News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Knight Capital -- >>> ‘Knight’mare Triggered Volume Plunge at Knight Capital Dark Pool.

Bloomberg

By Matt Jarzemsky and Steven Russolillo

9-25-12

http://blogs.wsj.com/marketbeat/2012/09/25/knightmare-triggered-volume-plunge-at-knight-capital-dark-pool/?mod=yahoo_hs

It’s no secret that trading volumes were unusually low over the summer. But one venue operated by Knight Capital KCG +2.30%Group, the brokerage firm roiled by a trading snafu last month, really took it on the chin.

A dark pool operated by Knight Capital saw volume plunge 44% in August from a month earlier, outpacing the 4% to 17% declines other dark pools suffered in a sluggish month overall, according to research provided by Tabb Group.

Dark pools are electronic venues that match up trades without publicly displaying bids and offers. Trades are published on the tape only after completion. Money managers generally prefer executing large orders “in the dark” because it lessens the odds of tipping the market.

Knight’s trading malfunction, which stemmed from software errors, resulted in $440 million in losses for Knight and prompted the firm to seek rescue funding from a group of six financial firms, including Jefferies Group JEF +0.14%TD Ameritrade AMTD -1.22%and Stifel Financial SF +1.46%, customers of Knight.

“This is a good opportunity to reiterate just how much reputation and trust plays into trading,” says Cheyenne Morgan, a research analyst at Tabb Group. ”Trust has always been the name of the game in trading and becomes even more critical when trading off-exchange.”

A Knight spokeswoman confirmed Tabb’s data were accurate, but said the slide in volume stemmed from business disruptions as the firm regrouped from its Aug. 1 trading problems, not customers’ perception of the firm.

“Market share rebounded really quickly with the recapitalization announcement,” the Knight spokeswoman said in a chat with MarketBeat. “It wasn’t a reputational issue. It was a business disruption, and our strong reputation is why our market share came back.”

Knight declined to give details on September trading volumes, saying the information will be released Oct. 17, the day Knight is set to report earnings.

Knight last week said the average daily dollar amount of shares traded by its market-making group fell 34.5% in August from a month earlier. Daily average equity volume at its Knight Direct unit, which provides electronic trading tools to broker-dealers and investors, tumbled 47.9%.

The firm fared better during the month than some expected. Sandler O’Neill analysts last week reduced the amount of per-share losses they expect Knight to report for the third quarter, saying the volume decline was not as steep as they expected.

Average daily trading levels in August clocked in at their lowest levels since 2007. Dark pools across the board saw month-over-month volumes decline. Platforms operated by Credit Suisse CSGN.VX +0.25%and Goldman Sachs sa GS +1.90%w volumes decline by 14% and 2%, respecitvely, while BIDS Trading and Liquidnet each experienced 17% declines in August, according to Tabb.

For Knight, its Knight Match platform suffered the most out of all the dark pools compiled by Tabb.

“As we push through to the end of September, it will be interesting to see if Knight can regain trust and recover from those volumes lost in August or if their relationships suffered some permanent damage,” Cheyenne says. “Only time will tell.”

<<<

New Oriental Education -- >>> New Oriental Education Is Winning The Battle Against The Short Sellers

September 24, 2012

by: Adam Gefvert

about: EDU, includes: AMBO, CAST, MHP, XRS, XUE

http://seekingalpha.com/article/883731-new-oriental-education-is-winning-the-battle-against-the-short-sellers?source=yahoo

New Oriental Education (EDU) has recently taken some big hits. On July 17, it took a 34% hit down to $14.62 after the SEC announced it will investigate its accounting practices. The very next day, Muddy Waters wrote a "strong sell" research report that hit the stock another 35% down to $9.50. The company has since recovered all its losses from the Muddy Waters report, to close at $14.92 on September 21st. It looks like it will soon recover from the hit from the SEC investigation news as well.

As of August 31, 15.15 million shares of EDU were short, or about 10% of the total shares outstanding. If the SEC ruling ends up being favorable, it will likely push the stock well into the $20s.

On September 21, Wells Fargo gave a positive report about EDU that caused the stock to rise about 8% to $14.92. Wells Fargo stated:

Wells Fargo expects New Oriental Education's SEC investigation overhang to be resolved favorably and in a timely manner. Additionally, the firm believes expected valuation range is $24-$31 and that the current discount is unjustified. Shares are Outperform rated.

Trace Urdan, senior analyst of Wells Fargo, has specialized in the for-profit education sector since 1998. His conviction on New Oriental implies that Muddy Waters might have overlooked some things in its analysis.

SEC Investigation

New Oriental says the SEC will determine if there is a sufficient basis for the consolidation of Beijing New Oriental Education and Technology Group, a variable interest entity (VIE) of the company, and its wholly-owned subsidiaries, into the company's consolidated financial statements. The SEC is likely looking at the potential incorrect revenue recognition accounting from the variable interest entities (VIEs), and might require some additional protections for shareholders.

Muddy Waters' Report Might Be Exaggerating

I'm not saying that Muddy Waters is wrong in his report, he might be correct. I'm usually with the short sellers, but it's worth discussing the other side. Enough investors can jump on the bullish EDU bandwagon, and that will push the stock back up before the SEC investigation resolution. Additionally, in my opinion, Muddy made lots of claims about EDU, but none of them by itself conclusively proves that EDU is fraudulent.

Muddy states that EDU's auditor, Deloitte, will likely resign due to fraudulent reporting by the company. I don't think that Muddy showed enough evidence to support such a strong conclusion. However, I do think it's probable that the company will have to change some of its accounting practices, do some minor account restating and/or increase its internal controls as a result of the SEC investigation, but probably nothing as drastic as an auditor resignation.

The following are three accusations that Muddy Waters made, that might have been exaggerated.

1. EDU has numerous franchisees even though its CEO, Louis Hsieh, said that all of its stores are owned by the company.

In the report, Muddy Waters states:

The fact that EDU is lying about whether it has franchises - a fundamental aspect of its business model - implies that franchising is a big problem for EDU. After researching EDU's franchising for six months, including having chilling encounters with China's spy agency, we have our baseline count of franchises; but, our count might understate the extent. Therefore in this report, we are going to prove only that EDU is lying - that it is in fact franchising. We will give EDU the opportunity to come to the market confessional and admit to investors what is really going on. Should we find any inaccuracies at that point, we reserve the right to publicly release more information on EDU's franchise network.

