News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

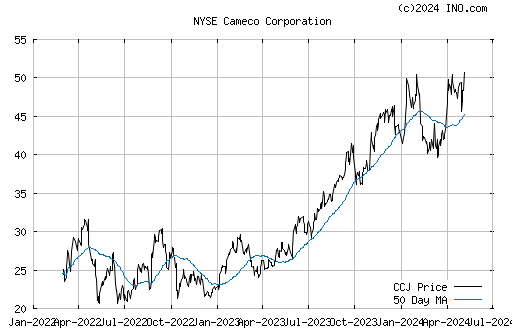

a couple more big candles and its like the good old days--life of Riley

Trump has been heckling --hecklers

caused Shares to drop

apart from INDIA and CHINA; the potential hostile US-RUSSIAN relations are good for U-238

Hello Uranium !

This chart from a month ago :

And here's its' move today :

Your post I see was from Aug. 2015

That was long ago !

.

.

Don't have one but I like the trend.

What is your price target? The 30day chart looks to be getting a pop IMO

Uranium producer Cameco (NYSE:CCJ) is emerging as a rare bright spot among Canada’s largest mining companies on signs nuclear power is shaking off its post-Fukushima slump, according to a Bloomberg analysis.

Cameco (NYSE:CCJ): Q2 EPS of $0.12 misses by $0.09.

Revenue of $565M (+12.6% Y/Y) misses by $16.04M.

Massive India deal. Cameco back to 35+ within 1 year

CCJ seems like a great long term play here...

Lots of positive action here! I highly recommend getting on board while the price is still low!

I believe this stock will double in 2015. I'm surprised there is no activity on this board.

Maybe new 52 week high today, no?

$CCJ - Cameco Corp: A Few Reasons Why I'm Bullish On This Canadian Metals And Mining Play

http://seekingalpha.com/article/1904271-cameco-corp-a-few-reasons-why-im-bullish-on-this-canadian-metals-and-mining-play?source=email_rt_article_readmore

As an investor who doesn't mind a conservative income-driven play every once in a while, I've decided to shift my focus to the industrial metals & mining sector and highlight several of the reasons behind my decision to remain bullish on shares of Cameco Corp. (CCJ).

#1: Recent Performance & Trend Behavior

On Monday, shares of CCJ, which currently possess a market cap of $8.34 billion, a forward P/E ratio of 20.95, and a dividend yield of 1.85% (CDN $0.40), settled at a price of $21.10/share. Based on their closing price of $21.10/share, shares of CCJ are trading 4.09% above their 20-day simple moving average, 10.13% above their 50-day simple moving average, and 6.13% above their 200-day simple moving average. These numbers indicate a short-term, mid-term, and long-term uptrend for the stock which generally translates into a moderate buying mode for both near-term traders and longer-term investors.

(click to enlarge)

#2: 36-Month Dividend Behavior

Since December 29, 2010, the company has increased its quarterly distribution once in the last three years, with the most recent increase having taken place in May of 2011. The company's forward yield of 1.85% (CDN $0.40) coupled with its ability to maintain its quarterly distribution over last three years, make this particular metals & mining play a highly considerable option, especially for those who may be in the market for a conservative stream of quarterly income.

#3: Comparable Dividend Growth

Not only does the partnership's 1.85% dividend yield and 36-month dividend behavior make this particular stock a highly attractive option for most income-driven investors, its dividend growth over the last three years versus one of its sector-based peers is also something investors should almost certainly consider. From a comparable standpoint, CCJ's dividend has grown a solid 38% over the past three years, whereas the dividend growth of its Canadian-based peer MFC industrial (MIL) has only increased 20% over the same period.

(click to enlarge)

#4: Recent Update at its Cigar Lake Uranium Project

On Monday, December 16, Cameco announced that jet boring had been underway at its Cigar Lake uranium project in Saskatchewan, and the site is on track to begin ore production by Q1 2014. Investors should note that Cigar Lake, which originally was scheduled to begin production this year, has suffered various delays due to flooding and a series of technical challenges. As long as there aren't any subsequent weather-related or technological issues, I see no reason why production wouldn't begin by Q1 2014.

Risk Factors (Most Recent 40-F)

According to the company's most recent 40-F there are a number of risk factors investors should consider before establishing a position Cameco Corp. These risk factors include but are not limited to:

#1 - The company's actual sales volumes or realized prices for any of its products or services could be lower than what it expects, and for any reason, including changes in market prices or loss of market share to a competitor, results could be negatively impacted.

#2 - Certain production costs may be higher than the company had planned, or in some cases where the necessary supplies are not available, developmental and exploratory, as well as fully operable mining projects could be negatively impacted.

#3 - If, for any reason, the company's mineral reserve and resource estimates are not as reliable as had been estimated, results from operations could see a significant decline.

Conclusion

For those of you who may be considering a position in Cameco Corp. I'd keep a watchful eye on a number of things over the next 12-24 months as each could play a role in both the company's near-term and long-term growth. For example, near-term investors should focus on the recent performance and trend behavior of the company while longer-term investors should focus on the company's dividend growth over the next 12-24 months as well as any further developments that may occur with regard to its Cigar Lake uranium project.

$CCJ- Cameco Corporation (USA) declares $0.10 dividend

Cameco Corporation (CCJ) declares $0.10/share quarterly dividend, in line with prior.

Forward yield 1.99%

Payable Jan 15; for shareholders of record Dec. 31; ex-div Dec. 27.

Nice bounce today.

$CCJ - Cameco reports third quarter financial results

http://finance.yahoo.com/news/cameco-reports-third-quarter-financial-123000717.html

... "SASKATOON, SASKATCHEWAN--(Marketwired - Oct 30, 2013) -

ALL AMOUNTS ARE STATED IN CDN $ (UNLESS NOTED)

strong third quarter and year-to-date results - higher revenue, gross profit and net earnings

higher sales volumes and average realized prices in our uranium and fuel services segments

reconfirmed annual sales guidance

at Cigar Lake began jet boring in waste rock

we were granted 10-year operating licences at McArthur River, Key Lake and Rabbit Lake

delivered our first shipments of Canadian uranium to China under the new Canada-China Nuclear Co-operation Agreement

Cameco (CCO.TO) (CCJ) today reported its consolidated financial and operating results for the third quarter ended September 30, 2013 in accordance with International Financial Reporting Standards (IFRS).

"Our strong third quarter and year-to-date financial results reflect the strength of our contracting strategy in this lower price environment," said Tim Gitzel, president and CEO, "providing us with higher average realized prices that are well above the current uranium spot price.

"We're starting to see some of the cost benefits of the restructuring we undertook earlier in the year and, overall, we are on track to deliver on our outlook, even expecting to realize better results in some areas than previously indicated. We have adapted to the current challenging market conditions and we continue to pursue a growth plan to take advantage of the opportunity we see in the long term."" ...

