News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

CVS Health (CVS) Sees Large Growth in Short Interest

By: MarketBeat | August 20, 2021

• CVS Health Co. (NYSE:CVS) was the recipient of a large growth in short interest in the month of July. As of July 30th, there was short interest totalling 16,100,000 shares, a growth of 15.9% from the July 15th total of 13,890,000 shares. Based on an average daily volume of 6,220,000 shares, the short-interest ratio is currently 2.6 days...

Read Full Story »»»

DiscoverGold

DiscoverGold

Can CVS Stock Reach $100? Pounding The Table On My Top 2021 Pick

Aug. 24, 2021 12:20 PM ET

CVS Health Corporation (CVS)

Read the article at this link to also see the graphics:

https://seekingalpha.com/article/4451526-cvs-stock-reach-100-top-2021-pick?mail_subject=cvs-can-cvs-stock-reach-100-pounding-the-table-on-my-top-2021-pick&utm_campaign=rta-stock-article&utm_content=link-0&utm_medium=email&utm_source=seeking_alpha

People are overlooked for a variety of biased reasons and perceived flaws. Age, appearance, personality. Bill James and mathematics cuts straight through that. Billy, of the twenty thousand knowable players for us to consider, I believe that there is a championship team of twenty five people that we can afford. Because everyone else in baseball undervalues them. Like an island of misfit toys.

-Peter Brand, Moneyball (2011)

CVS Health prices tender offer for up to ~$2.05B senior notes

Aug. 23, 2021 11:48 AM ETCVS Health Corporation (CVS)By: Ravikash, SA News Editor

CVS Health (CVS +0.2%) priced the tender offer for up to ~$2.05B of its 4.3% senior notes due 2028.

(the "Notes").

The reference yield is 1.250%. Total consideration $1.162.08 per $1,000 principal amount of notes validly tendered.

The company said notes validly tendered prior to 5:00 p.m., New York City time on Aug. 20 will be eligible to receive the total Consideration, which includes the early tender payment of $30 per $1,000 principal amount of notes.

CVS Health expects to accept for purchase and make payment for notes validly tendered on Aug. 24.

Sounds as if they will be redeeming notes to push out the due date.

Q3 2021 EPS Estimates for CVS Health Co. (CVS) Cut by Oppenheimer

By: MarketBeat | August 9, 2021

CVS Health Co. (NYSE:CVS) - Research analysts at Oppenheimer decreased their Q3 2021 earnings estimates for CVS Health in a research note issued on Wednesday, August 4th. Oppenheimer analyst M. Wiederhorn now forecasts that the pharmacy operator will earn $1.73 per share for the quarter, down from their previous forecast of $1.82. Oppenheimer also issued estimates for CVS Health's Q4 2021 earnings at $1.59 EPS, FY2021 earnings at $7.77 EPS, Q1 2022 earnings at $2.02 EPS, Q2 2022 earnings at $2.19 EPS, Q3 2022 earnings at $2.05 EPS and FY2022 earnings at $8.31 EPS...

Read Full Story »»»

DiscoverGold

CVS Health (CVS) PT Raised to $101.00 at Deutsche Bank Aktiengesellschaft

By: MarketBeat | August 4, 2021

CVS Health (NYSE:CVS) had its price target lifted by stock analysts at Deutsche Bank Aktiengesellschaft from $95.00 to $101.00 in a report issued on Thursday, The Fly reports. The firm presently has a "buy" rating on the pharmacy operator's stock. Deutsche Bank Aktiengesellschaft's target price points to a potential upside of 23.85% from the company's previous close...

Read Full Story »»»

DiscoverGold

CVS Stock Slides As COVID Cost Concerns Cloud Earnings Beat, Guidance Boost

By: TheStreet | August 4, 2021

• New CEO Karen Lynch said the quarter was highlighted by "broad sales and earnings outperformance, as well as sequential operating margin improvement."

CVS Health Corp. (CVS) posted stronger-than-expected second quarter earnings Wednesday, and lifted its full year profit guidance, thanks in part to a solid rebound in retail and pharmacy sales.

The stock traded lower, however, after the retailer said it would raise its minimum wage to $15 per hour in 2022 and noted COVID-related costs would rise over the final half of this year.

CVS said adjusted earnings for the three months ending in March were pegged at $2.42 per share, down 8.3% from the same period last year but well ahead of the Street consensus forecast of $2.06 per share. Group revenues, CVS said, rose 11.1% from last year to $72.6 billion, again topping analysts' estimates of a $70.3 billion tally.

Looking into the 2021 financial year, CVS lifted its forecast for adjusted earnings, which it now sees in the region of $7.70 to $7.80 per share, from its prior forecast of $7.56 to $7.68 per share.

"We delivered another quarter of strong results and once again raised our outlook for the year," said CEO Karen Lynch. "This quarter was highlighted by broad sales and earnings outperformance, as well as sequential operating margin improvement."

"We continue to play a critical role in helping America prevail against the pandemic while demonstrating the effectiveness of our unique business model, which is focused on meeting customer needs through innovations that make health care more local, affordable and connected," she added.

CVS shares were marked 3.23% lower in early trading immediately following the earnings release to change hands at $81.41 each.

Pharmacy Services revenues rose 9.7% to $38.3 billion, CVS said, Retail sales rose 14.3% to $24.73 billion, "driven by increased prescription volume, COVID-19 vaccinations and diagnostic testing and higher front store revenues across all product categories.

The group's healthcare benefits division saw sales rise 11.1% to $20.5 billion as it added Aetna's operations to its legacy business.

Read Full Story »»»

DiscoverGold

CVS Health EPS beats by $0.35, beats on revenue, raises guidance • 6:31 AM

CVS Health (NYSE:CVS): Q2 Non-GAAP EPS of $2.42 beats by $0.35; GAAP EPS of $2.10 beats by $0.39.

Revenue of $72.61B (+11.1% Y/Y) beats by $2.34B.

Raised GAAP diluted EPS guidance range to $6.35 to $6.45 from $6.24 to $6.36 vs. $5.47 in FY20

Raised Adjusted EPS guidance range to $7.70 to $7.80 from $7.56 to $7.68 vs. $7.67 consensus.

Raised cash flow from operations guidance range to $12.5 billion to $13.0 billion from $12.0 billion to $12.5 billion vs. $15.9B in FY20

CVS Health (CVS) Stock Jumps After Retail-Driven Earnings Beat; Profit Guidance Boost

By: TheStreet | August 4, 2021

• New CEO Karen Lynch said the quarter was highlighted by "broad sales and earnings outperformance, as well as sequential operating margin improvement."

CVS Health Corp. (CVS) posted stronger-than-expected second quarter earnings Wednesday, and lifted its full year profit guidance, thanks in part to a solid rebound in retail and pharmacy sales.

CVS said adjusted earnings for the three months ending in March were pegged at $2.42 per share, down 8.3% from the same period last year but well ahead of the Street consensus forecast of $2.06 per share. Group revenues, CVS said, rose 11.1% from last year to $72.6 billion, again topping analysts' estimates of a $70.3 billion tally.

Looking into the 2021 financial year, CVS lifted its forecast for adjusted earnings, which it now sees in the region of $7.70 to $7.80 per share, from its prior forecast of $7.56 to $7.68 per share.

"We delivered another quarter of strong results and once again raised our outlook for the year," said CEO Karen Lynch. "This quarter was highlighted by broad sales and earnings outperformance, as well as sequential operating margin improvement."

"We continue to play a critical role in helping America prevail against the pandemic while demonstrating the effectiveness of our unique business model, which is focused on meeting customer needs through innovations that make health care more local, affordable and connected," she added.

CVS shares were marked 1.15% higher in pre-market trading immediately following the earnings release to indicate an opening bell price of $84.97 each.

Pharmacy Services revenues rose 9.7% to $38.3 billion, CVS said, Retail sales rose 14.3% to $24.73 billion, "driven by increased prescription volume, COVID-19 vaccinations and diagnostic testing and higher front store revenues across all product categories.

The group's healthcare benefits division saw sales rise 11.1% to $20.5 billion as it added Aetna's operations to its legacy business.

Read Full Story »»»

DiscoverGold

Earnings Previews: CVS Health (CVS),...

By: 24/7 Wall St. | August 2, 2021

CVS Health

The country’s second-largest provider of health care plans, CVS Health Corp. (NYSE: CVS), has seen its stock price rise by more than 34% in the past 12 months. For the year to date, shares are up about 23%. The 12-month gain is about 5% below that of UnitedHealth but about 4% more year to date. Since July 1, the stock trades roughly flat, having recovered from a mid-month plunge related to the recall of a sunscreen product.

Analysts remain bullish on the stock, with 19 of 26 surveyed brokerages giving the stock a Buy or Strong Buy rating. The rest rate the shares at Hold. At a recent price of around $82.40, the stock’s upside potential based on a median price target of $95.50 is about 16%. At the high price target of $107, the implied upside is almost 30%.