It's interesting that Muddy didn't go into more detail about the franchisees, and hasn't yet done so. Muddy has taken the position of "I'm going to let EDU get on its hands and knees and admit the amount of franchisees it has, or we will further discredit them." What's the point of this? Why not just release the information it has about the franchisees right away? This stance that Muddy is taking makes me a little skeptical about its conviction on the information.

New Oriental responded to the Muddy Waters allegations by reiterating that all 664 of its schools and learning centers were its own. However, it did start a program in fiscal year 2010 that allows third parties to offer its "Pop Kids" English program. But that never exceeded 21 facilities in total, and is immaterial to the company.

It has been over two months so far, and Muddy still hasn't followed up with its threat of further discrediting New Oriental and releasing its franchisee research. However, I do agree with Muddy that New Oriental should've mentioned the franchisee program. It's kind of strange to completely leave it out even if it is immaterial.

2. Its high gross margin isn't realistic.

Muddy claims that EDU's gross margin of 60.1% for fiscal year 2011 is "far in excess of what is possible." Compared to its peers: Ambow Education (AMBO), Tal Education Group (XRS), Xueda Education Group (XUE), and ChinaCast (CAST), with gross margins of 57%, 46%, 29.5%, and 47.9%, respectively, EDU's is certainly a bit higher. However, it isn't that much higher and since EDU is the biggest, and supposedly best, for-profit educational services company of its peers, it's reasonable to think it runs its business more efficiently. I realize that Muddy thinks all those companies are fraudulent with the exception of XUE, however, that is also debatable.

On EDU's Q4 2011 earnings call, Louis Hsieh explained how the company can achieve its 60% gross margin:

"So we're like Wal-Mart but with a Tiffany price. So we offer one thing under one roof for them and so we're doing the same thing now to K-12."

Muddy states that its research as well as that of Credit Suisse have discovered that EDU's prices are really not above its peers. However, Credit Suisse' report from November 2011 still gave EDU a price target of $33.88. It said:

EDU is a solid player but not the best in K12. We initiate coverage on EDU with OUTPERFORM based on: (1) more sophisticated pricing system; (2) efforts to move up the value chain; and (3) the prospect that the MaxEn segment can create a new niche market."

Maybe the more sophisticated pricing system is what makes its gross margin so high.

3. EDU's Beijing operation (which is 35% of EDU's reported revenue) has prepared fraudulent financial statements for 2009-2011.

The Beijing operation reported that it had an exemption from corporate income tax called the enterprise income tax (EIT) exemption. However, Muddy claimed that it didn't really have this exemption and did indeed pay it.

Taxes are complicated in China and are done differently than in the US. I think there is a high probability of a misunderstanding of the situation by Muddy. Muddy states that "a slight but telling inconsistency supports the conclusion that the Beijing operation's financials are fraudulent." I think to say that the entire financials are fraudulent due to "a slight inconsistency" about a tax exemption is a bold statement.

Likely Endgame

I believe the likely endgame scenario is the SEC will have New Oriental restate its accounting due to the confusion with the VIEs, but nothing major will happen. When the SEC investigation concludes, the stock should bounce back to the $20s.

Some reasons why I'm predicting this is because it has been two months since the Muddy Waters report, and there has been no indication of excess damage. No financial employees have reportedly left, and its auditor hasn't resigned. New Oriental has continued with its growth plans. For example, earlier this month it partnered up with McGraw-Hill Education (MHP) to advance English-language education to Chinese students.

New Oriental is a large Chinese company with a market cap of over $2B, and earlier this year was over $4B. The SEC would only cause a delisting or major restructuring as a last resort. The SEC especially now doesn't want to ruin rapport with China as the country has finally said it would allow "observational visits" from American audit-firm inspectors. This step towards potential joint inspections by both Chinese and US inspectors could start a bull rally among Chinese ADRs since it will restore some trust among US investors. But that is fodder for another article.

<<<

AspenBio -- >>> AspenBio Pharma shares rocket on company news

September 27, 2012

Kathleen Lavine

Denver Business Journal

http://www.bizjournals.com/denver/news/2012/09/27/aspenbio-pharma-shares-rocket-on.html?ana=yfcpc&page=all

AspenBio Pharma Inc. soared 49 percent Thursday on a spate of news from the Castle Rock medical-device maker.

AspenBio (Nasdaq: APPY) told investors it will begin a key clinical test of its key product, AppyScore — a device to help doctors diagnose appendicitis — in the fourth quarter following what it called a “productive meeting” with the U.S. Food and Drug Administration.

It also is shuffling its board and rebranding itself.

Four board members have stepped down, the company said: Greg Pusey, Doug Hepler, Mark Ratain and Michael Merson. New board candidates are being sought, but AspenBio said it “ultimately intends to have a smaller sized board.”

--------------------------------------------------------------------------------

> MORE: AspenBio Pharma set to market AppyScore.

--------------------------------------------------------------------------------

“Additionally, a rebranding of the company is underway and is expected to include the evaluation of new company and product names, as well as associated logos,” AspenBio’s announcement said. “The company intends to propose a new company name later this year and such change will require shareholder approval.”

In the statement, President and CEO Steve Lundy said AspenBio is “very pleased with the recent progress we have made in executing on our key development objectives. Most importantly, after meeting with the FDA, we plan to initiate our pivotal study in the U.S. during the fourth quarter. We are currently modifying the study protocol in accordance with the FDA’s constructive feedback, and we continue to engage hospitals across the U.S. for participation in our study.”

Lundy also said the company is “preparing to launch the product in Europe once we obtain a CE Mark, which we anticipate receiving during the fourth quarter.”

A CE — or Conformite Europeenne — Mark means a product meets European Union health, safety and environmental rules.

As Greg Avery reported in the Aug. 3 Denver Business Journal, AspenBio has had a rough time of it over the last couple of years.

