News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Stock Farmer

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Honestly did not expect such a drastic increase in AS/OS, when the company is producing so much revenue. I get the idea that it increases future revenue but does not bode well for the current PPS situation.

Bought some more on the dip, which may not have bottomed yet.

Still a proponent of the company. Looks like it is going to take longer than expected.

Maybe the SPQS shares for the bottling equipment are being sold today on the news. Could be about 375 million shares based on the OS increase in late September. Everyone wants to know when the 700 million shares will hit the market or if they are restricted. Were the SPQS shares restricted?

1 billion shares is a big number for just over 1 month.

I don’t think a profitable company will bear the fruit of an undervalued SP forever, the ball will eventually get rolling; especially an OTC company that actually produces a ball [product], (and a lot of them at that).

Lots of backseat drivers. When you manage a company to $15 million in revenue in just a couple years and to over $30 million the next year then maybe I would listen to your opinions. Who cares? I can sleep comfortably in the backseat knowing Kathryn is at the wheel and wait patiently to reach the mountain top.

“Are we there yet?” LOL

Tweeting CEO with increasing revenue = $, $ $

“Tweeting CEOs = Danger, danger danger” LOL

Been in for over a year. Easy to sit back and wait for SP to follow net income.

Well said. Agree. All about the revenues (net income) and keeping up with the Orders. It would be nice to know the derivative deal with TRX (maybe some of Kate’s preferred shares), but is secondary to the growth and profitability of HIRU. Those details will be easily ironed out.

Probably the best OTC company at this price IMO. Certainly my easiest long hold penny stock I’ve ever had.

Good point. Glad I’ve been here over a year now. Just hope to double or triple my position by next year. Easiest penny stock long hold I’ve ever been in.

Thanks for updating the inbox. It looks good.

My only comment is I’m not sure if the picture of Shaq should be included. He is the ambassador for WTER not HIRU. I do understand that HIRU sells water to WTER. I just don’t want people drawing the wrong conclusion that SHaq is HIRU’s ambassador.

HIRU Catalysts converging. Share cancellation, Walmart and Water Source One deals, Europe deals, Vlade Divac…

Been here over a year quietly holding. Just set it and forget it. It’s not a matter of if it reaches 0.05 or 0.10, it’s a matter of when.

Profit margin is much higher in the bottled water industry. Probably 30%-50% would be my guess.

Definitely need to see a quarterly report with some more meat in it.

Looks reasonable. I Definitely want to plug several valuation methods into excel and compare the numbers.

Definitely no concerns here in the long term.

I calculated it based on an estimated earnings per share that is based on net income. I misspoke when I said net Revenue. Net income is profit.

https://www.fool.com/investing/how-to-invest/stocks/how-to-value-stock/

Generally figure about one cent SP for every million in net Income

This stock is not as reactive to news it seems. I’ve seen stocks go to 10-20 cents just on news with no tangible revenue. Based on income to date, I’m not shocked about HIRUs current SP, but a bit surprised news hasn’t caused some bigger short term runs.

I did a rough SP estimate based on the Current OS and a conservative P/E of 10 below.

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=164588157

Level 2 Very thin.

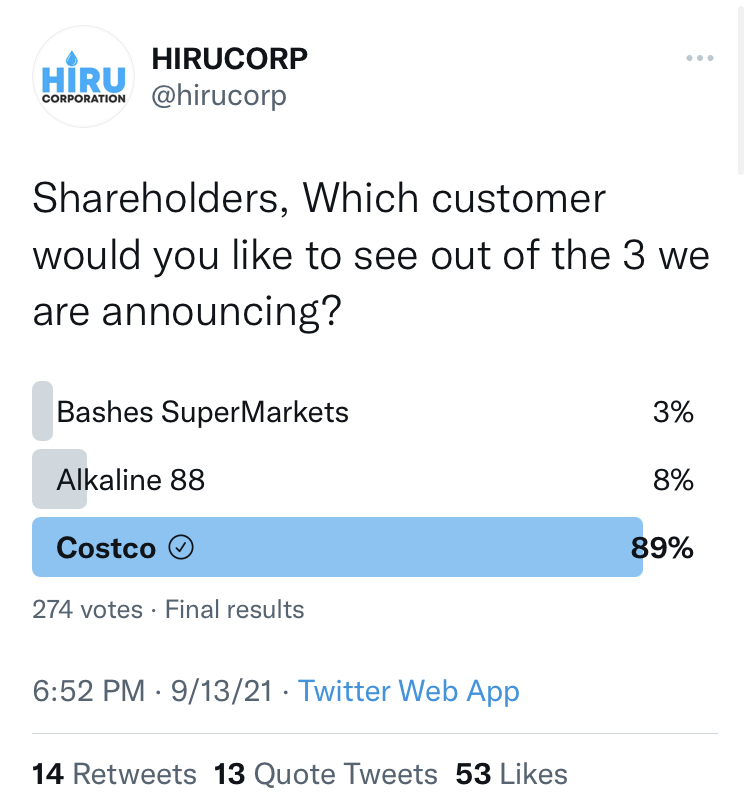

Tweet. $HIRU

Here is the previous tweet of the three customers:

Safest buy in the OTC. Should gain about a cent for every million in revenue.