The consensus revenue estimate is $70.27 billion, up 1.7% sequentially and about 7.8% year over year. Adjusted earnings per share (EPS) are forecast at $2.07, which would be three cents higher sequentially and down nearly 22% year over year. For the full year, analysts are looking for EPS of $7.67, up 2.2%, and revenue of $281.75, or about 4.9% more year over year.

The stock trades at 10.8 times expected 2021 EPS, 10.0 times estimated 2022 earnings and 9.1 times estimated 2023 earnings. The stock’s 52-week range is $55.36 to $90.61. CVS Health pays an annual dividend of $2.00 (yield of 2.43%)...

Read Full Story »»»

DiscoverGold

CVS Health (CVS) Expected to Beat Earnings Estimates: Should You Buy?

By: Zacks Equity Research | July 28, 2021

The market expects CVS Health (CVS) to deliver a year-over-year decline in earnings on higher revenues when it reports results for the quarter ended June 2021. This widely-known consensus outlook is important in assessing the company's earnings picture, but a powerful factor that might influence its near-term stock price is how the actual results compare to these estimates.

The stock might move higher if these key numbers top expectations in the upcoming earnings report, which is expected to be released on August 4. On the other hand, if they miss, the stock may move lower.

While the sustainability of the immediate price change and future earnings expectations will mostly depend on management's discussion of business conditions on the earnings call, it's worth handicapping the probability of a positive EPS surprise.

Zacks Consensus Estimate

This drugstore chain and pharmacy benefits manager is expected to post quarterly earnings of $2.07 per share in its upcoming report, which represents a year-over-year change of -21.6%.

Revenues are expected to be $70.08 billion, up 7.3% from the year-ago quarter.

Estimate Revisions Trend

The consensus EPS estimate for the quarter has been revised 0.23% lower over the last 30 days to the current level. This is essentially a reflection of how the covering analysts have collectively reassessed their initial estimates over this period.

Investors should keep in mind that an aggregate change may not always reflect the direction of estimate revisions by each of the covering analysts.

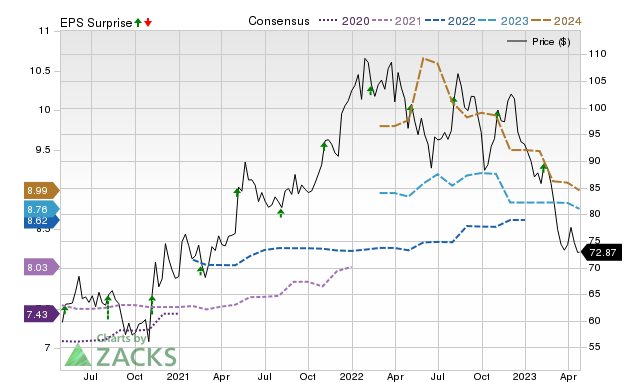

Price, Consensus and EPS Surprise

Earnings Whisper

Estimate revisions ahead of a company's earnings release offer clues to the business conditions for the period whose results are coming out. Our proprietary surprise prediction model -- the Zacks Earnings ESP (Expected Surprise Prediction) -- has this insight at its core.

The Zacks Earnings ESP compares the Most Accurate Estimate to the Zacks Consensus Estimate for the quarter; the Most Accurate Estimate is a more recent version of the Zacks Consensus EPS estimate. The idea here is that analysts revising their estimates right before an earnings release have the latest information, which could potentially be more accurate than what they and others contributing to the consensus had predicted earlier.

Thus, a positive or negative Earnings ESP reading theoretically indicates the likely deviation of the actual earnings from the consensus estimate. However, the model's predictive power is significant for positive ESP readings only.

A positive Earnings ESP is a strong predictor of an earnings beat, particularly when combined with a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold). Our research shows that stocks with this combination produce a positive surprise nearly 70% of the time, and a solid Zacks Rank actually increases the predictive power of Earnings ESP.

Please note that a negative Earnings ESP reading is not indicative of an earnings miss. Our research shows that it is difficult to predict an earnings beat with any degree of confidence for stocks with negative Earnings ESP readings and/or Zacks Rank of 4 (Sell) or 5 (Strong Sell).

How Have the Numbers Shaped Up for CVS Health?

For CVS Health, the Most Accurate Estimate is higher than the Zacks Consensus Estimate, suggesting that analysts have recently become bullish on the company's earnings prospects. This has resulted in an Earnings ESP of +0.54%.

On the other hand, the stock currently carries a Zacks Rank of #3.

So, this combination indicates that CVS Health will most likely beat the consensus EPS estimate.

Does Earnings Surprise History Hold Any Clue?

Analysts often consider to what extent a company has been able to match consensus estimates in the past while calculating their estimates for its future earnings. So, it's worth taking a look at the surprise history for gauging its influence on the upcoming number.

For the last reported quarter, it was expected that CVS Health would post earnings of $1.72 per share when it actually produced earnings of $2.04, delivering a surprise of +18.60%.

Over the last four quarters, the company has beaten consensus EPS estimates four times.

Bottom Line

An earnings beat or miss may not be the sole basis for a stock moving higher or lower. Many stocks end up losing ground despite an earnings beat due to other factors that disappoint investors. Similarly, unforeseen catalysts help a number of stocks gain despite an earnings miss.

That said, betting on stocks that are expected to beat earnings expectations does increase the odds of success. This is why it's worth checking a company's Earnings ESP and Zacks Rank ahead of its quarterly release. Make sure to utilize our Earnings ESP Filter to uncover the best stocks to buy or sell before they've reported.

CVS Health appears a compelling earnings-beat candidate. However, investors should pay attention to other factors too for betting on this stock or staying away from it ahead of its earnings release.

Read Full Story »»»

DiscoverGold

CVS Health Co. (CVS) Given Consensus Recommendation of "Buy" by Brokerages

By: MarketBeat | July 22, 2021

• CVS Health Co. (NYSE:CVS) has been given a consensus recommendation of "Buy" by the nineteen analysts that are currently covering the firm, Marketbeat.com reports. Four research analysts have rated the stock with a hold rating, eleven have issued a buy rating and one has given a strong buy rating to the company. The average 12 month price target among brokerages that have issued ratings on the stock in the last year is $92.47...

Read Full Story »»»

DiscoverGold

CVS Health Target of Unusually Large Options Trading (CVS)

By: MarketBeat | July 22, 2021

• CVS Health Co. (NYSE:CVS) was the recipient of some unusual options trading activity on Wednesday. Traders bought 125,959 call options on the stock. This represents an increase of approximately 984% compared to the average daily volume of 11,619 call options...

Read Full Story »»»

DiscoverGold

CVS Health: Still An Attractive Value Opportunity

Jul. 14, 2021 4:28 PM ET

CVS Health Corporation (CVS)

Daniel Petersen

Deep Value, Long Only, Value, Growth

Contributor Since 2020

A 22 year old student with a great interest in the stock market and value investing. I believe I know a fair bit about the topic, and that I could provide helpful guidance sharing my thoughts.

Summary

The company has been paying down debt, and will soon continue to raise the dividend.

The growth has been consistent and is expected to continue.

The stock is currently offering low double digits in stock returns from the current share price.

CVS Beats Revenue Expectations Aided By COVID-19 Testing And Vaccinations

Introduction

Recent years have not been kind to investors of CVS Health (NYSE:CVS), who have experienced six years of price stagnation. Apart from no share appreciation, the dividend has not grown, no shares have been bought back and the company is still carrying a lot of debt, which is making investors hesitant about buying the company.

A majority of investors would stay away from a company with those characteristics, which is exactly why I am drawn to this company. Value is often found where no one else is looking.

Who is CVS Health?

CVS Health is a major US company, operating within the healthcare segment. The company is the owner of the CVS pharmacy chains, the US health insurance provider, Aetna, among other businesses as well. It is the largest US- only corporation and the largest to only serve one country. It is also a member of the Fortune 500 list, and the Fortune global 500.

The company used to have a stellar performance of dividend increases, but was paused after the Aetna acquisition. As debt is being repaid and the business continues to grow, it is only a matter of time, before the increases will continue.

