Sunday, September 24, 2023 6:41:22 AM

The section Purposes makes clear that it's related to secondary market operations (pooling loans into securities). So, restricted and, for instance, unrelated to refinancings and loan modifications.

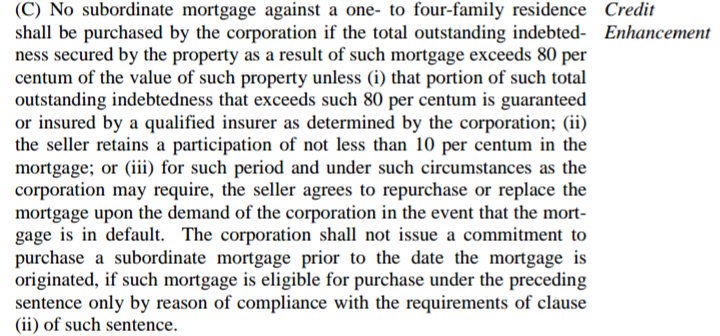

In turn, these secondary market operations are restricted in the Credit Enhancement clause, that requires a maximum credit risk of 80% LTV, unless there is one of the 3 prerequisites:

(i) The portion > 80% LTV, is insured by the borrower (PMI)

(ii) The seller retains > 10% of the mortgage.

(iii) 100% guaranteed against default by the seller.

For instance, the PLMBS were illegal and today's CRT too (not among the enumerated)

Also, the law that split Fannie Mae into two, the current Fannie Mae and Ginnie Mae, makes clear that the latter kept everything related to the special assistance functions (Federal programs to help borrowers)

A Conservatorship isn't a state with a free pass to break the law or Accounting Standards, regardless of being in the best interests of FHFA and its hedge funds guard.

And outside Conservatorship, the same restricted activities.

The Dems/Trump's deregulation is no other thing than breaking the laws playing the fool covering them up (corrupt litigants, etc), or enacting new laws that break existing laws:

-2008 HERA (Pelosi, Calabria): UST backup of FnF, duplicated. Mandatory release, removed. Breach of the Fee Limitation of U.S. clause with the 4.2 bps for Affordable Housing funds managed by HUD and UST; a Warrant to protect the taxpayer ; infinite rate on SPS.

-2012 TCCA (Pelosi, Watt, Waters) for 10 bps TCCA fee.

-2021 CARES Act for the continuation of the TCCA fees.

Very different from your

FHFA policies will change dependent on the political party in power.

Glidelogic Corp. Becomes TikTok Shop Partner, Opening a New Chapter in E-commerce Services • GDLG • Jul 5, 2024 7:09 AM

Freedom Holdings Corporate Update; Announces Management Has Signed Letter of Intent • FHLD • Jul 3, 2024 9:00 AM

EWRC's 21 Moves Gaming Studios Moves to SONY Pictures Studios and Green Lights Development of a Third Upcoming Game • EWRC • Jul 2, 2024 8:00 AM

BNCM and DELEX Healthcare Group Announce Strategic Merger to Drive Expansion and Growth • BNCM • Jul 2, 2024 7:19 AM

NUBURU Announces Upcoming TV Interview Featuring CEO Brian Knaley on Fox Business, Bloomberg TV, and Newsmax TV as Sponsored Programming • BURU • Jul 1, 2024 1:57 PM

Mass Megawatts Announces $220,500 Debt Cancellation Agreement to Improve Financing and Sales of a New Product to be Announced on July 11 • MMMW • Jun 28, 2024 7:30 AM