Patience Pays. 5-25 cents in 2022.

HIRU working and updating late on a Sunday. The company updates shareholders and follows through better than 99% of OTC mergers (yes I made that number up but it seems appropriate). I thought I worked long hours.

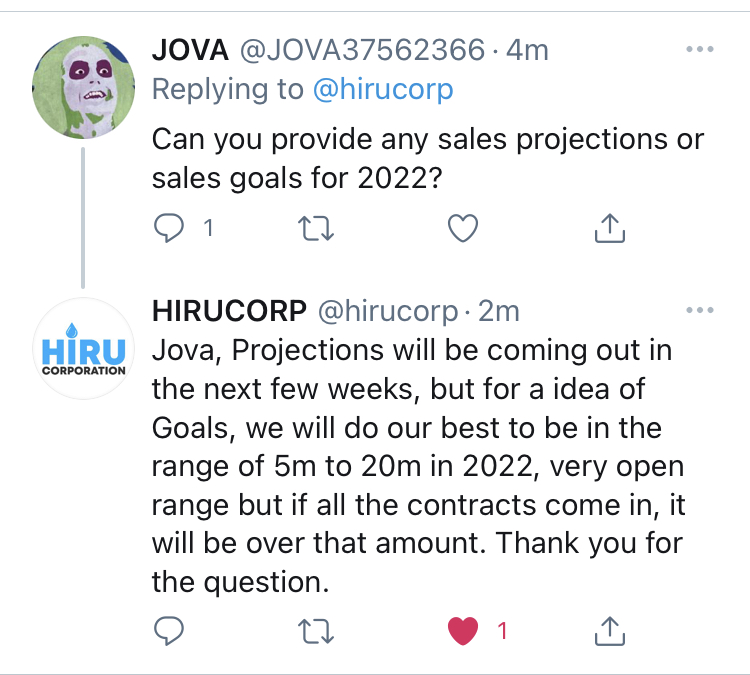

$HIRU Valuation based on Net Income

1,748,182,295 Outstanding Shares

*Assuming ultra conservative P/E of 10

Net Income———— Stock Price

$500,000 ——— 0.003

$1,000,000 ——— 0.006

$10,000,000 ——— 0.06

$20,000,000 ——— 0.12

$50,000,000 ——— 0.30

This is my 2 cents of where the PPS could settle once the flood of FOMO and News Momentum subsides. Short term PPS could go much higher than HIRU’s Net income would suggest.

Remember HIRU is #1 supplier in Arizona for bottled water and ice

Daily ice production capacity of 100 tons!

100 X 2000 = 200000 lbs a day. At a conservative $1 per 10 lb bag

$20,000 per day capacity just for the ice!

All IMO

Sweet! Patience Pays.

Won’t be long now if it is just the one minor correction in the quarterly report. HIRU did not mention any other required changes in their tweet. It seems like turnaround on OTCmarkets is proportional to the extent of the changes. Obviously I don’t know what they have on their plate, and I’m not going to use the overused and OTC cuss word “Soon”.

Good post. Agree. TransUnion Healthcare holding Symposium on Nov 4 for Patient Access in a Pandemic. Not sure if they will have CLXhealth present or not.

![]()

Definitive Agreement as stated in LOI.

https://backend.otcmarkets.com/otcapi/company/financial-report/248195/content

I tend to agree with this interpretation. Typically, there’s a couple things in your analysis I’m not on board with. This time we’re on the same page.

Good explanation BTW.

I consulted the oracle, scanned for chart patterns, read the tea leaves, shook the magic 8 ball and cracked open the fortune cookie.

Everything’s pointing positively north for PASO’s next Pasos.:

The oracle didn’t speak English but I perceived that he was smiling when he spoke, although he wore a Covid mask so I can’t be 100% certain. However, he removed the mask as he shuffled away with his cane which gesture I took as great things will be revealed soon and Travel will be unencumbered by Covid as he APPtly walked away.

Checking the PASO charts turned on the proverbial light bulb for me. It was truly a Tadaa moment. I noticed a cup and handle, Bullish pennants, the head and shoulders knees and toes, and last but certainly not least - a miniature sleigh and 8 tiny reindeer - Brightly signaling an early Christmas for PASO shareholders.

The tea leaves were clear, not literally but figuratively. In reality they were Green. Evidently many Green Days ahead for us Patient shareholders who have Access to cosmic Solutions. No more Boulevard of Broken Dreams. The leaves remained Green even when I turned over a new leaf, leaving a lasting impression on me as I noted my observations down on a leaflet.