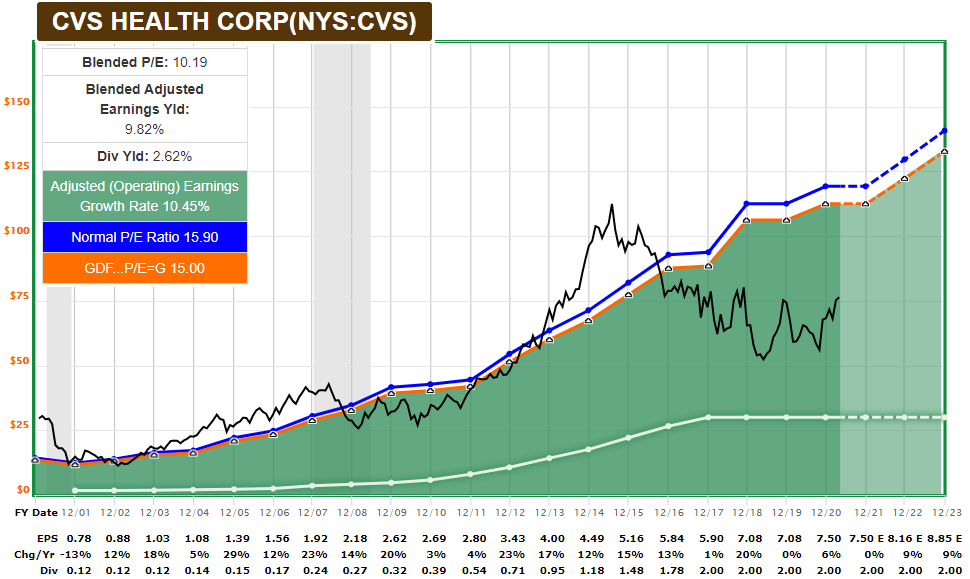

Fundamentals

The revenue growth is very consistent, which is very encouraging. Growth has averaged high single digits and is a mix of organic- and acquired growth. The company bought Aetna in 2018, which is the cause of the recent increase in revenue growth. Excluding acquisitions, low single digits in revenue growth are seen and is expected by analysts to continue.

CVS stock revenue

(Source: Macrotrends.com)

A consistently growing top line is impressive, but a growing bottom line is equally important. CVS has managed to keep their margins stable within a tight range, which has helped to increase the bottom line. The only major fluctuation seen, was in connection with the purchase of the LTC business, in which CVS took a $6.1b impairment of capital assets charge.

While their net profit margins have never fully recovered to the +3% range, the company has still managed to grow on a per-share-basis, but it did come at the cost of a high debt pile. Nevertheless, growing net income, stable margins and low capital expenditures, have turned the company into an efficient cash flow producer.

CVS stock net income

(Source: Macrotrends.com)

Management has not been hesitant in distributing the cash, which is of course a good thing, but some of the timings have been questionable. Buying back shares in 2014-2015 with a p/e above 20 just to issue additional stock 3 years later at a p/e of ~9, is an inefficient use of money and hurt shareholders.

They bought back shares when they should have been issuing shares, and issued shares when they should have been repurchasing shares.

Besides having repurchased their own shares, the company also has an impressive history of dividend payments. The dividend has not been reduced since its first payout, but has not been increased in recent years either. It is currently yielding 2.45% with a low payout ratio of 26.7%. Very manageable and a lot of room to climb, when the company has paid down their debt.

CVS shares outstanding

(Source: Macrotrends.com)

The company has an excellent growing topline and stable margins, which is leading to consistent net income and a lot of free cash flow. The dividend is safe, but is being held down by its debt burden. Recent timings of issuance of shares and repurchasing stock seem questionable, but unfortunately not uncommon to see among other businesses as well.

Valuation

As with most slow/medium growing companies, a 15 multiple is close to intrinsic value. The company has been through periods of overvaluation and undervaluation, but has always returned to the multiple. Even though the share price has been stagnant, the underlying business continues to strengthen, and that is what is important. A return to a standard 15 p/e would give it a price of ~$114, which I would consider a fair valuation.

Sometimes a business is trading at a low multiple because of debt. A company can comfortably carry 3x their free cash flow in net debt. CVS as of their latest quarter is carrying $56.3b in net debt and FCF of $13b, which is leaving ~$16b in excess debt that I would add to its market cap to ensure not overpaying. That gives the company a slightly higher multiple, but still below a fair 15 multiplier.

Fastgraph EPS

(Source: Fastgraphs.com)

Free cash flow is very much in line with operating earnings and is showing strong growth as well. It is expected to decline this year, but should stabilize soon after. A 15 multiple would indicate a fair price of ~$113, very close to the price of operating earnings. With the excess debt added to its market cap, we get a ~9.4 p/fcf multiple, slightly higher than its current 8.2 multiple, but still in deep value territory.

Fastgraphs FCF

(Source: Fastgraphs.com)

Stock chart

Quick disclaimer. A technical analysis by itself is not a good enough reason to buy a stock, but combined with the fundamentals of the company, it can greatly narrow your price target range when buying.

I buy when fundamentals and stock chart performance align. I missed the initial entry when the stock found support at its 200- month moving average back in Marts 2020, but still bought a small position the following days. I patiently waited for a potential dip in October 2020, but it missed the moving average by ~3.5%, which would have been my price target.

The stock has since broken above its 50- month moving average and looks to be heading upwards. I will continue to hold my shares, and still find its current valuation attractive.

https://seekingalpha.com/article/4439238-cvs-health-stock-still-an-attractive-value-opportunity?mail_subject=cvs-cvs-health-still-an-attractive-value-opportunity&utm_campaign=rta-stock-article&utm_content=link-0&utm_medium=email&utm_source=seeking_alpha

Tradingview

(Source: Tradingview.com)

Final thoughts

This is a company with great fundamentals. It seems very predictable and consistent, pointing towards the business having a competitive edge. The general sentiment towards the business is skewed because of previous years of price stagnation, despite the underlying business continuing to strengthen.

The dividend increases and share repurchases was paused to pay down debt, which has improved a lot. Debt still remains high, but it is quickly improving. A combination of the underlying business continuing to grow, the balance sheet improving and soon dividend increases and share buybacks to resume, the market cannot continue to value it with such low multiples.

My estimate of a fair valuation is near $113, and is based on operating earnings and free cash flow. Stock chart performance is pointing towards the stock having found support and should rebound with time.

I am therefore giving it a “bullish” rating.

CVS Health Co. to Post Q1 2022 Earnings of $2.11 Per Share, Truist Securiti Forecasts

By: MarketBeat | July 8, 2021

CVS Health Co. (NYSE:CVS) - Research analysts at Truist Securiti issued their Q1 2022 earnings per share estimates for CVS Health in a report released on Tuesday, July 6th. Truist Securiti analyst D. Macdonald expects that the pharmacy operator will post earnings of $2.11 per share for the quarter. Truist Securiti also issued estimates for CVS Health's Q2 2022 earnings at $2.11 EPS, Q3 2022 earnings at $2.05 EPS, Q4 2022 earnings at $1.92 EPS and FY2023 earnings at $8.88 EPS. CVS Health (NYSE:CVS) last issued its quarterly earnings results on Tuesday, May 4th. The pharmacy operator reported $2.04 earnings per share for the quarter, beating analysts' consensus estimates of $1.72 by $0.32. CVS Health had a return on equity of 14.45% and a net margin of 2.73%. The business had revenue of $69.10 billion for the quarter, compared to the consensus estimate of $68.33 billion. During the same quarter in the previous year, the company posted $1.91 earnings per share. CVS Health's revenue for the quarter was up 3.5% compared to the same quarter last year...

Read Full Story »»»

DiscoverGold

CVS Health Co. (CVS) Plans $0.50 Quarterly Dividend

By: MarketBeat | July 7, 2021

CVS Health Co. (NYSE:CVS) declared a quarterly dividend on Wednesday, July 7th, RTT News reports. Shareholders of record on Friday, July 23rd will be paid a dividend of 0.50 per share by the pharmacy operator on Monday, August 2nd. This represents a $2.00 dividend on an annualized basis and a yield of 2.46%...

Read Full Story »»»

DiscoverGold

$CVS I thought vaccines would bring them a ton of extra foot traffic..

By: Options Mike | July 5, 2021

• $CVS I thought vaccines would bring them a ton of extra foot traffic.. seams like that is not really happening now.. for me loves this in dec @ 74 now.. I'm hesitant on it.. maybe off the 77 area if it pulls back

Read Full Story »»»

DiscoverGold

Insider Selling: CVS Health Co. (CVS) EVP Sells 2,781 Shares of Stock

By: MarketBeat | June 29, 2021

CVS Health Co. (NYSE:CVS) EVP Alan Lotvin sold 2,781 shares of the stock in a transaction on Monday, June 28th. The stock was sold at an average price of $83.67, for a total value of $232,686.27. Following the sale, the executive vice president now owns 61,048 shares in the company, valued at approximately $5,107,886.16. The transaction was disclosed in a filing with the Securities & Exchange Commission, which is available through this link...

Read Full Story »»»

DiscoverGold

CVS Health Co. (CVS) Given Consensus Rating of "Buy" by Brokerages

By: MarketBeat | June 29, 2021

Shares of CVS Health Co. (NYSE:CVS) have earned a consensus recommendation of "Buy" from the nineteen analysts that are covering the stock, MarketBeat reports. Four equities research analysts have rated the stock with a hold rating, eleven have given a buy rating and one has given a strong buy rating to the company. The average 12 month target price among brokers that have covered the stock in the last year is $92.47...

Read Full Story »»»

DiscoverGold

CVS Health (CVS) Given New $95.00 Price Target at Deutsche Bank Aktiengesellschaft

By: MarketBeat | June 22, 2021

CVS Health (NYSE:CVS) had its price objective reduced by analysts at Deutsche Bank Aktiengesellschaft from $99.00 to $95.00 in a research report issued on Tuesday, The Fly reports. The firm currently has a "buy" rating on the pharmacy operator's stock. Deutsche Bank Aktiengesellschaft's price objective would suggest a potential upside of 13.07% from the stock's previous close...

