Alternatively (1) cash payback or (2) debt refinance they said in the ER CC, well. Will see.

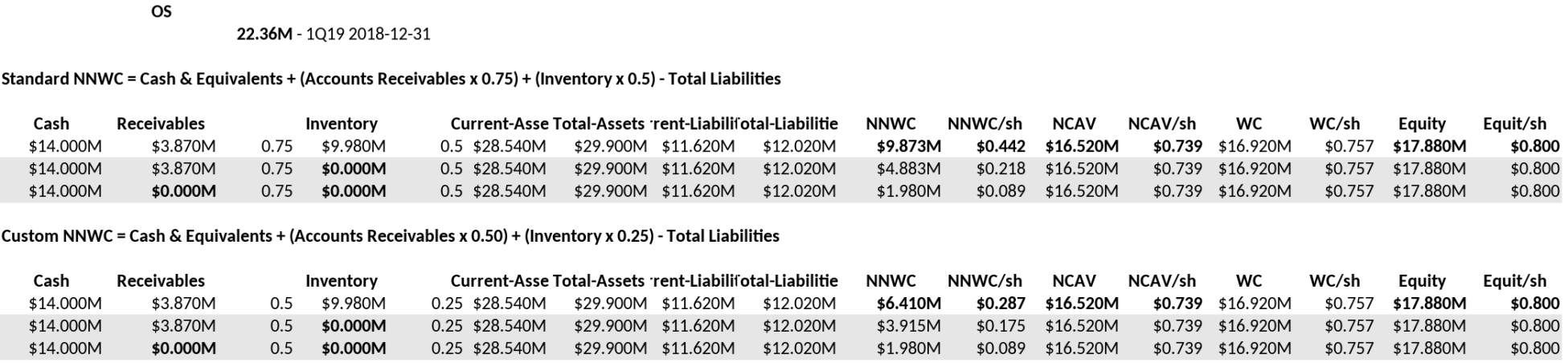

Here the not so bad balance sheet value:

equity 80c/sh, WC 76c/sh, NCAV 74c/sh, NNWC 44c/sh

(copy/paste from SoS on ST)

PS: It is an interesting loss of MCAP here over the last days, sort of more than 50% for a temporary 30% revenue haircut.

So that might not be the case? Or just overdone?

Ownership is around 26% tutes and many increased in 4Q18.

Possible that they will support SP?

Still on WL

News

News  Market Data

Market Data  Discover

Discover