News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

active long

navycmdr

![]()

active long

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

active long

Freddie Mac mortgage portfolio is

now $3.496 Trillion - it increased

+3.2% in March annual rate ....

Fannie Mae book of business continues slump in March

Apr. 25, 2024 -Federal National Mortgage Association (FNMA) StockFMCCBy: Max Gottlich, SA News Editor

https://seekingalpha.com/news/4094526-fannie-mae-book-of-business-continues-slump-in-march

$Booom ! Freddie Mac mortgage portfolio

increases at 3.2% annual rate in March

https://seekingalpha.com/news/4094592-freddie-mac-mortgage-portfolio-increases-at-32-annual-rate-in-march?mailingid=35163240&messageid=2900&serial=35163240.1181&source=email_2900&utm_campaign=rta-stock-news&utm_content=link-3&utm_medium=email&utm_source=seeking_alpha&utm_term=35163240.1181

Federal Home Loan Mortgage Corporation

(FMCC) | By: Liz Kiesche, SA News Editor

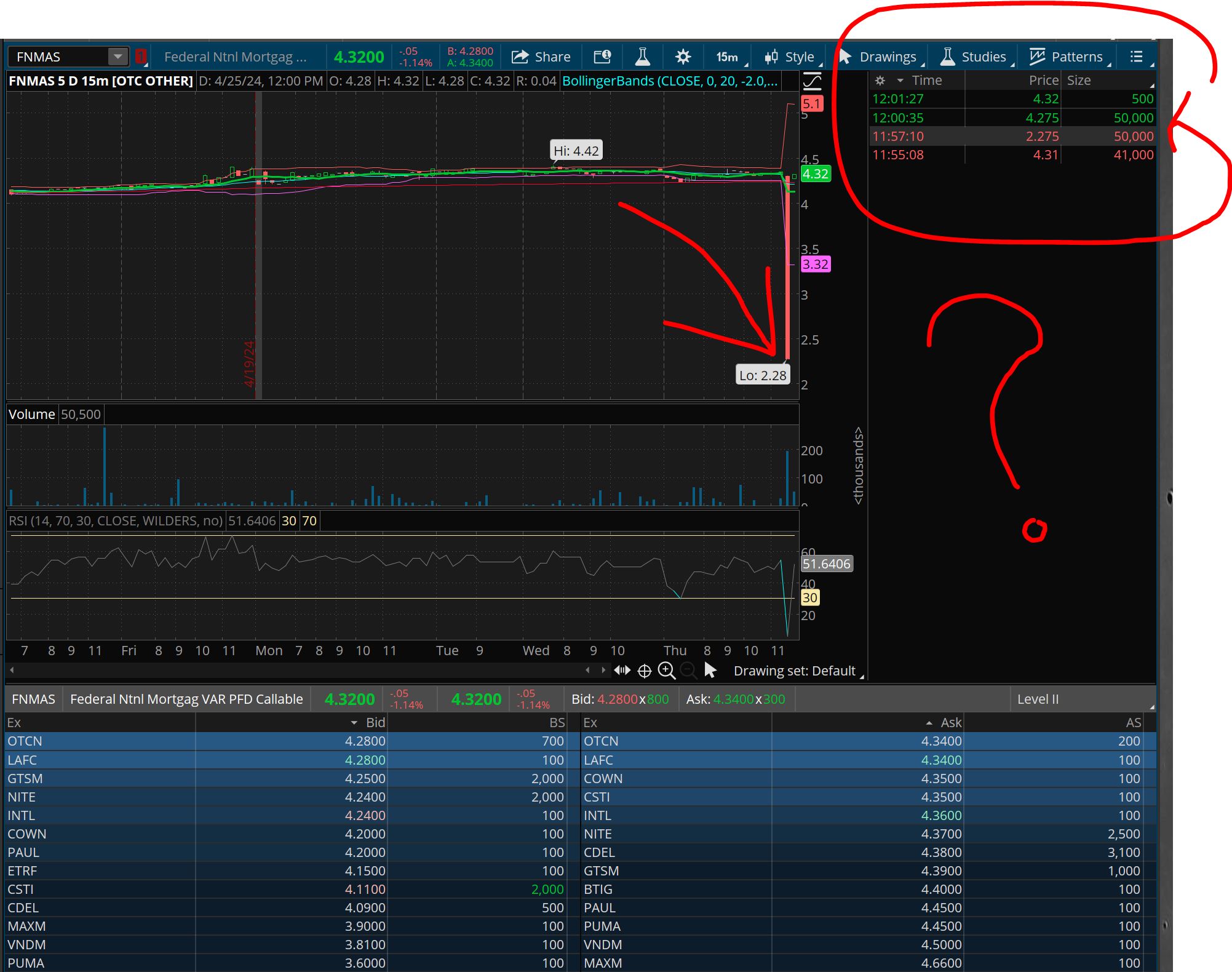

what jus traded happened to FNMAS ???

50,000 shares @ $2.275 ? -$2.15 ?

major TANK ?? fat finger mistake ? dunno but CRAZY

Are credit bureaus, housing groups in cahoots to kill @FICO scores? https://t.co/1MGIA1SUts | So why did the major credit bureaus raise the cost of buying credit scores for mortgages?? Because they can and @joeBiden says not a word.... @Experian_US

— Richard Christopher Whalen (@rcwhalen) April 25, 2024

Fannie Mae Housing Forecast thru 2025 ....

Releasing the GSEs from conservatorship into an offering, with a consent decree defining their allowable ROE, periodic commitment fee, etc, would go a long way towards helping @POTUS address #HPI, the @federalreserve manage their MBS rolloff & in supporting market liquidity.

— joshua rosner (@JoshRosner) April 16, 2024

1) Fannie and Freddie had an implied guarantee for years without impact to ratings 2) today they would exit with a periodic commitment fee that provides a stand-by line behind significant statutory and regulatory capital. It seems Chris is playing for the greedy asset managers…

— joshua rosner (@JoshRosner) April 15, 2024

Newly leaked video reveals grueling 3rd amendment negotiations between Ed DeMarco and Tim Geithner