AppyScore — a blood-based appendicitis test designed to help emergency room doctors rule out acute appendicitis — showed disappointing accuracy in 2010 tests. AspenBio’s share price plummeted. Executives were replaced.

Twice in the past year, AspenBio organized reverse stock splits to keep the company’s stock listed on the Nasdaq exchange.

But AspenBio revamped AppyScore since the disappointing 2010 tests, and Lundy told Avery in August that the company hoped to have its diagnostic product, which has no direct competition, on the market by 2014.

“The company’s healthier than it’s ever been,” Lundy said then. “It’s got a product that’s proven it’s robust in the tests we’ve had it in. In all the key areas, we have got great experience [on staff].”

On July 30, Ceva Santé Animale S.A., a French animal health company, bought worldwide licensing rights to develop and sell AspenBio’s cow, horse and pig fertility medicines in a deal raising as much as $2 million for AspenBio, which is now focused exclusively on AppyScore

<<<

Alvarion -- >>> Poised To Triple: Portfolio Update

September 23, 2012

by: Mark Gomes

http://seekingalpha.com/article/882591-poised-to-triple-portfolio-update?source=yahoo

ALVARION (ALVR) has been a money loser for investors, highlighting the risks of investing in unprofitable "value" plays. The company has invested $100M in R&D over the past 3 years, but has struggled to monetize its technology/patents. Enter Hezi Lapid, who has taken the helm as CEO. During his last stint at ALVR, the stock rose 800% to $17 in one year. Lapid has been cracking the whip and has the company moving toward profitability and a possible buyout, something I predicted in a recent Seeking Alpha article.

This is a value stock with an asterisk (also known as a possible value trap). We'll remove the asterisk when the company begins to post a profit. There are many ways to win, but it's possible to lose your entire investment for a shot at making 10x your money.

ATTUNITY (ATTU) is taking off on exploding demand for Big Data. Along with Splunk (SPLK), ATTU provides key technology to customers of Amazon Web Services (AWS). Attunity Cloudbeam synchronizes customer data to Amazon and replicates it to the servers on Amazon's network. Splunk enables visibility, analytics, and a growing number of other services as it relates to the company's data. Splunk crushed it July-quarter estimates, posting 71% growth, prompting investors to bid the shares up to a $3B market cap.

Similarly, ATTU posted 110% growth in its June quarter. The shares remains under the radar, but have been on the move as investors start to realize that it is 1/7th the size of SPLK, but trading at 1/40th the price. We introduced this stock at $3.36 (split adjusted) early this year. After rocketing to a 52-week high of $9.75, it's been taking a breather, offering new investors a chance to get in before the next run. See our valuation analysis on Seeking Alpha for more.

DATAWATCH (DWCH) is a Big Data related software company we introduced to Pipeline Data customers several months ago. We planned to write it up for Seeking Alpha after visiting the company in May. However, I left for a 3-month stint in Europe, so this pick remained under wraps. On the day of my return, the company delivered blowout results, sending the shares up nearly 30%

Despite the recent run, it has plenty of upside to go. It's a classic Three-Stage stock, which took off with the early-2011 appointment of accredited CEO, Michael Morrison ("Great Find" - Stage 1). The shares nearly doubled from 3 to 5 in a few weeks on the news. After that, the stock went nowhere for 12-months, as Morrison settled in and formulated his plan ("Wait Time" - Stage 2). Recently, the last few quarters have been outstanding, driving the stock from under 6 to over 20 this year ("Gold Mine" - Stage 3).

Looking at Morrison's track record and recent board addition, we expect DWCH to continue hiring sales people and driving sales, with an eye toward selling the company for maximum shareholder value.

FACEBOOK (FB) may be pressured in the near-term due to uncertainty regarding its mobile monetization strategy, eccentric CEO, and share lock-up expirations. However, these concerns are either unwarranted (Zuckerberg is a bona fide genius; we don't care if he talks to Wall Street…just make us money) or things that will clear up in due course (see Pandora's most recent quarter -- mobile monetization is coming).

In the meantime, many investors are overlooking one of the most important investment consideration -- Facebook has revolutionized how the world connects and communicates. Like Bezos, Zuckerberg appears to be building deep hooks and moats to ensure long-term global dominance. When the time is right, the profit spigot will be opened. We've all seen it happen many times before. Most investors would see it in FB if they'd just stop thinking about the next 6-months and consider the enormous and unassailable position the company has created. MySpace messed up and Facebook took the reigns.

Unless we see something come around to take its place, we'll recommend being invested here. The near-term issues do matter though, so start with a small position and scale in prudently.

LEAPFROG (LF) hit the mother lode with its LeapPad Explorer. This "iPad for children" is a learning device that quickly earned the trust and admiration of American families. Leapfrog is revered by parents everywhere, but lumpy execution has held its full potential in check. LeapPad 2 was recently released, but investors are fearful that competing products like the iPad and Kindle will steal LF's thunder.

We love the new management team and the company's excellent communications with shareholders. However, for now, we're classifying LF as a "Wait Time" stock until we see if the LeapPad still has momentum.

LIONS GATE (LGF) LGF has positioned itself to seize control of the massive teen demographic now that Warner Bros' Harry Potter series has concluded. Warner Bros President has been quoted as saying, "We're not going to replace Harry Potter with any single movie - not unless we had a Twilight or a Hunger Games." Well, Lions Gate has both and much more, due in part to its Summit acquisition. The company has also acquired the rights to a large stable of promising titles, each one of which LGF will cross-market with the others.

If successful, we'll remove the asterisk from its Hot Trend classification later this year. In the meantime, the risk/reward is well-placed for investors who have an appetite for risk (and commensurately big profits). FYI, LGF's next home-run teen franchise might be "Divergent". The book is gaining traction at a meteoric pace, setting LGF up for a blockbuster movie release in early-2014.

LANTRONIX (LTRX) is a new-management turnaround. New products are being introduced at a record pace. Some new products can take up to 18-months to gain traction, but they already have 12-months under their belts. LTRX is still in "wait time", but that should change within 2-3 quarters. Company is profitable and management has been executing well against its promises. It's not often you can say that about a company with a $30M market cap.

As always, "Wait Time" stocks require patience and positions should be built accordingly. See our earnings analysis for more.

