News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Matamec Announces Agreement for the Sale of its Royalties in the Timmins Gold Camp to Metalla Royalty & Streaming Ltd.

7:47 am ET May 4, 2017 (Market Wire) Print

Net Smelter Royalties on the Hoyle-Matheson and Montclerg Properties to be Sold

MONTREAL, QUEBEC--(Marketwired - May 4, 2017) - Matamec Explorations Inc. ("Matamec" or the "Company") (TSX VENTURE:MAT)(OTCQB:MHREF) is pleased to announce that it has entered into a binding sale and purchase agreement with Metalla Royalty & Streaming Ltd. ("Metalla") for the sale of its royalties on the Hoyle-Matheson Royalties (HMR) Property and the Montclerg Property. Both properties are located in the world-class Timmins Gold Camp, an area that has produced more than 70 million ounces of gold from large deposits.

The purchase price payable for the Royalties is made up of $500,000 in cash and Two Million (2,000,000) shares of Metalla valued at $0.50 per share. Matamec will also receive warrants to purchase another One Million (1,000,000) shares of Metalla at $0.75 per share for a period of two years. The shares and the warrant shares cannot be traded 12 months from the closing date. The closing of the transaction is subject to certain customary closing conditions.

"The proceeds from the sale of these royalties will enhance Matamec's value for its shareholders," said André Gauthier, Matamec's President and CEO. "At the same time, it allows us to focus our efforts on exploration - for gold at Matamec's other gold properties, as well as for energy and technology-related metals at properties held in its Energy portfolio."

About Matamec

Located in Montreal (Québec), Matamec Explorations Inc. is a junior mining exploration company in which activities are based on two main axes of development: gold, and key elements for technologies related to energy with properties containing, among others, lithium (Tansim-owned at 100%), Cobalt (Fabre-100% owned), nickel (Vulcain-100% owned) and rare earths (Kipawa-72% owned by Matamec).

Matamec's main focus is the development of the Kipawa Heavy Rare Earth Elements (HREE) deposit, a joint venture owned at 72% by Matamec and 28% by Ressources Québec (acting as agent of the Government of Québec); Toyota Tsusho Corp. (Nagoya, Japan) holds a 10% royalty on net profit in the deposit.

In addition to the activities in energy sector, Matamec is exploring for gold, with properties located in the area of the Hoyle Pond Mine in Timmins, ON, as well as four in the Quebec Plan Nord region in similar geological settings as established gold-producing mines. These include two in proximity to the Éléonore Mine (in James Bay, QC): Sakami (50%) and Opinaca Gold West (100%).

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Visit us on Facebook: https://www.facebook.com/MatamecInc

Andre Gauthier, President (514) 844-5252 info@matamec.com CHF Capital Markets Cathy Hume, CEO +1 416-868-1079 x231 cathy@chfir.com

Interesting video clip on the Rare Earth project with CEO

http://www.b-tv.com/matamec-explorations-inc-ceo-clip/

Matamec Partners with Necando Solutions

Matamec Explorations Inc.

TSX VENTURE : MAT

OTCQB : MHREF

image: http://media3.marketwire.com/logos/20160404-matameclogo_200.jpg

Nmx

April 20, 2017 07:59 ET

Matamec Partners with Necando Solutions to Leverage IBM Cloud and Artificial Intelligence Technology

Data collected during the course of Matamec's innovation activities at the Kipawa Rare Earths project will be exploited through the use of IBM cloud and artificial intelligence technology, in order to discover new models that will optimize the project

MONTREAL, QUEBEC--(Marketwired - April 20, 2017) - Matamec Explorations Inc. ("Matamec" or the "Company") (TSX VENTURE:MAT)(OTCQB:MHREF) is pleased to announce a collaboration with Necando Solutions that will leverage cutting-edge technology to mine data generated through its research activities. The goal of this initiative is to take advantage of IBM's tool, including the cognitive technology known as Watson, to process a large volume of data and discover models that will enable the optimization of the Kipawa Rare Earths project.

Since 2015, Matamec has been working to develop innovative ways to improve and optimize mining operations as well as metallurgical processes at Kipawa. These innovation-related activities are summarized in the diagram below:

Kipawa Innovation Diagram: http://media3.marketwire.com/docs/IBMcloud.jpg

"Our work to improve the Kipawa project over the past two years has been generating a lot of data that would take researchers years to process," explained Andr Gauthier, Matamec's President and CEO. "By working with Necando to leverage the power of IBM's artificial intelligence and data cloud platforms, we will be able to process the data to optimize all aspects of the project much more quickly and effectively."

About Necando

Necando Solutions is a strategic consulting firm specializing in information technology solutions. It offers a full spectrum of technology services, from analysis to integration and development. It has a strong reputation for excellence based on individual customer experiences.

As an elite partner of IBM, they have a team of seasoned, mobile and bilingual experts who are committed to meeting the expectations of their clients. Their team excels at proposing solutions to the challenges that arise in an ever-changing technological and commercial landscape.

At Necando Solutions, the use of technology and process optimization, together with effective change management planning, stimulates innovation and drives sustainable growth.

About Matamec

What is in the future of Matamec for shareholders.

Good Morning,

Every now and then comes along a pinksheet or pennystock that has huge potential. Now I come from this mindset after 20 years of playing the penny-arcade and from my professional experience of having my own business as a corporate profiler and Merger and Acquisitions for the last 16 years.

Trading pennystocks is an art and science that requires an absolute discipline in understanding the nature of pennystocks. Trading in this venue is not for most and from history's standpoint most (98%) of all pennystocks, fail or flounder at the bottom to never return.

Now we have in Matamec a truly well run and in my belief a pennystock that has long-term investment potential. I have never considered a pennystock as an investment, but a mechanism to build wealth by trading and not holding to augment your earnings into investment grade securities.

I see huge upside with MHREF as we move closer to the actual operational stage.

The 2016 year was a dormant year and the overall commodity sector really took a beating for the last few years, however, I believe the rime has come and we should see a positive 2017 and beyond.

The company so far has been extremely discipline in controlling the issue of shares or maintaining a lid on the execution or retailing other wise known as diluting the pool by running the operational stage, Administration and R&D. This is very positive and is what drags down most pennystocks and leaves investors holding worthless stock to never be able to recoup their principle investment. This company, so far is and appears to have shareholders interest in mind and that is the beginning to feel comfortable with your investment.

It doesn't surprise me that we are still lingering down in the subpennies, but eventually this will change as we move forward. As I mentioned above the commodity sector and most importantly the Rae Earth Element has not fully been appreciated. This in my opinion is about to change.

As the world moves into a renewable source for our energy needs the Kipawa project with Toyota as a partner ( of 10%) is only going to enhance our investment that will command credibility and as such, so will the investment for us shareholders. Let's not forget the collaboration with 28% by Resources Qubec (acting as agent of the Government of Qubec).

As the company has noted from their analysis, the Kipawa project is a 2. $b recoverable mining project over a period of 15 years.

So when we break this down to actual revenue per year, it is 16 $m.

Now I'm not going into the operational costs since this part still has to be determined and giving actual numbers may prove to be unproductive at this time, but the company has mentioned in one of their past statements that a 25 $m capital outlay needs to be obtained. This original capital expenditure is only the beginning, but still well within making this enterprise a profitable venture for us and the company.

Currently our market cap is around 5$m US$ with 137m O/S and generally is within the scope of pennystock companies that truly have a business model.

As we move forward going into 2017 and closer to operational stage, which I believe to be around 2017 Fall, when in 2018, we will be in full production, the share price will start it's climb and I expect this to happen by the middle to fall of this year or the spring of 2018.

Currently the company maintains a burn rate of 12 $k per month , but we can count on this to drastically to go up once we go into operational stage, but with a potential of 16 $m per year of revenue or 1 $m per month, one has to agree that we are looking at an eventual considerable multiple increase in the share price.