$CCJ - Cameco: Size Matters

http://seekingalpha.com/article/1784752-cameco-size-matters?source=email_rt_article_readmore

00

Cameco (CCJ) was created in 1988 through the merger of two Canadian crown (government-owned) corporations. It's IPO debuted on the Toronto exchange in 1991 and a NYSE listing occurred in 1996. The McArthur River mine, the highest grade mine in the world (16.36% U3O8, 100 times the global average), began production in November 2000. Cameco's share of the proven and probable resources is 264 mil lbs. The mine has produced 230 mil lbs in the last 13 years. CCJ's current year share is over 13 mil lbs.

Cameco's produces around 14% of the world's uranium, with 2012 production of 21.9 mil lbs. They forecast output in 2018 of 36 mil lbs. Its total proven and probable reserves are about 465 mil lbs with another 531 mil lbs in the inferred/measured and indicated categories. That's one hell of a lot of uranium. CCJ's size and resources make it an attractive investment for the moderately conservative investor who is aware that mining is inherently risky.

Here's the good news

(all dollar amounts in Canadian currency)

2012 revenue of $2.321 bil, gross margin of 31%, net earnings of $266 mil (.67/share), adjusted earnings of $447 mil (1.13/share), cash from operations of $644 mil (1.63/share)

Estimated profit for 2013 on Yahoo ranges from .53/share to 1.05 with the consensus at .80 corresponding to a P/E of 23. BMO Investorline shows the consensus at .91.

Current year and next year estimates are declining slightly with the 2013 current versus 90 days ago dropping from 1.01 to .91 (BMO).

2014 has dropped from 1.30 (90 day) to 1.15 . At 1.15 the P/E is a very attractive 16 given the long term demand for uranium

Sales for the first two quarters of 2013: $826 mil

Cash from operations through the first two quarters of 2013:$233 mil

Cash position as at June 30/13 is $331 mil (.83/share)

Current ratio, June 30/13 = 2.58

Net debt to equity, June 30/13 = .20. Debt rated BBB+ (investment grade) by S&P.

Tangible book value approximately $12/share, 1.54 x current share price

Profitable and cash flow positive over the last 10 years

Has paid a quarterly dividend continuously since 1996. Current payment of .39/share equals a 2.1% yield

The share price is near the bottom of a 2 year range of $16.40-$25.00. Technically neutral, CMF (Chaikin Money Flow) has turned positive over the last 9 sessions, MACD crossover recently, 200 day moving average is above the 50 day. Obviously a beaten down stock, but not to the point of capitulation a la Nov. 2008 at $11.78. Those buyers are up 57% plus dividends. Not out of the park but a decent return over 5 years with some measure of safety.

Uranium isn't like oil or copper. The demand is fairly constant and, in a Fukushima-free world, would be steadily, if slowly, rising. With 60+ reactors under construction and new mine supply a virtual no-show, the market should be a lot more buoyant than it is. But, long term, the uranium market looks strong.

And, Cameco is the way to play it with Mr. Graham's "margin of safety". It's large enough, strong enough and has a long history of dividend payments. The price here looks reasonable although certainly not in the bargain bin. I would scale in to this stock, with the possibility of getting more shares with the same amount of cash when the inevitable correction appears. (If anyone knows when this correction is going to happen, please e-mail me).

If it can go wrong, it will (maybe)

The Japanese reactor re-start is delayed. That surplus of uranium continues to weigh on the price

Fukushima II

The Cigar Lake mine suffers further lengthy delays. This is kind of a two-edged sword as it would probably move the spot price needle, boosting a portion of CCJ's revenue.

Growing public opposition to nuclear power, from an environmental viewpoint and/or an objection to the high cost of construction

And, of course, the always present possibility of another financial panic, or least an ugly downdraft.

I think the balance of probabilities is in Cameco's favour. For an investor with a longer view, CCJ offers the chance of truly superior gains or, at the very least, a reasonable return on one's money. For those of us who think uranium is going to be lively territory in 5 years, Cameco is the best bet, having some downside support while being leveraged to a rising U3O8 price.

My opinion of my opinion

The preceding is my opinion, of course. There are many other opinions. Some of them worthwhile, others just fluff. Read them, decide for yourself, then make an informed investment decision. The one opinion you might want to discard is your personal broker's. They get paid to make trades. If you make some money along with them, that's just a bonus.

looking like U308 spot has bottomed too.

$CCJ - Saskatoon, Saskatchewan, Canada, October 1, 2013

chttp://www.cameco.com/media/news_releases/2013/?id=754

Cameco Provides Date for Q3 Results and Conference Call (71.21 KB PDF)

Cameco 2013 Q3 Conference Call

Cameco (TSX:CCO) (NYSE:CCJ) will issue its third quarter results before markets open on Wednesday, October 30, 2013.

Cameco invites investors and the media to join its second quarter conference call with the company's senior executives on Wednesday, October 30, 2013 at 1:00 p.m. Eastern.

Cameco will discuss the financial results and company developments before opening the call to questions from investors and the media.

To join the call, please dial (866) 225-0198 (Canada and US) or (416) 340-8061. An operator will put your call through. A live audio feed of the conference call will be available from a link on cameco.com.

A recorded version of the proceedings will be available on our website, shortly after the call, and on post view until midnight, Eastern, November 30, 2013, by calling (800) 408-3053 (Canada and US) or (905) 694-9451 (Passcode 7039949#).

Profile

Cameco, with its head office in Saskatoon, Saskatchewan, is one of the world's largest uranium producers. The company's uranium products are used to generate electricity in nuclear energy plants around the world, providing one of the cleanest sources of energy available today. Cameco's shares trade on the Toronto and New York stock exchanges.

As used in this news release, "Cameco" or the "company" means Cameco Corporation, a Canadian corporation and its subsidiaries and affiliates unless stated otherwise.

Hey slick, this might have seen some bottoming here.

$CCJ - Cameco Poised For Nuclear Upturn

http://seekingalpha.com/article/1717212-cameco-poised-for-nuclear-upturn?source=email_rt_article_readmore

Uranium spot prices are at a seven year low. Long-term demand for uranium is increasing as new reactors come online and Japanese reactors prepare to resume operations in mid 2014. A significant uranium supply channel is going offline as the Megatons to Megawatts Program wraps up in November. While timing is uncertain, I expect an upsurge in uranium prices from today's levels. Cameco (CCJ), the world's largest uranium producer, is positioned to benefit.

Industry Trends

According to the World Nuclear Association, there are 432 operable nuclear reactors in the world. They required about 143 million pounds of uranium to operate in 2013. Global uranium production was about 129 million pounds in 2012.

In its Global Nuclear Fuel Market: Supply and Demand 2013-2030 report earlier this month, WNA estimates world Uranium demand to increase to 214 million pounds by 2030. This demand will be generated by the 68 reactors currently under construction and 489 which are planned or proposed to come online before 2030. Approximately 50% of reactors under construction, planned or proposed are based in China.

