News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

>>> High-Grade Bond-Fund Outflows Hit $35.6 Billion, Smashing Record

Bloomberg

By Claire Boston, Olivia Raimonde, and Alex Harris

March 19, 2020

https://www.bloomberg.com/news/articles/2020-03-19/investors-pull-record-35-6-billion-from-investment-grade-debt?srnd=premium

Withdrawal dwarfs second-largest outflow of $7.3 billion

Record $249 billion added to government money-market funds

Investors withdrew an unprecedented $35.6 billion from U.S. funds that buy up investment-grade debt this week as the global market rout from the spreading coronavirus intensified. At the same time, a record $249 billion poured into U.S. government money-market funds.

The withdrawals from corporate high-grade debt blow through the previous record $7.3 billion outflow from last week, according to Refinitiv Lipper. Funds that buy junk bonds lost $2.9 billion in the five business days ended March 18, while leveraged loan investors withdrew about $3.5 billion.

Credit markets had another volatile week amid a worldwide meltdown in risk assets. Risk premiums on investment-grade bonds reached levels not seen since the financial crisis, while junk bond yields breached 10% for the first time in more than eight years.

”The number is off the charts, but so is the magnitude of this market correction,” Dorian Garay, a portfolio manager at NN Investment Partners, said in reference to the investment-grade bond outflows.

Despite the turmoil, investment-grade companies including Walt Disney Co. and PepsiCo Inc. seized moments of relative calm to issue new debt. Many firms selling bonds this week were doing so to reduce their reliance on the commercial paper market, where prices have risen rapidly amid a broad market seize-up. Lipper fund flow data covers investment-grade funds that manage about $1.3 trillion in assets.

“The flows into IG have been so steady over the past eight years, that it was like the farmer coming with a daily handful of grain to feed the turkey in the back yard,” said Gregory Staples, head of fixed income at DWS Investment Management. “Today what the farmer had in his hand was an axe.”

Investment-grade bonds are poised for another one of the largest weekly losses on record as spreads widen to crisis levels. The three most recent daily outflows from high-grade funds and exchange-traded funds are the largest on record, Bank of America Corp. strategists led by Hans Mikkelsen said in a report Wednesday.

Money-Market Funds

The Federal Reserve stepped in on Tuesday, announcing that it would reintroduce the Commercial Paper Funding Facility, a measure it used during the financial crisis to shore up short-term funding markets.

Total assets in government money-market funds rose to an all-time high of $3.09 trillion in the week ended March 18, according to Investment Company Institute data that stretches back to 2007.

The prior weekly inflows record of $176 billion was set in September 2008 during the financial crisis caused by the collapse of Lehman Brothers.

Prime money-market funds, which tend to invest in higher-risk assets such as commercial paper, saw outflows of $85.4 billion, the largest move since October 2016, according to ICI. Total assets fell to $713 billion.

<<<

>>> Fed unleashes commercial paper funding to support non-bank companies

by Brian CheungReporter

Yahoo Finance

March 17, 2020

https://investorshub.advfn.com/secure/post_new.aspx?board_id=8141

The Federal Reserve announced Tuesday that it will open a commercial paper funding facility to support the financing needs of companies facing stress amid the coronavirus outbreak.

The facility will support rollovers of commercial paper, a commonly used form of unsecured, short-term debt issued to raise funds.

With businesses forced to close and with consumer activity capped by quarantines around the country, concern has built up over previous weeks that companies will not be able to find funding to survive the public health crisis.

The commercial paper funding facility will establish a special purpose vehicle (SPV) that will purchase unsecured and asset-backed commercial paper from eligible companies as long as the paper is rated A1/P1 as of March 17. The facility would be available to companies of various industries, not just banks.

“An improved commercial paper market will enhance the ability of businesses to maintain employment and investment as the nation deals with the coronavirus outbreak,” the Fed said in a statement.

The facility was opened in coordination with the U.S. Treasury, which will provide $10 billion of credit production via its Exchange Stabilization Fund.

The Fed has taken a number of uncommon actions recently amid the coronavirus outbreak.

An emergency 50 basis point cut from the Federal Reserve on March 3 was not enough to stop market turmoil, and on Sunday night, the central bank made another abrupt announcement by slashing rates to zero.

Fed Chairman Jerome Powell said the central bank’s actions over the past two weeks did not calm financial conditions as policymakers hoped, spurring the second emergency meeting.

In addition to pushing rates down to zero, the Fed also restarted the crisis-era policy of asset purchases, announced U.S. dollar swap lines, and eased bank rules to encourage lending.

<<<

>>> Fed to Widen Treasury Buying, Expand Repo to Ease Market Strain

Bloomberg

By Matthew Boesler

March 12, 2020

https://www.bloomberg.com/news/articles/2020-03-12/n-y-fed-to-conduct-purchases-across-range-of-maturities-k7ozy3u5?srnd=premium

The Federal Reserve took aggressive steps Thursday to ease what it called “temporary disruptions” in Treasury financing markets, flooding the market with liquidity and widening its purchases of U.S. government securities in a measure that recalls the quantitative easing it used during the financial crisis.

The Federal Reserve Bank of New York said in a statement that the moves were “to address temporary disruptions in Treasury financing markets” at the direction of Fed Chairman Jerome Powell in consultation with the Federal Open Market Committee.

U.S. stocks trimmed staggering losses of more than 8% earlier in the day as investors absorbed the Fed’s muscular decision.

The buying will include coupon-bearing notes and match the maturity composition of the Treasury market, it said. Ten-year U.S. Treasury yields fell sharply to trade around 0.68%.

“The Treasury securities operation schedule includes a change in the maturity composition of purchases to support functioning in the market for U.S. Treasury securities,” the New York Fed said.

Term repo operations in large size have also been added to help markets function, it also said. The New York Fed said it would offer $500 billion in a three-month repo operation at 1:30 p.m. and repeat the exercise tomorrow, along with another $500 billion in a one-month operation, and continue on a weekly basis for the rest of the monthly calendar.

<<<

>>> Stampede Into Treasuries Sets Up Auctions at Record Low Rates

Bloomberg

By Emily Barrett

March 8, 2020

https://www.bloomberg.com/news/articles/2020-03-08/stampede-into-treasuries-sets-up-auctions-at-record-low-rates?srnd=premium

Haven rush pushes 10-year yields to unprecedented levels

ECB to meet Thursday with expectations divided on outcome

Flight-to-safety in the world’s largest bond market will take on new meaning this week, with some Wall Street firms considering contingency plans for the spread of the coronavirus.

While traders await updates on their working arrangements, there may be little standing in the way of the haven trade that drove the U.S. 10-year yield down to an unprecedented 0.66% Friday amid an equities rout. The market will be watching for further liquidity strains in Treasury futures, and how that might translate into demand for more haven assets at this week’s Treasury auctions. Over the weekend, Saudi Arabia declared an all-out price war in the oil market, adding to the wall of worries over a looming recession and signs of strain in credit markets that have driven investors to the safety of Treasuries.

The Treasury is poised to sell a combined $78 billion of coupon securities at historically low yields. Wednesday brings $24 billion of 10-year notes. To get a sense of the ferocity of the bond rally in recent days as fear over the virus’s impact intensified, the last auction of this maturity, on Feb. 12, drew a yield of 1.62%.

This week's 10-year auction could easily break prior record-low yield

“Given those moves we’re seeing in the 10-year, that implies to me there’s a lack of inventory out there and you’ve got to think the auctions will go well,” said Lee Ferridge, a macro strategist at State Street Corp. “The risk from here has to be that things get worse before they start getting better.”

He’s now looking for the 10-year yield to head toward 0.5%, from a closing level of 0.76% last week.

Relentless demand has taken the maturity’s price to lofty levels going into this week’s auction. The current 10-year carries a higher price than any reopening since 2009.

Friday’s market moves have already drawn comparisons with the financial crisis, though with less confidence that policy makers can do much to combat the economic impact of the disease.

Markets barely registered last week’s pledge from the Group-of-Seven that it was ready to act, and the emergency rate cut from the Federal Reserve. As for the robust U.S. jobs report, Columbia Threadneedle strategist Ed Al-Hussainy dismissed it as “roadkill for this rates market.”

The underwhelmed market reaction to the Fed demonstrated the difficult task facing European Central Bank Governor Christine LaGarde on Thursday. Economists are split on whether the bank will unleash monetary stimulus at this meeting, and hopes are building instead for some fiscal response.

In the meantime, market participants are fixated on what sort of liquidity conditions will greet them in what promises to be another turbulent week.