Of course, much of this rise in the share price will be dependent upon the financial package that the company needs to secure it's capital needs to move into operational stage, but still, we should see a significant increase to at least 10 fold from the current price of .05 USA$.

One can reasonably be comfortable to the understanding that a major price hike is in the future and if the timeline on actual operational and the capital financial package is made public, we will see a move by the end of this year going into spring 2018.

I see the first point of resistance on the share price to be around .10 and this will give us a MC of $13m, still well below the fair value. I am not looking at PE ratio since pennystock companies generally are never tabulated on PE, but straight accounting. I expect this movement to begin near the muddle of 2017 through the end of spring 2018 since the winter months well probably have very little impact.

With 16 $m in potential revenue for the first year of operation expected for 2018, but 2017, should allow for us to have a share price to be well over .10$. Again, of course this is dependent upon the financial package and how it is laid out with the equity end of the deal.

But let's assume that our O/S move up from 137m to 250m, even at 250 O/S one can see that under the current share price of .04 USA is still well under the fair value of MC $10m. Even at .10 the MC will be $25m still well under fair value if the figures of retrieval reserves is based on $16m per year.

If the $16m achievable resources is met and not mentioning the actual burn at the time during operation we could very well command a share price of .10 giving a MC of $13m straight up accounting without a PE ratio calculated. So one can see definitely .25 without any problem.

Now you must take into acct the gold aspect of other claims. This needs to be calculated into the overall worth and the other claims yet still to be realized with respect to feasibility and operational costs to profitability assessment.

With the Kipawa project we should bode well on it's own merit and adding the other assets (claims) we can commend a share price of well over a $1.00 in the years to come and I believe this company will eventually move out of the pennyarcade and become a true investment grade company.

I recommend this a buy at the current price of .04 and under .10. Always do your due diligence and never invest more than you can lose.

Have a good day

varok

The Holmium factor for the Kipawa

Holmium oxide price worldwide from 2010 to 2025 (in U.S. dollars per kilogram)*

https://www.statista.com/statistics/450166/global-reo-holmium-oxide-price-forecast/

If I take your 30000 (US) tons a year as factual, it represents 27215542 kilograms. Therefore, at 49 dollars US a kilo (2017 US price) it would be about 1.3 billion US dollars annually for holmium oxide sales for Matamec and not taking into account other oxides. It would be fantastic for Matamec shareholders.

Have a good day

varok

Check out the new updated website.

http://www.matamec.com/

Have a good day

varok

Matamec Announces Commencement of New Drilling Program on the Sakami Gold Property

8:48 am ET March 28, 2017 (Market Wire) Print

3,000m campaign on Zone 25 seeks to confirm the extension of gold mineralization to the west and follow up on previous results that include 21.05m of 4.94g/t Au

MONTRÉAL, QUÉBEC--(Marketwired - March 28, 2017) - Matamec Explorations Inc. ("Matamec" or the "Company") (TSX VENTURE:MAT)(OTCQB:MHREF) and Canada Strategic Metals ("CSM") (TSX VENTURE:CJC)(FRANKFURT:YXEN)(OTCBB:CJCFF) are pleased to announce the commencement of drilling on the Sakami property, of which the two companies each own 50%. A total of 3,000m of drilling is planned on the shore of Sakami Lake to extend the known mineralized body to the west. Drilling in 2016 suggests that the mineralization is thicker and locally richer in this direction. It also confirms the relatively consistent orientation of the mineralization, which allows for more aggressive step-outs of 90m.

The figures below illustrates the distribution of mineralized intervals and planned drilling.

Figure 1. Oblique image of Zone 25 showing the distribution of mineralized intervals created using a 1g/t lower limit and shown as spheres according to the thickness. Red traces represent the planned drilling.

http://media3.marketwire.com/docs/029_1.pdf

Figure 2. Vertical section looking west, showing the proposed drill traces in red with respect to the possible extensions to Zone 25 (grey polygon).

http://media3.marketwire.com/docs/029_2.pdf

CSM recently exercised an option to acquire an additional 20% of the Sakami property from Matamec in exchange for 1 million shares in the company and a commitment to spend CDN$ 2,000,000 in exploration work per year for the next five years, during which time it must also complete an independent bankable feasibility study. Please see the press release from February 14th, 2017 for more details of the option agreement and the ownership structure of the property. During the period covered by the option agreement, CSM will remain the operator of the exploration works, supervised by a management committee comprising two representatives of CSM and two representatives of Matamec.

Guy Desharnais, P.Geo., Ph.D. (OGQ No.1141), is a Qualified Person as per NI 43-101; he is employed by SGS Canada Inc., is independent of Matamec, designed the drill program and has reviewed and approved the technical content of this press release.

"We are pleased to see the Sakami project moving forward," said André Gauthier, President and CEO of Matamec. "We believe there is significant gold potential at the property, and look forward to the results of this latest drilling program."

About Matamec

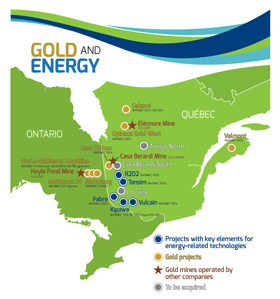

Map showing location of Matamec Gold and Energy Properties: http://media3.marketwire.com/docs/651c_e.jpg

Located in Montreal (Québec), Matamec Explorations Inc. is a junior mining exploration company in which activities are based on two main axes of development: gold, and key elements for technologies related to energy with properties containing, among others, lithium (Tansim-owned at 100%), Cobalt (Fabre-100% owned), nickel (Vulcain-100% owned) and rare earths (Kipawa-72% owned by Matamec).

Matamec's main focus is the development of the Kipawa Heavy Rare Earth Elements (HREE) deposit, a joint venture owned at 72% by Matamec and 28% by Ressources Québec (acting as agent of the Government of Québec); Toyota Tsusho Corp. (Nagoya, Japan) holds a 10% royalty on net profit in the deposit.

In addition to the activities in energy sector, Matamec is exploring for gold, with three properties (HMR (1% NSR), Matheson JV (50%) and Pelangio (100%)) located in the area of the Hoyle Pond Mine in Timmins, ON, as well as four in the Quebec Plan Nord region in similar geological settings as established gold-producing mines. These include two in proximity to the Éléonore Mine (in James Bay, QC): Sakami (50%) and Opinaca Gold West (100%).

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Visit us on Facebook: https://www.facebook.com/MatamecInc

Andre Gauthier, President (514) 844-5252 info@matamec.com CHF Capital Markets Cathy Hume, CEO +1 416-868-1079 x231 cathy@chfir.com

It's a new year and I strongly believe we are going to be able to pacify and give reason to First Nation's concerns.

The company has two much invested and stake in the Kipawa project just to walk away. This is not how these things turn out. Negotiations is key and the right team is in place to get a deal.

This part I really like and find enough credible reasons why they will never give up on Kipawa and why I have always stayed.

" Matamec's Kipawa Deposit contains Holmium, the Heavy Rare Earth Element Essential to New Storage Technology that Allows for 1000x More Data to be Stored than Ever Before. "

" the recent discovery by a team of nano-science researchers, mainly from IBM's Almaden Research Center in San Jose, California, of the ability to store one bit (1b) of data on a single holmium (Ho) atom. The breakthrough findings were published in the peer-reviewed journal Nature earlier this month (cf. Nature, vol. 543 pp. 226-228, 9 March 2017). "

" Holmium (Ho - atomic number 67) is a heavy rare earth element (HREE) that is part of the Lanthanide series of elements. Matamec's Kipawa Rare Earths JV, its flagship project being developed in partnership with Resources Qubec, is one of North America's most advanced rare earths projects."

Also, the commodity sector appears to be gaining some strength and this will bode well and let's not forget their little gold claim and partner.

So you see, although, we've had slow trading sessions over the past year, but we have never truly been out of the realm of not having a viable rare earth company. The business model is real and the future is bright.

I am still in the belief that the turnaround is upon us and 2017 will become a pivot point on us moving forward.

This is one of a very few pennystocks that I consider to be an investment quality issue and should be in everybody's portfolio regardless of the performance over the last few years.

Yes many of us were met with a timing sequence, but I think that is now behind us. Let's not forget, this issue is a mining issue and the last few years were, to say the least, a dismal sector to be in.

Whatever happens, I am buying at this level and consider it a great point for new investors to take part. This company is undervalued and in time it will benefit us in the long term.

Have a good day

varok

Although it may take time for the many possible commercial applications to come to market, the discovery of the ability to save a single bit of data on a holmium atom represents a quantum leap in data storage technology and offers great potential for computing. An entire computer's hard drive could possibly be stored in a piece of jewelry or sewn into a garment, for example, and smaller data storage devices could greatly improve the evolving "internet of things" applications, where more and more everyday items can be connected to the Internet

Read more at http://www.stockhouse.com/news/press-releases/2017/03/15/matamec-welcomes-breakthrough-discovery-ibm-scientists-store-1-bit-of-data-on-a#0dg1KJKMTXASZPkS.99

News today seems pretty big imo, it seems that Holmium could be EXTREMELY valuable in the very near future....

Matamec Consolidates its Gold Position by Signing a Letter of Intent to Acquire Two Gold Properties in Quebec

Casa Berardi South, just south of the Casa Berardi Mine, and Troilus North, on the Northern Extension of the former Troilus Mine

MONTRÉAL, QUÉBEC--(Marketwired - Sept. 12, 2016) - Matamec Explorations Inc. ("Matamec" or the "Company") (TSX VENTURE:MAT)(OTCQX:MHREF) is pleased to announce the signature of a memo of understanding (MoU) by means of which it may acquire the Casa Berardi South and Troilus North gold properties from Greg Explorations Inc. (Greg), subject to certain conditions (see the MoU section for more details).

With the properties it already owns, including the new Opinaca Gold West property, Matamec will hold an interest in the following gold properties (see Figure 1 for their locations):

•Near the Casa Berardi Mine, owned and operated by Hecla Québec, north of La Sarre in northwest Québec: The Casa Berardi South property (acquired at 100%) captures a rock structure that is parallel and analogous to the Casa Berardi mine for 15 kilometres, and has been relatively unexplored to date - see the Casa Berardi South Property section and Figure 2;

•In the northwest extension of of the former Troilus Mine host package, located northwest of Chibougamau, Québec: The Troilus North property (100%) straddles a northeastern extension of the volcanic sequence hosting the Troilus Mine deposit for about 10km - see the Troilus North Property section and Figure 3;

•In the geological setting that hosts the Éléonore mine near James Bay in Québec: ?The Sakami property, 50% owned by Matamec, covers the Opinaca-La Grande geological contact, and the results of its Summer 2016 drilling campaign in the La Pointe Zone included 4.94 g/t Au over 21.05m - see the Sakami and Opinaca Gold West section and Figure 4;

?The new Opinaca Gold West property, 100% owned by Matamec, is situated along the same geological formation as Goldcorp's Éléonore gold mine where new gold potential along this trend has been identified. The claims block covers a series of geochemical gold-arsenic anomalies and geological elements that suggests the presence of a gold bearing system along approximately 40 km - see the Sakami and Opinaca Gold West section and Figure 4;

•Along the stratigraphic rock formations east of the Hoyle Pond Mine owned and operated by Goldcorp in Timmins, Ontario: Matamec holds a royalty of 1% NSR on the new HMR property, a 50% interest in the Matheson JV property, and a 100% interest in the Pelangio property - see the HMR/MJV/Pelangio Properties section and Figure 5;

•In the promising setting of the historic Candego mine, in the Gaspé region: The Valmont property hosts Pb-Zn-Ag-Au mineralization from the historic Candego mine and several gold-bearing vein systems - see Valmont Property section and Figure 1.

"The gold potential associated with the geology of these properties, located across Quebec and in Ontario, is promising," said André Gauthier, President and CEO of Matamec. "Their quality and scope strengthens the company's gold portfolio and its position in the market."

Figure 1 "Locations of Matamec's Gold Properties" is available at the following link: http://media3.marketwire.com/docs/1068995a_Fig1.jpg

A. Casa Berardi South Property

The Casa Berardi South property covers 10,000 hectares (ha) in 180 claims. The property is accessible by a main gravel road and by a network of forestry roads. The property northern limit is located 2km south of the Casa Berardi Mine owned by Hecla Mining. The accumulated gold production at the mine at the end of 2015 reached 1.966 million ounces of gold and the deposit retains proven reserves of 2.119 million tonnes (mt) of 3.41 g/t Au and probable reserves of 8.104 mt of 4.34 g/t Au (http://www.hecla-mining.com/casa-berardi).

The property's appeal lies in its repetition of the structural and lithological context that characterizes the Casa Berardi deposit. To the south of the deposit, an assemblage of volcanic and sedimentary rocks could host a gold bearing structure parallel to the known deposit. The area has seen very limited exploration to date. The reader is cautioned that there is no guarantee that the grade and style of mineralization identified on the Casa Berardi deposit will be identified at the Company's Casa Berardi South property.

The target types for this property include vein systems and disseminated sulphide hosted in graphitic sediments, conglomerates and iron formations, mainly along stratigraphic contacts.

Initial exploration work will seek to compile information from historical assessment reports to identify showings of mineralization and anomalous gold zones.

Figure 2 "Casa Berardi South Property" is available at the following link: http://media3.marketwire.com/docs/1068995a_Fig2.jpg

B. Troilus North Property

The Troilus North property has 7,700 hectares in 143 claims following the northeast extension of the former Troilus Mine structure. The property is accessible via a 150-km gravel road that links the city of Chibougamau, in northern Québec, to the former Troilus mine site.

The property covers a large granite batholith surrounded by the volcanic sequence hosting the gold-copper Troilus Mine deposit. About 2 million ounces of gold and 70,000 tonnes of copper were produced from open pits between 1995 and 2010 from Troilus (http://sulliden.com/investors/news/_2016/).

Data mining in public files combined with geophysical and remote sensing data processing were recently completed as part of the acquisition process. The new exploration model suggests an extension of the Troilus structure to the northeast for about 10 kilometres inside the Troilus North property. The reader is cautioned that there is no guarantee that the mineralization identified on the Troilus Mine deposit will be identified at the Company's Troilus North property.

Sulliden Mining Capital currently owns the Troilus Mine mining lease, with the objective to restart an underground operation based on a new resources estimate (Technical Report on the Troilus Gold-Copper Mine Mineral Resources Estimate, Québec, Canada, June 2016).

Figure 3 "Troilus North Property" is available at the following link: http://media3.marketwire.com/docs/1068995a_Fig3.jpg

C. Sakami and Opinaca Gold West Properties

Sakami Property

The property is held at 50% and covers a major geological contact between two very favourable sub- provinces for hosting gold deposits. The geology of this geological contact includes Opinaca metasedimentary rocks and the mafic volcanics and iron formations of the La Grande in association with a major deformation zone, particularly along the tectonic contact between the sub-provinces of La Grande-Opinaca. The mineralization style and tectonic setting have many similarities with the Éléonore mine owned by Goldcorp and the Cheechoo prospect, held by Sirios Resources (Please see the April 25, 2016 press release for more information).

The summer 2016 exploration campaign revealed that Vein 25 increases in thickness and grade to the northwest and remains wide open in this direction. The results from this summer include 43.30 m of 2.21 g/t Au and 21.05 m of 4.95 g/t Au, in drill holes PT-16-91 and PT-16-92 respectively (Please see the September 8, 2016 press release for more information).

In addition to the drilling already described, the 2016 field work included a total of 210 km of geophysical survey lines in the La Pointe, Île and JR West sectors, and a mapping and prospecting campaign in the Péninsule, Île and JR West sectors. The results of this exploration work will be shared as soon as they become available.

Opinaca Gold West Property

The Opinaca Gold West property includes 289 claims covering 15,000 hectares. The James Bay Road crosses the property. The claims block controls over 40 kilometres of prospective volcano-sedimentary belt in a generally east-west orientation.

At a regional scale, the property straddles a major magnetic contrast connected with the Goldcorp Éléonore Mine (proven and probable reserves of 4.17 million tonnes (mt) at 6.49 g/t Au for 0.87 million ounces (moz) Au and 24.15 mt at 5.76 g/t Au for 4.48 moz Au respectively*) located about 50 kilometres to the east. The reader is cautioned that there is no guarantee that mineralization on the Éléonore property is indicative of the type of mineralization on the Opinaca Gold West property.

Historical works have identified geological indicators of a gold bearing system such as arsenopyrite and tourmaline. High gold-arsenic concentrations were also observed from lake sediments in the property area.

* (Mineral Reserves And Resources As of December 31, 2015. http://www.goldcorp.com/English/Investor-Resources/Reserves-and-Resources/default.aspx).

Figure 4 "Sakami and Opinaca Gold West Properties" is available at the following link: http://media3.marketwire.com/docs/1068995a_Fig4.jpg

D. HMR/MJV/Pelangio Property

The Matheson JV held at 50% and the Matheson-Pelangio (100%) properties lie along the stratigraphic rock assemblages which is the host to many of the gold deposits in the Timmins mining camp. This large property contains several targets defined by till drilling campaigns that have not been sufficiently drill tested.

New Hoyle Royalties-Matheson Property (HMR)

Following the PREAA announced on March 2nd, 2016 with Glencore and Goldcorp, Matamec now holds royalties of 1% NSR on the HMR property. On April 16, Matamec reviewed and restated the gold potential of this property. Based on its review, Matamec believes that the mineralized series of gold veins being mined and processed at Goldcorp's Hoyle Pond Gold Mine trends onto the HMR property. The similarity between the rock sequences, structural interpretation and mineralized zones occurring on the Mill Creek/Colbert Zone and at the Hoyle Pond Gold Mine is striking. These two zones are on either side of the HMR, with the prospective geological and structural packages trending onto it from both directions. The April 16, 2016 press release summarizes the publicly available information that forms the basis of this conclusion.

Figure 5 "HMR/MJV/Pelangio Properties" is available at the following link: http://media3.marketwire.com/docs/1068995a_Fig5.jpg

E. Valmont Property

The Valmont property is 3,895 hectares in size and is located 120 kilometres to the west of the city of Gaspé. The Pb-Zn-Ag-Au mineralization from the historic Candego mine are associated with the subvertical ESE trending Candego shear zone. Historic production is stated at 68,497 tonnes of 6.35% Pb, 4.28% Zn, 170 g/t Ag et and 0.68 g/t Au. Several gold bearing vein systems have been identified on the property: Cromar, Marsoui and St- Francois. A new data compilation is ongoing.

Guy Desharnais, P.Geo., Ph.D. (OGQ No.1141), is a Qualified Person as per NI 43-101; he is employed by SGS Canada Inc., is independent of Matamec, and has reviewed and approved the technical content of this press release.

Memorandum of Understanding (MoU)

Signed on September 12 between Matamec and Greg, the MoU targets an increased collaboration between the two companies to meet the following objectives:

1.To allow Matamec to increase its portfolio of gold properties in geological settings linked to deposits or mines in production in Province of Québec by the acquisition of certain of Greg's gold properties, and to proceed with financing thereafter. To date, the parties have agreed that the North Troilus and South Casa Berardi held by Greg will be part of this transaction (the "gold projects");

2.To transfer energy-related projects of Matamec and Greg into a new mining company (NewCo), to be constituted, in which Matamec will be the main shareholder. This new company will be exclusively dedicated to exploration and development of industrial minerals deposits related to energy.

To achieve this objective, an update of the technical reports (prepared in compliance with the National Instrument 43-101 for the Standards of Disclosure for Mineral Projects) and an independent valuation of each property of Matamec and Greg will be completed this fall. This will allow the parties to agree on the fair market value (FMV) of the gold projects that will be transferred by Greg to Matamec and the energy-related projects which will be transferred by the parties to NewCo. The planned acquisition of the Greg gold projects will probably be completed through the issuance of shares of Matamec on the main basis of the ratio of the FMV of these properties on all properties of Matamec and Greg. As for the acquisition of energy related projects by NewCo, the terms remain subject to negotiation between the parties. The final terms of these transactions must be confirmed in the near future by the parties and remain subject to certain conditions such as, notably, the approval from each Board of Directors of Matamec and Greg as well as regulatory approval a new mining company (NewCo) to be formed in Matamec's case.

The parties have agreed on a timetable targeting, especially, (i) identification of the gold projects and industrial mineral projects, as well as the confirmation of their value, by end of September 2016; (ii) the incorporation of NewCo and the execution of the required agreements to put in place the different transactions targeted by the MoU by the end of October 2016; and (iii) put in place the initial financing of NewCo by the end of November 2016.

The agreement between Matamec and Greg aims to establish a well-experienced exploration and development mining team in order to (i) demonstrate the gold potential of Matamec and (ii) support, within a new company, the exploration and development of industrial mineral deposits related to energy.

About Matamec

Matamec Explorations Inc. is a junior mining exploration company whose main focus is in developing the Kipawa HREE JV deposit owned at 72% by the Company and 28% by Ressources Québec (acting as agent of the Government of Québec); Toyota Tsusho Corp. (Nagoya, Japan) holds a 10% royalty on net profit in the deposit. Furthermore, the Company is exploring more than 35 km of strike length in the Kipawa Alkalic Complex for rare earths-yttrium-zirconium-niobium-tantalum mineralization on its Zeus property.

The Company is also exploring for gold, base metals and platinum group metals. In Québec, the Company is exploring for strategic metals such as lithium, tantalum, and beryllium on its Tansim property and for precious and base metals on its Vulcain property.

Forward-looking information

This news release contains "forward-looking information" within the meaning of Canadian securities legislation. Generally, forward-looking statements can be identified by the use of forward-looking terminology such as "scheduled", "anticipates", "expects" or "does not expect", "pursue", "targeted", or "believes", or variations of such words and phrases that state that certain actions, events or results "may", "could", "would", "might" or "will" be taken, occur or be achieved. Forward-looking statements are based on assumptions management believes to be reasonable at the time such statements are made. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. Although Matamec has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. Factors that may cause actual results to differ materially from expected results described in forward-looking statements include, but are not limited to, those risk factors set out in the Company's year-end Management Discussion and Analysis dated December 31, 2015 and other disclosure documents available under the Company's profile at www.sedar.com. Forward-looking statements contained herein are made as of the date of this press release and Matamec disclaims any obligation to update any forward-looking statements, whether as a result of new information, future events or results or otherwise, except as required by applicable securities laws.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Follow us on Twitter: https://twitter.com/MatamecInc

Visit us on Facebook: https://www.facebook.com/MatamecInc

Andre Gauthier

President

514 844 5252

info@matamec.com

MONTRÉAL, QUEBEC--(Marketwired - Sept. 8, 2016) - Matamec Explorations Inc. ("Matamec" or the "Company") (TSX VENTURE:MAT)(OTCQX:MHREF) is pleased to announce its increased presence in the geological setting that hosts the Éléonore mine near James Bay in Quebec.

Matamec has acquired 100% of the Opinaca Gold West property for a lump sum of $68,852 with a 2% royalty that is redeemable for $500,000, payable to the vendor. The property is situated along the same geological formation as Goldcorp's Éléonore gold mine where new gold potential along this trend has been identified.

The Opinaca Gold West property includes 289 claims covering 15,000 hectares (see Figure 1). The James Bay Road crosses the property. The claims block controls over 40 kilometres of prospective volcano-sedimentary belt in a generally east-west orientation. It covers a series of geochemical gold-arsenic anomalies and geological elements that indicate the presence of a gold bearing system along approximately 40 km.

At the regional scale, the property straddles a major magnetic contrast connected with the Goldcorp Eleonore Mine (proven and probable reserves of 4.17 million tonnes (mt) at 6.49 g/t Au for 0.87 million ounces (moz) Au and 24.15 mt at 5.76 g/t Au for 4.48 moz Au respectively*) located about 50 kilometres to the east. The reader is cautioned that there is no guarantee that mineralization on the Éléonore property is indicative of the type of mineralization on the Opinaca Gold West property.

Historical works have identified geological indicators of a gold bearing system such as arsenopyrite and tourmaline. High gold-arsenic concentrations were also obtained from lake sediments in the property area.

* (Mineral Reserves And Resources As of December 31, 2015. http://www.goldcorp.com/English/Investor-Resources/Reserves-and-Resources/default.aspx)

"With the acquisition of the Opinaca Gold West property, Matamec is building on our conviction that the James Bay region still has lots of gold potential," said André Gauthier, President and CEO of Matamec. "The company's gold portfolio is growing significantly."

Along with this announcement, Matamec and Canada Strategic Metals (CSM) (TSX VENTURE:CJC)(FRANKFURT:YXEN)(OTCBB:CJCFF) are very pleased to report the latest drill results for the Sakami property. Drilling on the Northwest extension of Zone 25 (main zone) has returned an intersection of 1.87 g/t Au over 27.00 metres including 3.14 g/t Au over 5.00 metres, from hole PT-16-93 (see table below).

"These results from Zone 25, including those that have already been announced from the first two drill holes, are very encouraging for Matamec," said André Gauthier. "We look forward to receiving the remainder of the results from the Summer 2016 exploration campaign."

The result from PT-16-93 together with PT-16-91 and PT-16-92 confirm that Zone 25 increases in thickness and grade to the northwest (see Figures 2, 3, and 4). This lens remains wide open in this direction and we are very keen to test the continuity of this thick zone of gold mineralization in the next drill campaign. Note that the grade of the intervals are relatively consistent; there are no extreme grade assays that carry very low grade intervals. The very thick intervals and their relative position suggest a possible merging of Zone 22 and 25 in this direction, as illustrated in Figure 4.

The drilling of PT-16-96 and 97 confirms the mineralization trend to the extreme south east, and the lack of significant assay results in the remaining drill holes testifies to the complex geology occurring at this apparent fold nose on the La Pointe Peninsula. All significant results for the latest campaign are presented in the table below.

Table of mineralized intersections from 2016 drilling

Hole # From (m) To (m) Length * (m) Au (g/t)

PT-16-91** 165.20 208.50 43.30 2.21

Including 176.00 187.50 11.50 3.46

PT-16-92** 203.60 252.15 48.55 2.52

Including 206.95 228.00 21.05 4.94

Including 206.95 225.00 18.05 5.38

PT-16-93 252.00 279.00 27.00 1.87

Including 253.00 258.00 5.00 3.14

And Including 271.00 277.00 6.00 2.69

PT-16-94 NSV

PT-16-95 NSV

PT-16-96 124.00 125.00 1.00 1.73

PT-16-97 136.00 156.50 20.50 0.55

PT-16-98 NSV

PT-16-99 66.00 69.00 3.00 1.33

78.00 81.00 3.00 1.08

91.50 93.00 1.50 1.97

124.50 127.50 3.00 1.07

169.00 170.50 1.50 2.86

* The Company estimates the true width of the mineralized zone at 70 to 95% of the core length.

** Results already announced in a press release dated September 6, 2016.

Sectors Explored in the Summer 2016 Exploration Program

The 2016 Summer program covered 4 areas of the property, and included a drilling campaign of 9 holes totaling 2,058 m on the La Pointe sector. It also comprised a total of 210 km of geophysical survey lines in the La Pointe, Île and JR West sectors, and a mapping and prospecting campaign in the Péninsule, Île and JR West sectors. The remaining results of this exploration work will be shared as soon as they become available.

Guy Desharnais, P.Geo., Ph.D. (OGQ No.1141), is a Qualified Person as per NI 43-101; he reviewed and approved the technical content of this press release.

About Matamec

Matamec Explorations Inc. is a junior mining exploration company whose main focus is in developing the Kipawa HREE JV deposit owned at 72% by the Company and 28% by Ressources Québec (acting as agent of the Government of Québec); Toyota Tsusho Corp. (Nagoya, Japan) holds a 10% royalty on net profit in the deposit. Furthermore, the Company is exploring more than 35 km of strike length in the Kipawa Alkalic Complex for rare earths-yttrium-zirconium-niobium-tantalum mineralization on its Zeus property.

The Company is also exploring for gold, base metals and platinum group metals. Its gold portfolio includes the Hoyle-Matheson Royalties (see the March 2, 2016 and April 28, 2016 press releases), Matheson JV (MJV) and Pelangio properties located along strike and in close proximity to Goldcorp's Hoyle Pond Mine in the prolific gold mining camp of Timmins, Ontario. Matamec holds a 50% undivided interest in the MJV property and is its operator. In addition, the Company holds a 1% NSR royalty in the Montclerg Property located 48 km northeast of Timmins along the Pipestone Fault.

In Québec, the Company is exploring for strategic metals such as lithium, tantalum, and beryllium on its Tansim property and for precious and base metals on its Valmont and Vulcain properties.

This news release contains "forward-looking information" within the meaning of Canadian securities legislation. Generally, forward-looking statements can be identified by the use of forward-looking terminology such as "scheduled", "anticipates", "expects" or "does not expect", "pursue", "targeted", or "believes", or variations of such words and phrases that state that certain actions, events or results "may", "could", "would", "might" or "will" be taken, occur or be achieved. Forward-looking statements are based on assumptions management believes to be reasonable at the time such statements are made. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. Although Matamec has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. Factors that may cause actual results to differ materially from expected results described in forward-looking statements include, but are not limited to, those risk factors set out in the Company's year-end Management Discussion and Analysis dated December 31, 2015 and other disclosure documents available under the Company's profile at www.sedar.com. Forward-looking statements contained herein are made as of the date of this press release and Matamec disclaims any obligation to update any forward-looking statements, whether as a result of new information, future events or results or otherwise, except as required by applicable securities laws.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Figure 1 is available at the following address : http://media3.marketwire.com/docs/1068689a_Fig1.jpg

Figure 2 is available at the following address: http://media3.marketwire.com/docs/1068689a_Fig2.jpg

Figure 3 is available at the following address: http://media3.marketwire.com/docs/1068689a_Fig3.jpg

Figure 4 is available at the following address: http://media3.marketwire.com/docs/1068689a_Fig4.jpg

Follow us on Twitter: https://twitter.com/MatamecInc

Visit us on Facebook: https://www.facebook.com/MatamecInc

Andre Gauthier

President

(514) 844-5252

info@matamec.com

Press Release: Matamec Announces that Canada Strategic Metals Has Acquired 50% Interest in the Sakami Property as the Sakami Summer Exploration Program Comes to a Close

11:14 am ET August 18, 2016 (Dow Jones) Print

Matamec Announces that Canada Strategic Metals Has Acquired 50% Interest in the Sakami Property as the Sakami Summer Exploration Program Comes to a Close

MONTRÉAL, QUÉBEC--(Marketwired - Aug. 18, 2016) - Matamec Explorations Inc. ("Matamec" or the "Company") (TSX VENTURE:MAT)(OTCQX:MHREF) and Canada Strategic Metals ("CSM") (TSX VENTURE:CJC)(FRANKFURT:YXEN)(OTCBB:CJCFF) are pleased to announce that the Summer 2016 Exploration Program at the Sakami property has been completed (see June 28th, 2016 press release). With the completion of this exploration program, CSM has fulfilled its obligations as per the option agreement signed on August 16, 2013, and has acquired a 50% interest in the Sakami property, which has been recently enlarged with the addition of 93 claim cells (see Figure 1 : Map of the Sakami Property).

Areas Explored During the 2016 Summer Exploration Program

The 2016 Summer program covered 4 areas of the property, and included a drilling campaign of 9 holes totaling 2,058 m on the La Pointe sector. It also comprised a total of 210 km of geophysical survey lines in the La Pointe, Île and JR West sectors, and a mapping and prospecting campaign in the Péninsule, Île and JR West sectors. The results of this exploration work will be shared as soon as they become available.

Sakami Property Geology

The property covers a major geological contact between two sub-provinces that are very favourable for hosting gold deposits. This geological setting comprises the Opinaca sediments, the La Grande mafic volcanics, and iron formations in association with a strong deformation zone, notably near the tectonic contact of the La Grande-Opinaca sub-provinces. The mineralization style and tectonic setting share considerable similarities with the Eleonore mine held by Goldcorp (see figure 2: Regional Geology Map, and the July 6, 2016 press release).

Since the announcement of expanded mineralization of the Cheechoo deposit by Sirios Resources on March 29, we have seen several significant exploration budgets announced along this major tectonic boundary. These include exploration programs by Sirios Resources (April 22, 2016-5.5M$CAD), Midland Exploration with Osisko Exploration (June 16, 2016-1M$CAD), and Les Mines Opinaca with Eastmain Resources and Azimut Exploration (June 16, 2016-2M$CAD).

Guy Desharnais, P.Geo., Ph.D. (OGQ No.1141), is a Qualified Person as per NI 43-101; he reviewed and approved the technical content of this press release.

"In the current climate of renewed interest in gold exploration in James Bay, we are eagerly looking forward to receiving the results of the summer 2016 exploration campaign," said André Gauthier, President and CEO of Matamec. "It further enhances the depth and breadth of gold properties in the Company's portfolio, not only in James Bay but also in Timmins in Ontario, which effectively demonstrates that Matamec's strategic vision, 'From Gold to Rare Earths,' is an added value for shareholders of the Company."

Option Granted to CSM

On August 16, 2013, Matamec signed an option agreement with CSM in which the latter could acquire a 50% interest in the Sakami gold project by spending CAD$2,250,000 in exploration work and other conditions over a period of three (3) years. Now that CSM holds a 50% undivided interest in the Sakami property, it has 180 days to exercise its option to acquire an additional 20% interest in the property. To do so, it must issue 1,000,000 shares of CSM to Matamec, and complete an independent bankable feasibility study within the next five (5) years. During this period, CSM must spend a minimum of $2 million in exploration activities before the end of each year until the independent bankable feasibility study is completed.

About Matamec

Matamec Explorations Inc. is a junior mining exploration company whose main focus is in developing the Kipawa HREE JV deposit owned at 72% by the Company and 28% by Ressources Québec (acting as agent of the Government of Québec); Toyota Tsusho Corp. (Nagoya, Japan) holds a 10% royalty on net profit in the deposit. Furthermore, the Company is exploring more than 35 km of strike length in the Kipawa Alkalic Complex for rare earths-yttrium-zirconium-niobium-tantalum mineralization on its Zeus property.

The Company is also exploring for gold, base metals and platinum group metals. Its gold portfolio includes the Hoyle-Matheson Royalties (see the March 2, 2016 and April 28, 2016 press releases), Matheson JV (MJV) and Pelangio properties located along strike and in close proximity to Goldcorp's Hoyle Pond Mine in the prolific gold mining camp of Timmins, Ontario. Matamec holds a 50% undivided interest in the MJV property and is its operator. In addition, the Company holds a 1% NSR royalty in the Montclerg Property located 48 km northeast of Timmins along the Pipestone Fault.

In Québec, the Company is exploring for strategic metals such as lithium, tantalum, and beryllium on its Tansim property and for precious and base metals on its Valmont and Vulcain properties.

This news release contains "forward-looking information" within the meaning of Canadian securities legislation. Generally, forward-looking statements can be identified by the use of forward-looking terminology such as "scheduled", "anticipates", "expects" or "does not expect", "pursue", "targeted", or "believes", or variations of such words and phrases that state that certain actions, events or results "may", "could", "would", "might" or "will" be taken, occur or be achieved. Forward-looking statements are based on assumptions management believes to be reasonable at the time such statements are made. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. Although Matamec has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. Factors that may cause actual results to differ materially from expected results described in forward-looking statements include, but are not limited to, those risk factors set out in the Company's year-end Management Discussion and Analysis dated December 31, 2015 and other disclosure documents available under the Company's profile at www.sedar.com. Forward-looking statements contained herein are made as of the date of this press release and Matamec disclaims any obligation to update any forward-looking statements, whether as a result of new information, future events or results or otherwise, except as required by applicable securities laws.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Follow us on Twitter: https://twitter.com/MatamecInc

Visit us on Facebook: https://www.facebook.com/MatamecInc

Maps associated with this press release are available at the following addresses:

http://media3.marketwire.com/docs/160818_MAT_Sakami_Property_Claim_Cells_Fig1.pdf

http://media3.marketwire.com/docs/160818_MAT_Sakami_Property_Regional_Geological_Map_Fig2.jpg

Matamec Explorations inc.

Andre Gauthier

President

(514) 844-5252

info@matamec.com

The Sakami Summer Exploration Program Launches Amidst a Rush of Interest in Mineral Exploration Along the La Grande-Opinaca Tectonic Boundary in the Baie James Sector

12:23 pm ET July 6, 2016 (Market Wire) Print

MONTREAL, QUEBEC--(Marketwired - Jul 6, 2016) - Matamec Explorations inc. ("Matamec" or the "Company") (TSX VENTURE:MAT)(OTCQX:MHREF) and Canada Strategic Metals ("CSM") (TSX VENTURE:CJC)(FRANKFURT:YXEN)(OTCBB:CJCFF) are pleased to announce that the exploration program of almost CAD$700,000 that recently started on the Sakami property (see June 28th, 2016 press release), is taking place as a rush of interest in the mineral exploration is happening along the La Grande-Opinaca Tectonic Boundary in the Baie James Sector (See figure 1: Regional Geology).

Since the announcement of expanded mineralization of the Cheechoo deposit by Sirios Resources on March 29, we have seen several significant exploration budgets announced. These include exploration programs by Sirios Resources (April 22, 2016-5.5M$CAD), Midland Exploration with Osisko Exploration (June 16, 2016-1M$CAD), and Les Mines Opinaca with Eastmain Resources and Azimut Exploration (June 16, 2016-2M$CAD).

Sakami Property

Option Agreement - Sakami Property

On August 16, 2013, Matamec signed an option agreement with CSM in which the latter could acquire a 50% interest in the Sakami gold project by spending CAD$2,250,000 in exploration work and other conditions over a period of three (3) years.

Geology

The property covers a major geological contact between two sub-provinces that are very favourable for hosting gold deposits. This geological setting comprises the Opinaca sediments, the La Grande mafic volcanics, and iron formations in association with a strong deformation zone, notably near the tectonic contact of the La Grande-Opinaca sub-provinces. The mineralization style and tectonic setting share considerable similarities with the Eleonore mine held by Goldcorp (see April 4th and 25th, 2016 press releases).

Focus areas

The Summer 2016 program plans to test 4 separate areas, including a 2,000 m drill campaign on the La Pointe sector. Ground geophysics, mapping and prospecting around previously defined anomalies will be completed over the Péninsule, Île and JR sectors (see figure 2).

Significant gold potential in the La Pointe Zone

A 2,000 m drilling program is planned on the La Pointe area to extend Zone 25 to the northwest and southeast. The drilling program is also aimed at increasing the size of the main gold zone (Zone 25) to the west-northwest and the south-east, as well as its extension at depth. In addition, a stratigraphic exploration hole is planned in the south portion of La Pointe (see figure 3, Location of projected drilling holes.)

The most significant drillhole intervals of the La Pointe zone are located along the northwest limit of the model, which remains open in that direction. Recent remodeling of the La Pointe zone revealed two superimposed main structures (veins 22 and 25), which have a relatively predictable continuity, as well as potential for additional veins (see figure 4: Vertical section). These mineralized horizons are sub-parallel to the major tectonic contact, which span more than 15 km on the Sakami property.

Guy Desharnais, P.Geo., Ph.D. (OGQ No.1141), is a Qualified Person as per NI 43-101; he reviewed and approved the technical content of this press release.

"Since 2013, Matamec has been progressing well on this gold project. We have good reason to expect continued success with this Summer 2016 exploration program," said André Gauthier, President and CEO of Matamec. "Moreover, the breadth of the Company's gold property portfolio clearly demonstrates that Matamec's strategy, "From gold to rare earths," is an added value for shareholders of the company".

About Matamec

Matamec Explorations Inc. is a junior mining exploration company whose main focus is in developing the Kipawa HREE JV deposit owned at 72% by the Company and 28% by Ressources Québec (acting as agent of the Government of Québec); Toyota Tsusho Corp. (Nagoya, Japan) holds a 10% royalty on net profit in the deposit. Furthermore, the Company is exploring more than 35 km of strike length in the Kipawa Alkalic Complex for rare earths-yttrium-zirconium-niobium-tantalum mineralization on its Zeus property.

The Company is also exploring for gold, base metals and platinum group metals. Its gold portfolio includes the Hoyle-Matheson Royalties, Matheson JV and Pelangio properties located along strike and in close proximity to the Hoyle Pond Mine in the prolific gold mining camp of Timmins, Ontario. The Company holds a 50% undivided interest in the Matheson JV, with International Explorers and Prospectors inc. holding the remaining 50% undivided interest. The Company is the operator of the MJV. MJV property consists of 60 mining titles. In addition, the Company holds a 1% NSR royalty in the Montclerg Property located 48 km northeast of Timmins along the Pipestone Fault.

In Québec, the Company is exploring for strategic metals such as lithium, tantalum and beryllium on its Tansim property and for precious and base metals on its Sakami, Valmont and Vulcain properties.

This news release contains "forward-looking information" within the meaning of Canadian securities legislation. Generally, forward-looking statements can be identified by the use of forward-looking terminology such as "scheduled", "anticipates", "expects" or "does not expect", "pursue", "targeted", or "believes", or variations of such words and phrases that state that certain actions, events or results "may", "could", "would", "might" or "will" be taken, occur or be achieved. Forward-looking statements are based on assumptions management believes to be reasonable at the time such statements are made. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. Although Matamec has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. Factors that may cause actual results to differ materially from expected results described in forward-looking statements include, but are not limited to, those risk factors set out in the Company's year-end Management Discussion and Analysis dated December 31, 2015 and other disclosure documents available under the Company's profile at www.sedar.com. Forward-looking statements contained herein are made as of the date of this press release and Matamec disclaims any obligation to update any forward-looking statements, whether as a result of new information, future events or results or otherwise, except as required by applicable securities laws.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Figures 1 to 4 are available at the following link: http://media3.marketwire.com/docs/1061713aFig.pdf

Follow us on Twitter: https://twitter.com/MatamecInc

Visit us on Facebook: https://www.facebook.com/MatamecInc

Andre Gauthier, President (514) 844-5252 info@matamec.com

Matamec Provides an Update to the Kipawa Rare Earths Joint Venture Project

MONTREAL, QUEBEC--(Marketwired - June 20, 2016) - Matamec Explorations Inc. (« Matamec » or the « Company ») (TSX VENTURE:MAT)(OTCQX:MHREF) is very pleased to announce that its 2015-2017 objectives are being achieved as planned for the Kipawa rare earths joint venture project ("the JV"), of which 72% is owned by Matamec. At the formation of the JV in January 2015, the joint venture held funds of $ 4M CAD. As of March 31st 2016, the JV has invested $1,970,000 CAD in reaching the objectives. The joint venture plans to invest the remaining $2,030,000 CAD over the next year in pursuit of its 2015-2017 objectives.

In the context of sustainable development, the success of the Kipawa rare earth project is contingent upon the completion of the following four undertakings: developing a technically robust metallurgical process flowsheet; achieving economic viability for the project; reaching environmental objectives; and obtaining social acceptability. The 2015-2017 objectives were established accordingly as follows:

1.Optimize metallurgical flowsheet;

2.Demonstrate the recovery of rare earths from silicate minerals on an industrial scale;

3.Evaluate opportunities to reduce the environmental footprint of the project;

4.Update Feasibility Study, previously published in October 2013;

5.Continue the social acceptance process with indigenous communities and local populations involved in the project;

6.Continue discussions with strategic financial and industrial partners.

For further information, we invite you to consult the various management reports that Matamec has filed with SEDAR for the Kipawa rare earth Joint Venture project, as well as the information that has been and will continue to be posted on Matamec's website.

About Matamec

Matamec Explorations Inc. is a junior mining exploration company whose main focus is in developing the Kipawa HREE JV deposit owned at 72% by the Company and 28% by Ressources Québec (acting as agent of the Government of Québec); Toyota Tsusho Corp. (Nagoya, Japan) holds a 10% royalty on net profit in the deposit. Furthermore, the Company is exploring more than 35 km of strike length in the Kipawa Alkalic Complex for rare earths-yttrium-zirconium-niobium-tantalum mineralization on its Zeus property.

The Company is also exploring for gold, base metals and platinum group metals. Its gold portfolio includes the Hoyle-Matheson Royalties, Matheson JV and Pelangio properties located along strike and in close proximity to the Hoyle Pond Mine in the prolific gold mining camp of Timmins, Ontario. The Company holds a 50% undivided interest in the Matheson JV, with International Explorers and Prospectors inc. holding the remaining 50% undivided interest. The Company is the operator of the MJV. MJV property consists of 60 mining titles. In addition, the Company holds a 1% NSR royalty in the Montclerg Property located 48 km northeast of Timmins along the Pipestone Fault.

In Québec, the Company is exploring for strategic metals such as lithium, tantalum and beryllium on its Tansim property and for precious and base metals on its Sakami, Valmont and Vulcain properties.

In August 2013, Matamec signed an option agreement where Canada Strategic Metals ("CSM") can acquire an interest of up to 50% in the Sakami gold project, located in the James Bay region of northern Quebec, by committing CAD$2.25 million in exploration work within 3 years. Today, CSM has spent around CAD$1,600,000, with $695,000 remaining to be spent before August 16, 2016. One of the four areas explored for gold on the Sakami property, the La Pointe zone, shows evidence of significant gold potential, as reported in the last press release dated April 4, 2016.

This news release contains "forward-looking information" within the meaning of Canadian securities legislation. Generally, forward-looking statements can be identified by the use of forward-looking terminology such as "scheduled", "anticipates", "expects" or "does not expect", "pursue", "targeted", or "believes", or variations of such words and phrases that state that certain actions, events or results "may", "could", "would", "might" or "will" be taken, occur or be achieved. Forward-looking statements are based on assumptions management believes to be reasonable at the time such statements are made. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. Although Matamec has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. Factors that may cause actual results to differ materially from expected results described in forward-looking statements include, but are not limited to, those risk factors set out in the Company's year-end Management Discussion and Analysis dated December 31, 2014 and other disclosure documents available under the Company's profile at www.sedar.com. Forward-looking statements contained herein are made as of the date of this press release and Matamec disclaims any obligation to update any forward-looking statements, whether as a result of new information, future events or results or otherwise, except as required by applicable securities laws.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Follow us on Twitter: https://twitter.com/MatamecInc

Visit us on Facebook: https://www.facebook.com/MatamecInc

Andre Gauthier, President

(514) 844-5252

info@matamec.com

Again right on Varok.

Good to see someone with the balls to make bold predictions.

Monitoring this stock closely.

Looking forward to seeing OTC action rev up.

MHREF - Another great week.

Again, I'm not talking about the OTCBB exchange on this issue. I'm referring to the TSX exchange where most of the volume is making extreme headway.

Remember, this issue is a sleeper, meaning the interest is just now taking notice.

On April 4th at the open the price was sitting at .035 on the OTCBB and now at the end of April we are sitting at .053. This is an increase of 51%.

Friday the close on the TSX was .06 a 52 week high on huge volume of 543K.

I predict that this issue will hit .10 within the next week or two giving it a fair value of

$14m MC.

Remember, there are no shares available and it must go higher.

Have a good day

varok

Indeed Mr. Fmeded.

You know the saying. "If they build it they will come".

Right now all the action is on the TXS exchange and volume is increasing every day.

We will get our day very shortly.

Large blocks indicates that big money is flowing in.

One thing for sure, this issue isn't going to need 3-5 million shares to make a huge spike. Oh we will get that volume, but I believe, since shares are non-existent, the MM will let it run for a possible double and then entice sellers. They (MM) will be forced to play on momentum, not by their rules, but the rules of science in levity. Gravity of inversion is the one area that MM can't control and will be forced to play into an arena that is controlled by anxiety and emotion of a stock that has gone ballistic. Now of course this scenario requires the company to maintain a handle on the O/S in the interim.

Have a good day

varok

Right on Varok - seems only you and me truly believe in this one.

I am taking any opportunity to add.

To me this is already a real company - I mean after all why would a huge Japanese conglomerate (Toyota) sign up to a deal with some BS fake mining company ?? (Doesn't make any sense).

The PR to watch for is the issue with First Nation.

There is no doubt that First Nation will collaborate with MHREF and once this is announced, you will see a huge spike and the reason why I say this, is because there are just NO shares available.

This company has been in R%D for the last five years without selling shares to stay afloat and this makes this penny play a real company.

Their main project or claim has completed all it's assaying and environmental concerns and now it's just moving into operational phase which is scheduled for 3rd/4th qtr. this year.

I see target .10 on the announcement of First Nation and then on to .20 above once we move into operational stage.

Also consider the claims portfolio which is considerable and yet to move into R%D.

Time to add.

Have a good day

varok

There is gold is them thare hills.

Oh yes this baby is gonna explode when the rare earths get going later in the year...

My take on the future of Matamec

Good Afternoon,

Every now and then comes along a pinksheet or pennystock that has huge potential. Now I come from this mindset after 20 years of playing the penny-arcade and from my professional experience of having my own business as a corporate profiler and Merger and Acquisitions for the last 16 years.

Trading pennystocks is an art and science that requires an absolute discipline in understanding the nature of pennystocks. Trading in this venue is not for most and from history's standpoint most (98%) of all pennystocks, fail or flounder at the bottom to never return.

Now we have in Matamec a truly well run and in my belief a pennystock that has long-term investment potential. I have never considered a pennystock as an investment, but a mechanism to build wealth by trading and not holding to augment your earnings into investment grade securities.

I see huge upside with MHREF as we move closer to the actual operational stage.

The company so far has been extremely discipline in controlling the issue of shares or maintaining a lid on the execution or retailing other wise known as diluting the pool by running the operational stage, Administration and R&D. This is very positive and is what drags down most pennystocks and leaves investors holding worthless stock to never be able to recoup their principle investment. This company, so far is and appears to have shareholders interest in mind and that is the beginning to feel comfortable with your investment.

It doesn't surprise me that we are still lingering down in the subpennies, but eventually this will change as we move forward.

As the world moves into a renewable source for our energy needs the Kipawa project with Toyota as a partner is only going to enhance our investment that will commend credibility and as such, so will the investment for us shareholders.

As the company has noted from their analysis, the Kipawa project is a 2. $b recoverable mining project over a period of 15 years.

So when we break this down to actual revenue per year, it is 16 $m.

Now I'm not going into the operational costs since this part still has to be determined and giving actual numbers may prove to be unproductive at this time, but the company has mentioned in one of their past statements that a 25 $m capital outlay needs to be obtained. This original capital expenditure is only the beginning, but still well within making this enterprise a profitable venture for us and the company.

Currently our market cap is under 1 $m with 120m O/S and generally is within the scope of pennystock companies that truly have a business model.

As we move forward going into 2015 and closer to operational stage, which I believe to be around 2016 when we will be in full production the share price will start it's climb and I expect this to happen by the end of this year or the spring of 2015.

Currently the company maintains a burn rate of 12 $k per month , but we can count on this to drastically to go up once we go into operational stage, but with a potential of 16 $m per year of revenue or 1 $m per month, one has to agree that we are looking at an eventual considerable multiple increase in the share price.

Of course, much of this rise in the share price will be dependant upon the financial package that the company needs to secure it's capital needs to move into operational stage, but still, we should see a significant increase to at least 10 fold from the current price of .07.

One can reasonably be comfortable to the understanding that a major price hike is in the future and if the timeline on actual operational and the capital financial package is made public, we will see a move by the end of this year going into spring.

I see the first point of resistance on the share price to be around .25 and this will give us a MC of 3 $m, still well below the fair value. I am not looking at PE ratio since pennystock companies generally are never tabulated on PE, but straight accounting. I expect this movement to begin near the end of 2014 through the end of spring 2015 since the winter months well probably have very little impact.

With 16 $m in potential revenue for the first year of operation expected for 2016, but 2017, should allow for us to have a share price to be well over 1.00$. Again, of course this is dependant upon the financial package and how it is laid out with the equity end of the deal.

But let's assume that our O/S move up from 120m to 250m, even at 250 O/S one can see that under the current share price of .07 is still well under the fair value of MC 2 $m. Even at .25 the MC will be 6 $m still well under fair value if the figures of retrieval reserves is based on 16 $m per year.

If the 16 $m achievable resources is met and not mentioning the actual burn at the time during operation we could very well command a share price of .65 giving a MC of 16 $m straight up accounting without a PE ratio calculated. So one can see definitely .50 without any problem.

Now you must take into acct the gold aspect of other claims. This needs to be calculated into the overall worth and the other claims yet still to be realized with respect to feasibility and operational costs to profitability assessment.

With the Kipawa project we should bode well on it's own merit and adding the other assets (claims) we can commend a share price of well over a $1.00 in the years to come and I believe this company will eventually move out of the pennyarcade and become a true investment grade company.

I recommend this a buy at the current price of .07 and under .13. Always do your due diligence and never invest more than you can lose.

Have a good day

varok

Canada Strategic Metals Inc.: Regional Setting of the Sakami Gold Property

9:32 am ET April 25, 2016 (Market Wire) Print

Canada Strategic Metals Inc. ("Canada Strategic Metals" or "the Company") (TSX VENTURE: CJC)(FRANKFURT: YXEN)(OTCBB: CJCFF) and Matamec Explorations Inc. (TSX VENTURE: MAT)(OTCQX: MHREF) are pleased to announce that the La Pointe Zone of the Sakami property shows evidence of significant gold potential. The property covers a major geological contact between two sub-provinces that are very favorable for hosting gold deposits. This geological setting comprises the Opinaca sediments, the La Grande mafic volcanics, and iron formations in association with a strong deformation zone, notably near the tectonic contact of the La Grande-Opinaca sub-provinces. The mineralization style and tectonic setting share considerable similarities with the Eleonore mine held by Goldcorp and the Cheechoo showing held by Sirios Resources, such as :

-- The mineralization associated with silicified paragneiss containing fine

quartz veinlets.

-- An alteration of quartz and brown tourmaline with minor arsenopyrite

mineralization.

-- An association of gold mineralization with a very proximal tonalite

intrusion.

-- The presence of gold mineralization associated with silicified

paragneiss of the Opinaca basin, including fold structures.

The reader is cautioned that there is no guarantee that mineralization of the grade reported on the Cheechoo deposit will be identified on the Company's Sakami project.

Recently, Sirios Resources announced significant gold results on the Cheechoo project with an intersection of 12.08 g/t Au over 20.3 meters (see press release of March 29, 2016 by Sirios Resources), as well as the closing of a private placement with Goldcorp in the amount of $ 962,000 (see press release of February 23, 2016).

Significant gold potential in the La Pointe Zone (Sakami Property)