's performance in response has not been quite as bad as last time around, CSCO fell over 7% on Thursday. That is the worst single-day performance for the stock since its last earnings report. Two quarters in a row now, CSCO has fallen substantially on earnings. That is quite the difference from the previous four quarters when the stock rose each time.

Last Monday, we highlighted Cisco (CSCO) in a Dividend Stock Spotlight noting that although it has an attractive dividend, the technical picture was mixed with the stock at a bit of a crossroads at the bottom of a longer-term uptrend thanks to a rough-looking shorter term. The past few months' declines have come following the aforementioned earnings report in August and a weak quarter from competitor Arista Networks (ANET) further dampening the outlook for CSCO. These catalysts since the summer in conjunction with today's declines have brought the stock under support between $45-46 and also broken the longer-term uptrend that had been in place over the past few years. Since it's high on July 15th, CSCO has declines more than 22% and shed $42.8 billion in market cap. To put that into perspective, that decline is within $1 bn of the current market caps of Advanced Micro Devices (AMD), Humana (HUM), Progressive (PGR), and Marriott Hotels (MAR).

Read Full Story »»»

DiscoverGold

Cisco confirms fears of a ‘broad-based’ slowdown in tech spending

By: MarketWatch | November 13, 2019

Large enterprises sending expenditures through more processes and sometimes downsizing deals, Cisco executives say, as stock falls in late trading

Cisco Systems Inc. sparked fears of a tech-spending slowdown with its last forecast. With its latest projections, it may have confirmed them.

Cisco CSCO, -5.14% projected that revenue would decline by 5% or more in the current period when it reported quarterly earnings Wednesday afternoon, news that sent shares down by about the same percentage in after-hours trading. In a conference call and interview with MarketWatch, executives described a slowdown that had been confined to smaller parts of the market three months ago suddenly expanding into almost all corners of the world.

“It feels like there’s a bit of a pause,” Chief Executive Chuck Robbins said in the conference call. “We saw things like conversion rates on our pipeline were lower than normal, which says things didn’t close the way we have historically seen it. ... It was really just stuff slipping. We saw some large deals get done, but got done smaller.”

In an interview with MarketWatch following the call, Chief Financial Officer Kelly Kramer said that large businesses were putting purchases through more review processes, meaning orders were taking longer to get done.

“It wasn’t just big deals getting smaller, the buying cycle is lengthening,” Kramer said.

The insights provided Wednesday suggest that concerns are warranted, well beyond Cisco’s near-term future. Cisco has long been seen as a harbinger of potential macro problems for the tech ecosystem, as purchases of large networking equipment largely presage purchases of other equipment and software to use on new networks. A customer base of large companies and governments spread across the globe also make it a useful proxy for tech spending, and top executives have shown a longtime willingness to provide insights on their dealings with customers.

After saying three months ago that spending was slowing from telecommunications clients and emerging markets — especially China, which is not a huge market for Cisco — executives repeatedly described the slowdown as “broad-based.” Kramer told MarketWatch that growth declined in eight out of the top 10 countries in which Cisco sells, and the slowdown in Cisco’s Enterprise and Commercial businesses shows that some of the world’s largest companies are holding the pursestrings tighter heading into the end of the calendar year.

Corporate America is heading toward a new nadir in an earnings recession that could last the entire calendar year, and Cisco’s disclosures on Wednesday suggest that the decline is starting to show up in their willingness to spend, especially on large tech upgrades. Cisco will survive, and its push into more software will soften any blow, but other tech companies may not be so lucky.

Read Full Story »»»

DiscoverGold

Why Cisco Fell Flat in Q1

By: 24/7 Wall St. | November 13, 2019

Cisco Systems, Inc. (NASDAQ: CSCO) released fiscal first-quarter financial results after markets closed Wednesday. The firm said that it had $0.84 in earnings per share (EPS) and $13.2 billion in revenue, compared with consensus estimates that called for $0.81 in EPS and $13.09 billion in revenue. The same period from last year had $0.75 in EPS and $13.07 billion in revenue.

