News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

naturalborninvestor

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Luncis going to get crushed when the 0.2% tax drop passes. Just when trust and stability is starting to return, developers and validators feel to make "explorations" about their own financial renumeration. This proposal is exposing the weakness of a community-driven decision process. Validators have gained so much decision-power from staking that an outcome suboptimal to the majority is the most likely result. It will be hard to regain that market trust for a second time once the "explorations" are revised.

US and China reach landmark audit inspection deal

Agreement gives US regulators access to Chinese accounts in effort to keep listings on New York exchanges

https://www.ft.com/content/a9d18d7e-1e75-49fb-842d-d8554b420553

Facebook ruins it. Dragging down the entire market, including BABA. VIPS just follows Baba's price action.

Forget About Alibaba, Buy Vipshop Instead

Nov. 09, 2021 6:27 AM ETVipshop Holdings Limited (VIPS)BABA, BABAF, JD,PD,TCEHY,TCTZF18

Source:

https://seekingalpha.com/article/4467235-forget-about-alibaba-buy-vipshop-instead

Summary

VIPS has been profitable for 35 quarters in a row.

Due to many strategic advantages, the company is positioned to stay a relevant player in the Chinese e-commerce industry.

The stock is currently trading at multiples that are 60-80% below those of BABA.

Therefore VIPS is a great buying opportunity for value-investors that want to invest in China.

Asian girls with online and packaging products and mobile phones.

VichienPetchmai/iStock via Getty Images

Even within the group of undervalued Chinese stocks, Vipshop Holdings (VIPS) is valued very cheap. Below I will show why it is very likely that VIPS will be able to keep its leading market position as a discount e-commerce platform and that a P/E ratio of below 8 is significantly too low for such a great company. 35 profitable (=positive net income) quarters in a row are proof that the company's business is rock solid.

In order to confidently hold any Chinese stock, it is especially important to really understand the company that you invest in. I believe due to the fact that I have now lived in China for five years and am able to understand Mandarin, I can give a unique and deeper insight into Chinese companies.

Company overview

Business model

VIPS is an online discounter that sells mainly fashion and cosmetics products via its ???APP. The company works together with reputable brands (e.g. right now on their front page I can see Puma, New Era, FILA, etc.) and buys products from them in bulk to sell them for a lower price than competitors are able to.

Vipshop App

Source: Vipshop (???) App

The company organizes "Flash Sales" twice a day, during which it advertises products that are especially cheap for a limited time, giving users a feeling of urgency to buy immediately. While the company's investor relations usually only talk about these flash sales, many users use the app very similar to how they use Taobao (without paying much attention to these flash sales) and save 5-10% compared to the Taobao price. E.g. I have just looked up a branded detergent that my wife (who is Chinese) usually buys on Taobao/T-Mall, and I can see that on the VIPS app it is 8% cheaper. My wife's reaction after showing her: "next time we must use ??? to buy this".

With this simple example, I want to show three things: First, VIPS is able to offer real value to its customers (a good brand for a low price). But second, many users, like my wife, will out of habit mainly use Alibaba's (BABA) or JD.com's (JD) online platforms to purchase products. Just like consumers in the West will automatically go to Amazon when buying things online. This is reflected in the revenues as VIPS has only around 10% of the revenues of BABA and JD. However, VIPS is still a big player in this market and is the third biggest e-commerce platform in terms of revenues. Certainly, this company is highly relevant as almost everybody in China knows this company. And third, while historically the company focused on fashion and cosmetics, nowadays you can buy pretty much anything that you can also buy on Taobao or JD (e.g. phones, furniture, toothpaste, etc.)

VIPS is working with partner companies (it has over 20,000 of them) with whom it co-organizes these sales events. In many cases, the sales events are for products that the partners want to get rid off due to being out of season or just being slow-moving articles. VIPS is also a great way for partners to significantly increase revenues by selling products for a lower price without diluting their higher-margin products on other platforms. Combined with VIPS' deep customer insight, the company, therefore, is also of great value to its partners.

Economic moat

The company has many strategic advantages that it can use to defend its position in the future. Below I will give a short overview of the three most important ones. Also, it should be noted that JD & Tencent (OTCPK:TCEHY) hold 9.3% and 7.3% of the company's shares, which makes it less likely that they will attack VIPS' business as they are benefiting from VIPS' success.

