Wednesday, March 22, 2017 12:01:36 AM

Problem 1.

Registered users

As of August of last year, the company was at 950k registered users

(Source: Most recent 10Q, Nov 2016)

Yesterday they PRed 1M users. Question number one: How many users did they add in Which means they added 50k users (Registrations is not the same as daily users, mind you).

They are not growing fast enough. 50k new registrations in 7 months = 7.5k registrations / month, or less than 1%

Problem 2.

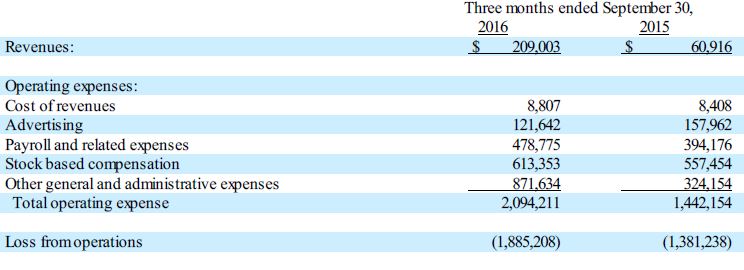

Significant operating losses:

950k users all in all provided them with roughly $200k in revenue last quarter. Let's be more generous, lets round it up significantly. 950k user gets them to $100k/revenue a month. Their loss from operations is about $600k/ month. It means since last report they probably lost $2M. We will know exact amount soon enough

Problem 3.

Forward revenue.

If you put 1 and 2 (above) together, you will see that their estimated revenue could NOT increase significantly. Their user base grew at the rate of 5% in 6 months. Their revenue, most likely, grew at the same pace. Remember how I rounded up above? Such a small increase in registrations means I can estimate flat revenue QoQ. So same $300k of revenue and same $500k/mo in net losses from operations. Ok, let's say there was zero stock compensation, zero other SG&A (which will not be a zero, by the way). Still, their advertising and payroll is double the revenue and this is not likely to change in the future. Losing money hand over fist. Yes, they did raise almost $3M. So what? In the last 9 months their loss from operations was exactly $6M. You do the math.

1M registrations got them to $100k/mo in revenues... or about 10 cents per registration.

Problem 4.

Payroll

According to most recent 10q, they had 24 full-time employees. Yet, payroll (excluding stock compensation) is ridiculous $500k/quarter. (And if you include stock compensation, it adds up to $1.1M in compensation in 3 (THREE!!!)months for 24 people. Which means, each employee averages $20k/quarter. (excl comp) or $50/k quarter (including stock comp). I can see management getting paid this much (yeah, for growing registrations 50k in six months, let's celebrate!), but c'mon, this is totally messed up. American weed dream, in other words

Problem 5.

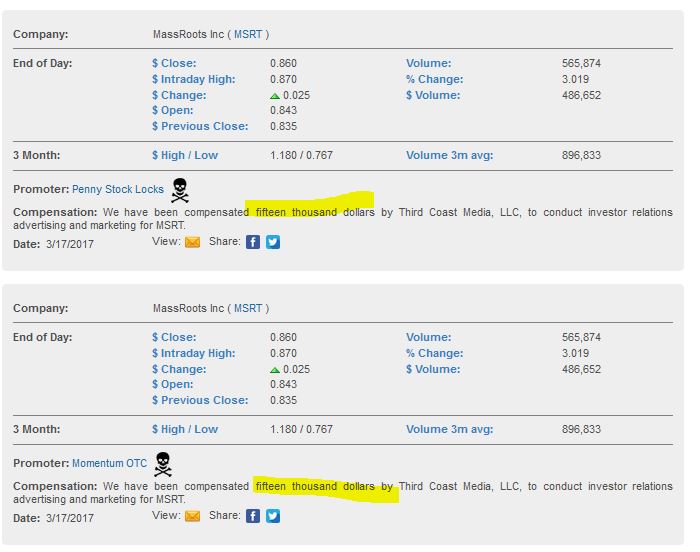

Stock promotion

Annual report is imminent. Company is heavily promoting their stock in order to stimulate run-up into earnings. (Here is a sample, but I found at least 4 stock promoters that picked up this stock last Friday). Each of those gets compensated $15k, for the total of at least $60k. Hey, that's almost their monthly revenue! No biggie.

Such promotion hasn't done much to the stock, though. Share price increased from $0.87 open on a Monday to $0.89 close on a Tuesday.

And, as I mentioned, annual report is imminent. I will speculate that if company was expecting stock price to rise due organically to very positive report, they wouldn't pay tons of money in an attempt to spike the price. Which, in my own opinion, could mean only one thing, the report will show more losses.

Problem 6.

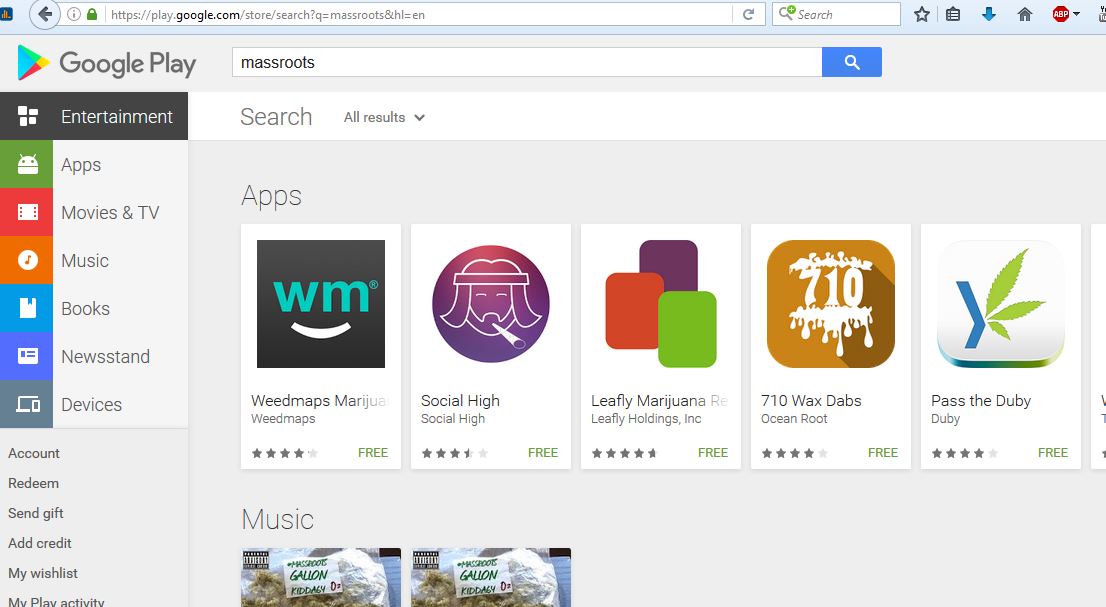

Google Play store

Look at this business update from about a month ago:

Then look at the google play store as of today (3/21).

Nope. It's not there. If anything, the number of initial registrations may have gone up, but the number of users actually dropped significantly due to Android users (over 50% of the market in the US in controlled by Android, and is not being able to use this app)

Problem 7.

Dilution.

At the end of 2014, weighted average number of common shares was 14 Millions

At the end of 2015, it was 44M

At the end of Sep 2016, company had 54M O/S

Last known data shows about 67M O/S

The company issues approximately 20M shares annually. Keeping today's market cap constant (which I doubt will be the case), a year from now each share will be worth about 25% less given current rate of dilution.

Let's recap.

Although valued at nearly $75 million, the company brings less than $100k in monthly revenues. At the same time their operating losses exceed $500k/month. Their registrations are hardly growing. Their current number of active users is not public.

1M registrations got them to $100k/mo in revenues... or about 10 cents per registration.

They are not even present in google play store, which covers over 50% of the market in the US, and even more market outside of the US

They are paying hefty bucks for stock promotion, alas it's barely moving the needle

Their annual report will be here shortly. Last year it was published on March 30 so I probably give it another week. I don't anticipate any significant improvement to operating profits, though.

And it still continues to trade at $75 million valuation. For how much longer? The bear case here is quite convincing

The only source of capital is new stock/new warrants/p-notes etc. This will dilute stock further. (in case you are wondering, they have 200M A/S, so long way to go in diluting the heck out of this stock)

Considering all of the above, I would say this is definitely significant market underperform. Not even a 'hold', I would recommend getting out, taking whatever profits, and not looking back. Alternatively, shorting this stock might also prove to be a viable option.

I will be interested in hearing bull case here, however, please be specific, saying things like 'to the moon' and 'the market will grow' are not specific enough. Looking for tangible evidence before I can pull the trigger.

16

Recent GWAV News

- Greenwave Technology Solutions Further Strengthens its Balance Sheet • PR Newswire (US) • 04/23/2024 11:07:00 AM

- Greenwave Technology Solutions Regains Compliance with Nasdaq Market Value of Listed Securities Requirement • PR Newswire (US) • 04/04/2024 12:08:00 PM

- Greenwave Technology Solutions Strengthens Balance Sheet by Approximately $14.87 Million • PR Newswire (US) • 04/01/2024 01:55:00 PM

- Greenwave Technology Solutions' Scrap App Launches A.I. Features to Scale and Grow into New Markets • PR Newswire (US) • 03/26/2024 12:08:00 PM

- Greenwave Technology Solutions' Second Shredder Currently Being Connected to Power Grid by Dominion Energy Ahead of Schedule • PR Newswire (US) • 03/25/2024 12:34:00 PM

- Greenwave Technology Solutions Successfully Restructures Debt to Facilitate Continued Growth • PR Newswire (US) • 03/19/2024 11:23:00 AM

- Greenwave Technology Solutions' Scrap App Expands to Richmond, VA Market as it Continues to Capture Market Share • PR Newswire (US) • 03/04/2024 04:37:00 PM

- Greenwave Technology Solutions' Second Shredder Scheduled to Be Connected to Power Grid by April 9, 2024 • PR Newswire (US) • 02/15/2024 08:18:00 PM

- Form SC 13G/A - Statement of acquisition of beneficial ownership by individuals: [Amend] • Edgar (US Regulatory) • 02/14/2024 09:11:06 PM

- Greenwave Technology Solutions Releases Shareholder Update • PR Newswire (US) • 02/13/2024 04:00:00 PM

- Form SCHEDULE 13G - Statement of acquisition of beneficial ownership by individuals • Edgar (US Regulatory) • 01/31/2024 09:30:33 PM

- Greenwave Technology Solutions' Scrap App Continues Capturing Market Share • PR Newswire (US) • 01/30/2024 06:21:00 PM

- Greenwave Technology Solutions Receives License from Ohio Bureau of Motor Services • PR Newswire (US) • 01/24/2024 03:47:00 PM

- Greenwave Technology Solutions Generates More than $9 Million Revenue in Q4 2023 • PR Newswire (US) • 01/22/2024 05:31:00 PM

- Greenwave Technology Solutions Commences Operation of Metal Baler, Wire Stripper, and Sheers at Non-Ferrous Processing Facility • PR Newswire (US) • 01/19/2024 01:45:00 PM

- Greenwave Technology Solutions' Scrap App Expands to Second Market as it Continues to Capture Market Share • PR Newswire (US) • 12/19/2023 06:11:00 PM

- Form 8-K - Current report • Edgar (US Regulatory) • 11/27/2023 10:15:41 PM

- Form 8-K - Current report • Edgar (US Regulatory) • 10/13/2023 08:49:08 PM

- Form 8-K - Current report • Edgar (US Regulatory) • 10/06/2023 09:15:11 PM

- Second Automotive Shredder at Greenwave Expected to Materially Increase Carrollton Facility's Revenues Beginning in Q4 2023 • PR Newswire (US) • 09/28/2023 01:37:00 PM

- Greenwave Technology Solutions Announces its Shear Baler is Now Fully Operational at its Cleveland Facility • PR Newswire (US) • 09/26/2023 12:00:00 PM

- Greenwave Technology Solutions Launches Scrap App with AI Pricing Engine in Development • PR Newswire (US) • 09/14/2023 12:08:00 PM

- Form 424B4 - Prospectus [Rule 424(b)(4)] • Edgar (US Regulatory) • 09/12/2023 09:15:18 PM

- Form DEF 14A - Other definitive proxy statements • Edgar (US Regulatory) • 08/31/2023 09:25:16 PM

FEATURED Cannabix's Breath Logix Alcohol Device Delivers Positive Impact to Private Monitoring Agency in Montana, USA • Apr 25, 2024 8:52 AM

Bantec Reports an Over 50 Percent Increase in Sales and Profits in Q1 2024 from Q1 2023 • BANT • Apr 25, 2024 10:00 AM

Kona Gold Beverages, Inc. Announces Name Change to NuVibe, Inc. and Initiation of Ticker Symbol Application Process • KGKG • Apr 25, 2024 8:30 AM

Axis Technologies Group and Carbonis Forge Ahead with New Digital Carbon Credit Technology • AXTG • Apr 24, 2024 3:00 AM

North Bay Resources Announces Successful Equipment Test at Bishop Gold Mill, Inyo County, California • NBRI • Apr 23, 2024 9:41 AM

Epazz, Inc.: CryObo, Inc. solar Bitcoin operations will issue tokens • EPAZ • Apr 23, 2024 9:20 AM