“Markets are functioning, but it seems to me that on a day when the 10-year yield is lower by 20 basis points, that’s not orderly, that’s a gap,” said Mike Schumacher, head of rates strategy at Wells Fargo Securities, referring to the most extreme levels in Friday’s trading.

“I wish I had more answers,” he said. “We all do.”

What to Watch

Fed officials are in a blackout period ahead of the March 17-18 meeting, but markets will be fixated on the message from the ECB on Thursday.

The New York Fed will release new schedules on March 12 for its Treasury purchases and repo operations

Here’s the economic calendar:

March 10: NFIB small business optimism

March 11: MBA mortgage applications; consumer price index; real average earnings; monthly budget statement

March 12: Producer price index; jobless claims; Bloomberg consumer comfort; household change in net worth

March 13: Import/export prices; Bloomberg U.S. economic survey; University of Michigan sentiment

The auction slate is busy:

March 9: $42 billion of 13-week bills; $36 billion of 26-week bills

March 10: $38 billion of 3-year notes

March 11: $24 billion of 10-year notes reopening

March 12: 4-, 8-week bills; $16 billion of 30-year bonds reopening

<<<

>>> JPMorgan Sees ‘Early Signs’ of Stress on Credit and Funding

Bloomberg

By Joanna Ossinger

March 7, 2020

https://www.bloomberg.com/news/articles/2020-03-08/jpmorgan-sees-early-signs-of-stress-on-credit-and-funding?srnd=premium

The fallout from the global spread of coronavirus may be starting to affect credit and funding markets, according to JPMorgan Chase & Co.

Supply-chain disruptions and demand shock from the virus fallout could already be causing cash-flow problems for businesses, JPMorgan strategist Nikolaos Panigirtzoglou wrote in a note Friday. That’s probably even more true for smaller companies and those in sectors like travel and lodging, he said.

“If these shifts in credit and funding markets are sustained over the coming weeks and months, especially in the issuance space, credit channels might start amplifying the economic fallout from the Covid-19 crisis,” Panigirtzoglou said. Unless “credit support by central banks and/or governments is broad, fast and direct, we note credit markets are facing an increased risk of the cycle turning with a lot more downgrades or even defaults over the coming months.”

Credit markets suffered their worst day in a decade on Friday amid fears that coronavirus will hurt corporate income and stymie some companies’ ability to repay their debt. Travel- and leisure-related companies were hit, while energy-company bonds and loans fell further into distress. A derivatives index that measures the perceived risk of corporate credit surged by the most since at least 2011 and in Europe the cost of insuring senior financial debt skyrocketed.

High-grade CDS index spread jumps by most since at least 2011

Market concerns about ratings downgrades and companies dropping to junk status are justified by a look at credit fundamentals, the JPMorgan report said. The median net-debt-to-Ebitda ratio for companies in JPMorgan’s high-grade and high-yield companies in the U.S. and Europe has risen steeply in the past decade and is now higher than in the previous two cycles in 2007/2008 and 2001/2002, it said.

“Companies are currently much more vulnerable to a decline in incomes and/or a rise in corporate bond spreads and yields than in the previous two recessions,” Panigirtzoglou wrote. “This is especially true for U.S. credit and for Euro high yield given the absence there of the backstop from the European Central Bank’s corporate bond program that solely benefits Euro high grade.”

There are some signs of stress in Yankee issuance as well, the report said, noting it tends to be more sensitive to funding concerns because non-U.S. companies can find it harder to raise dollar funding relative to domestic U.S. companies in periods of stress.

Read more: Europe’s ‘Zombie’ Borrowers Besieged by Spread of Coronavirus

It’s also the case that credit appears most vulnerable to an economic downturn, according to the note, using an analysis which looks at the historical behavior of various asset classes around past U.S. recessions, particularly the move from the pre-recession peak to the trough during the event.

relates to JPMorgan Sees ‘Early Signs’ of Stress on Credit and Funding

“Rate markets are now implying that something that looks like a U.S. recession is almost a certainty and have become even more disconnected from risky asset classes,” Panigirtzoglou wrote. “U.S. credit seems to be still most vulnerable to U.S. recession risks followed by U.S. equities.”

<<<

>>> Hottest Bond Market in History Is Starting to Make Some Nervous

Bloomberg

By Cecile Gutscher and Anchalee Worrachate

March 3, 2020

https://www.bloomberg.com/news/articles/2020-03-03/hottest-bond-market-in-history-is-starting-to-make-some-nervous?srnd=premium

Duration bets at a record as coronavirus spurs caution

Haven play may turn dangerous if doomsday doesn’t come

Surging rate-cut expectations and a desperate lunge for safe assets amid the coronavirus outbreak have earned the bond market a lot of fans in recent weeks. The resulting rally is creating a few detractors, too.

A growing chorus of strategists and money managers is voicing concern as investors charge into government debt at seemingly any price.

The fear is they’re exposing themselves to interest rate risk like never before, risking a precipitous slump on even a modest bump in yields. One breakthrough in the fight against the illness, or a sign the global economy is recovering faster-than-expected, might be all it takes.

The yield on 10-year Treasuries touched an all-time low on Monday but traders didn’t have to look far for clues of just how fast the narrative can change. The S&P 500 Index surged 4.6% on bets central banks would coordinate to limit the economic impact of the virus. The moves highlight belief in some corners that policy action will stoke growth, creating upward pressure for stocks and bond yields.

“If things go a little better -- if there is a cure in the next two, three months or if with warmer weather the virus fades -- then long-end rates will sell off,” said Alberto Gallo at Algebris Investments. “Duration is expensive to protect the portfolio.”

The London-based money manager said he’s using short positions in credit to hedge the risk of a deeper sell-off.

Bond duration risk rises to record

Amid a rally so ferocious that it has stirred speculation some Treasury yields could even be headed below zero, the danger of rising bond yields still seems remote. Even those flagging it as a concern aren’t ready to unwind their bets on longer bonds -- for now.

The Federal Reserve’s announcement Friday that it was ready to act if needed took 10- and 30-year Treasury yields to new lows, with futures markets now pricing in more than 100 basis points of Fed cuts this year. The announcement by the Fed, a rare departure from typical central bank protocol, ushered in similar assurances from the Bank of Japan and the Bank of England.

The yield on the Bloomberg Barclays Global Aggregate Bond Index, which includes developed and emerging-market debt from governments and corporations, tumbled to 1.05% Monday, its lowest ever.

Global bond yields hit record low as investors seek virus havens

Still, the risks of taking one-way bets on bonds at such elevated valuations loom large. Sensitivity to changes in rates measured by duration is running at a record 8.6 years in the Bloomberg Barclays Global Aggregate Treasuries Index. That means every percentage point increase in average yields would spark a price decline of about 8.6%.

Bond traders throwing their faith behind policy makers should also be thinking about how steps to shore up confidence will affect those bets, according to Jim McCormick, the London-based global head of desk strategy at NatWest Markets. A boost to economic growth would ultimately mean higher long-dated yields.

“Central banks will likely cut and unlikely unwind them when things settle, but a recovery plus more fiscal policy should pressure the back end of the curve,” he said. “The curve steepens if the combination of policy response works.”

A sobering assessment by the OECD Monday did little to assuage market panic. The Paris-based group warned of possible global contraction this quarter and cut its full-year growth to just 2.4% from 2.9%, which would be the weakest since 2009.

As the number of new virus cases in China declines, those elsewhere are climbing, with countries like Brazil and Pakistan reporting instances of the illness for the first time.

But if measures to contain and stamp out the illness take hold, China returns to work and records an upswing in growth in the second quarter, bets on expensive government bonds may start to look dangerous.

Bond momentum signals tracked by a type of systematic investors known as trend followers have turned so extreme their bullish bets are now vulnerable to profit-taking, according to JPMorgan Chase & Co.

TLT posts its largest weekly outflow in more than a month

Wariness is reflected in passive flows in the world’s most heavily traded government debt product, the iShares 20+ Year Treasury Bond fund, which shows investors’ love affair with duration may be cooling somewhat. The ETF just posted its largest weekly outflow in more than a month.

“Chasing bonds when yields are at an all-time low seems very risky,” said Mark Dowding, a money manager at BlueBay Asset Management, who has a neutral stance on duration. “At the same time it seems that news flow on the virus will get worse before it gets better.”

<<<

>>> Coronavirus Chaos Slams Credit Markets, Brings Deals to a Halt

Bloomberg

By Hannah Benjamin and Tasos Vossos

February 26, 2020

European bond market faces first day without deals in 2020

Warnings mount of hit to earnings as virus impacts growth

https://www.bloomberg.com/news/articles/2020-02-26/coronavirus-chaos-brings-corporate-debt-market-to-its-knees?srnd=premium

The global credit machine is grinding to a halt.