The mystic magic 8 ball was short and sweet with its response. It simply and succinctly said “Yes”, not quite apropos since I had asked the mysterious orb how many Partners PASO had joining the global CLX Health consortium. I asked if I’d be a millionaire soon and got a resounding Definite Maybe.

Finally the Fortune Cookie was popped open like a clam to gift a pearl. The winning numbers were revealed 777, which I’ve been able to verify since. Dinner last night was $7.77 (TRU story) foreshadowing a future stock price. I checked CLXHEALTH’s followers only to bolster my beliefs:

Facts or fiction we’ll find in the future.

Chuck Norris’s facts still exist as prominently placed in the stickies. Nothing has changed except PASO’s potentials.

I sit confidently with what I know and don’t fret over what I don’t.

With their new follows, I’m thinking an Airline.

CLX does not “disappear” upon closing of the Reverse Merger. CLX is the surviving company that takes over the public company.

Better Analogy:

PASO is like a home that has a good foundation and walls (Good share structure and RM candidate). It could be move in ready without too much cost, time or effort since there’s no termite damage or mold (no toxic debt). It will be a lot cheaper and quicker than buying a new home in this upscale neighborhood (cheaper than an IPO). It is in a great location (publicly traded). CLX decides its a structure they can work with and buys it (takes majority control with preferred shares). CLX brings in the carpenters, plumbers and painters to finish it as they see fit under their own construction management (New Board of Directors, lawyers, accountants to make sure all is in order). Finally, CLX moves in their furniture so the family can make themselves at home (brings in the business and employees). Lastly, they put the new address in their name and remove the sign on the wall that says “The PASObilities” and put a new sign up saying “CLX Health your TruPass to a HealthyAmerica”, more fitting for the new owners of the home (Name and Ticker change). The Deed is signed and it’s a done deal (DA signed and RM complete).

Let’s close this deal!

CLX following some new entities, 24 now.

__Twitter.png)

Very well done! Thank you for this great executive summary.

Thanks for all the time and effort here as clearly evident by all the factual detail in that informative post. MM.

Are JG and other insiders barred from the Tender Offer? I would think anyone that had common shares would have the option. I’m hopeful JG and other insiders would take the tender offer if they’re still 100% confident.

That could improve the marketability of the stock.

When that many shares hit the OS, price drop is inevitable, the frosting has to be spread thinner.

Tender offer with 6% annual dividend looking more enticing all the time.

PASO Security Details 9-22-2020

Ready for a catalyst here. Not much of a chart follower especially on penny stocks but it looks like we have not bottomed quite yet to me. Sub 3.5 threes look like they’ll be on the menu today and I wish I had the funds to get a big plateful of PASO.

Tru that.

A “D“ is added to the ticker to indicate a Dividend. It should go away in 20 days.

If you own more than 5% of the OS, you’re considered an insider which has to be disclosed as I understand.

I think that also applies if you have non public info, qualifiying him as an insider as well.

Finally, signing a NDA can restrict certain trading activities depending on what is in it.

I agree. That’s why CLXHealth is merging in, making PASO a giant meaty sandwich or juicy hamburger. You need the bread to make the sandwich.

The signed DA and completion of the RM will open the revenue gates for PASO.

You’re right to suggest that it is CLXHEALTH that will bring the real value to the PASO ticker with their handful plus of joint ventures and global partners. The contracts and deals will take over the steering wheel of the Stock Price.

I agree. That’s why CLXHealth is merging in, making PASO a giant meaty sandwich or juicy hamburger. You need the bread to make the sandwich.

The signed DA and completion of the RM will open the revenue gates for PASO.

You’re right to suggest that it is CLXHEALTH that will bring the real value to the PASO ticker with their handful plus of joint ventures and global partners. The contracts and deals will take over the steering wheel of the Stock Price.

Conversion Ratio will be the same for all Series C Convertible Preferred Shares IMO. Doesn’t make sense to have two different Conversion Ratios on the same Series C stock, otherwise I would have expected to see one Series for the dividend shares and one class of preferred stock for the voluntary shares.

It should be 250:1 based on PRs. I don’t understand the 200:1 Conversion Ratio you mentioned but you have a lot more experience on these matters than I do.

Fun starts when the whiny kids go to sleep with their PASOfiers.

My two cents from in earlier post linked below.

Technically I should have called it Conversion “Ratio” not Rate but same idea. At this point for me it is a toss up whether to convert additional shares To preferred shares or just Roll with the freebie (5% dividend) preferred C shares I will get.

At a price of 0.06 it is a wash other than the 6% annual dividend on the preferred shares.

Most likely there will be a holding period For the preferred shares of a year. Not sure though..

I would not throw all my eggs in the PASO preferred basket fwiw.

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=158056038