Read Full Story »»»

DiscoverGold

$70.36 Billion in Sales Expected for CVS Health Co. (CVS) This Quarter

By: MarketBeat | June 21, 2021

Brokerages expect CVS Health Co. (NYSE:CVS) to announce $70.36 billion in sales for the current fiscal quarter, according to Zacks Investment Research. Seven analysts have issued estimates for CVS Health's earnings. The lowest sales estimate is $68.94 billion and the highest is $73.26 billion. CVS Health reported sales of $65.34 billion in the same quarter last year, which indicates a positive year-over-year growth rate of 7.7%. The firm is scheduled to announce its next earnings results on Wednesday, August 4th...

Read Full Story »»»

DiscoverGold

Stumbling CVS Health (CVS) Could Stage a Climb

By: Schaeffer's Investment Research | June 15, 2021

• The 40-day moving average has been bullish for the stock in the past

• The stock has been cooling off from its recent highs

The shares of CVS Health Corporation (NYSE:CVS) have been falling since their recent May 24 four-year high of $90.61, which the stock climbed to after three-straight months of gains. Up 1.6% to trade at $85.98 at last check, CVS is flashing a historically bullish signal on the charts.

More specifically, the equity just came within one standard deviation of its ascending 40-day moving average, after spending several months above it. According to data from Schaeffer's Senior Quantitative Analyst Rocky White, six similar signals have occurred in the past three years. CVS Health stock enjoyed a positive return one month later in 67% of those cases, averaging a 5% gain. From its current perch, a comparable move would put CVS above the $90 level and close to its aforementioned four-year high.

Puts have been more popular than usual, too, leaving plenty of pessimism to be unwound in the options pits. This is per CVS' 10-day put/call volume ratio at the International Securities Exchange (ISE), Cboe Options Exchange (CBOE), and NASDAQ OMX PHLX (PHLX), which sits in the 97th percentile of its annual range.

What's more, CVS is seeing attractively priced premiums at the moment. The security's Schaeffer's Volatility Index (SVI) of 19% sits in just the 2nd percentile of its annual range, indicating options players are pricing in low volatility expectations right now.

Read Full Story »»»

DiscoverGold

Done! Thanks DG!!

Why 4 Jefferies Franchise List Stocks Could Be Big Second-Half Winners

By: 24/7 Wall St. | June 14, 2021

CVS Health

This top stock for more conservative accounts offers a very solid entry point. CVS Health Corp. (NYSE: CVS) is one of the largest health care companies in the United States, providing retail, mail and specialty pharmacy dispensing services and pharmacy benefits. CVS has become one of the most vertically integrated publicly traded health care companies.

CVS serves employers, insurance companies, unions, government employee groups, health plans, prescription drug plans, Medicaid managed care plans, plans offered on public health insurance and private health insurance exchanges, other sponsors of health benefit plans and individuals. This segment operates retail specialty pharmacy stores and specialty mail order, mail order dispensing, and compounding pharmacies, as well as branches for infusion and enteral nutrition services.

CVS completed a $69 billion purchase of health care provider Aetna in November of 2018 and remains one of the top picks for 2021 and beyond, as CVS has become one of the most vertically integrated publicly traded health care companies

Investors in CVS Health stock receive a solid 2.35% dividend. The Jefferies price target is $95, while the posted consensus price target is $94.29. The shares ended Friday trading at $85.47 apiece...

Read Full Story »»»

DiscoverGold

CVS Health (CVS) Updates FY 2021 Earnings Guidance

By: MarketBeat | June 8, 2021

• CVS Health (NYSE:CVS) updated its FY 2021 earnings guidance on Tuesday. The company provided earnings per share guidance of $7.560-7.680 for the period, compared to the Thomson Reuters consensus earnings per share estimate of $7.660. The company issued revenue guidance of -.

Several analysts have recently issued reports on the stock. Citigroup boosted their price objective on shares of CVS Health from $83.00 to $98.00 in a research note on Wednesday, May 5th. Royal Bank of Canada boosted their price objective on shares of CVS Health from $80.00 to $91.00 and gave the company an outperform rating in a research note on Wednesday, May 5th. Morgan Stanley boosted their price objective on shares of CVS Health from $86.00 to $92.00 and gave the company an overweight rating in a research note on Wednesday, April 14th. Credit Suisse Group lifted their target price on shares of CVS Health from $91.00 to $100.00 and gave the company an outperform rating in a report on Thursday, May 6th. Finally, Jefferies Financial Group lifted their target price on shares of CVS Health from $90.00 to $95.00 and gave the company a buy rating in a report on Wednesday, May 5th. Four analysts have rated the stock with a hold rating, eleven have issued a buy rating and one has given a strong buy rating to the company. CVS Health has a consensus rating of Buy and an average target price of $92.82.

Read Full Story »»»

DiscoverGold

Insider Selling: CVS Health Co. (CVS) EVP Sells 37,594 Shares of Stock

By: MarketBeat | June 8, 2021

• CVS Health Co. (NYSE:CVS) EVP Daniel P. Finke sold 37,594 shares of the company's stock in a transaction dated Monday, June 7th. The shares were sold at an average price of $86.60, for a total transaction of $3,255,640.40. Following the transaction, the executive vice president now owns 60,904 shares in the company, valued at $5,274,286.40. The transaction was disclosed in a filing with the SEC, which is available at the SEC website...

Read Full Story »»»

DiscoverGold

CVS Health Co. (CVS) Given Consensus Recommendation of "Buy" by Analysts

By: MarketBeat | June 4, 2021

Shares of CVS Health Co. (NYSE:CVS) have been assigned an average rating of "Buy" from the nineteen analysts that are currently covering the firm, Marketbeat Ratings reports. Four investment analysts have rated the stock with a hold recommendation, eleven have issued a buy recommendation and one has assigned a strong buy recommendation to the company. The average twelve-month price target among analysts that have issued a report on the stock in the last year is $92.82.

Read Full Story »»»

DiscoverGold

CVS Sees Significant Increase in Short Interest

By: MarketBeat | June 2, 2021

CVS Health Co. (NYSE:CVS) saw a significant growth in short interest in May. As of May 14th, there was short interest totalling 20,090,000 shares, a growth of 22.6% from the April 29th total of 16,380,000 shares. Based on an average trading volume of 7,270,000 shares, the short-interest ratio is presently 2.8 days.

Read Full Story »»»

DiscoverGold

CVS Health (CVS) Issues FY 2021 Earnings Guidance

By: MarketBeat | June 1, 2021

CVS Health (NYSE:CVS) issued an update on its FY 2021 earnings guidance on Tuesday morning. The company provided EPS guidance of 7.560-7.680 for the period, compared to the Thomson Reuters consensus EPS estimate of $7.660. The company issued revenue guidance of -.

Read Full Story »»»

DiscoverGold

CVS Health (CVS) Sees Unusually-High Trading Volume on Analyst Upgrade

By: MarketBeat | May 19, 2021

CVS Health Co. (NYSE:CVS) shares saw unusually-strong trading volume on Wednesday after BMO Capital Markets raised their price target on the stock from $90.00 to $96.00. BMO Capital Markets currently has a market perform rating on the stock. Approximately 541,008 shares changed hands during mid-day trading, a decline of 92% from the previous session's volume of 7,091,201 shares.The stock last traded at $88.03 and had previously closed at $88.61...

Read Full Story »»»

DiscoverGold

CVS Health (CVS) PT Raised to $93.00 at Wolfe Research

By: MarketBeat | May 19, 2021

CVS Health (NYSE:CVS) had its price target upped by investment analysts at Wolfe Research from $82.00 to $93.00 in a research report issued on Wednesday, The Fly reports. The brokerage presently has an "outperform" rating on the pharmacy operator's stock. Wolfe Research's price objective would indicate a potential upside of 4.95% from the stock's previous close...

Read Full Story »»»

DiscoverGold

CVS Health Corporation's (NYSE:CVS) Stock On An Uptrend: Could Fundamentals Be Driving The Momentum?

Simply Wall St

Wed, May 19, 2021, 3:37 AM·4 min read

https://finance.yahoo.com/news/cvs-health-corporations-nyse-cvs-073740262.html

CVS Health (NYSE:CVS) has had a great run on the share market with its stock up by a significant 22% over the last three months. We wonder if and what role the company's financials play in that price change as a company's long-term fundamentals usually dictate market outcomes. Specifically, we decided to study CVS Health's ROE in this article.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

How Do You Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for CVS Health is:

10% = US$7.4b ÷ US$71b (Based on the trailing twelve months to March 2021).

The 'return' refers to a company's earnings over the last year. Another way to think of that is that for every $1 worth of equity, the company was able to earn $0.10 in profit.

What Has ROE Got To Do With Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

CVS Health's Earnings Growth And 10% ROE

To begin with, CVS Health seems to have a respectable ROE. Be that as it may, the company's ROE is still quite lower than the industry average of 15%. Although, we can see that CVS Health saw a modest net income growth of 8.1% over the past five years.

