News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

2morrowsGains

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

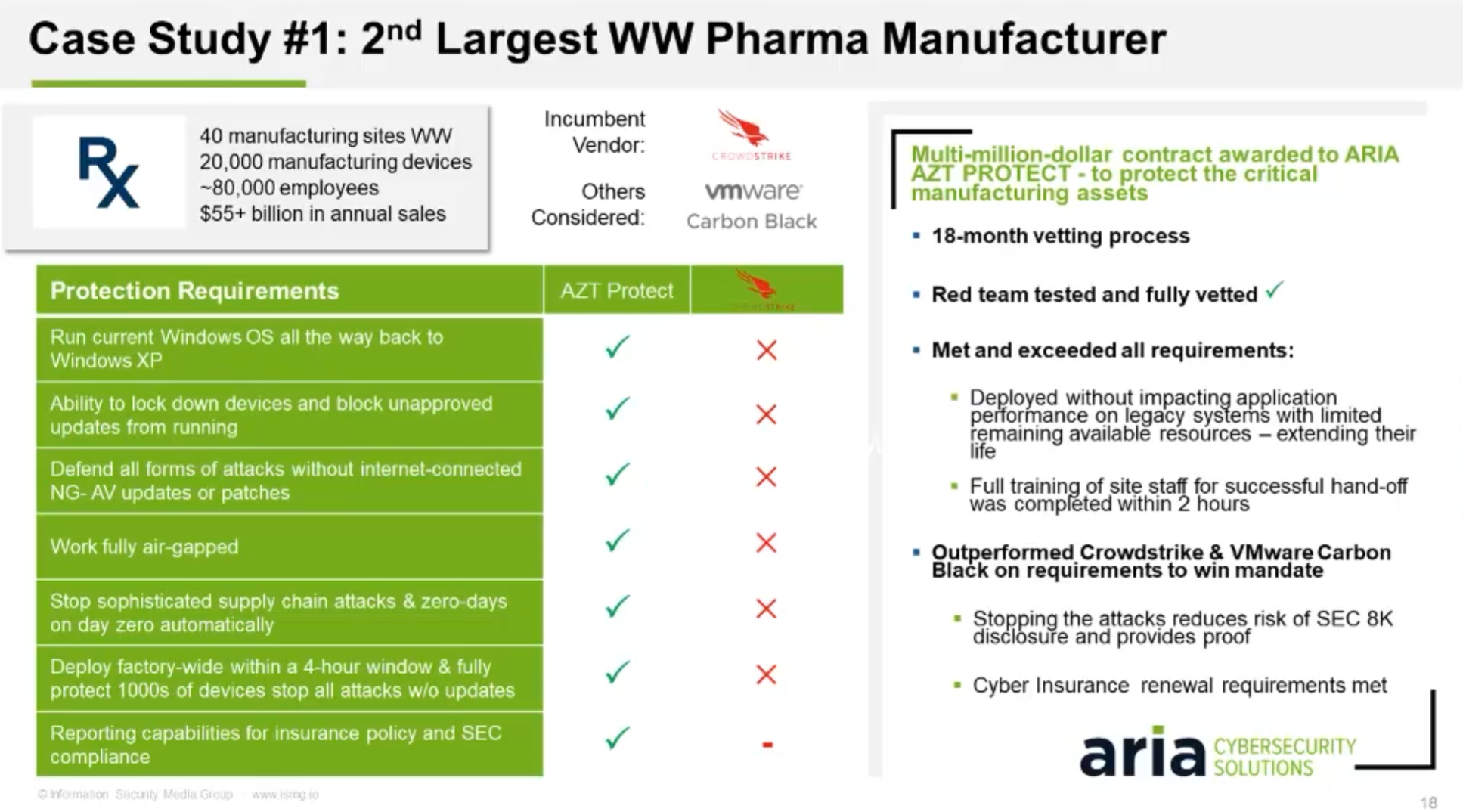

CSPI...Re: Slide 18...Pfizer is the pharma company that deployed AZT PROTECT across their global manufacturing (IMO). You never know but look at the numbers on slide 18 and compare them with Pfizer...

From the slide...

- 2nd Worldwide Largest Pharm Manucaturer

- 40 manufacturig facilities wolrdwide

- 80,000 Employees

- $55B in anual sales.

Pfizer...

- https://currentaffairs.adda247.com/biggest-pharmaceutical-company/

- Our global manufacturing network includes more than 35 sites across six continents.

https://www.pfizercentreone.com/pfizers-global-manufacturing-network#:~:text=Our%20global%20manufacturing%20network%20includes%20more%20than%2035%20sites%20across%20six%20continents.

- Full Time Employees: 88,000

https://finance.yahoo.com/quote/PFE/profile

- $55B+ in annual sales

https://finance.yahoo.com/quote/PFE/financials

https://www.databreachtoday.com/showOnDemand.php?webinarID=5538

SRTS...So do I. lol

SRTS...Nice. Up a good clip AH's. Hope you hold a good amount. Been a while since I owned it.

HTGB...Heritage Global Inc. Reports First Quarter 2024 Results

Company Reports Operating Income of $2.6 Million

Subsequent to First Quarter Company Closed an Equipment Sale and Real Estate Lease Transaction With Multi-National Pharmaceutical Company

SAN DIEGO--(BUSINESS WIRE)-- Heritage Global Inc. (NASDAQ: HGBL) (“Heritage Global,” “HG” or “the Company”), an asset services company specializing in financial and industrial asset transactions, today reported financial results for the first quarter ended March 31, 2024.

Heritage Global Chief Executive Officer Ross Dove commented, “2024 is off to a solid start with continued profitability in the business. Our financial division is executing well and benefiting from heightened economic pressures driving increases in charged-off credit cards and non-performing loans. Our industrial division continues to see healthy levels of equipment and asset auction activity, but faced a tough comparison in the quarter given a large auction that took place in the first quarter of 2023. Importantly, subsequent to the close of the first quarter, our auction division, in conjunction with our partners, completed a highly accretive transaction involving the sale of equipment and a 10-year building lease on the recently acquired pharmaceutical plant in Fenton, Missouri.

“Looking forward, the pipeline is strong across our businesses and we look forward to continuing to drive long term organic growth and profitability. Additionally, M&A is a strategic focus as we move forward and we are seeing increased opportunities in the markets we serve,” Mr. Dove concluded.

First Quarter 2024 Highlights:

The Company achieved operating income of $2.6 million for the first quarter of 2024, as compared to operating income of $3.9 million in the first quarter of 2023.

EBITDA totaled $2.7 million in the first quarter of 2024 versus EBITDA of $4.0 million in the first quarter of 2023 and Adjusted EBITDA was $2.9 million compared to $4.2 million in the prior-year quarter.

Net income totaled $1.8 million or $0.05 of diluted earnings per share for the first quarter of 2024, as compared to net income of $2.8 million or $0.08 of diluted earnings per share in the prior-year quarter.

The Company strengthened its balance sheet by increasing stockholders’ equity to $63.0 million as of March 31, 2024, compared to $61.1 million as of December 31, 2023, and increased net working capital to $15.0 million at the end of the first quarter of 2024, compared to $11.6 million at the end of the fourth quarter of 2023. The Company’s available and unused balance on its credit facility remains at $10.0 million as of March 31, 2024. The strengthened balance sheet and liquidity positions the Company well to pursue its M&A strategy.

As of March 31, 2024, the Company held a gross balance of investments in notes receivable of $37.3 million, recorded in both notes receivable and equity method investments.

First Quarter Conference Call

Management will host a webcast and conference call on Thursday, May 9, 2024, at 5:00 p.m. ET to discuss financial results for the first quarter of 2024. Analysts and investors may participate via conference call, using the following dial-in information:

1-800-830-9649 (Domestic)

1-213-992-4624 (International)

To access the webcast, individuals can use this link. The conference call will also be available in the Investor Relations section of the Company’s website. To listen to a live broadcast, go to the site or click on the webcast link at least 10 minutes prior to the scheduled start time in order to register.