The $2.6 trillion international bond market where the world’s biggest companies raise money to finance themselves, has come to a virtual standstill around the world as the coronavirus spreads fear through company boardrooms.

In Europe, which had been enjoying the strongest ever start to the year -- with 239 billion euros ($260 billion) of bonds sold in January alone -- Wednesday saw no deals for the first time in 2020. The U.S. hasn’t seen a transaction since Friday while Asia, where the virus first emerged, has slowed to a trickle.

While such shutdowns are common during public holidays such as Christmas, they are extremely rare at other times of year.

Investors are rattled by the potential impact on company earnings from disruption caused by the virus, which has seen huge parts of global supply chains shutting down.

“It’s pretty serious,” said Shanawaz Bhimji, a fixed-income strategist at ABN Amro Bank NV, calling it a “very difficult” moment for investments in credit markets.

Deep Freeze

Coronavirus takes its toll on European primary bond market activity

Honeywell International Inc., Virgin Money UK Plc and Transport for London are among the European borrowers readying deals before financial markets started turning hostile.

Borrowing costs in euros for investment-grade companies have surged to 95 basis points, the highest level reached this year, according to a Bloomberg Barclays index, while default swaps insuring the debt of high-grade companies surged to the highest in four months. A closely-watched measure of risk in the junk-bond market also soared to a six-month high on Wednesday.

The number of coronavirus cases continues to climb, with the global death toll nearing 3,000. U.S. health officials have warned citizens to prepare for an outbreak, while South Korea has also emerged as a hot spot, with more than 1,000 reported cases there.

The worsening crisis is already taking a toll on companies’ balance sheets, with drinks maker Diageo Plc set to book as much as a 325 million-pound ($422 million) hit to organic net sales following significant disruption in Greater China since the end of January. French food maker Danone SA lowered its target for 2020 sales growth after slowing bottled water sales in China.

In the U.S., Mastercard Inc. shares tumbled as much as 7% this week after the company cut its revenue forecast as the spreading virus curbs international travel, while Apple Inc. said demand for iPhones in China tumbled 28% in January on the previous month.

Just four borrowers have visited Europe’s debt market so far this week, including ING Groep NV with a downsized sale of Additional Tier 1 notes on Monday. New deal announcements have also dried up, with only one mandate from the region yesterday.

Any sign that the epidemic is stabilizing may prove a fillip for sales, according to Luke Hickmore, investment director at Aberdeen Standard Investments in Edinburgh.

“We have seen before that any stability in markets tends to attract new issuance,” he said.

<<<

>>> There’s a Wall of Cash Eager to Buy Treasuries on Any Price Dip

Bloomberg

By Liz McCormick and Ruth Carson

February 16, 2020

https://www.bloomberg.com/news/articles/2020-02-16/there-s-a-wall-of-cash-eager-to-buy-treasuries-on-any-price-dip?srnd=premium

It’s ‘a resilience play that makes sense’: BlackRock’s Thiel

Pensions, mutual funds and hedge funds have all piled in

Investors overseeing trillions of dollars are plowing money into U.S. government debt like never before, in a wave that’s only gaining strength as the spreading coronavirus casts doubt on the global growth outlook.

Evidence of the insatiable demand can be found across the fixed-income universe. Pensions, which have been ramping up bond allocations for more than a decade after a change in regulations, now hold a record amount of longer-dated Treasuries. Bond mutual funds saw a historic inflow of money last year, with no sign of a slowdown. Even hedge funds have piled in.

The wall of cash is a boon to American taxpayers as the federal deficit swells. It’s keeping Treasury yields, a benchmark for global borrowing, near all-time lows. With buyers ready to pounce, even surging stocks, record auction sizes and the tightest labor market since the 1960s can barely make a dent in bond prices.

“Treasuries are a resilience play that makes sense,” said Scott Thiel, chief fixed-income strategist at BlackRock Inc. “And so far, people have been rewarded for coming in and buying when yields get to the high end of the range.”

Investors have been buying on dips in Treasury prices

Just weeks ago, global economic reflation and the seeming inevitability of higher yields were the buzz among strategists and investors. The virus’s onslaught is unraveling that narrative, which already faced skepticism from those who argue that persistently low inflation and shifting demographics will pull yields lower.

“I expect the Treasury 10-year yield to fall to zero, perhaps within two years,” said Akira Takei, a global fixed-income fund manager at Asset Management One Co., which oversees more than $450 billion. “I’ve been overweight U.S. Treasuries. That’s based on my view that developed economies are facing a combination of aging demographics and falling birth rates, slow growth and low inflation.”

Investors snapping up Treasuries as an insurance policy have turned the U.S. yield curve on its head. With inflation still subdued and concern mounting that the spreading illness will damage an already fragile global economy, traders have boosted bets on Federal Reserve rate cuts in 2020. That prospect is in turn supporting equities.

The appetite for debt has extended to sovereign obligations of all flavors. One example: Greek 10-year rates once near 45% slid below 1% this month. The country’s junk rating is proving little deterrent with the world’s pile of negative-yield debt climbing above $13 trillion amid the latest global bond rally.

Benchmark 10-year U.S. yields have dropped to around 1.6%, from a 2020 peak of 1.94% in the first week of the year. The world’s biggest bond market has earned about 2.2% this year, after a 6.9% return in 2019 -- the best performance since 2011.

READ MORE

Bond Market Braces for Fresh Trillion-Dollar Fund Flow Wave

Bond Funds See Record Inflows After Virus Spurs Bets on Stimulus

Inverting Treasury Curve Shows Global Fear More Than U.S. Slump

“You still need a duration ballast and shock absorber,” said Con Michalakis, chief investment officer of retirement fund Statewide Superannuation Pty., which manages about $7 billion in Adelaide, Australia. “And I don’t see yields moving materially higher from here.”

The likely economic hit from the virus reinforces that view. Fed Chairman Jerome Powell last week cited the outbreak as a risk. Goldman Sachs Group Inc. predicts it will subtract two percentage points from annualized global growth this quarter.

“If the Fed is staying super-accommodative -- basically in reflation mode -- then you want to buy equities, credit and, strangely, you also want to buy Treasuries,” said Ralph Axel, an analyst at Bank of America Corp.

The demand for Treasuries in some corners has been building for years. U.S. corporate pensions, for example, have been big buyers since the federal Pension Protection Act, passed in 2006.

For the top 100 funds, with combined assets of more than $1.4 trillion, the fixed-income allocation surged to about 49% at the end of 2018 from 29% in 2005, as equities’ share fell by half to 31%, according to Milliman Inc., a pension and risk advisory firm. JPMorgan Chase & Co. strategists estimate the debt portion topped 50% as of December.

An up-to-date read on retirement funds’ demand can be seen in the record surge in Strips, which are created when Treasuries are split into principal- and interest-only securities. Pensions tend to favor these assets, which have longer duration, or sensitivity to interest-rate changes, to match the length of their liabilities.

Pension funds' Treasury demand seen in Strips rise

Soaring stocks are also spurring buying of bonds on price declines.

U.S. public pensions, with total assets of over $4 trillion, have kept holdings steady over the past five years, at about 25% in fixed income, 50% in public equities and the rest in alternative investments, according to data from the Pew Charitable Trusts.

As equities have climbed, the funds have needed to buy more debt to keep the breakdown stable, said Greg Mennis, director of public sector retirement systems at Pew.

Veteran bond manager Dan Fuss says he’s been been buying Treasuries as a safety play. He points to last week’s 10-year auction as a sign that yields won’t bust higher anytime soon. A measure of demand for the $27 billion sale was the highest since March.

“When you look at the bids for the 10-year notes, you’d have thought, ‘Wow, the government was giving out free ice cream’,” said Fuss, vice chairman of Loomis Sayles & Co. “There’s just more money available to invest than there’s marketable investment opportunities, and no risk of inflation at this time.”

<<<

>>> Kraft Heinz’s Junk Downgrade Rekindles Bond Market Jitters

By Molly Smith and Jonathan Roeder

February 14, 2020

https://www.bloomberg.com/news/articles/2020-02-14/kraft-heinz-cut-to-junk-by-fitch-following-lackluster-earnings?srnd=premium

Packaged-food company cut to high yield by Fitch and S&P

More BBB debt has some investors wary that others may follow

Kraft Heinz Co., the iconic food giant created in a merger five years ago, was downgraded to junk by two credit raters, raising fresh worries among investors that a slowing economy could threaten the broader corporate bond market.