So, there might be other aspects that are positively influencing earnings growth. For instance, the company has a low payout ratio or is being managed efficiently.

However, not to forget, the company does have a decent ROE to begin with, just that it is lower than the industry average. So this also provides some context to the earnings growth seen by the company.

As a next step, we compared CVS Health's net income growth with the industry and were disappointed to see that the company's growth is lower than the industry average growth of 13% in the same period.

past-earnings-growth

Earnings growth is a huge factor in stock valuation. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. This then helps them determine if the stock is placed for a bright or bleak future. What is CVS worth today? The intrinsic value infographic in our free research report helps visualize whether CVS is currently mispriced by the market.

Is CVS Health Making Efficient Use Of Its Profits?

CVS Health has a three-year median payout ratio of 36%, which implies that it retains the remaining 64% of its profits. This suggests that its dividend is well covered, and given the decent growth seen by the company, it looks like management is reinvesting its earnings efficiently.

Additionally, CVS Health has paid dividends over a period of at least ten years which means that the company is pretty serious about sharing its profits with shareholders.

Existing analyst estimates suggest that the company's future payout ratio is expected to drop to 24% over the next three years. As a result, the expected drop in CVS Health's payout ratio explains the anticipated rise in the company's future ROE to 13%, over the same period.

Summary

In total, it does look like CVS Health has some positive aspects to its business. In particular, it's great to see that the company is investing heavily into its business and along with a moderate rate of return, that has resulted in a respectable growth in its earnings.

The latest industry analyst forecasts show that the company is expected to maintain its current growth rate. .

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

$70.36 Billion in Sales Expected for CVS Health Co. (CVS) This Quarter

By: MarketBeat | May 15, 2021

Equities research analysts expect CVS Health Co. (NYSE:CVS) to post sales of $70.36 billion for the current fiscal quarter, Zacks Investment Research reports. Seven analysts have provided estimates for CVS Health's earnings. The highest sales estimate is $73.26 billion and the lowest is $68.94 billion. CVS Health posted sales of $65.34 billion during the same quarter last year, which would indicate a positive year-over-year growth rate of 7.7%. The firm is scheduled to announce its next earnings report on Wednesday, August 4th.

On average, analysts expect that CVS Health will report full year sales of $281.64 billion for the current year, with estimates ranging from $278.48 billion to $284.34 billion. For the next financial year, analysts anticipate that the business will report sales of $294.11 billion, with estimates ranging from $290.26 billion to $298.20 billion. Zacks Investment Research's sales averages are an average based on a survey of research firms that cover CVS Health.

Read Full Story »»»

DiscoverGold

The Smartest Stocks to Buy With $1,000 Right Now

Patient investors should be handsomely rewarded by this combination of growth and value stocks.

By: Sean Williams

https://finance.yahoo.com/m/d8f2149a-68a0-3528-bc6b-8ff103ce21f0/the-smartest-stocks-to-buy.html?source=eptyholnk0000202&utm_source=yahoo-host&utm_medium=feed&utm_campaign=article&yptr=yahoo

May 14, 2021 at 5:51AM

It's no secret that the stock market is one of the greatest wealth creators on the planet. Given the proper amount of time for investment theses to play out, great companies can generate game-changing wealth for patient investors.

What folks might not realize about Wall Street is that you don't need to be a millionaire to build wealth. If you have $1,000 that won't be needed to pay bills or cover emergencies, that's more than enough to begin or further your trek toward financial independence.

Here are some of the smartest stocks you can buy right now with $1,000.

CVS Health

For value-stock investors, pharmacy-chain CVS Health (NYSE:CVS) looks ripe for the picking.

Healthcare stocks are usually highly defensive and perfect to buy during a recession. That's because we don't get to choose when we get sick or what ailment(s) we develop, which sustains demand for drug and device makers. The same can't be said for CVS and its pharmacy peers, which were hammered by the coronavirus lockdowns. Less foot traffic into its stores and fewer clinic visits clearly hurt multiple aspects of its business.

The good news is that this is all temporary. What was a negative last year has quickly turned into a positive catalyst, with foot traffic higher in CVS stores as people look to get vaccinated.

CVS Health's management team has also shown the ability to think outside the box. Instead of growing horizontally, the company acquired health-benefits provider Aetna in late 2018. Adding Aetna increased the organic growth rate for the combined company and is leading to significant cost synergies. It also creates an incentive for more than 20 million insured individuals to stay within the CVS pharmacy network. Pharmacy sales are where CVS generates its juiciest margins.

Additionally, don't overlook the company's buildout of approximately 1,500 HealthHUB health clinics nationwide. These clinics will be primarily tasked with getting patients who have chronic health conditions in touch with specialists. HealthHUB gives CVS Health the opportunity to build rapport with potential repeat customers to its pharmacy.

A forward price-to-earnings ratio of just over 10 is simply too low for such a profitable business.

CVS: To $100 And Beyond

May 10, 2021 8:26 PM ET

CVS Health Corporation (CVS)

https://seekingalpha.com/article/4427116-cvs-to-100-and-beyond?mail_subject=cvs-cvs-to-100-and-beyond&utm_campaign=rta-stock-article&utm_content=link-0&utm_medium=email&utm_source=seeking_alpha

Summary

CVS is currently priced as a struggling company.

The prescription market is not a winner take all and investors should not be scared of AMZN's entrance.

Debt repayment is just starting to show benefits.

Expect CVS to be re-rated once buybacks and dividend increases resume.

CVS has the potential for a double at these levels by the end of FY25.

Overview

CVS (CVS) has been a retail stalwart for decades. At its most basic roots, CVS sells healthcare & beauty products, whilst providing pharmacy services. They currently hold 9,900+ stores across 49 states. Their foot print is large, as similar to Walmart (WMT); 75% of the U.S. population lives within five minutes of a CVS store. They are also one of America's top employers with an employee count that sits at over 300,000. With the acquisition of AETNA, and growing adoption of MinuteClinics, they now provide health coverage for over 23 million members and can combine their retail stores to create what management calls a 'Health Hub'.

During the COVID-19 pandemic, CVS's strength and capability came to the forefront as they were tasked by the federal government to go into long-term care facilities and nursing homes to administer the first COVID-19 vaccines. Through this program alone CVS was able to deliver 7.8 million on-site vaccinations. They have flexed their muscles once again by boasting that they have the capability to administer 20-25 million shots a month, which far exceeds the supply they can obtain.

This pandemic has brought to light the importance of CVS in the U.S. and I believe it will help change how investors look at the healthcare giant moving forward.

A simple re-rating from a more positive outlook from the market could lead to market-beating returns in the next few years. Combine that with the potential for significant buybacks and dividend increases, CVS is looking like a great total return play for long term investors.

Since its peak in 2015, CVS is down 25%, trading at less than 10xFCF.

Chart

Data by YCharts

Is Amazon A Problem?

On November 17th, 2020, Amazon (AMZN) announced that they will be offering free prescription deliveries for Amazon Prime members. This news alone sent CVS down 7% in a day. Just the thought of Amazon's entrance wiped $9 billion off their market cap in the blink of an eye.

Although it is true, Amazon tends to do well with all the endeavors it undertakes, rarely has it wiped solidified companies off the map. I would also like to point out that if Amazon's leadership wants a piece of your pie, you are doing things right, or are in a growing industry. In CVS's case, it's both. Think of Amazon's entrance into the streaming world. None of Netflix (NFLX), Disney (DIS), HBO Maxx, or Hulu took a hit. There was more than enough demand and room for all players to grow.

The fear of Amazon has also been played out against UPS (UPS), who for years, was put in the same situation that CVS is in now. UPS became the unloved legacy player in the e-commerce/delivery market while Amazon received all the attention from investors. The thought was that Amazon was slowly 'killing' UPS. From 2017 through early 2020, UPS traded flat as revenue grew at a fairly consistent pace. Even with a quickly growing e-commerce industry, UPS was looked at as Amazon's (AMZN) next victim. The pandemic struck and e-commerce trends accelerated. All players in that market have done great as the demand for their service far outweighs the risks of the stringent competition.

Chart

Data by YCharts

The healthcare market is not a zero sum game. Never has been and never will be. Although Amazon might bring you your prescription without you having to leave your house, they will never be able to provide the physical services such as vaccinations and health checkups/physicals that CVS can.

Not only am I not worried about Amazon, neither is management. Guidance continues to be raised or reiterated, meanwhile analysts have been consistently providing upward EPS revisions. Over the last three months, 21 revisions have been issued on CVS. All 21 of them have been upward.

Debt Is the Elephant In The Room

The market also seems to be highly uncomfortable with the high debt load. The AETNA acquisition brought on $45 billion of new financing, and they also assumed $8 billion of AETNA's debt as well. This left interest expense up 3x where it was before the acquisition. At the end of FY17, interest expense totaled $1.06 billion. In FY19, that number was now at $3.035 billion, which certainly does not bode well for free cash flow.