Replay

A replay of the call will be available on the Company’s website approximately three hours after the call ends through May 23, 2024. To access the replay, dial 1-844-512-2921 (domestic) or 1-412-317-6671 (international). The replay pin number is 11155834. The replay can also be accessed on the Investor Relations section of the Company’s website.

About Heritage Global Inc. (“HG”)

Heritage Global Inc. (NASDAQ: HGBL) values and monetizes industrial & financial assets by providing acquisition, disposition, valuation, and lending services for surplus and distressed assets. This aids in facilitating the circular economy by diverting useful industrial assets from landfills and operating an ethical supply chain by overseeing post-sale account activity of financial assets. Specialties consist of acting as an adviser, in addition to acquiring or brokering turnkey manufacturing facilities, surplus industrial machinery and equipment, industrial inventories, real estate, and charged-off account receivable portfolios through its two business units: Industrial Assets and Financial Assets.

https://ih.advfn.com/stock-market/NASDAQ/heritage-global-HGBL/stock-news/93818001/heritage-global-inc-reports-first-quarter-2024-re

CSPI...DAMN! I missed the webinar this morning...Did anyone listen to it?? I was registered and signed in to listen in, but got sidetracked and missed the presentation.😣

HGBL...Reports after the close. This one has been holding at what looks to be good support near a 52wk low, which has dgiven me time to build a decent position (avg cost approx $2.50 a share).

Not expecting a blowout Q, although it should be decent.

Looking @ HGBL as a good long term hold that diversifies a bit of my portfolio into another sector.

Here's more info on the company Heritage Global Inc. (HGBL)...

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=174281057

ACDC...LOL. Yes👍

ACDC...+15% today...Back over $8. Nice turnaround.

ACDC ($7.09)...EPS beats big, Sales miss by a hair... ProFrac Holding Corp. Reports First Quarter 2024

Financial and Operational Results

WILLOW PARK, TX – May 9, 2024 – ProFrac Holding Corp. (NASDAQ: ACDC) (“ProFrac”, or the “Company”) today announced financial and operational results for its first quarter ended March 31, 2024.

First Quarter 2024 Results

·- Total revenue grew approximately 19% sequentially to $581.5 million over the fourth quarter revenue of 2023

·- Net income was $3.0 million compared to a net loss of $96.5 million in the fourth quarter of 2023

·- Adjusted EBITDA(1) grew approximately 46% sequentially over the fourth quarter to $159.7 million

·- Net cash provided by operating activities grew approximately 85% sequentially over the fourth quarter to $79.1 million

- Capital expenditures totaled $59.9 million

·- Free cash flow(2) grew 102% sequentially to $25.8 million

Matt Wilks, ProFrac’s Executive Chairman, stated, “We are very pleased with our first quarter results, which demonstrate meaningful progress on the strategic initiatives we began emphasizing in the back half of 2023. ProFrac’s greater scale, utilization and efficiencies are demonstrated by lower costs and higher profitability. As we outlined on our previous earnings call and as shown by these results, we deployed a substantial number of fleets in a disciplined manner during the first quarter.”

Outlook

In the Stimulation Services segment, the Company anticipates pricing to remain steady. Because of our superior cost structure and operating leverage, we continue to see opportunities to further improve profitability per fleet.

In the Proppant Production segment, volumes and profitability are expected to improve as we see third party volumes expand alongside our stimulation services segment volumes.

Business Segment Information

The Stimulation Services segment generated revenues of $517.3 million in the first quarter of 2024, which resulted in $125.0 million of Adjusted EBITDA.

The Proppant Production segment generated revenues of $77.7 million in the first quarter of 2024, which resulted in $28.4 million of Adjusted EBITDA. Approximately 31% of the Proppant Production segment’s revenue was intercompany.

The Manufacturing segment generated revenues of $43.5 million in the first quarter of 2024, which resulted in $4.4 million of Adjusted EBITDA. Approximately 78% of the Manufacturing segment’s revenue was intercompany.

Our Other Business Activities generated revenues of $41.7 million in the first quarter of 2024, which resulted in $3.6 million of Adjusted EBITDA. The Other Business Activities solely relate to the results of Flotek.

Capital Expenditures and Capital Allocation

Cash capital expenditures totaled $59.9 million in the first quarter, an increase sequentially, due to fleet deployments during the quarter and other growth-related initiatives including fleet upgrades and mine optimization.

For the full year 2024, the Company still expects to incur maintenance-related capital expenditures of between $150 million and $200 million. Growth-related capital expenditures across all segments are expected to remain approximately $100 million in 2024, as the Company continues to monitor market conditions, industry dynamics and customer demand to appropriately align spending levels and growth initiative timelines. Currently, growth capital expenditures for 2024 are expected to be primarily related to mine improvements and frac fleet upgrades.

Balance Sheet and Liquidity

Total net debt outstanding as of March 31, 2024 was $1.06 billion, a decrease of approximately $26 million from the fourth quarter.

Total cash and cash equivalents as of March 31, 2024 was $28.3 million, of which $5.2 million was related to Flotek and not accessible by the Company.

As of March 31, 2024 the Company had $166.9 million of liquidity, including approximately $23.1 million in cash and cash equivalents, excluding Flotek, and $143.8 million of availability under its asset-based credit facility.

Footnotes

(1) Adjusted EBITDA is a financial measure not presented in accordance with generally accepted accounting principles (“GAAP”) (a “Non-GAAP Financial Measure”). Please see “Non-GAAP Financial Measures” at the end of this news release.

(2) Free Cash Flow is a Non-GAAP Financial Measure. Please see “Non-GAAP Financial Measures” at the end of this news release.

Conference Call

ProFrac has scheduled a conference call on Thursday, May 9, 2024 at 11:00 a.m. Eastern time / 10:00 a.m. Central time. Please dial 412-902-0030 and ask for the ProFrac Holding Corp. call at least 10 minutes prior to the start time of the call, or listen to the call live over the Internet by logging on to the website at the address https://ir.pfholdingscorp.com/news-events/ir-calendar. A telephonic replay of the conference call will be available through May 16, 2024 and may be accessed by calling 201-612-7415 and using passcode 13745998#. A webcast archive will also be available at the link above shortly after the call and will be accessible for approximately 90 days.

About ProFrac Holding Corp.

ProFrac Holding Corp. is a technology-focused, vertically integrated, innovation-driven energy services holding company providing hydraulic fracturing, proppant production, other completion services and other complementary products and services to leading upstream oil and natural gas companies engaged in the exploration and production ("E&P") of North American unconventional oil and natural gas resources throughout the United States. Founded in 2016, ProFrac was built to be the go-to service provider for E&P companies' most demanding hydraulic fracturing needs. ProFrac is focused on employing new technologies to significantly reduce "greenhouse gas" emissions and increase efficiency in what has historically been an emissions-intensive component of the unconventional E&P development process. ProFrac Corp. operates in three business segments: stimulation services, proppant production and manufacturing. For more information, please visit ProFrac’s website at www.PFHoldingsCorp.com.

https://ih.advfn.com/stock-market/NASDAQ/profrac-ACDC/stock-news/93812700/form-8-k-current-report

SD...Stuck my toe back in the water on today's dip to the $13.30's. It's a crap shoot but I think if I can hold on til next year I may make some decent gains.

We'll see what happens.

CSPI...Yes. Bought a few more @ approx $11.45...I was going to ask you the same thing. Too bad you missed it. Maybe get another shot though, You never know.

I know what you mean about missing opportunites though...I missed buying more CXDO in the $3.80's today. Hoping for CXDO to keep sliding lower. I'm in no hurry to sell any more until next year and will accumulate more at the right price.

CXDO...Was down 17% today...This is more than likely due to a shelf filing yesterday. Good buying opportunity especially if it keeps dropping (IMO). The CEO made clear yesterday on the cc that shelf is good for 3 years and is not for immediate use. Said it's a testament to good corporate governance. If and when Crexendo uses it, it will be for future srtategic investments and most likely be for accretive acquisitions.

