Tuesday, February 07, 2017 9:27:35 PM

Follow this closely and feel free to validate it yourself. This will help people understand the REAL value here, so they wont miss an epic run, because they didn't understand what they own...

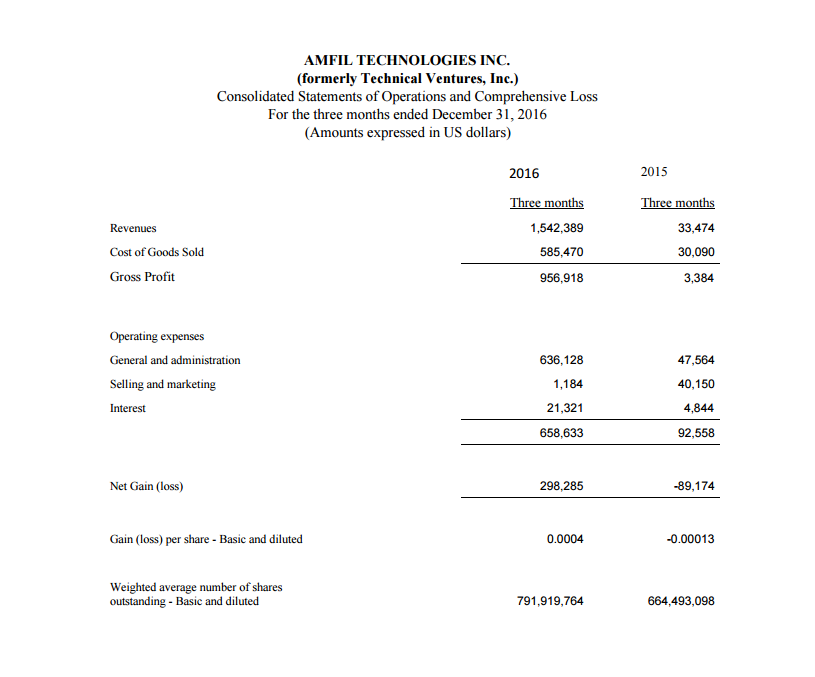

The net gain for the three months ended December 31 2016 was $298,285 compared to a net loss of $89,174 for the three months ended December 31, 2015. The gains for the current period relate to the recent acquisition of Snakes & Lagers Inc. being added to the financial statements.

With 791,919,764 shares outstanding and a $298,285 net gain last quarter, they had a .00038 EPS (earnings per share).

However, if we use the NEW share count, they had...

$298,285 (quarterly profit) / 421,919,764 (current OS) = .0007 EPS

If we forward annualize this EPS, we get...

.0007 X 4 (quarters) = .0028 forward EPS

This means that if AMFE climbed to .028, it would still only have a Forward 10p/e.

Now, if we look at the p/e AVERAGE of ALL USA stocks, per Investopedia:

The average market P/E ratio is 20-25 times earnings

Slow growth companies in boring sectors (utilities, etc), might have a p/e this low, but rapid growth companies can easily have a p/e in the hundreds... 100 p/e X .0028 EPS = .28 per share

Im not saying this is going to be like Amazon, but their p/e is just shy of 200 and its been as high as 3735!... Does AMFE, which grew 4500% last Q deserve a p/e higher than just 7 (currently)?

Based on the market average, AMFE is very undervalued. .. but if we consider that this is an MJ play and that you dont even need to have revenue/profits to see a 9 figure market cap, it makes this a must own at this $9,000,000 valuation.... It could JUSTIFIABLY run 1000%+ from here, especially when you consider the sector + the 2018 Cali Green Rush coming.

Heck, most MJ stocks dont even have a p/e ratio to even be discussed, which makes them VERY risky at $100,000,000++ valuations. You gotta be profitable to have a p/e... Most MJ plays have a valuation built on pure hype/speculation, while AMFE has a FUNDAMENTAL reason to see those levels, based on universally accepted market statistics

The GroZone subsidiary isn't even factored into this ultra low valuation... IMO this subsidiary is worth $30,000,000++ to the market cap alone, based on speculative potential... Most MJ penny stocks have low margin uncompetitive products. AMFE has a 1 for a kind system that could eliminate the need for pesticides, which is the sectors #1 concern right now, due to the new pesticide testing laws. Users of AMFEs system will be able to label their MJ "organic", instead of being confiscated for not passing the mandatory independent testing on each and every 5-10lbs of MJ grown. Proof: http://investorshub.advfn.com/boards/read_msg.aspx?message_id=128487444

My postings contain many opinions. So please do your own research

and validation.

Recent FUNN News

North Bay Resources Announces Composite Assays of 0.53 and 0.44 Troy Ounces per Ton Gold in Trenches B + C at Fran Gold, British Columbia • NBRI • Jun 18, 2024 9:18 AM

VAYK Assembling New Management Team for $64 Billion Domestic Market • VAYK • Jun 18, 2024 9:00 AM

Fifty 1 Labs, Inc Announces Acquisition of Drago Knives, LLC • CAFI • Jun 18, 2024 8:45 AM

Hydromer Announces Attainment of ISO 13485 Certification • HYDI • Jun 17, 2024 9:22 AM

ECGI Holdings Announces LOI to Acquire Pacific Saddlery to Capitalize on $12.72 Billion Market Potential • ECGI • Jun 13, 2024 9:50 AM

Fifty 1 Labs, Inc. Announces Major Strategic Advancements and Shareholder Updates • CAFI • Jun 13, 2024 8:45 AM