News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

>>> Copart (CPRT) -- Speaking of old cars, Copart (NASDAQ:CPRT) also stands to benefit from the trend of aging automobiles. The company runs an online auction and remarketing service for used and salvaged vehicles. By all accounts, business is booming. Copart has reported fiscal Q3 financial results that beat the consensus forecasts of Wall Street analysts. The company announced EPS of 39 cents, narrowly beating estimates of 38 cents. Revenue in the quarter totaled $1.13 billion, slightly ahead of analyst estimates of $1.11 billion. Overall sales were up 10% from a year earlier.

https://finance.yahoo.com/news/3-transportation-stocks-buy-now-164311348.html

Each business segment at Copart saw growth in the quarter, with U.S. insurance volumes rising 6.8% year-over-year (YOY), non-insurance business increasing 23% and dealer sales volumes gaining 18%. The company reported having $4.3 billion of cash on hand as of March 31. On an earnings call, management singled out elevated prices for new vehicles as a tailwind for their business.

CPRT stock is up 14% this year and has risen 205% over the last five years.

<<<

---

>>> Tesla to unveil robotaxi self-driving car in August, Elon Musk says

by Anthony Robledo

USA TODAY

4-5-24

https://www.msn.com/en-us/autos/news/tesla-to-unveil-robotaxi-self-driving-car-in-august-elon-musk-says/ar-BB1l9DpE?OCID=ansmsnnews11

Elon Musk announced that Tesla will unveil its robotaxi this summer.

The X owner and Tesla CEO unveiled the Aug. 8 release date on a post Friday.

The entrepreneur has previously discussed efforts to create Tesla cars without human controls and for existing vehicles to gradually improve its Full Self-Driving Capability, which are not fully autonomous.

The technological feat has been a longtime goal for Musk, who has said autonomous taxis could revolutionize modern transportation by becoming more popular than human-driven cars and that automaker would be "worth basically zero."

Musk wanted to release robotaxis in 2020

In April 2019, Musk revealed that he expected Tesla robotaxis to be fully operating by 2020.

The company predicted that driverless vehicles would withstand 11 years and 1 million miles, earning the company $30,000 in annual profit. He also shared that the cars would would be accompanied by a ride-share app similar to both Uber and Airbnb.

U.S. and Chinese regulators have currently only approved self-driving cars in limited and experimental instances on public roads.

The automotive company faces lawsuits and investigations related to crashes with its existing autopilot and Full Self-Driving driver-assistance systems, which the company has Tesla has explained were the result of inattentive drivers.

Tesla shares down after low-cost EV plans are scrapped

Musk's announcement comes after a Reuters report revealed that Tesla has scrapped plans for its long-promised inexpensive car, according to three sources familiar with the matter and company messages.

Investors have been relying on the project to drive its growth into a mass-market automaker, according to Reuters.

Musk has often described affordable electric cars for the masses as a primary mission. In 2006, he said his "master plan" had to prioritize manufacturing luxury models before financing a "low cost family car."

Tesla shares closed down $6.21, or 3.63%, at $164.90 on Friday.

<<<

---

>>> Tesla, Inc. (NASDAQ:TSLA) -- 14-day RSI: 31.26

https://www.insidermonkey.com/blog/5-oversold-blue-chip-stocks-to-buy-right-now-1274453/2/

Number of Hedge Fund Holders: 82

Based in Austin, Texas, Tesla, Inc. (NASDAQ:TSLA), designs, develops, manufactures, sell and leases fully electric vehicles and energy generation and storage solutions. Its current portfolio of products includes Model 3 and Model S sedans, Model Y, Model X SUVs, and Cybertruck, while upcoming products include Tesla Roadster and Tesla Semi – a light commercial vehicle.

On January 24, Tesla, Inc. (NASDAQ:TSLA) released its financial results for Q4 2023. Its revenue increased by 3% y-o-y to $24.3 billion, while net income surged by 115% y-o-y to $3.7 billion. Its normalized EPS of $0.71 missed consensus estimates by $0.03.

Tesla, Inc. (NASDAQ:TSLA) ranks highest on our list of 11 oversold blue chip stocks to buy right now based on the value of shares held by hedge funds. As of Q4 2023, 82 hedge funds owned shares worth $6.3 billion. In its Q4 2023 investor letter, Tsai Capital Corporation, an investment management firm, made the following comments about Tesla, Inc. (NASDAQ:TSLA):

“Tesla has significant and underappreciated competitive advantages across multiple verticals including electric vehicles, software and energy storage. Misunderstood by much of Wall Street – and consequently a favorite of short sellers – Tesla continues to grow rapidly and increase its lead over the competition while delighting consumers in the process. [. . .] While we expect competition for EVs to intensify and for Tesla to lose market share over time, we also believe the company will increase production and deliveries from approximately 1.8 million vehicles today to approximately 15 million vehicles in 2030 and further its lead in autonomous driving capability. In fact, we expect Tesla will eventually license its autonomous driving software, creating high-margin (70-80%), recurring licensing revenue. Tesla is also one of only two companies that dominate the energy storage market, which has the potential to grow to several hundred billion in revenue as power plants around the world increase their focus on renewable energy.”

<<<

---

>>> Saia sees 19% jump in February shipments

Freight Waves

by Todd Maiden

March 4, 2024

https://finance.yahoo.com/news/saia-sees-19-jump-february-224344083.html

Less-than-truckload carrier Saia Inc. reported an 11% year-over-year (y/y) increase in tonnage per day during February. The increase was the combination of a 19% jump in shipments, which was partially offset by a 6.7% decline in weight per shipment.

The y/y per-day growth rates accelerated from January, when the carrier’s shipments increased 11.8% and tonnage was up 3.3%. Inclement weather in January led to a larger-than-normal number of terminal closures during the month. Saia (NASDAQ: SAIA) also had an easier tonnage comp in February (down 7.6% last year), which was twice the decline that was logged in January 2023.

The February increases were a little better than the fourth quarter, when shipments were up 18% y/y and tonnage increased 8%.

March is a big month for LTL carriers and volumes in the period will dictate results for the first quarter. The month also provides a strong indication on demand for the full year.

Saia doesn’t provide any revenue-based metrics like yields or revenue per shipment in its intraquarter updates, however, management said on its fourth-quarter call in February that it expects revenue per shipment to increase by a low-single-digit percentage in 2024.

The company is executing a big growth plan this year. A $1 billion capital expenditures outlay includes roughly $550 million for real estate. The budget includes the 28 terminals it recently acquired from bankrupt Yellow Corp. (OTC: YELLQ) as well as other additions and expansions. In total, it expects to grow its net door count by 12% to 14% this year.

The bulk of the remaining budget will be used to purchase tractors and trailers.

Other carriers like ArcBest (NASDAQ: ARCB), Old Dominion (NASDAQ: ODFL) and XPO (NYSE: XPO) are expected to provide updates for February in the coming days.

<<<

---

>>> Murphy USA Inc. (MUSA) engages in marketing of retail motor fuel products and convenience merchandise. The company operates retail stores under the Murphy USA, Murphy Express, and QuickChek brands. It operates retail gasoline stores principally in the Southeast, Southwest, and Midwest United States. The company was founded in 1996 and is headquartered in El Dorado, Arkansas.

<<<

https://finance.yahoo.com/quote/MUSA/profile?p=MUSA

---

>>> Old Dominion Freight Line, Inc. (NASDAQ:ODFL)

https://finance.yahoo.com/news/13-best-performing-p-500-170755396.html

Year Share Price Gains: 337%

Old Dominion Freight Line, Inc. (NASDAQ:ODFL), as the name suggests, is a freight and shipping company. This leaves it vulnerable to both high fuel prices and slow economic output, both of which are the predominant features of today's investment climate.

During Q2 2023, 25 out of the 910 hedge funds surveyed by Insider Monkey had bought and owned Old Dominion Freight Line, Inc. (NASDAQ:ODFL)'s shares. Cliff Asness' AQR Capital Management is the largest shareholder out of these, owning 162,745 shares that are worth $60 million.

<<<

---

>>> Old Dominion Freight Line -- Less-than-truckload (LTL) specialist Old Dominion Freight Line makes up for its small 0.3% yield with a blistering 35% annualized dividend growth rate over the last five years and a minuscule 12% payout ratio.

https://www.fool.com/investing/2023/09/07/4-top-dividend-payers-of-the-sp-500/?source=eptyholnk0000202&utm_source=yahoo-host&utm_medium=feed&utm_campaign=article

Despite being the second-largest LTL shipper in the U.S., it is the most efficient operator in its industry, with an ROIC of 34% and a net profit margin of 21%.

However, in its most recent quarter, revenue and EPS dropped a nerve-racking 15% and 20% amid softness in the U.S. trucking industry as it continued to rightsize from a pandemic-aided boom. Still, management believes it maintained its 12% market share in the quarter, highlighting that it is not a company-specific slowdown.

Furthermore, the third-largest LTL shipper, Yellow, recently filed for Chapter 11 bankruptcy protection, which could boost Old Dominion as it picks up incremental sales growth from its beleaguered peer. However, after posting total returns of over 1,400% over the last decade, the company trades at a lofty 38 times earnings -- making this another dividend-grower to consider dollar-cost averaging into over time.

<<<

---

Re-post from Dew's board - >>> Container Shipping Has Cratered, as Ship Owners Try to Avoid Unprofitable Trips

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=171998444

A slowdown in orders from big importers bring prices to ‘unsustainable’ levels ahead of ocean shipping’s busiest season

https://www.wsj.com/articles/ocean-freight-rates-slump-as-demand-for-apparel-and-electronics-weakens-460d0a0c

https://lgi.laufer.com/news/container-shipping-has-cratered-as-ship-owners-try-to-avoid-unprofitable-trips/

Date: Tuesday, May 23, 2023

Source: Wall Street Journal

Boxship owners are losing money on once-lucrative trans-Pacific routes from Asia as weaker demand for apparel, furniture and electronics cuts into ocean carriers’ earnings.

It is an ominous sign as the shipping industry approaches its peak season. Demand normally rises during the summer and early autumn as retailers bring in higher levels of merchandise for crucial selling periods, such as the year-end holidays.

Ship operators including A.P. Moller-Maersk and Hapag-Lloyd say they need freight rates to increase to cover their operating costs. For now, there are too many ships in the water bidding for cargo, resulting in heavy competition on prices.

Average daily freight rates from Asia to the U.S. West Coast across the Pacific are at roughly $1,500 per 40-foot container, compared with more than $14,000 a year ago, according to the Freightos Baltic Index. The cost to send a box from Asia to Europe is at roughly $1,400, compared with nearly $11,000.

The rates for both trade lanes are hovering around 2019 levels, but fuel and labor expenses are higher now than before the pandemic.

“Spot rates are at a level that in the long run are not sustainable, with costs up by 25% to 30% since 2019,” Rolf Habben Jansen, chief executive of Hapag-Lloyd, said on the German box-ship company’s earnings call earlier this month. In some cases, certain voyages don’t make sense “because you simply lose too much money,” he said.

Box-ship operators were among the biggest pandemic winners. Orders for imported goods began to climb in 2020 as consumer spending surged on demand for products as diverse as electronics and chairs. Supply-chain delays made slots on ships harder to get, helping push freight rates up to about $20,000 a box on some routes.

Several companies posted record profits, largely because of higher prices and elevated demand. Demand began to taper last year as orders to move cargo dried up, prompting carriers to cancel sailings along some of the world’s busiest trade routes.

Pricing power for ship operators has diminished, but some publicly listed operators still produced hefty early-year profits. A recovery in prices during the peak season is doubtful, said Peter Sand, chief analyst at shipping-data provider Xeneta. “The shippers are in the driving seat to set freight rates,” he said.

Shipping companies now face the same uncertainty that surrounds some of their biggest customers, such as Amazon.com, Walmart and Home Depot. A number of retailers have said in recent weeks that they remain cautious about the financial health of consumers, but also pointed to progress in reducing bloated inventories. Target, the Minneapolis-based retail chain, said Wednesday that shoppers are pulling back on discretionary purchases and shifting spending to essentials such as food and household goods.

Cargo volumes into the U.S. slumped this year amid the broad decline in orders from retailers and manufacturers. The nation’s busiest container-port complex, at Los Angeles and Long Beach, Calif., handled the equivalent of about 1.74 million import containers in the first quarter of 2023, a 32% decline from last year’s record volumes.

Etc.

<<<

---

Ferrari - >>> If you only buy one auto stock, it should be luxury supercar maker Ferrari for three simple reasons.

https://www.fool.com/investing/2023/04/18/why-ferrari-hermes-and-coca-cola-are-no-brainer-bu/

First, its core customers are so affluent that they're largely resistant to inflation, rising rates, and other macro headwinds.

Second, it's not struggling with supply chain issues like many other automakers because it only produces a few thousand vehicles every year.

Lastly, Ferrari's pricing power enables it to consistently sell its vehicles at much higher gross margins than lower-end automakers do. That elasticity also allows it to comfortably raise its prices to offset any higher supply chain and production costs.

Between 2017 and 2022, Ferrari's annual shipments rose from 8,398 to 13,211 vehicles as its revenue grew at a compound annual growth rate (CAGR) of 8%. Its adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) margin expanded from 30.3% to 34.8%, and its adjusted EPS grew at a CAGR of 13%.

Analysts expect Ferrari's revenue and adjusted EPS to grow 15% and 22%, respectively, in 2023. A major catalyst this year will be the recent launch of its all-electric Purosangue SUV, which already has a backlog of orders for at least the next two years.

Ferrari's stock isn't cheap at 41 times forward earnings, but its stable growth, resilience during economic downturns, high margins, and growth potential in the booming luxury EV market all justify that premium valuation.

<<<

---

Genuine Parts - >>> What Has Been 'Genuinely' Reliable Since President Truman In 1948?

Investor's Business Daily

by MATTHEW GALGANI

03/01/2023

https://www.investors.com/research/breakout-stocks-technical-analysis/auto-parts-retailer-genuine-parts-posts-continuous-dividend-payouts-as-gpc-stock-azo-orly-test-drive-new-buy-zones/?src=A00220

A lot has changed since 1948 when Harry Truman was President and Ford (F) unveiled the '49 Ford, its new car of year. But one thing hasn't. Since going public in 1948, Genuine Parts (GPC) has paid a cash dividend every year. And 2023 marks the auto parts retailer's 67th consecutive year of increased dividends paid to shareholders.

Fast forward to today and GPC stock joins peers O'Reilly Automotive (ORLY) and AutoZone (AZO) in the driver's seat on the lookout for a new breakout. Genuine Parts also earns placement on the IBD Breakout Stocks Index, which gets updated weekly.

With a 91 Composite Rating, GPC stock trails just behind O'Reilly's score of 93. AutoZone, which just posted a surprise earnings gain but then skidded lower, holds an 81 Composite Rating. Fellow auto parts leader Advance Auto Parts (AAP) also initially popped on earnings but retreated below its 50-day line. It lags the others with a 41 rating.

Napa Brand Drives Steady Growth For Genuine Parts

Founded in 1928, Genuine Parts is global in scope, divided into two major divisions:

Automotive Parts Group, comprising about 66% of net sales, distributes replacement parts in the U.S., Canada, Mexico, Australasia, France, the United Kingdom, Ireland, Germany, Poland, the Netherlands, Belgium, Spain and Portugal.

Industrial Parts Group, comprising about one-third of net sales, distributes industrial replacement parts in the U.S., Canada, Mexico and Australasia.

In North America, the company primarily sells auto parts under the Napa brand. In Europe, Genuine Parts sells Napa products under a variety of banners, such as GROUPAUTO France and GROUPAUTO UK.

Worldwide, Genuine Parts has roughly 58,000 employees with a network of over 10,000 locations in 17 countries.

On Feb. 23, the company reported Q4 and full-year 2022 numbers. Both earnings growth and sales growth came in at 15% in the fourth quarter. EPS rose to $2.05 while Q4 revenue exceeded $5.5 billion.

Over the last three years, Genuine Parts has posted average annual sales growth of 9% and average EPS gains of 22%. The company earns an A SMR Rating, which tracks sales growth, profit margins and return on equity.

Building on its impressive streak of dividend payments, the auto parts leader's current yield is 2.00% on an annualized basis.

Genuine Parts Vs. Auto Parts Peers ORLY, AZO and AAP

While Genuine Parts and its peers did not make the latest list of new buys by the best mutual funds, institutional investors have shown signs of demand for GPC stock.

Genuine Parts has posted three quarters of rising fund ownership, That outpaces one quarter for O'Reilly and Advance Auto Parts, and zero for AutoZone.

Plus, 70 funds with an A or A+ rating from IBD own shares of GPC stock.

Over the last year, Genuine Parts showed a 13% increase in the number of funds with a position in GPC stock, topping that of its auto parts competitors.

In terms of market capitalization, O'Reilly Automotive and AutoZone clearly surpass the others. But at $21 billion, Genuine Parts qualifies as leading large cap.

Genuine Parts continues to work on an early stage cup with handle. The buy point is 180.85.

The relative strength line retreated as GPC stock formed its base, but has come off its recent lows. Look for the RS line to get closer to a 52-week high as the buy point nears.

Within the cup with handle, GPC stock has flashed several days of above-average volume, pointing to demand among large investors. Genuine Parts currently trades 2% shy of the buy point.

Showing that stocks tend to move in groups, ORLY and AZO stock retreated Tuesday, as did Genuine Parts. All three auto parts retailers are testing buy points and buy zones, but face tests as the market indexes look to find support.

<<<

---

Copart - >>> Copart earns incredible profits. The company's operating margin in the first half of its fiscal 2023 was almost 37% -- extremely high. However, despite plenty of cash, management has never paid a dividend in its nearly 30 years as a public company, and it hasn't repurchased any shares since 2019. This is because it believes it can put its cash to better use.

https://www.fool.com/investing/2023/02/23/2-recession-proof-growth-stocks-im-loving-now/?source=eptyholnk0000202&utm_source=yahoo-host&utm_medium=feed&utm_campaign=article

During its fiscal 2022, which ended in July 2022, Copart acquired around 1,200 new acres of land for storing vehicles for its auctions. According to management, the company owns more than 90% of its 16,000 acres, allowing it to execute its plans without taking a third-party landlord into consideration.

Adding new vehicle yards and expanding existing ones helps Copart increase its competitive advantage in the resilient vehicle-auction space. The company's primary customers are insurance companies looking to get rid of loads of damaged vehicles at maximum prices. By having more than 200 locations, and still growing, Copart can handle their heavy volumes. And it has a large base of buyers, pushing bids higher to the satisfaction of insurance companies.

Vehicles can be damaged in accidents or during natural disasters, and these unfortunate events don't take time off during recessions. This isn't to say that Copart's financial results are completely unaffected by macro-economic conditions -- results right now are being affected by abnormally high used car prices. However, this industry always has demand, and Copart is one of the biggest players in the space.

A sensible choice

I don't know when a recession will strike next. But they're regular economic occurrences. That's why having some more recession-proof stocks like Tractor Supply and Copart in your portfolio could make a lot of sense.

However, if I had to pick just one to buy today, I'd choose Tractor Supply over Copart. Trading at around 30 times its earnings, Copart trades at a more expensive valuation than its 10-year average, as the chart below shows. By contrast, Tractor Supply trades in line with its average.

Chart showing Tractor Supply's PE ratio lower than Copart's since 2018.

This suggests that Copart might be a little overvalued right now, and I don't think I'm alone in that belief. Copart's management seems to agree. Consider that management is authorized to repurchase over 81 million shares whenever it sees fit. But it hasn't done so in over three years.

Therefore, for the more value-conscious investor, I'd wait with Copart's management on the sidelines for a better price, whereas Tractor Supply stock appears to already be trading at a fair price today.

<<<

---

>>> Auto parts firm LKQ to buy Uni-Select in $2.1 billion deal

Reuters

2-272-23

https://www.msn.com/en-us/money/topstories/auto-parts-firm-lkq-to-buy-uni-select-in-2-1-billion-deal/ar-AA180048?OCID=ansmsnnews11

(Reuters) -LKQ Corp said on Monday it would buy Uni-Select Inc in an all-cash deal valued at about C$2.8 billion ($2.06 billion), looking to tap into the Canadian company's strong presence in the aftermarket auto parts business.

The deal comes as rising interest rates force customers to hold on to their vehicles for longer, spurring demand for repairs and other services.

In Canada, Uni-Select deals with over 1,000 customers and supports over 16,000 automotive repair and collision repair shops.

Uni-Select's shareholders will receive C$48 per share, a premium of 19.2% to the stock's close on Friday.

The equity value of the transaction is C$2.11 billion, based on calculations by Reuters.

Boucherville, Quebec-based Uni-Select distributes automotive refinish and industrial coatings and related products in North America, while LKQ sells OEM recycled and aftermarket parts, replacement systems among others.

"While it has been years since LKQ completed platform M&A, we do think this deal makes strategic sense," Stephens analyst Daniel Imbro said.

LKQ intends to fund the transaction through a combination of cash on hand and new debt and has secured bridge financing commitments from Bank of America and Wells Fargo.

<<<

---

AutoZone, Inc - 10 recession stocks -

https://finance.yahoo.com/news/10-companies-industries-money-during-165619500.html

Industry: Automotive Retail

S&P 500 Outperformance in 2008: 27.12%

AutoZone, Inc. (NYSE:AZO) is a retailer and distributor of automotive replacement parts and accessories. The company is based in Memphis, Tennessee.

On December 7, David Bellinger at MKM Partners reiterated a Buy rating on AutoZone, Inc. (NYSE:AZO) shares while raising his price target to $2,650.

Vehicle part retailers like AutoZone, Inc. (NYSE:AZO) tend to perform well in a weak economy, as more people choose to repair their cars instead of buying new ones. This was proven by the returns generated by the company between October 9, 2007, and March 9, 2009, which stood at 22%. The company also grew its sales by 5.7% in 2008.

Carillon Tower Advisers, an investment management company, mentioned AutoZone, Inc. (NYSE:AZO) in its second-quarter 2022 investor letter. Here’s what the firm said:

“AutoZone, Inc. (NYSE:AZO) sells automotive replacement parts and accessories. The company reported another solid quarterly update that highlighted particularly robust growth in its commercial segment, market share gains, and stable gross margins. Additionally, investors have appreciated the company’s historically stable business model that is positioned to perform well in periods of economic stress.”

<<<

---

>>> High ROIC Stock #1: AutoZone Inc. (AZO) - Return on invested capital: 180.5%

https://www.suredividend.com/high-roic-stocks/

After opening its first store on July 4th, 1979, AutoZone has grown into the leading retailer and distributor of automotive replacement parts and accessories, with more than 6,000 stores in the U.S., Puerto Rico, Mexico, and Brazil. AutoZone carries new and re-manufactured parts, maintenance items, and accessories for cars, SUVs, vans, and light trucks.

AutoZone has proven to be recession–resistant thanks to the nature of its business. During rough economic periods, the sales of new cars fall significantly, causing the average age of cars to increase. This favors AutoZone’s business. In the Great Recession, when most companies saw their earnings plunge, AutoZone grew its EPS by 18% in 2008 and another 17% in 2009.

<<<

---

Old Dominion - >>> 3 Top Trucking Stocks Under Heavy Accumulation

FX Empire

by Lucas Downey

February 6, 2023

https://finance.yahoo.com/news/3-top-trucking-stocks-under-130904222.html

Here are three companies under heavy accumulation.

Old Dominion Freight Line Inc. (ODFL) Analysis

First is the less-than-truckload hauler Old Dominion Freight Line (ODFL). The trucking stock is up 30% in 2023.

Healthy institutional accumulation has likely helped lift the shares higher, which you can see via the MAPsignals chart below. Since November there’ve been 6 unusually large volume inflows (green bars):

With a 12-month forward P/E of 30.8, shares could be attractive after a pullback. According to FactSet, the company is estimated to earn $13.30 per share in fiscal year 2024.

One thing is for sure, the shares have been in demand lately.

Knight-Swift Transportation Holdings Inc. (KNX) Analysis

Next up is Knight-Swift Transportation (KNX) which is another trucking company that operates in 3 segments: trucking, logistics, and intermodal. At MAPsignals, we believe in following large institutional flows. With the stock gaining 18% in 2023, we believe healthy accumulation is part of the story.

Since late November there’ve been 8 days where the stock jumped in price alongside outsized volumes. That can mean there’s institutional interest:

The 12-month forward P/E is pegged at 15.2X according to FactSet. Also, the company is expected to earn $4.64 per share in fiscal year 2024.

This unusual trading action suggests investors are expecting upside for the company in 2023.

Schneider National Inc. (SNDR) Analysis

The number 3 trucking firm racing higher this year is Schneider National (SNDR). This company provides transportation and logistics services. The market cap is just over $5.2 billion.

The stock has been an outperformer recently, jumping 26% in 2023. Notably, the shares have seen 4 large accumulation signals since November:

There’s no question the stock could be extended at these levels. However, this is one of the most in-demand trucking stocks according to MAPsignals research.

Strong sector leadership could mean there’s more upside for the group in 2023.

Bottom Line

ODFL, KNX, & SNDR represent 3 of the top trucking stocks so far in 2023. Healthy institutional accumulation signals make these stocks worthy of extra attention.

<<<

---

Old Dominion Freight Line - Boasting a total return north of 1,200% over the last decade, less-than-truckload (LTL) hauling specialist Old Dominion Freight Line has smashed the market.

https://www.fool.com/investing/2023/01/28/4-stocks-with-high-dividend-growth-to-buy-in-2023/?source=eptyholnk0000202&utm_source=yahoo-host&utm_medium=feed&utm_campaign=article

Almost exactly as it sounds, LTL hauling consists of picking up partial loads from multiple locations and delivering them to one or many drop-offs. While far more complicated than traditional truckload hauling, this complexity acts like a moat for Old Dominion. With nearly 11,000 tractors, 43,000 trailers, 24,000 employees, 255 service centers, and linehaul dispatchers and software needed to coordinate everything, successful new entrants to the industry are rare.

Equally as important for investors, Old Dominion's operations are best in class. Consider its profit margin and return on invested capital (ROIC) -- a measure of a company's profitability from its debt and equity -- compared to its LTL peers.

Thanks to this outsized profitability, Old Dominion decided to initiate a dividend in 2017 and has raised it by 284% in the years since. Though the company's dividend yield of 0.4% may seem diminutive, it only amounts to 9% of its net income -- leaving an incredible runway for future increases.

To top everything off, Old Dominion's price-to-earnings (P/E) ratio of 27 is well below the 40 level it often saw in 2022. Posting 43% earnings per share (EPS) growth through the first three quarters of 2022, Old Dominion looks more enticing than ever.

<<<

---

>>> Southwest Airlines reinstates dividend, sees strong travel demand

Reuters

December 7, 2022

https://news.yahoo.com/southwest-airlines-reinstates-quarterly-dividend-115829890.html

(Reuters) -Southwest Airlines Co on Wednesday became the first major U.S. airline to reinstate its quarterly dividend, more than two years after suspending it in the wake of the coronavirus pandemic.

U.S. airlines have benefited from pent-up demand for leisure trips and a gradual return of lucrative business travel, helping them post strong quarterly earnings despite worries of an economic slowdown.

"Our fourth-quarter 2022 outlook remains strong, and we have a solid plan for 2023," Chief Executive Officer Bob Jordan said in a statement.

In a regulatory filing ahead of its investor day on Wednesday, Southwest said it was expecting "strong leisure revenue trends" to continue into the first quarter of next year, while business travel was expected to improve.

The carrier also trimmed its fourth-quarter fuel cost forecast by about 5 cents per gallon, compared with its previous estimate.

Southwest declared a third-quarter dividend of 18 cents per share, the same level at which it was prior to the pandemic. The dividend will be paid on Jan. 31.

The airline did not detail any stock buyback plans, which have been fiercely opposed by unions, who have asked U.S. airlines to focus on investing in their workers and fixing operational issues.

As part of the federal COVID-19 relief package, airlines had been prohibited from buying back their shares. The ban, however, expired on Sept. 30.

<<<

---

>>> U.S. Congress averts railroad 'Christmas catastrophe,' Biden says

Reuters

December 1, 2022

By David Shepardson and Moira Warburton

https://finance.yahoo.com/news/1-biden-administration-makes-case-184803591.html

WASHINGTON, Dec 1 (Reuters) - Congress gave final approval to a bill blocking a national U.S. railroad strike that could have devastated the American economy but rejected a measure that would have provided paid sick days to railroad workers.

The U.S. Senate voted 80 to 15 on Thursday to impose a tentative contract deal reached in September on a dozen unions representing 115,000 workers, who could have gone on strike on Dec. 9.

The bill now goes to President Joe Biden, who will sign it into law. Once the bill becomes law, any strike would be considered illegal and the strikers could be fired.

Eight of 12 unions have ratified the deal. But some labor leaders have criticized Biden, a self-described friend of labor, for asking Congress to impose a contract that workers in four unions have rejected over its lack of paid sick leave.

"We have spared this country a Christmas catastrophe in our grocery stores, in our workplaces, and in our communities," Biden said in a statement that praised Congress for acting to avoid devastating economic consequence for workers' families.

A rail strike could have frozen almost 30% of U.S. cargo shipments by weight, stoke already surging inflation, cost the American economy as much as $2 billion a day and stranded millions of rail passengers.

The U.S. House of Representatives approved the bill to block a strike on Wednesday and separately voted to require seven days of paid sick leave for rail workers.

Paid sick leave was one of the outstanding issues in the negotiations. There are no paid short-term sick days under the tentative deal after unions asked for 15 and railroads settled on one personal day.

Teamsters President Sean O'Brien harshly criticized the Senate vote on sick leave. "Rail carriers make record profits. Rail workers get zero paid sick days. Is this OK? Paid sick leave is a basic human right. This system is failing," O'Brien wrote on Twitter.

The measure to provide seven paid sick days did not win the required 60-vote supermajority in the Senate and was not endorsed by the White House.

A total of 52 senators, including 44 Democrats, two independents and six Republicans voted to mandate sick leave for rail workers, while 42 Republicans and Democratic Senator Joe Manchin voted against it saying he was sympathetic to workers' concerns but said Congress should not "renegotiate a collective bargaining agreement that has already been negotiated."

CONGRESSIONAL POWERS

Congress invoked its sweeping powers to block strikes involving transportation - authority it does not have in other labor disputes - because of the significant impact a rail stoppage could have on the U.S. economy, especially at the height of the holiday shopping season.

The Senate earlier on Thursday rejected a proposal by Senator Dan Sullivan to extend the cooling-off period by 60 days to allow for further negotiations.

Biden has praised the proposed contract, which includes a 24% compounded pay increase over five years and five annual $1,000 lump-sum payments, and he had asked Congress to impose the contract without any modifications.

American Association of Railroads CEO Ian Jefferies praised the vote.

"None of the parties achieved everything they advocated for" Jefferies said in a statement and added "without a doubt, there is more to be done to further address our employees’ work-life balance concerns."

Without the legislation, rail workers could have gone out next week, but the impacts would be felt as soon as this weekend as railroads stopped accepting hazardous materials shipments and commuter railroads began canceling passenger service.

U.S. Chamber of Commerce CEO Suzanne Clark praised "Congress for averting a catastrophic rail strike" and called it "a win for our country."

Senator Bernie Sanders and others denounced railroad companies for refusing to offer paid sick leave.

"They are maybe the worst case of corporate greed that I have seen," Sanders said. "That is really barbaric in the year 2022 in America."

The contracts cover workers at carriers including Union Pacific, Berkshire Hathaway Inc's BNSF, CSX , Norfolk Southern Corp and Kansas City Southern.

<<<

---

>>> Skyworks and MediaTek Collaborate to Offer End-to-End 5G Automotive Solutions

BusinessWire

November 13, 2022

https://finance.yahoo.com/news/skyworks-mediatek-collaborate-offer-end-040200548.html

MediaTek and Skyworks Develop 5G New Radio Design Enabling Seamless Integration With Automotive Communications Systems

MUNICH, November 14, 2022--(BUSINESS WIRE)--Skyworks Solutions, Inc. (Nasdaq: SWKS) today announced that the company has engaged with MediaTek to offer a complete modem-to-antenna automotive-grade 5G solution. This 5G New Radio Sky5A RF front-end solution will accelerate the deployment of this cutting-edge protocol across an array of automotive OEM and consumer service offerings.

"The rollout of 5G is reshaping the automotive market with a variety of safety and entertainment telematics applications to improve the driving experience," said Martin Lin, deputy general manager of the Wireless Communications Business Unit at MediaTek. "Through this collaboration with Skyworks, MediaTek is providing OEMs and automotive customers a complete solution that offers high performance, reliability and flexibility to meet the growing demands for bandwidth and advanced connectivity in next-generation vehicles."

As automotive OEMs create entirely new vehicle platforms with cutting-edge processing and sensing capabilities to support advancements in electric vehicle (EV) technology, driver-assistance systems (ADAS), and artificial intelligence, they are looking for solutions that can support the expanded data and connectivity demands of these next-generation innovations.

"This strategic initiative allows Skyworks and MediaTek to address the stringent requirements of the global automotive industry," said John O’Neill, vice president of marketing at Skyworks. "Our combined engineering expertise enables our customers to innovate new vehicle communication architectures, with the confidence that their designs will continue to meet future bandwidth needs and the rapid evolution of global wireless networks."

The 5G NR Sky5A RF front-end complete solution was designed for automotive applications, supporting 3GPP R15 and R16 standards, bandwidth exceeding 100MHz, flexible antenna architectures, regional optimization, aux ports to support the addition of future bands, and full automotive grade reliability qualification.

Skyworks will be exhibiting at Electronica Stand B5-138, taking place in Munich from Nov. 15-18, 2022, where the company will be highlighting its latest infrastructure, IoT, automotive, timing and power solutions.

About Skyworks

Skyworks Solutions, Inc. is empowering the wireless networking revolution. Our highly innovative analog and mixed signal semiconductors are connecting people, places and things spanning a number of new and previously unimagined applications within the aerospace, automotive, broadband, cellular infrastructure, connected home, defense, entertainment and gaming, industrial, medical, smartphone, tablet and wearable markets.

Skyworks is a global company with engineering, marketing, operations, sales and support facilities located throughout Asia, Europe and North America and is a member of the S&P 500® and Nasdaq-100® market indices (Nasdaq: SWKS). For more information, please visit Skyworks’ website at: www.skyworksinc.com.

<<<

---

>>> O'Reilly Automotive, Inc. (ORLY), together with its subsidiaries, operates as a retailer and supplier of automotive aftermarket parts, tools, supplies, equipment, and accessories in the United States. The company provides new and remanufactured automotive hard parts and maintenance items, such as alternators, batteries, brake system components, belts, chassis parts, driveline parts, engine parts, fuel pumps, hoses, starters, temperature control, water pumps, antifreeze, appearance products, engine additives, filters, fluids, lighting products, and oil and wiper blades; and accessories, including floor mats, seat covers, and truck accessories. Its stores offer auto body paint and related materials, automotive tools, and professional service provider service equipment. The company's stores also provide enhanced services and programs comprising used oil, oil filter, and battery recycling; battery, wiper, and bulb replacement; battery diagnostic testing; electrical and module testing; check engine light code extraction; loaner tool program; drum and rotor resurfacing; custom hydraulic hoses; and professional paint shop mixing and related materials. Its stores offer do-it-yourself and professional service provider customers a selection of products for domestic and imported automobiles, vans, and trucks. As of December 31, 2021, the company owned and operated 5,759 stores in the United States, and 25 stores in Mexico. O'Reilly Automotive, Inc. was founded in 1957 and is headquartered in Springfield, Missouri.

<<<

---

O'Reilly Automotive - 3 Top E-Commerce Stocks to Buy Right Now

Motley Fool

By Bradley Guichard

Mar 27, 2022

https://www.fool.com/investing/2022/03/27/3-top-e-commerce-stocks-to-buy-right-now/?source=eptyholnk0000202&utm_source=yahoo-host&utm_medium=feed&utm_campaign=article

Let's start with an unconventional e-commerce company. O'Reilly Automotive ( ORLY 1.54% ) probably isn't the first name that pops into your head when it comes to online shopping. However, its growth strategy has an omnichannel focus. Professional service providers can now place orders and receive local delivery with O'Reilly's proprietary platform made just for them. At the same time, DIY customers can do the same through the company's website.

O'Reilly could also capitalize on the enormous inflation we see in the new and used car markets. Gone are the days of haggling with the dealer for a deal well below the manufacturer's suggested retail price (MSRP). Instead, new car buyers are getting sticker shock. Thanks to dwindling inventories and the rising cost of new cars, used car prices have been up more than 40% over the past year. As a result, it's a good bet many drivers will be holding on to their vehicles longer, and the demand for parts from both professional service providers and DIY car owners will remain strong.

The company is already posting impressive results with revenue increasing to $13.3 billion in 2021, up 15%. The company's diluted earnings per share (EPS) also increased 32% to reach $31.10 last year. That was due in part to the company's lucrative share buyback program, which totaled nearly $2.5 billion in 2021 alone. O'Reilly stock has gained over 40% in the past year, and the company is set up to continue its impressive run long term.

<<<

>>> Top Railroad Stocks for Q1 2022

CP, CNI, and GBX are top for value, growth, and momentum, respectively

Investopedia

By MATTHEW JOHNSTON

February 01, 2022

https://www.investopedia.com/investing/railroad-stocks/

The railroad industry is one of the major components of the transportation sector and is closely tied to the economy's growth. Railroad companies operate vast networks that transport agricultural products, packaged foods, commodities, electronics, and other goods to companies and consumers. Major companies in the industry include Union Pacific Corp. (UNP), Norfolk Southern Corp. (NSC), and CSX Corp. (CSX).

The railroad industry does not have its own benchmark, but as a part of the broader transportation sector, its performance can be reasonably approximated by the iShares Transportation Average ETF (IYT). IYT has underperformed the broader market with a total return of 20.6% over the past 12 months, below the Russell 1000's total return of 23.0%.1 These performance figures and all others below are as of Jan. 11, 2022.

Here are the top 3 railroad stocks with the best value, the fastest growth, and the most momentum.

Best Value Railroad Stocks

These are the railroad stocks with the lowest 12-month trailing price-to-earnings (P/E) ratio. Because profits can be returned to shareholders in the form of dividends and buybacks, a low P/E ratio shows you’re paying less for each dollar of profit generated.

Best Value Railroad Stocks

Price ($) Market Cap ($B) 12-Month Trailing P/E Ratio

Canadian Pacific Railway Ltd. (CP) 74.75 49.9 20.2

CSX Corp. (CSX) 36.30 80.5 22.8

Canadian National Railway CO. (CNI) 122.28 86.4 23.3

Canadian Pacific Railway Ltd.: Canadian Pacific Railway is a Canada-based company that offers rail transportation services, including intermodal shipping, rail siding construction, and logistics services. The company announced in mid-December that it has completed its acquisition of Kansas City Southern (KSU), a cross-border railroad between the U.S. and Mexico, for approximately $31 billion. The shares of Kansas City Southern were placed in a voting trust upon the close of the acquisition, ensuring that the railroad operates independently of Canadian Pacific until the U.S. Surface Transportation Board makes a decision on the companies' joint railroad control application. The board's review of Canadian Pacific's proposed control of Kansas City Southern is expected to be finalized during the fourth quarter of 2022.2

CSX Corp.: CSX is a transportation company that provides rail, intermodal, and rail-to-truck transload services and solutions. It serves customers in a variety of markets, including energy, industrial, construction, agricultural, and consumer products.

Canadian National Railway Co.: Canadian National Railway is a Canada-based transportation company that offers fully-integrated rail and other transportation services, including intermodal, trucking, freight forwarding, warehousing, and distribution.

Fastest Growing Railroad Stocks

These are the top railroad stocks as ranked by a growth model that scores companies based on a 50/50 weighting of their most recent quarterly YOY percentage revenue growth and their most recent quarterly YOY earnings-per-share (EPS) growth. Both sales and earnings are critical factors in the success of a company.

On Nov. 15, 2021, President Biden signed into law the Infrastructure Investment and Jobs Act, which will invest approximately $550 billion in America's roads and bridges, water infrastructure, resilience, internet, and more. Of this $550 billion, $66 billion will be allocated to improving America's passenger and freight rail system.3

Therefore ranking companies by only one growth metric makes a ranking susceptible to the accounting anomalies of that quarter (such as changes in tax law or restructuring costs) that may make one or the other figure unrepresentative of the business in general. Companies with quarterly EPS or revenue growth of over 2,500% were excluded as outliers.

Fastest Growing Railroad Stocks

Price ($) Market Cap ($B) EPS Growth (%) Revenue Growth (%)

Canadian National Railway Co. (CNI) 122.28 86.4 81.7 11.5

CSX Corp. (CSX) 36.30 80.5 34.4 24.3

Trinity Industries Inc. (TRN) 30.87 3.0 57.1 9.6

Canadian National Railway Co.: See company description above.

CSX Corp.: See company description above.

Trinity Industries Inc.: Trinity Industries provides rail transportation products and services in North America. It offers railcar leasing and management services, as well as railcar manufacturing and modifications. The company announced in October financial results for Q3 of its 2021 fiscal year (FY), the three-month period ended Sept. 30, 2021. Net income attributable to shareholders rose 27.5% compared to the year-ago quarter. Revenue rose 9.6% YOY. Trinity Industries said that results were adversely impacted by labor shortages, turnover, and disruptions in supply chains, partly due to the economic impact of the COVID-19 pandemic. However, it expects profitability and demand for railcars to continue improving.4

Railroad Stocks With the Most Momentum

These are the railroad stocks that had the highest total return over the last 12 months.

Railroad Stocks with the Most Momentum

Price ($) Market Cap ($B) 12-Month Trailing Total Return (%)

Greenbrier Companies Inc. (GBX) 40.82 1.3 17.2

Union Pacific Corp. (UNP) 246.42 158.4 15.6

CSX Corp. (CSX) 36.30 80.5 14.7

Russell 1000 N/A N/A 23.0

iShares Transportation Average ETF (IYT) N/A N/A 20.6

Greenbrier Companies Inc.: Greenbrier Companies is a supplier of equipment and services to global freight transportation markets. The company designs and manufactures freight railcars and marine barges in North America, Europe, and Brazil. It also provides freight railcar wheel services, parts, maintenance, and retrofitting services in North America. Greenbrier announced in late October the appointment of President and Chief Operating Officer (COO) Lorie Tekorius, to the role of chief executive officer (CEO), effective March 1, 2022. Co-founder, Chairman, and CEO William A. Furman will assume the newly created role of Executive Chair on that same date.5

Union Pacific Corp.: Union Pacific connects 23 states in the western two-thirds of the U.S. by rail. It operates rail transportation services from all major West Coast and Gulf Coast ports to eastern gateways, connects with Canada's rail systems, and serves all six major Mexico gateways. The company announced in December that its board of directors approved a 10% increase in the quarterly dividend on the company's common shares, bringing it to $1.18 per share. The dividend was payable on Dec. 30, 2021 to shareholders of record as of Dec. 20, 2021.6

CSX Corp.: See above for company description.

<<<

>>> O'Reilly Automotive, Inc. (ORLY), together with its subsidiaries, operates as a retailer of automotive aftermarket parts, tools, supplies, equipment, and accessories in the United States. The company provides new and remanufactured automotive hard parts and maintenance items, such as alternators, batteries, brake system components, belts, chassis parts, driveline parts, engine parts, fuel pumps, hoses, starters, temperature control, water pumps, antifreeze, appearance products, engine additives, filters, fluids, lighting products, and oil and wiper blades; and accessories, including floor mats, seat covers, and truck accessories. Its stores offer auto body paint and related materials, automotive tools, and professional service provider service equipment. The company's stores also offer enhanced services and programs comprising used oil, oil filter, and battery recycling; battery, wiper, and bulb replacement; battery diagnostic testing; electrical and module testing; check engine light code extraction; loaner tool program; drum and rotor resurfacing; custom hydraulic hoses; and professional paint shop mixing and related materials. Its stores provide do-it-yourself and professional service provider customers a selection of products for domestic and imported automobiles, vans, and trucks. As of December 31, 2020, the company operated 5,616 stores. O'Reilly Automotive, Inc. was founded in 1957 and is headquartered in Springfield, Missouri.

<<<

>>> CSX Corporation (CSX), together with its subsidiaries, provides rail-based freight transportation services. The company offers rail services; and transportation of intermodal containers and trailers, as well as other transportation services, such as rail-to-truck transfers and bulk commodity operations. It transports chemicals, agricultural and food products, automotive, minerals, forest products, fertilizers, and metals and equipment; and coal, coke, and iron ore to electricity-generating power plants, steel manufacturers, and industrial plants, as well as exports coal to deep-water port facilities. The company also offers intermodal transportation services through a network of approximately 30 terminals transporting manufactured consumer goods in containers; and drayage services, including the pickup and delivery of intermodal shipments. It serves the automotive industry with distribution centers and storage locations, as well as connects non-rail served customers through transferring products from rail to trucks, which includes plastics and ethanol. The company operates approximately 19,500 route mile rail network, which serves various population centers in 23 states east of the Mississippi River, the District of Columbia, and the Canadian provinces of Ontario and Quebec, as well as owns and leases approximately 3,539 locomotives. It also serves production and distribution facilities through track connections. CSX Corporation was incorporated in 1978 and is headquartered in Jacksonville, Florida.

<<<

>>> Old Dominion Freight Line, Inc. (ODFL) operates as a less-than-truckload (LTL) motor carrier in the United States and North America. It provides regional, inter-regional, and national LTL services, including expedited transportation. The company also offers various value-added services, such as container drayage, truckload brokerage, and supply chain consulting. It owns 9,288 tractors and 42 maintenance centers. As of August 3, 2021, it owned 248 service centers. Old Dominion Freight Line, Inc. was founded in 1934 and is based in Thomasville, North Carolina.

<<<

>>> United Parcel Service, Inc. (UPS) provides letter and package delivery, transportation, logistics, and financial services. It operates through three segments: U.S. Domestic Package, International Package, and Supply Chain & Freight. The U.S. Domestic Package segment offers time-definite delivery of letters, documents, small packages, and palletized freight through air and ground services in the United States. The International Package segment provides guaranteed day and time-definite international shipping services in Europe, the Asia Pacific, Canada and Latin America, the Indian sub-continent, the Middle East, and Africa. This segment offers guaranteed time-definite express options. The Supply Chain & Freight segment provides international air and ocean freight forwarding, customs brokerage, distribution and post-sales, and mail and consulting services in approximately 200 countries and territories; and less-than-truckload and truckload services to customers in North America. This segment also offers truckload brokerage services; supply chain solutions to the healthcare and life sciences industry; shipping, visibility, and billing technologies; and financial and insurance services. The company operates a fleet of approximately 127,000 package cars, vans, tractors, and motorcycles; and owns 58,000 containers that are used to transport cargo in its aircraft. United Parcel Service, Inc. was founded in 1907 and is headquartered in Atlanta, Georgia.

<<<

$EXN Excellon Resources Inc., a silver mining and exploration company, acquires, explores for, evaluates, develops, and finances mineral properties in Mexico and Canada. The company primarily explores for silver, lead, zinc, and gold deposits. It holds 100% interests in the Platosa property covering an area of 11,000 hectares located in Durango State, Mexico; the Evolución property that covers an area of 45,000 hectares situated in the states of Durango and Zacatecas, Mexico; and the Silver City Project totaling an area of 164 square kilometers in Saxony, Germany. The company also holds 100% interests in the Kilgore Project that covers an area of 6,788 located in Clark County, Southeastern Idaho; and the Oakley Project covering an area of 2,833 hectares in Oakley, Idaho. Excellon Resources Inc. was incorporated in 1987 and is based in Toronto, Canada.

$IDEX 2021 Earth Day MEG China

$NAK The global rare earth market will grow in value from $8.1 billion in 2018 to more than $14.4 billion by 2025 as demand for electric vehicles, cellphones and other products rise.

$IDEX Ideanomics Mobility is a turnkey solution that provides economic and operational confidence. With a synergistic ecosystem of products and services, we are helping commercial fleets navigate the barriers of electrification across vehicles, charging and energy. From vehicle procurement, to charging infrastructure, to energy management, we are demystifying fleet electrification, and delivering the simplicity and scalability our customers are looking for.? https://ideanomics.com/our-company/

>>> Top Railroad Stocks for Q2 2021

CP.TO, CSX, and GBX are top for value, growth, and momentum, respectively

Investopedia

By NATHAN REIFF

Mar 17, 2021

https://www.investopedia.com/investing/railroad-stocks/?utm_campaign=quote-yahoo&utm_source=yahoo&utm_medium=referral

The railroad industry is one of the major components of the transportation sector and is closely tied to the economy's growth. Railroad companies operate vast networks that transport agricultural products, packaged foods, commodities, electronics, and other goods to companies and consumers. Major companies in the industry include Union Pacific Corp. (UNP), Norfolk Southern Corp. (NSC), and CSX Corp. (CSX).

The railroad industry does not have its own benchmark, but as a part of the broader transportation sector its performance can be reasonably approximated by the iShares Transportation Average ETF (IYT). IYT has outperformed the broader market with a total return of 78.4% over the past 12 months, above the Russell 1000's total return of 53.5%.1 The benchmark figures above and all statistics in the tables below are as of March 15.

Here are the top 3 railroad stocks with the best value, the fastest growth, and the most momentum.

Best Value Railroad Stocks

These are the railroad stocks with the lowest 12-month trailing price-to-earnings (P/E) ratio. Because profits can be returned to shareholders in the form of dividends and buybacks, a low P/E ratio shows you’re paying less for each dollar of profit generated.

Best Value Railroad Stocks

Price ($) Market Cap ($B) 12-Month Trailing P/E Ratio

Canadian Pacific Railway Ltd. ( CP.TO) CA$464.64 CA$61.9 25.8

CSX Corp. (CSX) 93.48 71.3 26.0

Union Pacific Corp. (UNP) 212.67 142.5 27.0

Canadian Pacific Railway Ltd.: Canadian Pacific Railway is a Canada-based company that offers rail transportation services, including intermodal shipping, rail siding construction, and logistics services. In early march, Canadian Pacific announced updates to its Hydrogen Locomotive Program, whose goal is to create a locomotive that produces zero emissions. In the latest development, Canadian Pacific plans to retrofit a diesel-powered locomotive with Ballard hydrogen fuel cells. It would be the first hydrogen-powered line-haul freight locomotive in North America.2

CSX Corp.: CSX provides domestic and international freight transportation services. The company offers rail, domestic container shipping, barging, intermodal, and contract logistics services between global hubs. The company's rail transportation services are focused in the eastern U.S. In February, CSX announced that its board of directors authorized an 8% increase in its quarterly dividend, from $0.26 to $0.28 per share. The new dividend was paid on March 15, 2021.3

Union Pacific Corp.: Union Pacific transports agricultural, automotive, chemical, and other products. The company provides routes from West Coast and Gulf Coast ports to eastern gateways, Canada, and Mexico.

Fastest Growing Railroad Stocks

These are the railroad stocks with the highest year-over-year (YOY) operating income, also called operating earnings, growth for the most recent quarter. Rising earnings show that a company’s business is growing and is generating more money that it can reinvest or return to shareholders. Operating income excludes non-operating income and expenses (such as investment gains or losses), one-time items, as well as interest and taxes. This helps investors get a clearer picture at the strength of the underlying business without the effect of unusual one-off events, such as large tax credits, asset sales, or lawsuit settlements. If you decided to invest in a company, it's still important to look at these one-off non-operating expenses and incomes, as they can still influence a company's overall financial health.

Fastest Growing Railroad Stocks

Price ($) Market Cap ($B) Operating Income Growth (%)

CSX Corp. (CSX) 93.48 71.3 5.3

Canadian Pacific Railway Ltd. ( CP) 372.40 49.6 2.6

Norfolk Southern Corp. (NSC) 260.27 65.6 1.4

Source: YCharts

CSX Corp.: See company description above.

Canadian Pacific Railway Ltd.: See company description above. Note that common shares of Canadian Pacific Railway Ltd. trade on both the Toronto Stock Exchange and the New York Stock Exchange.4

Norfolk Southern Corp.: Norfolk Southern is a rail transportation company operating primarily in the Southeast, East, and Midwest. The company transports raw materials, intermediate products, and finished goods. Through agreements with other carriers, it also provides service throughout the U.S., as well as transport of overseas freight.

Railroad Stocks with the Most Momentum

These are the railroad stocks that had the highest total return over the last 12 months.

Railroad Stocks with the Most Momentum

Price ($) Market Cap ($B) 12-Month Trailing Total Return (%)

Greenbrier Companies Inc. ( GBX) 48.83 1.6 172.2

Norfolk Southern Corp. (NSC) 260.27 65.6 80.5

Kansas City Southern ( KSU) 219.81 20.0 73.9

Russell 1000 N/A N/A 53.5

iShares Transportation Average ETF (IYT) N/A N/A 78.4

Source: YCharts

Greenbrier Companies Inc.: Greenbrier Companies is primarily engaged in the design, manufacture, and marketing of railroad freight car equipment. The company manufactures both railcars and marine vessels, provides repair and refurbishment for intermodal and conventional railcars, and provides complementary leasing and services. In February, Greenbrier announced plans to form GBX Leasing, a joint venture with The Longwood Group, a transportation equipment advisory and asset management firm. GBX Leasing will develop a portfolio of leased railcars primarily built by Greenbrier. The initial equity investment in the JV will benefit from specific tax advantages related to financial losses under the U.S. CARES Act passed in early 2020 to address the impact of the COVID-19 pandemic.5

Norfolk Southern Corp.: See company description above.

Kansas City Southern: Kansas City Southern is a holding company that, through its subsidiaries, operates a railroad system providing shippers with freight services in commercial and industrial markets in the U.S. and Mexico.

<<<

>>> Canadian Pacific to buy Kansas City Southern in $25 billion railway bet on trade

Yahoo Finance

Nandakumar D, Ann Maria Shibu and Rebecca Spalding

March 20, 2021

https://finance.yahoo.com/news/canadian-pacific-buy-kansas-city-034255096.html

Canadian Pacific to buy Kansas City Southern in $25 billion railway bet on trade

(Reuters) - Canadian Pacific Railway Ltd agreed on Sunday to acquire Kansas City Southern in a $25 billion cash-and-stock deal to create the first railway spanning the United States, Mexico and Canada, standing to benefit from a pick-up in trade.

It would be the largest ever combination of North American railways by transaction value. It comes amid a recovery in supply chains that were disrupted by the COVID-19 pandemic, and follows the ratification of the US-Mexico-Canada Agreement (USMCA) last year that removed the threat of trade tensions that had escalated under former U.S. President Donald Trump.

"Think about what we've gone through, think about the importance in North America of near-shoring that is occurring. This network uniquely provides a supply chain that allows our customers and our partners to actually benefit from that and leverage that opportunity," Canadian Pacific Chief Executive Keith Creel told Reuters in an interview.

The combination needs the approval of the U.S. Surface Transportation Board (STB). The companies expressed confidence this would happen by the middle of 2022, given that the deal would unite the smallest of the seven so-called Class I railways in the United States, which meet in Kansas City and have no overlap in their routes. The combined railway would still be smaller than the remaining five Class I railways.

The STB updated its merger regulations in 2001 to introduce a requirement that Class I railways have to show a deal is in the public interest. Yet it provided an exemption to Kansas City Southern given its small size, potentially limiting the scrutiny that its acquisition will be subjected to.

"I don't see it as the kind of consolidation that should raise concerns because it's what you call an end-to-end or vertical merger. Their networks fit nicely with each other and help fill out North America with real service," said economist Clifford Winston, a senior fellow at the Brookings Institution who specializes in the transportation sector.

An STB spokesman said the regulator had not yet received a filing from the companies, which would start its formal review process. He declined to comment further.

Still, Canadian Pacific agreed in its negotiations with Kansas City Southern to bear most of the risk of the deal not going through. It will buy Kansas City Southern shares and place them in an independent voting trust, insulating the acquisition target from its control until the STB clears the deal.

Were the STB to reject the combination, Canadian Pacific would have to sell the shares of Kansas City Southern, and one source close to the agreement suggested they could be divested to private equity firms or be relisted in the stock market. Kansas City Southern shareholders would keep their proceeds.

There is a $1 billion reverse breakup fee that Canadian Pacific would have to pay Kansas City Southern if it cannot complete the formation of the trust, the source added.

Shareholders of Kansas City Southern will receive 0.489 of a Canadian Pacific share and $90 in cash for each Kansas City Southern common share held, valuing Kansas City Southern at $275 per share, a 23% premium to Friday's closing price, the companies said in a joint statement. Including debt, the deal is valued at $29 billion.

Kansas City Southern shareholders are expected to own 25% of Canadian Pacific's outstanding common shares, the companies said. Canadian Pacific said it will issue 44.5 million shares and raise about $8.6 billion in debt to fund the transaction.

It is the top M&A deal announced thus far in 2021. While it is the biggest ever involving two rail companies, it ranks behind Berkshire Hathaway's purchase of BNSF in 2010 for $26.4 billion. For a Factbox on the deal highlights see:

Creel will continue to serve as CEO of the combined company, which will be headquartered in Calgary, the companies said in a statement.

The companies also highlighted the environmental benefits of the deal, saying the new single-line routes that would be created by the combination will help shift trucks off crowded U.S. highways and cut emissions.

Rail is four times more fuel efficient than trucking, and one train can keep more than 300 trucks off public roads and produce 75% less greenhouse gas emissions, the companies said in the statement.

FAILED BIDS

Calgary-based Canadian Pacific is Canada's No. 2 railroad operator, behind Canadian National Railway Co Ltd, with a market value of $50.6 billion.

It owns and operates a transcontinental freight railway in Canada and the United States. Grain haulage is the company's biggest revenue driver, accounting for about 58% of bulk revenue and about 24% of total freight revenue in 2020.

Kansas City Southern has domestic and international rail operations in North America, focused on the north-south freight corridor connecting commercial and industrial markets in the central United States with industrial cities in Mexico.

Canadian Pacific's latest attempt to expand its U.S. business comes after it abandoned a hostile $28.4 billion bid for Norfolk Southern Corp in April 2016. Canadian Pacific's merger negotiations with CSX Corp, which owns a large network across the eastern United States, failed in 2014.

A bid by Canadian National Railway Co, the country's biggest railroad, to buy Warren Buffett-owned Burlington Northern Santa Fe was blocked by U.S. antitrust authorities more than two decades ago.

A private equity consortium led by Blackstone Group Inc and Global Infrastructure Partners (GIP) made an unsuccessful offer to acquire Kansas City Southern last year. The sources said that bid helped revive Canadian Pacific's interest in Kansas City.

BMO Capital Markets and Goldman Sachs & Co. LLC are serving as financial advisors to Canadian Pacific, while BofA Securities and Morgan Stanley & Co. LLC are serving as financial advisors to Kansas City Southern.

<<<

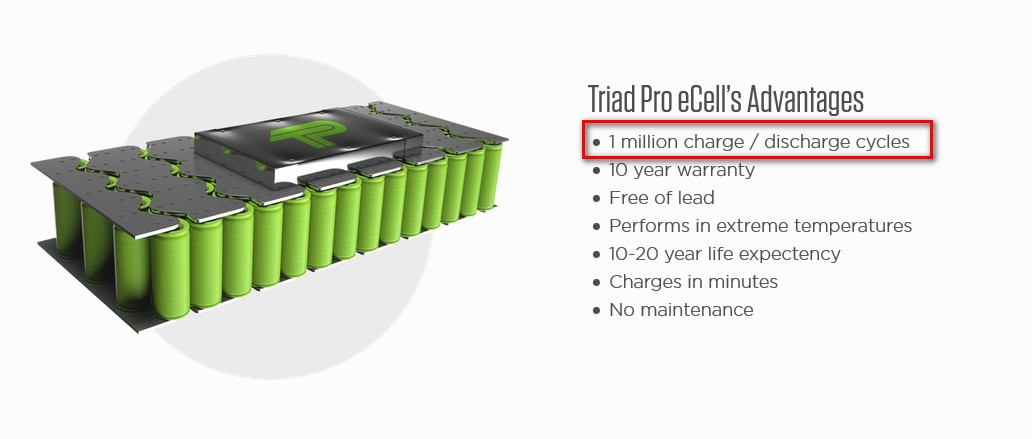

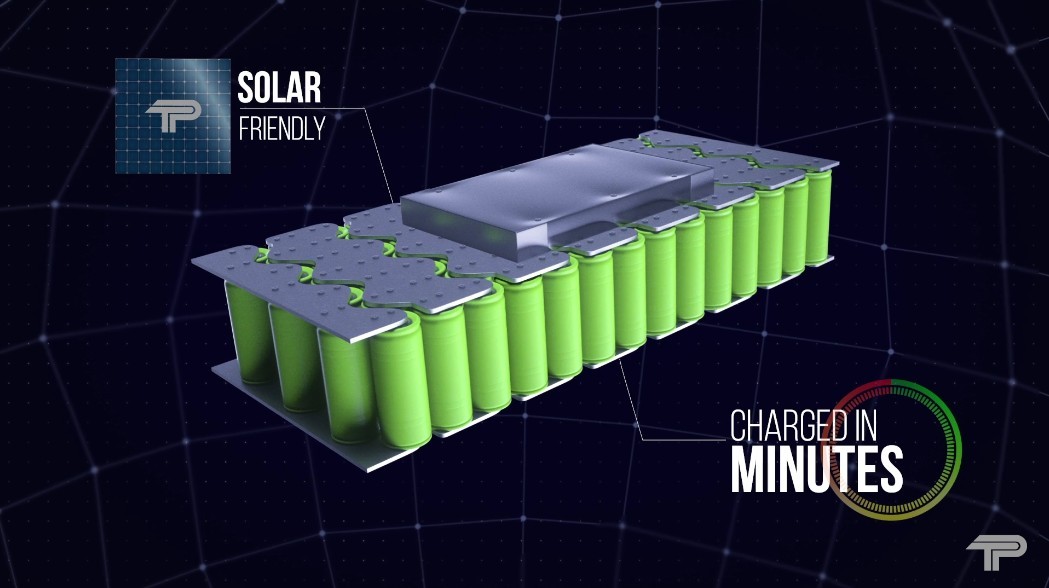

$TPII still the most promising breakthrough EV and fixed-site energy storage technology around. $TPII's super-capacitor energy storage technology replaces OR supplements lithium batteries in EVs, trucks, golf carts as well as fixed-site storage facilities.

Check out their site: http://www.TriadProInc.com

$TPII Breakthrough EV-Storage-Tech in production: Replacing Lithium!

http://www.TriadProInc.com

Watch the Video: http://www.TriadProInc.com/

>>> Railroads Make Up 36.7% Of This Transportation ETF

Seeking Alpha

Oct. 09, 2020

by Sven Carlin

https://seekingalpha.com/article/4378292-railroads-make-up-36_7-of-this-transportation-etf

Summary

Railroads are good businesses with a strong moat, high profitability, good growing dividends and buybacks that push stock prices higher. It is likely railroad stocks will keep being the stable ones within the transportation ETF.

The buyback game is a risky game to play and can't be played forever. The key is to sell at some point in time before the debt becomes a burden.

At the bottom of the article you have a video discussing the topic if you prefer watching.

We all know Warren Buffett owns a railroad, Burlington Northern Santa Fe. Therefore, it is always good to look into railroad stocks to see whether a railroad stock might fit your portfolio too. A way to get exposure to railroad stocks is the iShares Transportation Average ETF (IYT) as 36.7% of its weight consists of 4 railroad stocks:

Norfolk Southern (NSC)

Union Pacific (UNP)

Kansas City Southern (KSU)

CSX Corp. (CSX)

This article will describe the investment thesis for railroad stocks, give an overview of all railroad stocks traded in the US, discuss the main trends within the sector, the valuation and the risks of investing in them.

Railroad stocks investment thesis – Moats, Growth & Profitability

The 4 key ingredients that make something a great business to own are moat, growth, increasing profitability and fair price. We analyze the moat strength of railroads, the growth opportunities, profitability and valuation.

Railroad stocks offer a moat

A railroad is a typical Buffett business. Over the last few decades the sector has consolidated and the number of railroads fell from 40 to 7. Each railroad has its own geography and nobody wants to build new railroads because that would impact the profitability of the other and your own railroad. Once you build it, you own it and you can enjoy the economic benefits of it without worrying that somebody will build a new one next to you.

It is unlikely anybody could get permission to build a big, new railroad (not in my backyard) and it is also unlikely a new railroad would ever be profitable because of the competition. Therefore, we can say railroads have a wide moat.

Railroad stocks offer growth and sustainability

When you have a moat, and a stable infrastructure, the more business you do using your infrastructure, the more money you make because your costs increase less than your revenue, thanks to the fixed cost part.

The Association of American Railroads predicts a 30% increase in U.S. freight movements by 2040. That is not much per year, but when you have a moat, when you don’t need to worry about competition too much, when you can focus on reducing costs, improving operations and increasing profitability as much as possible, it adds up to significant profitability increases.

Rail is already the most efficient way to move freight as a gallon of fuel can move a ton of freight for 470 miles on average.

The fuel efficiency makes it also environmentally positive to move things with trains.

We have discussed how railroads offer a moat and growth. But that is not enough to make them a good investment. What you need are profitability and a good price.

Precision Scheduled Railroading Increases Railroad Profitability + Scale

Since the Staggers Rail Act of 1980 that deregulated railroads, railroads spent more than $710 billion on their infrastructure. They did that because it was profitable to do so. The average railroad had returns on capital employed between 7% and 13% over the last 15 years where the returns even increased over the last decade as more and more railroads implemented Precision Scheduled Railroading.

High profitability, a moat, stable businesses, a good return on capital and a focus on rewarding shareholders have pushed railroad stocks to extremely high levels.

Railroad stocks performance and valuation

Actually, over the last 5 years, all railroad stocks have beaten the S&P 500.

Railroad stocks performance over the last 5 years

What happened happened, and there is nothing we can do about it. What we have to do is see how railroad stocks fit our portfolio now. The best way to value a business like a railroad is to look at cash flows and future growth opportunities.

I have compiled a table that compares all railroad stocks and the free cash flow yield is between 3% and 3.7% except for CSX, but that might be due to the coal exposure CSX has, thus it can be considered riskier. If you are interested in individual analyses you can find all the links below.

Railroad stocks dividends and buybacks

All railroad stocks pay a dividend but their key focus is buybacks. All listed ones take on as much debt as possible in order to do as much buybacks as possible. This is probably the reason why railroad stocks have outperformed the S&P 500.

However, as they are taking on more and more debt to do buybacks at any price, as investors we have to be careful to get out in time because when the buybacks stop and liquidity dries up, railroad stock prices will likely crash. So, enjoy the ride while it lasts and see how holding a business with a yield slightly above 3% but relatively safe fits your portfolio.

3% free cash flow yield as valuation metric

A good valuation metric for railroad stocks is also what would a railroad be worth to an owner. Recently KSU rejected a takeover bid for a free cash flow yield of 3%. Thus, we could see that as a margin of safety in this environment. Investment funds that can borrow at below 2% see railroad stocks as attractive when those offer long-term growth and a 3% cash flow yield. However, I don’t think many can come up with more than $20 billion to buy the bigger railroads, so the investment thesis with the bigger railroads is based on the cash flow yield and buyback activity.

Railroad stocks investment thesis

The investment thesis depends on what perspective you take; a relative or absolute perspective.

From an absolute investing perspective, railroads offer a 3% cash flow yield in the form of dividends and buybacks, slow growth alongside a strong moat. Nothing wrong with their businesses and it is likely in 20 years everything will look the same with improved profitability and likely even more traffic. The debt piled up might be an issue if interest rates go up, but interest rates going up is also unlikely for the short to medium term. So, we have safety and quality alongside a yield between 3% and 3.7% on average.

From a relative perspective, with your bank giving you miserable returns on savings, with investment banks and hedge funds being able to borrow at ridiculously low rates, if the market starts liking railroad stocks with a 2% free cash flow yield, that will represent a 50% upside from current levels. Plus, all the buybacks might make it much easier for railroad stocks to go up and do well. Actually, I think that until the buyback game lasts, railroad stocks will likely outperform the market.

Further, with the Fed saying it will allow inflation and railroads focusing on cost savings, their actual margins might improve especially as interest rates on debt stay low. So, railroads could be a safe bet to add portfolio protection against the loose monetary environment we will likely have the coming decade.

Railroads go for automation that lowers costs and improves safety

I hope to have given you a good perspective on railroad stocks so that you can compare them to other investment opportunities you have and see what is the best investment that will lead you to your financial goals – that is the key, nothing else matters.

Railroad stocks as part of IYT

For now, railroad stocks give the necessary stability to IYT as the dividends haven't been cut in this environment and the buybacks stay strong. However, the buyback game can only last up till a point.