The packaged-food company was cut one level to BB+ by S&P Global Ratings, following Fitch Ratings earlier Friday. It will now become a so-called fallen angel, taking it out of investment-grade indexes.

Though Kraft Heinz, with just under $30 billion of debt, is a relatively small investment-grade issuer, it will become one of the top three in high yield. It’s just one of many companies that have wound up with a massive debt load as the result of deals, jeopardizing credit ratings in the process.

The food giant, created in a deal orchestrated by Warren Buffett and the private equity firm 3G Capital, is in the midst of a turnaround as its brands fall out of favor with consumers. It reported a drop in fourth-quarter sales Thursday that sent its bonds and stock tumbling, the latest sign that the company’s turnaround plan still has a long way to go.

“Kraft is to investment grade as Velveeta is to cheese,” said Christian Hoffmann, a portfolio manager at Thornburg Investment Management. “The ingredients dictate what something is and Kraft Heinz is junk.”

Profit Margins

That assessment is a far cry from the days of the merger when 3G went on a high-profile cost-cutting spree that was expected to eventually produce fatter profit margins. Instead, Kraft Heinz was left with a stable of tired brands and few new products that could appeal to consumers’ preference for more natural and less processed foods. Last year, it wrote down the value of its brand portfolio by more than $15 billion.

The turmoil has been a headache for Buffett’s Berkshire Hathaway Inc., whose stake over the past year has fallen to about $8.9 billion, down from $14 billion at the end of 2018. The stock was one of the worst performers last year.

S&P and Fitch cut the company one level to their highest junk rating. Kraft Heinz debt is already on the way to trading like junk. Its bonds due 2029 now yield about 3.5%, compared to the 2.88% for the average BBB company with similar duration. It’s the worst-performing issuer in both the U.S. and European markets Friday, and the cost to protect its debt against default has spiked to levels last seen in October.

Kraft Heinz bonds trade wider than BBB peers with similar duration

Fitch said Kraft Heinz may need to divest a sizable portion of its business in order to reduce debt. Kraft Heinz also needs to cut its dividend, Fitch said in August, but the company said Thursday it would maintain the annual $2 billion payout to shareholders. Fitch maintains a stable outlook, while S&P’s is negative. Moody’s rates the company one step above junk with a negative outlook as of Friday.

“We believe it’s important to Kraft Heinz shareholders to maintain our dividend during this time of transformation,” Michael Mullen, a spokesman for the company, said in an emailed statement earlier Friday. Kraft Heinz remains committed to reducing leverage “over time,” he said. The company plans to release a more detailed turnaround plan around the time of its next earnings report in early May.

Kraft Heinz was one of many companies with BBB ratings, the lowest level of investment grade, which now comprises half of the broader $5.9 trillion market. It’s grown steadily since the financial crisis, as a decade of low interest rates prompted companies to load up on debt for mergers and acquisitions, often at the expense of credit ratings.

UBS Group AG strategists led by Matthew Mish predict there could be as much as $90 billion of investment-grade debt to fall to high yield this year. That compares to just under $22 billion in 2019, close to a 20-year low, according to Bank of America Corp. strategists.

But a wave of fallen angels, which some investors fear, has yet to follow. Many strategists contend that BBB companies have the ability to defend their investment-grade ratings, whether by selling assets or cutting dividends. Companies like General Electric Co. and AT&T Inc. have done just that to stave off downgrades.

<<<

>>> Treasury Inversion Is Not About the U.S., It Is About the Whole World

Bloomberg

By Anchalee Worrachate and Liz McCormick

February 10, 2020

https://www.bloomberg.com/news/articles/2020-02-10/the-inverting-curve-is-flashing-global-fear-more-than-u-s-slump?srnd=premium

Safety grab may be bigger cause of inversion than U.S. outlook

Half of world’s haven pool is Treasuries: Eurizon’s Jen

The U.S. yield curve is flirting with another broad-based inversion again, reigniting Wall Street fears over the fate of the American economy.

A growing chorus of voices is being swayed by another notion: The signal might say more about the state of the world than the U.S. business cycle.

Treasuries now make up more than half of all global haven assets, double the share they accounted for during the financial crisis, according to Eurizon SLJ Capital. That complicates matters when long- and short-term yields flip: What used to be a reliable American recession indicator is instead an barometer of investors diving for cover worldwide.

It’s a narrative that makes a lot of sense as the threat from the coronavirus continues to grow, and it revives the frantic debate from last year about how much predictive power the curve actually has left.

Treasury yields flattening again as virus sparks global hunt for havens

“In a grab for safety and duration, everyone is going for U.S. Treasuries,” said Gregory Faranello, the head of U.S. rates at AmeriVet Securities. “The yield curve inversion is a signal now of global growth issues, and not really reflecting what is going on in the U.S.”

After a respite early last week the curve is once again flattening, and the gap between the rate on 10-year and three-month Treasuries narrowed for a third day on Monday. At the height of coronavirus angst and an equity sell-off at the end of last month it briefly inverted for the first time since October.

Bond yields typically rise alongside the duration of debt because they provide compensation for the effects of inflation. If rates on a 10-year note are lower than a three-month bill it suggests investors have a pessimistic view of growth and inflation a decade from now.

Stephen Jen, the chief executive officer at Eurizon SLJ, says global hunger for U.S. bonds helps explain American exceptionalism in growth, currency markets and stocks.

He predicts that by 2022, U.S. government debt will account for two-thirds of the world’s pool of haven bonds thanks to large issuance and quantitative easing by other central banks. His calculations are based on the outstanding amount of government debt in the U.S., Japan, and the three largest European economies, subtracting out the portion that is owned by central banks.

“The U.S. might, perversely, thrive because of troubles elsewhere,” Jen said in an interview. “When U.S. Treasury yields fall due to shocks outside of the U.S. that may or may not have an impact on the U.S. economy, it often provides added stimulus.”

It’s a view Federal Reserve officials are playing close attention to as global risks from the virus mount. In an interview with Bloomberg TV, Fed Vice Chairman Richard Clarida played down the inversion and said the negative spread is “really driven not so much by an outlook for the U.S. economy, but globally.” When there’s uncertainty money flows to America, he said, so current yield moves don’t reflect the U.S. outlook.

Campbell Harvey is credited with drawing the link between the slope of the yield curve and economic growth. The professor at Duke University’s Fuqua School of Business says corporate America is much more attuned to the yield curve signal and will take preventative action.

“CFOs and CEOs are more aware and aren’t likely to take on the risk of just ignoring it,” Harvey said. “They are being a little more cautious now.”

The gap between the yield on three-month and 10-year Treasuries recently slipped to as low as about minus 6 basis points. The spread -- which has inverted before each of the past seven U.S. recessions -- had initially fallen below zero in March 2019 as economic conditions deteriorated at the height of the trade war. The spread between two- and 10-year yields, which was negative as recently as September, remains above that mark at 17 basis points.

On Wall Street, strategists at JPMorgan Chase & Co. still see plenty of reason to fret the slope of the curve. Their favorite indicator -- and a part of the curve that remains inverted -- is the gap between two-year forward and one-year forward rates, which can shed light on the bond market’s expectations of what the Fed will do.

In this case, it shows a “rising probability of a more protracted Fed rate cut cycle extending to 2021,” said Nikolaos Panigirtzoglou, a strategist at JPMorgan.

For now, there aren’t many other alarm bells in an American economy with unemployment rates near 50-year lows and the longest stretch without a recession since World War II. Even so, economists forecast that GDP growth will slow to 1.8% compared with 2.3% in 2019, and it’s too early to determine whether the coronavirus outbreak in China will significantly affect the U.S. economy.

“When Treasuries become most dominant, investors from anywhere in the world naturally buy of lot of these bonds when they want a safe haven,” said Jen. “The yield curve in the U.S. is increasingly reflecting the fears of the rest of the world.”

<<<

>>> High-Tax States’ Bonds Are So in Demand That Ratings Don’t Matter

Bloomberg

By Danielle Moran

February 6, 2020

https://www.bloomberg.com/news/articles/2020-02-06/high-tax-states-bonds-so-in-demand-that-ratings-don-t-matter?srnd=premium

‘To boil it down, it’s 99.999% because of the SALT cap’

California, New York yields holding below the AAA benchmark

There’s so much money chasing after the bonds sold by America’s high-tax states that buyers don’t seem to care too much about what credit-rating companies think.