Approximately 13% of global nuclear fuel has been provided by blending down weapons-grade uranium in the "Megatons to Megawatts" program, which comes to an this year with the final shipment scheduled for November 2013.

While uranium prices and nuclear industry shares have been depressed since the Fukishima disaster in March 2011, this significant supply shift, coupled with Japan's plans to restart 6-16 reactors by mid 2014, may be the catalysts necessary to correct for the excessive pessimism in the wake of the Fukishima disaster.

Uranium Spot Price Chart

Uranium Spot Price data by YCharts

About Cameco

Cameco is the largest miner of uranium in the world, accounting for approximately 14% of global production. It has 465 million pounds of proven and probable uranium reserves, in a diverse portfolio of uranium deposits centered in Canada, Kazakhstan, the US and Austrailia.

Cameco owns the world's largest high-grade uranium mine at McArthur River and has completed 97% of the development of a mine and processing facility at the world's second largest high-grade uranium deposit at Cigar Lake. Both operations are based in politically-stable Saskatchewan Canada and partly owned by other companies.

Cameco's business has four basic segments:

Uranium Production, which involves mining and selling uranium oxide and accounted for 85% of profits and 38% of revenues in the past six months;

Fuel Services, which involves processing uranium oxide into fuel-ready UF6 and UO2 and accounted for 10% of profit and 9% of revenues in the past six months;

Intermediary Services, which involves connecting buyers and sellers of primary and secondary nuclear fuel material and accounted for 4% of profits and 13% of revenues in the past six months.

Energy Production, chiefly through an investment in Ontario's Bruce Power site which accounted for 0% of profits and 41% of revenues in the past six months.

The company is protected from temporarily low spot prices because most of its sales are through long-term contracts. According to its presentation at the September 13th Bank of America/Merrill Lynch Mining Conference, the company has fully committed its production until 2016 in long-term contracts.

The average realized price has been $47/lb over the past six months.

Drawing significantly on its new Cigar Lack mine, which, despite some delays, is slated to begin production in early 2014 with a per pound cash cost of $18.60, Cameco plans to increase annual production to 36 million pounds by 2018.

Source: Cameco Annual and Quarterly reports

CCJ Chart

CCJ data by YCharts

Investment Thesis:

Cameco has a strong position in an expanding industry with high barriers to entry and decreasing secondary nuclear fuel alternatives. Its portfolio of undeveloped properties allows it to take advantage of upward trends in uranium prices. Its relatively low cost of production and strong cash flows allow it to hold strong during periods of low prices.

There are several catalysts which could cause a mood shift in the industry, including the Japanese restart and the end of Megatons to Megawatts Program.

There are also several big picture upside catalysts which make me happy to take a long-term position in nuclear:

Nuclear, which still remains in many environmentalists' bad-books, may yet be embraced as an essential component of a clean energy solution to climate change.

There are several interesting "Nuclear Renaissance" projects being explored by Silicon Valley entrepreneurs and other new economy enthusiasts which could create considerable new demand for nuclear material such as thorium reactors and micro reactors.

Cameco's downside is limited by long-term contracts above current spot rates and its competitive all-in costs of production at its flagship high-grade mines.

Supply and demand are well balanced in the industry for the time being. Cameo claims its production is committed out to 2016 at prices well-above the current spot rate. Japan's shutdown has caused inventories to build, putting downward pressure on the thinly-traded short term uranium prices. Most of the significant buyers and sellers are engaged in long-term contracts. The next wave of long-term contracting, which will certainly happen before 2016, may drive prices upward as it did in late 2010 and early 2011.

Bottom Line

Cameco is a strong company in a growing nuclear industry that has been two years out of favor. Several catalysts are lined up to improve prospects in the industry. I consider CCJ a long-term buy.

$CCJ - BofA/Merrill Lynch Downgrades Cameco Corporation (CCJ) to Neutral

http://www.streetinsider.com/Downgrades/BofAMerrill+Lynch+Downgrades+Cameco+Corporation+%28CCJ%29+to+Neutral/8726650.html

$CCJ - Cameco in tax dispute, accused of offshoring profits in Switzerland

http://seekingalpha.com/currents/post/1299042?source=email_rt_mc_readmore

Cameco (CCJ -1.5%) has avoided paying hundreds of millions of dollars in Canadian taxes by setting up a subsidiary in Switzerland, the Canada Revenue Agency says.

At issue is a deal CCJ made in 1999 - when uranium prices were much lower - to sell uranium to its wholly-owned Swiss subsidiary; the allegation is that the subsidiary then sold the uranium for more and recorded the profits in Switzerland, where taxes are lower.

CCJ says it hasn't done anything wrong and estimates it could end up owing as much as $850M in Canadian corporate taxes if it loses the case.

$CCJ - Cameco: The Long Wait For Cigar Lake

http://seekingalpha.com/article/1700362-cameco-the-long-wait-for-cigar-lake?source=email_rt_article_readmore

Much has been said and written about a looming supply shortage in uranium pointing to the termination of the HEU agreement, the anticipated restart of nuclear power generation in Japan, and plans to increase the total number of power stations world-wide. The same chain of arguments typically also points to the shelving and down-scaling of many projects due to the presently very low uranium price environment. While we do not share the extreme bullish view of some analysts we still agree that fundamentals are slowly shifting in favor of uranium.

Listening to Cameco's (CCJ) last earnings call we could not help to notice yet again that this premier uranium mining company continues to reiterate a similar view:

"We're expecting average annual growth in uranium consumption in the order of 3% per year out to 2022."

said CEO Timothy Gitzel and proceeded to update investors on Cameco's largest growth project, the Cigar Lake mine development. He had some news to break, and the news wasn't pretty:

"[…] our capital expenditures at Cigar will increase by 15% to 25%. That's mainly because of some scope changes at the mine and at the AREVA mill, as well as the same upward pressure being felt on cost across the mining industry. In addition, the previous estimate only included our expenditures to first ore and not the capitalization of start-up costs."

In total numbers the announced increase translates to $165M to $275M in additional capex. News about Cigar Lake kept coming and only a few days later a conference call with another update on the project was scheduled on short notice. The news boiled down to the following excerpt of the release:

"During commissioning of the underground ore handling facilities in the mine, Cameco identified additional work that will delay jet boring in ore. Based on current information, Cameco expects to begin ore production during the first quarter of 2014"

"In addition, AREVA has advised Cameco that it has determined that further mill modifications are required and that the mill is expected to begin processing Cigar Lake ore by the end of the second quarter of 2014."

These delays are not the first experienced at this project. Originally start-up was scheduled for early 2008. In October 2006 the project had been 60% built when rock fall triggered water inflow that could not be contained. Remediation work went smoothly for some time and in June 2008 production start-up was still deemed possible by 2011. However, soon thereafter further water management problems arose delaying mine construction further. It took until October 2009 before de-watering could resume and early in 2010 Cameco crews were able to re-enter the main working level. Milling arrangements for Cigar Lake ore were amended late in 2011 to exclusive processing of ore at the Mc Clean Lake facility owned by Areva (70%), Denison Mines (DNN) (22.5%) and OURD (7.5%). Development progressed smoothly thereafter until a couple of weeks ago.

(click to enlarge)

(Illustartion of mining process taken from the company web site)

The Cigar Lake Mine

The mine at Cigar Lake in the Athabasca Basin is a world-first in many respects. The two 50:50 owners of this project, Cameco and Areva (ARVCF.PK), are trialing the jet boring mining technology which has been developed for ore bodies that are typical for this particular region in Saskatchewan, Canada. The Cigar Lake deposit is situated at over 400m depth. The ore body sits within highly variable rock and is frozen prior to mining to improve ground conditions and prevent water inflow. Access to the ore is achieved from tunnels running 25m below the ore body in the basement rock. Access holes are pierced into the ore body and high pressure water from oscillating and rotating jets is used to carve out cavities. The resulting ore slurry is collected in separate pipes and pumped to underground ROM rooms. The cavities in the ore are filled with concrete before the process is repeated. Jet boring has been tested in waste rock but never been applied in full scale before. The ore slurry is collected and taken to underground grinding and thickening circuits from where it is pumped to the surface and loaded on containers for transport to the mill.

The recent announcement followed water leakage from the ROM cavities. In order to control this outflow Cameco has decided to implement steel liners which has led to the latest delay. This has been described as a straight forward measure not posing any serious challenges in the conference call. The delays at the mill involve the installation of a ventilation and purging system to counteract the potential for the formation of increased hydrogen formation exists in the leaching circuit.

All going well, Cameco will be starting to produce ore at Cigar Lake early in 2014. This re will be stockpiled at the McClean Lake plant and processed as soon the upgraded plant comes online towards the middle of the year 2014. The plant design allows for some overcapacity and Areva has indicated that this will be used in order to catch up with mine output.

Economic Implications

Cameco is a Canadian company best known for mining uranium and accounting for 16% of world uranium production from its operating mines in North America and Kazakhstan. Cameco has a market capitalization of $7.9B and is trading at $19.88 at the time of writing. Despite the depressed uranium price the company still operates profitably and continues to pay dividends at just under 2% yield. The company had $331.6M in cash and $1.3B long term debt at the end of the second quarter 2013. Cameco sells a large portion of its uranium product through long-term contracts. Revenue is therefore partially independent of the uranium spot price.

CCJ Chart

CCJ data by YCharts

So far the share price has not suffered from the recent disclosures. On the contrary: the share price increased by almost 5% the day after the last earning call when the cost escalations were announced. Obviously, the other news reported on the day over-ruled the news about cost escalation.

The latest technical report on Cigar Lake was filed in 2011 showing a pre-tax NPV (8%) of $1.435B and an IRR of 32.8%. Payback was scheduled until 2017. This analysis was based on mine start up late in 2013. The presently announced delay is minimal compared to the estimated 15 years of mine life. The report also includes a sensitivity analysis with regards to changes in capex. According to this sensitivity analysis A 10% increase in capex reduces the NPV by about $50M. Using the announced worst case of a 25% capex increase therefore leads to a reduction of $125M in NPV to around $1.3B for this project.

It appears that the latest delay and cost escalation has no material impact on Cameco. The NPV of the Cigar Lake mine is still very healthy and financing the cost overruns will not cause a material problem. The company is yet to state the impact on its 5 year outlook, if any. Areva has indicated that it will be stockpiling ore until the plant at McClean Lake is ready and will be using overcapacity to catch up with production. We therefore do not anticipate a significant reduction in Cameco's long term production outlook.

$CCJ - Cameco to miss 2013 target for Cigar Lake uranium project

Cameco (CCJ) says additional work is required on its Cigar Lake uranium project in Saskatchewan, pushing the expected start of production into Q1 2014 from the end of this year.

CCJ says 97% of Cigar Lake is complete and the commissioning of mining systems is "well advanced," and the capital cost of the mill modifications is not expected to be material.

Cigar Lake already has suffered several delays due to flooding and a series of technical challenges; CCJ said last month its share of the capital cost for the project would increase by 15%-25% from the previous $1.1B estimate.

CCJ -0.5% premarket.

http://seekingalpha.com/currents/post/1266942?source=email_rt_mc_readmore

$CCJ - Cameco: The Single Best Investment For The Inevitable Uranium Rebound

http://seekingalpha.com/article/1622332-cameco-the-single-best-investment-for-the-inevitable-uranium-rebound?source=email_rt_article_readmore

Fear is one of the most primal of human emotions, it can be used to manipulate and used to motivate, but most importantly it can be used to pick up value when the market's fear has left solid companies beaten and bruised. Cameco Corp (CCJ) is one example of such a company. Just like BP's (BP) stock was hit hard following the Gulf Incident of 2010, CCJ has been a victim a fear in the aftermath of the Fukushima Disaster in Japan of 2011. While the turmoil of the time period sharply hurt uranium prices and nuclear perception across the globe, the price of uranium will inevitably rebound to pre-disaster levels, it is only a matter of time. Nuclear power, at the current moment, is the only efficient and effective option we have in dealing with climate change, particularly when coupled with the new prospect of electric cars. It may be some time before uranium demand returns to previous levels, but Cameco offers investors the best opportunity to reap the benefits when the time comes, while mitigating risk of loss in the meantime in an industry where many companies can hardly turn a profit.

The Stock Price

There was a time when CCJ was a $50 stock, and in the period preceding Fukushima in 2011, CCJ was marching onward yet again to the $40s, over double its current price. After an immediate 25% drop in price, the company finished the year down 50%. Since then CCJ has returned $1/s in dividends to shareholders, however it has not yet found the traction to bring itself out of the current trading range of between ~$19-23. Buying at the current level provides some technical support to the downside. At it's peak, CCJ was earnings almost $2/s in 2009, and the company was set to increase this number, however EPS has since dwindled to just under one dollar per share. However, they appear to have hit a trough and found support in recent quarters.

(click to enlarge)CCJ Share Price

The Financials

The company has solid financial backing behind it, with just over ~$12.50/s in book value and consistent book value growth over the last several years. In addition, the company has returned an increasing amount of cash over the last few years in an effort to placate shareholders, it is important to have a management team that is in touch with a company's stock price, and CCJ's certainly is one of the few. In addition, the company is actually only trading at 1.1 times net asset value, a key metric that has enabled to company to hold strong at the current share price over the last year and a half.