NUANCE (NUAN) is an increasingly valuable player in the ongoing technological revolution. We have followed the progress of its Dragon voice-recognition software since 1995. The journey was far longer than we could have imagined, but cloud computing has finally brought this innovation to the tipping point. We can envision speech recognition being combined with language translation (offered by our first Seeking Alpha article/triple, Lionbridge LIOX) to create the world's first universal translator, ala Star Trek. It's going to happen. It's just a matter of when.

PATIENT SAFETY TECHNOLOGIES (PSTX.OB) is a new addition to this list. A recent Seeking Alpha article tells the story well. The company has been demonstrating great traction and win-rates, leading us to anticipate 1,000 hospital-customers by 2015. Based on PSTX's operating model, that will translate into 36-cents on EPS, with a strong growth trajectory. Give that 36-cents a 15 multiple and we have ourselves a $5.40 stock -- a triple from current levels.

QAD SOFTWARE (QADA) sells software to product manufacturers. Once installed, it rarely comes out and the company collects an annual maintenance fee as insurance against failure. With U.S. manufacturing experiencing a renaissance, QADA stands to benefit for years to come. Despite its promising outlook, the company is selling for less than 1x its recurring maintenance revenue stream. With a 90%+ renewal rate, that revenue stream is just as good as Cloud subscription revenue -- sticky and profitable, making it very easy for the company to remain profitable. In fact, we've never lost money on a software stock with QADA's financial profile.

In addition to its exposure to the repatriation of manufacturing, QAD also provides leverage to the Fed's efforts to reflate the real estate market. The company owns its headquarters, which happens to sit atop an enormous piece of prime real estate overlooking the Pacific Ocean on a cliff in Santa Barbara, California. Its land dwarfs that of the numerous multi-million dollar estates that surround it. If that wasn't enough, due to accounting rule, the property has been being depreciated on its balance sheet for year, leaving its value severely understated on the balance sheet.

(click to enlarge)

In our estimation, this stock is worth well over $20. It just needs a catalyst. In the meantime, investors can hold the stock through good times and bad, collecting a 2% dividend while the company's balance sheet continues to grow.

RAINMAKER SYSTEMS (RMKR) may prove to be the most explosive name in our portfolio. RMKR has combined deep domain expertise in telesales and combined it with powerful Cloud-based software which enables large companies to create instant revenue streams by targeting small- and mid-sized customers. Its growing customer list includes the likes of AT&T, Cisco, Intel, Microsoft, and SAP. RMKR also outmaneuvered Digital River (DRIV) to win a piece of the lucrative Symantec business. Thus, despite its size, the company has established an enterprise-grade pedigree. See Ken Nagy's SeekingAlpha article for more background info.

Most recently, the company guided to sequential revenue growth for Q3/Q4, cash flow positive results, and signed Comcast to a large multi-year contract. Looking at the company's target operating model, we see net income growing exponentially, from around $2 million next year to $6 million in 2014 to $10 million in 2015. That would represent 37-cents per share.

The company needs to continue executing to reward investors. If it does, as a fast-growing Cloud vendor selling into tier-one accounts, a P/E of 20 would be very reasonable. That would result in a $7.50 share price, which makes RMKR a potential 7 bagger from current levels.

<<<

Alvarion -- >>> Is Alvarion Prepping Itself To Be Acquired?

April 19, 2012

by: Mark Gomes

http://seekingalpha.com/article/512651-is-alvarion-prepping-itself-to-be-acquired

Thursday morning, Alvarion (ALVR) announced the hiring of Hezi Lapid who replaces Eran Gorev as its CEO. For ALVR shareholders, Lapid's background paints an interesting picture of what's in store for Alvarion. Specifically, Pipeline Data believes that this move sets Alvarion up to be acquired. Here's why:

Hezi Lapid was most recently the CEO of Axerra. In October 2010, Axerra was acquired by DragonWave (DRWI). Prior to that, Lapid was the CEO of Innowave. Interestingly enough, that company was purchased in February 2003 by Alvarion. Thus, we establish Lapid's propensity for leading companies to acquisiton. just as important, a deep dive shows that buyers have been quite pleased with what Lapid has sold them.

In the case of Innowave, our research found that many Alvarion insiders credited Lapid and Innowave with ALVR's success in 2003. The impact on ALVR's stock was spectacular. During Lapid's only year at ALVR, its stock rose by 800%, culminating in a 2004 high of $17 per share. Since his departure, the shares have steadily fallen.

Lapid's sale of Axerra to DragonWave appears to be off to a similarly positive start. On the first earnings call after its acquisition, the company stated:

(Axerra's) product portfolio will strengthen DragonWave's solution for existing 2G and 3G networks, and their evolution to 4G packet architectures. As you can see, Axerra is already contributing.

In the following quarter, DRWI's CFO said:

Before we bought Axerra, they were doing $2 million to $2.5 million a quarter. In the two quarters that they've been with DragonWave, they've been in the $4 million per quarter range.

These successes provide potential acquirers with plenty of comfort in the quality of assets they obtain from under Lapid's leadership. So, what does this mean for ALVR's future under Lapid?

A deeper look into Axerra provides insight into why DRWI might consider buying ALVR next. The following slide from an Axerra presentation shows that its technology gives DRWI with a greater vested interest in WiMAX (ALVR's primary technology). In fact, Axerra allows service providers to convert any packet access network (Carrier Ethernet, broadband wireless including WiMAX, cable HFC, xDSL, xPON, etc.) into a full-service alternative to TDM access. We believe this capability could make ALVR / DRWI combination very synergistic.

On the buyer side of the equation, DragonWave's website states that its CEO, Peter Allen has

extensive experience in mergers and acquisitions and has been involved in numerous multi-billion dollar transactions

Indeed, the company has acquired a company in each of the last two years. Looking at ALVR's cost structure, it's easy to see how an acquirer could take advantage of operating synergies to make Alvarion a very accretive deal.

So, will DRWI's 2012 target be ALVR? Time will tell. In the meantime, investors will be heartened to discover that ALVR's board believes that Lapid's primary strength is business execution (no doubt, a reputation he first earned during his earlier stint with Alvarion). Indeed, a company contact informed us that ALVR's board is "intent on execution and returning the company to profitability" and referred to Hezi Lapid as "Mr. Execution".