The heavy demand overall has driven municipal yields to their lowest in more than six-decades. And with rates so low, the yield penalties that would typically differentiate a deeply indebted state from a thrifty one have become little more than rounding errors that in some cases contrast with their standing in the ratings pecking order.

California’s general-obligation debt, for example, is yielding about 1 basis points less than the AAA benchmark, even though the state is rated as many as four steps below that, according to data compiled by Bloomberg. New York, one step below AAA, is paying about 8 basis points less than top-rated borrowers. Over the past year, New Jersey’s yield premium has been cut nearly in half even though its rating hasn’t changed. Connecticut’s is roughly a third of what it was.

Both NY and CA debt yield less than top rated bonds

By contrast, bonds issued by AAA rated Texas and Florida, where there’s no state income tax, pay above-benchmark yields.

This dynamic shows how dramatic the demand has become for tax-exempt securities since President Donald Trump’s 2017 tax law limited state and local deductions. That change drove investors in high tax-states like California, New York and New Jersey into municipal bonds as an alternative way to drive down what they owe.

“To boil it down, it’s 99.999% because of the SALT cap,” said James Iselin, portfolio manager at Neuberger Berman Group LLC in New York. “Because there’s is so much demand in the market -- there is less of a credit differentiation that the market is making.”

<<<

>>> Corporate Debt: A Slow-Motion Train Wreck

FEBRUARY 4, 2020

BY SCHIFFGOLD

https://schiffgold.com/key-gold-news/corporate-debt-a-slow-motion-train-wreck/

Corporate debt has blown through the roof over the last several years. So much so that the Federal Reserve has issued warnings about the increasing levels of corporate indebtedness.

Borrowing by businesses is historically high relative to gross domestic product (GDP), with the most rapid increases in debt concentrated among the riskiest firms amid weak credit standards.”

But as Brandon Smith of alt-market.com noted in an article published at LewRockwell.com, this is a subject the mainstream media “seems specifically determined to avoid discussing these days when it comes to the economy.

Smith called corporate debt “the key pillar of the false economy.”

It has been utilized time and time again to keep the Everything Bubble from completely deflating, however, the fundamentals are starting to catch up to the fantasy.”

Business debt skyrocketed to a record $16 trillion in 2019. That represents a 5.1% year-on-year, much faster than economic growth. As a result, debt levels have also reached historic highs in terms of percentage of GDP. According to the Federal Reserve report, debt growth has outpaced economic output “through most of the current expansion.”

Smith pointed out that corporations have been using borrowed money for stock buybacks. He called this the single most vital mechanism behind stock market inflation.

Corporations buy their own stocks, often using cash borrowed from each other and from the Federal Reserve, in order to reduce the number of shares on the market and artificially boost the value of the remaining shares. This process is essentially legal manipulation of equities, and to be sure, it has been effective so far at keeping markets elevated.”

Smith said that corporate stock buybacks appear set to decline in 2020. But he doesn’t think this is because companies want to stop using the tactic. The problem is the amount of accumulated debt is outpacing falling profits. Corporate profits peaked in Q3 2018 and have been falling ever since.

Price-to-Earnings ratio, as well as the Price-to-Sales ratio, are now well above their historic peak during the dot-com bubble, meaning, stocks have never been more overvalued compared to the profits that corporations are actually bringing in.”

It’s not just that massive level of corporate debt that is worrisome. Much of the debt is categorized as risky. The Fed report expressed concern about the high level of leveraged loans and what it describes as “weak underwriting standards.” There are more than$1.1 trillion in leveraged loans outstanding. These are loans made to firms already deeply in debt. Think subprime loans for corporations.

A broad indicator of the leverage of businesses—the ratio of debt to assets for all publicly traded nonfinancial firms—is at its highest level in 20 years.”

As Smith points out, this level of borrowing always comes with consequences.

Even if central banks were to intervene on a level similar to TARP, which saturated markets with $16 trillion in liquidity, the amount of cash needed is so immense and the economic returns so muted that such measures are ultimately a waste of time. The Federal Reserve fueled this bubble, and now there is no stopping its demise. Though, they’re behavior and minimal response to the problem suggests that they have no intention of stopping it anyway.”

Peter Schiff has been saying the record stock market valuations have no real connection to the actual economy. He insists stocks really should be coming down and the only thing really supporting them is the Federal Reserve and all the money they’re printing with their QE program. Smith made a similar point.

While corporations, the Fed and Trump have been putting some effort into keeping stock markets from imploding, the real economy has been evaporating. Global import/exports are crashing, US manufacturing is in recession territory, US GDP is in decline (even according to rigged official numbers), US retail outlets are closing by the thousands, the poverty rate jumped in 30% of US counties in the past year, and high paying jobs are disappearing and being replaced with minimum wage service sector jobs.”

Smith called the corporate debt situation a “slow-motion train wreck.” And as he put it, a slow-motion wreck is still a wreck.

The damage can only be mitigated by removing one’s self from the train, and preparing for the fallout. Do not think that simply because the system has been able to drag it’s nearly lifeless body along for ten years that this means all is well. All bubbles collapse, and corporate debt has already sealed the fate of the Everything Bubble.”

<<<

>>> Ford’s Lending Arm Is Generating More Profit Than Ever

Bloomberg

Molly Smith and Keith Naughton

February 3, 2020

https://finance.yahoo.com/news/ford-lending-arm-generating-more-110001090.html

Ford’s Lending Arm Is Generating More Profit Than Ever

(Bloomberg) -- Aside from F-Series pickups hauling in gobs of profit, Ford Motor Co.’s automotive business isn’t carrying much weight lately.

Thank goodness for the finance guys.

Ford Credit, the lending arm that’s become accustomed to propping up the company in good times and bad, now generates about half the automaker’s profit, up from 15% to 20% in the past.

Ford Credit is designed to perform a relatively simple task: make loans to the dealers stocking vehicles, then the consumers who buy them. Now, Ford is relying on its finance unit to help fund multibillion-dollar outlays on electric and self-driving cars while it simultaneously racks up $11 billion in charges from a restructuring that could take years.

“It’s like the ballast that keeps the ship steady,” said Lawrence Orlowski, an analyst at S&P Global Ratings. “It’s a balancing act.”

Ford’s been selling fewer and fewer U.S. vehicles for the last three years, and it’s losing billions overseas, including in China, where its annual vehicle deliveries fell by half during that time span. On Tuesday, analysts expect the company to report lower fourth-quarter automotive revenue and a 44% plunge in adjusted net income. Profit on that basis could be the lowest since 2009.

Ford shares rose as much as 3.6% -- their biggest intraday in three months -- and traded up 2.7% to $9.06 as of 10:30 a.m. in New York. The stock rose 22% last year.

The second-largest U.S. automaker would be far worse off without its Ford Motor Credit Co. unit, which is effectively funding turnaround efforts by routinely borrowing in the debt markets and paying a dividend back to the parent company. The credit unit is expected to contribute almost $3 billion annually to Ford over the next two years, according to Benchmark Co. analyst Mike Ward. That’s up from just a $400 million contribution in 2017.

Ford Credit borrowed around $10 billion in the U.S. investment-grade bond market in the past year, apart from funds raised in other currencies and securitized debt. By contrast, it’s been more than three years since Ford Motor last issued bonds, according to data compiled by Bloomberg, as investors fretted about the company’s high debt load and slowing sales.

Credit graders are responding to Ford’s poor automotive performance, with Moody’s Investors Service the most aggressive so far. It downgraded Ford to junk in September, casting doubt on Chief Executive Officer Jim Hackett’s turnaround plan in the process.

S&P then cut Ford to the lowest investment-grade rating in October after the carmaker lowered its full-year profit forecast. Another downgrade by S&P would take Ford out of major high-grade indexes, which investors and analysts have contemplated for more than a year. If cut, Ford would be the largest U.S. nonfinancial high-yield issuer, which could add near-term pressure to its funding costs. It has about $35 billion of debt in the Bloomberg Barclays U.S. investment-grade index.

It’s not going to get any easier for the carmaker. Amid growing fears of an industry wide downturn, Ford is rolling out a critically important series of new sport utility vehicles and redesigning the F-150, its most profitable and best-selling model. Analysts are already flagging cost and execution risk tied to those introductions, especially after Ford botched the launch of its Explorer SUV last year.

“It’s quite clear Ford is not where it should be, but the finance arm is a bright spot,” said David Whiston, an equity strategist with Morningstar in Chicago who rates the automaker’s shares the equivalent of a buy. “Obviously you want the whole company operating at full power, which you don’t have right now.”

Ford Credit is contributing more and more to the parent’s earnings. In a normal operating environment, manufacturing cars and trucks should drive most of earnings, with credit only generating 15%-20% of profits, said Bloomberg Intelligence analyst Joel Levington. For much of last year, Ford Credit constituted somewhere around half the company’s profit.

Ford and its finance arm are inextricably linked. Each supports the other operationally and financially under a a relationship agreement that governs the connection between the two.

Ford Credit is also protecting the automaker’s prized dividend. The unit paid $2.4 billion back to its parent in the first nine months of 2019, covering the dividend cost for the entire year. That may be “unsustainable” in the long run, because Ford’s dividend consumes a much greater percentage of its cash flow than peers, according to BI’s Levington. Ford has repeatedly said it will not cut the dividend.

In a recession, Ford Credit’s role becomes even more important. It doesn’t play much in the subprime market, so the ratio of its losses to total customer bills outstanding stayed below 2% during the Great Recession, a low level. Its repossession rate never got higher than 3.2%.

Those strong metrics allowed Ford’s captive finance unit to generate a dividend for the parent even in 2009, when U.S. auto sales slumped to a 27-year low.

“With a healthy portfolio, a captive balance sheet in an economic downturn actually starts generating and kicking off a bunch of cash flow,” Tim Stone, Ford’s chief financial officer, said during a November interview at Bloomberg News headquarters in New York. “We take a very thoughtful approach to that business.”

Over the past two decades, Ford Credit has sent $28 billion up to Ford, according to company data.

“That’s not a bad thing -- that’s exactly the reason you want to have a healthy financial-services company,” said Hitin Anand, a senior analyst at CreditSights. “Ford Credit will come to the rescue of Ford Motor in more ways than one. It’s one of the best-run captive-finance companies in the entire universe.”

Finance companies can be a burden for manufacturers in downturns, as General Electric Co. discovered in the financial crisis. The conglomerate’s credit arm weighed on its share price as investors grew more concerned about complicated financial institutions. GE has been selling off and shrinking the unit’s assets for most of the last decade.

Ford Credit is a bright spot in Ford’s portfolio, and also among its peers. It prides itself on lending to consumers with higher credit scores, which keeps asset quality high and defaults low compared with rivals General Motors Financial Co. Inc. and Santander Consumer USA Holdings Inc.

In the third quarter, Ford Credit’s 60-day delinquency rate was just 0.14%. That’s low in an industry where 4.71% of auto loans were at least 90 days late, the highest in more than nine years, according to Federal Reserve data.

“As a credit analyst, I focus on glass half empty. Ford Credit is the positive part of the story,” said Olesya Zhovtanetska, senior director of public fixed income at SLC Management. “They need that cash cow.”

<<<

>>> Moody’s downgrades Ford credit rating to junk status

CNBC

SEP 9 2019

Associated Press

https://www.cnbc.com/2019/09/09/moodys-downgrades-ford-credit-rating-to-junk-status.html

Moody’s Investors Service has downgraded Ford’s credit rating to junk status.

The service says it expects weak earnings and cash generation as Ford pursues a costly and lengthy restructuring plan.

The ratings service said Ford’s outlook remains stable, but its cash flow and profit margins are below expectations and the performance of peer companies in the auto industry

Moody’s Investors Service has downgraded Ford’s credit rating to junk status.

The service says it expects weak earnings and cash generation as Ford pursues a costly and lengthy restructuring plan.

Ford responded with a statement saying that its underlying business is strong and its balance sheet is solid.

The rating for Ford’s senior unsecured notes and its corporate family dropped to Ba1, the top rating for debt that’s not investment grade. It had been Baa3, the lowest investment grade rating.

Ford’s fight to remain an American icon

Moody’s says it expects Ford’s restructuring to extend for several years with $11 billion in charges and a $7 billion cash cost.

The ratings service said Ford’s outlook remains stable, but its cash flow and profit margins are below expectations and the performance of peer companies in the auto industry. “These measures are likely to remain weak through the 2020/2021 period including a lengthy period of negative cash flow from the restructuring programs,” Moody’s Senior Vice President of Corporate Finance Bruce Clark wrote in a note to investors Monday.

Ford’s erosion in performance happened while the global auto industry was healthy, Clark wrote. Now the company and CEO Jim Hackett must address operational problems as demand for vehicles is softening in major markets, he wrote.

The company has $23.2 billion in cash, which is more than its debt, according to Moody’s. The stable outlook reflects Moody’s expectation that the restructuring will contribute to gradual improvement in earnings, profit margins and cash generation, Clark wrote.

Ford said it has plenty of liquidity to invest in its future.

“We are making significant progress on a comprehensive global redesign — reinvigorating our product lineup and aggressively restructuring our businesses around the world,” Ford’s statement said.

The statement said Ford already is addressing operating inefficiencies and problems with its China business.

<<<

>>> Debt-Laden Merchants Face Reckoning Amid Retail Apocalypse

Bloomberg

By Eliza Ronalds-Hannon

December 23, 2019

https://www.bloomberg.com/news/articles/2019-12-23/stores-that-stocked-up-on-debt-face-a-harsh-holiday-reckoning

Department stores fall out of favor with shoppers and lenders

Countdown is on for Forever 21’s plan to keep doors open

Retailers are strapping in for the final days of their traditional do-or-die holiday shopping period. For some, that could be meant literally, as creditors and vendors decide which ones are still worth supporting in a field plagued by fewer shoppers, more online competition and too much debt.

Some of the most familiar names -- Forever 21 Inc., Barneys New York Inc. and Payless Inc.-- have already collapsed into bankruptcy or liquidated this year. In 2019 alone, Coresight Research estimates, retailers have shut more than 9,300 stores. Among the survivors, fates have diverged, according to the restructuring experts at FTI Consulting Inc.

“The retail sector is becoming more segmented between winners and losers,” Christa Hart, a senior managing director in FTI’s retail and consumer practice, said in an interview. “The ‘average’ has disappeared.”

At Risk

Merchants could use a strong finish after last year’s holiday season, when retailers wound up with their worst sales drop for December since 2008, according to U.S. Census Bureau data analyzed by FTI. This holiday season “will be disproportionately great for the strong players and disproportionately weak for the other ones,” Hart said.

Some of the most vulnerable are the traditional department-store chains. Moody’s Investors Service predicted in a November report that by the end of 2019, those retailers will have seen their operating income fall by more than 15%. This, despite heavy investing to improve inventory efficiency and to build their online capabilities.

Department store sales have been declining for decades

“It’s not 1985 anymore,” said Perry Mandarino, head of restructuring and co-head of investment banking at B. Riley FBR Inc. “People don’t need a one-stop shop where they can get everything from vacuum cleaners to jewelry.”

Here are some retailers being closely watched by credit investors and lenders.

J.C Penney

Debt outstanding: About $4.2 billion

J.C. Penney Co. backed out of its appliance business earlier this year as one of the initiatives of new Chief Executive Officer Jill Soltau. She’s trying to design a strategy that will revive a chain suffering from slow-moving inventory and outdated merchandise.

Same-store sales, a key retail metric, dropped 9.3% last quarter. Foot traffic is falling and comparable sales have slid for five straight quarters.

Department stores should be focused on deepening their offerings in one particular area, such as appliances, FTI’s Hart said. “Sadly, many of these department stores took out their hardline and home businesses in favor of apparel, and now they are feeling the results of those decisions,” she said.

S&P Global Ratings cut J.C. Penney to CCC in August, noting that while the company doesn’t plan to file for bankruptcy, “we think an out-of-court restructuring is increasingly likely.” The following month, Bloomberg reported the chain is preparing for talks with its creditors on possible transactions to ease its debt burden.

A representative for the Plano, Texas-based retailer declined to comment.

Neiman Marcus

Debt Outstanding: About $5.7 billion

Neiman Marcus Group Inc. engineered an out-of-court note exchange in June that bought it more time to ease its high leverage.

But the luxury retailer still has about $700 million due by 2023, adjusted earnings continue to decline, and some of its bonds sell for a third of face value. Even the new debt issued during the exchange, which started trading at 97 cents, has already traded down to around half of its face value.

Credit raters take a dim view of Neiman Marcus. S&P said in June that the exchange didn’t make the debt load any less onerous and that there’s “continued risk of a restructuring or default over the next 12 months.”

The company is still mulling what to do with its successful European e-commerce business MyTheresa, and that may be its ticket back from the brink. It hired Lazard Ltd. in May to help it pursue a sale that could fetch more than $560 million.

A representative for the Dallas-based retailer declined to comment.

Belk Inc.

Debt outstanding: About $2.4 billion

Owned by Sycamore Partners LLC, this mid-priced chain concentrated in the southern U.S. typefies the pressures facing department stores, as shoppers seek out specialized outlets or take their household shopping online.

Belk is better off than some its peers, with a B2 rating from Moody’s. The credit rater cited a loyal customer base, better merchandising, good liquidity and stable cash flow in a June report. Another strength: About half its stores aren’t in malls, which are plagued by waning foot traffic.

Still, investors are shying from Belk’s term loan, which was quoted recently 71 cents on the dollar even after the company pushed its maturity out to 2025.

“Discount retailers are going to do better” than their higher-end peers in 2020, Mandarino said. “But they have to tailor their merchandise well. A lot of people have short attention spans, so you really have to cater to what your core buyer wants.”

A representative for New York-based Sycamore Partners declined to comment.

Forever 21

Debt Outstanding: About $350 million, excluding trade debt

Among all big retailers, Forever 21 Inc. may be the one whose survival is most at risk.

The trendy fashion chain went bankrupt in September, citing the cash-guzzling impact of an ambitious international expansion. Sales continue to lag, and revenue has been below expectations, Bloomberg reported in December. Inventory bottlenecks also threaten to curtail sales during the crucial holiday season, people familiar with the chain’s operations have said, making would-be rescuers hesitate to lend more money.

The company needs a new loan to finance its exit from bankruptcy, but prospective lenders are concerned about the weak results as well as the ongoing influence of husband-and-wife founders Do Won and Jin Sook Chang, who ran the company during its successful years as well as during its descent into insolvency.

A budget that Forever 21 filed with the bankruptcy court Nov. 16 cut its forecast for total sales in November to about $191 million, down 20% from what it predicted the month before.

A representative for Los Angeles-based Forever 21 declined to comment.

<<<

>>> The Bedrock of Ultra-Low Yields Is at Risk

Bloomberg

By Emily Barrett, Chikako Mogi, and James Hirai

December 29, 2019

https://www.bloomberg.com/news/articles/2019-12-29/the-bedrock-of-ultra-low-yields-is-at-risk-as-fiscal-tide-turns?srnd=premium

‘The green shoots of fiscal spending are happening’: Loomis

Fragile growth, monetary action still curbing rise in yields

The new decade could be the dawn of a tougher era for bond investors, as conditions that sustained the historic bull run in government debt fall away.

Unprecedented central bank action has dominated economic stimulus since the global crisis and suppressed yields around the world. The skew may now be shifting more toward fiscal expansion that could pressure rates higher. Austerity is on the wane in Europe, spending packages are landing in Asia, and U.S. borrowing is on track for even bigger records in the next couple of years.

The handoff from monetary to fiscal policy is a longer-run investment theme, says Mark Dowding at BlueBay Asset Management, and he’s already trading it in the U.K., by betting against gilts.

“When you look at the U.K., what we’re witnessing now is some pretty material easing in fiscal policy,” said Dowding. “It’s a theme that we expect to see more broadly.”

The Organisation for Economic Cooperation and Development says government spending globally has helped widen the fiscal deficit from 2.9% of world gross domestic product in 2018 to an estimated 3.3% next year. Also, OECD economists are among the growing ranks pushing for more disbursements to tackle slowing global growth and climate change.

The trouble for investors is working out when government spending may reach a critical mass to push yields higher. As of now it’s still in fledgling stages, while central banks continue to pump massive stimulus.

“To me this is the story of the next decade,” said Elaine Stokes, portfolio manager at Loomis Sayles & Co. “The green shoots of fiscal spending are happening across the globe, but it hasn’t gotten to a place where it is coordinated.”

“In the next 5 to 10 years it becomes a factor in markets,” Stokes said. “So that’s where the market has to go -- we have to turn to a rising rate environment from a falling rate environment.”

From South Korea to Brazil, a Global Guide to Stimulus Plans in 2020

The risk of a reversal in the last decade’s trend of falling yields is palpable. The governments of the two largest economies are spending more, and relying on debt to plug much of their revenue shortfall. Alicia Garcia-Herrero, chief economist for Asia Pacific at Natixis SA, sees China’s issuance growing as the budget gap widens from 7.9% this year to 9% of GDP.

“Monetary policy has been less effective by itself, especially in the EU and China, the economy thus calls for more expansionary fiscal policy to grow,” said Garcia-Herrero, who previously worked for the European Central Bank and the International Monetary Fund. “One drawback of fiscal expansion is its upward pressure on interest rates.”

So far that pressure is barely registering in borrowing costs. The world’s benchmark, the U.S. 10-year yield, is mired below 2%, and $11 trillion of debt worldwide yields less than zero. While that total has shrunk by more than a third since August -- when global yields troughed -- investors continue to seize on assets that offer some return. And it still looks way riskier to trade against haven flows and central bank purchases while the global economic outlook remains fragile.

Global rates sell-off has shrunk the pool of negative-yielding debt by a third

That’s a popular and persuasive case against higher yields in the U.S. for now, even as lawmakers on both sides of the aisle look ready to embrace blowout deficits. The Treasury may manage to keep borrowing steady this year -- albeit at a record level -- in part because the Federal Reserve’s current plan to stabilize short-term funding rates could trawl roughly $240 billion of bills out of the market in the coming months.

Investors like Dowding are focusing on regions where monetary policy looks most exhausted. He reckons the market is overestimating the likely stimulus from the Bank of England. And his call in the U.K. isn’t an outlier -- Goldman Sachs Group Inc. strategist George Cole estimated that issuance to fund current spending and public-sector investment could be worth a boost of around 25-40 basis points in gilt yields next year.

Across the channel, ECB President Christine Lagarde is clearly taking up the push for more fiscal spending and may have more success than her predecessor. That said, expansive policy is emerging mainly in the peripheral countries, as a backlash against austerity. The region’s savers -- including its largest economy -- aren’t showing much sign of shifting their stance.

“We’ve seen this movie before,” said Brad Setser, senior fellow at the Council on Foreign Relations. “There is building pressure in Germany to increase investment and increase green investment in particular, but so far it hasn’t catalyzed an enormous shift in policy.”

Lagarde Eyes Dozen Euro Members With Precious Room to Spend More

In Japan, BNP Paribas SA sees increased government spending helping the 10-year yield edge up to +0.1% in 2020 from its current level just below zero.

But the Bank of Japan is scooping up bonds at such a rate, it’s still swamping fiscal efforts so far, according to UBS chief Japan economist Masamichi Adachi. This month’s $239 billion spending package may be only just enough to avert a recession following October’s sales-tax increase.

“The stimulus package isn’t a bold shift from the past and won’t significantly affect the outlook for markets or the Japanese economy,” Adachi said. “At most, it helps support confidence.”

But the rationale for higher yields is in place, at least in theory. S&P Global Ratings’ leading arbiter on the quality of the world’s government debt said that it’s gotten sketchier, as countries have seized on low interest rates to borrow more.

“You’re looking at close to 65 or 70% of world GDP that has today a lower credit quality than it had pre-2008 crisis,” said Roberto Sifon Arevalo. Government debt is “riskier today than it was before, but it’s not reflected in the market.”

Emerging markets have tended to pay a higher price for profligacy than developed economies with more room to spend, he said. And it’s worth remembering that when S&P cut the U.S.’s top-shelf credit rating, in 2011, Treasury yields plummeted as investors flooded into the world’s safest debt market. But the overall trend is clear.

“The market seems a bit complacent with the idea that interest rates will stay low for the foreseeable future,” said Sifon Arevalo.