This is a hell'a strong management team. No reason to doubt them at their word.

Hold, Wait, & Accumulate!!!

CSPI...I agree. It is nice though to see cash @ over $27M ($3 a share) and still low/no debt.

We'll see what they have to say in the cc.

CSPI...Nice report...CSP Inc. Reports Fiscal Second Quarter 2024 Operating Results; 23% Growth in Services Revenue Drives Gross Margin Percentage Expansion to 47% and Nearly Five-Fold Increase in Net Income

ARIA Zero Trust PROTECT ("AZT PROTECT™" or "AZT") Launch Broadens to Address Mid-Market Opportunity While Fortune 500 Pipeline Increases; Global Pharmaceutical Company Signs Multi-Million Dollar AZT Contract

LOWELL, MA / ACCESSWIRE / May 8, 2024 / CSP Inc. (NASDAQ:CSPI), an award-winning provider of cybersecurity AI-driven solutions (AZT), security and packet capture products, managed IT and professional / cloud services and technology solutions, today announced results for the fiscal second quarter ended March 31, 2024. The Company also announced that the Board of Directors declared a quarterly dividend of $0.03 per share payable June 12, 2024, to shareholders of record on the close of business on May 24, 2024.

Recent Achievements and Operating Highlights

Services revenue and high margin AZT sale contributes to the expanded gross margin and net income of $1.6 million for the fiscal second quarter

Recently published case study of AZT PROTECT™ in The Journal, an award-winning publication from Rockwell Automation and Our PartnerNetwork™, reached a subscriber base of over 50,000. The Journal educates the industrial automation market on leading-edge methods, trends, and technologies

CRN®, a brand of The Channel Company, named CSPi Technology Solutions to its Managed Service Provider (MSP) 500 list in the Security 100 category for 2024.

Continued strong balance sheet allows the company to rapidly invest in AZT PROTECT™ market development initiatives

ARIA Cybersecurity Wins Global Infosec Cybersecurity Product Award for AZT PROTECT at RSA

ARIA Cybersecurity Wins Prestigious Globee Cybersecurity Product Award for AZT PROTECT

"Our business continued to operate at a high level during the quarter, and across the board we are building a pipeline that is in line with, or well above our internal plans. As a result, we continue to execute a strategy designed to generate sustained long-term growth and profitability," commented Victor Dellovo, Chief Executive Officer. "The consistent performance of our Technology Solutions (TS) business and robust balance sheet is enabling investment in certain sales and marketing initiatives to generate the desired growth outcomes for the High Performance Products (HPP) business, mainly with the AZT offering."

"We believe our multi-pronged market awareness strategy for the AZT offering is demonstrating the need and attractiveness to large Fortune 500 global brands. The effort has resulted in landing a major AZT customer - a global pharmaceutical company. With a dedicated sales team focused on this enterprise segment, we recently added three sales representatives to target mid-market companies while we build partnerships with organizations addressing both markets. Earlier this month, we also achieved another significant milestone with our partner Rockwell, and the publication of an AZT PROTECT™ deployment case study within a Fortune 500 company. This article published in The Journal is distributed to over 50,000 subscribers - readers that heavily rely on knowing the latest and best solutions to meet today's cybersecurity threats and challenges.

As we move forward, we believe the focus of our direct sales team and leveraging our new and expanding partnerships is going to significantly raise the profile of the AZT offering. Despite being less than a year removed from the launch, we are building traction in the market and the level of enthusiasm remains high, as does the new business lead pipeline. We are optimistic about the opportunities we have with AZT and look forward to the second half of our fiscal year."

Fiscal 2024 Second Quarter Results

Revenue for the fiscal second quarter ended March 31, 2024, was up slightly to $13.7 million compared to revenue of $13.3 million for the fiscal second quarter ended March 31, 2023. Services revenue constituted $5.2 million of overall sales, an increase of 23% compared to services revenue of $4.3 million in the year-ago fiscal second quarter. Gross profit for the three months ended March 31, 2024, was $6.5 million, or 47% of sales, compared to $5.0 million, or 38% of sales, representing a 9% improvement as higher margin services revenue along with the high margin AZT sale fueled the growth. The Company reported net income of $1.6 million, or $0.16 per diluted common share for the fiscal second quarter ended March 31, 2024, compared to net income of $0.3 million, or $0.03 per diluted common share for the fiscal second quarter ended March 31, 2023. Earnings per diluted common share are retroactively adjusted for the effects of a stock split effected in the form of a 100% stock dividend which occurred during the second fiscal quarter of 2024.

The Company had cash and cash equivalents of $27.1 million as of March 31, 2024, providing it with the resources to invest in market awareness and growth initiatives for its products and services, including the transformative AZT offering.

Fiscal Year 2024 Six Month Results

Revenue for the fiscal six months ended March 31, 2024, was $29.1 million compared with revenue of $31.6 million in same prior year period. Gross profit for the fiscal six months ended March 31, 2023, was $10.6 million, or 36% of sales compared with $10.8 million, or 34% of sales, reflecting a more favorable product mix and benefiting from the higher margin services revenue in the 2024 fiscal second quarter. The Company reported net income of $1.5 million, or $0.16 per diluted common share in the fiscal six months ended March 31, 2024 compared with net income of $1.3 million, or $0.14 per diluted common share for the fiscal six months ended March 31, 2023.

Conference Call Details

CSPi Chief Executive Officer Victor Dellovo and Chief Financial Officer Gary W. Levine will host a conference call at 10:00 a.m. (ET) today, May 8, 2024, to review CSPi's financial results and provide a business update. To listen to a live webcast of the call, the event link is https://www.webcaster4.com/Webcast/Page/2912/50580. Individuals also may listen to the call via telephone, by dialing 77-545-0523 or 973-528-0016 and use the Participant Access Code: 533105 when greeted by the live operator. For interested parties unable to participate in the live call, an archived version of the webcast will be available for approximately one year on CSPi's website.

CXDO...Not too shabby...Crexendo Announces First Quarter 2024 Results

PHOENIX, AZ / ACCESSWIRE / May 7, 2024 / Crexendo, Inc. (NASDAQ:CXDO), an award-winning premier provider of cloud communication platform and services, video collaboration and managed IT services designed to provide enterprise-class cloud solutions to any size business, today announced financial results for the first quarter ended March 31, 2024.

First Quarter Financial highlights:

Total revenue increased 14% year-over-year to $14.3 million

GAAP net income of $434,000, or $0.02 per basic common share and $0.01 per diluted common share

Non-GAAP net income of $1.9 million, or $0.07 per basic common share and $0.06 per diluted common share

Financial Results for the First Quarter of 2024

Total Revenue: Consolidated total revenue for the first quarter of 2024 increased 14%, or $1.8 million, to $14.3 million compared to $12.5 million for the first quarter of 2023.

Service Revenue: Consolidated service revenue for the first quarter of 2024 increased 10%, or $0.7 million, to $7.8 million compared to $7.1 million for the first quarter of 2023.

Software Solutions Revenue: Consolidated software solutions revenue for the first quarter of 2024 increased 25%, or $1.0 million, to $5.1 million compared to $4.1 million for the first quarter of 2023.

Product Revenue: Consolidated product revenue for the first quarter of 2024 increased 6%, or $0.1 million, to $1.3 million compared to $1.2 million for the first quarter of 2023.

Operating Expenses: Consolidated operating expenses for the first quarter of 2024 decreased 2%, or $(0.2) million, to $13.8 million compared to $14.0 million for the first quarter of 2023.

Net Income/(Loss): The Company reported net income of $0.4 million for the first quarter of 2024, or $0.02 per basic common share and $0.01 per diluted common share, compared to net loss of $(1.6) million, or $(0.06) loss per basic and diluted common share for the first quarter of 2023.