Source

q1-2021-data

Source

The bulk of their debt profile is maturing before 2030. If it is not refinanced and kicked down the road, management might be more cautious about committing larger amounts of capital directly to shareholders.

Management has not shied away from addressing their debt burden. This is what makes me so optimistic compared to other firms with so much debt. They are fully aware of the sentiment towards the debt and have been committed to driving it down with cash flow and cash on hand. In fact, they are doing it quite aggressively. As noted above, total long-term debt immediately after the acquisition took place, stood at $71.4 billion. The balance sheet in their most recent 10-Q has the debt at $59.2 billion. In the 1st quarter of FY21 alone, they paid back $3 billion of debt.

Management has repeatedly mentioned their target goal of reducing the leverage ratio down to 3x by 2022. At the current pace, it would not surprise me to see them reach that level before the end of FY21, or shortly after. Either way it seems as if they are ahead of schedule. Upon reaching that level is where my bull case for long term share holders truly begins.

Large Savings From Debt Repayment

Capital allocation towards shareholders since 2018 has been negligent. The dividend has remained flat, and buybacks were frozen. Upon CVS reaching the target leverage ratios mentioned above, CVS is looking to be even more of a cash flow machine.

The early debt repayments are already paying off. In FY19 and FY20, management had to commit $3 billion of cash just to interest paid. Q1FY21 was the first quarter since the AETNA acquisition that we have seen interest paid drop a meaningful amount; from $1.1 billion the year prior, down to $876 million. That equates to a 20% reduction in interest paid, or roughly $500 million in savings for FY21. This is a significant amount for a company that pays out $650 million a quarter in dividends.

If the interest expense savings were spread out evenly as dividend increases, that results in a 19.2% increased in the dividend for the year. This of course will not happen before they reach their leverage target, but it serves as an example to the flexibility management will have to return cash to shareholders in the near future. Those savings will most likely be used to keep chipping away at the debt, which I am all for. I have no doubt that when management starts, they will move quickly and aggressively to reach their compensation package figures.

Source

Chart

Data by YCharts

Valuation and Momentum

As earnings and revenue are projected to show consistent growth, there is no reason CVS should be trading as a 'dead in the water' value stock, especially as large buybacks and dividend increases are on the horizon. Estimates show a 3-4% growth in revenue each year through FY25. EPS growth is projected to be even more aggressive as synergies and cost savings from debt compound. By FY25

I believe CVS to be fairly valued between 15-16x earnings (where it traded before the acquisition and debt). This is slightly above the 5 YR average of 13.36 PE. As short term memory tends to prevail, CVS was once overvalued; trading at nearly 30xFCF and 22xEPS in 2016. Momentum and outlook has begun to turn. Both SA authors and Wall St. analysts remain bullish going forward.

The dividend also has lot of room to run. The current annual payout per share is $2.00. This means that the forward payout ratio for FY2025 (same $11.27 EPS as used below) is a mere 17%. A combination of compounding savings from debt repayments and conservative sales growth will certainly free up a lot of cash in the future for management to play with in the form of buybacks and dividends.

Upon reaching their debt goals, CVS could conceivably raise their dividend at 10% each year for the next 5 years, resulting in an annual payout of $3.22. Still this would only result in a 30% payout ratio based up FY25 estimates. I think it is more likely that management returns to a payout ratio along the lines of where it was before the acquisition. During the 2018 calendar year in which CVS acquired AETNA, CVS' EPS was $7.04.

The payout ratio at the time was 28.4%. If EPS does grow as expected, I project that the dividend by FY25 will be at least $3.00. A 50% increase of where it stands today. Dividend growth investors, and the market in general should be all over this. This is one of the main reasons why I believe CVS deserves a premium from where it is trading now.

Source

Since CVS tops analyst estimates quite frequently. I will be adding a moderate 5% premium to the median FY25 estimates. This brings my FY25 EPS estimate to $11.27. Using a 15x or 16x multiple on that and I find myself at an end of FY25 price target range between $169.05 and $180.32. This implies a 98%-111.9% price return. Investors would also be receiving a minimum of $9.50 a share in dividends during that period. A >24% CAGR without dividends reinvested in both cases.

Takeaway

For the reasons mentioned above, I will be rating CVS a BUY at current levels. Initiating a position at 8xFCF gives investors plenty of margin of safety, especially as the debt burden drastically falls and management has more freedom with their capital allocation.

This is one of the rare few stocks on the market today that I believe can provide dividend growth or yield investors with the potential for significant total return.

Getting some love finally--->>>CVS Climbed Higher, But The Stock Has Still A Long Way To Go

May 10, 2021 9:25 AM ET

Read at this link to see the charts and access the links:

https://seekingalpha.com/article/4426789-cvs-stock-climbed-higher-still-a-long-way-to-go?mail_subject=cvs-cvs-climbed-higher-but-the-stock-has-still-a-long-way-to-go&utm_campaign=rta-stock-article&utm_content=link-0&utm_medium=email&utm_source=seeking_alpha

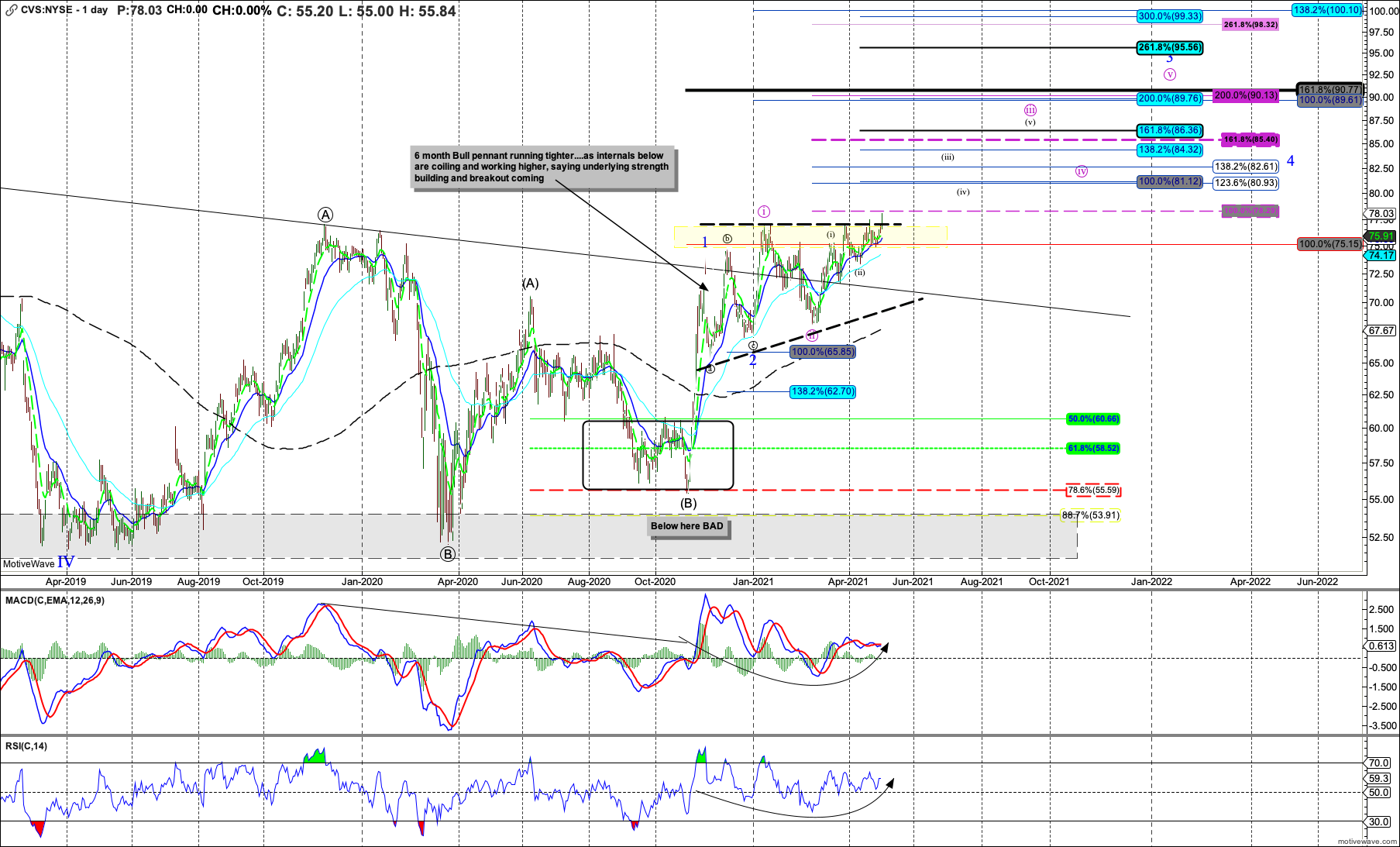

Early To Spot Bullish Setup in CVS

By: MPTrader | May 8, 2021

Back in early February, with CVS trading at 73.19, Mike Paulenoff alerted MPTrader members to a bullish technical setup in the stock, writing:

"CVS exhibits a potentially very powerful multi-month set up, and as a matter of fact, looks like it just ended a correction from 77.23 (1/12) to 71.04 (1/29, and right at its up-sloping 50 DMA)."