First, the company's brand is well known in China. On the one side, this helps to attract customers without spending too much on marketing, and on the other side, it also helps to convince more brands to enter into a partnership. Moreover, a bigger brand helps to generate trust among the app's users that the products are authentic. There have been a lot of problems with fake products sold via online platforms and therefore there is a big distrust among Chinese users towards pretty much any e-commerce platform. Many Chinese consumers worry that the products that they buy on VIPS' platform might be fake. But also many users worry about that when buying products on Taobao or JD.com. But users certainly have more trust in these bigger platforms compared to newer, smaller platforms.

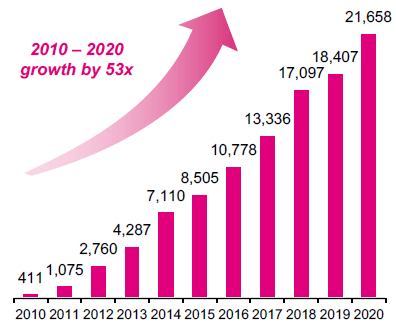

This also brings me to the second point. As mentioned above, VIPS is trying to turn many brands into its partners. Working directly with the brands helps to ensure that the products that are sold on the platform are authentic and therefore will gradually help to increase trust in the platform. Having many brands on the platform also increases revenues as it increases the likelihood that users can find the product they are looking for. For new players, it is difficult to build up such a huge network of partner brands. Below you can see how long it took VIPS to build up its network (the displayed number is the total number of partners):

Vipshop partners

Source: Q2 Investor Presentation

Third, the current market position and the high quantity for each flash sale give the company a lot of bargaining power when negotiating prices with its partner brands. This gives the company the ability to offer lower prices than smaller competitors. The big size and the long history also provide the company with a deep consumer understanding. For flash sale events the importance of that cannot be overstated as the company and its partners risk ending up sitting on piles of unsold inventory if VIPS doesn't know whether the users are interested in a product or if VIPS isn't accurate with its sales forecasting. The app has a lot of historic user data and additionally, users set reminders on the app for certain articles that they want to buy in future flash sales, giving VIPS additional user date.

Financial Performance

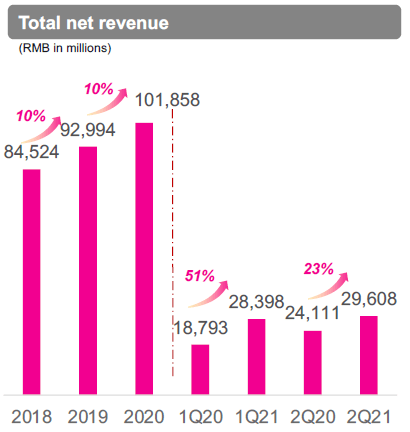

In the past VIPS' revenues have been increasing rapidly every year, but growth has slowed down as the company got larger and larger. In 2019 and 2020, the growth rate was around 10%. In the first half of this year, the company grew by 35% year on year, but that was only due to the very low sales in the first half of 2020, which was heavily impacted by COVID.

Vipshop revenue

Source: Q2 Investor Presentation

In the third quarter, the company expects to go back to a more reasonable growth rate (5-10%). As the Chinese e-commerce market is still growing with double-digit growth rates, it seems very likely that the company will be able to maintain such a 5-10% growth rate for a while. However, I don't expect much higher growth rates than that. In the short term (Q3, Q4), I expect supply chain constraints to hurt VIPS more than other competitors, as its partners will prioritize low-volume high-margin products instead of high-volume low-margin products.

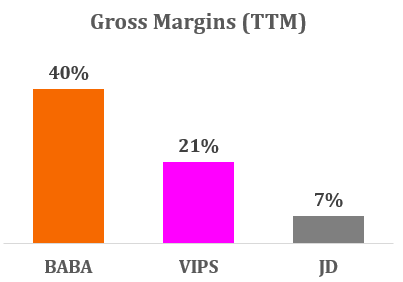

The charm of VIPS is the very stable profit margin. Comparing the gross margin of BABA, VIPS, and JD, we can see that VIPS is obviously not as profitable as BABA, but it still has three times the gross profit margin of JD. This is quite an accomplishment, considering JD has ten times the revenues of VIPS. Certainly, BABA's profit margin is the maximum that any e-commerce platform can achieve, but VIPS 21% gross margin is also not too shabby and is proof that the company's business is more than healthy.