In "3 Stocks To Triple On The Mobile Data Offloading Boom", we discussed ALVR's current valuation and opportunity. The company has certainly suffered from poor execution, but if you've done your homework, you can see that the company possesses a substantial amount of unlocked shareholder value. It has a large customer base, almost $200 million in revenue, continues to sign multi-million dollar deals, and files new patent applications at a near-monthly pace (and, more importantly, have been granted new patents at an equally torrid rate).

Yet, due to its many miscues, investors have left the company for dead. But this is how bottom fishing works. Through careful research, investors can assess the unlocked value of companies that are priced for death. With one right move, the company can find a way to unlock its true value. When that happens, investors can make several times their money.

To maximize profits, you can't invest after the fact. By that time, everyone sees how much unlocked value the company has and the shares are already significantly higher. You have to have vision into what can be done with the company's various assets under certain circumstances.

In the case of ALVR, the company has just handed the reigns to an executive with a track record of execution, value creation, and acquisition, potentially signaling a turning point in the company's fortunes...and that of its investors.

<<<

Horizon Pharma -

http://www.fool.com/investing/general/2012/09/20/biotech-investors-todays-big-plunge-and-rally.aspx

>>> Horizon Pharmaceuticals (Nasdaq: HZNP ) plunged 24%, after pricing a secondary offering at $3.50 per share significantly below yesterday’s close of $4.58. Even worse for existing investors, the offering size increased by 40%, from 15.3 million shares to 21.4 million. Dilution is a part of life for small cap biotechs, and the $75 million will go a long way to paying down debt, ramping up its sales force, and keeping the business funded for another 12 months. Horizon recently signed a deal with a Covidien (NYSE: COV ) subsidiary to sell Duexis, but bringing Rayos to market has raised cash burn to $70 million over the last 12 months. If successful, all will be forgiven; but if they don’t scale up fast enough, expect more dilution, likely in late 2013.

<<<

Peregrine -

http://ir.peregrineinc.com/releasedetail.cfm?ReleaseID=708954

September 24, 2012

Peregrine Pharmaceuticals Announces That It Has Discovered Major Discrepancies in Treatment Group Coding by an Independent Third-Party Vendor Responsible for Distribution of Blinded Investigational Product Used in Its Bavituximab Phase II Second-Line Non-Small Cell Lung Cancer Trial

The Company Is Currently Conducting a Detailed Review, Including Assessing Its Impact on Overall Trial Results; Investors Should Not Rely on Previously Reported Clinical Data Disclosed From This Phase II Trial at This Time; These Recent Findings Do Not Impact Other Ongoing Bavituximab Clinical Trials

TUSTIN, CA -- (Marketwire) -- 09/24/12 -- Peregrine Pharmaceuticals (NASDAQ: PPHM) announced today that during the course of preparing for an end-of-phase II meeting with regulatory authorities and following recent data announcements from its randomized, double-blind placebo-controlled Phase II trial of bavituximab in second-line non-small cell lung cancer, it discovered major discrepancies between some patient sample test results and patient treatment code assignments. Due to the double-blind nature of the trial, Peregrine was not permitted to have access to either patient group assignments or related product coding information. As part of the trial's execution, Peregrine contracted with independent third-party contractors to execute treatment group assignments and oversee clinical trial material coding and distribution according to established procedures. A subsequent review of information has determined that the source of these discrepancies appear to have been associated with the independent third-party contracted to code and distribute investigational drug product.

This discrepancy is specific to this trial and will have no impact on other ongoing bavituximab trials.

Peregrine intends to communicate further as soon as it is able to determine the impact of this issue. In the meantime, investors should not rely on clinical data that the company disclosed on or before September 7, 2012 from its Phase II bavituximab trial in patients with second-line non-small cell lung cancer or any presentations or other documents related to this Phase II trial.

About Peregrine Pharmaceuticals, Inc.

Peregrine Pharmaceuticals, Inc. is a biopharmaceutical company with a portfolio of innovative monoclonal antibodies in clinical trials focused on the treatment and diagnosis of cancer. The company is pursuing multiple clinical programs in cancer with its lead product candidate bavituximab and novel brain cancer agent Cotara®. Peregrine also has in-house cGMP manufacturing capabilities through its wholly-owned subsidiary Avid Bioservices, Inc. (www.avidbio.com), which provides development and biomanufacturing services for both Peregrine and outside customers. Additional information about Peregrine can be found at www.peregrineinc.com.

<<<

Questcor -- >>> Questcor: Primed For A Big Bounce

September 23, 2012

by: Efsinvestment

Edited by Adam Isaac

http://seekingalpha.com/article/882651-questcor-primed-for-a-big-bounce?source=yahoo

Questcor (QCOR) sunk almost 50% on September 19, 2012 after Aetna (AET) announced that it was going to stop coverage of Acthar for certain conditions. The company announced in the policy bulletin that Questcor's Acthar gel was medically essential for only infantile spasms. Aetna's policy bulletin suggested that the medicine is not superior to other therapies in the 18 other conditions that it was approved to treat. The policy document was immediately utilized by short sellers, and a negative report was issued. The market also took the news badly, and the stock lost almost half of its value in one day. However, the stock has already started recovering and the conference call by the company has helped to clear the issue. As I mentioned in my previous article, there remain strong prospects for the drug.

Acthar is a unique drug that does not compete with other treatment agents. Acthar should be used for patients who have been through other treatment regimes such as steroids. The drug is prescribed only to patients for whom the primary treatment has had no effect. Once the physician and patient reach for Acthar as a treatment approach, they have normally tried the primary treatments to no advantage. Acthar is high-priced product which is used in a very limited population. The conference call also clarified that the reimbursements for Acthar are never routine, and it works on a case by case basis. As the company announced, that Aetna only constituted 5% of the total reimbursements for Acthar. Other insurance providers would have to follow suit in order to justify such large fall in price. However, other insurers have not shown any sign of stopping coverage of Acthar.