The Prospects

This is where things pick up for the company. Yes, the company was hit hard by the Fukushima Disaster, and yes, the company has lost significant EPS as a result, however this is one of the few companies in the sector that is healthy enough to withstand the headwinds. As Uranium prices declined sharply from their mid $70s/lb pre-Fukushima levels to where they stand now at around ~$30/lb, CCJ has been hit badly, however as the company has held water in these trying times, a bottom was forming. Now, it appears that Uranium prices are set to rebound sharply in the coming months and years. A quote from the aforementioned article reads:

"Japanese utilities have been preparing to restart several of 42 reactors that were shut down after a tsunami caused a meltdown at the Fukushima-Daiichi nuclear plant in March, 2011. Earlier this month, Japan introduced legally binding requirements for nuclear plant operators bolster their tsunami defences, check for active earthquake faults under their plants, set up emergency command centres and install filters to reduce radioactive discharge from reactors."

It remains to be seen if this will materialize, however I think it is an inevitability that prices will return to their pre-disaster levels in the next five to ten years as the focus of public policy shifts away from the recession and back to the environmental landscape. France has shown the world how beneficial effective nuclear plants can be and as China is taking note, CCJ is set to benefit immensely. To sum up the level of skin in the game that CCJ has if prices rebound, I'd like to quote a previous article written by an apparently well researched fellow here on SA:

"Cameco is the world's largest producer of U3O8 uranium, a mineral whose only commercial use is to fuel nuclear power plants, and the second largest uranium producer in the world, behind Rio Tinto. Nuclear power accounts for around 15% of the world's electricity, and CCJ accounts for 20% of world uranium production, with 1010 million pounds of proven and probable reserves (53% more than any other publicly listed company)."

When Uranium prices rebound, CCJ will reap the profits. A number of catalysts exist for this. At the current price levels, investors can enter healthy, quality names like CCJ that stand to benefit from a global shortfall. The following excerpt explains exactly how a shortfall could materialize in the coming months:

" A uranium supply crisis is still brewing and the fundamentals do remain strong. Demand is stable and reasonably predictable. The weak spot price still threatens future mine supply with more closures, cancellations and deferrals of mining projects. The all-important catalyst at the end of this year is the end of the Russia-U.S. HEU "Megatons to Megawatts" program, which in our view will not be renewed. That means 24 million pounds (24 Mlb) of secondary supply comes offline with no replacement - equivalent to the entire production of CCJ. Uranium prices are too low to incentivize new builds right now. We think prices must rise, as will the equities."

Yet the best is yet to come. Anyone who has witnessed what the Chinese are capable of, when the government puts money and people to a task, knows that the future of nuclear growth in China means big money for CCJ.

(click to enlarge)Nuclear Outlook

Wrapup

Fear is an amazing emotion. The same fear that dragged down BP after the Gulf Crisis brought Uranium levels to lows after the Fukushima Disaster in Japan. As a result, many Uranium companies were hit hard, and some have not been profitable since. Cameco Corp has sustained throughout, and even increased it's dividend in the process. The company offers an attractive value play, and appears to be able to withstand market pressures for investors who are willing to wait for a Uranium price rebound. How long it takes, nobody can know for sure, however it is inevitable and only a matter of time. Tim Gitzel is the current CEO at Cameco, and his words on the potential in the Uranium market should offer investors promise:

"So this growth is not just something we think will happen. It's happening as we speak… it's just a question of how long it will take for that growth to become the more dominant force in the market than the challenges currently being faced."

Uranium has not been an exciting segment over the last few years for longs, and many investors have forgotten the opportunity that remains to be taken advantage of. Some however, recognize that the bottom is in, and that there are a variety of catalysts in the coming months and years that stand to propel CCJ forward. According to GlobalData,

"Uranium demand will climb from 105,531 met tons in 2012 to 145,680 met tons in 2020, representing an increase of 38% over the eight year period."

Investors who take note now and park capital in CCJ will be the ones who benefit the most.

$CCJ - Cameco misses by C$0.03, misses on revenue

http://seekingalpha.com/currents/post/1184972?source=email_rt_mc_readmore

Cameco (CCJ): Q2 EPS of C$0.15 misses by C$0.03.

Revenue of C$421M misses by C$102.95M. (PR)

$CCJ - Odds Favor Higher Uranium Prices

http://seekingalpha.com/article/1591642-odds-favor-higher-uranium-prices?source=email_portfolio&ifp=0

The spot uranium price for U3O8 reached a 7-year low last week at $36.50 per lb. Those who have followed the uranium sector know that uranium prices collapsed after the Fukushima incident in 2011. However, I believe the odds favor a rise in uranium prices in the long-term for the following reasons.

1) Japan will be restarting some of its nuclear reactors perhaps as early as this year. Following the Fukushima incident, all of Japan's roughly 50 nuclear reactors were shut down for safety reasons. Earlier this month, however, Japanese utilities have applied to reactivate 10 of those reactors. The Japanese central government supports the reactivation. It may or may not happen in 2013, but expect this first wave of reactors to be activated by 2014 with perhaps a second wave to come sometime after.

2) New nuclear reactors are being built across the world and will come online in the next several years. Currently, there are over 430 nuclear reactors operating around the world. 64 new ones are currently under construction. More than 150 are in the planning stages and 300 more have been proposed according to the World Nuclear Association. It takes several years for a reactor to be built, but demand will increase in the next several years as these reactors come online.

3) Uranium mine supply has fallen short of global demand for many years now. In 2013, global demand is expected to be 170 million lbs, growing to 220 million lbs by 2022. The shortfall has been made up by Russia's Megatons to Megawatts program, which converts highly-enriched uranium from Russian bombs into low-enriched uranium used by nuclear reactors. Russia is expected to supply about 24 million lbs of uranium this year through this program. The agreement with Russia ends at the end of this year leading to some uncertainty about future supply in 2014 and beyond. More than likely, a new agreement with Russia will be reached, but as of today that has not happened.

4) New mines need a uranium price of at least $60 per lb in order to justify the costs of developing and operating them. Uranium prices thus need to increase by more than 50% to make building new mines economic.

In the US, if you're looking at any new production, you're going to probably need $65 to $70 uranium. (Marin Katusa)

Investing

Investors can choose between uranium mining stocks or invest directly in the commodity. Here are three stocks to consider:

Cameco (CCJ) is the largest primary uranium producer in the world. Its two main projects (McArthur River and Cigar Lake) are the two largest high-grade mines in the world. Saying that they are high-grade would be an understatement. These are superior high-grade mines that are about 20 times richer than the average uranium mine in the world. CCJ is expected to grow its production from 21.9 million ounces in 2012 to 36 million ounces in 2018. McArthur River produced 13.6 million lbs in 2012 and Cigar Lake is in the final stages of development and is expected to start producing in mid-2013 and contribute 9 million lbs of production annually.

Denison (DNN) is an exploration company with no current production, but it has a portfolio of several interesting projects. The most promising project is probably the Wheeler River project. Drill results have indicated very high-grade resources. DNN's stake in this project is 60% with CCJ owning 30% and another company owning the remaining 10%. Other notable projects are in Africa and Mongolia. DNN has a 100% stake in the Mutanga project in Zambia and a 85% stake in a project in Mongolia. I'd be cautious with DNN because Africa and Mongolia are not considered to be safe mining areas like Canada, Mexico and the U.S.