— Matt Hill (@hill_matt) April 4, 2024

pic.twitter.com/iB6acdCEt2

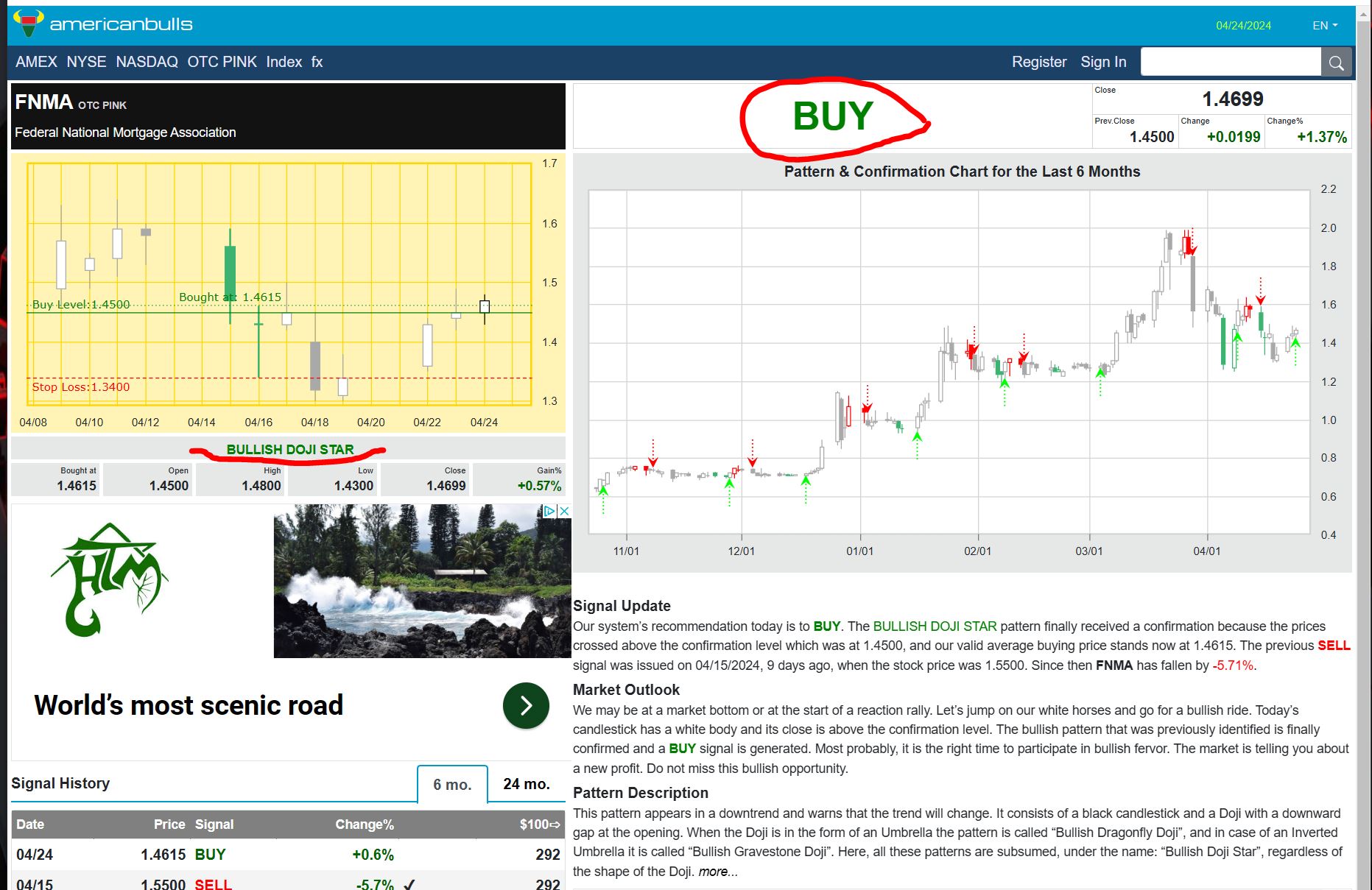

FNMA - BUY BUY BUY .... Bullish Doji Star ....

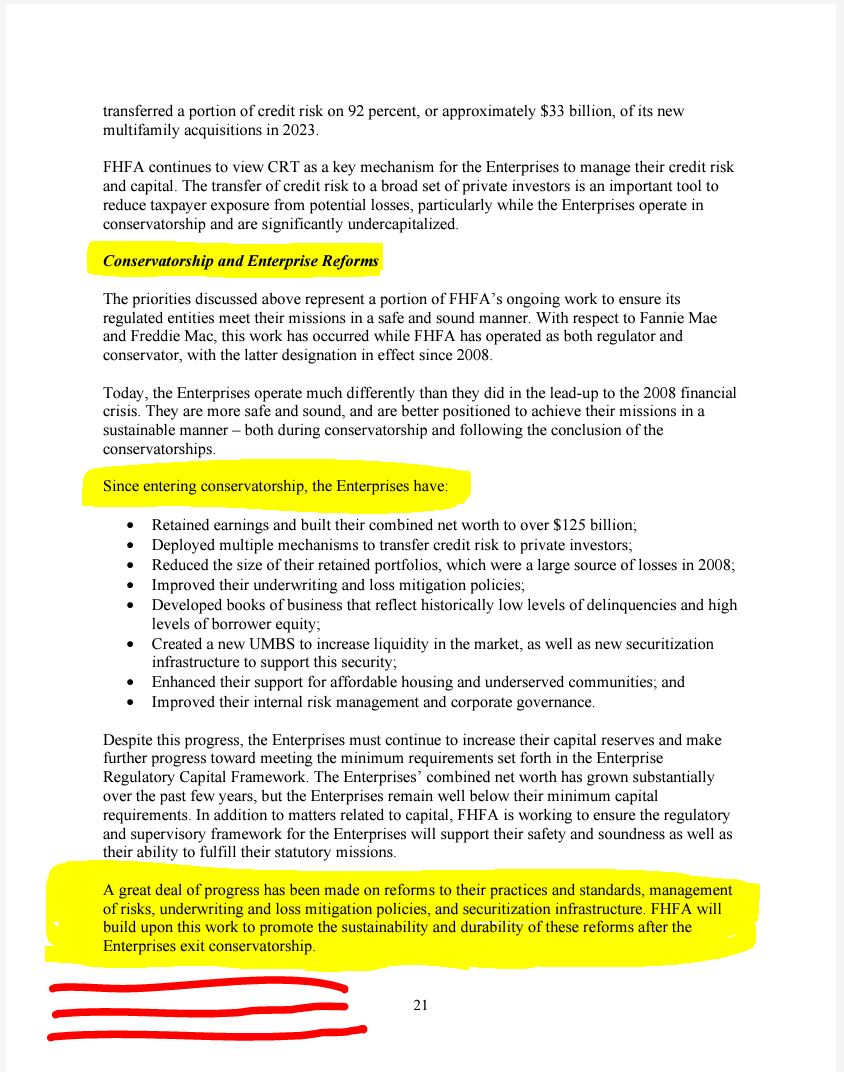

$Boooom ! ... as per the Director of the CONSERVATORSHIP ...

Reforms have been COMPLETED ! - EXIT CONSERVATORSHIP NOW !

Can’t believe it’s been almost 12 years since Ed DeMarco announced the Net Worth Sweep amendment at the 2012 MBA Annual Convention...

— Matt Hill (@hill_matt) April 25, 2024

He was pure fire!@FannieMae @FreddieMac @FHFA $FNMAS $FNMA #FannieGate pic.twitter.com/cp8YdUvdZv

$Boooom ! ... as per the Director of the CONSERVATORSHIP ...

Reforms have been COMPLETED ! - EXIT CONSERVATORSHIP NOW !

Buy Buy Buy ... Bullish Doji Star ... ...

Delinquencies on Agency MBS Decline in First Quarter

nbhatia@imfpubs.com

Delinquency rates were down for all three government agencies and in every late payment category as of the end of the first quarter of 2024, according to a new analysis by Inside Mortgage Trends of loans in agency mortgage-backed securities.

The overall delinquency rate across all three agencies declined 36 basis points in the first quarter to 2.78%.

The default rate for loans in Fannie Mae and Freddie Mac MBS dropped to 1.20% at the end of March, down from 1.37% at the end of December.

Some 6.97% of loans in Ginnie Mae MBS were in default at the end of March, down from 7.90% in the previous quarter. Both FHA and VA saw overall declines in late payments during the first quarter.

$Fannie $Mae Announces $Release of 1st Qtr 2024 Financial $Results

$Tuesday morning, April 30, 2024, before the opening of U.S. financial markets.

April 23, 2024

Company to Host Conference Call

WASHINGTON, DC – Fannie Mae (FNMA/OTCQB) today announced plans to report its first quarter 2024 financial results on Tuesday morning, April 30, 2024, before the opening of U.S. financial markets.

Fannie Mae has scheduled a conference call to discuss the company’s results at 8:00 a.m., ET, on April 30, 2024.

Prior to the call, the company’s first quarter 2024 earnings news release, quarterly report on Form 10-Q, and other supplemental information will be available on the company’s Quarterly and Annual Results webpage at fanniemae.com/financialresults. Following the call, a transcript will be published to the same webpage and will remain available until our next quarterly earnings announcement.

CONFERENCE CALL PARTICIPATION DETAILS – Fannie Mae First Quarter 2024 Financial Results

Event day and time

Tuesday, April 30, 2024

8:00 AM (ET)

Listen-only webcast:

https://event.webcasts.com/starthere.jsp?ei=1665149&tp_key=3a283801d1

Click on the link above to attend the presentation from your laptop, tablet, or mobile device. Audio will stream through your selected device. If you have difficulty accessing the webcast, please click the "Listen by Phone" button on the webcast player and dial the number provided.

Short Takes: Fannie Revises Originations Outlook Upward

Former Head of Correspondent Lending at Wells Lands at Mr. Cooper

bivey@imfpubs.com

Economists at Fannie Mae increased their originations forecast for 2024 even as interest rates

on mortgages are expected to remain elevated.

“We have revised upward our expectation for both purchase and refinance mortgage origination

volumes [in April compared with the forecast in March], due in particular to our more optimistic

home price growth expectation and somewhat lower mortgage rate path, along with an upgraded

expectation for home sales,” Fannie’s economics and strategic research group wrote Tuesday.

“We now expect 2024 purchase volumes to total just under $1.4 trillion, representing a

$31 billion upward revision from last month’s forecast and 14% growth from 2023.” ...

Biden administration issues final flood rule for federal-backed housing

Should help lower skyrocketing home insurance costs 🙃

— Tim Rood (@tim_rood_) April 23, 2024

latest from FHFA ...

All Americans, especially in underserved communities, deserve access to safe, decent and affordable housing. FHFA works with Fannie Mae and Freddie Mac on Equitable Housing Finance Plans showing how we will work toward these goals. #FairHousingMonth #FairLending->FairHousing pic.twitter.com/uMKD9BbiGd

— FHFA (@FHFA) April 23, 2024

All Americans, especially in underserved communities, deserve access to safe, decent and affordable housing. FHFA works with Fannie Mae and Freddie Mac on Equitable Housing Finance Plans showing how we will work toward these goals. #FairHousingMonth #FairLending->FairHousing pic.twitter.com/uMKD9BbiGd

— FHFA (@FHFA) April 23, 2024

more Fannie/Freddie GREEN ! ... FMCC 3X's FNMA vol

Agreed

— d.l. (@outerspace987) April 23, 2024

The very last sentence of a 28 page written testimony on the GSEs mentioned getting the GSEs ready for an exit from conservatorship. Judge for yourself what that means.

— Tim Rood (@tim_rood_) April 23, 2024

Fascinating trend in legislating and fiscal spending - find ways for the private sector to pay for or just finance the policy and outcomes the gov wants. CARES Act (servicers and mom and pop investors - “you mind covering those missed payments?” Or the GSEs - (opportunistic…

— Tim Rood (@tim_rood_) April 23, 2024

Agreed

— d.l. (@outerspace987) April 23, 2024

The very last sentence of a 28 page written testimony on the GSEs mentioned getting the GSEs ready for an exit from conservatorship. Judge for yourself what that means.

— Tim Rood (@tim_rood_) April 23, 2024

Fascinating trend in legislating and fiscal spending - find ways for the private sector to pay for or just finance the policy and outcomes the gov wants. CARES Act (servicers and mom and pop investors - “you mind covering those missed payments?” Or the GSEs - (opportunistic…

— Tim Rood (@tim_rood_) April 23, 2024

Fannie Mae Announces Tender Offer for Any and All of Certain CAS Notes

April 22, 2024

WASHINGTON, DC – Fannie Mae (FNMA/OTCQB) today announced that it has commenced fixed-price cash tender offers (each, an "Offer" and, collectively, the "Offers") for the purchase of any and all of the Connecticut Avenue Securities® (CAS) Notes listed below (the "Notes"), upon the terms and subject to the conditions set forth in the Offer to Purchase and related Notice of Guaranteed Delivery, each dated as of April 22, 2024 (collectively, the "Offer Documents"). Certain of the classes of Notes subject to the Offers were issued by the REMIC trusts identified in the table below (each, a "Trust"). Fannie Mae is the holder of the owner certificate issued by each Trust and, as a result, the sole beneficial owner of each Trust. The Offers will expire at 5:00 PM New York City time on Friday, April 26, 2024 (the "Expiration Time") unless extended or earlier terminated. Notes tendered may be withdrawn at any time at or before the Expiration Time by following the procedures described in the Offer Documents.

Fannie Mae has engaged BofA Securities as the designated lead dealer manager and Wells Fargo Securities as the designated dealer manager for the Offers. Fannie Mae has engaged Minority and Service-Disabled Veteran-owned Academy Securities, Inc. and Service-Disabled Veteran-owned Drexel Hamilton, LLC as advisors on the transaction. Global Bondholder Services Corporation will serve as the tender agent and information agent for the Offers. Fannie Mae is offering to purchase, subject to the conditions of the Offers, any and all of the Notes listed in the table below.

Represents the aggregate original principal amount of the applicable Class issued on the issue date thereof, less the aggregate original principal amount of such Class repurchased by the Company pursuant to one or more prior tender offers, if applicable. Does not include the original principal balance of the ineligible securities.

Holders must validly tender their Notes at or before the Expiration Time in order to be eligible to receive the Tender Offer Consideration, which will incorporate the monthly Certificate Percentages available on April 25, 2024. In addition, holders whose Notes are purchased in the Offers will receive accrued and unpaid interest from the last interest payment date to, but not including, the Settlement Date (as defined in the Offer to Purchase) for the Notes. Fannie Mae expects the Settlement Date to occur on April 30, 2024. Any Notes tendered using the Notice of Guaranteed Delivery and accepted for purchase are expected to be purchased on May 1, 2024, but payment of accrued interest on such Notes will only be made to, but not including, the Settlement Date.

Information on tendering the Notes is set forth in the Offer Documents. Holders of the Notes who would like copies of the Offer Documents may contact the tender agent for the Offers, Global Bondholder Services Corporation, at (855) 654-2015 (toll free) or (212) 430-3774 (banks and brokers) or contact@gbsc-usa.com. Copies of the Offer Documents are available at the following website: https://www.gbsc-usa.com/FannieMae/. Any questions regarding the terms of the Offers should be directed to BofA Securities, Inc. at (888) 292-0070 (toll free) or (980) 387-3907 (collect) or Wells Fargo Securities, LLC at (866) 309-6316 (toll free) or (704) 410-4820 (collect).

This release includes forward-looking statements, including statements relating to the timing and expected settlement and closing of the purchase of the Notes in a tender offer. These forward-looking statements are based on Fannie Mae’s present intent, beliefs or expectations, but forward-looking statements are not guaranteed to occur and may not occur. Actual results may turn out to be different from these statements. Factors that may lead to different results are discussed in "Risk Factors," "Forward-Looking Statements," and elsewhere in the Offer Documents and the documents incorporated by reference therein. All forward-looking statements are made as of the date of this press release, and Fannie Mae assumes no obligation to update this information.

$Freddie $Mac - $BUY ! ... Bullish Harami ...

FHFA : Incorporating Climate-Related Risks into Governance ...

Published: 4/22/2024

https://www.fhfa.gov//Media/Blog/Pages/Incorporating-Climate-Related-Risks-into-Governance.aspx

Following FHFA’s Conservatorship Scorecard guidance, Fannie Mae and Freddie Mac have made progress on developing foundational climate risk frameworks, integrating climate risk considerations into their strategic planning, incorporating climate risk considerations into their management and board reporting structures, and developing educational resources for their workforce. The Federal Home Loan Banks are continuing to individually develop their decision-making processes and governance structures in consideration of climate change.

Background

In October 2021, the Financial Stability Oversight Council (FSOC) released a report1 identifying climate change as an emerging and increasing threat to financial stability. Several international organizations and standard-setting bodies have recently developed frameworks to understand, assess, and manage climate-related risks to the entities or markets within their statutory jurisdictions. These include frameworks established by the Task Force on Climate-Related Financial Disclosures,2 Bank for International Settlements (BIS),3 and U.S. regulators (Office of the Comptroller of the Currency, Board of Governors of the Federal Reserve System, and Federal Deposit Insurance Corporation),4 as well as guidance5 and hypothetical scenarios6 developed by the Network for Greening the Financial System (NGFS).7

Federal Housing Finance Agency (FHFA)

FHFA, the conservator and regulator of Fannie Mae and Freddie Mac, and regulator of the Federal Home Loan Banks (collectively, the regulated entities), recognizes the emerging and increasing threat to all stakeholders in the housing system due to climate risk and the increased frequency and intensity of major natural disasters. Strong governance is foundational to managing an institution’s risk profile, particularly when the institution must address a constantly evolving landscape of risks. Accordingly, FHFA included the need to identify ways to incorporate climate change into regulated entity governance in its 2022-2026 Strategic Plan.8 Since 2022, FHFA has established goals for Fannie Mae and Freddie Mac (the Enterprises) to develop company-wide frameworks that incorporate climate risk into existing governance and risk management structures and decision-making, and to incorporate both short- and long-term strategies into the Enterprises’ strategic planning processes.

FHFA established an internal Climate Change and ESG9 Governance Working Group (Working Group) to evaluate the integration of climate risk into the corporate governance, risk management, and strategic planning structures of the regulated entities, and incorporation into operational and business decision-making. The Working Group meets regularly with the Enterprises and evaluates their progress through the annual Conservatorship Scorecard process, reviewing the establishment of foundational governance structures, decision-making processes, and risk management practices around climate risk. The Working Group also reviews progress made by the Federal Home Loan Banks in these areas.

Enterprises

Since 2022, the Enterprises have made distinct progress towards these goals and have been focused on: developing foundational climate risk frameworks, integrating climate risk considerations into strategic planning, incorporating climate risk considerations into management and board reporting structures, and establishing training and educational resources for their workforce.

Developing ?Climate Risk Frameworks

The Enterprises have developed initial climate risk frameworks that are incorporated in their enterprise risk management frameworks in consideration of the impact that climate change could have on the achievement of their mission, strategy, and business objectives.

The Enterprises continue to make progress and develop their capacity to measure the effects of climate risks and integrate climate-related risks into risk management structures:

Freddie Mac has developed climate scenario methodologies to better quantify the impact of climate events on housing affordability, property values, and credit risk;

Fannie Mae is working on finalizing climate scenario design and methodology for intended reporting in 2024; and

Both Ent?erprises completed exploratory climate scenario analysis exercises on flood risk in 2023.

Strategic Plan Integration

To assess and address climate-related risks and opportunities that could affect their businesses, the Enterprises have been incorporating climate issues into their corporate strategic plans and planning processes.

Each Enterprise has completed ESG materiality assessments that inform their ESG and climate strategic planning processes.

Fannie Mae’s 2023-2025 Strategic Plan includes climate risk management and supporting the housing ecosystem’s adaptation to climate change as priorities.10

Board and Management-level Reporting

Fannie Mae

The board Risk Policy and Capital Committee has primary oversight of climate-related risks.

The board Audit Committee provides oversight of ESG-related reporting, which includes climate risk.

The board Community Responsibility and Sustainability Committee oversees the development and implementation of Fannie Mae’s climate risk strategy.

There is a newly established Climate Risk Committee at the management level, and Fannie Mae has designated senior executive officers to oversee climate and ESG.

Freddie Mac

The board Risk Committee has primary oversight of climate related risks.

The board Audit Committee provides oversight of ESG-related reporting, which includes climate risk.

The board Mission and Housing Sustainability Committee provides oversight responsibilities for the development, planning, implementation, performance, and execution of Freddie Mac’s mission strategies and significant initiatives, including the review of sustainability initiatives with climate change implications or impacts.

Freddie Mac has also established several advisory and steering committees at the management level for ESG and climate risk reporting.

Training and Education

Over the last few years, the Enterprises have begun educating staff on the potential impacts of climate-related risks, taking into consideration the interconnectedness and multi-dimensional nature of climate-related topics that could reach all aspects of the organization.

Federal Home Loan Banks

The Federal Home Loan Banks also continue to develop their decision-making processes and governance structures in consideration of climate change. In June 2023, the Federal Home Loan Banks released an inaugural Corporate Social Responsibility Report11 highlighting governance and risk management as foundational to their ability to meet the needs of their members and districts.

FHLBank Mission and Foundational Principles

?

?Individually, each Federal Home Loan Bank is addressing climate-related risks in accordance with its own governance and management structures. For example, the Federal Home Loan Bank of Dallas’s 2022 ESG Report12?? highlights the formation of an ESG Committee providing oversight of the FHLBank’s ESG activities. The committee assists the executive management team and board with setting ESG strategy and reviewing reports and recommendations from subcommittees, including the Climate Risk Subcommittee. At the Federal Home Loan Bank of New York, “Climate and Natural Disaster” risks have been included into the scope of the board’s Risk Committee charter.

Summary

The work undertaken by the Enterprises and Federal Home Loan Banks in managing climate risks continues to be iterative and ongoing. For 2024, FHFA established priorities for the Enterprises in the Conservatorship Scorecard related to climate risks. For the governance area, this includes strengthening risk management capabilities in identifying, assessing, controlling, monitoring, and reporting on climate risk and incorporating these capabilities into the Enterprises’ overall risk frameworks.

Responsibilities of the FHFA Climate Change and ESG Governance Working Group:

Evaluate the integration of climate risk into the corporate governance, risk management, and strategic planning structures of the regulated entities, and incorporation into operational and business decision-making.

Monitor the development and maturation of the regulated entities’ climate risk frameworks and strategic planning processes.

??

Readers are encouraged to explore the FHFA Climate Change & ESG homepage for additional blogs and information related to climate risk.

1 Financial Stability Oversight Council, Report on Climate-Related Financial Risk, 2021, https://home.treasury.gov/system/files/261/FSOC-Climate-Report.pdf.

2 The Financial Stability Board, established to coordinate at the international level the work of national financial authorities and international standard-setting bodies in order to develop and promote the implementation of effective regulatory, supervisory and other financial sector policies, created the Task Force on Climate-Related Financial Disclosures in 2015 to improve and increase reporting of climate-related financial information.

3 The Bank for International Settlements is an international consortium of central banks and monetary authorities whose mission is to support central banks' pursuit of monetary and financial stability through international cooperation, and to act as a bank for central banks. See https://www.bis.org/about/index.htm. In 2022, the Basel Committee on Banking Supervision issued principles for the effective management and supervision of climate-related financial risks. See https://www.bis.org/press/p220615.htm.

4 On October 30, 2023, the Office of the Comptroller of the Currency, Board of Governors of the Federal Reserve System, and Federal Deposit Insurance Corporation jointly issued principles that provide a high-level framework for the safe and sound management of exposures to climate-related financial risks. See https://www.federalregister.gov/documents/2023/10/30/2023-23844/principles-for-climate-related-financial-risk-management-for-large-financial-institutions.

5 See https://www.ngfs.net/en/liste-chronologique/ngfs-publications.

6 See https://www.ngfs.net/ngfs-scenarios-portal/.

7 The NGFS is a voluntary group of central banks and supervisors that work together to contribute to the development of environment and climate risk management guidance and best practices in the financial sector for use both within and outside its membership.

8 See https://www.fhfa.gov/AboutUs/Reports/ReportDocuments/FHFA_StrategicPlan_2022-2026_Final.pdf.

9 ESG encompasses considerations of environmental, social, and governance factors. For the Enterprises, ESG covers their work to enhance environmental sustainability within the homes they finance, to advance consumer access to safe, resilient, and affordable housing opportunities in a sustainable manner, and to embed climate considerations within their board and management processes.

10 Fannie Mae’s 2023-2025 Strategic Plan is referenced in its 2022 Annual Report on Form 10-K (pp. 4) at https://www.fanniemae.com/media/46276/display.

11 See https://fhlbanks.com/the-federal-home-loan-banks-inaugural-corporate-social-responsibility-report/.?

12 See https://www.fhlb.com/getmedia/9cd26f43-96eb-4ac0-9dad-e109fd4abdb5/FHLBank-ESG-Report.pdf.

Authored by: Eric Kelley

Senior Strategic Analyst, Division of Conservatorship Oversight and Readiness

Authored by: Anne Marie Pippin

Deputy Director, Division of Conservatorship Oversight and Readiness

Authored by: La’Toya Holt

Senior Risk Analyst, Governance and Management Risk Branch, Office of Risk Analysis, Policy and Guidance and Development, Division of Enterprise Regulation

Editor: Varun Joshi

Economist, Climate Change and ESG Branch

FHFA : Incorporating Climate-Related Risks into Governance ...

Published: 4/22/2024

https://www.fhfa.gov//Media/Blog/Pages/Incorporating-Climate-Related-Risks-into-Governance.aspx

Following FHFA’s Conservatorship Scorecard guidance, Fannie Mae and Freddie Mac have made progress on developing foundational climate risk frameworks, integrating climate risk considerations into their strategic planning, incorporating climate risk considerations into their management and board reporting structures, and developing educational resources for their workforce. The Federal Home Loan Banks are continuing to individually develop their decision-making processes and governance structures in consideration of climate change.

Background

In October 2021, the Financial Stability Oversight Council (FSOC) released a report1 identifying climate change as an emerging and increasing threat to financial stability. Several international organizations and standard-setting bodies have recently developed frameworks to understand, assess, and manage climate-related risks to the entities or markets within their statutory jurisdictions. These include frameworks established by the Task Force on Climate-Related Financial Disclosures,2 Bank for International Settlements (BIS),3 and U.S. regulators (Office of the Comptroller of the Currency, Board of Governors of the Federal Reserve System, and Federal Deposit Insurance Corporation),4 as well as guidance5 and hypothetical scenarios6 developed by the Network for Greening the Financial System (NGFS).7

Federal Housing Finance Agency (FHFA)

FHFA, the conservator and regulator of Fannie Mae and Freddie Mac, and regulator of the Federal Home Loan Banks (collectively, the regulated entities), recognizes the emerging and increasing threat to all stakeholders in the housing system due to climate risk and the increased frequency and intensity of major natural disasters. Strong governance is foundational to managing an institution’s risk profile, particularly when the institution must address a constantly evolving landscape of risks. Accordingly, FHFA included the need to identify ways to incorporate climate change into regulated entity governance in its 2022-2026 Strategic Plan.8 Since 2022, FHFA has established goals for Fannie Mae and Freddie Mac (the Enterprises) to develop company-wide frameworks that incorporate climate risk into existing governance and risk management structures and decision-making, and to incorporate both short- and long-term strategies into the Enterprises’ strategic planning processes.

FHFA established an internal Climate Change and ESG9 Governance Working Group (Working Group) to evaluate the integration of climate risk into the corporate governance, risk management, and strategic planning structures of the regulated entities, and incorporation into operational and business decision-making. The Working Group meets regularly with the Enterprises and evaluates their progress through the annual Conservatorship Scorecard process, reviewing the establishment of foundational governance structures, decision-making processes, and risk management practices around climate risk. The Working Group also reviews progress made by the Federal Home Loan Banks in these areas.

Enterprises

Since 2022, the Enterprises have made distinct progress towards these goals and have been focused on: developing foundational climate risk frameworks, integrating climate risk considerations into strategic planning, incorporating climate risk considerations into management and board reporting structures, and establishing training and educational resources for their workforce.

Developing ?Climate Risk Frameworks

The Enterprises have developed initial climate risk frameworks that are incorporated in their enterprise risk management frameworks in consideration of the impact that climate change could have on the achievement of their mission, strategy, and business objectives.

The Enterprises continue to make progress and develop their capacity to measure the effects of climate risks and integrate climate-related risks into risk management structures:

Freddie Mac has developed climate scenario methodologies to better quantify the impact of climate events on housing affordability, property values, and credit risk;

Fannie Mae is working on finalizing climate scenario design and methodology for intended reporting in 2024; and

Both Ent?erprises completed exploratory climate scenario analysis exercises on flood risk in 2023.

Strategic Plan Integration

To assess and address climate-related risks and opportunities that could affect their businesses, the Enterprises have been incorporating climate issues into their corporate strategic plans and planning processes.

Each Enterprise has completed ESG materiality assessments that inform their ESG and climate strategic planning processes.

Fannie Mae’s 2023-2025 Strategic Plan includes climate risk management and supporting the housing ecosystem’s adaptation to climate change as priorities.10

Board and Management-level Reporting

Fannie Mae

The board Risk Policy and Capital Committee has primary oversight of climate-related risks.

The board Audit Committee provides oversight of ESG-related reporting, which includes climate risk.

The board Community Responsibility and Sustainability Committee oversees the development and implementation of Fannie Mae’s climate risk strategy.

There is a newly established Climate Risk Committee at the management level, and Fannie Mae has designated senior executive officers to oversee climate and ESG.

Freddie Mac

The board Risk Committee has primary oversight of climate related risks.

The board Audit Committee provides oversight of ESG-related reporting, which includes climate risk.

The board Mission and Housing Sustainability Committee provides oversight responsibilities for the development, planning, implementation, performance, and execution of Freddie Mac’s mission strategies and significant initiatives, including the review of sustainability initiatives with climate change implications or impacts.

Freddie Mac has also established several advisory and steering committees at the management level for ESG and climate risk reporting.

Training and Education

Over the last few years, the Enterprises have begun educating staff on the potential impacts of climate-related risks, taking into consideration the interconnectedness and multi-dimensional nature of climate-related topics that could reach all aspects of the organization.

Federal Home Loan Banks

The Federal Home Loan Banks also continue to develop their decision-making processes and governance structures in consideration of climate change. In June 2023, the Federal Home Loan Banks released an inaugural Corporate Social Responsibility Report11 highlighting governance and risk management as foundational to their ability to meet the needs of their members and districts.

FHLBank Mission and Foundational Principles

?

?Individually, each Federal Home Loan Bank is addressing climate-related risks in accordance with its own governance and management structures. For example, the Federal Home Loan Bank of Dallas’s 2022 ESG Report12?? highlights the formation of an ESG Committee providing oversight of the FHLBank’s ESG activities. The committee assists the executive management team and board with setting ESG strategy and reviewing reports and recommendations from subcommittees, including the Climate Risk Subcommittee. At the Federal Home Loan Bank of New York, “Climate and Natural Disaster” risks have been included into the scope of the board’s Risk Committee charter.

Summary

The work undertaken by the Enterprises and Federal Home Loan Banks in managing climate risks continues to be iterative and ongoing. For 2024, FHFA established priorities for the Enterprises in the Conservatorship Scorecard related to climate risks. For the governance area, this includes strengthening risk management capabilities in identifying, assessing, controlling, monitoring, and reporting on climate risk and incorporating these capabilities into the Enterprises’ overall risk frameworks.

Responsibilities of the FHFA Climate Change and ESG Governance Working Group:

Evaluate the integration of climate risk into the corporate governance, risk management, and strategic planning structures of the regulated entities, and incorporation into operational and business decision-making.

Monitor the development and maturation of the regulated entities’ climate risk frameworks and strategic planning processes.

??

Readers are encouraged to explore the FHFA Climate Change & ESG homepage for additional blogs and information related to climate risk.

1 Financial Stability Oversight Council, Report on Climate-Related Financial Risk, 2021, https://home.treasury.gov/system/files/261/FSOC-Climate-Report.pdf.

2 The Financial Stability Board, established to coordinate at the international level the work of national financial authorities and international standard-setting bodies in order to develop and promote the implementation of effective regulatory, supervisory and other financial sector policies, created the Task Force on Climate-Related Financial Disclosures in 2015 to improve and increase reporting of climate-related financial information.

3 The Bank for International Settlements is an international consortium of central banks and monetary authorities whose mission is to support central banks' pursuit of monetary and financial stability through international cooperation, and to act as a bank for central banks. See https://www.bis.org/about/index.htm. In 2022, the Basel Committee on Banking Supervision issued principles for the effective management and supervision of climate-related financial risks. See https://www.bis.org/press/p220615.htm.

4 On October 30, 2023, the Office of the Comptroller of the Currency, Board of Governors of the Federal Reserve System, and Federal Deposit Insurance Corporation jointly issued principles that provide a high-level framework for the safe and sound management of exposures to climate-related financial risks. See https://www.federalregister.gov/documents/2023/10/30/2023-23844/principles-for-climate-related-financial-risk-management-for-large-financial-institutions.

5 See https://www.ngfs.net/en/liste-chronologique/ngfs-publications.

6 See https://www.ngfs.net/ngfs-scenarios-portal/.

7 The NGFS is a voluntary group of central banks and supervisors that work together to contribute to the development of environment and climate risk management guidance and best practices in the financial sector for use both within and outside its membership.

8 See https://www.fhfa.gov/AboutUs/Reports/ReportDocuments/FHFA_StrategicPlan_2022-2026_Final.pdf.

9 ESG encompasses considerations of environmental, social, and governance factors. For the Enterprises, ESG covers their work to enhance environmental sustainability within the homes they finance, to advance consumer access to safe, resilient, and affordable housing opportunities in a sustainable manner, and to embed climate considerations within their board and management processes.

10 Fannie Mae’s 2023-2025 Strategic Plan is referenced in its 2022 Annual Report on Form 10-K (pp. 4) at https://www.fanniemae.com/media/46276/display.

11 See https://fhlbanks.com/the-federal-home-loan-banks-inaugural-corporate-social-responsibility-report/.?

12 See https://www.fhlb.com/getmedia/9cd26f43-96eb-4ac0-9dad-e109fd4abdb5/FHLBank-ESG-Report.pdf.

Authored by: Eric Kelley

Senior Strategic Analyst, Division of Conservatorship Oversight and Readiness

Authored by: Anne Marie Pippin

Deputy Director, Division of Conservatorship Oversight and Readiness

Authored by: La’Toya Holt

Senior Risk Analyst, Governance and Management Risk Branch, Office of Risk Analysis, Policy and Guidance and Development, Division of Enterprise Regulation

Editor: Varun Joshi

Economist, Climate Change and ESG Branch

Boooom ! -

Boooom ! -

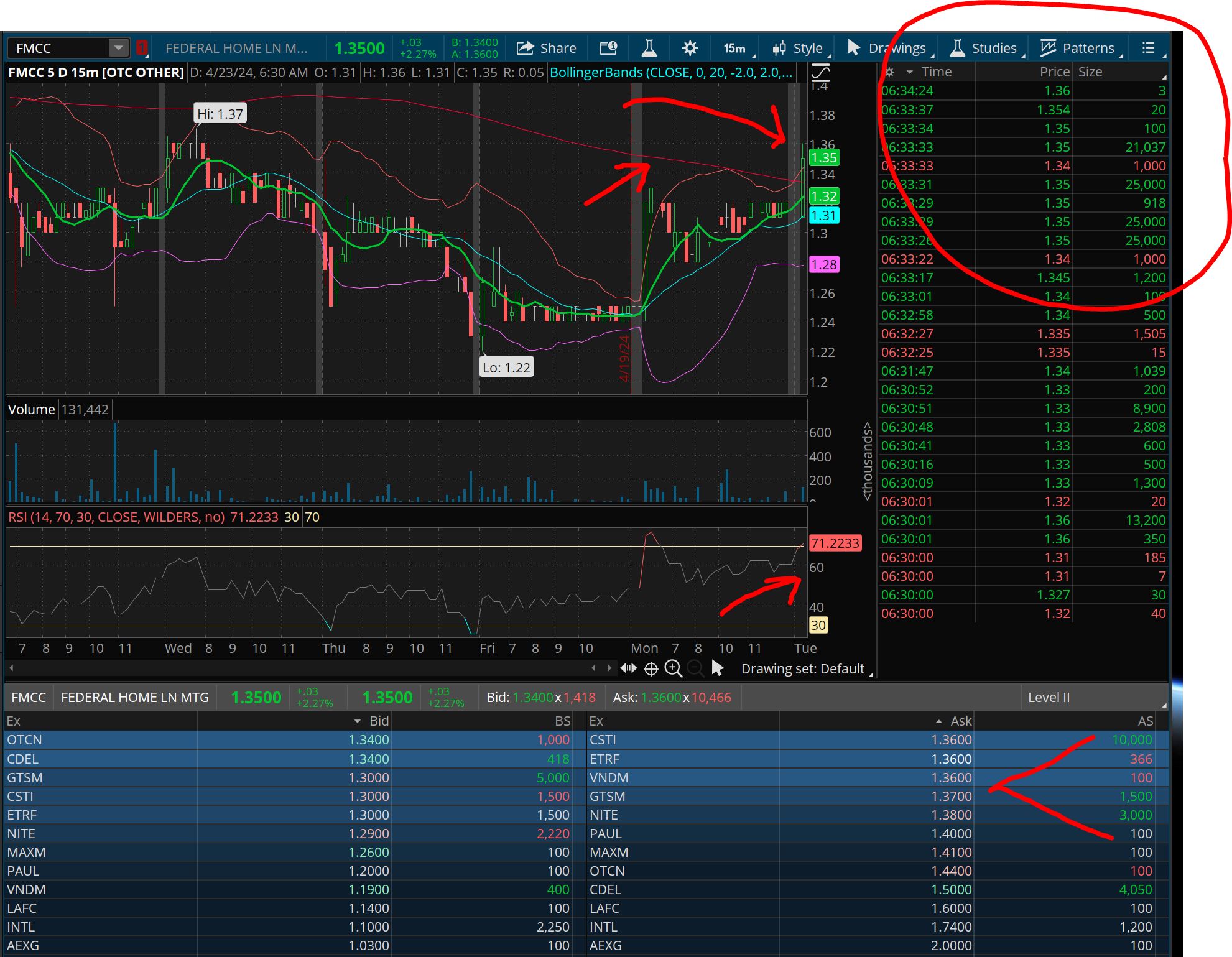

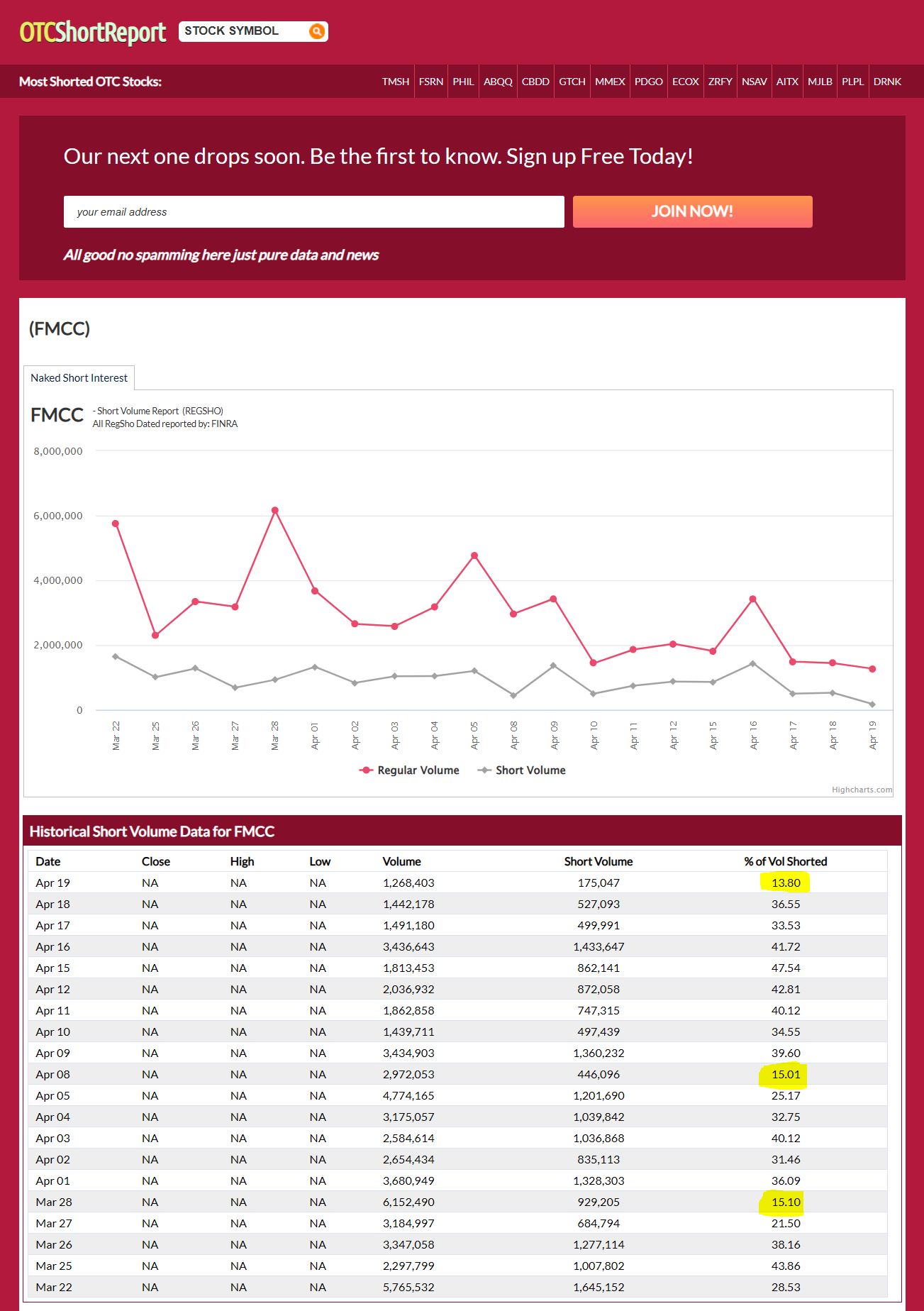

FMCC $1.31 -Shorts are headed for the exits ... 13.8% Fri

FMCC Naked Shorts Friday ....

FHFA no-bid contract deal -

In May 2023, I pressed FHFA Director Sandra Thompson on Doma Holdings: pic.twitter.com/NKeDYXNTw2

— Congressman William Timmons (@RepTimmons) April 19, 2024

FHFA no-bid contract deal -

In May 2023, I pressed FHFA Director Sandra Thompson on Doma Holdings: pic.twitter.com/NKeDYXNTw2

— Congressman William Timmons (@RepTimmons) April 19, 2024

never gonna happen - incompetent Q-tip is way over her head

Sandra has ZERO Leadership - will only do what she is told

Priscilla could get the JOB done but is outnumbered 2 - 1

Three women who, if they get together in the same room for half an hour, can unlock $100B+ for affordable housing:

— Fanniegate Hero (@DoNotLose) April 19, 2024

1. Janet Yellen, US Treasury

2. Sandra Thompson, FHFA

3. Priscilla Almodovar, Fannie Mae$FNMA #FANNIEGATE https://t.co/wF7Oq0rALe

Instead of addressing President Biden’s housing crisis, @HUDgov and @FHFA are pushing his radical climate agenda.

— Tim Scott (@SenatorTimScott) April 19, 2024

Families in communities like the one I grew up in want affordable homes and safe communities – not the Green New Deal. pic.twitter.com/w89vLNp3Gf

Morningstar DBRS assigned AAA ratings w “stable” outlook

to Fannie Mae & Freddie Mac on Thursday.

The rating service noted that the ratings were directly linked to the “long-term

local currency issuer rating” the firm currently has assigned to the U.S....

Sales of existing homes declined by 4.3% on a monthly basis in March, according to the

National Association of Realtors. “Though rebounding from cyclical lows, home sales are

stuck because interest rates have not made any major moves,” said Lawrence Yun,

chief economist at NAR.

Interest rates on mortgages have increased in April, hitting an average of 7.10% this week,

according to Freddie Mac...

Morningstar DBRS assigned AAA ratings w “stable” outlook

to Fannie Mae & Freddie Mac on Thursday.

The rating service noted that the ratings were directly linked to the “long-term

local currency issuer rating” the firm currently has assigned to the U.S....

Sales of existing homes declined by 4.3% on a monthly basis in March, according to the

National Association of Realtors. “Though rebounding from cyclical lows, home sales are

stuck because interest rates have not made any major moves,” said Lawrence Yun,

chief economist at NAR.

Interest rates on mortgages have increased in April, hitting an average of 7.10% this week,

according to Freddie Mac...

I was comparing scorecards between Calabria and Thompson this morning (no, seriously) and differences were very stark - Calabria: prepare the GSEs for exit - Thompson: affordable housing, climate, appraisal bias, and no mention of exit from conservatorship.

— Tim Rood (@tim_rood_) April 18, 2024

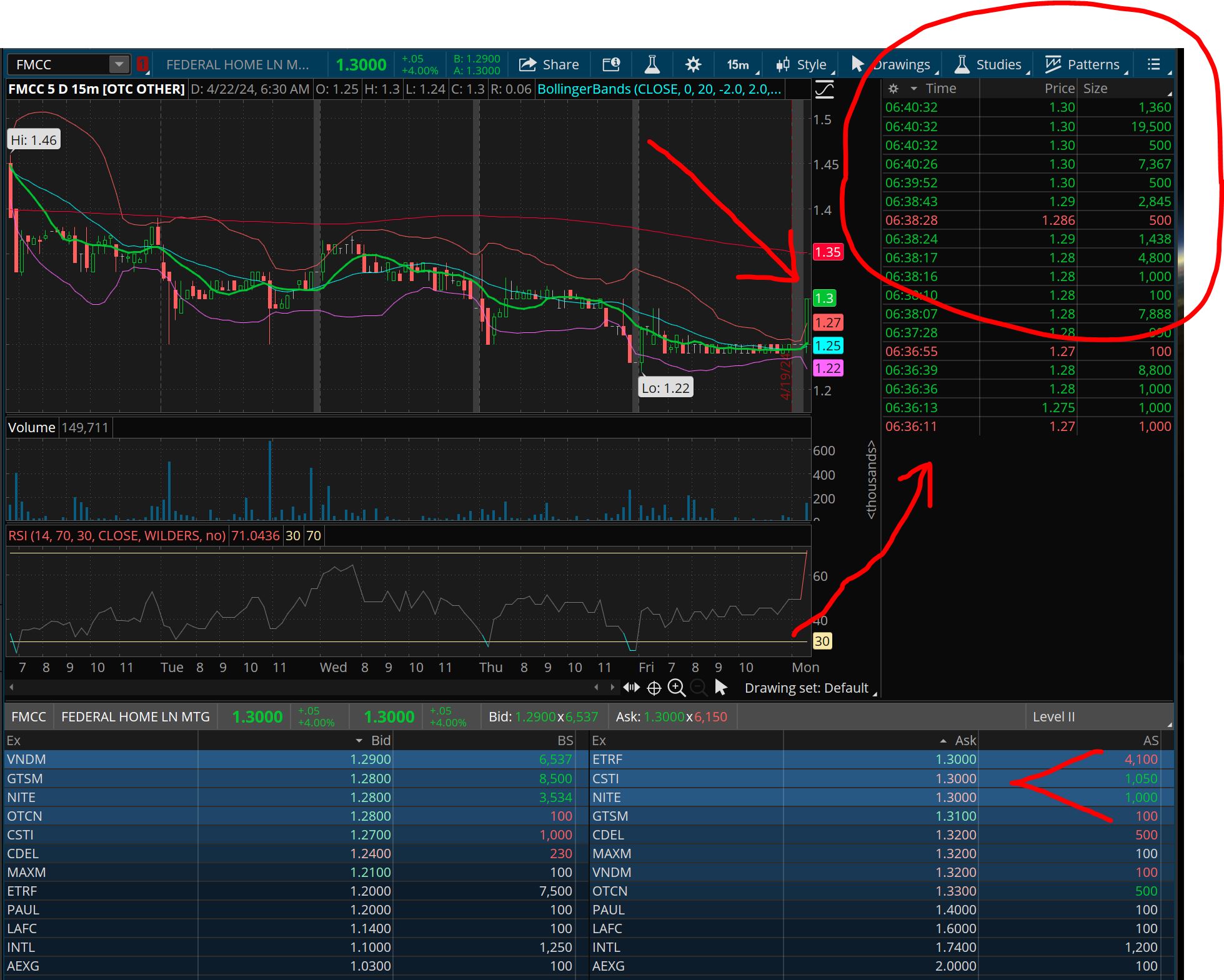

Yabba Dabba Dooooo !! - this time we BUST THRU $2 !!! ....

-

-

$Boooom ! - Freddie Mac wants a new role financing

Homeowners sitting on equity. One banking group isn’t happy.

if Banks don't like it - $IT'S a $GENIUS MOVE !!

($Very $Smart $Move - $ALREADY SOLID $PRODUCING $LOANS)

Published: April 17, 2024 at 5:30 p.m. ET - By Joy Wiltermuth

The housing giant could make a $850 billion splash in the market for

second-lien mortgages under a new proposal

A Wall Street lobbying group thinks Freddie Mac’s proposal is mission creep and wants

second-lien mortgages to stay in the domain of private credit. GETTY

-8.97%

Housing giant Freddie Mac wants the green light to expand its already dominant footprint

in the estimated $44.8 trillion U.S. housing market. But not everyone is on board.

Federal regulators want feedback on Freddie’s new proposal to allow it to start buying up

second-lien mortgages, a popular product among cash-strapped U.S. homeowners looking

to tap the equity in their properties, especially after mortgage rates shot up in the wake

of the pandemic.

Read: Homeowners scrambling for cash breathe new life into second-lien mortgage market

The aim is for Freddie to start buying fixed-rate second liens potentially by this summer, giving

borrowers a way to tap an estimated $32 trillion of equity built up in U.S. homes in recent years.

If approved, it would open the door for more borrowers to extract cash from their homes, without

having to refinance at current 30-year fixed mortgage rates of about 7.2%.

But a major financial-industry lobbying group said Wednesday that the second-lien market should

remain in the hands of private credit, not a partially government-backed entity.

“In the current market, closed-end second mortgages have been, and continue to be, successfully

originated and funded by private capital,” said Michael Bright, chief executive of the Structured

Finance Association, in a statement. “It is quite unclear what role the government-sponsored

enterprises have in funding these mortgage products, or how that fits into Freddie Mac’s overall

government-chartered mission objective.”

Freddie Mac FMCC, -5.38%, Fannie Mae FNMA, -8.97% and other government-sponsored

housing agencies already have a roughly $9.1 trillion stake in the estimated $13 trillion

U.S. residential-mortgage market.

While they don’t make loans, they buy up 30-year fixed-rate mortgages that conform to higher

lending standards put in place after the late-2000s subprime-mortgage crisis.

These lower-risk loans often end up bundled into bond deals with government guarantees that

primarily are owned by the Federal Reserve and banks, among other investors. Because of

these guarantees, investors consider the bonds to be a Treasury surrogate.

A hitch to Freddie’s proposal would be that it only buys second liens on homes where it already

financed the first mortgage.

Importantly, the proposal aims to limit how much homeowners can borrow in total against their

homes. Freddie said it plans to keep a borrower’s loan-to-value ratio at less than 80% when

looking at both first and second-lien mortgages on a home, keeping an equity cushion in place

in times of stress.

Servicing of the loans also would be overseen by Freddie, which means homeowners could

have access to payment pauses implemented by the government — such as the ones rolled

out during the COVID-19 pandemic, or in cases where homes are hit by hurricanes or other

natural disasters.

The SFA — which represents bond investors, issuers and Wall Street banks — called the

proposal “an unnecessary government encroachment into a sector that has been operating

successfully without government involvement.”

But Freddie’s charter, in place for decades, already indicates that it is authorized to purchase,

service, sell and deal in subordinate second liens.

BofA Global researchers estimated Wednesday that Freddie could end up owning around

$850 billion in second liens, given the huge swath of first-lien mortgages it already financed

at rates below 4%, and based on a combined loan-to-value ratio of 75%.

Fannie Mae, which hasn’t announced a similar program, could see volume of $1 trillion in

second liens when looking at the same parameters.

For context, the BofA Global researchers expect Wall Street to package up to a total of

about $11 billion in home-equity lines of credit and second liens into bond deals this year,

up from only $4.5 billion in 2023.

The U.S. housing market has been largely frozen since the Federal Reserve began

raising interest rates in 2022 to fight high inflation, a battle it continues to wage to this day.

$Boooom ! - Freddie Mac wants a new role financing

Homeowners sitting on equity. One banking group isn’t happy.

if Banks don't like it - $IT'S a $GENIUS MOVE !!

($Very $Smart $Move - $ALREADY SOLID $PRODUCING $LOANS)

Published: April 17, 2024 at 5:30 p.m. ET - By Joy Wiltermuth

The housing giant could make a $850 billion splash in the market for

second-lien mortgages under a new proposal

A Wall Street lobbying group thinks Freddie Mac’s proposal is mission creep and wants

second-lien mortgages to stay in the domain of private credit. GETTY

-8.97%

Housing giant Freddie Mac wants the green light to expand its already dominant footprint

in the estimated $44.8 trillion U.S. housing market. But not everyone is on board.

Federal regulators want feedback on Freddie’s new proposal to allow it to start buying up

second-lien mortgages, a popular product among cash-strapped U.S. homeowners looking

to tap the equity in their properties, especially after mortgage rates shot up in the wake

of the pandemic.

Read: Homeowners scrambling for cash breathe new life into second-lien mortgage market

The aim is for Freddie to start buying fixed-rate second liens potentially by this summer, giving

borrowers a way to tap an estimated $32 trillion of equity built up in U.S. homes in recent years.

If approved, it would open the door for more borrowers to extract cash from their homes, without

having to refinance at current 30-year fixed mortgage rates of about 7.2%.

But a major financial-industry lobbying group said Wednesday that the second-lien market should

remain in the hands of private credit, not a partially government-backed entity.

“In the current market, closed-end second mortgages have been, and continue to be, successfully

originated and funded by private capital,” said Michael Bright, chief executive of the Structured

Finance Association, in a statement. “It is quite unclear what role the government-sponsored

enterprises have in funding these mortgage products, or how that fits into Freddie Mac’s overall

government-chartered mission objective.”

Freddie Mac FMCC, -5.38%, Fannie Mae FNMA, -8.97% and other government-sponsored

housing agencies already have a roughly $9.1 trillion stake in the estimated $13 trillion

U.S. residential-mortgage market.

While they don’t make loans, they buy up 30-year fixed-rate mortgages that conform to higher

lending standards put in place after the late-2000s subprime-mortgage crisis.

These lower-risk loans often end up bundled into bond deals with government guarantees that

primarily are owned by the Federal Reserve and banks, among other investors. Because of

these guarantees, investors consider the bonds to be a Treasury surrogate.

A hitch to Freddie’s proposal would be that it only buys second liens on homes where it already

financed the first mortgage.

Importantly, the proposal aims to limit how much homeowners can borrow in total against their

homes. Freddie said it plans to keep a borrower’s loan-to-value ratio at less than 80% when

looking at both first and second-lien mortgages on a home, keeping an equity cushion in place

in times of stress.

Servicing of the loans also would be overseen by Freddie, which means homeowners could

have access to payment pauses implemented by the government — such as the ones rolled

out during the COVID-19 pandemic, or in cases where homes are hit by hurricanes or other

natural disasters.

The SFA — which represents bond investors, issuers and Wall Street banks — called the

proposal “an unnecessary government encroachment into a sector that has been operating

successfully without government involvement.”

But Freddie’s charter, in place for decades, already indicates that it is authorized to purchase,

service, sell and deal in subordinate second liens.

BofA Global researchers estimated Wednesday that Freddie could end up owning around

$850 billion in second liens, given the huge swath of first-lien mortgages it already financed

at rates below 4%, and based on a combined loan-to-value ratio of 75%.

Fannie Mae, which hasn’t announced a similar program, could see volume of $1 trillion in

second liens when looking at the same parameters.

For context, the BofA Global researchers expect Wall Street to package up to a total of

about $11 billion in home-equity lines of credit and second liens into bond deals this year,

up from only $4.5 billion in 2023.

The U.S. housing market has been largely frozen since the Federal Reserve began

raising interest rates in 2022 to fight high inflation, a battle it continues to wage to this day.

GOVT filed to have 8-0 Jury verdict THROWN OUT