In addition, the company emphasized that the policy decision was interim. It is likely to be reviewed in October, where the company hopes it will be overturned as negotiations carry on with the company. The usual reimbursement process for an Acthar prescription is very labor intensive, and the company has a team of over 30 reimbursement specialists working on the process. This grueling procedure to secure Acthar coverage or individual prescriptions has been ongoing constantly since late 2007. Requirements for achieving coverage for an Acthar prescription have amplified over time. The company contributes in the Medicaid program. It formerly announced that Medicaid will bring down its reimbursement rates for Acthar gel. This means that insurance companies will have to cover a lower ratio of the total cost. Questcor will get considerably more proceeds from sales to the government. As a result, the operating results of the company will be further improved as the company is already experiencing a healthy growth in sales.

Questcor Stock Price:

QCOR data by YCharts

Financial Highlights:

According to the earnings report, the firm recorded sales of $112.5 million due to the expanded physician usage of Acthar gel. The usage saw increase mainly in idiopathic nephrotic syndrome and MS exacerbations. The increase in sales was over 200% as compared to the last year, when the firm recorded sales of $46 million. Net income for the quarter was $41.5 million or $0.65 per diluted share, in contrast to $13.9 million, or $0.21 per diluted share for last year's equivalent quarter.

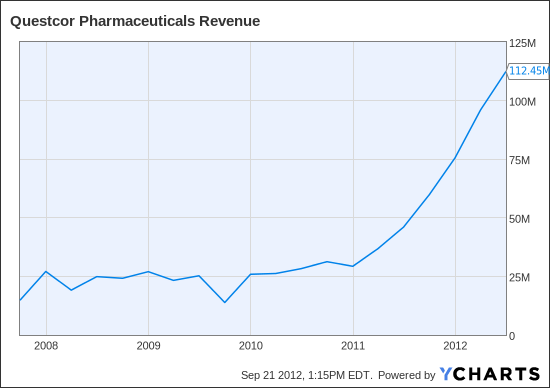

However, net sales for the first six months were $208.4 million, as compared to $82.8 million in the first six months of 2011. The company used $156.1 million in cash to buy 3.7 million shares of its common stock in the open market, at an average price of $41.85 per share, during the second quarter. Shares outstanding were 59.7 million at June 30, 2012 and 62.3 million at June 30, 2011.

Questcor dispatched 4,710 vials of Acthar during the quarter, up 94% compared to 2,430 vials in the same quarter last year. Quarterly vial batches are subject to considerable deviation due to the volume and timing of specific orders received from the company's distributor. The timing of these orders can considerably influence net sales and net income in any particular quarter. Channel inventory in the second quarter looks to be in the regular range.

Questcor Revenue:

QCOR Revenue data by YCharts

Summary:

As I have stated in my earlier article, Questcor has a unique product which faces very low competition at the moment. There remain huge growth prospects for the company due to the lower market penetration. In addition, the company is in a very healthy financial position. At the moment, there is no long term debt at the balance sheet of the company. Revenue has shown a strong growth trend. The company has surprised the market in its previous six earnings announcement, and I expect the trend to continue. I believe the stock will hit $40 again soon as the pressure of the news fades.

<<<

Rosetta Genomics

http://www.stockpickr.com/3-stocks-under-10-making-big-moves.html-0?puc=yahoo&cm_ven=YAHOO

>>> Rosetta Genomics (ROSG) develops and commercializes diagnostic tests based on microRNAs. This stock is trading up 5.6% to $6.55 in recent trading.

Today’s Range: $6.29-$6.87

52-Week Range: $1.40-$23.43

Volume: 3.1 million

Three-Month Average Volume: 1.6 million

From a technical perspective, ROSG is pushing higher here back above its 200-day at $6.09, and its flirting with its 50-day at $6.62 with above-average volume. This move is quickly pushing ROSG within range of triggering a major breakout trade. That trade will hit once ROSG manages to clear some near-term overhead resistance at $6.65 to $7.19 with high volume. At last check, ROSG has hit an intraday high of $6.87 and volume is well above its three-month average action of 1.6 million shares.

Traders should now look for long-biased trades in ROSG as long as its trending above its 200-day, and then once it sustains a move or close above those breakout levels with volume that’s near or above 1,610,000 shares. If that breakout triggers soon, then ROSG will have a great chance of re-testing or possibly taking out its next major overhead resistance levels at $9 to $12.

<<<

Groupon -- >>> Dual-Class Social Media Companies: Performance-Ownership Link?

September 11, 2012

includes: FB, GRPN, LNKD, Z, ZNGA

By Michelle Lamb

Senior Research Associate, GMI Ratings

http://seekingalpha.com/article/860761-dual-class-social-media-companies-performance-ownership-link?source=yahoo

Shareholders have long been concerned about multiple classes of stock with disparate voting rights since such a structure divorces decision-making power from financial exposure. Despite this, recent social media company IPOs have chosen to have two or sometimes three classes of common stock with different voting power and it appears many are currently suffering in the marketplace.

As Nell Minow recently explained, "[t]he essential principle at the core of capitalism is the assurance that investors' money will be honorably managed by the corporate executives. That means if their interests are mis-aligned, the shareholders can replace managers with better ones. That cannot happen if the insiders control the voting stock." Studies have shown the presence of dual classes of stock reduces investment by institutional investors, and has become a risk factor in many corporate governance screens, including ours at GMI Ratings, because of its relationship to increased governance risk. Indeed, the structure is only adopted at a minority of public companies (only 40 S&P 500 and 268 Russell 3000 companies). However, several high profile companies - specifically recent social media IPOs Facebook (FB), Groupon (GRPN), LinkedIn (LNKD) and Zynga (ZNGA) - recently adopted multiple class share structures and many have since suffered major stock price declines or developed other governance concerns.

In addition, the largest and one of the most influential public pension funds, CalPERS, recently announced that it would: "Develop an IPO governance expectations document, explaining the governance expectations [it] has for public companies… [and] address core governance standards of accountability and transparency such as removing dual class, classified, or plurality voting structures." Companies with dual class share structures are under close examination and it would appear likely that CalPERS, among other large public funds, will engage privately with such firms to persuade them to remove differential voting rights and implement a one-share, one-vote structure.

Below we outline the details of these structures and the companies' recent troubles.