Uranium Energy (UEC) is an exploration company with a little bit of production. Almost all of its projects are located in the U.S. Its production comes from the Palangana mine in Texas, which produced 69,000 lbs of uranium in the last quarter. The mine is being expanded which should increase production. Production should also increase when the Goliad mine, currently being developed, comes online. Initial production should begin within the next 12 months. UEC also owns its own processing plant in Texas which serves both the Palangana and Goliad mines.

While the mining stocks are one way to go, I prefer Uranium Participation (URPTF.PK), which is a company that does nothing more than purchase uranium and hold it in storage. It is thus directly linked to the price of uranium. It holds uranium in two forms: U3O8 and UF6. After uranium is mined, it is converted to U3O8 and then to UF6. The stock often trades at either a premium or discount to its underlying uranium assets similar to a closed-end fund. But URPTF is neither an ETF or a closed-end fund. It is a stock.

Final Thoughts

Uranium demand is fairly predictable considering that we know how many reactors are online. As long as reactors are up and running, they need to be refueled. However, another wild-card event like Fukushima could provide another crippling blow to the nuclear industry. Unfortunately, these events can't be predicted. Barring another incident that creates fear and uncertainty, the need for uranium should continue to grow as more and more reactors come online.

This will stop Japan from selling its stockpile so cheap...

Japan's Prime Minister Shinzo Abe has won a majority in the upper house, ending a political stalemate as he now controls both houses of parliament. The reshuffle paves the way for Japan to return to nuclear power, in a move poised to curb LNG imports and reduce the share of gas for power generation.

All but two of the Japan's 50 nuclear reactors are currently mothballed and refused permission to operate. However, newly adapted safety regulation may help operators to restart their nuclear plants.

Four of Japan's 10 main regional utilities - Kansai Electric Power, Shikoku Electric Power, Kyushu Electric Power and Hokkaido Electric Power – filed an application in early July to restart reactors under new, more stringent safety regulations imposed in the wake of the 2011 Fukushima Daiichi incident.

The return to nuclear would reduce the share of gas in Japan's energy mix and electricity prices. The Institute for Energy Economics in Japan (IEEJ) forecasts restarting twenty six of the country's nuclear power stations in 2014 could lower the electricity fuel cost by 1.8 trillion yen ($0.019) and reduce generation costs by about 2 yen/kWh...

$CCJ - Bear of the Day

http://finance.yahoo.com/news/bear-day-cameco-ccj-045512946.html

Although there has been some strength in the mining sector lately, the overall trend for the space hasn’t been good. The industry has been hampered by low levels of demand, concerns about emerging markets, and a strong dollar which has pushed many investors out of commodities.

While this bearish outlook has manifested itself in silver and gold miners, a number of other segments have also been hit by this trend. In particular, the miscellaneous segment—which includes firms that mine for items like uranium, rare earths, and palladium/platinum—could also face weakness ahead, such as in the case of Cameco (CCJ).

Cameco in Focus

The Canadian-based firm is a relatively well-known name in the uranium mining space, operating several properties in the Saskatchewan province of Canada. The company also has a few locations in the U.S. Midwest, in addition to a Kazakhstani property as well.

Beyond their mining segment, the company is also engaged in a bit of nuclear energy production. This is represented by a minority stake the company has in Bruce Power L.P. which produces power in a few Ontario reactors.

Cameco Outlook

Thanks to its relatively diverse operations and the company’s focus on a key product like uranium, CCJ hasn’t seen that bad of a 2013 so far. In fact, the company is positive from a year-to-date look, adding about 5% in the time frame, though it has experienced extreme volatility too.

While this definitely represents a bit of outperformance when compared to others in the space, investors should be concerned that this will not last in the months ahead. This is particularly true when investors consider the estimate revision picture, and projected growth rates for this company.

Earnings Estimates

While CCJ analysts are expecting solid growth for both the current quarter and next quarter periods, this isn’t expected to translate to the full year time frame. For this time period, analysts are looking for an earnings contraction of about 15% year-over-year, well below the struggling industry and its average.

Furthermore, investors should note that the consensus has fallen like a stone for the full year time frame, with estimates going from $1.23/share 90 days ago to their current level just below $1.00/share. Plus, it isn’t like CCJ has a great track record when it comes to earnings dates, as the over the last four quarters the company has seen an average surprise of -23.17%.

Thanks to these factors, CCJ has earned itself a Zacks Rank #5 (Strong Sell), suggesting that it is due to fall back to Earth and underperform peers in the months ahead. And the stock also has an underperform Zacks Recommendation which means that the longer-term outlook isn’t any better for this firm.

Better Picks

If investors really want to stay in the miscellaneous segment of the mining industry, there are only a handful of choices. The space currently has one of the lowest Zacks Industry Ranks, so top Ranked stocks are few and far between.

Still, there are a handful of #1 Ranked stocks that could be worth investing in, including Avalon Rare Metals (AVL), Impala Platinum (IMPUY), and Stillwater Mining (SWC). All of these have seen their Ranks surge to the top echelon in the past week too, and thus they may be better picks than CCJ for the months ahead.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report >>

AVALON RARE MTL (AVL): Free Stock Analysis Report

CAMECO CORP (CCJ): Free Stock Analysis Report

IMPALA ADR (IMPUY): Free Stock Analysis Report

STILLWATER MNG (SWC): Free Stock Analysis Report

Zacks Investment Research

$CCJ - Cameco Port Hope Conversion Facility Workers Accept Contracts

http://finance.yahoo.com/news/cameco-port-hope-conversion-facility-154607775.html

SASKATOON, SASKATCHEWAN--(Marketwired - Jul 5, 2013) - Cameco (CCO.TO) (CCJ) announced today that unionized employees at Cameco's Port Hope conversion facility have voted to accept new collective agreements.

More than 250 employees, represented by United Steelworkers locals 13173 and 8562, have agreed to three-year contracts that include a six per cent wage increase over the term of the agreements. The previous contracts expired on June 30, 2013.

Cameco's Port Hope plant is the only uranium conversion facility in Canada producing uranium hexafluoride (UF6) and the only commercial supplier of natural uranium dioxide (UO2) conversion services needed to produce fuel for Candu nuclear reactors. Total workforce at the Port Hope conversion facility, including managers and salaried employees, is approximately 370.

Profile

Cameco, with its head office in Saskatoon, Saskatchewan, is one of the world's largest uranium producers. The company's uranium products are used to generate electricity in nuclear energy plants around the world, providing one of the cleanest sources of energy available today. Cameco's shares trade on the Toronto and New York stock exchanges.

As used in this news release, "Cameco" or the "company" means Cameco Corporation, a Canadian corporation and its subsidiaries and affiliates unless stated otherwise.