BABA vs VIPS vs JD gross margins

Source: Author of this article

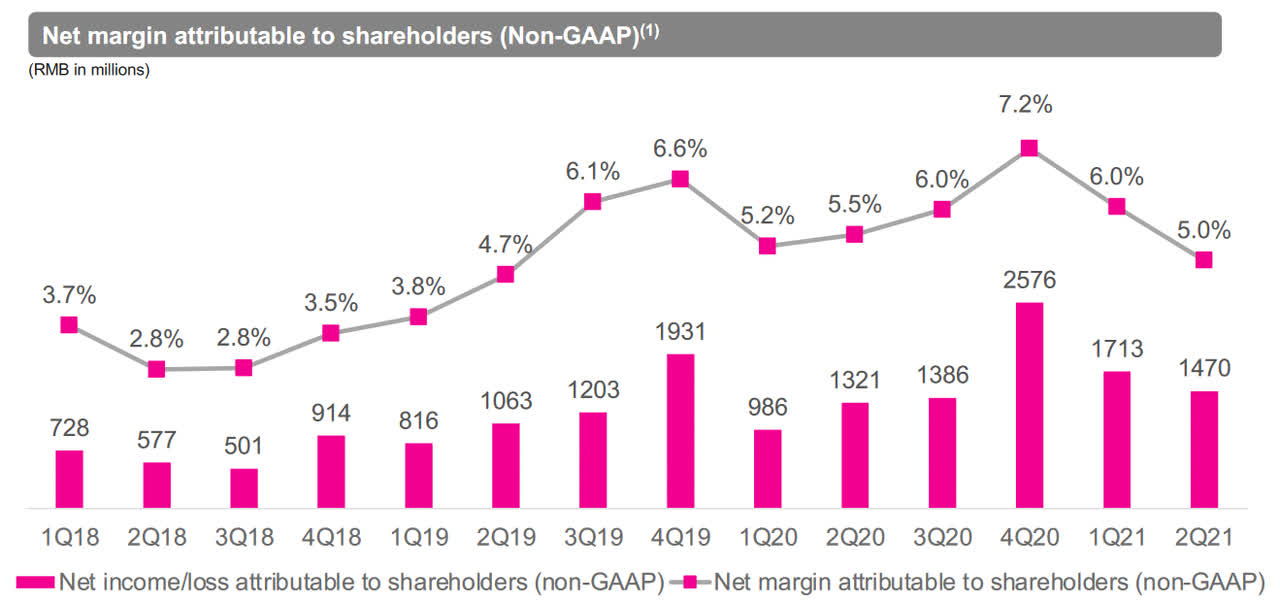

Even more so when looking at the net profit margin. Since the end of 2012, the company was able to post positive net earnings for 35 quarters in a row. So, even though the net margins are very thin, these margins are at least also very stable. Until 2018 the company's net margin was hovering around 3-4%. However, after 2018 the company was able to increase its net margin to 5-6%.

Vipshop net margin

Source: Q2 Investor Presentation

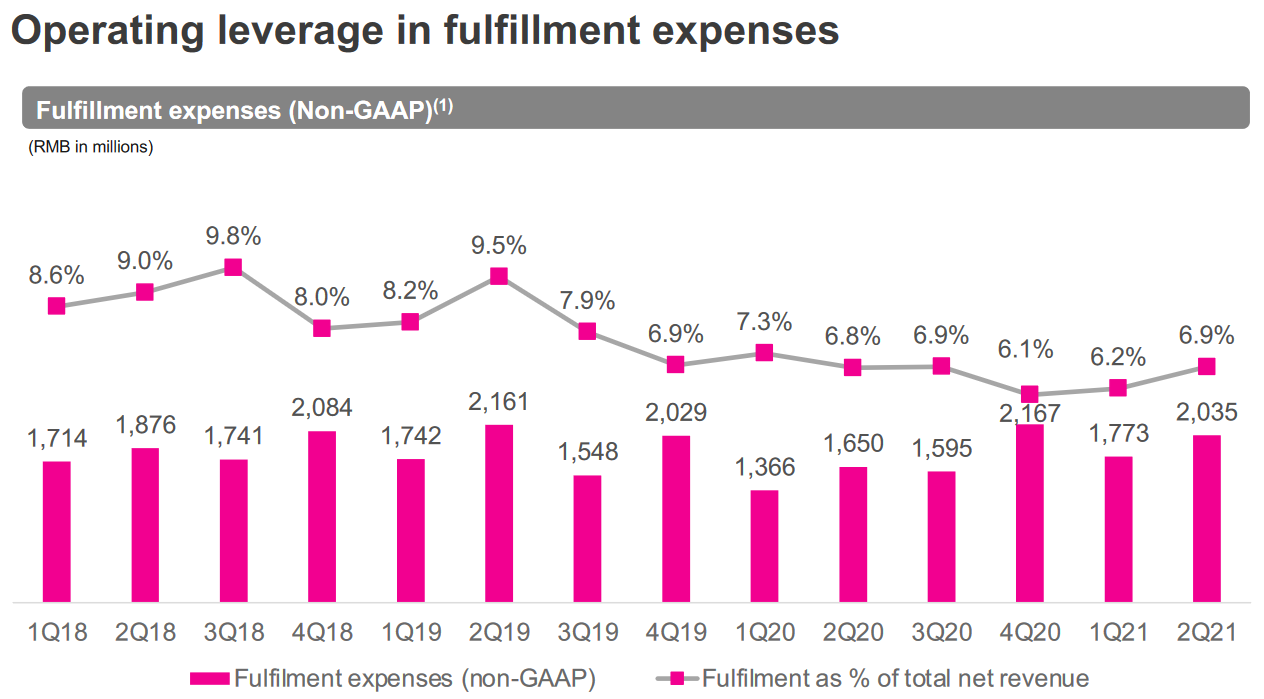

The main reason for the improvement comes from the reduction of logistics costs. In 2019, the company switched its delivery company and has started to work almost exclusively with SF Express. Since then, fulfillment costs have been down significantly:

Vipshop fulfillment expenses

Source: Q2 Investor Presentation

Some bulls will also mention the very high free cash flows of the company, which are significantly higher than the company's net income. However, the truth is that these higher FCFs were only possible through aggressive working capital management, and these higher levels therefore should not be sustainable going forward. I expect FCFs to be in line with the company's net income.

Based on all these numbers above, it should be obvious that the company has gradually growing revenues and a very stable net profit margin. And on top of that, the company uses even a big share of its earnings ($500M in 2021) to buy back its shares.

Valuation

Just like most Chinese companies that I analyze, also VIPS has virtually no debt and a huge pile of cash. The $3B cash, that the company has on its balance sheet, is worth 40% of the total market cap.

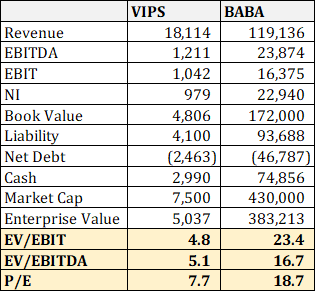

By purely looking at the financials of BABA, most investors agree that the company is undervalued. Below I want to show that VIPS is cheap even compared to the already cheaply valued BABA. Based on the trailing twelve months results, VIPS is trading at multiples that are 60-80% lower than those of BABA:

VIPS vs BABA valuation

Source: Author of this article

Additionally, regulation-related risks are drastically lower for VIPS than for BABA, as the Chinese government focuses mostly on the biggest companies, such as Alibaba, Tencent, and Baidu. Many regulatory changes are actually helping "smaller" companies like VIPS, as they weaken the bigger players.

On the other side, without government intervention, BABA certainly has a much deeper economic moat than VIPS, which is also reflected in BABA's higher margins. Also, BABA has been growing roughly three times faster over the last few years. However, also BABA's growth will eventually slow down as the market matures.

It is difficult to accurately quantify these different risk profiles and future growth rates, but I believe that most value investors are happy to buy VIPS for a 60-80% discount rather than paying the full price to get BABA's growth-rate and economic moat.

Risks

Political risks/VIE risk

Many others have already warned about investing in Chinese ADRs, and you can find one of these very bearish articles here.

As I also mention in my other articles on Chinese stocks, before investing in any Chinese company, investors must first make the decision for themselves whether they think the risk is too big to invest in Chinese companies or not. I suggest to first familiarize yourself with all the differences between investing in a US stock and investing in a Chinese ADR.

From my own research and experience, I came to the conclusion that the risk is overblown. I certainly believe there is an additional risk, but not to such an extent as the market currently prices in. To explain my whole reasoning on this topic would make this article too long but I plan to write a separate article which only discusses this topic in the future. (the summary is pretty much this: 1) China will not just take away investors' stocks as it has more assets in the West than the other way around 2) Delisting in the US is not bad 3) Regulation helps small and middle-sized companies)

Competition

E-commerce certainly is a competitive industry. On the one side even nowadays many new players still try to enter the market and fight for revenues. Due to its explosive growth Pinduoduo (PDD) will likely become the new third-largest player very soon. On the other side, there are much bigger players than VIPS (JD & BABA).

However, in many cases, all these other companies are fighting for different market revenues. New players usually compete with BABA and JD, and not so much with VIPS, as VIPS' flash sale approach is rather unique and puts VIPS in its own "little" niche. Also, VIPS has already proven over the last 35 quarters, that it is able to consistently generate profits despite all the competition. The mentioned economic moat will protect the company's position.

Bottom Line

Not every company needs to become the next Alibaba or Amazon in order to be a profitable investment for its shareholders. VIPS sits very comfortably in the third position behind BABA and JD, and focuses on its own business to generate great returns for its shareholders.

My only worry right now is that due to supply chain constraints, Q3 and Q4 will temporarily hurt the business. I, therefore, give this stock only a "bullish" rating instead of a "very bullish". I will review the situation after Q4 but already hold a small position until then since I believe any possible concern about the company is already more than priced in.

Anyone left here? Starting to look interesting.

Q1 2021 out - making good progress

FIRST QUARTER 2021 FINANCIAL HIGHLIGHTS

During the first quarter we continued strengthening our balance sheet by reducing debt and leverage, while improving liquidity and shareholders' equity. First quarter financial results and highlights included the following:

GAAP book value per share was $4.27 at March 31, 2021, an increase of 1.7% from $4.20 at December 31, 2020.

Economic book value(2) per share of $4.02 at March 31, 2021.

GAAP net income of $8.0 million, or $0.13 per basic and diluted share.

Core earnings(1) of $6.1 million, or $0.10 per basic and diluted share.

Economic return on GAAP book value(3) was 3.1% for the quarter.

2.19% annualized net interest margin (1)(4)(5) on our investment portfolio.

Recourse leverage was 2.0x at March 31, 2021.

On March 23, 2021, we declared a first quarter common dividend of $0.06 per share.

Repurchased $6.7 million in aggregate principal amount of our convertible senior unsecured notes at an average discount of 6.3% to par value.

The company clearly stated that it intends to use the proceeds from the latest offering for corporate uses other than bitcoin mining operations. So, what's the point of predicting it will add another quadrillion rigs!? It would also be money badly spent. The mining business is already valued at an unsustainably high multiple, so better hope they can actually pull out an innovative business model in their legacy security/insurance sector.

Both MFA and TWO reported flat Q1 dividends. Personally, I'd be OK if divs stay at $0.06 this quarter. Did any Reit increase dividends?

I do like REITs as "big board" stocks right now. Heavily in WMC as it trades way under book value, but MFA, MITT, TWO, IVR are all great options that pay regular dividends and benefit from opening up of the economy

Thought that's your job lol

The recovery already happened. Look at tourism (CCL) or airlines (LUV). What's left to recover?

Agree. Should at least pass $10 next week. BTC over $61k now.

Moving again. Took a while to build support and new momentum.

Not a lawsuit. It's a lawyer's job advertisement. They want you to hire them as investigators.

It has "free fall" written all over it now. Below $5 soon.

Watch out for the short squeeze

This is not a Ch.11 nor a Ch.7 and the company is neither bankrupt nor insolvent like the companies that usually have to go this route. So, a comparison to what usually happens in bancruptcy proceedings is totally irrelevant. They have options to raise debt, equity or a combination of both, and if coupled with a re-listing on Nasdaq, investors will be plenty because the underlying fundamentals are intact.

Why do people assume that bonds, if at all, would have to be repurchased at par value from cash? The company would simply issue a new class of bonds and use the proceeds to trade in the old bonds. Issue solved. There should be ample interest, given the company is stronger, bigger and financially healthier today than it was at IPO times.

Great video putting things into perspective

Luckin Coffee sell out or buy the dip

Yep, also see s nice bounce coming. Total over-reaction to a common procedure.

Back in. Love the drama.

Secoo Announces Receipt of Preliminary Non-Binding “Going Private” Proposal

QD owns 28.9% ownership in Secoo Inc.

January 11 2021 - 03:00AM

GlobeNewswire Inc.

Secoo Holding Limited (“Secoo” or the “Company”) (NASDAQ: SECO), ?Asia’s leading online integrated upscale products and services platform, today announced that its board of directors (the “Board”) has received a preliminary non-binding proposal letter, dated January 10, 2021, from Mr. Richard Rixue Li, founder, Chairman of the Board and Chief Executive Officer of the Company, proposing to acquire all of the outstanding class A ordinary shares of the Company, par value US$0.001 per share (the “Class A Shares”), not owned by him or his affiliates for US$3.27 per American depositary share (“ADS,” with every two ADSs representing one Class A Share), or US$6.54 per Class A Share in cash in a going private transaction (the “Proposed Transaction”). The Proposed Transaction, if completed, would result in Secoo becoming a privately-held company, and Secoo’s ADSs would be delisted from the NASDAQ Global Market.

A copy of the proposal letter is attached as Exhibit A to this press release.

The Board has formed a special committee consisting of independent directors Messrs. Jun Wang and Jian Wang to evaluate and consider the Proposed Transaction.

The Board cautions the Company’s shareholders and others considering trading in its securities that the Board just received the non-binding proposal letter and no decisions have been made with respect to the Company’s response to the Proposed Transaction. There can be no assurance that any definitive offer will be made, that any agreement will be entered into or that this or any other transaction will be approved or consummated. The Company does not undertake any obligation to provide any updates with respect to this or any other transaction, except as required by applicable law.

About Secoo Holding Limited

Secoo Holding Limited (“Secoo”) is Asia’s leading online integrated upscale products and services platform. Secoo provides customers a wide selection of authentic upscale products and lifestyle services on the Company’s integrated online and offline shopping platform which consists of the Secoo.com website, mobile applications and offline experience centers, offering over 400,000 SKUs, covering over 3,800 global and domestic brands. Supported by the Company’s proprietary database of upscale products, authentication procedures and brand cooperation, Secoo is able to ensure the authenticity and quality of every product offered on its platform.

For more information, please visit http://ir.secoo.com.

I'm here for multi bags. $6.8 book value!

Q3 2020 Earnings Call Transcript

https://www.nasdaq.com/articles/qudian-inc.-qd-q3-2020-earnings-call-transcript-2020-12-14

Qudian Inc. Reports Third Quarter 2020 Unaudited Financial Results

https://ih.advfn.com/stock-market/NYSE/qudian-QD/stock-news/83891781/qudian-inc-reports-third-quarter-2020-unaudited-f

Only 130 board marks? Is ihub dead?

$10 in 2020, $20 in 2021. Looks like SEC gave the green light to Nasdaq reinstatenent

Going with SONN weekly pincher into next week. That little bounce end of October wasn't it, yet.

http://schrts.co/ZkMWUuyn

Chart looks so ready to run eom

Liking how this trades in a weak market. Think we see another spike soon.

SONN weekly may be more imminent

http://schrts.co/WPwYTEpk

JFU weekly looking great for another bounce

http://schrts.co/zhjxutwU

Must come back down to $3.50 range to be a good trade opportunity again

Turned out to be a pretty nice trade. Cup & handle pattern, so short on the the handle for now.

Getting some attention again. I think we have a confirmed bottom.

There is more action for QD on the Stocktwits board (in case anyone wonders).

https://stocktwits.com/symbol/QD

JFU moving. Pincher hasn't even opened yet.

JFU another weekly pincher to put on watch. Still speculative, though. Got a first entry filled.

http://schrts.co/GAbGMHrn

LKNCY weekly looks pretty awesome now

They are recycling the previous sales PR, right? The $5M reported a few days ago is included in this 3-month aggregate $7.2M figure. Sneaky. I guess just an opportunity to issue some more shares