Facebook

Pre-IPO Facebook had adopted a dual-class share structure, which many claim followed Google's (GOOG) example from 2004 with both firms giving their Class A common stock one vote per share and Class B 10 votes per share. As we recently explained in a Forbes blog, pre-IPO founder Mark Zuckerberg held "almost 57 percent of the voting power of the stock through ownership and voting power over other shareholders' stock via what is known as an irrevocable proxy. You all know what irrevocable means. So that really means that elections and any issues at the annual meeting are his to decide." The company's share price is now infamously on the decline, falling from a closing price of $38 at its May IPO to an all-time low last week around $18. The company has also made headlines for insider stock sales, and its PR struggles to defend its originally all-male board and concerns over directors' lack of independence (which included the sole female member it recently appointed, the COO Sheryl Sandberg.) GMI Ratings assigned Facebook an ESG Rating of D since its IPO.

Groupon

Groupon, the e-commerce discount company, has come under fire for several reasons in the past year since its November 2011 IPO. Most recently its share price slide from IPO closing price of $26 to this week's price around $4, but also in past months for its apparent lack of financial expertise (and resultant restatements). We wrote a pieces for Forbes in April on the various board overcommitments, interlocking relationships and lack of financial expertise. Recently some of Groupon's investors, like Marc Andreesen have begun selling their shares. Again, this is a company with a multiple class share structure with the disparate voting rights favoring insiders - its Class B common stock has 150 votes per share and its Class A has one vote per share. As of December last year, the three founders (Eric Lefkofsky, Bradley Keywell and Andrew Mason) controlled 100 percent of the Class B and about 33 percent of the Class A common stock, resulting in about 57 percent of the voting power. GMI Ratings does not include Groupon in its coverage universe as of this date.

LinkedIn

Another social media company with 1 vs 10 votes per share for their Class A vs B common stock respectively, the professional networking company LinkedIn nevertheless has a share price that has actually increased somewhat since its IPO. This may explain how it has avoided as much intense media scrutiny as its peers, however the governance concerns of such an ownership structure remain. As of their 2012 proxy, LinkedIn's "all executive officers and directors as a group" controlled 76.8 percent of the company's voting power; the largest contributors to this total include Chairman Reid Hoffman's beneficial ownership of 45.4 percent of the Class B voting power (and he controls 39.4 percent of the company's overall voting power), Sequoia Capital's 17.8 percent control (via Director Michael Moritz) and Greylock Partners' 14.9 percent of the overall voting power (via Director David Sze).

Zillow (Z)

This online real estate marketplace company shares the same 1 vs 10 votes per share, dual-class ownership model. Zillow is not part of the GMI Ratings coverage universe for ESG Ratings yet, but has had an "Aggressive" AGR accounting risk rating since its IPO which has now changed to "Very Aggressive". Zillow's all-male board of directors appears to be closely associated with either Microsoft or its spin-off Expedia, the firm that purchased Zillow founder and CEO Spencer Rascoff's former company Hotwire.com in 2003. Indeed, five of the eight directors were associated with Expedia in one way or another. Included on the board is Executive Chairman Rich Barton who himself had founded Expedia and was the prior CEO of Zillow before he was succeeded by Spencer Rascoff in September 2010. The company's current AGR rating places them in the 6th percentile among all companies in North America (indicating higher governance risk than 94 percent of companies). Among its accounting red flags are its rate of Mergers and Acquisitions, and its ratio of Goodwill to Total Assets. We described the concerns related to its aggressive purchasing strategy and potential goodwill estimate revision risk in a piece here last week. As of their 2012 proxy, Directors Barton and Lloyd Fink held 56.5 and 43.5 percent of the Class B voting power, contributing to the "All executive officers and directors as a group" total of 87.5 percent of the company's voting power.

Zynga

In an exceptional move, the online social gaming company Zynga created not just two classes of stock with disparate voting rights, but a third class of "supershares" wholly owned by Chairman and CEO Mark Pincus - his class enjoys 70 votes per share while the shares available to the public have only one vote per share. The other class of stock, available only to company insiders, has seven votes per share. As of their 2012 proxy filing, Mr. Pincus owned 14.6 percent of the company but controlled 37.6 percent of the vote due to his 100 percent ownership of the Class C shares. "All executive officers and directors as a group" control 45.6 percent of the voting power of the company. Zynga is among the social media companies to have seen a major share price decline since its IPO, falling from about $9 last December to around $3 this week. Zynga is not part of the GMI Ratings coverage universe as of this date.

Conclusion

What is now referred to as "the Zuckerberg Grip," this voting control exercised by insiders via multiple class share structures is becoming "the new normal" for tech company IPOs. Whether their governance woes and share price declines are directly related to their choice in ownership structure remains a contentious debate; we have our opinion.

Company

IPO date

Share Class

(Votes per share)

Share Price at IPO

Closing Share Price 9/5/2012

Facebook

5/18/2012

Class A common (1), Class B common (10)

$38.23

$18.58

Groupon

11/4/2011

Class A common (1), Class B common (150)

$26.11

$4.18

LinkedIn

5/19/2011

Class A common (1), Class B common (10)

$94.25

$113.28

Zillow

7/20/2011

Class A common (1), Class B common (10)

$35.77

$42.43

Zynga

12/16/2011

Class A common (1), Class B common (7), Class C common (70)

$9.50

$2.92

<<<

Groupon -- >>> The Bizarro World of Social Media

By AnnaLisa Kraft

September 11, 2012|

Tickers: AMZN, GRPN, YELP

http://beta.fool.com/leglamp/2012/09/11/the-bizarro-world-of-social-media/11364/?ticker=AMZN&source=eogyholnk0000001

AnnaLisa is a member of The Motley Fool Blog Network -- entries represent the personal opinions of our bloggers and are not formally edited.

In the Bizarro world of internet stocks, an insider NOT selling becomes the headline. Like this one over Labor Day weekend from All Things D, “Groupon Co-Founder Eric Lefkowsky Doesn’t Sell Millions of Shares.” Turns out he transferred some 18.7 million shares to a family charitable foundation as well as some LLCs. Whew!