Contact:

$CCJ - CEO's Corner - questions and videos

http://www.cameco.com/investors/ceo_corner/

$CCJ - Cameco Business Video

http://www.cameco.com/about/

$CCJ - Commodities Today: Oil And Uranium Looking Bullish

http://seekingalpha.com/article/1531182-commodities-today-oil-and-uranium-looking-bullish?source=yahoo

... "Uranium

Much of our focus recently has been upon Ur-Energy (URG), which has defied gravity and continued its climb higher. The stock has left everyone in the dust, including producers such as Cameco (CCJ) and Uranium Energy Corporation (UEC); two other names we are bullish of. For readers of ours who were not with us during the last uranium bull market we want to explain the industry and how the stock prices generally fluctuate.

Summer has claimed much of the gains some of the uraniums had, but defying the typical downturn has been Ur-Energy, which has nearly doubled since May.

(click to enlarge)

Source: Yahoo Finance.

First, in the early stages of the bull market the juniors who are bringing projects online tend to do best, a category that Ur-Energy finds itself in currently. Then the juniors who are in the exploration phase tend to power the sector higher as investors redeploy their gains in the next wave of mines. This is followed by the large producers outpacing the industry, which indicates that the party is officially over. Generally during this last phase the junior exploration companies have already seen their stock prices fall dramatically and it is pretty obvious as to what is happening.

With all of this said, we want to point out that we are yet to see the first phase as the entire industry is concerned. The rally is having the foundation put in place by those early birds, but it cannot start until the Russians officially pull out of their agreement to supply the world with cheap uranium. We expect this to happen, everyone expects this to happen and the Russians should do it as they will get over 5x more per pound by pulling out of the agreement. It is a simple business decision and one which is merely months away. This is why we are so bullish of the sector right now." ...

$CCJ - Cues from Cameco

Publisher: U3O8.biz

Author: Vivien Diniz

June 30, 2013

http://www.u3o8.biz/s/MarketCommentary.asp?ReportID=590635&_Type=Market-Commentary&_Title=Cues-from-Cameco

If there is one uranium company investors should be familiar with, it is Cameco (TSX:CCO,NYSE:CCJ). Cameco is one of the world's largest publicly traded uranium companies, with 25 years of experience under its belt. The company supplies over 14 percent of the world's uranium from mines in Canada, the United States and Kazakhstan. Among its Canadian properties, Cameco operates the low-cost McArthur mine which is the world's largest high-grade uranium mine. The company is also looking to bring Cigar Lake --- the world's second highest-grade uranium deposit --- online this year.

Uranium Investing News reached out to Cameco to see how the biggest kid on the playground has been dealing with the slump in uranium prices and what investors can expect from the uranium producer in the future.

"In 2012 we adjusted our growth strategy to increase annual supply to 36 million pounds of U3O8 by 2018 (previous target was 40 million pounds by 2018)," Carey Hyndman, a spokesperson for the company, told Uranium Investing News. "We expect to grow production primarily from brownfield expansions and development projects. Our greenfield projects will provide options and will be advanced at a pace measured to market opportunities."

The company has indeed been busy working on its growth strategy. In the latter half of 2012, Cameco made a number of acquisitions that it believes will serve it well in the future. These include attaining majority ownership of the Millennium project in Saskatchewan and acquiring nuclear fuel product and service broker and trader NUKEM as well as the Yeelirrie project in Australia.

"In the context of our uranium growth strategy, we are currently focused on brownfield expansion (around existing infrastructure) and on developing projects with greater near-term certainty," Hyndman said.

The uranium miner is also interested in growth markets and in particular is taking advantage of the opportunities presented by reactors being built in China, India and the Middle East. The company sees the progress on intergovernmental agreements as a positive factor that will lead to Canadian uranium being supplied many of those markets. Currently, Cameco has two long-term supply agreements with Chinese utilities and is continuing to look for more opportunities.

Near-term benefits

There are several catalysts on the horizon for uranium, including Japan's reactors coming back online post-Fukushima, the end of the Highly Enriched Uranium (HEU) program in the United States and the influx of proposed and planned reactors world wide. As a result, analysts are calling uranium the number-one contrarian investment in the current market, with prices getting reading to soar at some point in the near-term future. Should all the stars line up as market watchers hope, Cameco could be the first to benefit from the coming rise in prices.

"We have a number of projects that are ready to respond, should the market reflect a need for more uranium," Hyndman said.

When demand increases, investors can expect Cameco to ramp up production at Inkai (Kazakhstan), develop the Millennium project (Saskatchewan) and develop the Kintyre project (Australia) and/or the Yeelirrie project (Australia) once the markets take a turn for the better.

Cigar Lake start up

The development of Cameco's Cigar Lake deposit was brought to an abrupt stop in June of 2005 when extreme flooding caused a delay and what was initially expected to be a six-month setback turned into an indefinite delay. Now, in 2013, the company has received its operating license from the Canadian Nuclear Safety Commission and is targeting a startup in Q4 2013.

"We have worked very hard to address the water inflow risk by increasing our pumping, water treatment and surface storage capacities, modifying the underground mine layout to increase the distance from water-bearing rock formations, and by increasing the use of freeze technology. We continue to make solid progress at Cigar Lake and the operating license was an important part of our path forward," Hyndman said. "The jet boring system continues to be tested and we are preparing for commissioning in ore in mid-2013. We remain on track for the first packaged pounds of U3O8 in the fourth quarter of 2013."

Acquisitions?

The Athabasca Basin is Canada's most prolific region for uranium. With current prices, the high-grade deposits of the basin have made it one of the only profitable regions operating. That explains the flurry of activity that has surrounded the region, with exploration companies staking their claims where they can, hoping to develop the next great deposit.

With that in mind, Uranium Investing News had to ask what Cameco thinks of the aggressive exploration efforts being made in the Athabasca Basin.

"What's good for the industry, is good for Cameco. More investment means more development of possible projects, so that is always encouraging," Hyndman said.

Not to be overlooked, a big player in the region will no doubt be keeping an eye out for acquisition targets. Without giving away too much, Cameco offered some insight on the criteria that it uses when gauging potential targets.

"Timing, price, project fundamentals and many other factors will be considered when we look at corporate development opportunities that could benefit Cameco."

Good article about this stock and company at Seeking Alpha this morning by Vineet Dutta:

http://seekingalpha.com/article/1119381-cameco-an-alternative-metal-play-that-is-beginning-to-look-attractive

Cameco and Denison Mines Look to Benefit From Rebounding Uranium Demand http://finance.yahoo.com/q?s=DNN <<<<< #demand #mkt #yuan #japan #yen #urainum

I'm guessing customers won't be forcing the spot price down any/much longer:

http://www.mining.com/uranium-set-to-get-a-boost-from-japanese-election-outcome-71924/

Japan coming back on line doesn't hurt either and is good news all around...

Japan PM set to order nuclear restart at weekend

TOKYO — Japan's prime minister is set to defy fierce public sentiment this weekend and order nuclear reactors back online for the first time since Fukushima, as he seeks to head off a summer energy crunch.