Non-GAAP: Non-GAAP net income of $1.9 million for the first quarter of 2024, or $0.07 per basic common share and $0.06 per diluted common share, compared to non-GAAP net income of $0.6 million or $0.02 per basic and diluted common share for the first quarter of 2023.

EBITDA and Adjusted EBITDA: EBITDA for the first quarter of 2024 of $1.3 million compared to a loss of $(0.7) million for the first quarter of 2023. Adjusted EBITDA for the first quarter of 2024 of $2.0 million compared to $0.7 million for the first quarter of 2023.

Cash and Cash Equivalents: Total cash and cash equivalents at March 31, 2024 was $11.0 million compared to $10.3 million at December 31, 2023.

Cash Flow: Cash used for operating activities for the first quarter of 2024 was $(0.2) million compared to $(1.6) million used for the first quarter of 2023. Cash used for investing activities for the first quarter of 2024 was nill compared to $(0.0) million used for the first quarter of 2023. Cash provided by financing activities for the first quarter of 2024 was $0.8 million compared to cash used in financing activities of $(0.2) million for the first quarter of 2023.

Management Commentary

"Our superb performance in the first quarter of 2024 reflects our unwavering commitment to innovation, operational excellence, and delivering value to our shareholders and customers. We are very pleased with the strong financial results, including a 14% year-over-year organic increase in total revenue to $14.3 million as well as GAAP profitability." Said Jeff Korn Crexendo Chief Executive Officer and Chairman of the Board. "Our revenue growth remains robust, driven by a 25% growth in the software solutions segment as well as a double digit increase in telecom service revenue which equated to very solid performance across all revenue segments."

Korn added "We remain steadfast in our efforts to streamline costs and improve operational effectiveness. Our efforts resulted in GAAP net income of $434,000, non-GAAP net income of $1.9 million and Adjusted EBITDA of $2.1 million, demonstrating our ability to deliver profitable growth and create value for our shareholders. This is now the third quarter in a row of GAAP profitability which is particularly meaningful. Looking ahead, we remain focused on driving organic growth, pursuing larger opportunities, and exploring accretive acquisitions to further accelerate our expansion. Our strong performance in the first quarter of 2024, coupled with the demand for our services positions us well for continued success. We are confident in our ability to sustain our growth momentum and capitalize on market opportunities, supported by our dedicated team and strong market positioning. I remain highly excited and enthusiastic about our future."

Conference Call

Crexendo management will hold a conference call today, May 7, 2024, at 4:30 PM Eastern time to discuss these results. Company CEO Jeff Korn, CFO Ron Vincent, and President and COO Doug Gaylor will host the call, followed by a question-and-answer period.

FTK...Flotek Announces First Quarter 2024 Results Reflecting Improved Profitability

HOUSTON, May 7, 2024 /PRNewswire/ -- Flotek Industries, Inc. ("Flotek" or the "Company") (NYSE: FTK) today announced operational and financial results for the quarter ended March 31, 2024, highlighted by significant improvement in profitability metrics as compared to the first quarter of 2023.

Financial Summary (in thousands, except per share amounts)

Three months ended March 31,

2024

2023

% Change

Total Revenues

$ 40,374

$ 48,007

(16) %

Gross Profit

$ 8,821

$ 1,880

369 %

Adjusted Gross Profit (1)

$ 10,075

$ 2,647

281 %

Net Income

$ 1,562

$ 21,343

(93) %

Diluted Income (Loss) Per Share

$ 0.05

$ (0.12)

n/a

Adjusted EBITDA (1)

$ 4,026

$ (3,851)

n/a

First Quarter 2024 Highlights

Reported net income of $1.6 million compared to net income of $21.3 million for the first quarter of 2023. Net income for the first quarter of 2023 benefited from $30.6 million in non-cash gains. Excluding these non-cash gains, first quarter 2024 net income improved by $10.8 million.

Delivered significant year-over-year improvements in gross profit, adjusted gross profit(1) and adjusted EBITDA(1) of $6.9 million, $7.4 million and $7.9 million, respectively.

Realized gross profit margin and adjusted gross profit margin(1) of 22% and 25%, respectively.

Achieved the 3rd consecutive quarter of net income and 11th consecutive quarter of improvement in adjusted EBITDA(1) as a percentage of revenue.

Reduced borrowings outstanding under the Asset Based Loan by 58% (or $4.4 million) compared to year-end 2023.

Full Year 2024 Profitability Outlook

As a result of the numerous cost reductions and efficiency gains implemented throughout 2023, the Company expects a substantial increase in margins compared to 2023. In 2023, our gross margin was 13% and our net income was $24.7 million. Flotek expects 2024 adjusted gross profit margin(2) to range between 18% and 22%, as compared to 2023 adjusted gross profit margin(1) of 15%. The Company expects 2024 adjusted EBITDA(2) to range between $10 million and $16 million as compared to $1.5 million in 2023(1).

Management Commentary

Chief Executive Officer Dr. Ryan Ezell commented, "Our first quarter results continue the positive financial and operational trends that began during 2022. We achieved our third consecutive quarter of net income. Adjusted EBITDA(1) during the quarter exceeded the entire year of 2023. Using the mid-point of our guidance, we expect a nearly 800% increase in annual adjusted EBITDA(2) versus 2023(1).

During the quarter we realized 19% sequential growth in our ProFrac related revenue while our data analytics segment revenues increased 18% from the fourth quarter of 2023. While our first quarter external chemistry customer sales realized 27% year over year growth, they declined sequentially, which is consistent with the first quarter in each of the last three years. We expect these revenues will show a substantial increase during the second quarter and we anticipate annual growth in external chemistry customer sales for 2024.

Our numerous financial improvements continue to validate the initiatives executed over the past 18 months aimed at building a resilient business that can sustain profitability through the volatility inherent in our industry."

First Quarter 2024 Financial Results

Revenue: Flotek reported total revenues of $40.4 million for the first quarter 2024, which was a decrease of $7.6 million, or 16%, compared to total revenues of $48.0 million for the first quarter 2023. The decline in revenue compared to the first quarter 2023 was the result of lower related party activity that was partially offset by a 13% increase in revenue from external customers.

Revenue from external chemistry customers during the first quarter 2024 declined by approximately $6.0 million as compared to the fourth quarter 2023 due primarily to normal seasonal declines. The Company anticipates external chemistry customer revenues to increase significantly in the second quarter 2024.

Revenue associated with the Company's data analytics segment increased to $1.7 million, an 18% improvement as compared to the fourth quarter 2023. Revenues from data analytics totaled $2.5 million during the first quarter 2023.

Gross Profit: The Company generated gross profit of $8.8 million during the first quarter 2024 as compared to gross profit of $1.9 million for the first quarter 2023. The improvement in first quarter 2024 gross profit was the result of successful initiatives to drive cost improvements with respect to freight, logistics and materials, and revenue attributable to the estimated annual minimum chemistry purchase requirements contained in the ProFrac supply agreement. The measurement period during 2023 for annual minimum chemistry purchase requirements was June 1, 2023 through December 31, 2023.

Adjusted Gross Profit (Non-GAAP)(1): Flotek generated adjusted gross profit of $10.1 million during the first quarter 2024 compared to adjusted gross profit of $2.6 million for the first quarter 2023. Adjusted gross profit excludes non-cash items, primarily amortization of contract assets.

Selling, General and Administrative ("SG&A") Expense: SG&A expense totaled $6.1 million for the first quarter 2024 compared to $6.5 million for the first quarter 2023. The improvement was the result of lower personnel costs and professional fees during the 2024 period.

Net Income and EPS: Flotek reported net income of $1.6 million, or $0.05 per diluted share, for the first quarter 2024. This compares to net income of $21.3 million, or $(0.12) per diluted share, for the first quarter 2023. Net income for the first quarter 2023 benefited from a $26.1 million non-cash gain related to the fair value adjustment of the Company's convertible notes, as well as a $4.5 million gain from the partial forgiveness of the Company's PPP loan.

Adjusted EBITDA (Non-GAAP)(1): Adjusted EBITDA was $4.0 million in the first quarter 2024 as compared to negative $3.9 million in the first quarter 2023.

(1) A non-GAAP financial measure. See the "Unaudited Reconciliation of Non-GAAP Items and Non-Cash Items Impacting Earnings" section in this release for more information, including reconciliations to the most comparable GAAP measures.

(2) A non-GAAP financial measure. See the "Unaudited Reconciliation of Non-GAAP Items and Non-Cash Items Impacting Earnings" section in this release for more information, including reconciliations to the most comparable GAAP measures. We are unable to reconcile this forward-looking non-GAAP financial measure to the most directly comparable GAAP financial measure without unreasonable efforts, as we are unable to predict with a reasonable degree of certainty the impact of certain items that would be expected to impact the GAAP financial measure, including, among other items, the future amortization of our contract assets, certain stock-based compensation costs and the impact of the revaluation of certain liabilities, which is based upon our future stock price. These items do not impact the non-GAAP financial measure.

Conference Call Details

Flotek will host a conference call on May 8, 2024, at 9:00 a.m. CT (10:00 a.m. ET) to discuss its first quarter 2024 results. Participants may access the call through Flotek's website at www.flotekind.com under "News" within the Investor Relations section or by telephone toll free at 1-800-836-8184 (international toll: 1-646-357-8785) approximately five minutes prior to the start of the call. Following the conclusion of the conference call, a recording of the call will be available on the Company's website.

An updated corporate presentation that will be referenced on the call will be posted to the Investor Relations section of Flotek's website at www.flotekind.com prior to the start of the earnings conference call.

About Flotek Industries, Inc.

Flotek Industries, Inc. is an advanced technology-driven, green chemical and data analytics company providing unique and innovative completion solutions that have a proven, positive impact on sustainability and reducing the overall environmental impact of energy on air, land, water and people. Flotek has an intellectual property portfolio of over 170 patents and a global presence in more than 59 countries throughout North America, Latin America, the Middle East and North Africa. Flotek has established collaborative partnerships focused on sustainable and optimized chemistry and data solutions which improve well performance and allow its customers to generate higher returns on invested capital.

Flotek is based in Houston, Texas and its common shares are traded on the New York Stock Exchange under the ticker symbol "FTK". For additional information, please visit www.flotekind.com.

CXDO...Crexendo Selects Oracle Cloud Infrastructure to Support Unprecedented Company Growth

PHOENIX, AZ / ACCESSWIRE / May 7, 2024 / Crexendo®, Inc. (NASDAQ:CXDO), an award-winning premier provider of cloud communication platforms and services, video collaboration, and managed IT services designed to provide enterprise-class cloud solutions to any size business, today announced availability of its hosted services globally on Oracle Cloud Infrastructure (OCI), marking a pivotal moment in Crexendo's rapid growth and geographic expansion.

Working with OCI will help simplify Crexendo partners' business of operating a unified communications platform, and the security-first approach of OCI allows customers to not have to compromise between reliability, security, and cost. With more than 4.5 million users on Crexendo's NetSapiens platform, this move offers unparalleled flexibility, enabling partners to use the software platform according to their preferences, whether in their own cloud environment or within Oracle's secure cloud.

"Our customers celebrate having the industry's leading platform, and we sought to match this level of performance with the industry's leading hosting partner in OCI," said Jeff Korn, CEO and chairman, Crexendo. "We rigorously assessed where our customers would receive the highest performance and the decision to partner with Oracle was unequivocal."

Korn continued, "OCI's distributed cloud architecture enables us to think globally with location independence, expanding our market reach and enhancing the customer experience. The superior price-performance of OCI enables us to deliver incredible value to our customers, solidifying our position as a trusted partner in their journey. With more than 430,000 customers trusting Oracle, Crexendo joins a prestigious community of innovators and industry leaders. Together, we're redefining the future of cloud communication solutions and revolutionizing the way businesses communicate and connect in today's digital age."

"We're excited that Crexendo has selected Oracle Cloud Infrastructure as their cloud platform of choice for their unified communications as a service offering," said David Hicks, group vice president, ISV Business and Marketing Development, Oracle. "OCI will help support Crexendo's current and future business plans. Specifically, OCI's superior price-performance and data egress advantages, its global datacenter footprint, and its price consistency give Crexendo a predictable platform for international expansion of their business."

https://finance.yahoo.com/news/crexendo-selects-oracle-cloud-infrastructure-130000700.html

CXDO...Crexendo is a well oiled growth machine with a strong track record. This will remain my top long term hold until something changes. (Was waaaaay overweight the stock heading into this year, and took advantage of the pop to higher prices to sell over 1/2. But since I've accummulated some back in the low/mid $'4's and currently CXDO is @ approx 30% my portfolio).

Here's a morsal from their last cc's Q&A ...

Mike Latimore

One more quick one here. I guess can you provide any color on just how January and February have played out from a bookings perspective? Kind of is it normal seasonality, better or worse? Just how are you -- how did you see January and February relative to kind of those normal months at the start of the year?

Jeffrey Korn

Mike, as you know, we don't give guidance, but we don't give guidance, Mike. But as I said in my comments, I'm very pleased with the results we're seeing for Q1.

So I don't want to say much more than that. But I wouldn't have indicated that we expect double-digit growth if we didn't see Q1 going well.

Doug Gaylor

Yes. And I would tell you, Mike, that sales momentum is very strong right now.

We continue to add new reseller partners out there, and our funnel for sales opportunities is as strong as it's ever been.

So we're not seeing any slowdown in opportunities out there and bookings continue to have great momentum.

Earnings after the close.

We'll see what happens.

CSPI...Wednesday will be interesting. I'll be holding...(CSPI is currenty my #4 position).

CXDO is by far my #1 position, FTK @ #2, and SBOW @ #3.

CSPI..."We are honored that our AZT PROTECT solution has been selected as one of the world's best cybersecurity products by the InfoSec® judging committee."

ARIA Cybersecurity Wins Global Infosec Cybersecurity Product Award for AZT PROTECT

https://finance.yahoo.com/news/aria-cybersecurity-wins-global-infosec-120000464.html

AESI...Trimmed another 1/3 this morning...Atlas Energy Solutions Announces First Quarter 2024 Results; Increases Quarterly Dividend

AUSTIN, Texas, May 06, 2024--(BUSINESS WIRE)--Atlas Energy Solutions Inc. (NYSE: AESI) ("Atlas" or the "Company") today reported financial and operating results for the quarter ended March 31, 2024.

First Quarter 2024 Highlights

Total sales of $192.7 million

Net income of $26.8 million (14% Net Income Margin)

Adjusted EBITDA of $75.5 million (39% Adjusted EBITDA Margin) (1)

Net cash provided by operating activities of $39.6 million

Adjusted Free Cash Flow of $71.1 million (37% Adjusted Free Cash Flow Margin) (1)

Dune Express construction remains on-time and on-budget

Declares increased quarterly dividend of $0.22 per share ($0.16 per share fixed, $0.06 per share variable), payable May 23, 2024

John Turner, President, CEO & CFO, commented, "The first quarter was a monumental one for our company with the closing of the Hi-Crush acquisition. We are already realizing benefits from the transaction through increased scale and are excited with the way the transaction positions us for long-term success. We’re looking forward to the remainder of the year, as we recently floated our two new dredges at our Kermit facility and began producing sand from the eighth OnCore mine, which is located in the Midland Basin. Our response to the recent mechanical fire at our Kermit facility was swift and decisive, and I’m proud of the team’s efforts to insulate our customers from any disruption in service. We expect to continue servicing our customers while we finish up the repairs to the facility."

First Quarter 2024 Financial Results

First quarter 2024 total sales increased $51.6 million, or 37% when compared to the fourth quarter of 2023, to $192.7 million. Product sales increased $13.4 million, or 13% when compared to the fourth quarter of 2023, to $113.4 million. First quarter 2024 sales volumes increased to 3.9 million tons, or 54% when compared to the fourth quarter of 2023, which was offset by lower average pricing experienced during the period. Service sales increased by $38.1 million, or 93% when compared to the fourth quarter of 2023, to $79.2 million. The increase in service sales was due to an increased number of active jobs during the period coupled with the service sales contribution, which only includes 27 days for the month of March, associated with the previously announced acquisition of Hi-Crush Inc. ("Hi-Crush").

First quarter 2024 cost of sales (excluding depreciation, depletion and accretion expense) ("cost of sales") increased by $40.1 million, or 60% when compared to the fourth quarter of 2023, to $106.7 million. The increase in our cost of sales was primarily driven by cost of sales contribution associated with the Hi-Crush operations, which only includes 27 days for the month of March.

Selling, general and administrative expenses ("SG&A") for the first quarter of 2024 increased $15.5 million, or 114% when compared to the fourth quarter of 2023, to $29.1 million, driven primarily by $10.6 million in non-recurring transaction costs related to the acquisition of Hi-Crush, along with $4.2 million in stock-based compensation.

Net income for the first quarter of 2024 was $26.8 million, and Adjusted EBITDA for the first quarter of 2024 was $75.5 million.

Liquidity, Capital Expenditures and Other

As of March 31, 2024, the Company’s total liquidity was $360.9 million, which was comprised of $187.1 million in cash and cash equivalents (held in cash, CDs, and two- and three-month Treasury bills), $73.8 million of availability under the Company’s ABL Facility, and $100 million of availability under the Company's Delayed Draw Term Loan Facility; the Company had $50.0 million of borrowings outstanding under the ABL Facility and $1.2 million of outstanding undrawn letters of credit.

Net cash used in investing activities was $235.1 million during the first quarter of 2024, driven largely by the cash consideration component related to the Hi-Crush acquisition, along with costs associated with the construction of the Dune Express. We continue to expect the Dune Express to come online in the fourth quarter of 2024.

Quarterly Cash Dividend

On May 6, 2024, the Board of Directors (the "Board) of Atlas declared an increased dividend to common stockholders of $0.22 per share, or approximately $24.1 million in aggregate to shareholders. The dividend includes a $0.16 per share base dividend and a $0.06 per share variable dividend. The dividend will be payable on May 23, 2024 to shareholders of record at the close of business on May 16, 2024.

Subsequent Events

Kermit Facility Operational Update

As previously reported, on Sunday, April 14th, a mechanical fire occurred at the Atlas mine in Kermit, Texas. The team began to move temporary loadout equipment to the Kermit facility within 48 hours of the incident. On Thursday, April 25, Atlas reopened the Kermit facility and began to fulfill a portion of Kermit facility customer commitments with sand produced and loaded from that facility. We continue to review the financial impact of the incident and believe we will have the Kermit facility fully operational by the end of 2Q 2024.

Conference Call Information

The Company will host a conference call to discuss financial and operational results on Monday, May 6, 2024 at 9:00am Central Time (10:00am Eastern Time). Individuals wishing to participate in the conference call should dial (877) 407-4133. A live webcast will be available at https://ir.atlas.energy/. Please access the webcast or dial in for the call at least 10 minutes ahead of the start time to ensure a proper connection. An archived version of the conference call will be available on the Company’s website shortly after the conclusion of the call.

The Company will also post an updated investor presentation titled "Investor Presentation May 2024", in addition to a "May 2024 Growth Projects Update" video, at https://ir.atlas.energy/ in the "Presentations" section under "News & Events" tab on the Company’s Investor Relations webpage prior to the conference call.

About Atlas Energy Solutions

Atlas Energy Solutions Inc. is a leading proppant producer and proppant logistics provider, serving primarily the Permian Basin of West Texas and New Mexico. We operate 12 proppant production facilities across the Permian Basin with a combined annual production capacity of 28 million tons, including both large-scale in-basin facilities and smaller distributed mining units. We manage a portfolio of leading-edge logistics assets, which includes our 42-mile Dune Express conveyor system, which is currently under construction and is scheduled to come online in the fourth quarter of 2024. In addition to our conveyor infrastructure, we manage a fleet of 120 trucks, which are capable of delivering expanded payloads due to our custom-manufactured trailers and patented drop-depot process. Our approach to managing both our proppant production and proppant logistics operations is intently focused on leveraging technology, automation and remote operations to drive efficiencies.

We are a low-cost producer of various high-quality, locally sourced proppants used during the well completion process. We offer both dry and damp sand, and carry various mesh sizes including 100 mesh and 40/70 mesh. Proppant is a key component necessary to facilitate the recovery of hydrocarbons from oil and natural gas wells.

Our logistics platform is designed to increase the efficiency, safety and sustainability of the oil and natural gas industry within the Permian Basin. Proppant logistics is increasingly a differentiating factor affecting customer choice among proppant producers. The cost of delivering sand, even short distances, can be a significant component of customer spending on their well completions given the substantial volumes that are utilized in modern well designs.

We continue to invest in and pursue leading-edge technologies, including autonomous trucking, digital infrastructure, and artificial intelligence, to support opportunities to gain efficiencies in our operations. To this end, we have recently taken delivery of next-generation dredge mining assets to drive efficiencies in our proppant production operations. These technology-focused investments aim to improve our cost structure and also combine to produce beneficial environmental and community impacts.

While our core business is fundamentally aligned with a lower emissions economy, our core obligation has been, and will always be, to our stockholders. We recognize that maximizing value for our stockholders requires that we optimize the outcomes for our broader stakeholders, including our employees and the communities in which we operate. We are proud of the fact that our approach to innovation in the hydrocarbon industry while operating in an environmentally responsible manner creates immense value. Since our founding in 2017, our core mission has been to improve human beings’ access to the hydrocarbons that power our lives while also delivering differentiated social and environmental progress. Our Atlas team has driven innovation and has produced industry-leading environmental benefits by reducing energy consumption, emissions, and our aerial footprint. We call this Sustainable Environmental and Social Progress.

We were founded in 2017 by Ben M. "Bud" Brigham, our Executive Chairman, and are led by an entrepreneurial team with a history of constructive disruption bringing significant and complementary experience to this enterprise, including the perspective of longtime E&P operators, which provides for an elevated understanding of the end users of our products and services. Our executive management team has a proven track record with a history of generating positive returns and value creation. Our experience as E&P operators was instrumental to our understanding of the opportunity created by in-basin sand production and supply in the Permian Basin, which we view as North America’s premier shale resource and which we believe will remain its most active through economic cycles.

https://finance.yahoo.com/news/atlas-energy-solutions-announces-first-120000722.html

AESI...researcher, Got to thinking about o&g prices and decided to sell 1/3 of my AESI holdings today (@$22+) before the report next week. I have good profits in the stock and thought it would be a good idea to take some off the table. Still hold a decent position though and thanks again for the heads-up last December.

Also...

Going to ride my entire FTK position into earnings.

Sold some SBOW today and will hold the rest for now.

STCN...$12.50. Inched up to a 52wk High.⬆️...Very illiquid though.

CSPI...Now @ $12...Stay tuned for next week's webinar...

(I added back a bit today going into the webinar & earnings)

ARIA and Rockwell Automation Discuss the Unique Requirements to Protect Industrial Applications in Their Latest Webinar

Webinar: CybeRx - How to Automatically Protect Rockwell OT Customers from Today's Cyber-attacks

LOWELL, MA / ACCESSWIRE / April 25, 2024 / ARIA Cybersecurity Solutions, a CSPi business (NASDAQ:CSPI), has warned of the rapidly escalating cybersecurity risks facing companies with operational technology (OT) in the manufacturing sector. In a new webinar, "CybeRx - How to Automatically Protect Rockwell OT Customers from Today's Cyber-Attacks" we will discuss why the Perdue model, passive defenses and AV/NGAV are not stopping the most dangerous attacks.

In this webinar you will hear from Rockwell about the unique set of requirements that are needed to protect your production application's attack surface and how Aria's AZT Protect has helped meet this need. We will delve into the composition of supply chain attacks and finally hear about a case study in how one of the world's largest pharma manufactures used ARIA AZT PROTECT in combination with Rockwell's industrial automation suite to protect their environment and meet their challenging OT requirements.

Gary Southwell, General Manager of ARIA Cybersecurity, is joined by Thomas House, Life Sciences Cyber and Digital Consultant, Rockwell Automation.

Webinar scheduled for Thursday, May 9, 2024

11:00 AM EDT

To access the full webinar, please visit: https://hubs.ly/Q02t-sv20

https://finance.yahoo.com/news/aria-rockwell-automation-discuss-unique-120000711.html

CLMB...Earnings report came in a bit soft (although not terrible). Taken from the management commentary..."During the quarter we experienced softer volumes across select key vendors, primarily related to the timing of their respective sales cycles. This includes a key vendor from our acquisition of DataSolutions in October 2023. Although this adversely affected our bottom line in Q1, we expect to return to growth with these vendors in the back half of the year."

The cc is early tomorrow. Should be interesting.

Climb Global Solutions Reports First Quarter 2024 Results

Q1 2024 Net Sales Up 9% YoY to $92.4 Million, with Adjusted Gross Billings Up 16% to $355.3 Million

EATONTOWN, N.J., May 01, 2024 (GLOBE NEWSWIRE) -- Climb Global Solutions, Inc. (NASDAQ:CLMB) (“Climb”, the “Company”, “we”, or “our”), a value-added global IT channel company providing unique sales and distribution solutions for innovative technology vendors, is reporting results for the first quarter ended March 31, 2024.

First Quarter 2024 Summary vs. Same Year-Ago Quarter

Net sales increased 9% to $92.4 million.

Adjusted gross billings (a non-GAAP financial measure defined below) increased 16% to $355.3 million.

Net income was $2.7 million or $0.60 per diluted share compared to $3.3 million or $0.74 per diluted share.

Adjusted EBITDA (a non-GAAP financial measure defined below) was $5.5 million compared to $5.7 million.

https://finance.yahoo.com/news/climb-global-solutions-reports-first-200500876.html

SBOW...Should be up tomorrow. FTK & AESI are two big o&g holdings for me and they both report next week. Think I'll be OK holding those 2 into earnings also. We'll see what happens.

SBOW...Earnings are out. I'm not an o&g expert, but at first glance, the report looks good...

(adj EPS $2.09)

SilverBow Resources Announces First Quarter 2024 Financial and Operating Results

Results top consensus expectations driven by higher production and lower capital expenditures generating record quarterly EBITDA and strong quarterly free cash flow

Total debt reduced by $178 million since closing its South Texas acquisition in late 20231; First quarter 2024 leverage ratio of 1.35x2 lower than pre-acquisition announcement

Year-to-date outperformance leads to increase in full-year production expectations and free cash flow outlook

https://ih.advfn.com/stock-market/NYSE/silverbow-resources-SBOW/stock-news/93762382/silverbow-resources-announces-first-quarter-2024-f

SBOW...Nice comparison.

SBOW...O&G prices were lower when SBOW gave guidance in Feburary, so hopefully guidance doesn't drop.

Looks like SBOW just hit what might be a bit of support so I added more in the $29.70's. Makes me heavier in the stock than I want to be, so hopefully I get a chance to sell some off after earnings for higher prices. We'll see what happens,

2024 Outlook:

In response to commodity prices, the Company lowered its previously planned capital investments in dry gas-focused areas by approximately $75 million, resulting in a revised 2024 capital program budget of $470 - $510 million

At current commodity prices, the Company expects to generate $125 - $150 million of estimated FCF, which is currently earmarked for significant debt reduction

The Company is maintaining planned investment in oil and liquids projects while keeping oil and liquids production guidance at previously announced levels. Revised capital investments reduce expected natural gas volumes by 13%

Production is expected to increase approximately 50% year-over-year to 85.2 - 93.5 MBoe/d, post-recent acquisition, oil production is expected to increase 70% year-over-year and comprise 25% - 30% of 2024 production mix

SBOW...Stock price has hit the sh!tter past couple days, but it hasn't been on overly high volume. So I thought WTH, and added a little more this morning @ avg $30.12. Earnings tomorrow.

SMCI...Hope you do well valuemind. I had a couple good trading days and am out now.

Still have the urge to trade it though because of the wild swings, so I removed it from my watchlist.

Good luck.👍

SMCI...hweb, I know, right? Just played the early morning dips averaging down on some rather large trades (knowing earnings were coming), and ended up making good profit when the stock bounced. I guess it could have went the other way though.

SMCI...Nice action continues on SMCI...I have been very successful at using it as a trading vehicle over the past couple days. Haven't decided yet if I'm going to hold into earnings, (thinking about holding onto a small position).

Hope you're making a mint on this one valuemind.👍

CLMB..."As we look ahead to the remainder of 2024, I'm incredibly encouraged by the opportunities that lie ahead, confident in our team's ability to innovate, adapt, and continue delivering exceptional value," said Dale Foster, CEO of Climb Channel Solutions."

Climb Channel Solutions' Commitment to Excellence Recognized with Multiple Prestigious Awards in Q1 2024

https://finance.yahoo.com/news/climb-channel-solutions-commitment-excellence-110000184.html

SBOW...Thanks. My position is small compared to some of my other holdings, so I'll ride it into earnings w/ you and go from there.

SBOW...Today's news...SilverBow Resources Successfully Executing Strategic Priorities to Drive Shareholder Value

Business Wire

Files Investor Presentation and Sends Letter to Shareholders Highlighting Track Record of Profitable Growth

Board Urges Shareholders to Vote "FOR" ALL of SilverBow’s Highly Qualified Directors on the WHITE Proxy Card

HOUSTON, April 29, 2024--(BUSINESS WIRE)--SilverBow Resources, Inc. (NYSE: SBOW) ("SilverBow" or the "Company") today released an investor presentation and mailed a letter to shareholders in connection with the Company’s 2024 Annual Meeting of Shareholders (the "2024 Annual Meeting"). Both will be filed with the U.S. Securities and Exchange Commission. Additional company resources for the 2024 Annual Meeting can be found at www.futureofsilverbow.com.

Highlights include:

SilverBow Has a Strong Track Record of Outperformance: Since 2021, our total shareholder return is 503%, compared to 193% for the XOP E&P Index.1

Management Is Successfully Executing its Proven Strategy: We are generating strong operating results and recently set quarterly records for free cash flow and adjusted EBITDA.2 We expect this momentum to continue; and

The Board Is Acting in Shareholders’ Best Interests: Our Board is composed of independent directors that bring direct industry expertise and public company board and executive leadership experience.

The full text of the letter follows:

Dear Fellow Shareholders,

SilverBow Resources’ Board and management team remain laser-focused on positioning the business to continue driving value for ALL shareholders. Our stock has significantly outperformed the XOP Index over the last several years.

On the other hand, Kimmeridge Energy Management Company, LLC, is running a costly proxy fight to gain control of your Company without paying you a premium for your investment. Kimmeridge has one goal: to force a dilutive, value-destructive combination with Kimmeridge Texas Gas (KTG).

Shareholders should note:

SilverBow Has a Strong Track Record of Outperformance: Since 2021, our total shareholder return is 503%, compared to 193% for the XOP E&P Index. 1

Management Is Successfully Executing its Proven Strategy: We are generating strong operating results and recently set quarterly records for free cash flow and adjusted EBITDA.2 We expect this momentum to continue.

The Board Is Acting in Shareholders’ Best Interests: Our Board is composed of independent directors that bring direct industry expertise and public company board and executive leadership experience.

To protect the value of your investment, using the WHITE proxy card, please vote "FOR" all SilverBow director nominees: Gabriel L. Ellisor, Kathleen McAllister and Charles W. Wampler.

You can learn more about the quality of our Board, positive governance changes and SilverBow’s value creation opportunity at www.futureofsilverbow.com.

Additional information that outlines our strategy can be found in the investor presentation SilverBow recently published at www.futureofsilverbow.com/investor-presentation.

SilverBow’s Proven Strategy Is Delivering Results

Our Board has been overseeing a clear and proven strategy to drive shareholder value by:

Building a scaled and durable portfolio characterized by a deep inventory of drilling opportunities and commodity diversity;

Driving efficiencies and enhancing margins to capture sustainable capital efficiencies and greater margins;

Delivering profitable growth through continued execution of our returns-focused strategy; and

Strengthening the balance sheet and deepening liquidity, with strong free cash flow generation.

The results of this strategy:

Secured decade+ of high-quality drilling inventory with about 1,000 locations across our 220,000 net acres;

Executed a transformative South Texas acquisition in late 2023 that enhanced scale and added important capital allocation flexibility;

Achieved peer-leading cost structure (opex 40%+ lower than peer average and cash G&A 65%+ lower than peer average) and best-in-class margin profile (EBITDA margin 20%+ higher than peer average);

Posted 21% average ROCE (2021-23);

Generated four consecutive years of free cash flow through ongoing capital discipline;

Improved our capital structure through a lower debt, higher liquidity focus; and

Optimized 2024 plan to maximize free cash flow and fund high-return oil and liquids developments.

Our success is being recognized by the market. The Company has outpaced the XOP E&P index since 2021, delivering total shareholder returns of 503% compared to 193% for the XOP E&P Index, as well as outsized returns over one-, three- and five-year periods.1,3

SilverBow’s Highly Qualified Directors Are Also Further Enhancing Our Governance

A strong Board and robust governance practices are critical to sustained value creation. Our legacy existing governance structure was adopted in the aftermath of our 2016 financial restructuring. As our original ownership has changed, our Board is evolving SilverBow’s governance to better align with best practices.

After discussions with our current shareholders, we are proposing significant governance changes at the upcoming 2024 Annual Meeting:

Declassifying the Board and providing for the annual election of all directors;

Adopting a majority voting standard in uncontested elections of directors; and

Eliminating the supermajority vote requirements for shareholders to amend certain provisions of our certificate of incorporation.

We have also continued to strengthen our Board with new skill sets, collective experiences and enhanced diversity.

We have a highly engaged, experienced Board that is working to maximize value. Since 2023, SilverBow has added four highly qualified new independent directors, which we believe gives us the right balance of valuable company knowledge and fresh perspectives in the boardroom. Each director has extensive experience in the energy sector, including Leland T. "Lee" Jourdan, the Board’s most recent addition.

Our three independent directors who are up for election at this year’s Annual Meeting – Gabriel L. Ellisor, Kathleen McAllister and Charles W. Wampler – bring extensive public company board and executive leadership experience. Of note, Kathleen McAllister is a recent addition to the Board, joining in January 2023.

Our Directors Are Independent, Highly Qualified and Not Conflicted

Gabriel L. Ellisor

Significant financial experience developed through 25 years in the finance sector of the oil and gas industry

Extensive M&A experience at Rivington Capital and serving as CFO of two oil and gas acquisition vehicles exited within five years for proceeds of $2.5 billion

Expertise in successfully raising capital at energy companies

Kathleen McAllister

Significant experience overseeing financial and operational functions at large multinational companies

Public company CEO and CFO experience at capital-intensive global companies in the energy value chain

Expertise executing strategic transactions, including leading Transocean Partners’ IPO in 2014

Charles W. Wampler

Significant understanding of E&P company challenges leveraging 40+ years of industry experience

Decades of operational expertise, including working as COO of large multinational energy companies

Track record of overseeing employee safety and minimizing environmental impacts of E&P operations

In contrast to Kimmeridge’s highly conflicted nominees who have a personal interest in supporting Kimmeridge’s dilutive proposal, our directors are focused on delivering value for SilverBow shareholders.

Kimmeridge’s Proxy Fight Is About Forcing a Value-Destructive Combination With Kimmeridge Texas Gas (KTG); Its Highly Conflicted Nominees Are Incentivized to Carry Out Kimmeridge’s Self-Serving Agenda

We have put out extensive information about our two-year engagement with Kimmeridge. This includes reaching a deal on agreed terms, which Kimmeridge ultimately reneged on because they were unable to secure financing. Most recently, Kimmeridge presented a value-destructive proposal to merge KTG with SilverBow which undervalued SilverBow while substantially overvaluing its own KTG assets. The SilverBow Board previously rejected the proposal, determining that it was NOT in the best interests of SilverBow shareholders. SilverBow published our analysis of the proposal in our April 22, 2024 shareholder letter, also available here.

Although Kimmeridge withdrew its proposal, we believe they are pursuing a proxy contest in an attempt to gain control of SilverBow and ultimately force this value-destructive transaction upon our shareholders.

We strongly believe appointing Kimmeridge’s nominees to the Board would jeopardize SilverBow’s proven strategy and business plan and ultimately diminish shareholder value. Kimmeridge’s three nominees – Carrie Fox, Douglas Brooks and Katherine Minyard – are not aligned with all SilverBow shareholders, and we believe the self-interested agenda of Kimmeridge and their nominees risks impeding our progress, ability to pursue non-Kimmeridge related business opportunities and the value we are poised to create for our shareholders.

https://finance.yahoo.com/news/silverbow-resources-successfully-executing-strategic-120000102.html

SBOW...What do you think researcher? Earnings are Thursday...SBOW looks to be pretty unuervalued base on estimates. so I'm thinking on holding my current position into the report and possibly adding. Would like to get your opinion. (It's inching up a notch as I type).

FTK...Alliance Global Partners initiates coverage on Flotek Industries (NYSE:FTK) with a Buy rating and announces Price Target of $7.

Current price $3.47.

👍resercher59 ‼️🍻

CLMB...Climb Channel Solutions Launches Partnership with Automox, Providing Leading Endpoint Management Solution to North American Partners

EATONTOWN, N.J., April 25, 2024 (GLOBE NEWSWIRE) -- Climb Channel Solutions, an international specialty technology distributor and wholly owned subsidiary of Climb Global Solutions, Inc. (NASDAQ: CLMB), announced the launch of a new partnership with Automox, a leading cloud-native IT automation endpoint management solution, now available to their North American partners.

With the addition of Automox, Climb partners can provide customers the capabilities to save time, eliminate risk, and automate the patching, configuration, and control of all Windows, macOS, and Linux endpoints with one modern IT operations platform. Adding Climb as a distributor is a strategic move for Automox as they expand their channel efforts with the goal of switching to over 50% of business via the channel.

Cooper Herrera, Manager of Channel Sales at Automox, said, “We're proud and excited to partner with Climb Channel Solutions. As the leading cloud-native IT automation endpoint management solution, Automox fits perfectly in Climb's stack of business-critical technologies. Thousands of solution providers, VARs, systems integrators, corporate resellers, and consultants now have access to cloud-native IT automation at scale.”

Automox partners with industry-leading companies to extend the sales reach for Automox's cloud-native IT operations platform. Their dedicated channel team is focused on helping resellers sell across a wide range of market segments, from small-to-medium sized businesses (SMBs) to large, multi-location corporate enterprises - and across all vertical markets.

“We are excited about the addition of Automox to our North American line cards,” says Dale Foster, CEO of Climb Channel Solutions. “It is important to us to continue to bring on leading emerging technology for our partners to satisfy the need of their customers. As automation becomes a focus for tech industry, signing vendors, such as Automox, helps us ensure our partner ecosystem is enabled with the best of the best.”

https://www.globenewswire.com/news-release/2024/04/25/2869486/0/en/Climb-Channel-Solutions-Launches-Partnership-with-Automox-Providing-Leading-Endpoint-Management-Solution-to-North-American-Partners.html