Similarly, Yelp (NYSE: YELP) shares spiked 22% when insiders did not sell during the lockup expiration and Facebook shares rose 6% when it was announced Mark Zuckerberg would not sell shares for a year. It’s a dangerous sector when not selling instead of insider buying becomes the news.

Groupon (NASDAQ: GRPN) in particular has suffered in this netherworld of social media stocks down almost 90% from its high hitting a low on $4.00 on September 4. Then there is ‘frenemy” Howard Schulz , CEO of Starbucks who quit the board in April making a mega-million dollar coupon deal with archrival Living Social. More indignities have been heaped on as top salespeople leave including national sales executive Lee Brown and Jayne Cooke, who brokered some of Groupon’s most successful deals with Gap and Nordstrom.

Like a superhero bound and humiliated by a nemesis the Q2 earnings release on August 12 which reported a 4% decline in gross billings to $1.29 billion since Q1 (Gross billings are what businesses are charged for the Groupon deal) and disappointing on revenues from analysts’ estimates humbled the stock as share price dropped 43% over little more than two weeks. The call also cited major weakness in Europe with exchange rates and economic malaise hurting their numbers. Still, that begs the question if Europeans are so strapped shouldn’t a discount deal site do well? CEO Andrew Mason informed on the call that deals over $100 in Europe weren’t selling well but are initiating a deal ‘personalization’ program much like they already have in the States to improve sales.

But all is not lost for Groupon. Groupon Now!, a service which enables mobile users to get an immediate deal based on their geographical location, is gaining ground. Mobile use of Groupon is up 33% in North America partly due to Groupon Now!

Then there’s Groupon Goods, a direct-to-consumer site offering physical merchandise at a discount. This segment is growing 30% if revenues are counted in the same manner as revenue from Groupon deals. But Barclays analyst Mark May downgraded the stock believing the Goods strategy is a risk to profit margins. May was also concerned about customer growth stalling. He predicted 15% downside to $4.00. Prophecy fulfilled.

Also unfortunate for Groupon was the exodus of early investors like Battery Ventures, Andreesen Horowitz and Kinnevik Investment AB. Groupon still has loyal friends in T. Rowe Price and Morgan Stanley who have upped their stakes. Oldest and firmest friend New Enterprise Associates hasn’t sold any shares and neither has Kleiner Perkins.

Yelpers Not Selling

Similar headlines ran after the lock up expiration for Yelp and the stock has risen almost 30% since then. It rose another 6% after CEO Jeremy Stoppleman spoke optimistically of the company’s mobile future at a Citigroup conference on September 5. He emphasized ads would be, ”unobtrusive to the user” and remarked that mobile unique users are up 25%. Yelp is a service which allows users to review businesses and products and is monetized by paid ads from businesses. According to a study just released by UC Berkeley economics professors a rise of even a half star rating on Yelp reviews increases the likelihood of packing a restaurant at peak hours by 33%. Note that the businesses have no control over the review content but the ads can attract new customers.

The move in Yelp may have capped short term upside but all these social media stocks are quite fragile like social butterflies, and if you’re interested, the price will likely come down.

For these social media stocks it’s all about mobile and insiders not selling stock. Both have negative EPS, Yelp at $0.37 and Groupon at $0.19 and both, even now, have short interests of over 20%. What’s interesting is the forward P/E for Dec 31, 2013 for Yelp is 516 but for Groupon is 11.38 if the share price doesn’t move at all. Could it be that Groupon has sunk to a level where it is a buy? It has $1.5 billion in cash. An ambitious, call it heroic, push against Amazon.com (NASDAQ: AMZN) on two fronts with the Groupon Goods business and against Living Social, of which Amazon owns a 29% stake, could prove very interesting to watch.

It already hit the price target of $4.00 that Barclays predicted. I wish I was as good as a prognosticator as Mark May but maybe Groupon is a better buy than Yelp right here. As long as Bizarro headlines keep coming out like “Summer intern Susie Creamcheese is NOT selling her Groupon shares!!!” there is a glimmer of hope for Underdog!

<<<

Groupon -- >>> Groupon: What It's Done And What It Will Do

September 11, 2012

by: BH News Wire

http://seekingalpha.com/article/858611-groupon-what-it-s-done-and-what-it-will-do?source=yahoo

After having what was believed to be a successful IPO, Groupon (GRPN) shares finally took a nose dive after three months of better than expected success. Shares are now down over 83 percent since the IPO. It turns out that Google's $6 billion offer to Groupon would have been the better option after a series of earnings disappointments, a gaggle of accounting adjustments, and several quarters in the red. With its first profitable quarter now in the rear view mirror and with more profitable quarters expected to follow, is now the time to buy Groupon at under $5?

One of my trading mantras is that if a stock's price has gone down 80 percent in under a year, it can always go down another 80 percent. Groupon is no exception. The company has done a good job staying at the front of the market as Google Offers and Living Social have still not come close to surpassing the daily deals site. Most of its competition has come from a host of companies beefing up their rewards programs. This includes rewards and cash back programs from credit card companies along with customer rewards programs of many restaurants and retailers. They can leverage their already profitable businesses to create deals similar to Groupon's at a cheaper cost to their partner companies. In addition many of Groupon's previous partners have realized they can promote their own deals and not have to pay the hefty 50 percent premium that Groupon usually takes.

Based on analyst estimates, Groupon is expected to have around 30 percent per annum earnings growth over the next five years, along with a 37 cent earnings per share estimate in 2013. At its current price of $4.26, Groupon actually looks like a good value buy right now. This low valuation is by no means an oversight by the market. Many investors expect more accounting mistakes and missed earnings over the next few years. Groupon's revenue was $1.6 billion in 2011 and its expected revenue in 2013 is $2.83. Many Groupon subscribers have already gotten sick of daily deals e-mails that are for the most part useless, so growing the business by that much in such a short time is going to be a giant challenge.

Right now I would put a hold-to-sell recommendation on Groupon. The bubble looks like it's finished bursting for now, but I still do not trust the management or business model enough to make Groupon a part of my portfolio. I would expect shares to fluctuate between $3 and $6 over the next year and I don't believe Groupon's infamous one day swings will become a thing of the past. Shares are simply too volatile for the average investor.

<<<

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |