Thursday, March 09, 2017 9:55:28 PM

Follow this closely and feel free to validate it yourself. This will help people understand the numbers, along with the significant gain potential here...

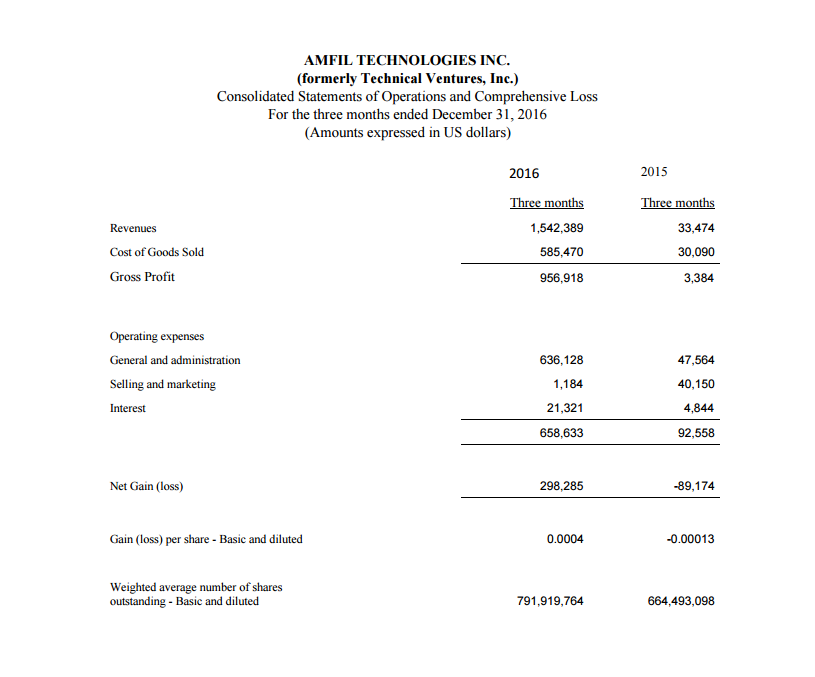

The net gain for the three months ended December 31 2016 was $298,285 compared to a net loss of $89,174 for the three months ended December 31, 2015. The gains for the current period relate to the recent acquisition of Snakes & Lagers Inc. being added to the financial statements.

With 444,807,264 shares outstanding and a $298,285 net gain last quarter, they had a .0007 EPS (earnings per share).

If we forward annualize this EPS, we get...

.0007 X 4 (quarters) = .0028 forward EPS

which means that if AMFE climbed to .028, it would still only have a Forward 10p/e.

Now, if we look at the p/e AVERAGE of ALL USA stocks, per Investopedia:

The average market P/E ratio is 20-25 times earnings

http://www.investopedia.com/terms/p/price-earningsratio.asp

Slow growth companies in boring sectors (utilities, etc), might have a p/e this low, but small rapid growth companies can easily reach a p/e in the hundreds... 100 p/e X .0028 EPS = .28 per share

Im not saying this is going to be like Amazon, but their p/e is just shy of 200 and its been as high as 3735!... Does AMFE, which grew 4500% last Q deserve a p/e higher than just 6 (currently)?

Based on the market average, AMFE is undervalued. .. but if we consider that this is an MJ play and that you dont even need to have revenue/profits to see a 9 figure market cap, it makes this a strong buy at this $7,000,000 valuation.... It could justifiably run 1000%+ from here, especially when you consider the sector they are in (MJ), the 3rd Snakes location coming, exclusive distibution deals, Interloc Kings, etc....

Heck, most MJ stocks dont even have a p/e ratio to even be discussed, which makes them VERY risky at their overinflated valuations. You gotta be profitable to have a p/e... Most MJ plays have a valuation built on pure hype/speculation of what they MIGHT do in the future... while AMFE has a FUNDAMENTAL reason to see much higher levels, based on widely accepted market statistics = safer investment, with the same amount of upside potential.

The GroZone subsidiary isn't even factored into this ultra low valuation... IMO the GZ subsidiary is worth this market cap alone, based on speculative potential... Most MJ penny stocks have low margin uncompetitive products. AMFE has a 1 for a kind system that could eliminate the need for pesticides, which is the sectors #1 concern right now, due to the new pesticide testing laws. Users of AMFEs system will be able to label their MJ "organic", instead of being confiscated for not passing the mandatory independent testing on each and every 5-10lbs of MJ grown. Proof: http://investorshub.advfn.com/boards/read_msg.aspx?message_id=128487444

(feel to copy and share any of my posts)

FYI, this doesn't use the new/reduced OS numbers...

My postings contain many opinions. So please do your own research

and validation.

Recent FUNN News

Glidelogic Corp. Becomes TikTok Shop Partner, Opening a New Chapter in E-commerce Services • GDLG • Jul 5, 2024 7:09 AM

Freedom Holdings Corporate Update; Announces Management Has Signed Letter of Intent • FHLD • Jul 3, 2024 9:00 AM

EWRC's 21 Moves Gaming Studios Moves to SONY Pictures Studios and Green Lights Development of a Third Upcoming Game • EWRC • Jul 2, 2024 8:00 AM

BNCM and DELEX Healthcare Group Announce Strategic Merger to Drive Expansion and Growth • BNCM • Jul 2, 2024 7:19 AM

NUBURU Announces Upcoming TV Interview Featuring CEO Brian Knaley on Fox Business, Bloomberg TV, and Newsmax TV as Sponsored Programming • BURU • Jul 1, 2024 1:57 PM

Mass Megawatts Announces $220,500 Debt Cancellation Agreement to Improve Financing and Sales of a New Product to be Announced on July 11 • MMMW • Jun 28, 2024 7:30 AM