<<<

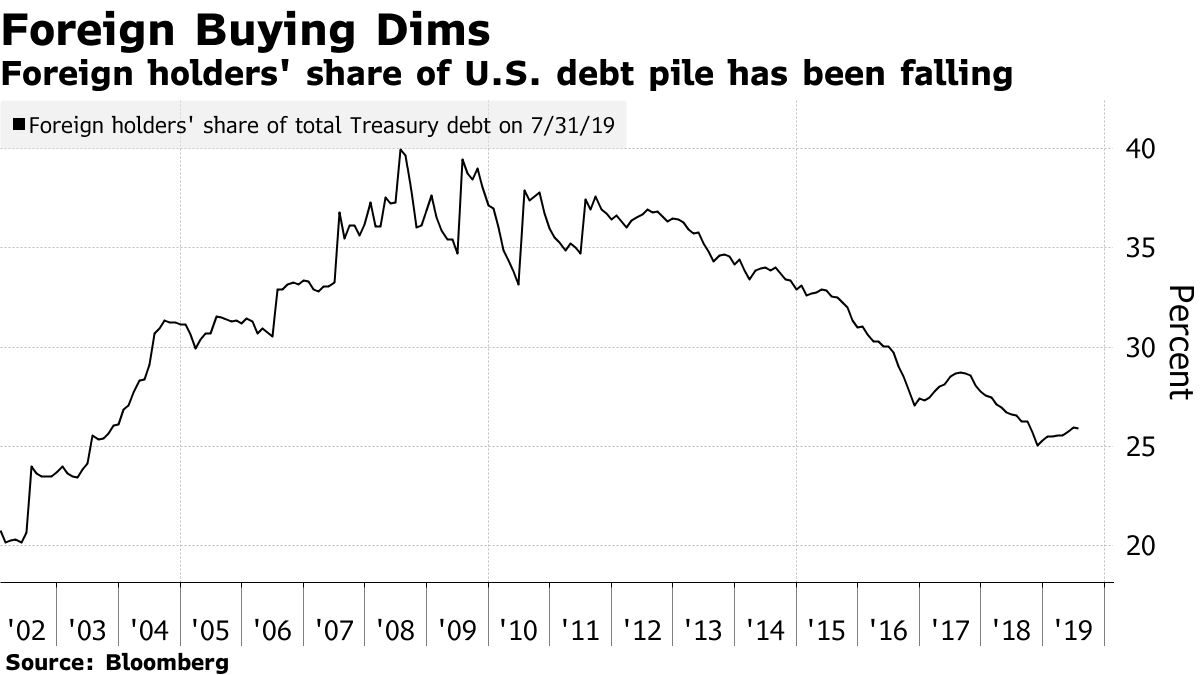

>>> The Corporate Bond Market’s $100 Billion Buyer Is Here to Stay

Bloomberg

By Molly Smith and David Caleb Mutua

December 26, 2019

https://www.bloomberg.com/news/articles/2019-12-26/the-corporate-bond-market-s-100-billion-buyer-is-here-to-stay?srnd=premium

Foreign demand seen underpinning U.S. high-grade debt in 2020

Global investors flee $11 trillion of negative-yielding assets

The U.S. corporate-bond market’s $100 billion benefactor isn’t going anywhere in 2020.

Foreign demand will continue to underpin high-grade debt next year as global investors extend their hunt for higher-paying assets in the face of over $11 trillion of negative-yielding securities around the world, according to market watchers.

“There’s simply not enough high-quality income-producing assets to meet the demand,” Mark Kiesel, chief investment officer of global credit at Pacific Investment Management Co., said in an interview. “That’s the reason that credit did so well this year. It wasn’t just the fact that the Fed and other central banks cut rates. The fact is that there’s just that much demand.”

While hardly anyone expects a repeat of 2019, which has seen blue-chip company bonds return more than 14% -- the most in a decade -- many predict solid single-digit gains from a market they readily admit looks expensive by most conventional measures. That’s partly based on the expectation that money managers outside the U.S. will continue to pile in. They’ve bought $114 billion of bonds on a net basis this year through the third quarter, according to Federal Reserve flow of funds data.

Foreign Flows

Dealers have sold more bonds to non-U.S. investors than they've bought

Global central banks have cut interest rates roughly 90 times over the past year, the largest cumulative easing since the financial crisis, according to Canadian Imperial Bank of Commerce data. While the Fed accounted for three of those, taking its policy rate down to a range of 1.5% to 1.75%, that’s still higher than much of the rest of the developed world, including Japan and Europe, where rates are near or even below zero.

“It’s very hard for the average foreign investor to survive -- we’re still at a point now where it’s max desperation,” said Hans Mikkelsen, head of high-grade credit strategy at Bank of America Corp. “Basically there’s only one game in town for foreign investors, and that’s the U.S. corporate bond market.”

A lower fed funds rate also has its advantages. For one, it tends to make it cheaper for international buyers to protect against the risk of currency fluctuations. Three-month dollar-hedging costs based on forward contracts for euro- and yen-based investors have dropped significantly this year.

That’s “a positive for demand from those investors staying pretty strong,” said Barry McAlinden, senior fixed-income strategist for the Americas at UBS Global Wealth Management.

And if rates continue to decline, as some forecasters expect, that will almost certainly bolster demand for relatively higher-paying assets such as U.S. investment-grade company debt, market participants say.

The average U.S. investment-grade corporate bond yields 2.87%, or about 1 percentage point more than Treasuries. In Europe, absolute yields on company bonds sit at just 0.47%, similar to the 0.46% that Japanese corporate debt pays.

That’s why institutional investors like Japan’s Government Pension Investment Fund, the largest of its kind in the world, say they’re preparing to buy more bonds outside local markets.

“They are being pushed out of Japan,” said Tetsuo Ishihara, a U.S. macro strategist at Mizuho Financial Group Inc.’s fixed-income unit in New York, referring to Japanese institutional investors broadly. “There’s nowhere else to go.”

<<<

>>> Apollo and Blackstone Are Stealing Wall Street’s Loans Business

Bloomberg

By Lisa Lee

December 18, 2019

https://www.bloomberg.com/news/articles/2019-12-18/apollo-and-blackstone-are-stealing-wall-street-s-loans-business

Growth of private credit comes at expense of leveraged lending

Apollo sees $200 billion of debt going private over five years

On the surface it was a classic leveraged takeover -- $1.8 billion of debt to fund the acquisition of Gannett Co. And just like hundreds before it, front and center was Apollo Global Management. Except this time, the private equity giant wasn’t the borrower. It was the lender.

The deal is part of a major shift occurring in global finance. Direct lenders, including more and more hedge funds and buyout firms, are preparing to dish out billions of dollars at a time to lure borrowers away from the $1.2 trillion leveraged loan market.

It’s the latest push by alternative asset managers into what was once the exclusive territory of the world’s biggest investment banks. And while Wall Street voluntarily ceded much of its business lending to medium-sized companies in the aftermath of the financial crisis, this time the iron grip it has on arranging the industry’s bigger loans is being pried open, jeopardizing some of its juiciest fees.

“Direct lenders have raised significant capital to allow them to commit to larger deals,” said Randy Schwimmer, head of origination and capital markets at Churchill Asset Management. “It’s an arms race.”

Investment returns from direct lending outpace gains from high-yield loans, bonds

It’s a striking reversal of fortune for syndicated-lending desks that spent the last 10 years luring business away from the high-yield bond market, the original source of buyout financing for big, risky companies. Even as recently as the beginning of the year, deals in excess of $1 billion were largely seen as the private domain of bulge-bracket banks, which arrange and sell them to institutional investors.

Not anymore.

Apollo said last month that it’s looking to do deals in the $2 billion range. Rival Blackstone Group Inc. is actively pitching a trio of billion-dollar financings that it intends to hold entirely itself, according to a person with knowledge of the matter. (The firm declined to comment.) And private-credit standouts including Owl Rock Capital and HPS Investment Partners are also setting their sights on bigger loans.

The $1.8 Billion financing of New Media Investment Group Inc.’s acquisition of Gannett came on the heels of a $1.25 billion direct loan by Goldman Sachs Group Inc.’s private-investment arm -- one of the few of its kind under a Wall Street bank -- and HPS to fund Ion Investment Group’s purchase of financial data provider Acuris.

And in October, a group of about 10 lenders including Owl Rock banded together to provide a $1.6 billion loan to refinance the debt of insurance brokerage Risk Strategies.

“There are bigger pools of capital” now, said Craig Packer, co-founder of Owl Rock, which controls more than $14 billion. “Our holdings of individual loans are therefore larger than was previously available from smaller lenders.”

Fading Fees

Investors have plowed hundreds of billions of dollars into private debt funds in recent years, lured by premiums that are more than five percentage points higher than competing public debt, according to a Goldman Sachs analysis.

Assets under management now exceed $800 billion, based on the most recent data available from London-based research firm Preqin, including over $250 billion of dry power. In contrast, leveraged loan growth has begun to stall, with the size of the U.S. market now hovering around $1.2 trillion, up less than 4% from a year earlier.

Partly as a result of direct lenders increasingly allowing borrowers to bypass the syndication process, compensation for arranging leveraged loans has plunged. Fees are down 29% this year through November, to about $8.5 billion, versus the same period last year, according to Freeman Consulting Services estimates.

The biggest players in the industry say the shift is just getting started.

Apollo predicts as much as 10% of the more than $2.5 trillion high-yield loan and bond market will go private over the next five years, John Zito, co-head of global corporate credit, said at the company’s Nov. 7 Investor Day.

The alternative asset manager sees the privatization of global credit mirroring a similar trend that’s swept equity markets in recent years.