He added, "If reasonably accurate, [this] means that CVS is entering a new upleg that should challenge and take out 77.23 in route to a new ATH-zone projected into the 80-83 area."

Fast-forward to this past week, in which the stock took out a 14-month resistance zone at 77.00/40 on Monday, and closed Friday at 85.11, a full 16% above its price at Mike's initial alert.

What's next for CVS? As long as any forthcoming weakness is contained above 81.50, CVS remains poised for upside continuation into Mike's next optimal target zone at 88-90. (See chart below.)

Join Mike and our members in our Trading Diary for constant intraday discussion just like CVS, about individual stocks, ETFs, Macro Indices, Cryptocurrencies, Interest rates, and Commodities.

Read Full Story »»»

DiscoverGold

CVS earns positive views from analysts after Q1 results beat expectations

May 05, 2021 2:16 PM ETCVS Health Corporation (CVS)By: Dulan Lokuwithana, SA News Editor22 Comments

After a better-than-expected Q1 earnings report for 2021 lifted its shares ~4.4% yesterday, CVS Health (CVS +2.3%) has continued its upward momentum today as several Wall Street analysts raised its price target.

RBC Capital Markets reiterates the outperform rating and raised the price target by ~13.8% to $91.00 per share indicating a premium of ~12.2% to the last close.

Encouraged by the progress of the company’s integrated model, Analyst Anton Hie expects room for more upside in shares assuming earnings growth to accelerate further to reach the management’s targets.

Jefferies reaffirms the buy rating and the price target upped to $95.00 from $90.00 per share implies an upside of ~17.1% to the previous close.

Despite the negative impact on cold, cough, and flu products due to COVID-related headwinds, the analyst Brian Tanquilut notes the recent market share gains made by the company.

Meanwhile, maintaining the overweight rating Cantor Fitzgerald has raised the price target by ~2.2% to $92.00 per share implying an upside of ~13.4% to the last close.

Pointing to the company’s healthy free cash flow generation, the analyst Steven Halper expects CVS to reach its post-merger leverage targets.

With a neutral rating on the stock, Seeking Alpha contributor Geoff Considine argued that CVS was prioritizing its deleveraging efforts ahead of dividend growth.

Where Fundamentals Meet Technicals: TGT, CVS, EBAY

By: Lyn Alden Schwartzer | May 5, 2021

This week’s issue of “Where Fundamentals Meet Technicals” looks at one bearish and two bullish stocks...

CVS Health: Potential Breakout

Today, CVS Health (CVS) closed at its highest price since late 2019. Garrett’s chart is pretty bullish:

Harry Dunn graced EWT with a cameo today, by posting a bullish chart on CVS:

If we look at the company’s F.A.S.T. Graph, it’s unusually cheap:

The pharmacy chain acquired the health insurer Aetna a while back with a combination of equity and debt financing, and has been using its income cash flow to deleverage.

Normally high debt is a bad thing, but when a cheap company has high debt for a reason (a specific acquisition in this case), and is plowing cash flow into debt payoff, that gives investors a very clear investment path towards improving fundamentals...

* * *

Read Full Story »»»

DiscoverGold

CVS earns positive views from analysts after Q1 results beat expectations • 2:16 PM

After a better-than-expected Q1 earnings report for 2021 lifted its shares ~4.4% yesterday, CVS Health (CVS +2.3%) has continued its upward momentum today as several Wall Street analysts raised its price target.

RBC Capital Markets reiterates the outperform rating and raised the price target by ~13.8% to $91.00 per share indicating a premium of ~12.2% to the last close.

Encouraged by the progress of the company’s integrated model, Analyst Anton Hie expects room for more upside in shares assuming earnings growth to accelerate further to reach the management’s targets.

Jefferies reaffirms the buy rating and the price target upped to $95.00 from $90.00 per share implies an upside of ~17.1% to the previous close.

Despite the negative impact on cold, cough, and flu products due to COVID-related headwinds, the analyst Brian Tanquilut notes the recent market share gains made by the company.

Meanwhile, maintaining the overweight rating Cantor Fitzgerald has raised the price target by ~2.2% to $92.00 per share implying an upside of ~13.4% to the last close.

Pointing to the company’s healthy free cash flow generation, the analyst Steven Halper expects CVS to reach its post-merger leverage targets.

With a neutral rating on the stock, Seeking Alpha contributor Geoff Considine argued that CVS was prioritizing its deleveraging efforts ahead of dividend growth.

Earnings Call Transcript - CVS Health Corporation (CVS) CEO Karen Lynch on Q1 2021 Results - Earnings Call Transcript

May 04, 2021 12:54 PM ET

CVS Health Corporation (CVS)

https://seekingalpha.com/article/4424124-cvs-health-corporation-cvs-ceo-karen-lynch-on-q1-2021-results-earnings-call-transcript?mail_subject=cvs-cvs-health-corporation-cvs-ceo-karen-lynch-on-q1-2021-results-earnings-call-transcript&utm_campaign=rta-stock-article&utm_content=link-0&utm_medium=email&utm_source=seeking_alpha

Contributor Since 2007

Seeking Alpha's transcripts team is responsible for the development of all of our transcript-related projects. We currently publish thousands of quarterly earnings calls per quarter on our site and are continuing to grow and expand our coverage. The purpose of this profile is to allow us to share with our readers new transcript-related developments. Thanks, SA Transcripts Team

CVS Health Corporation (NYSE:CVS) Q1 2021 Results Conference Call May 4, 2021 8:00 AM ET

Company Participants

Katie Durant - Senior Director of Investor Relations

Karen Lynch - President and Chief Executive Officer

Eva Boratto - Executive Vice President and Chief Financial Officer

Jon Roberts - Chief Operating Officer

Alan Lotvin - President of Pharmacy Services

Daniel Finke - Executive Vice President and President of Health Care Benefits

Neela Montgomery - Executive VP & President of Pharmacy and Retail

Conference Call Participants

Rivka Goldwasser - Morgan Stanley

Steven Valiquette - Barclays Bank PLC

Lisa Gill - JPMorgan Chase & Co

Albert Rice - Crédit Suisse AG

Michael Cherny - BofA Securities

Eric Percher - Nephron Research LLC

Robert Jones - Goldman Sachs Group, Inc.

Justin Lake - Wolfe Research, LLC

Lance Wilkes - Sanford C. Bernstein & Co., LLC.

Operator

Ladies and gentlemen, good morning, and welcome to the CVS Health First Quarter 2021 Earnings Conference Call. At this time all participants are in a listen-only mode, a question-and-answer will follow CVS Health’s prepared remarks at which point we will review instructions on how to ask your questions. As a reminder, today's conference is being recorded.

I would now like to turn the call over to Katie Durant, Senior Director of Investor Relations for CVS Health. Please go ahead.

Katie Durant

Thank you, and good morning, everyone. Welcome to the CVS Health First Quarter 2021 Earnings Call.

I'm joined this morning by Karen Lynch, President and CEO; and Eva Boratto, Executive Vice President and CFO. Following our prepared remarks, we will host a question-and-answer session that will include Jon Roberts, Chief Operating Officer; Alan Lotvin, President, Pharmacy Services; Dan Finke, President, Healthcare benefits; and Neil Montgomery, President of Retail and Pharmacy.

Our press release and a slide presentation have been posted to our website, along with our Form 10-Q that we filed with the SEC this morning.

During this call, we will make certain Forward-Looking Statements reflecting our current views related to our future financial performance, future events, industry and market conditions as well as the expected consumer benefits of our products and services, and our financial projections. Our Forward-Looking Statements are subject to significant risks and uncertainties that could cause actual results to differ materially from what may be indicated in them.

We strongly encourage you to review the information in the reports we file with the SEC regarding these risks and uncertainties, in particular, those that are described in the cautionary statement concerning Forward-Looking Statements and Risk Factors section in our most recent annual report on Form 10-K this morning's earnings press release and included in our Form 10-Q.

During this call, we will use non-GAAP financial measures when talking about the Company's performance and financial condition. In accordance with SEC regulations, you can find a reconciliation of these non-GAAP measures to the comparable GAAP measures in this morning's earnings press release and the reconciliation document posted on the Investor Relations portion of our website.

Today's call is being broadcast on our website, where it will be archived for one year. Now I would like to turn the call over to Karen.

Karen Lynch

Good morning, everyone, and thank you for joining our call today. In what continues to be an unprecedented environment, CVS Health has delivered strong first quarter results. For all of us the past year has been defined by the pandemic and our response to it.

In the first quarter, CVS Health orchestrated an all-out effort to vaccinate Americans against COVID-19. I’m proud to say we have helped achieve the President's accelerated 100-day goal of 200 million vaccines. This would not have been possible without the dedication and effort of our approximately 300,000 colleagues who worked tirelessly throughout the pandemic and delivered when they were needed the most.

Our results show we are providing superior value by creating an integrated health care model that is centered around the consumer. Our unparalleled capabilities, reach and relationship with customers uniquely positions us to support them throughout their lifetime.

Our strong first quarter delivered revenue growth of 3.5%. We generated adjusted earnings per share of $2.04, up nearly 7% versus first quarter of 2020. As a result, today, we are increasing our adjusted earnings per share guidance to $7.56 to $7.68 to reflect the momentum across our business. Importantly, our performance reflects both growth in new and current markets. Eva will provide more details on our outlook and our results.

Before turning to our three business segments, I would like to underscore our ability to anticipate, deliver and exceed customers' health care expectations. Today, we will share where we are seeing momentum and highlight several important achievements.

It is clear that consumers want convenience, transparency, choice and control over their health care. That is why we are engaging consumers in new and different ways by working to meet their health needs in the community, in the home and virtually.

Each of our businesses performed at or better than our expectations this quarter. We delivered strong results in the Health Care Benefits segment, fueled by continued growth in government services.

During the first quarter, utilization approached near normal baseline levels. We have continued momentum in our Government Services business. We increased membership across all Medicare business lines in the first quarter. We outperformed with dual eligible members, delivering over 30% growth and we significantly expanded our reach, adding 14 new states.

Finally, as we announced last quarter, we will reenter the public exchanges in 2022. We expect to enter up to eight states where we believe we can make a meaningful impact and maximize returns with our first ever Aetna-CVS branded offerings. We are committed to helping provide access to affordable care for all Americans.

We also achieved strong revenue and operating income growth in Pharmacy Services, building on the foundation of our specialty management capabilities and overall service excellence. As we announced last week, we delivered market-leading results in controlling drug costs for commercial clients with only a 2.9% overall drug trend, with 34% of clients experiencing negative trend in 2020.

Specialty Pharmacy revenue was up 7.2% year-over-year. This reflects new net wins due to our success in our trend management programs, which continue to resonate in the marketplace and drive more customers into our channels. Specialty Pharmacy spend management also remains a steady growth engine and key differentiator in the market. We are well positioned for continued growth in 2022.

Our Retail segment continues to play a vital role in the delivery care and wellness is an integral part of our customer and community strategy. Since we began, we successfully administered over 23 million COVID tests and over 17 million vaccines through April. We are currently administering vaccines in 49 states and in more than 8,300 CVS locations. A third of vaccinations have been administered to members of underrepresented communities.

Our strong second dose compliance of over 90% is the result of our consumer-centric digital approach. We schedule round trip visits, looking both appointments at once and we also provide appointments for second doses only.

We are successfully driving health services engagement among customers who are new to CVS Health through COVID testing and vaccines. This has helped somewhat offset the impact of a weak flu, cough and cold season. Although early, we have seen improvement in April, as vaccinated customers are more actively shopping in CVS location part of a nationwide trend.

For those customers that are new to us through COVID testing, we have realized about a 9% conversion in filling a new prescription at CVS Pharmacy. We continue to attract consumers to our CarePass subscription program with approximately 4.5 million members in total, up approximately 18% from 2020.

Building on the success of our employer and university program, we recently expanded our Return Ready offering to include vaccinations. We have already administered 40,000 doses, and client interest in this new service is strong and growing. Overall, we have successfully navigated through a challenging retail environment while capturing additional benefits from new customers we are bringing into CVS Health.

As the nation's leading diversified health services company, we are advancing our technology and using CVS Health assets to connect consumers across the health care ecosystem. We are addressing the most prevalent, costly and complex health conditions by expanding our platform to deliver more integrated care.

Our approach combines both face-to-face and virtual points of care that are personalized to the individual. We prioritize the most valuable interventions, the next best action a member can take, that will lead to a positive impact on their health and on medical costs.

For example, early results in our Transformed Diabetes program show an 8% improvement in changing Medicare members behaviors. This program is on-track to exceed its projected medical cost savings and return on investment of two to one. With approximately 1.5 million members having access to this program today, we expect to add an additional 1.3 million members this year.

Our new medical benefit plans are designed with low co-pay or no co-pay at MinuteClinic. We have approximately seven million Aetna members enrolled, up from about two million members or 350% member growth year-over-year. These plans offer broad access to affordable and convenient care with many CVS Health assets.

First quarter results show Aetna commercial members are substantially more likely to use a MinuteClinic when enrolled in this type of plan compared to those without the benefit. In fact, these members are approximately 50% more likely to visit a MinuteClinic for an acute medical need, immunization or COVID test.

We also expanded our HealthHUB offerings to include new services around behavioral health, an increasingly important component of care, especially during the pandemic. Our strategy is to deliver a single integrated experience that connects individuals to a CVS care team, virtually and face-to-face, by navigating consumers to the best site of care.

We are a company focused on delivering the most convenient connected experiences for our customers across our CVS Health digital assets. Our ability to redefine the health experience in an increasingly digital and hybrid world, combined with our vast health assets and understanding of consumers' health, uniquely positions us for growth.

There are three areas where I want to specifically highlight some of our achievements in the last quarter. They include: using our digital assets to expand engagement with our members; expanding into new services and offerings; and leveraging digital capabilities to enhance the customer experience and improve our cost structure.

Starting with engagement. We saw a more than 80% increase in visits to our flagship digital properties year-over-year. Growth was primarily driven by engagement in our expanded set of digital health services, such as COVID testing, vaccinations and Omni-channel pharmacy.

Next, we are expanding access to care through our digital and virtual channels. We launched a digital-first primary care model that helps consumers navigate the best site of care for their health needs. And lastly, we are also harnessing technology such as AI, machine learning services and natural language processing to simplify our process and optimize our cost structure.

We recently announced the launch of our CVS Health Ventures fund that gives us insight into new digital health innovations. This approach allows us to invest in and partner with high-potential early-stage companies to drive technology-enabled innovation and digital health care.

Rising to meet the challenge of COVID-19 has advanced the transformation of the health care industry. For CVS Health, the chance to serve our nation at such a critical time has further proven the value of our strategy.

We have made significant progress in the expansion of our vaccine and diagnostics businesses. We are focused on building broader capabilities in home health, virtual care and health services. Our investments in these areas as well as our digital transformation have allowed us to be there for every meaningful moment of health and will enable us to capture the lifetime value of each of our customers.

And finally, we are exploring every avenue for growth and increased returns. Accordingly, we will hold our 2021 Investor Day on December 9th, hopefully, in New York, conditions permitting, where the management team and I will more fully outline our longer-term strategic priorities and our financial road map for sustainable, profitable growth.

In closing, our results this quarter show that our strong brand and national presence is allowing us to meet individuals where they are. It makes us an increasingly integral part of their everyday health.

Now I will turn it over to our Chief Financial Officer, Eva Boratto.

Eva Boratto

Thanks, Karen, and good morning, everyone. As Karen stated, our strong performance across the enterprise continued in the first quarter. We delivered solid revenue growth of 3.5%, as a result of strong net new business, plus the expansion of our successful COVID-19 testing and vaccine programs.

Adjusted earnings per share of $2.04 increased 6.8% and exceeded our expectations. Our cash flows remain strong, generating $2.9 billion of cash from operations. We paid down over $3 billion of long-term debt in the quarter, while returning $656 million to shareholders through dividends.

Since the close of the Aetna transaction, we have paid down a net of more than $15 billion in long-term debt, and we remain on-track with our low three times leverage goal in 2022. We are maintaining our discipline of capital allocation strategy and managing our balance sheet to generate additional cash flows.

Across the Company, we are executing on our modernization and cost savings initiatives, for which technology is at the core. As mentioned last quarter, we implemented an AI-enabled capability to efficiently address COVID-related calls. This intelligent agent addressed over eight million calls for frequently asked questions. And we are expanding this technology to call centers across the enterprise.

We are also using AI and other technologies to simplify our prior authorization processes. We are decreasing the workload on providers and shortening the time it takes to get patients on appropriate therapy. This improves the overall patient experience while maintaining the clinical rigor, quality improvements and safety programs that are vital to our clients.

We have taken advantage of the increasing virtualization of work to rethink our infrastructure and are on-track to close 63 non-retail facilities, resulting in a 2.5 million square foot reduction in office space by the end of Q2. We are pleased with our progress to-date on these initiatives, and significant opportunity remains.

Now let's take a look at our results by segment. Our Health Care Benefits segment total revenues increased 6.7% year-over-year, driven by continued growth in our Government Services business. The repeal of the HIF and Medicare risk-adjusted revenue pressured that result.

Total membership increased about 215,000 sequentially, with Medicaid membership up about 100,000 or 4%, driven by the continued suspension of eligibility redetermination and the new business win of Kentucky Foster's program effective January 1st.

Our Medicare portfolio continues to grow, with Medicare Advantage and Med Sup membership increasing sequentially about 230,000, up over 6%. Within our PDP, membership increased nearly 4% sequentially. Converting existing commercial and PDP members to Medicare Advantage is one of our core growth strategies in Government Services.