Yoshihiko Noda is expected to tell Kansai Electric Power (KEPCO) to re-fire two idled reactors at its Oi plant serving the industrial heartland of western Japan.

The controversial move comes amid fears that electricity demand will outstrip supply as temperatures soar and air-conditioners get cranked up, further crimping Japan's wobbly economic recovery.

Noda is due Saturday to meet Issei Nishikawa, the pro-nuclear power governor of central Fukui prefecture, which hosts the plant. Nishikawa is widely expected to tell the prime minister he is ready to accept the restarts after he received safety assurances Friday from the operator.

The nod from Nishikawa is the final link in the chain for Noda, who has become a vocal advocate of nuclear power being brought back into the energy mix for resource-poor but electricity-hungry Japan.

The country's 50 working reactors -- which along with the four crippled units at Fukushima contributed around a third of Japan's electricity before the disaster -- have been offline since the last one was shuttered in early May.

Public opposition in the aftermath of the tsunami-sparked meltdowns at Fukushima in March 2011 left Japan's political classes tip-toeing around the issue of restarts.

Radiation was spread over homes and farmland in a large area of northern Japan when the massive tsunami swamped cooling systems at Fukushima Daiichi.

No one is officially recorded as having died as a direct result of the meltdowns, but tens of thousands of people were evacuated and many remain so, with warnings some areas will be uninhabitable for decades.

Anti-nuclear sentiment among the public has run into increasingly apocalyptic warnings of power shortfalls, the most dire of which predicted Kansai's manufacturing base could see a one-fifth gap.

KEPCO has cautioned this will mean blackouts, which are expected to wallop producers already struggling against a tide of economic uncertainty and export markets stumbling under the pressure of Europe's debt crisis.

However, Noda's conviction that Japan could not do without nuclear power was not enough, forcing him to seek cover from international bodies and local politicians.

The government's own rules say reactors must pass International Atomic Energy Agency-approved stress tests designed to demonstrate they could withstand a natural disaster, and then get assent from their host communities.

Last week Noda set out the case for restarts in a televised press conference, saying they "support people's lives," but added that "I want to seek the understanding of local governments."

"Nuclear generation is an important power source (and) energy security is one of the country's most important issues," he added.

Earlier this week the mayor of the town of Oi, Shinobu Tokioka, gave his approval, after being offered safety assurances by an expert panel.

He said he believed the town "should fulfil its duty of supplying energy".

Fukui's governor is expected to fall in line after meeting Friday with the president of Kansai Electric Power, who promised continued effort towards attaining "the world's top-safety standards", Jiji Press reported.

Noda said last week a nuclear re-start was not a short-term solution and atomic power had its place in the country's future energy mix.

"If electricity fees go up due to an increasing dependence on fossil fuel, it would affect people like retailers, small- and mid-size companies and general households which are barely making ends meet," he said.

"If that leads to a hollowing out of business, it would decrease employment opportunities. The temporary operation of the reactors in summer would not secure our way of life."

http://www.google.com/hostednews/afp/article/ALeqM5gYZptGs0kH0sZamYi4SIxDnQ2Zmw?docId=CNG.12982d97427da8dc8346dbd722ef25c5.2d1

Nice to see Cameco PPS rising a bit! I noticed we did well even in a market down day, and then today is the icing on the cake, staying strong over $20. I'm hoping we've turned the corner, and by the end of next year when the Russian/American plan to turn Russian nukes to power runs out, the price for Uranium should increase exponentially. The other reason I expect such an outcome is that China (not to mention India) has already been talking to both the Canadian Prime Minister, as well as the CEO of Cameco for a steady stream of our Yellow Cake! Anyways, this is a long term hold, and if you're wise, you can make a double or more from here, within few years.

Undervalued Uranium Miners On The Verge Of Being Acquired By Cameco...

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=76134409

http://seekingalpha.com/article/626001-undervalued-uranium-miners-on-the-verge-of-being-acquired-by-cameco?source=yahoo

Uranium Forecast: The Nuclear Industry’s Fundamental Shortage

http://www.wallstreetdaily.com/2012/04/26/uranium-price-forecast-the-nuclear-industrys-fundamental-shortage/

Speed the Way to PEA

Galaxy Prepares to Advance Two Quebec Graphite Projects

By Greg Klein

Imagine the disappointment. While performing airborne electro-magnetic surveys in eastern Quebec in 1998, the Finnish company Outokumpu found many strong conductors. That raised their hopes for massive sulphides and, with visions of a base metals discovery dancing in their heads, they followed up with groundwork. All they found was graphite. But one company’s trash is now another’s treasure.

Fourteen years later, the carbon allotrope is no longer mineral non grata but the mineral du jour, and Outokumpu’s disappointment is Galaxy Capital’s TSXV:GXY flagship Sun Graphite Project. With an experienced graphite hand in President/CEO Chris Healey, Galaxy is ready to push the project as fast as its potential will allow. “With the surface outcrops where we are, you can advance a property very quickly,” he declares.

Read more about this and other graphite plays. http://resourceclips.com/2012/04/11/speed-the-way-to-pea/

|

Followers

|

35

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

275

|

|

Created

|

07/02/04

|

Type

|

Free

|

| Moderators | |||

This board is for fundamental and technical discussion about Cameco Corp., CCJ.

Cameco is the world's largest uranium producer accounting for 19% of world production from its mines in Canada and the US.

Our leading position is backed by more than 500 million pounds of proven and probable reserves and extensive resources.

Cameco holds premier land positions in the world's most promising areas for new uranium discoveries in Canada and Australia as part of an intensive global exploration program.

Cameco is also a leading provider of processing services required to produce fuel for nuclear power plants, and generates 1,000 MW of clean electricity through a partnership in North America's largest nuclear generating station located in Ontario, Canada.

www.cameco.com/investor_relations/about_us/

Cameco Corporation (Cameco) is primarily engaged in the exploration for and the development, mining, refining and conversion of uranium for sale as fuel for generating electricity in nuclear power reactors in Canada and other countries. The Company has a 31.6% interest in Bruce Power L.P. (BPLP), which operates the four Bruce B nuclear reactors in Ontario. The Company wholly owns Zircatec Precision Industries, Inc., whose primary business is the fabrication of nuclear fuel bundles. Cameco's 52.7% subsidiary Centerra Gold Inc. (Centerra) is involved in the exploration for and the development, mining and sale of gold. Cameco has four segments: uranium, fuel services, nuclear electricity generation and gold. In June 2006, the Company acquired a 19.5% interest in UNOR Inc, whose principal properties are 226 mineral claims in northwestern Nunavut on the Hornby Basin.

2121-11th Street West

Saskatoon, SK S7M 1J3

(306) 956-6200

(306) 956-6201

http://www.cameco.com/

Daily One-Year Charts

Weekly Five-Year Charts

Communism's True Believers Won't Give Up -

http://www.henrymakow.com/communisms_useful_idiots_wont.html

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |