News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Any action? I can see unlimited authorised shares...that’s not good is it.

Just registered for the free investor conference to hear about this company.

https://www.eventbrite.ca/e/gcff-virtual-conference-2021-base-metals-and-energy-metals-day-registration-132479691323?aff=RY

Well ?.....Here come the BIG Players !

Boy, sure was wrong about the SPY (thanks to that pre-and post-election), which led me to back away from several fine prospects. Why even Ceylon here is one....Where the volumes have been too frighteningly low in my mind

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=159112178

![]()

That was then....

![]()

Well no, for if the S&P were to start to start turning down (which it is seemingly threatening to do),

I don't think I'd want to be long much in anything (yet)....

![]()

![]()

That S&P chart looks scary...you going to hedge with some graphite plays? :)

For me it's just that the broad markets are so long in the tooth

Doesn't seem overly likely

![]()

It could move faster with volume

Well no because, in actual fact, it's ON peoples' radar and it's increasing rapidly.....

FRIDAY

![]()

MONDAY

nowwhat

Ya fantastic. Below radar going up nice and slowly

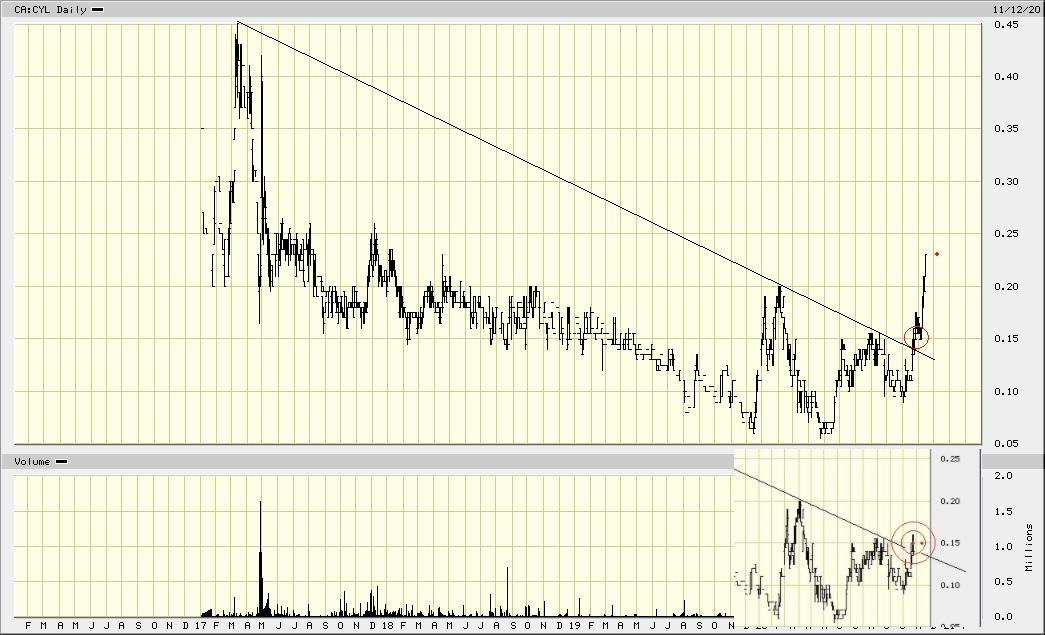

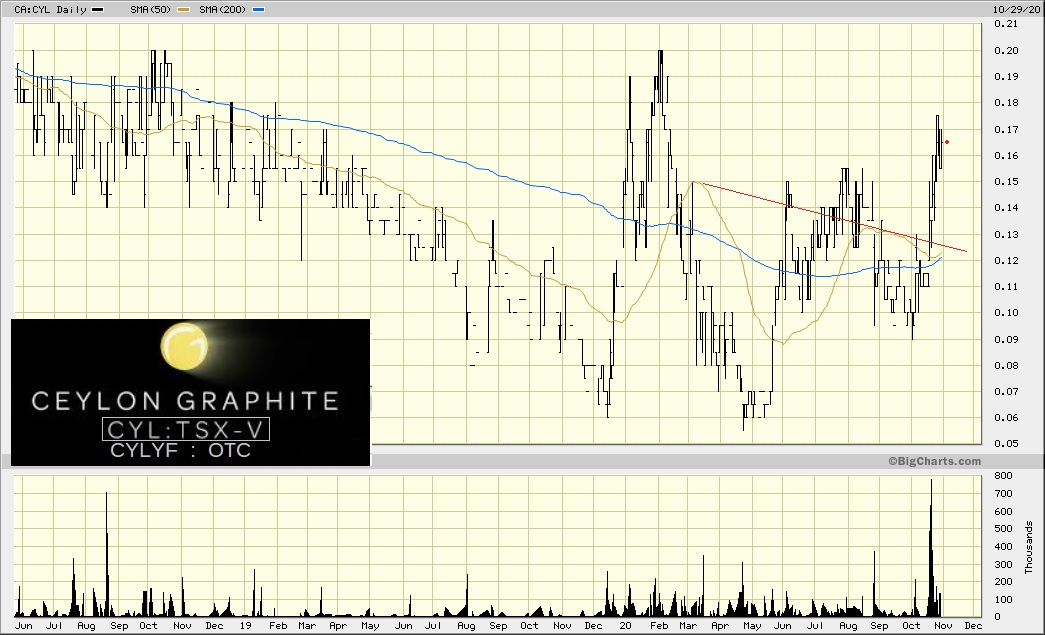

Well......It's certainly quite a crazy chart !

At least we know THAT much.

![]()

This one is a good comparable to Ceylon because they are both in Sri Lanka.

Just from a preliminary overview on just their graphite, they have leases in Sri Lanka for 8 kilometers of mineable property rights. Ceylon has 121 shaft mines that are 1 kilometer each. They have just done a round of offerings so they now have a lot of cash (Ceylon) to build out their mines and the CEO says they will be self sufficient, using working capital. They have a huge profit margin on what they pull out of their shaft mines. For every $200/ton spent they make $1200-$1500 per ton and it will be more with graphite prices rising.

Ameca says they can open pit mine which is cheaper but they will only pull the graphite from the surface and they only have 8 kilometers of mine compared to Ceylon's 121 kilometeres of deep shaft mines.

I think Ceylon is way undervalued and a better investment than Ameca just on my initial reading from their website and just based on the graphite alone. Ceylon is on the radar of a lot of institutional investors from the DD I've done.

Pay attention to the part of Ameca's site that shows their plans for the shell:

"Obtain shell company for next round of financing" that sounds like they are going to dilute even though it also says the projects are currently owner financed.

Sri Lanka also carries political risk and is not considered as environmentally friendly as North American graphite miners but certainly better than China which is all they have in that part of the world right now.

Just preliminary thoughts. Thanks for the heads up on this one.

Thoughts on STHC?

Look at Nouveau Monde for short term into long term growth. They have a huge graphite resource in Quebec with a newly constructed pilot mine and institutional investors. The CEO is very smart and savvy and they will be big players in the North American graphite market soon.

This is a long term play but could pop on graphite prices rising.

They are going to use the proceeds from the offering they just did to build out more of their vertical shaft mines (they have 121 in Sri Lanka that are about a kilometer in size each).

They have a unique graphite story in that they mine vertically in shaft mines rather than horizontally in open pits because the graphite is condensed in veins that are very pure. They also have extremely high profit margins on what they are able to pull out of these shaft mines.

Long term potential is huge on this one.

Any thoughts on how high this can go short term

Offering extended to raise $6 million USD through selling up to 90 million units comprised of one share and .3073 of a warrant

https://www.otcdynamics.com/cylyf-ceylon-updates-private-placement/?utm_campaign=twitter&utm_medium=twitter&utm_source=twitter

Vertical shaft mined "vein" fine grade graphite in Sri Lanka

|

Followers

|

4

|

Posters

|

|

|

Posts (Today)

|

0

|

Posts (Total)

|

32

|

|

Created

|

07/16/17

|

Type

|

Free

|

| Moderators | |||

| Volume | |

| Day Range: | |

| Bid Price | |

| Ask Price | |

| Last Trade Time: |