Wednesday, April 15, 2015 3:00:57 PM

Gross profit margin is the percentage of gross profit in relation to total revenue.

Let's look at facts

Below is the annual data for 2014.

Gross profit divided by total revenue gives you 27% of gross margin.

Now, let's try to understand where this money goes. R&D is a small part of it, but mostly it's SG&A (Selling, general expenses, administrative expenses)

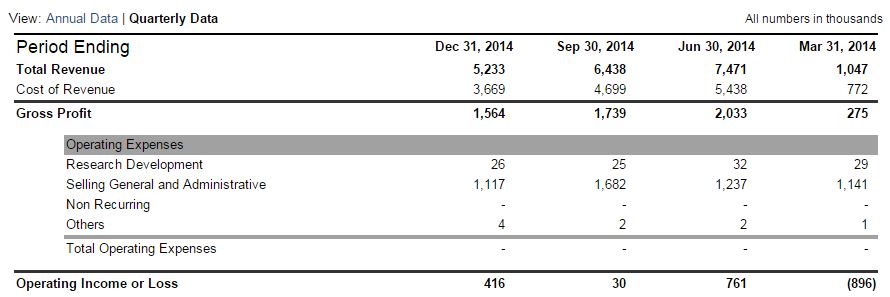

Check out the same 2014 divided by quarters.

Please note two trends as they are of huge importance

TREND 1

Gross margin percentage in Q1 was 26%, Q2 was 27%, Q3 was 27%, Q4 was 29.9% <--- That's even better then I remembered off the top of my head

TREND 2

SG&A expenses are pretty much flat, every quarter at just over a million bucks (SG&A represents non-production cost, like employee salary, fax machine, paper etc.)

Hence, my reasoning regarding operating income (and consequently net income) % growth in a previous post. The company has openly stated in their 10-K that they intend to take advantage of economies of scale in the future.

Add to that consolidation of all paper-work back-end office related activities in one location. Every acquisition will make it cheaper for us to do business as a percentage of total revenue because of the economies of scale.

On another note, someone is openly bashing about Q4 being better than Q1.

Here is another statement found in company's 10-K filing:

Please note, bookings at year end for customers DO NOT necessarily translate in immediate Q4 revenue for the installer

But let's get back to my original thought.

What happens if revenue keeps growing (we just announced several large commercial projects in Q1 in addition to a record-high sales in residential in March alone) and SG&A stays pretty much flat? I'm not saying it's not going to increase, i'm just saying that as revenues grow it (SG&A) will represent a much smaller percentage of total gross margin. Compare Q1 of last year with Q4 of last year. Same SG&A. Huge operating loss in Q1, huge operating income in Q4.

Yes, there may be a slight blip in SG&A expenses in Q1 attributable to NASDAQ listing fees, however, we only uplist once. The outlook is incredible.

Bottom line to me is this is a great investment and temporarily drop it price doesn't represent true value.

Does anyone have any concerns or comments? Please share.

Avant Technologies Equipping AI-Managed Data Center with High Performance Computing Systems • AVAI • May 10, 2024 8:00 AM

VAYK Discloses Strategic Conversation on Potential Acquisition of $4 Million Home Service Business • VAYK • May 9, 2024 9:00 AM

Bantec's Howco Awarded $4.19 Million Dollar U.S. Department of Defense Contract • BANT • May 8, 2024 10:00 AM

Element79 Gold Corp Successfully Closes Maverick Springs Option Agreement • ELEM • May 8, 2024 9:05 AM

Kona Gold Beverages, Inc. Achieves April Revenues Exceeding $586,000 • KGKG • May 8, 2024 8:30 AM

Epazz plans to spin off Galaxy Batteries Inc. • EPAZ • May 8, 2024 7:05 AM