Total revenue increased 2% year over year, with product revenue up 1% and service revenue up 4%. Revenue by geographic segment was: Americas up 4%, EMEA up 4%, and APJC down 8%. Product revenue performance was led by growth in Security, up 22% and Applications, up 6%. Infrastructure Platforms revenue was down 1%.

Deferred revenue was $18.6 billion, up 11% in total, with deferred product revenue up 24%. Deferred service revenue was up 4%.

Looking ahead to the fiscal second quarter, the company expects to see EPS in the range of $0.75 to $0.77 and revenues declining in the range of 3% to 5% year over year. Consensus estimates are calling for $0.79 in EPS and $12.77 billion in revenue for the coming quarter.

Chuck Robbins, chairman and CEO of Cisco, commented:

We delivered a solid quarter against a challenging macro environment. We’re focused on continuing to drive innovation, transform our business and exceed our customers’ expectations.

Shares of Cisco closed Wednesday at $48.46, within a 52-week range of $40.25 to $58.26. The consensus analyst price target is $54.96. Following the announcement, the stock was down about 5% at $45.85 in the after-hours session.

Read Full Story »»»

DiscoverGold

Will Cisco Earnings Give Any Clue to China Trade Talks?

By: 24/7 Wall St. | November 13, 2019

Cisco Systems Inc. (NASDAQ: CSCO) is scheduled to release its fiscal first-quarter financial results after the markets close on Wednesday. The consensus estimates are calling for $0.81 in earnings per share (EPS) and revenue of $13.09 billion. In the same period of last year, the company said it had EPS of $0.75 and $13.07 billion in revenue.

The company previously issued guidance for the fiscal first quarter. Cisco expected to see revenue flat to up 2% year over year and EPS in the range of $0.80 to $0.82. Gross margin was tabbed at 64% to 65% (compared to 63.9% in the fourth quarter of 2019) and operating margin was expected to come in at 32% to 33% (versus 32.6% in the fourth quarter).

The first-quarter outlook reflected little to no growth, and the U.S. trade question with China was unlikely to help Cisco.

In the fiscal fourth quarter, the company’s quarterly results were just barely enough to exceed estimates, but a narrow hit is no different from a big miss these days. For the 2019 fiscal year, sales in the company’s Asia-Pacific/Japan/China business unit rose 3% to $7.85 billion, but fourth-quarter sales were down 4% to $2 billion.

Excluding Wednesday’s move, Cisco had underperformed the broad markets, with the stock up nearly 12% year to date. In the past 52 weeks, the stock was up closer to 3%.

A few analysts weighed in on Cisco ahead of the report:

• RBC has a Buy rating with a $56 price target.

• Piper Jaffray has a Neutral rating with a $51 target.

• Baird’s Buy rating comes with a $54 target price.

• Credit Suisse has a Neutral rating with a $49 price target.

• KeyCorp rates it as Overweight with a $54 target price.

• Goldman Sachs has a Neutral rating and a $48 price target.

• Evercore ISI’s Outperform rating comes with a $60 target.

Shares of Cisco traded up less than 1% to $48.70 on Wednesday, in a 52-week range of $40.25 to $58.26. The consensus price target is $54.96.

Read Full Story »»»

DiscoverGold

Cisco Systems Is Cut to Neutral at Piper Jaffray, Price Target of $51

By: TheStreet | November 11, 2019

The downgrade comes ahead of Cisco's first-quarter earnings on Wednesday.

Cisco Systems (CSCO - Get Report) declined in premarket trading Monday after shares of the maker of networking gear were downgraded to neutral from

overweight at Piper Jaffray.

Cisco is expected to report fiscal first-quarter earnings on Wednesday. Analysts surveyed by FactSet expect the company to earn 81 cents a share in the period on sales of $13.07 billion.

Piper Jaffray analyst James Fish downgraded Cisco to neutral from overweight with a price target of $51, down from $55.

Shares of Cisco fell 1.35% to $48.17 in premarket trading Monday. The stock has risen 12.69% so far in 2019 but has declined 6.87% over the last three months.

The analyst cited "a slowing macro environment across Enterprise and Service Provider," and "cycles hitting a peak earlier this year," for the downgrade. He also cited lack of a near-term catalyst, and risk to fiscal 2020 and 2021 estimates, according to The Fly.

Fish, however, said he sees downside for the stock as "fairly limited from here." Material 2021 catalysts, Fish said, include the rollout of 5G and 400G switching.

Sixteen analysts who cover the stock rate it a buy, 14 have it as a hold, and there are two sells, according to Bloomberg. The average price target is $54.

Read Full Story »»»

DiscoverGold

Cisco (CSCO) Gears Up for Q1 Earnings: What's in the Cards?

By: Zacks Equity Research | November 7, 2019

Cisco Systems, Inc. CSCO is slated to release first-quarter fiscal 2020 results on Nov 13.

For first-quarter fiscal 2020, Cisco expects revenues to grow in the range of 0-2% on a year-over-year basis. The Zacks Consensus Estimate for first-quarter revenues is pegged at $13.08 billion, almost flat when compared with the year-ago reported figure.

Non-GAAP earnings are anticipated between 80 cents and 82 cents per share. The Zacks Consensus Estimate for earnings has been steady for the past 30 days at 81 cents, indicating an improvement of 8% from the prior-year quarter.

Notably, the company surpassed the Zacks Consensus Estimate for earnings in the trailing four quarters, the average beat being 2.02%

Factors Likely to Influence Q1 Results

Cisco’s fiscal first-quarter results are likely to reflect robust adoption of its security solutions, including web security, unified threat, and network security and advanced threat offerings.

Moreover, growing clout of the company’s latest subscription-based Catalyst 9000 switching platform, Cat9K and Nexus 9K is likely to have accelerated Switching revenue growth in the fiscal first-quarter.

Further, strength in company’s Wave 2 offerings and Meraki solutions is likely to have driven growth in wireless domain.

Also, in data-center vertical, momentum in the HyperFlex data-center solution is likely to have continued in the quarter under review, in turn aiding the top-line performance.

Positive trends including, persistent customer shift from 100G to 400G architectures and growing adoption of multi-cloud platforms are likely to get reflected in the company’s fiscal first-quarter performance. Moreover, increase in enterprise spending on cybersecurity and 5G infrastructure network as 5G deployment accelerates, are likely to have favored adoption of Cisco’s offerings in the fiscal first-quarter, in turn aiding the top line.

The company is integrating AI and ML capabilities into enterprise collaboration solutions aimed at increasing productivity of users, and improve engagement. This in turn is expected to have bolstered adoption of Webex Meetings, Webex Devices and Webex Teams, among others, in the first quarter. This in turn is expected to have driven the fiscal first-quarter top line.

Nonetheless, decline in order growth on headwinds pertaining to the U.S.-China trade war and weakness in service provider and enterprise vertical is likely to have affected the fiscal first-quarter top line.

Moreover, increasing investments on product enhancements amid stiff competition from Arista ANET, Juniper JNPR and F5 Networks FFIV in networking infrastructure market is likely to have limited margin expansion in the fiscal first-quarter.

Noteworthy Developments in Q1

During the fiscal first-quarter, Cisco strengthened its collaboration portfolio with latest Webex Control Hub Extended Security Pack featuring robust cybersecurity capabilities. Companies like Wacker Chemie AG and NTT Communications, are looking forward to utilize Cisco’s latest Webex Control Hub Extended Security Pack. The pack offers CASB standard anti-malware features, providing users with data security from malicious attacks.

Cisco is anticipated to boost user engagement and adoption on enhanced data security provisions by integrating its cybersecurity capabilities across Webex portfolio.

Moreover, the company concluded Voicea acquisition. Cisco plans to enrich Webex portfolio with Voicea’s AI-based voice-recognition and transcription capabilities.

Cisco also completed acquisition of CloudCherry, a Customer Experience Management (CEM) company, aimed at enhancing the company’s Contact Center Solutions business.

Zacks Rank

Currently, Cisco carries a Zacks Rank #4 (Sell).

Read Full Story »»»

DiscoverGold

New Meraki Go Networking Solution Delivers a Competitive Edge for Small Business

By: PR Newswire | November 6, 2019

SAN JOSE, Calif., Nov. 6, 2019 /PRNewswire/ -- Cisco Meraki, Cisco's (CSCO) industry-leading cloud-managed IT platform, today launches Meraki Go, a complete line of cloud managed networking products specifically designed to help independent businesses with no IT team transform to better meet the needs of customers and employees. The new Meraki Go network switches and security gateway with an optional security subscription, powered by Cisco Umbrella, are available today on meraki-go.com.

Meraki Go marries Cisco's industry-leading networking hardware, with the power of the cloud, to provide businesses with simple, secure, and mobile app-based control over their network, as well as information-rich business insights.

"The internet has become as critical as having water and electricity, costing businesses dearly in lost sales and customers if it's slow or loses connectivity," said Lee Peterson, Product Manager for Meraki Go. "Every investment a business makes needs to work harder and do more, and Meraki Go provides high performance business networking, plus visibility, control, insights, and analytics that allow owners to make business decisions confidently."

Meraki Go hardware is managed from the user-friendly Meraki Go mobile app, and is deployed via an easy installation process, which takes less than 10 minutes and requires no prior IT experience. The suite of products includes WiFi access points, network switches, and a security gateway with an optional security subscription for increased protection that's effortless. This means that no matter the type or location, businesses can leverage Meraki Go and start adding value instantly.

This is not the typical enterprise networking solution – Meraki Go understands that every business is personal, unique, and looking to stand out from the competition. Everything about these products is designed to be DIY and make businesses better. With built-in, step-by-step visual instructions on how to get started, a technical support team that can be contacted from within the app, and analytics to enable increased revenue and efficiency, Meraki Go is a business's secret weapon. On-site or on the go, being cloud-based and app-managed means businesses stay protected from vulnerabilities with automatic updates. Access to the Meraki Go App and technical support are all provided at no extra cost.

Businesses can help put a stop to poor user experiences, underperforming apps, and guests leaving bad user reviews. With Meraki Go, business critical services like email, accounting, and point of sale can be prioritized over less critical applications, like streaming HD videos or downloading software updates. In real-time, businesses can see which of these applications and devices are consuming the most data, and then set limits on them, ensuring other users aren't impacted. Rather than having to constantly monitor activity, network notifications are automatically sent to the Meraki Go mobile app, alerting the business if heavy usage is detected or if the internet connection drops, allowing customers to make adjustments before the business is negatively impacted.

"We're excited to deliver enterprise-grade hardware, powerful cloud technology, and optional cyber threat protection backed by Cisco, the world's largest cyber-security company," said Peterson. "These are the same technologies used by Fortune 500 companies, now available, affordable, and simple to install for all businesses."

For more information on the new Meraki Go solution, please visit meraki-go.com. Partners interested in selling Meraki Go, should visit meraki-go.com/partner-program/

Meraki Go Models and MSRP* (USD/GBP/EUR)

Meraki Go Mobile App – Available for free in the Apple App Store and Google Play Store

Indoor Access Point – $149 USD

Outdoor Access Point – $199 USD

Network Switch – starting at $229 USD, available in 8, 24 and 48 ports, with optional POE

Security Gateway – $149

Security Subscription – $120/year

*Manufacturer Suggested Retail Price, excluding tax

All hardware includes local power supply. No license or subscription required to use. Optional Security Subscription can be used with the Security Gateway only.

Read Full Story »»»

DiscoverGold

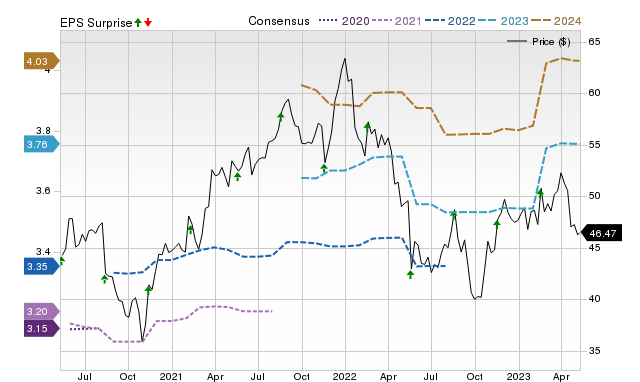

Cisco Systems (CSCO) Reports Next Week: Wall Street Expects Earnings Growth

By: Zacks Equity Research | November 6, 2019

Cisco Systems (CSCO) is expected to deliver a year-over-year increase in earnings on higher revenues when it reports results for the quarter ended October 2019. This widely-known consensus outlook gives a good sense of the company's earnings picture, but how the actual results compare to these estimates is a powerful factor that could impact its near-term stock price.

The earnings report, which is expected to be released on November 13, 2019, might help the stock move higher if these key numbers are better than expectations. On the other hand, if they miss, the stock may move lower.

While the sustainability of the immediate price change and future earnings expectations will mostly depend on management's discussion of business conditions on the earnings call, it's worth handicapping the probability of a positive EPS surprise.

Zacks Consensus Estimate

This seller of routers, switches, software and services is expected to post quarterly earnings of $0.81 per share in its upcoming report, which represents a year-over-year change of +8%.

Revenues are expected to be $13.08 billion, up 0% from the year-ago quarter.

Estimate Revisions Trend

The consensus EPS estimate for the quarter has been revised 0.76% lower over the last 30 days to the current level. This is essentially a reflection of how the covering analysts have collectively reassessed their initial estimates over this period.

Investors should keep in mind that an aggregate change may not always reflect the direction of estimate revisions by each of the covering analysts.

Price, Consensus and EPS Surprise

Earnings Whisper

Estimate revisions ahead of a company's earnings release offer clues to the business conditions for the period whose results are coming out. This insight is at the core of our proprietary surprise prediction model -- the Zacks Earnings ESP (Expected Surprise Prediction).

The Zacks Earnings ESP compares the Most Accurate Estimate to the Zacks Consensus Estimate for the quarter; the Most Accurate Estimate is a more recent version of the Zacks Consensus EPS estimate. The idea here is that analysts revising their estimates right before an earnings release have the latest information, which could potentially be more accurate than what they and others contributing to the consensus had predicted earlier.

Thus, a positive or negative Earnings ESP reading theoretically indicates the likely deviation of the actual earnings from the consensus estimate. However, the model's predictive power is significant for positive ESP readings only.

A positive Earnings ESP is a strong predictor of an earnings beat, particularly when combined with a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold). Our research shows that stocks with this combination produce a positive surprise nearly 70% of the time, and a solid Zacks Rank actually increases the predictive power of Earnings ESP.

Please note that a negative Earnings ESP reading is not indicative of an earnings miss. Our research shows that it is difficult to predict an earnings beat with any degree of confidence for stocks with negative Earnings ESP readings and/or Zacks Rank of 4 (Sell) or 5 (Strong Sell).

How Have the Numbers Shaped Up for Cisco?

For Cisco, the Most Accurate Estimate is lower than the Zacks Consensus Estimate, suggesting that analysts have recently become bearish on the company's earnings prospects. This has resulted in an Earnings ESP of -0.41%.

On the other hand, the stock currently carries a Zacks Rank of #3.

So, this combination makes it difficult to conclusively predict that Cisco will beat the consensus EPS estimate.

Does Earnings Surprise History Hold Any Clue?

While calculating estimates for a company's future earnings, analysts often consider to what extent it has been able to match past consensus estimates. So, it's worth taking a look at the surprise history for gauging its influence on the upcoming number.

For the last reported quarter, it was expected that Cisco would post earnings of $0.82 per share when it actually produced earnings of $0.83, delivering a surprise of +1.22%.

Over the last four quarters, the company has beaten consensus EPS estimates four times.

Bottom Line

An earnings beat or miss may not be the sole basis for a stock moving higher or lower. Many stocks end up losing ground despite an earnings beat due to other factors that disappoint investors. Similarly, unforeseen catalysts help a number of stocks gain despite an earnings miss.

That said, betting on stocks that are expected to beat earnings expectations does increase the odds of success. This is why it's worth checking a company's Earnings ESP and Zacks Rank ahead of its quarterly release. Make sure to utilize our Earnings ESP Filter to uncover the best stocks to buy or sell before they've reported.

Cisco doesn't appear a compelling earnings-beat candidate. However, investors should pay attention to other factors too for betting on this stock or staying away from it ahead of its earnings release.

Read Full Story »»»

DiscoverGold

Cisco Doubles Down on Small Business Commitment

By: PR Newswire | November 6, 2019

LAS VEGAS, Nov. 6, 2019 /PRNewswire/ -- Cisco Partner Summit -- Today, at Cisco Partner Summit, Cisco announced a renewed commitment to Small Business by offering customers and partners a simple, secure and flexible portfolio, dedicated Cisco support, a multi-year awareness campaign and increased partner investments to capitalize on the small business opportunity.

Today, small business is big business! It represents millions of individual companies representing two-thirds of the global GDP. Now more than ever, small businesses are facing a pace of change unlike ever before. Small businesses must address an increasingly savvy customer base who expect digital experiences, amazing customer service and simple user interfaces. With the increased utilization of cloud and web-based applications, a strong and secure network is the essential life blood of any small business.

Collected under the Cisco Designed for Business brand, the newly launched portfolio delivers the right products at the right price for small businesses to thrive. To accelerate growth, Cisco is doubling partner investments for this market and creating an easy and frictionless experience for both partners and smaller customers with faster response times and immediate access to expertise….all things asked for by small businesses.

"The pace of change and transformation is phenomenal. Businesses of all sizes are struggling to stay relevant, compete for customers, and manage efficiencies," said Marc Monday, Global Head of Small Business at Cisco. "Cisco's goal is to give small businesses access to the same best in class technology capabilities as our enterprise customers, but also balancing with simplicity and usability so the customer can focus on what matters most, growing their business."

While small businesses are savvy, they are also struggling with complexity. Cisco is now responding and supporting small businesses faster with the new Virtual Demand Center (VDC). VDC generates and satisfies the demand generated by Cisco marketing activities with a low or no-touch sales motion. For partners, the VDC provides actionable opportunities that are ready to engage and, for customers it delivers faster response times and immediate access to expertise.

Cisco is also getting behind partners who understand the small business market by significantly increasing its partner investments to scale and improve partner profitability. By initiating new programs, incenting partners on growth, streamlining the deal approval process as well as enabling partners to seek out new small business customers, there has never been a better time for partners to double down on small.

New offerings and key changes to the partner programs include:

• New 'Perform Plus' incentive: A new global performance incentive that rewards partners who focus on Mid-size and Small business customers, with a quarterly cash rebate. Cisco is also increasing the investment in partners who demonstrate targeted growth behaviors, but may not be able to capitalize on other incentives. This incentive launches in Cisco Q3 FY20.

• 'CMSP Express' Program : A redesigned Cloud and Managed Service Program to address Managed Services Providers (MSPs) selling to Small Business customers.

• X-Sell available globally: A sales community created via co-investment with partners that includes Cisco-led training and joint selling to scale to the Small business opportunity.

• Streamlined Deal Registration: Significantly accelerated approval time for deals under certain sizes allowing partners to act quickly in the fast-paced market.

Lastly, Cisco has a curated portfolio of products – including some new product developments - specifically designed for small business. Cisco Designed for Business will offer solutions that enable small businesses to connect, compute & collaborate, securely. New additions to the portfolio include Cisco Business Wireless Access Points, a new Meraki Go full stack and the new Catalyst 1K switch, an affordable entry point to the world-class Catalyst range of switches for small business...

Read Full Story »»»

DiscoverGold

Cisco's Game-Changing Collaboration Suite Gets Even Better with Single Platform Advantage, Great New Features and Devices Plus New Ways to Buy

By: PR Newswire | November 6, 2019

Today at Cisco Partner Summit, Cisco has announced five major innovations to its Collaboration portfolio to help CIOs step up and speed up their workplace transformation. Most CIOs are deep in transforming their organizations but are facing huge challenges including having to make big changes while protecting their existing on-prem, cloud and hybrid collaboration investments. In addition, CIOs are striving to provide a modern and unified experience for their employees across one single calling, messaging and meetings platform so they can improve employee productivity. With 95% of the Fortune 500 using Cisco's collaboration suite, Cisco is uniquely positioned to solve these issues and enable CIOs to deliver secure, easy-to-use and ultimately more engaging and energizing experiences for users anywhere, regardless of what devices they use.

"For CIOs, giving employees amazing collaboration experiences shouldn't be hard. They should be able to give them the best collaboration tools on the planet. And tools should be super-secure and simple to manage," said Amy Chang, EVP and GM, Collaboration, Cisco. "The good news is that we're listening, and we've tapped into our deep engineering know-how to deliver just that. All cloud? All on prem? Hybrid? It shouldn't matter. We've got it."

To help CIOs transform their workplaces faster, Cisco has announced five critical innovations. They are:

1. Single Platform Advantage and unified modular app. The Single Platform Advantage means we are delivering all workloads (calling, messaging, meeting, devices and contact center) in an integrated fashion from a single platform. For users, this means that no matter if you're on your mobile, a desktop or another device you will have a familiar, consistent way of working. Transition from your mobile device to a meeting room device with the flick of a finger. For IT this means unparalleled admin control and security from a single pane of glass.

The Single Platform Advantage includes:

- Edge and hybrid services. This allows customers to link what they currently have and deliver enhanced capabilities from the cloud.

- Cognitive Collaboration. This slipstreams context and intelligence throughout every interaction, every day.

- Enterprise-class security and compliance. Our true end-to-end encryption protects data in transit, at rest, and in use. Our multilayer security includes Data Loss Protection to meet compliance and regulatory needs and is validated and continuously monitored to comply with stringent internal and third-party industry standards.

- Analytics and management. Cisco Webex Control Hub lets you manage large-scale deployments centrally and make data-driven decisions. Real-time performance visibility and diagnostics allow you to deliver the best user experience every time. Understand how each room is being used and optimize your assets accordingly. In the contact center, understand agent call volume and customer journeys to help shape better outcomes.

And it's all delivered over a global backbone optimized for real-time media.

The unified modular app means we get it—we know you want the tools you rely on to do your job to be cut from the same cloth. We've been working hard to unify all our apps in this way—so you feel familiar with a new-to-you tool on day one. Today, we announce several new ways we've unified our call, message and meet tools. For instance, when you join a meeting from Webex Teams you'll now have the same host controls as you'd have from Webex itself. And you'll be able to see and take part in the chat, too. Also, we've unified the way you see presence—whether your co-workers are busy or free.

We also take a huge leap in offering these tools in a modular manner—it's one app, but IT can configure it to align to each group's needs or workstyles. Give your warehouse workers (who never join virtual meetings but spend all day messaging and calling) exactly what they need. No more and no less.

2. Calling is core to global business and Cisco is going big on cloud calling. With Cisco, that doesn't mean you need to abandon your on-prem calling investment. We meet you where you are and make sure your users get the advanced features they need.

Webex is the only platform that has the proven scale, security and features to meet the calling needs of today's multi-site, mid-market and large enterprises. IT management can preserve their existing Cisco and 3rd party PBX investments, while taking of advantage of Webex cloud applications and centralized management and analytics services.

Three enhancements:

3. New devices bring the power of AI and whiteboarding to spaces small and large. Collaboration tools should do more than just connect people—they should remove tedious tasks, help you get and stay engaged and make life at work easier. Our AI-infused operating system for devices does just that. Part of the Single Platform Advantage, it "knows" who you are, lets you start your next meeting with your voice, and gives you deep professional information about the people with whom you're meeting. (Learn more about all of those features and others that can truly change your next meeting here.)

Today we're announcing two new options to intelligently transform more spaces. One is perfectly sized for your desk, the other is boardroom big.

- Webex Desk Pro: Think of it as an instant office—give it to the executive, the desk worker or put in a jump space for the whole team to use. It squeezes all the high-end features you find in our award-winning portfolio into a 27-inch, 4K touchscreen device with a USB-C connection. It is web-app enabled, so no need for an extra screen or charging station. It doesn't only work with Webex—use it with any conferencing service. You choose. Walk up and it will recognize and greet you by name. Is your home office a bit, um, messy and that big meeting starts in two minutes? Blur out the background or choose a virtual one. Noise suppression makes sure a barking dog doesn't bring the meeting to a halt.